Indonesia Integrated Facility Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

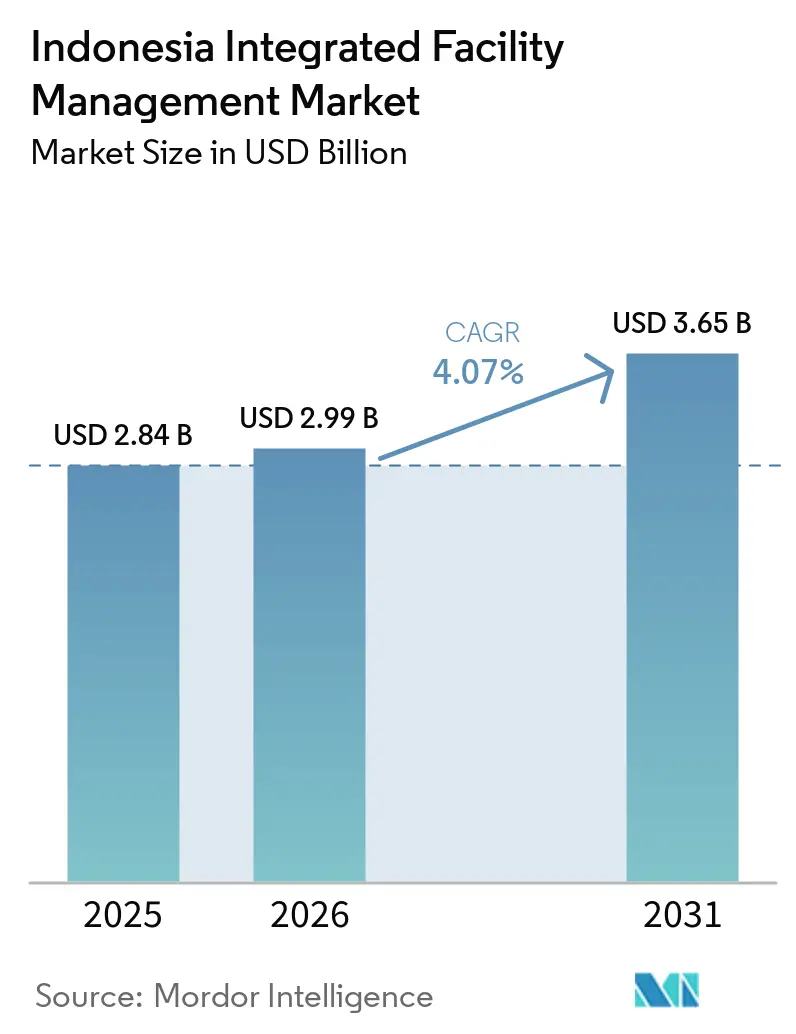

| Base Year Market Size (2025) | USD 2.84 Billion |

| Market Size (2026) | USD 2.99 Billion |

| Market Size (2031) | USD 3.65 Billion |

| Growth Rate (2026 - 2031) | 4.07% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Integrated Facility Management Market Analysis by Mordor Intelligence

The Indonesia Integrated Facility Management Market size is expected to grow from USD 2.84 billion in 2025 to USD 2.99 billion in 2026 and is forecast to reach USD 3.65 billion by 2031 at 4.07% CAGR over 2026-2031.

The Indonesia integrated facility management market is being supported by tighter green and smart building compliance, since Ministerial Regulation No. 21 of 2021 set green building thresholds for large offices, commercial buildings, residential buildings, and hospitals, while Regulation No. 10 of 2023 extended automation, energy management, and cybersecurity requirements to qualifying high-rise buildings. The addressable service base is also widening because green building certified area reached 7.4 million m² in 2024, and the PUPR roadmap targets 16.5 million m² by 2030, which increases recurring demand for audits, commissioning, and ongoing building performance management. Demand is spreading beyond the main metro clusters because 251 cities and districts were participating in Indonesia’s Smart City program by 2024, which supports wider adoption of integrated digital building operations. Competitive conditions remain balanced rather than highly concentrated because global providers bring operating systems, procurement scale, and technology tools, while regional and domestic firms remain relevant in cost-sensitive and relationship-led contracts. Growth in the Indonesia integrated facility management market is still moderated by technician shortages, fragmented equipment sourcing, inter-island logistics, and labour cost obligations that make national service delivery more complex than headline demand alone suggests.

Key Report Takeaways

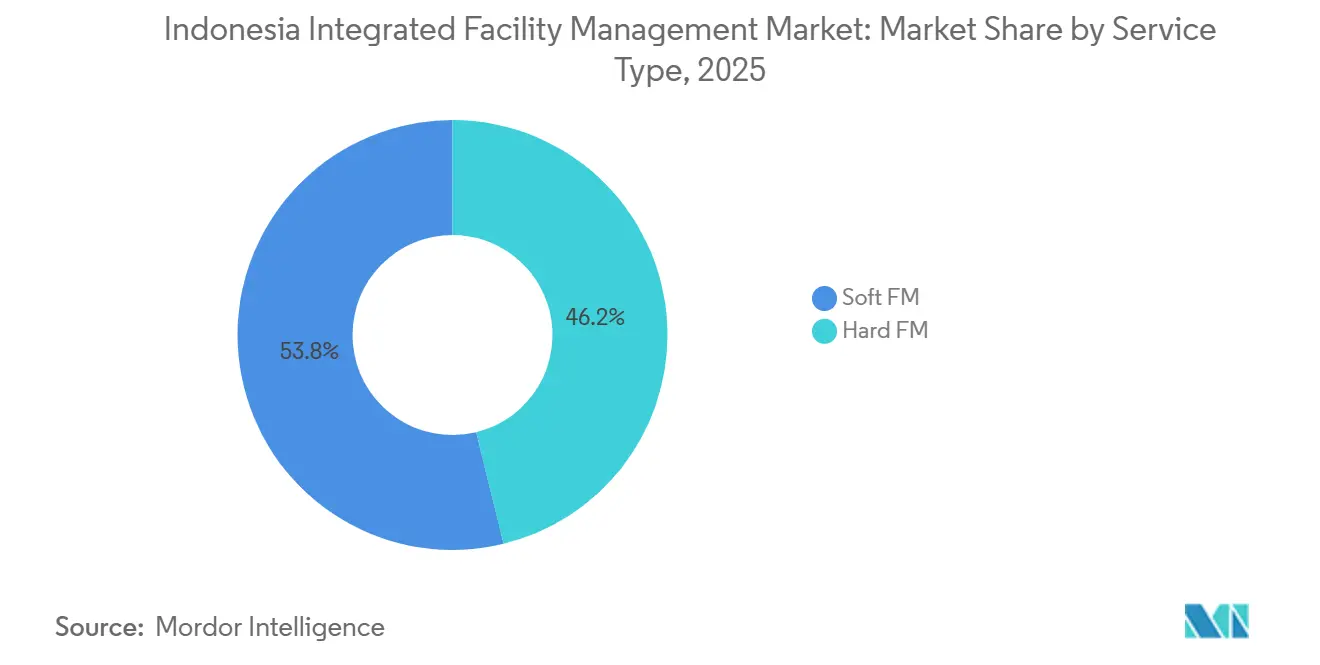

- By service type, Soft facility management held 61.6% of the Indonesia integrated facility management market share in 2025, while Hard FM is forecast to expand at a 5.1% CAGR through 2031.

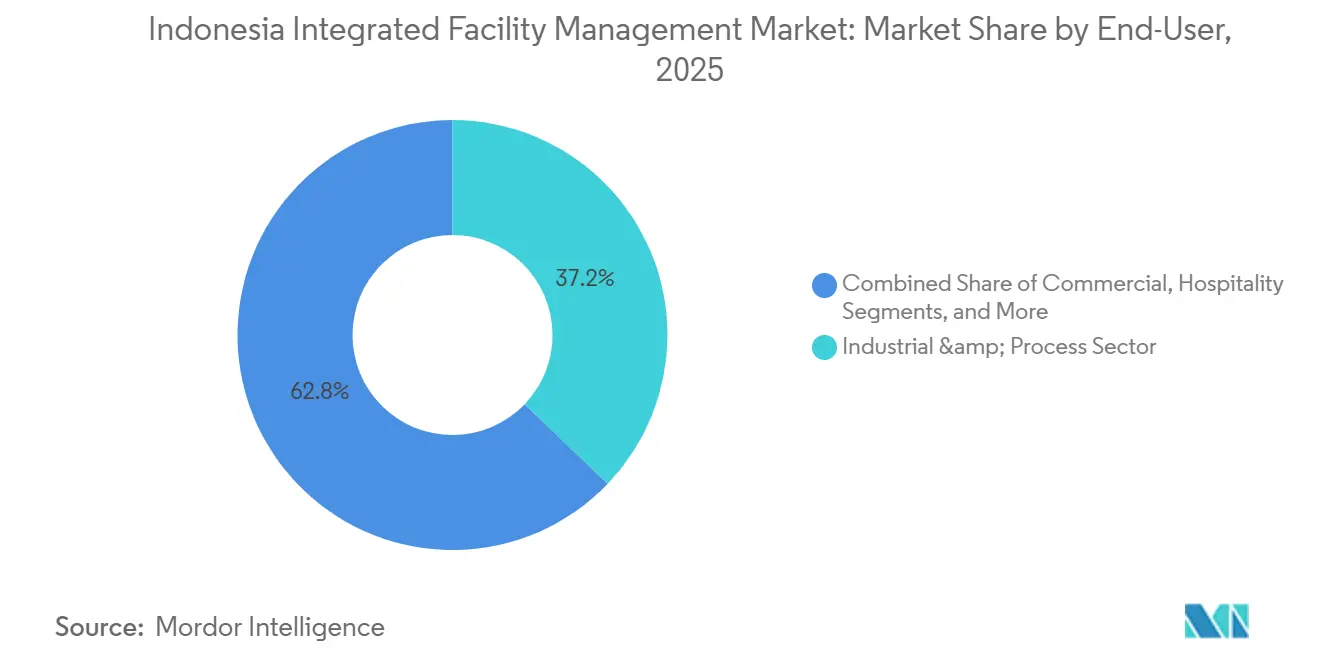

- By end user, the industrial and process sector accounted for 27.8% of the Indonesia integrated facility management (IFM) market size in 2025, while the commercial segment is projected to grow at a 4.9% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Indonesia Integrated Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Expansion of Commercial Real Estate in Urban Hubs | +1.4% | Greater Jakarta, Surabaya, Bandung, Medan | Short term (≤ 2 years) |

| Growing Outsourcing Trend to Focus on Core Competencies | +1.0% | National, with early concentration in Jakarta and key industrial corridors | Medium term (2-4 years) |

| Government Incentives for Green and Smart Buildings | +0.8% | National, with early gains in Jakarta, Surabaya, and Bandung | Long term (≥ 4 years) |

| Rising ESG-Linked Asset Management Mandates by Sovereign Funds | +0.5% | National, particularly infrastructure-heavy corridors | Medium term (2-4 years) |

| Digital Twin Adoption for Predictive Maintenance | +0.4% | Urban centers with high-rise and institutional stock | Long term (≥ 4 years) |

| Facility Consolidation in Decommissioned Oil and Gas Sites | +0.3% | Offshore Kalimantan, East Java, Sumatra coastal zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Commercial Real Estate in Urban Hubs

The Indonesia integrated facility management market is benefiting from tighter office supply in premium urban districts, where Jakarta’s CBD Grade A occupancy stayed above 75% in Q4 2024, and no new Grade A buildings were completed during the prior two years.[1]CBRE Indonesia, “Jakarta Office Market Update Q4 2024,” CBRE Indonesia, cbre.co.id That setting is pushing landlords to compete more on building performance, tenant service quality, and operating reliability than on the simple expansion of floor space. The same pattern is visible in newer asset categories, since INA and DayOne established a Batam data center platform with 72.4 MW capacity that was fully contracted by a global hyperscaler for ten years, which points to steady demand for power, cooling, safety, and security management.[2]Indonesia Investment Authority, “Annual Report 2024,” Indonesia Investment Authority, ina.go.id In near-term office supply, only two new Grade A towers, Two Sudirman and Indonesia One, are scheduled for completion in 2027 and 2028, which supports continued demand for strong service standards in existing stock. This keeps the Indonesia integrated facility management (IFM) market closely tied to asset-quality competition in major urban hubs rather than to growth in building count alone.

Growing Outsourcing Trend to Focus on Core Competencies

The Indonesia integrated facility management market is seeing stronger outsourcing demand from institutions that previously kept building operations in-house, especially in transport, healthcare, and event infrastructure. ISS Indonesia’s reappointment at the Jakarta International Convention Center and its appointment across TransJakarta’s 231 km BRT network show that large public-facing assets are now using structured service contracts at an operating scale. That demand matters because the TransJakarta network serves more than one million passenger trips a day, so cleaning, maintenance, and support services must be delivered with repeatable processes and clear service control. JLL’s appointment at Bali International Hospital adds another example, since a high-complexity healthcare asset moved into an internationally managed building operations model soon after inauguration. As outsourcing broadens from private commercial buildings to public and quasi-public assets, the Indonesia IFM market gains a larger base of multi-site and longer-duration contracts.[3]JLL, “Bali International Hospital Appoints JLL As Building Management Partner,” JLL, jll.com

Government Incentives for Green and Smart Buildings

The Indonesia integrated facility management market is being boosted by regulations that require energy performance, automation, and operational monitoring as part of basic compliance rather than optional upgrades. Ministerial Regulation No. 21 of 2021 applies green building requirements to office buildings of at least 50,000 m², commercial and residential buildings of at least 5,000 m², and hospitals of at least 20,000 m².[4]International Energy Agency, “Indonesia Smart Building And Green Building Compliance Overview,” International Energy Agency, iea.org Regulation No. 10 of 2023 adds smart building obligations for high-rise buildings with eight or more floors, including automation, energy management, and cybersecurity provisions. Johnson Controls’ work at Thamrin Nine showed what this means in practice, because the project delivered a 30% reduction in energy use through YORK chiller systems and building automation, then achieved BCA Green Mark Platinum certification. The AC performance standards tightened by the Ministry of Energy and Mineral Resources in October 2024 also support hard-service demand, since a higher CSPF threshold and the removal of single-star units create a replacement and upgrade cycle across existing building stock.

Rising ESG-Linked Asset Management Mandates by Sovereign Funds

The Indonesian integrated facility management (IFM) market is also benefiting from stricter asset oversight by long-term capital providers, which now expect measurable operating and sustainability performance from portfolio assets. INA stated that ESG screening was embedded in every investment decision in 2024, supported by an ESG Portfolio Monitoring System and a Governance, Sustainability, and Resilience score of 64%, ahead of the 53% global sovereign wealth fund average cited in its annual report. INA’s infrastructure holdings accounted for 77% of its accumulated USD 3.4 billion investment by the end of 2024, indicating that large built assets under institutional ownership are increasingly being reviewed through compliance, safety, and resource-efficiency lenses. The discipline becomes stronger when global co-investors are involved, because ADIA, APG, Manulife Investment Management, and Allianz Global Investors also add their own due diligence expectations around reporting and controls. Third-party credentials are becoming more useful in this context, which is why ISS Indonesia’s EcoVadis 2025 Bronze Medal, awarded in March 2026, matters as a procurement signal for institutional clients.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Skilled Technicians for Advanced Systems | -1.2% | National, most acute in outer islands and secondary cities | Short term (≤ 2 years) |

| Fragmented Supplier Base Inflating Procurement Costs | -0.8% | National | Medium term (2-4 years) |

| Low Technology Adoption Among Small Facility Owners | -0.5% | Tier-2 and tier-3 cities, secondary commercial stock | Long term (≥ 4 years) |

| Labour Law Uncertainties and Contractual Rigidities | -0.4% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled Technicians for Advanced Systems

The Indonesia integrated facility management market still faces a skill bottleneck in building automation, HVAC optimization, fire systems, and other advanced technical services that are becoming more important under newer building rules. The gap is visible in digital operations because the 2025 ITB work on HVAC digital twins assumed technicians who could manage IoT sensors, live data flows, and system tuning. That skill profile is limited outside the main Java corridor, which makes high-standard service deployment uneven across the country. Indonesia’s island geography makes the constraint harder to solve because moving specialist teams to outer-island industrial and energy sites adds travel, housing, and response-time pressure. UEM Edgenta’s FY2025 emphasis on multi-skilling, competency-based training, and cross-deployment shows that workforce development is a sector-wide operating need rather than a short-term staffing issue.

Fragmented Supplier Base Inflating Procurement Costs

The Indonesia IFM market remains exposed to uneven equipment sourcing, especially for chillers, MEP parts, and fire suppression components, where certified distributors coexist with many informal traders. More than 130 mandatory SNI standards were in effect across safety, health, and environmental areas by 2024, but supplier-level enforcement still varies, which complicates quality verification for service providers. This cost burden is lower for multinational operators with larger buying systems because procurement scale improves price access and delivery coordination across projects. Local and regional firms face higher per-unit costs and more uncertain lead times, which can weaken their position in technically demanding bids where uptime guarantees matter. Margin pressure becomes sharper when imported components are needed under multi-year contracts priced in rupiah, because equipment exposure and delivery risk are hard to pass through cleanly to clients.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Soft FM Leads While Hard FM Gains from Compliance Requirements

Soft facility management (FM) retained 61.6% of the Indonesia integrated facility management (IFM) market size in 2025, which reflected the country’s labor-intensive operating model across cleaning, security, office support, catering, and related workplace services. The Indonesia integrated facility management market has long favored soft services because many owners first outsourced visible day-to-day operations before moving into deeper technical outsourcing. That pattern still holds in many facilities where cleaning quality, manpower reliability, and front-line support shape user experience more directly than advanced engineering systems. Soft-service demand is also being strengthened by stricter hygiene expectations in healthcare and hospitality, where operators want more formal compliance controls and service tracking. In security, the market is moving toward more integrated delivery, as OCS Indonesia’s May 2025 partnership with Baharkam Polri showed that institutional clients are looking for scalable models that combine governance and operational oversight.

Hard FM is the faster-moving part of the Indonesia IFM industry, and it is forecast to rise at a 5.1% CAGR through 2031 as automation, HVAC performance, fire safety, and MEP reliability become compliance requirements that are harder to postpone. The smart building rules and tighter AC efficiency standards are moving owners toward retrofit, commissioning, and performance-monitoring work across existing high-rise stock. Johnson Controls’ completed work at Thamrin Nine gave the Indonesia IFM market a visible benchmark because the project paired advanced chiller plant design with building automation and delivered a 30% energy reduction. Catering remains more fragmented than cleaning or security, yet remote industrial and energy projects are increasingly favouring integrated camp management contracts where supply continuity and workforce servicing must be maintained across difficult locations. This keeps Soft FM dominant by current revenue, while Hard FM gains ground as compliance and energy performance become more central to asset operations.

By End User: Industrial Demand Forms the Base While Commercial Expands Fastest

The industrial and process sector accounted for 27.8% of the Indonesia integrated facility management market size in 2025, giving it the largest end-user position across the current revenue mix. Industrial demand is anchored in remote sites, heavy operations, and utility-scale assets where food services, housekeeping, maintenance, and safety support must run continuously rather than as periodic outsourced tasks. Aden Indonesia’s three-year contract at the Halmahera mining site covered catering, housekeeping, and laundry for around 400 personnel, which shows how deeply integrated service packages are entering remote resource operations. ISS Indonesia’s August 2025 contract with Indo Raya Tenaga for the Jawa 9 and 10 power plant added a second example of industrial clients turning to structured FM with technology adoption and occupational health and safety controls. Oil and gas decommissioning adds another industrial layer because more than 630 offshore platforms and PTK-040/2023 planning requirements create a long-tail need for inspection, maintenance, and repair support.

The commercial segment has the fastest growth forecast in the Indonesia IFM market and is projected to expand at a 4.9% CAGR through 2031, supported by premium office operations, logistics facilities, data centers, and healthcare-linked built assets. This growth is closely tied to occupier preference for reliable and professionally managed buildings where uptime, service quality, and compliance matter more than basic cost minimization. ISS Indonesia’s OPPO manufacturing facility contract showed this shift clearly, because the scope combined cleaning, gardening, and integrated pest management with real-time IFM performance tracking. Healthcare is also becoming more important, and JLL’s appointment at Bali International Hospital covered building operations, infrastructure systems, and environmental impact monitoring under international standards. Public and institutional assets add further headroom, since the Indonesia integrated facility management (IFM) market is now reaching convention venues, bus rapid transit networks, and ministry-linked hospital facilities through larger outsourced service models.

Geography Analysis

Geographic share figures for the Indonesia integrated facility management market were not disclosed, but current demand is concentrated in the large urban and institutional corridors where premium office, transit, healthcare, and high-rise assets are most established. Greater Jakarta remains the clearest anchor because premium office occupancy held above 75% in the CBD through Q4 2024 while no new Grade A supply entered during the prior two years, which increased the operating importance of existing stock. Surabaya and Bandung are also relevant in the regulatory buildout, since the green and smart building push is expected to gain early traction there alongside Jakarta. Medan appears in the near-term commercial real estate demand map, reflecting the spread of formal facility operations beyond a single-city pattern. Across these urban centers, the Indonesia integrated facility management market is being shaped by compliance-led service demand rather than by simple expansion of basic manpower contracts.

Outside Java’s main commercial corridor, the geography story becomes more specialized and more operationally uneven. Batam stands out because INA and DayOne built a hyperscale data center platform there with 72.4 MW capacity fully committed by a global hyperscaler, creating continuous demand for power, cooling, security, and technical uptime management. Bali gained importance in healthcare-led demand after JLL was appointed building management partner for Bali International Hospital in the Sanur Health Special Economic Zone. Offshore Kalimantan, East Java, and Sumatra coastal zones matter for a different reason, because decommissioning and late-life energy assets need inspection, maintenance, repair, and camp-support capabilities that differ from urban office FM.

The wider national opportunity is becoming more visible because 251 cities and districts had joined the Smart City program by 2024, which broadens the digital building management base beyond the traditional Java core. At the same time, the Indonesia integrated facility management market still expands unevenly across the archipelago because more than 17,000 islands make spare-parts movement and technician dispatch slower and costlier than in a contiguous geography. This creates a two-speed pattern in which Jakarta and other major hubs adopt advanced FM practices faster, while smaller and more remote locations remain more selective in-service scope and technology use. Over time, the green building roadmap from 7.4 million m² of certified area in 2024 to 16.5 million m² by 2030 should widen recurring service demand across several provinces, but execution capability will still determine where revenue is captured first.

Competitive Landscape

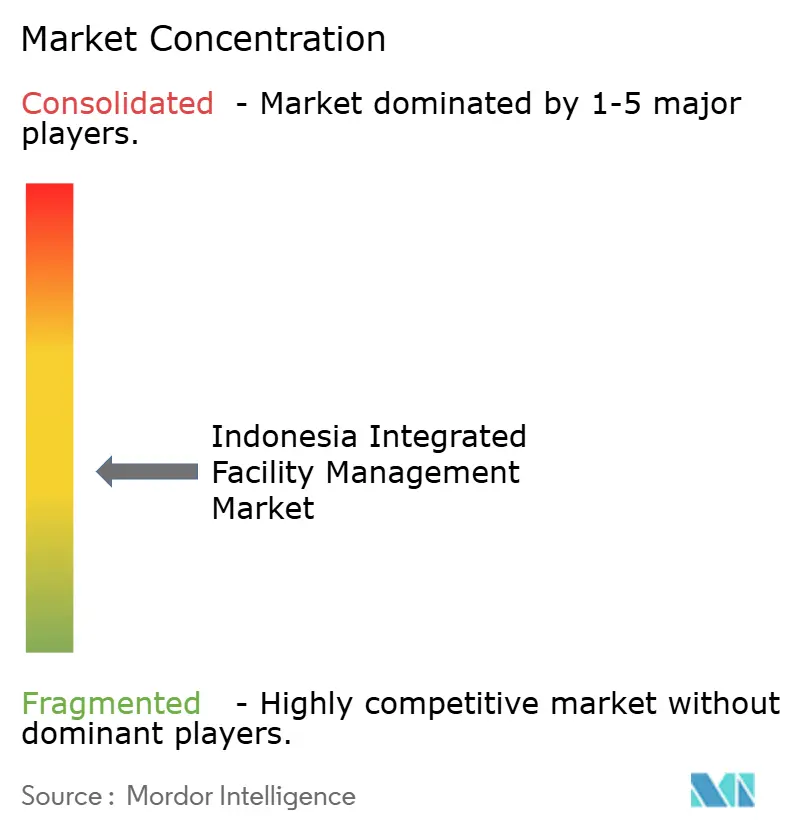

The Indonesia integrated facility management market is moderately fragmented, with global providers holding stronger positions in marquee contracts while local and regional firms remain active across smaller and more price-sensitive engagements. ISS A/S is one of the most visible operators in the country, and its Indonesia business reported more than 30 years of local operations and 45,000 domestic employees while adding contracts in transport, power, manufacturing, and healthcare during 2025. Johnson Controls competes from a building technology base, using installed HVAC, automation, and fire systems to create recurring hard-service opportunities around performance upgrades and long-term maintenance. JLL remains strongest where international operating standards and institutional asset requirements matter, which was visible in its 2025 appointment at Bali International Hospital. This mix means the Indonesia integrated facility management market is not led by a single dominant firm, and client choice still varies sharply by building type, geography, and service complexity.

Several strategic moves in 2025 and 2026 show how leading companies are building position through contract wins tied to specialized operating needs. ISS Indonesia expanded through public mobility and industrial operations, including TransJakarta, Jawa 9 and 10, OPPO Indonesia, and multiple healthcare sites, which shows a deliberate multi-vertical contracting approach. Johnson Controls strengthened its standing through the completed Thamrin Nine project, where measurable energy savings and advanced automation created a reference case for hard FM linked to green certification. UEM Edgenta moved in a different direction and used technical specialization to expand its Indonesia footprint, including a geothermal supply FM contract in Bandung during FY2025.

There is still room in the Indonesia integrated facility management market where demand is real, but formal contract penetration is lower than in landmark assets. Mid-market commercial sites, smaller manufacturers, and secondary hospitals remain less structured in procurement, which opens space for providers that can deliver standardization without the cost profile of premium multinational service models. Angkasa Pura Supports’ 2025 launch of an integrated FMS platform shows how domestic players are trying to use digital standardization to compete more effectively on service control and cost. A separate niche is emerging in offshore decommissioning support, where more than 630 aging platforms and PTK-040/2023 planning requirements create a technically narrow but valuable service area with no clear dominant provider yet.

Indonesia Integrated Facility Management Industry Leaders

PT ISS Indonesia

PT CBRE Indonesia

PT Jones Lang LaSalle Indonesia

Cushman & Wakefield plc

Sodexo S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: INA led DayOne Data Centers’ Series C round, exceeding USD 2.0 billion. INA anchored a hyperscale data center investment platform targeting APAC and European markets. The flagship Batam facility, with 72.4 MW capacity fully committed by a global hyperscaler, requires specialist FM for power, precision cooling, and security systems on a continuous basis.

- March 2026: ISS Indonesia received the EcoVadis 2025 Bronze Medal. ISS Indonesia was recognized with an EcoVadis Bronze sustainability rating, giving institutional clients a third-party validated ESG credential that is increasingly used as a pre-qualification threshold.

- November 2025: Johnson Controls and Thamrin Nine completed a Jakarta green building project. Johnson Controls completed a multi-year collaboration at Thamrin Nine, reducing energy use by up to 30% through YORK chiller plant design and Metasys Building Management System integration. The project achieved BCA Green Mark Platinum certification, and Johnson Controls continues to provide ongoing service and maintenance.

- October 2025: Angkasa Pura Supports launched an Integrated Facility Management System. PT Angkasa Pura Supports unveiled a unified FMS platform combining e-cleaning, e-maintenance, e-patrol, parking management, manpower service, and ATM care into a single digital ecosystem, repositioning the company as a domestic technology-driven IFM provider capable of competing with global platforms.

Indonesia Integrated Facility Management Market Report Scope

The Indonesia Integrated Facility Management Market Report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, Fire Systems and Safety, and Other Hard Facility Management Services], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and Other Soft Facility Management Services]), End User (Commercial (includes BFSI, IT and Telecom, Retail and Warehouses, etc.), Hospitality (includes Eateries, Restaurants and Large-Scale Hotels), Institutional and Public Infrastructure (includes Government Establishments, Education, Transportation such as Airports and Railways, etc.), Healthcare (includes Public and Private Healthcare Facilities), Industrial and Process Sector (includes Manufacturing, Energy including Oil and Gas Exploration, Mining, etc.), and Other End-User Industries (Multi-House Residential, Entertainment, Sports and Leisure)). The Market Forecasts are Provided in Terms of Value (USD).

| Hard Facility Management | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Facility Management | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process Sector |

| Other End-User Industries |

| By Service Type | Hard Facility Management | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Facility Management | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By End User Industry | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process Sector | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

What is the current size of Indonesia integrated facility management?

The Indonesia integrated facility management market was valued at USD 1.89 billion in 2025 and is projected to reach USD 2.44 billion by 2031 at a 4.4% CAGR over 2026-2031.

Which service category leads revenue in Indonesia?

Soft FM led with 61.6% share in 2025, supported by strong demand for cleaning, security, office support, and other labor-intensive workplace services.

Which service category is growing the fastest through 2031?

Hard FM is forecast to grow at 5.1% CAGR through 2031 as smart building rules, AC efficiency upgrades, and compliance needs push more technical outsourcing.

Which end-user group contributes the most demand?

The industrial and process sector held the largest share at 27.8% in 2025, backed by mining, power, remote-site operations, and other continuous-service environments.

Why is commercial demand rising so quickly?

Commercial is the fastest-growing end-user segment at 4.9% CAGR through 2031 because occupiers increasingly prefer professionally managed buildings, data centers, logistics assets, and high-spec healthcare facilities.

What are the main factors limiting expansion across the country?

The main constraints are shortages of skilled technicians, fragmented procurement channels, slower technology adoption among smaller owners, labour cost rigidity, and the operational complexity of serving sites across more than 17,000 island

Page last updated on: