Asia-Pacific Integrated Facility Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

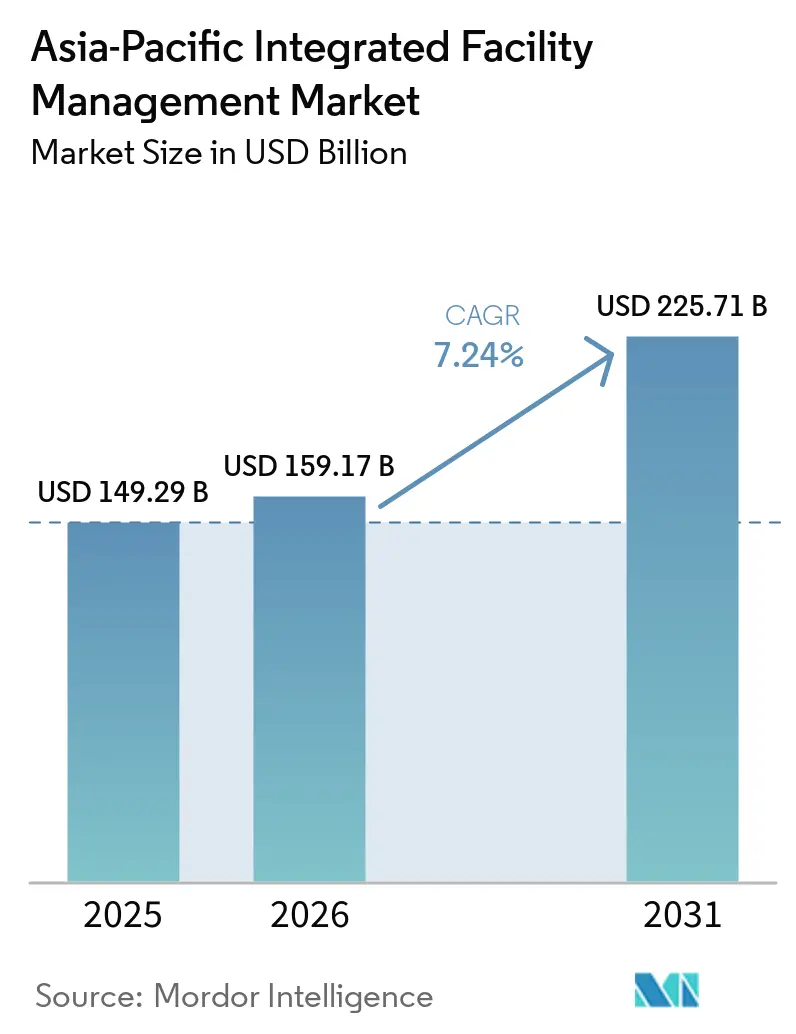

| Base Year Market Size (2025) | USD 149.29 Billion |

| Market Size (2026) | USD 159.17 Billion |

| Market Size (2031) | USD 225.71 Billion |

| Growth Rate (2026 - 2031) | 7.24% CAGR |

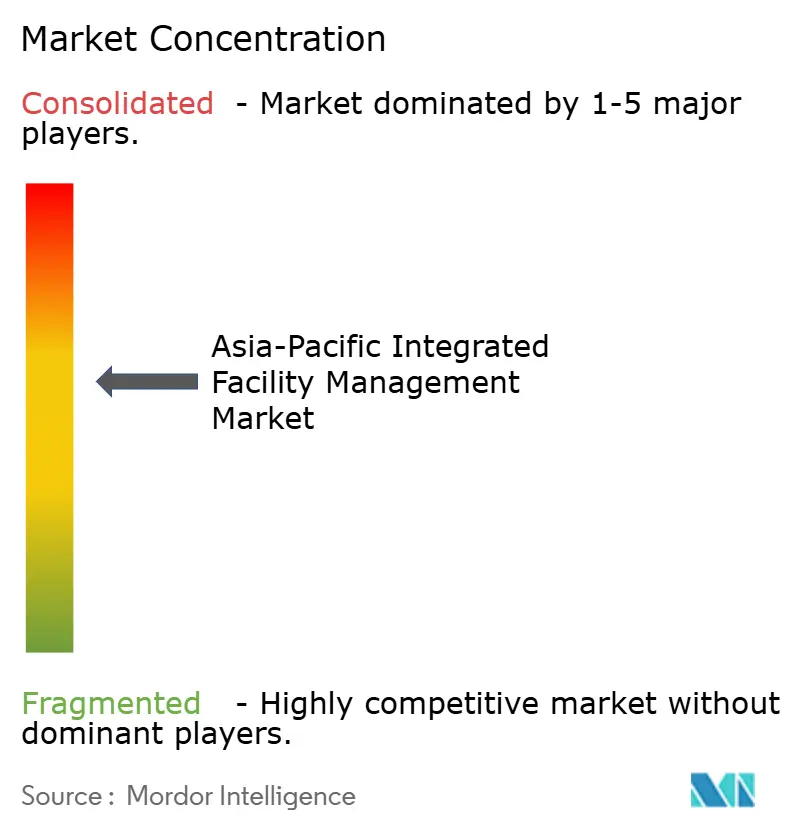

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Integrated Facility Management Market Analysis by Mordor Intelligence

The Asia-Pacific Integrated Facility Management market size is expected to grow from USD 149.29 billion in 2025 to USD 159.17 billion in 2026 and is forecast to reach USD 225.71 billion by 2031 at 7.24% CAGR over 2026-2031. The Asia-Pacific integrated facility management (IFM) market is expanding because corporate occupiers, governments, and institutional asset owners are treating facility operations as a performance function instead of a support cost. Energy regulation, portfolio digitalization, and post-pandemic real estate reconfiguration are moving contracts toward outcome-based delivery with stronger reporting and embedded technology. The Asia-Pacific IFM market also retains meaningful room for expansion in developing economies where outsourced facility management (FM) penetration remains below international practice, leaving space for providers with broad technical and service capabilities. Competition is separating into digitally enabled operators that can support predictive maintenance and live reporting, and traditional operators that still depend on manual delivery, while cyber exposure and labor shortages are adding pressure to margins in advanced markets. Carbon pricing is reinforcing this shift because measurable energy savings are making higher-specification contracts easier to justify and improving the position of providers with verifiable efficiency credentials.

Key Report Takeaways

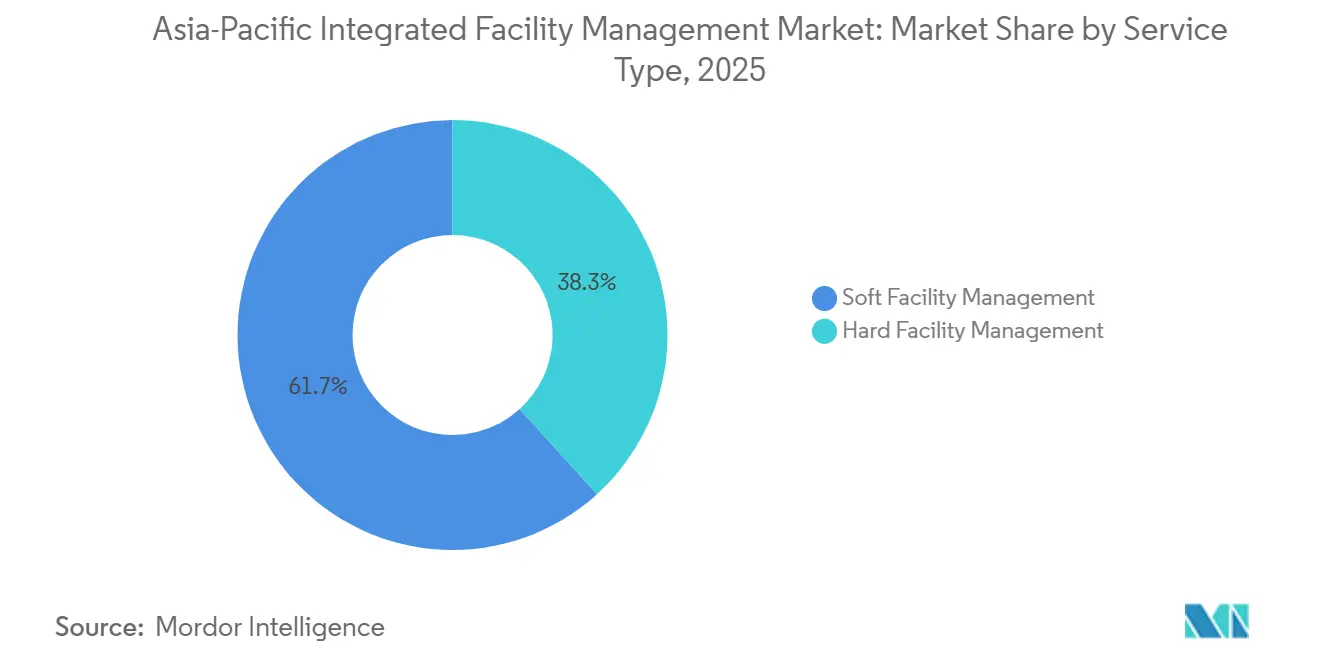

- By service type, Soft FM Services held 61.72% of the Asia-Pacific integrated facility management market share in 2025, while Hard FM Services is projected to advance at the fastest 7.74% CAGR through 2031.

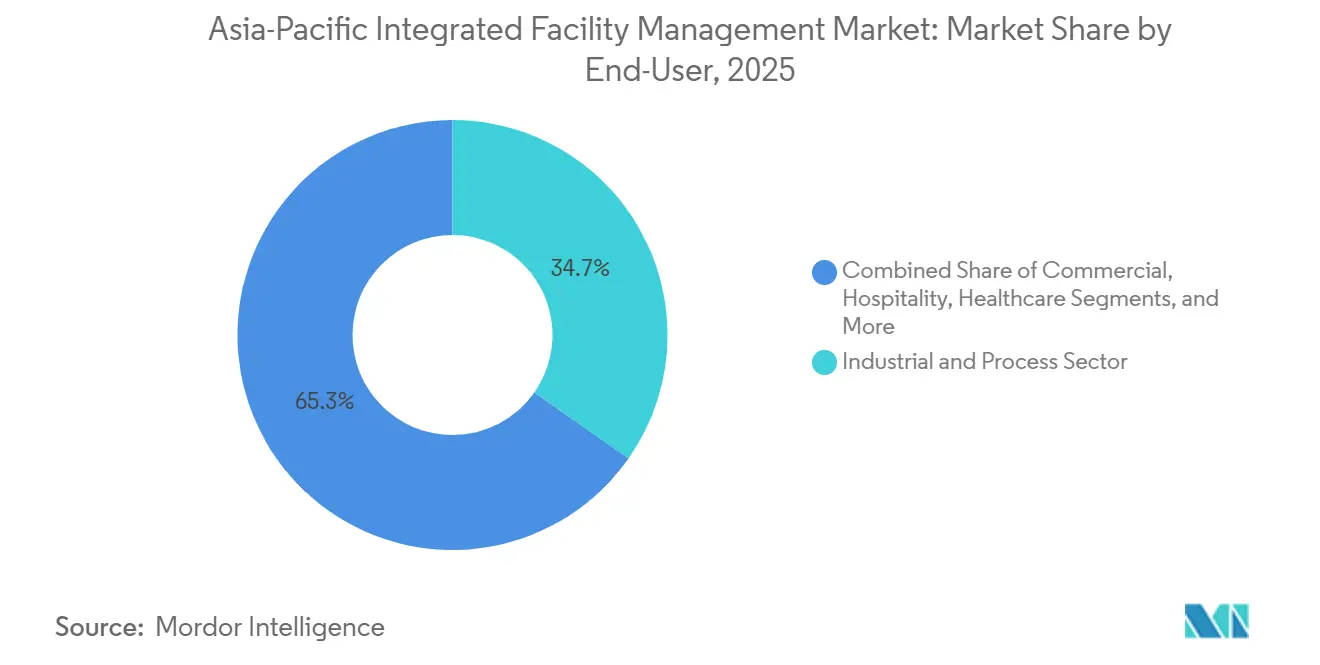

- By end user, the Industrial and Process Sector accounted for 34.73% share of the Asia-Pacific IFM market size in 2025, while Commercial is forecast to record the highest 7.64% CAGR through 2031.

- By geography, China represented 25.33% share of regional revenue of APAC IFM market in 2025, while India is set to post the fastest 8.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Integrated Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Adoption of IoT and Smart Building Technologies in Facility Management | +1.8% | Global, led by Singapore, Japan, South Korea, and Australia | Medium term (2-4 years) |

| Rising Demand for Energy Efficiency and Green Buildings Compliance | +1.5% | APAC core, Singapore, Australia, China, and Hong Kong, with spillover to Malaysia and India | Medium term (2-4 years) |

| Government Net-Zero Carbon Mandates Accelerating Retro-Commissioning Contracts | +1.0% | Singapore, Hong Kong, Australia, and New Zealand, with expansion into Malaysia and India | Long term (≥ 4 years) |

| Rapid Commercial Real Estate Growth in Tier 2 Asia-Pacific Cities | +0.9% | India, Vietnam, and Indonesia, with secondary gains in Malaysia and the Philippines | Short term (≤ 2 years) |

| Outsourcing Trend Among Multinational Corporations for Non-Core FM Functions | +0.8% | Global MNC hubs, Singapore, India, and Australia, with emerging demand in Vietnam and Indonesia | Short term (≤ 2 years) |

| Aging Building Stock Pushing Predictive Maintenance-As-A-Service Models | +0.6% | Japan, South Korea, and Australia, with early-stage activity in China Tier 1 cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Adoption of IoT and Smart Building Technologies in Facility Management

Connected building systems are moving from optional upgrades to routine operating tools in commercial portfolios across the APAC integrated facility management market.[1]Singapore Green Building Council, “Singapore Green Building Masterplan,” Singapore Green Building Council, www.sgbc.sg Singapore's Green Building Masterplan places strong emphasis on better building performance, which raises the value of integrated monitoring and service response in daily operations. The Building Control Act changes for existing buildings also make energy performance and plant efficiency more visible in operating decisions, which pushes owners to rely on data-rich FM models rather than manual rounds alone. Shanghai's 2025 green building rules add further momentum because higher baseline performance standards increase the importance of system integration from commissioning through operations.[2]Shanghai Municipal People's Government, “Shanghai Passes Green Building Regulations,” Shanghai Municipal People's Government, english.shanghai.gov.cn This is widening the commercial gap between providers that can connect sensors, asset data, and work orders in one workflow and providers that only offer task-based delivery. As adoption broadens, the Asia-Pacific integrated facility management market is likely to reward operators that can turn building data into faster service decisions, clearer compliance records, and more stable service quality.

Rising Demand For Energy Efficiency and Green Buildings Compliance

Energy efficiency has become a procurement requirement rather than a discretionary upgrade in much of the Asia-Pacific integrated facility management market. Singapore's Mandatory Energy Improvement regime for large energy-intensive buildings requires audits and measurable reductions in energy use intensity, which brings FM providers directly into compliance planning and execution. Shanghai now requires all new civilian buildings to meet at least a one-star green standard, while government and large public buildings must reach the highest three-star level. Hong Kong has broadened mandatory energy audits to 11 building types and shortened the audit cycle to 5 years, which raises the need for recurring technical review and follow-through. These rules favor providers that can combine maintenance, retro-commissioning, and digital reporting in one contract because owners need proof of operational improvement and not only service coverage. The result is a stronger bidding position for companies with certified energy management capabilities across the APAC integrated facility management market.

Government Net-Zero Carbon Mandates Accelerating Retro-Commissioning Contracts

Net-zero policies are creating a separate stream of retrofit and retro-commissioning work inside the Asia-Pacific IFM market. JLL's reappointment under the Whole of Australian Government property services arrangement in 2026 included a specific mandate to support Net Zero initiatives across 28 federal entities, which shows how public procurement is tying FM delivery to climate targets. The New Zealand Green Building Council also tightened its Green Star Buildings framework in 2026 by requiring a 15% upfront carbon reduction for projects that previously targeted 4-Star certification. These policy moves shift demand away from one-time corrective interventions and toward longer operating programs that track building performance over time. They also make contract renewal more defensible for incumbents that can document carbon, energy, and asset outcomes in a way owners can use for reporting. The Asia-Pacific integrated facility management market therefore gains support from net-zero frameworks that turn technical operations into part of a building owner's compliance pathway.

Rapid Commercial Real Estate Growth in Tier 2 Asia-Pacific Cities

Demand is no longer concentrated only in first-tier business districts, and the Asia-Pacific integrated facility management market is spreading into secondary cities as new office, logistics, and mixed-use assets come online. This matters because first-lease mandates in newer Grade-A buildings usually involve broader scopes, including technical maintenance, cleaning, security, and reporting from day 1. The opportunity is strongest where multinational occupiers and domestic developers are expanding together, since procurement standards rise quickly when new supply is backed by institutional capital. Secondary city growth also helps integrated providers enter accounts before service models are fragmented across multiple vendors. Over time, this can improve retention because early operators often become embedded in operating routines, compliance documentation, and site-level staffing structures. For the Asia-Pacific IFM market, the practical effect is a wider field of greenfield outsourcing opportunities beyond the region's most saturated urban cores.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Regulatory Codes Across Asia-Pacific Jurisdictions Increasing Compliance Costs | -0.8% | Global APAC, most acute in Southeast Asia, including Malaysia, Indonesia, Vietnam, and the Philippines | Long term (≥ 4 years) |

| Cybersecurity Vulnerabilities Arising From Connected Building Systems | -0.6% | Global, led by Singapore, Japan, South Korea, and Australia | Medium term (2-4 years) |

| Low Penetration of IFM in Small and Medium Enterprises Due to Cost Sensitivity | -0.5% | Southeast Asia and South Asia, particularly Indonesia, Vietnam, and India Tier 2+ | Short term (≤ 2 years) to Medium term (2-4 years) |

| Skilled Labor Shortages in Hybrid Hard-Soft FM Roles Post-Pandemic | -0.4% | Japan, Singapore, and Australia, with secondary impact in South Korea and New Zealand | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Regulatory Codes Across Asia-Pacific Jurisdictions Increasing Compliance Costs

Cross-border FM delivery remains difficult because APAC jurisdictions apply different rules for building energy performance, safety, audit cycles, and reporting. A provider serving Singapore, Australia, India, and Southeast Asia cannot rely on one compliance playbook, which raises overhead and slows standardization. Research on smart building adoption in Malaysia also identified the absence of specific legislation and policy frameworks as a major barrier, alongside data-sharing and ownership issues.[3]Nur Anisah Binti Tuwot and Wee Siaw-Chui, “Challenges to the Adoption of Smart Building Systems: A Property Management Perspective,” International Journal of Research and Innovation in Social Science, rsisinternational.org These frictions matter most in regional contracts where clients want consistency across sites but local operating rules force market-by-market customization. Local operators that stay within one jurisdiction often avoid part of this burden, which can make them look cheaper even when their scope is narrower. Until standards align further, the APAC IFM market will continue to face margin pressure from duplicated compliance work and uneven operating requirements.

Cybersecurity Vulnerabilities Arising From Connected Building Systems

Connected building systems are expanding the operational cyber risk carried by the Asia-Pacific integrated facility management market because HVAC, access control, lighting, and fire systems now share more digital touchpoints. The issue is not limited to data loss, since a building systems breach can also disrupt physical operations and create safety exposure for owners and service providers. Taiwan has already responded by promoting locally made smart building hardware in government settings to reduce infrastructure exposure and improve control over critical systems.[4]James Baron, “Smart Vision: Taiwan Leading in Intelligent Buildings,” Taiwan Business TOPICS, topics.amcham.com.tw This kind of response shows that cyber resilience is becoming part of building procurement and not only an IT concern. For FM providers, the commercial challenge is that clients want the efficiency benefits of connected systems but may hesitate to place all technical control under one vendor if liability boundaries remain unclear. That tension can slow full-service adoption in the most advanced part of the Asia-Pacific integrated facility management market even when digital tools improve maintenance quality and reporting.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Facility Management Services Accelerates as MEP Complexity Rises

Soft FM accounted for 61.72% of regional revenue in 2025, while Hard FM is set to expand at a 7.74% CAGR through 2031. Soft facility management services remained the larger pool because cleaning, security, office support, and catering are labor-intensive and widely outsourced across commercial, institutional, and public facilities. Even so, the balance is shifting because energy codes and equipment complexity are increasing the value of technical maintenance inside integrated contracts. Hard FM benefits directly from the growing stock of MEP-heavy assets, including data centers and life-sciences campuses, where uptime and compliance matter as much as routine service coverage. This is pushing the Asia-Pacific integrated facility management market toward contracts where engineering depth carries more pricing power than basic task execution.

The hard FM opportunity is also changing the revenue model because predictive maintenance and remote monitoring add recurring digital layers to what used to be scheduled or break-fix work. Singapore's periodic air-conditioning plant audit requirement and Hong Kong's broader audit scope both strengthen demand for providers that can interpret plant data and translate it into corrective action. Samsung Electronics' Factorial Seongsu building in South Korea showed how integrated building controls can support lower energy use and stronger smart building credentials, which reinforces the case for technically capable operators. In the integrated facility management industry, providers that combine field technicians, energy expertise, and building systems visibility are better positioned than pure soft-service vendors to capture the faster-growing side of the APAC integrated facility management market.

By End User: Industrial And Process Sector Anchors Demand While Commercial Accelerates

The Industrial and Process Sector represented 34.73% of regional demand in 2025, while Commercial is forecast to grow at the fastest 7.64% CAGR through 2031. Industrial facilities remain central to the Asia-Pacific integrated facility management market because manufacturing, mining, and energy sites need continuous asset upkeep, safety oversight, and tightly managed service environments. Sodexo's 2026 Rio Tinto contract in Australia's Pilbara shows how industrial mandates often combine accommodation, transport, catering, and facility maintenance under one long-duration arrangement. These contracts tend to be sticky because operators become embedded in remote site logistics, workforce services, and compliance routines. The commercial segment is growing faster because Grade-A offices, logistics assets, data centers, and multinational occupiers are expanding the need for single-provider service coordination.

Healthcare is also moving up the quality curve, with hygiene, uptime, and regulated environments pushing buyers toward broader integrated scopes. ISS's 2025 Southeast Asia healthcare renewal showed the scale and duration that public healthcare accounts can support in this part of the region. Institutional and public infrastructure demand remains steady because procurement cycles are long and service continuity is valued, as seen in Compass Group Australia's 25-year Melton Hospital partnership announced in 2024. Across the integrated facility management industry, this mix favors providers that can adjust delivery models by site criticality while still offering one operating framework across the APAC IFM market.

Geography Analysis

China held 25.33% of the Asia-Pacific integrated facility management market share in 2025, while India is projected to grow at 8.54% CAGR through 2031. China's scale still gives the region its broadest demand base because major commercial districts and industrial corridors both require large service networks. Shanghai's Green Building Regulations, effective in 2025, reinforce this demand by raising minimum green standards for new civilian buildings and higher thresholds for major public assets. That requirement supports providers that can manage energy performance, reporting, and technical upkeep in one delivery stack. India is the fastest-growing country position in the regional mix because commercial expansion, multinational build-outs, and infrastructure investment are widening the base for integrated outsourcing.

In the APAC IFM market, Japan's opportunity is different because the market is mature, buildings are older, and labor shortages make outsourced coordination more attractive. In Tokyo and other large urban centers, owners are giving more attention to retrofit economics as demolition costs and embodied carbon considerations rise. South Korea is adding momentum through smart building adoption, and Samsung Electronics' Factorial Seongsu project gives corporate occupiers a visible example of what integrated controls can deliver in operating performance. Australia and New Zealand remain among the most developed outsourcing environments in the region, with procurement models that place greater weight on outcomes and sustainability. JLL's 2026 reappointment under the Australian Government property services program shows how public clients are linking property services with Net Zero execution and long-term reporting duties.

The rest of Asia-Pacific, including Vietnam, Indonesia, Malaysia, the Philippines, and Thailand, remains the clearest outsourcing frontier for the APAC integrated facility management market. These countries still trail the most outsourced markets, yet procurement practices are shifting as multinational occupiers expect broader service bundles and stronger reporting discipline. Newer Grade-A offices, logistics parks, and mixed-use developments in these markets often start with broader outsourced scopes than legacy buildings, which helps integrated providers enter accounts early. Taken together, the region combines mature retrofit demand in advanced economies with first-generation outsourcing opportunities in emerging ones, which gives the Asia-Pacific IFM market a broad and differentiated growth base.

Competitive Landscape

The Asia-Pacific integrated facility management market is moderately concentrated at the top and still fragmented across the wider field, with global operators leading large enterprise mandates and domestic specialists holding depth in local accounts. Sodexo, ISS, CBRE, Cushman & Wakefield, and JLL remain prominent in regional enterprise and government work because they can package hard and soft services with governance, reporting, and digital tools. Domestic groups such as Aeon Delight, NIPPON KANZAI, Bluspring Enterprises, and Ventia continue to matter because local compliance knowledge and labor networks still shape execution quality. This creates a competitive split inside the Asia-Pacific integrated facility management market between scale providers that sell integrated platforms and local operators that compete on proximity, staffing, and jurisdiction knowledge. The result is not a winner-take-all structure, but a market where contract type and client sophistication strongly influence who can compete.

Strategic moves in 2025 and 2026 show that leading providers are using contract renewals to deepen capability positions rather than only add volume. ISS extended a major global integrated facilities services contract in 2026, which underlined the strength of incumbency when service delivery is tied closely to client operating systems. Cushman & Wakefield also renewed its global agreement with BHP in 2025 and aligned the scope with BHP's Workplace Digital and AI Roadmap, which shows how workplace technology is becoming part of FM value creation. JLL's reappointment for Australian Government property services added a clear Net Zero mandate, which demonstrates how sustainability execution is now embedded in large public-sector contracts. These examples suggest that the Asia-Pacific integrated facility management market rewards providers that can connect service operations with digital, workplace, and decarbonization agendas.

White-space opportunities remain strongest in healthcare, life sciences, data centers, and public infrastructure because these environments place a premium on reliability, auditability, and specialized technical knowledge. Procurement standards such as ISO 41001, ISO 45001, and ISO 14001 are also raising entry barriers by making formal systems and certified processes more important in bid evaluation. That trend narrows the room for informal price competition and supports larger providers when clients need one accountable operator across several service lines. At the same time, the long tail of smaller local providers means the APAC integrated facility management market still offers room for consolidation, partnership models, and specialist niche plays.

Asia-Pacific Integrated Facility Management Industry Leaders

CBRE Group, Inc.

Jones Lang LaSalle Incorporated

Sodexo SA

ISS A/S

Compass Group PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Sodexo SA was awarded a seven-year contract, with a three-year extension option, to manage Rio Tinto's Pilbara fly-in fly-out accommodation villages, operational sites, and community facilities in Western Australia. The agreement covers approximately 19,000 FIFO rooms across 25 villages and around 2,900 residential houses, with a strong Indigenous employment and local procurement commitment, supporting approximately 2,500 Sodexo roles in the Pilbara region.

- March 2026: ISS A/S extended its Integrated Facilities Services contract with a large global customer for two years, effective Q3 2027, at an annual contract value exceeding DKK 700 million (USD 109 million). The agreement encompasses cleaning, catering, technical and building maintenance, engineering, and workplace experience services delivered globally, including across ISS's APAC operations spanning Australia, China, Hong Kong, India, Indonesia, Japan, Malaysia, New Zealand, and Singapore.

- February 2026: JLL was reappointed as a property service provider under the Whole of Australian Government Property Services Coordinated Procurement Arrangements, a five-year contract covering 28 Federal Government entities, with a specific mandate to drive Net Zero initiatives across managed property portfolios. JLL has maintained a 25-year relationship with the Australian Government.

- February 2026: JLL secured a six-year contract with the Australian Department of Defence to provide National Program Services for the Defence Estate Works Program, managing and coordinating estate projects across Defence's extensive portfolio and using integrated digital platforms for risk management and investment prioritization.

- January 2026: ISS A/S signed a six-year contract with the Australian Department of Defence, valued at approximately DKK 300 million (USd 46.7 million) annually, to deliver integrated facility services, including accommodation management, cleaning, catering, and technical services, across 85 Defence locations in South Australia and Western Australia.

Asia-Pacific Integrated Facility Management Market Report Scope

The Asia-Pacific Integrated Facility Management Market Report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, Fire Systems and Safety, and Other Hard Facility Management Services], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and Other Soft Facility Management Services]), End User (Commercial (includes BFSI, IT and Telecom, Retail and Warehouses, etc.), Hospitality (includes Eateries, Restaurants and Large-Scale Hotels),Institutional and Public Infrastructure (includes Government Establishments, Education, Transportation such as Airports and Railways, etc.), Healthcare (includes Public and Private Healthcare Facilities), Industrial and Process Sector (includes Manufacturing, Energy including Oil and Gas Exploration, Mining, etc.), and Other End-User Industries (Multi-House Residential, Entertainment, Sports and Leisure)), and Geography (China, Japan, India, South Korea, Australia, NewZealand, and Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

| Hard Facility Management | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft Facility Management | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management Services |

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process Sector |

| Other End-User Industries |

| China |

| Japan |

| India |

| South Korea |

| Australia |

| New Zealand |

| Rest of Asia-Pacific |

| By Service Type | Hard Facility Management | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft Facility Management | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management Services | ||

| By End User | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process Sector | ||

| Other End-User Industries | ||

| By Geography | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

What is the 2026 size of the Asia-Pacific integrated facility management market?

The market stands at USD 159.17 billion in 2026 and is projected to reach USD 225.71 billion by 2031 at a 7.2% CAGR.

Which service type is growing fastest across Asia-Pacific integrated facility management?

Hard FM is the fastest-growing service type, with a projected 7.74% CAGR through 2031, supported by rising MEP complexity and energy compliance needs.

Which end-user group generates the most demand in this region?

The Industrial and Process Sector led demand in 2025 with a 34.73% share, supported by the scale and maintenance intensity of manufacturing, mining, and energy assets.

Which country is expanding fastest in this regional landscape?

India is the fastest-growing country market, with an expected 8.5% CAGR through 2031, supported by commercial development, multinational expansion, and infrastructure investment.

Why are energy regulations becoming so important for facility management providers?

Energy audits, building efficiency rules, and net-zero mandates are pushing owners to buy contracts that include technical maintenance, compliance reporting, and measurable performance improvements.

What is shaping competition among major providers in Asia-Pacific integrated facility management?

Large contracts increasingly favor operators that combine digital platforms, sustainability execution, and multi-service delivery, while local specialists still compete strongly on compliance knowledge and staffing reach.

Page last updated on: