Thailand Integrated Facility Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

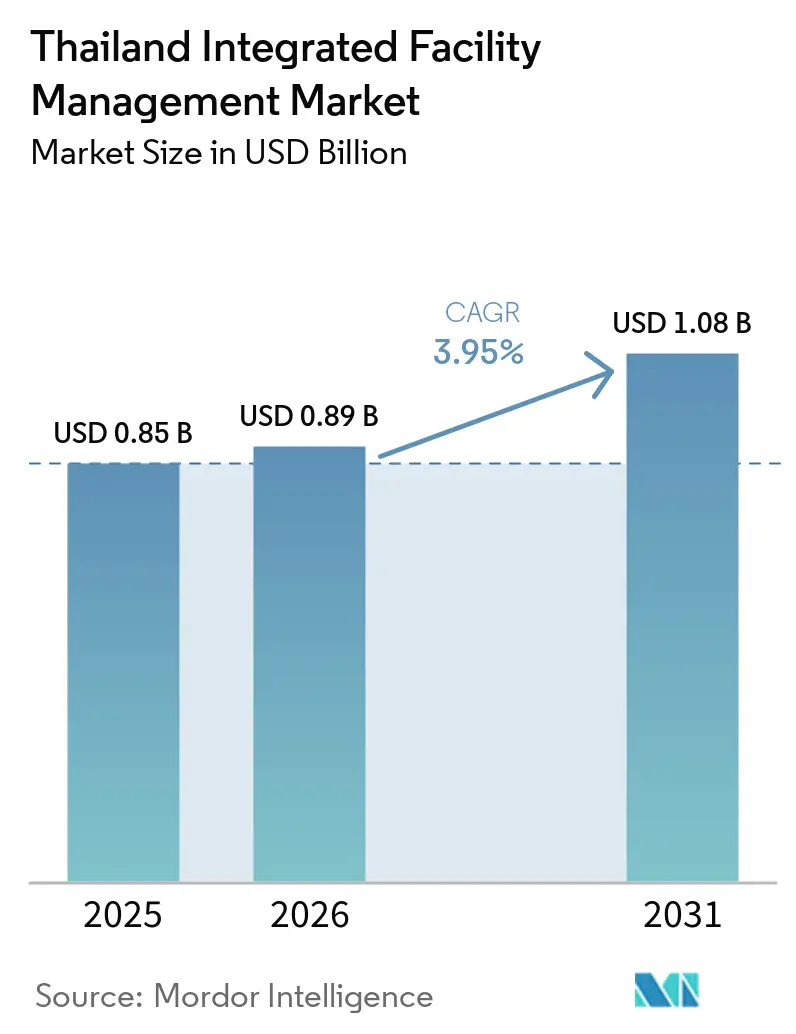

| Base Year Market Size (2025) | USD 0.85 Billion |

| Market Size (2026) | USD 0.89 Billion |

| Market Size (2031) | USD 1.08 Billion |

| Growth Rate (2026 - 2031) | 3.95% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Integrated Facility Management Market Analysis by Mordor Intelligence

The Thailand Integrated Facility Management Market size is projected to expand from USD 0.85 billion in 2025 and USD 0.89 billion in 2026 to USD 1.08 billion by 2031, registering a CAGR of 3.95% between 2026 to 2031.

The Thailand integrated facility management (IFM) market is moving toward performance-led contracts as buyers place more weight on technical capability, compliance delivery, and service continuity than on low-cost outsourcing alone. Foreign direct investment into the Eastern Economic Corridor is widening the pipeline of factories, logistics assets, and digital infrastructure projects that need stronger technical support and longer contract coverage. The building energy code is also changing service scope because commercial building owners now need operators that can support audits, optimization work, and measurable energy outcomes across large assets. Certification standards, especially ISO 41001, are raising the entry barrier in public tenders and large multinational accounts, which is pushing procurement toward a smaller group of proven operators. At the same time, labour shortages in technical roles are making delivery quality, training depth, and automation capability more important in the Thailand IFM market.

Key Report Takeaways

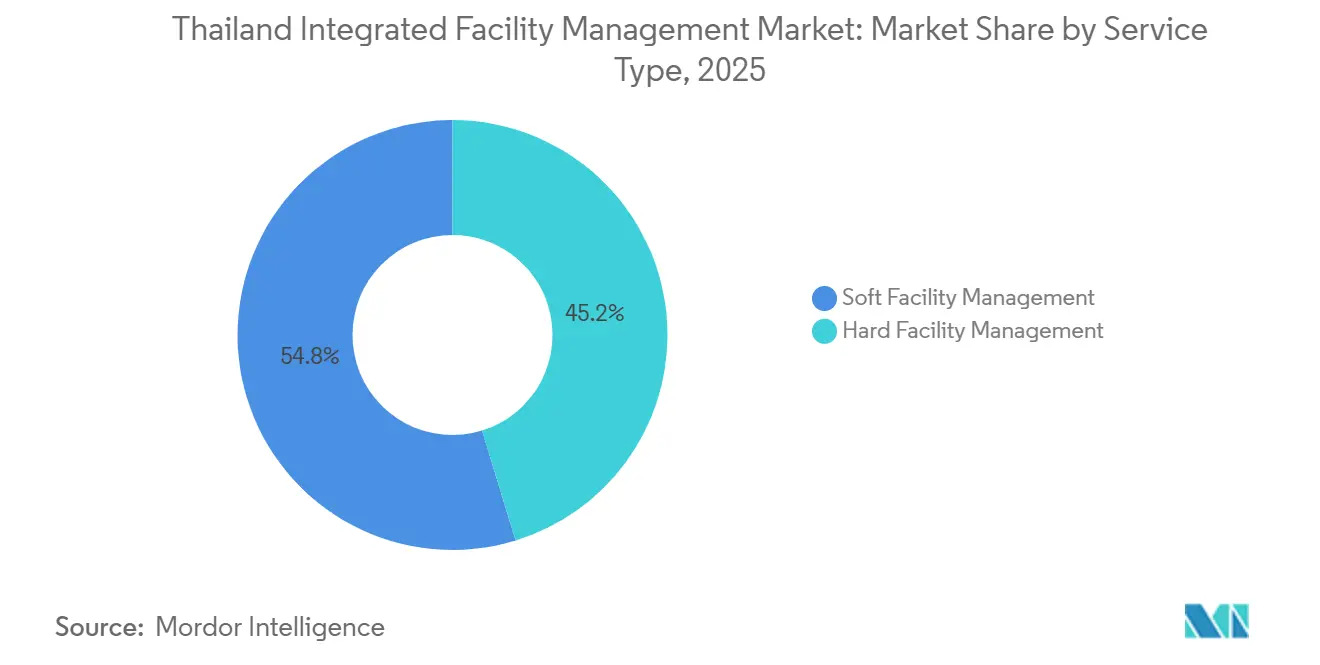

- By service type, soft facility management held 54.76% of the Thailand integrated facility management market share in 2025, while hard FM is forecast to expand at a 4.62% CAGR through 2031.

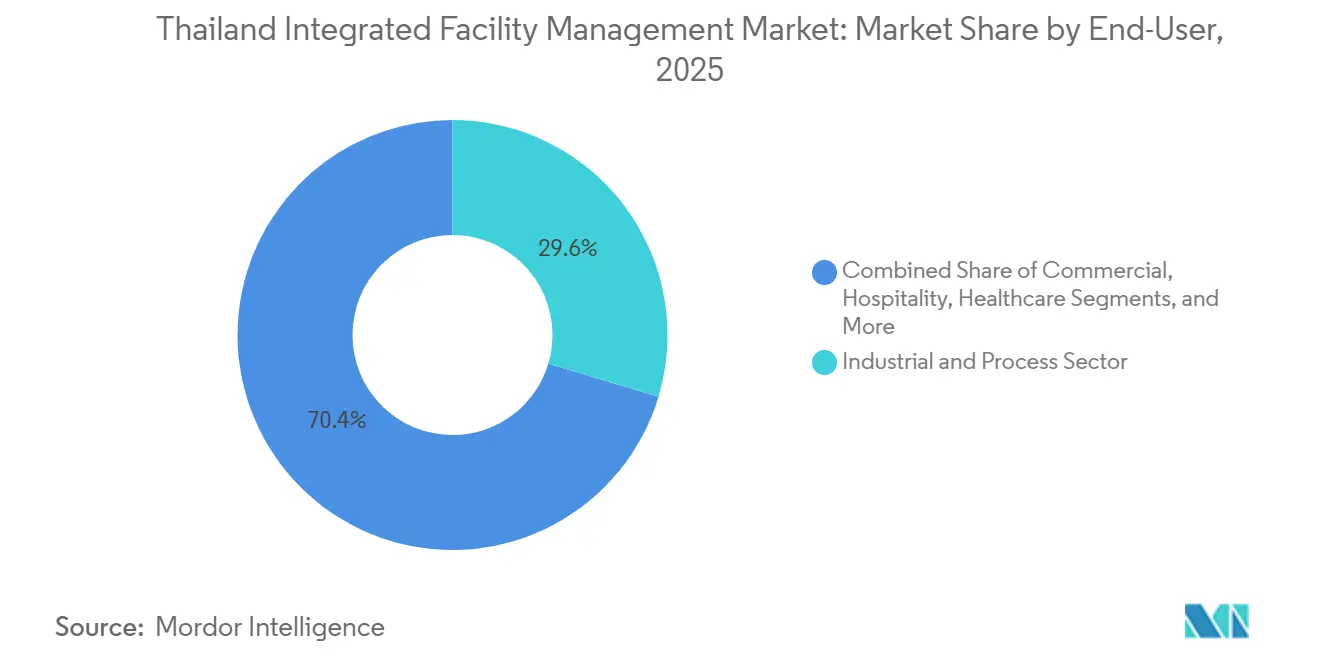

- By end-user, the industrial and process sector accounted for 29.63% of the Thailand integrated facility management (IFM) market size in 2025, while the commercial sector is projected to grow at a 4.81% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Thailand Integrated Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Investment in Eastern Economic Corridor Industry Parks | +1.0% | National, concentrated in Chonburi, Rayong, and Chachoengsao | Medium term (2-4 years) |

| Government Mandates on Commercial Buildings for Energy Efficiency | +0.8% | National, with early gains in the Bangkok metropolitan area | Short term (≤ 2 years) |

| Expansion of Special Economic Zones | +0.6% | National, with key zones including Tak, Sa Kaeo, Songkhla, and Mukdahan | Medium term (2-4 years) |

| Mandatory ISO 41001 Adoption in Public Sectors | +0.4% | National | Short term (≤ 2 years) |

| Thailand Industrial Property Clustering and Industry City Development | +0.3% | EEC provinces and Greater Bangkok | Medium term (2-4 years) |

| Rising FDI-Driven Corporate Campus and Digital Infrastructure Investments | +0.2% | National, with spillover to the EEC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Investment in Eastern Economic Corridor Industry Parks Drives Integrated FM Demand

The EEC remains the clearest demand engine for the Thailand integrated facility management market because it concentrates large industrial estates, transport links, and new infrastructure within a relatively compact operating corridor.[1]Eastern Economic Corridor Office, “Eastern Economic Corridor (EEC) Overall Development Plan,” Eastern Economic Corridor Office, eeco.or.th Its 2023-2027 development plan targets THB 500 billion (USD 14.5 billion) in actual investment, while developed industrial land in the EEC reached 110,275 rai by H1 2025, up 7% from the end of 2024. That scale matters because multi-tenant estates need providers that can coordinate engineering, security, cleaning, compliance, and reporting across many buildings instead of serving a single site at a time. U-Tapao Airport’s Eastern Aviation City, Laem Chabang Port Phase 3, and the high-speed rail link are creating permanent facilities where MEP upkeep, fire systems, and building management systems become core service lines rather than optional add-ons. In May 2025, Prospect Development announced THB 6.5 billion (USD 188.4 million), equivalent to USD 188.4 million, for the Bangpakong Industrial Estate in the EEC, aimed at automotive, digital, and food processing users that require stronger technical operating support. As those facilities move from construction into steady operations, the Thailand integrated facility management (IFM) market gains a more durable stream of contracts tied to uptime, compliance, and asset performance rather than one-time support work.

Government Mandates on Commercial Buildings for Energy Efficiency Reshape FM Service Scope

Thailand’s Building Energy Code, issued under ministerial regulation B.E. 2563 pursuant to the Energy Conservation Act B.E. 2535, applies energy-saving requirements to new or significantly modified buildings above 2,000 sq m and has been fully enforced since March 2023.[2]Department of Alternative Energy Development and Efficiency, “Building Energy Code (BEC) - Requirements of the Law,” Department of Alternative Energy Development and Efficiency, bec.dede.go.th The code covers six systems, including building envelope, lighting, air-conditioning, hot water, overall energy consumption, and renewable energy, which has widened the technical scope that owners now expect from FM partners. DEDE’s Energy Efficiency Plan targets a 30% reduction in Thailand’s energy intensity by 2037, and the building sector carries a 1,574-ktoe electricity demand reduction target within that plan. This changes procurement in the Thailand IFM market because energy auditing, BMS optimization, and performance reporting now sit closer to the center of contract design, especially for larger commercial assets. Bangkok Metropolitan Administration reinforced that direction in December 2025 through an energy conservation training program for 74 government officials under the Bangkok Energy Action Plan 2024-2030, extending operating scrutiny across public buildings in the capital. As a result, the Thailand integrated facility management market is seeing stronger demand for operators that can demonstrate measurable savings, documented procedures, and credible technical supervision in day-to-day building operations.

Expansion Of Special Economic Zones Broadens Market Reach Beyond Core Cities

Thailand’s 10 Special Border Economic Zones had attracted THB 55.2 billion (USD 1.6 billion), in cumulative private and industrial estate investment by late 2025, while infrastructure completion averaged 90% across the zones. Royal Decree No. 797, effective June 6, 2025, lowered corporate income tax to 10% for BOI-designated businesses operating within SEZs for 10 consecutive accounting periods, materially improving the operating case for manufacturers and logistics tenants. This is important for the Thailand integrated facility management (IFM) market because it draws organized operations into provinces that were historically served by smaller and less formal service networks. Once SEZ tenants move beyond commissioning and enter routine operations, their needs shift toward recurring contracts for warehousing support, technical maintenance, security, cleaning, and compliance coordination across larger footprints. Songkhla and Sa Kaeo stand out because Songkhla’s Phase 1 industrial estate reached 69% operational occupancy and Sa Kaeo completed customs infrastructure supporting border logistics and manufacturing activity. That gradual geographic spread gives the Thailand IFM market a broader demand base, while favouring providers with provincial delivery capacity, local labour access, and the ability to standardize service quality outside Bangkok.

Mandatory ISO 41001 Adoption Elevates Contract Standards and Favors Certified Operators

ISO 41001:2018 is the only certifiable international facility management standard, and it is gaining traction in Thailand as a practical filter in structured procurement. OCS Thailand, part of IFS Group, became the first FM company in Thailand to achieve ISO 41001 certification in March 2024, which moved the standard from a niche differentiator to a recognized benchmark for serious buyers. CBRE Thailand later confirmed the same certification within a broader service model that also references LEED and TREES-aligned building practices.[3]Phatsareephak Srikanchananon, “A Smarter, Sustainable Approach to Property Management in Thailand,” CBRE Thailand, cbre.co.th The standard matters in the Thailand integrated facility management market because it focuses on governance, risk control, service continuity, and performance review, all of which are central concerns in public buildings and multinational operating sites. As more tenders require documented systems instead of basic manpower deployment, smaller operators without certification face a higher risk of exclusion from large accounts. This is gradually consolidating the upper tier of the Thailand integrated facility management (IFM) market around firms that can combine certification, training systems, and measurable operating controls.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled Labor Shortage in Technical FM Roles | -0.6% | National, most acute in EEC industrial zones and Bangkok CBD | Medium term (2-4 years) |

| Fragmented Regulatory Oversight Across Multiple Agencies | -0.4% | National | Long term (≥ 4 years) |

| High Competition from Price-Focused Staffing Outlets | -0.3% | National, most acute in soft FM segments | Short term (≤ 2 years) |

| Consolidation Gaps Between Traditional IFM Contracts and Legacy Facility Structures | -0.2% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Skilled Labor Shortage in Technical FM Roles Constrains Hard FM Expansion

Thailand’s labour challenge is structural, making it a deeper restraint on the Thailand IFM market than a short-term hiring cycle would suggest. The country’s total fertility rate fell to 1.16 in 2023, it entered ageing-society status in the same year, and it is projected to become a super-ageing society by 2036. NESDC projects labour demand of 44.71 million by 2037 against a working-age population of 40.7 million, creating a gap likely to affect technical and mid-skilled roles most severely. The pressure is especially acute in MEP engineering, HVAC servicing, and BMS operations because these functions sit inside the fastest-growing parts of the Thailand integrated facility management market and cannot easily be filled with general labour. JLL noted that 40% of FM professionals in high-income countries are expected to retire by 2026 and that 56% of organizations plan to use predictive maintenance technologies, yet Thailand still faces weak digital readiness, with 74.1% of youth lacking foundational digital skills and only 5% of industries having adopted Industry 4.0 by 2024. Unless operators accelerate training and automation, the Thailand integrated facility management (IFM) market will continue to experience margin pressure, uneven service quality, and slower capacity build-out in technical accounts.

Fragmented Regulatory Oversight Creates Compliance Friction Across Portfolios

The Thailand integrated facility management market operates across overlapping requirements from energy authorities, construction regulators, industrial estate administrators, and EEC-related approvals, which complicates service delivery for providers managing mixed portfolios. This matters most for operators handling commercial buildings, factories, and public assets under one contract because inspection cycles, reporting formats, and operating obligations do not align under a unified system. The absence of a national FM licensing framework also makes client due diligence more difficult, especially in the mid-market where procurement teams have fewer internal resources to evaluate provider capability. That gap allows lower-quality entrants to compete on price before buyers can fully assess technical depth, compliance discipline, or service continuity systems. In the Thailand IFM market, this creates procurement friction that slows contract closure and makes standardization harder across national accounts. Until oversight becomes more coordinated, larger providers with stronger internal compliance teams are likely to maintain an advantage over smaller firms that struggle to navigate multiple agencies simultaneously.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Soft FM Leads While Hard FM Gains from Technical Demand

Soft facility management (FM) held 54.76% of the market in 2025, giving it the largest role in the Thailand integrated facility management (IFM) market and reflecting the broad installed base of commercial buildings, industrial estates, retail centers, and hospitality assets that need daily support. Cleaning, security, landscaping, and other support services remained central because they are required across asset classes and are easier to bundle into recurring contracts than specialized engineering work. Security services and cleaning or housekeeping were the two largest soft FM sub-segments, which explains why labour scale and route density still matter for winning high-volume accounts. Sodexo Amata Services, which serves more than 95 corporate clients in EEC industrial estates, demonstrates how multi-tenant parks convert routine service lines into long-running integrated mandates with steady renewal potential. Landscaping is also becoming more structured in premium projects because One Bangkok includes 108 rai of development area and 50 rai of managed green space, increasing coordination among grounds teams, common-area maintenance, and broader site operations.

Hard FM is the fastest-growing service type in the Thailand IFM market, with a 4.62% CAGR through 2031, as newer facilities require greater engineering oversight and faster response times. Thailand’s data center service revenue is projected at THB 14.2 billion (USD 411.6 million), in 2026, up 9% from 2025, signalling a larger installed base of technically intensive sites that need constant monitoring and uptime support. These facilities require continuous MEP supervision, precision cooling control, and fire suppression compliance, making them difficult to serve with a low-skill staffing model. BOI approvals for 18 data center projects worth THB 389.14 billion (USD 11.3 billion), in H1 2025 suggest that the Thailand integrated facility management industry will continue shifting toward contracts with higher technical intensity and stronger 24/7 service expectations. As those assets move into full operation, hard FM will continue raising the quality threshold and renewal logic across the Thailand integrated facility management market.

By End-User: Industrial And Manufacturing Anchors Demand While Commercial Advances Faster

Industrial and manufacturing accounted for 29.63% of the Thailand integrated facility management market size in 2025, making it the largest end-user base and tying market demand closely to Thailand’s role as a regional production hub. Automotive, electronics, food processing, and pharmaceuticals all require organized site operations, supporting larger bundled contracts than many smaller building categories can support. The China+1 relocation pattern strengthened that position during 2024 and 2025, when BOI approved 959 projects worth THB 647.65 billion (USD 18.8 billion), in H1 2025 alone. In industrial estates, contracts often run for longer durations and include MEP maintenance, clean-room upkeep, waste handling, site security, and contractor coordination, which gives providers a stable revenue base once accounts are secured. Sodexo Amata’s long-standing presence in Amata City Chonburi and Amata City Rayong, serving more than 95 corporate clients across food, engineering, security, and cleaning services, illustrates the operational depth that leading estates now expect from the Thailand integrated facility management industry.

Commercial is the fastest-growing end-user in the Thailand IFM, with a 4.81% CAGR through 2031, supported by Grade A office launches, mixed-use districts, and retail expansion beyond Bangkok’s core business zones. JLL managed 7.5 million sq m of property in 2024, with offices accounting for 80% of that total, demonstrating how central commercial buildings remain to premium FM delivery in Thailand. Mixed-use projects such as One Bangkok are also broadening the operating brief because they combine offices, retail, open space, and public areas within a single managed environment. Residential FM is expanding alongside Bangkok’s luxury and serviced-apartment pipeline, and CBRE Thailand’s partnership with the Nai Lert Butler Academy shows that service expectations are moving closer to hospitality standards in higher-end assets. Healthcare is gaining attention because Thailand’s medical service position supports institutional expansion, while government and public-sector accounts remain important in volume terms despite tighter pricing pressure and closer compliance review.

Geography Analysis

Geographic market shares were not disclosed, but Bangkok and the wider metropolitan area remained the main center for premium contracts in the Thailand IFM market because the capital concentrates Grade A offices, mixed-use developments, hospitality assets, and public buildings. The city also remains at the forefront of compliance-led service demand, as the building energy code and related public-sector initiatives increase the need for measurable energy performance in larger buildings. This has helped Bangkok become the strongest location for ISO-led procurement, technology-enabled monitoring, and bundled commercial mandates that require more than labour deployment alone. One Bangkok adds to that concentration because it raises expectations for district-wide coordination across offices, shared spaces, green areas, and tenant services. For the Thailand IFM market, Bangkok therefore remains the leading arena for premium differentiation, service innovation, and renewal-based competition rather than simple price bidding.

The fastest rise in technical contract complexity is taking place in Chonburi, Rayong, and Chachoengsao, where the EEC continues to concentrate industrial estates, logistics capacity, and infrastructure investment. Developed industrial land reached 110,275 rai in the EEC by H1 2025, and that land base supports a broad mix of factories, warehouses, and support buildings that need integrated operating models. Sodexo Amata’s command-center-based model in Amata City Chonburi and Amata City Rayong demonstrates how service delivery in the corridor is moving toward multi-site coordination and round-the-clock monitoring. In practical terms, the EEC provides the Thailand integrated facility management market with its deepest pool of industrial demand and its strongest runway for hard FM expansion.

Outside Bangkok and the EEC, the Thailand integrated facility management market is extending into Songkhla, Sa Kaeo, Tak, and Mukdahan as SEZ development lifts logistics and manufacturing activity in border locations. Songkhla’s operational occupancy and Sa Kaeo’s completed customs infrastructure already show that these zones are moving from policy intent into functioning industrial and logistics platforms. That transition matters because FM demand in these provinces starts with basic operational coverage and can mature into integrated contracts once tenant density and compliance needs increase. Over time, this wider footprint should make the Thailand integrated facility management market less concentrated in Bangkok alone, while still favouring operators that can maintain service consistency across provincial and urban sites.

Competitive Landscape

The Thailand integrated facility management market is moderately fragmented, with multinational firms strongest in premium commercial and industrial mandates and domestic players retaining large volumes in soft FM and mid-market contracts. JLL Thailand and CBRE Thailand anchor the upper tier, as JLL managed 7.5 million sq m in 2024 and held more than 50% share in Bangkok’s prime office management segment, while CBRE Thailand’s 2026 platform manages 2.9 million sq m with more than 700 property management professionals. IFS Group remains the leading domestic full-service platform, with more than 30,000 employees, THB 7 billion (USD 203 million), in annual revenue, and multiple operating certifications supporting work across aviation, pharmaceuticals, and public administration. G4S Thailand also retains meaningful scale in integrated security-plus-FM work, supported by more than 18,000 staff and more than 40 years of operations in the country. This structure keeps the Thailand integrated facility management market competitive, while creating a clear divide between premium integrated contracts and high-volume labour-led accounts.

Certification and operating systems are becoming stronger competitive filters in the Thailand integrated facility management market because large buyers now require documented governance, continuity planning, and measurable service outcomes. OCS Thailand’s ISO 41001 certification in 2024 and CBRE Thailand’s later adoption of the same standard demonstrate how quickly compliance credibility has moved into the core of procurement. JLL’s Command Centre role at One Bangkok and Sodexo Amata’s 24/7 command center in the EEC are clear examples of strategic initiatives that strengthen renewal potential by tying service delivery to real-time control and reporting rather than stand-alone manpower supply. CBRE Thailand’s partnership with the Nai Lert Butler Academy is another example because it links property management with service training aligned to higher-end commercial and residential expectations.

An important open opportunity in the Thailand integrated facility management market exists in the industrial mid-market, where factories, logistics parks, and data centers require stronger technical support than basic outsourcing can provide but may not fit the full pricing model of global operators. ISS World’s five-year APAC partnership expansion, valued at DKK 100 million (USD 14 million), points to the type of long-duration, multi-service contract structure that larger providers aim to replicate in stable client environments. Domestic operators still hold a structural advantage in many provincial accounts because they remain closer to local labour pools, local language requirements, and smaller site economics. That balance between premium multinational capability and local operating reach is likely to keep the Thailand integrated facility management market moderately fragmented even as certification, technology, and command-center models continue separating the top tier from the rest.

Thailand Integrated Facility Management Industry Leaders

CBRE Group, Inc.

Jones Lang LaSalle Incorporated

PCS Security and Facility Services Limited

ISS A/S

IFS Facility Services Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: The Eastern Economic Corridor Office conducted multiple investment roadshows in China, Belgium, and France focused on the EECiti smart city project, medical services, and BCG economy clusters. These initiatives are expected to accelerate foreign corporate campus establishment within the EEC, directly expanding the pipeline for long-term integrated FM contracts at new greenfield facilities.

- February 2026: IFS Group received the THAIHRM Best Workplace Award 2026 at Gold Level and was awarded Workplace Excellence Certification for 2026-2028, recognizing its human resource practices and workforce development programs across its 30,000-employee base in Thailand.

- January 2026: CBRE Thailand published its strategic vision for sustainable property management, confirming ISO 41001 certification and a formal partnership with the Nai Lert Butler Academy to deliver hospitality-grade service training to on-site FM teams across Bangkok and Phuket. The firm manages more than 2.9 million sq m with a team of more than 700 professionals, positioning it strongly for public-sector tenders that explicitly require ISO 41001 compliance.

- December 2025: Sodexo Amata Services celebrated its 10th anniversary in the EEC, highlighting major operational upgrades including the 24/7 Amata Command Center for security and fire alarm monitoring, solar energy programs, EV motorcycle fleet deployment, and carbon footprint tracking across its portfolio serving more than 95 corporate clients at Amata City Chonburi and Amata City Rayong.

Thailand Integrated Facility Management Market Report Scope

Thailand Integrated Facility Management Market Report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, Fire Systems and Safety, and Other Hard Facility Management Services], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and other Soft Facility Management Services]), End User (Commercial (includes BFSI, IT and Telecom, Retail and Warehouses, etc.), Hospitality (includes Eateries, Restaurants and Large-Scale Hotels), Institutional and Public Infrastructure (includes Government Establishments, Education, Transportation such as Airports and Railways, etc.), Healthcare (includes Public and Private Healthcare Facilities), Industrial and Process Sector (includes Manufacturing, Energy including Oil and Gas Exploration, Mining, etc.), and Other End-User Industries (Multi-House Residential, Entertainment, Sports and Leisure)). The Market Forecasts are Provided in Terms of Value (USD).

| Hard Facility Management | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft Facility Management | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management Services |

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process Sector |

| Other End-User Industries |

| By Service Type | Hard Facility Management | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft Facility Management | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management Services | ||

| By End User Industry | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process Sector | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

What is the forecast outlook for facility management in Thailand through 2031?

The Thailand integrated facility management market was valued at USD 0.85 billion in 2025 and is forecast to reach USD 1.08 billion by 2031, with a 3.95% CAGR during 2026-2031.

Which service category currently leads in Thailand?

Soft FM led in 2025 with a 54.76% share because cleaning, security, landscaping, and other support services are needed across commercial, industrial, hospitality, and mixed-use assets.

Which service category is expanding the fastest?

Hard FM is growing the fastest at a 4.62% CAGR through 2031 because data centers, advanced factories, and complex building systems require stronger MEP, HVAC, and BMS support.

Which end-user group contributes the most demand?

Industrial and manufacturing led with 29.63% of demand in 2025, supported by EEC growth, factory investment, and long-duration contracts tied to technical maintenance, waste handling, and site security.

Why are commercial buildings becoming more important for providers?

Commercial is the fastest-growing end-user at a 4.81% CAGR through 2031 as Grade A offices, mixed-use projects, and retail expansion raise demand for bundled, compliance-led, and experience-focused service models.

What is the main operating risk for providers in Thailand?

The biggest constraint is the shortage of skilled technical labor, especially in MEP, HVAC, and digital building operations, which raises delivery pressure just as contract complexity is increasing.

Page last updated on: