South Korea Integrated Facility Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

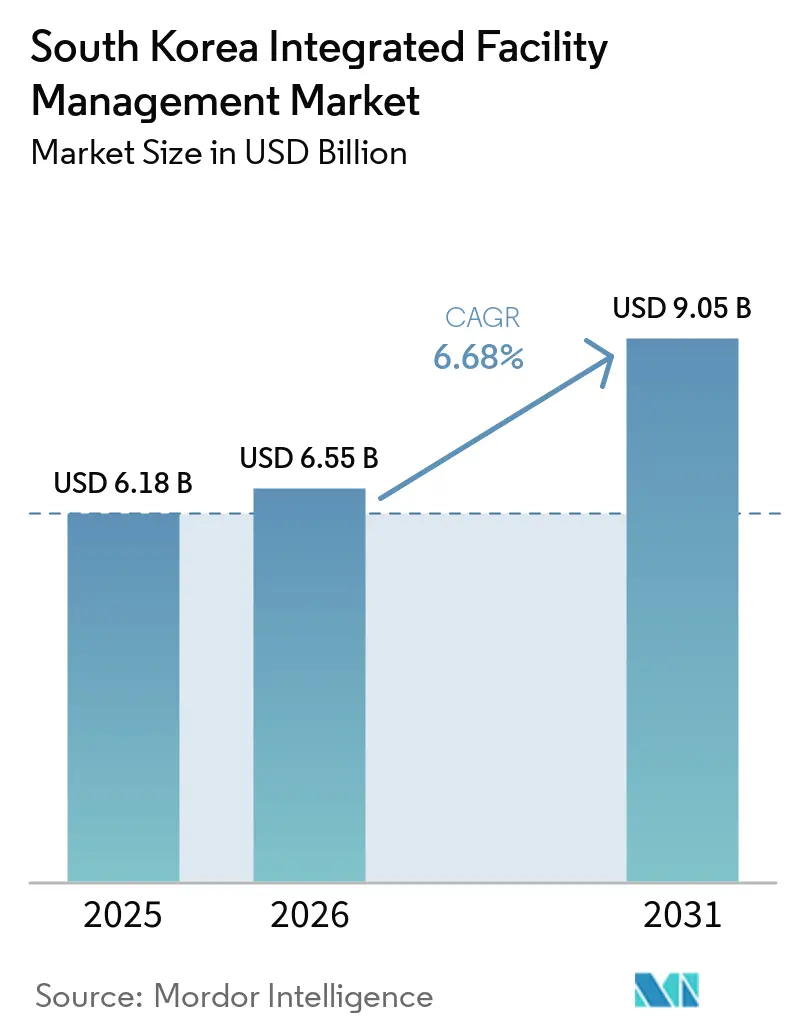

| Base Year Market Size (2025) | USD 6.18 Billion |

| Market Size (2026) | USD 6.55 Billion |

| Market Size (2031) | USD 9.05 Billion |

| Growth Rate (2026 - 2031) | 6.68% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Integrated Facility Management Market Analysis by Mordor Intelligence

The South Korea Integrated Facility Management Market size is expected to grow from USD 6.18 billion in 2025 to USD 6.55 billion in 2026 and is forecast to reach USD 9.05 billion by 2031 at 6.68% CAGR over 2026-2031.

In 2026, the South Korea integrated facility management market is built on a broader base of outsourced real estate operations, smart infrastructure upgrades, and new technical facilities that require a single operator to coordinate multiple service lines. The shift from separate service contracts to integrated delivery is changing how buyers compare vendors, because pricing, accountability, reporting quality, and measurable savings now sit within one operating framework instead of several disconnected scopes. Public-sector green remodeling requirements under the 3rd Basic Green Building Plan and tighter Zero-Energy Building standards are also widening the pipeline for retrofit-heavy contracts that demand technical depth and longer execution cycles. Large-scale data center investment is adding another layer of demand for continuous power, cooling, fire safety, and security management, which raises the value of Hard FM capability within the South Korea integrated facility management (IFM) market. Labor shortages outside major cities and new bargaining pressures in outsourced workforces will keep cost control difficult for some operators, but the South Korea IFM market will continue to benefit from multi-year outsourcing, compliance, and infrastructure investment cycles.

Key Report Takeaways

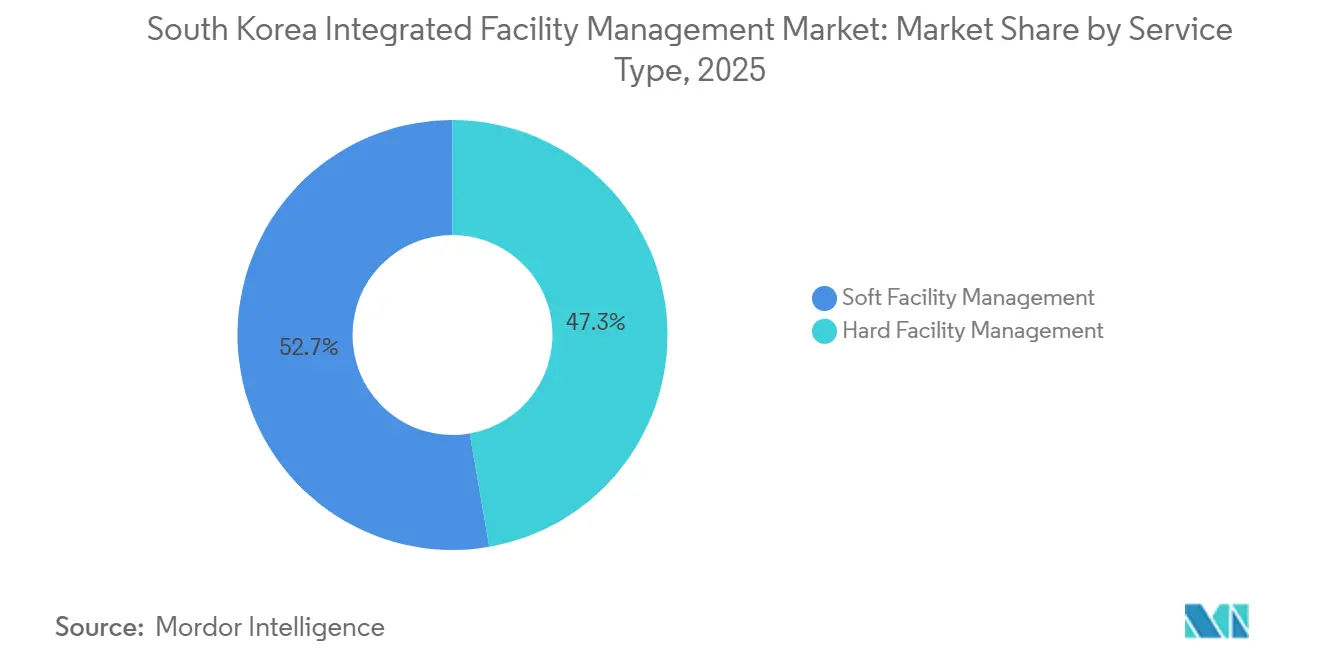

- By service type, soft facility management led the South Korea integrated facility management market with 52.7% market share in 2025, while hard facility management recorded the highest projected CAGR at 7.6% through 2031.

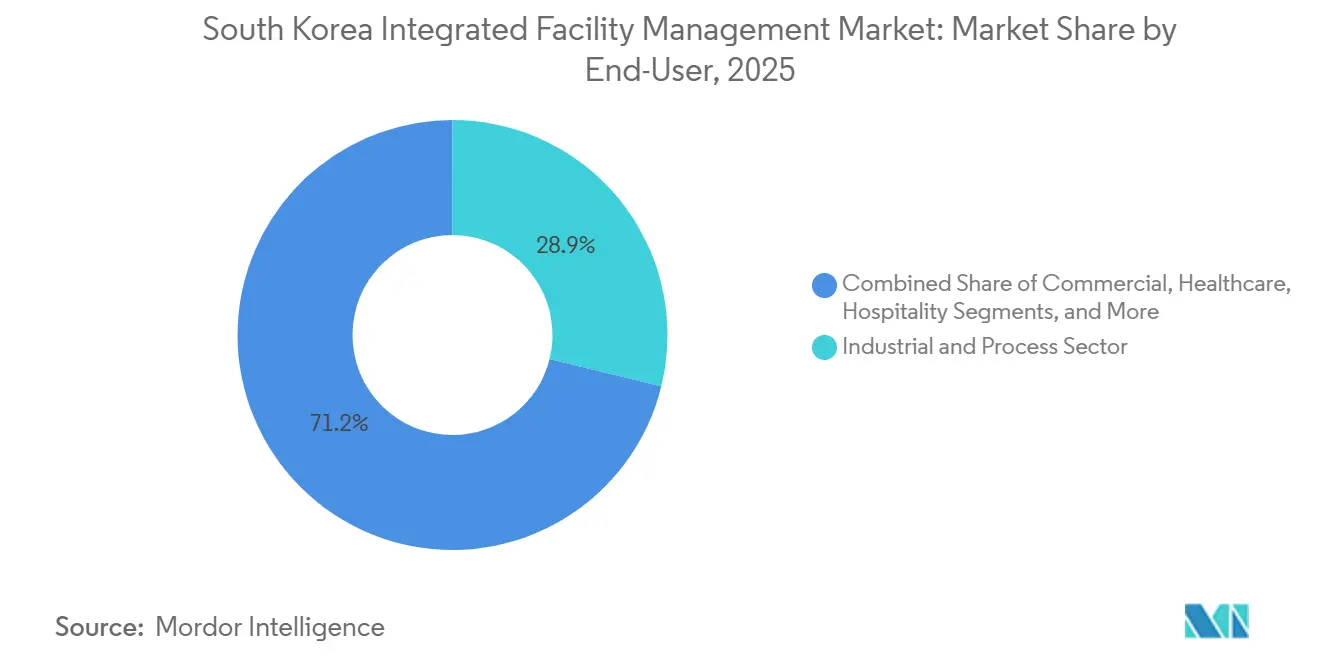

- By end-user, the industrial and process sector held 28.9% of the South Korea integrated facility management (IFM) market share in 2025, while the Commercial segment is forecast to expand at 7.6% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Korea Integrated Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Multi-Service Integrated Contracts | +1.5% | Seoul Capital Area and major metropolitan CBDs | Short term (≤2 years) |

| Acceleration of Smart Building Retrofits for Energy Efficiency | +1.2% | National, with early gains in Seoul, Incheon, and Sejong | Medium term (2-4 years) |

| Outsourcing Trend Among Chaebol-Owned Real-Estate Arms | +0.9% | National, centered on Seoul, Ulsan, and Pohang | Medium term (2-4 years) |

| Increase in Foreign Direct Investment in Data Centers | +0.7% | Gyeonggi Province, Ulsan, Jeollanam-do | Short term (≤2 years) |

| Government's K-New Deal Funding for Green Infrastructure | +0.5% | National, with capital concentration in public-asset clusters | Long term (≥4 years) |

| Rapid Growth of Logistics Warehouses Driven by E-Commerce | +0.4% | Greater Seoul Area and Gyeonggi logistics corridors | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Multi-Service Integrated Contracts

The consolidation of cleaning, security, MEP maintenance, energy management, asset services, and workplace support into a single service model is becoming a standard buying pattern in the South Korean integrated facility management market. Cushman & Wakefield Korea entered this space with an IFM service that launched with 9 global companies and targeted 15-20% reductions in maintenance costs by combining janitorial services, food management, disaster prevention, and data center support under one provider. That structure reduces accountability gaps that often arise when several subcontractors share the same building, and no single operator owns the final service outcome. It also supports performance-based billing, as clients can measure uptime, energy use, safety outcomes, and service quality through a single contract rather than multiple disconnected fee lines. As more large occupiers and asset owners adopt this format, vendors without multi-trade capability are losing ground in tender shortlists, and an integrated scope is becoming the first test of relevance.

Acceleration Of Smart Building Retrofits for Energy Efficiency

Energy-focused retrofits are moving from optional improvement programs to formal compliance and asset-value agendas across the South Korea integrated facility management market. South Korea's 3rd Basic Green Building Plan for 2025-2029 expanded the push for phased green remodeling in public buildings and tightened the operating context around Zero-Energy Building implementation.[1]Smart City Korea, “Green Remodeling and Zero-Energy Building Policy Updates,” Smart City Korea, smartcity.go.kr That policy environment favours operators that can combine HVAC upgrades, BEMS deployment, commissioning, preventive maintenance, and energy reporting within one managed contract. A Korean retrofit case at Factorial Seongsu also strengthened the commercial case for these projects, as Samsung Electronics' b.IoT solution delivered a 27% energy reduction between June and September 2025 and supported the country's first SmartScore Gold certification in January 2026. As building owners look for measurable savings instead of one-off repair work, the retrofit pipeline is shifting toward providers that can keep technical systems optimized after the initial upgrade is complete.

Outsourcing Trend Among Chaebol-Owned Real-Estate Arms

Chaebol-linked property groups are reshaping the South Korea integrated facility management market by treating facility operations as a growth platform rather than only an internal support function. Hyundai GBFMS rebranded as Hyundai Property in March 2026 and openly positioned itself as a total real estate service platform and a "K-IFM company" that intends to compete for third-party contracts beyond the Hyundai group perimeter. POSCO WIDE already provides facility management not only for group assets but also for external clients such as Naver and NCsoft, which shows that open-market work is now a practical outlet for mature in-house capability.[2]POSCO WIDE, “Facility Management Services and External Client Operations,” POSCO WIDE, poscowide.com This change reflects the growing complexity of mixed-use developments, knowledge industry centers, and data-intensive campuses, where general internal teams struggle to match the technical range now required. It also opens space for technology partnerships, because chaebol affiliates can pair local access and operating scale with software, analytics, and specialist systems from multinational or domestic technology partners.

Increase In Foreign Direct Investment in Data Centers

Data center construction is creating one of the most specialized demand pools in the South Korea integrated facility management market because these facilities need uninterrupted control across cooling, electrical systems, fire suppression, security, and digital monitoring. SK Group and Amazon Web Services announced a KRW 7 trillion investment, equal to USD 5.11 billion, for a large AI data center in Ulsan with an initial 100 MW capacity planned for 2029 and later expansion toward 1 GW. In January 2026, Koramco Asset Management announced the K Square Data Center Uijeongbu project at 80,000 sq m and 100 MW, and the company said it plans to invest KRW 10 trillion, equal to USD 7.4 billion, by 2032, with LG CNS joining the facility operations consortium. The AI Data Center Special Act, scheduled for implementation in February 2026, further improves the project pipeline by simplifying permit procedures through the Ministry of Science and ICT. Each hyperscale or AI-focused campus can support a long contract cycle, so early positioning on design, commissioning, and operating standards is becoming a decisive competitive advantage for integrated FM providers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Certified FM Technicians in Provincial Regions | -0.8% | Non-capital provinces, North and South Chungcheong, Jeolla, Gangwon | Medium term (2-4 years) |

| Persistent Unionization Risks in Soft FM Labor | -0.6% | National, acute in large metropolitan FM operations | Short term (≤2 years) |

| Low Profitability Pressures from Cost-Plus Contracts | -0.4% | National | Short term (≤2 years) |

| Cybersecurity Liabilities in IoT-Enabled Building Systems | -0.3% | National, most acute in data center and smart building clusters | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Shortage Of Certified FM Technicians in Provincial Regions

Provincial expansion remains difficult because the supply of qualified technicians is not keeping pace with the rising complexity of managed assets in the South Korea integrated facility management market. A March 2026 survey of 300 housing managers found that 56.7% considered staffing levels inadequate, while 63.7% pointed to stronger repair demand and 49.7% cited rising inspection and administrative obligations. The problem becomes more serious outside the capital region, where operators have a thinner pool of trained labour, weaker local subcontractor depth, and less flexibility when technicians need to cover multiple sites. Remote monitoring tools can help with visibility and alarms, but they do not replace hands-on technical work for MEP systems, life-safety assets, or urgent repairs that require certified personnel on site. This bottleneck reduces service consistency, slows expansion into non-capital provinces, and narrows the pace at which providers can extend the South Korea integrated facility management market beyond its strongest urban bases.

Persistent Unionization Risks in Soft FM Labor

Labor relations tightened in 2025 for the outsourced workforces that support cleaning, security, catering, and similar soft-service scopes across the South Korea integrated facility management market. The August 2025 amendment to the Trade Union and Labour Relations Adjustment Act established a legal basis for subcontracted workers to bargain directly with principal employers in cases where those employers substantially shape working conditions.[3]TUAC Secretariat, “Collective Bargaining Rights for Subcontracted Workers in Korea,” TUAC, tuac.org By March 2026, more than 20,000 subcontract workers across 58 branches of the Korean Metal Workers' Union had submitted bargaining demands to 18 principal employers, which showed how quickly the new framework could move from legal change to practical pressure. Soft FM providers are especially exposed because a large share of their delivery model still depends on outsourced labour and cost-plus structures that leave limited room to absorb new compliance and wage obligations. Demand for services is still present, but the cost of maintaining margins will rise if renegotiation, labour oversight, and workforce stabilization become more complex across large contracts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Soft FM Holds the Largest Base While Hard FM Gains on Technical Work

Soft Facility Management (FM) held 52.7% of the South Korea integrated facility management (IFM) market share in 2025, which kept it as the largest service category by revenue contribution. That position came from the long-established demand for cleaning, security, office support, catering, and related workplace services across dense commercial, institutional, and mixed-use building stock. Security and office support are already seeing gradual labour substitution through AI-based access control, remote CCTV monitoring, and centralized command functions, which reduce the number of personnel required per managed site. Catering remains more resilient than several other soft services because large employers still connect food quality, wellness, and daily workplace experience with staff productivity and tenant satisfaction. Even with its scale, Soft FM does not fully dominate profit pools in the South Korea IFM industry, because unit pricing remains lower than technical services and wage pressure has become harder to absorb after recent labour law changes.

Hard FM in the South Korea IFM market is projected to grow at a 7.6% CAGR from 2026 to 2031, which makes it the fastest-growing service type in the period under review. Growth is tied to AI data centers, pharmaceutical cleanrooms, semiconductor support buildings, advanced logistics facilities, and smart mixed-use towers that depend on continuous MEP uptime and qualified technical teams. Fire systems and safety services remain the most stable hard-service line because building compliance rules make them less discretionary than many support tasks, and renewals are often tied to statutory obligations. Asset management is also gaining weight as owners of older commercial properties use BEMS, IoT sensor networks, and condition-based maintenance planning to extend equipment life and reduce emergency repair spending. LG Electronics reported average annual energy savings of 8.4% over three years after a BEMS installation at the Osong Pulmuone Technology Institute, which supports the case for more optimization-led contracts within the South Korea IFM market.

By End User: Industrial Sites Lead While Commercial Demand Builds Faster

The industrial and process segment accounted for 28.9% of the South Korea IFM market size in 2025, making it the largest end-user group in the country. Its lead came from the scale of automotive, steel, semiconductor, energy, and chemical assets that require continuous inspection, hazardous-material controls, shutdown planning, and 24-hour plant support at premium service levels. These contracts are usually larger and longer than many office or retail assignments, so they provide stronger visibility and a more stable revenue base for providers that can meet technical and safety requirements. POSCO WIDE's work across both group assets and external client campuses shows how industrial operating discipline is now crossing into advanced commercial environments as well. Institutional and public infrastructure assets are also becoming more important because green remodeling obligations are widening the volume of retrofit, compliance, and energy-management work that technical FM providers can address.

The commercial segment in the South Korea IFM market is projected to expand at a 7.6% CAGR from 2026 to 2031, which places it ahead of all other end-user categories by growth pace. Demand is rising across BFSI offices, IT and telecom campuses, retail chains, warehouse facilities, and co-location data center environments, especially where grade-A assets require stronger reporting and technical coordination. Cushman & Wakefield Korea's IFM entry aimed directly at global technology and financial clients, which confirms that international providers see commercial occupiers as the clearest initial opening for scale in South Korea. Smaller residential towers, mixed-use assets, and knowledge industry centers are also adding volume because these properties increasingly need semi-professional operating models instead of informal building supervision. That broader base should support steady contract formation even when the largest individual mandates continue to come from industrial complexes and premium commercial assets.

Geography Analysis

The Seoul Capital Area represents the largest concentration of the South Korea integrated facility management market because it combines the highest density of grade-A office buildings, data centers, logistics parks, financial occupiers, and sophisticated procurement teams. CBRE Korea reported that e-commerce operators accounted for 33% of leased logistics floor area in the Greater Seoul Area during the first half of 2025, which sustained warehouse FM demand across the Gyeonggi logistics corridor. Savills also reported that South Korea online retail transactions rose 5.4% in 2024 to KRW 171.5 trillion, and that larger transaction base continues to support the operating needs of distribution and fulfilment facilities. Incheon is also building a fresh smart urban management pipeline after the city and LG CNS agreed in October 2025 to transform five aging planned districts with AI- and robot-based services.

The southeastern industrial corridor around Ulsan, Pohang, and Busan forms the second major demand zone for the South Korea integrated facility management market. Its base still comes from petrochemicals, automotive production, steelmaking, marine logistics, and port-linked distribution assets, which create durable demand for plant support, utilities management, safety compliance, and technical maintenance. The AWS and SK Group AI data center project in Ulsan is widening the corridor from conventional industrial maintenance to critical-systems management and advanced cooling oversight. That shift will likely attract more specialist international providers into an area that was previously shaped more heavily by chaebol-linked operating models. Busan's logistics position also keeps regional demand broad because port and distribution facilities require continuous security, environmental services, and operational support alongside technical maintenance.

Non-capital regions are gaining greater strategic value as the AI Data Center Special Act supports easier project development beyond Seoul and encourages more dispersed digital infrastructure investment. Planned projects in places such as Uijeongbu, Jeollanam-do, Chungcheong, and Gangwon will widen the geographic base of technically demanding contracts as new campuses and support facilities move forward. Even so, staffing shortages outside the capital continue to slow execution and make service quality harder to standardize in provincial markets where training depth remains limited. That gap means providers with stronger workforce-development systems, centralized control capabilities, and remote monitoring tools should be in a better position as the South Korea integrated facility management market spreads beyond its current urban core.

Competitive Landscape

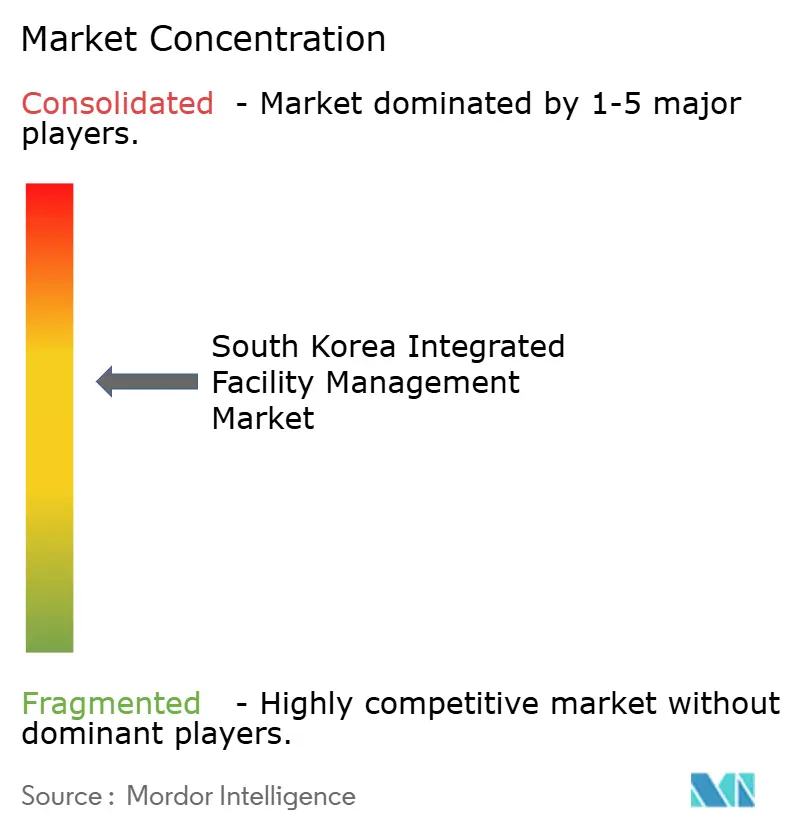

Competition in the South Korea integrated facility management market had moderate consolidated at the top in 2025, but it is spread across several groups rather than controlled by a small national cluster. Global real estate and workplace services firms such as CBRE, JLL, Cushman & Wakefield, ISS, and Sodexo focus on larger multinational and premium commercial mandates where platform scale, global procurement, and integrated reporting matter most. Domestic players such as Hyundai Property, POSCO WIDE, LG CNS, CJ Facilities Management, and Lotte Property bring local relationships, asset familiarity, and group-linked operating experience that remain important in Korean procurement cycles. A further layer of specialized domestic operators, including S1 Corporation, S&I Corporation, and Kolon LSI, competes through niche building expertise, monitoring tools, and operating certifications rather than broad portfolio scale. This structure keeps national concentration low even though prime office and data center sub-segments can be more tightly contested by a smaller group of qualified bidders.

Recent strategic moves show that providers are widening scope and capability instead of only adding labour volume. CBRE agreed to acquire Industrious for USD 1.6 billion in 2025, which strengthens its ability to combine workplace operations with core FM and offer multinational occupiers a more unified building service model. Hyundai Property's March 2026 repositioning showed that chaebol FM subsidiaries now want third-party mandates as a formal growth path, not simply as occasional spillover work from existing group capabilities. Veolia Korea's April 2025 contract extension across four Catholic Medical Center hospitals also showed that healthcare campuses remain an attractive vertical for long-duration technical and energy-oriented service agreements.

Technology is becoming the clearest separator in the South Korea integrated facility management market because clients increasingly want energy optimization, access management, building control, and field response in one operating environment. LG CNS stated that its Cityhub Building platform combines data collection, facility control, energy optimization, and blockchain-based access management through one dashboard, which gives it a broader digital layer than many pure-play FM competitors. Samsung Electronics' b.IoT deployment at Factorial Seongsu created a local performance benchmark after the building achieved a 27% energy reduction and the country's first SmartScore Gold certification in January 2026. Providers that can connect these software layers with dependable field execution, certified technical teams, and measurable reporting should hold the stronger position as outsourcing expands into more complex assets.

South Korea Integrated Facility Management Industry Leaders

Jones Lang LaSalle Incorporated

Cushman & Wakefield plc

ISS A/S

Colliers International Group Inc.

CBRE Group, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Hyundai GBFMS rebranded as Hyundai Property, repositioning as a "total real estate service platform" and "K-IFM Company" with explicit intent to compete for third-party FM contracts beyond the Hyundai group perimeter, signaling a structural shift in how chaebol FM subsidiaries approach open-market competition in South Korea.

- January 2026: Koramco Asset Management announced the K Square Data Center Uijeongbu project, an 80,000 sq m, 100 MW facility with 2 buildings to meet high-efficiency AI and hybrid cloud demand. LG CNS joined the operations consortium, and Koramco committed a KRW 10 trillion (USD 7.4 billion) investment plan by 2032, directly adding a large-scale critical FM demand pipeline in Gyeonggi Province.

- January 2026: Factorial Seongsu became the first building in South Korea to receive a SmartScore Gold certification, deploying Samsung Electronics' b.IoT AI-based integrated building solution and achieving 27% energy reduction between June and September 2025, establishing a market reference for energy-efficiency-tied FM contracts.

- December 2025: S&I Corporation secured the FM contract for the CJ ENM Center in Sangam-dong, Seoul, covering all facility operations including inspection, maintenance, energy management, environmental services, cleaning, safety, and security for the broadcasting and content production complex, a significant integrated FM win for a domestic specialist in a high-uptime media facility.

South Korea Integrated Facility Management Market Report Scope

The South Korea Integrated Facility Management Market Report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, Fire Systems and Safety, and Other Hard Facility Management Services], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and Other Soft Facility Management Services]), End User (Commercial (includes BFSI, IT and Telecom, Retail and Warehouses, etc.), Hospitality (includes Eateries, Restaurants and Large-Scale Hotels), Institutional and Public Infrastructure (includes Government Establishments, Education, Transportation such as Airports and Railways, etc.), Healthcare (includes Public and Private Healthcare Facilities), Industrial and Process Sector (includes Manufacturing, Energy including Oil and Gas Exploration, Mining, etc.), and Other End-User Industries (Multi-House Residential, Entertainment, Sports and Leisure)). The Market Forecasts are Provided in Terms of Value (USD).

| Hard Facility Management | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft Facility Management | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management Services |

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process Sector |

| Other End-User Industries |

| By Service Type | Hard Facility Management | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft Facility Management | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management Services | ||

| By End User Industry | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process Sector | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

What is the 2031 outlook for integrated facility management in South Korea?

The South Korea integrated facility management market was valued at USD 6.18 billion in 2025 and is forecast to reach USD 9.05 billion by 2031, growing at a 6.68% CAGR over 2026-2031.

Which service area is growing the fastest through 2031?

Hard FM is expected to post the fastest growth at 7.6% CAGR through 2031 as demand rises from data centers, advanced industrial facilities, technical retrofits, and compliance-driven maintenance.

Why are data centers becoming important for facility management providers in South Korea?

New AI and hyperscale campuses require uninterrupted cooling, power, fire safety, and security support, which creates long-duration, technically complex contracts that are larger than conventional office assignments.

Which end-user group creates the biggest current demand?

The industrial and process segment led in 2025 with 28.9% share because South Korea's automotive, steel, semiconductor, energy, and chemical assets need continuous plant support and safety-led maintenance.

What is the main challenge for providers trying to grow outside Seoul?

Provincial expansion is limited by a shortage of qualified technicians, which makes it harder to maintain service quality, scale technical delivery, and support more sophisticated contracts in non-capital regions.

Page last updated on: