Ireland Integrated Facility Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

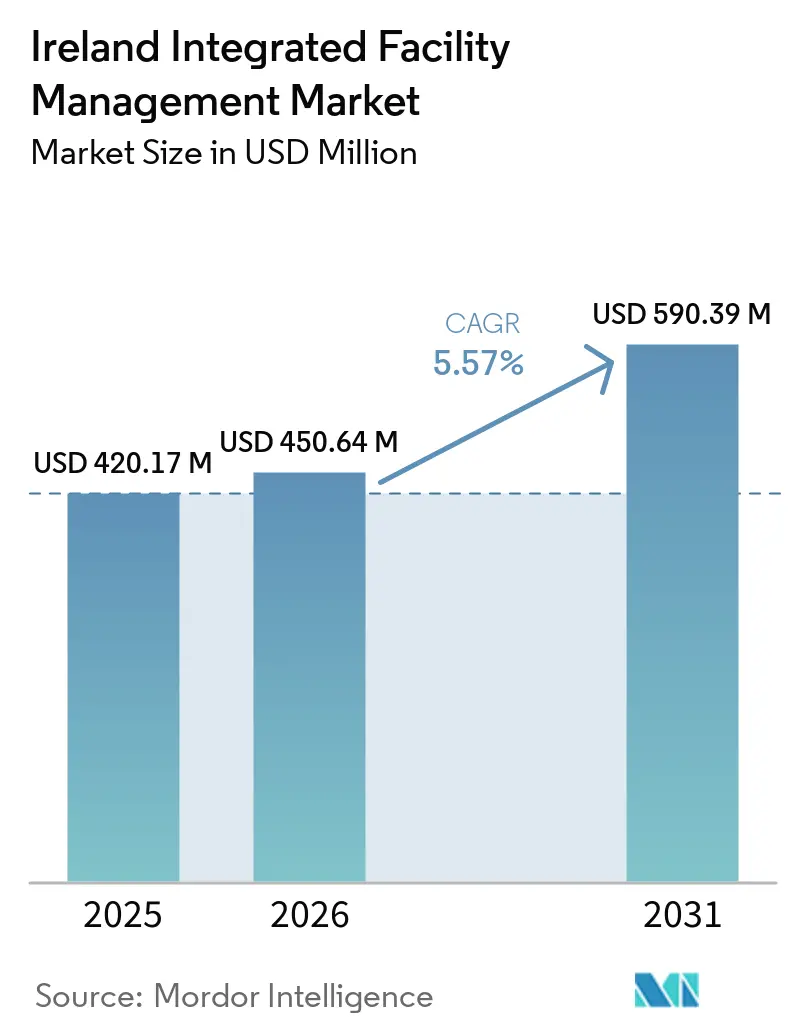

| Base Year Market Size (2025) | USD 420.17 Million |

| Market Size (2026) | USD 450.64 Million |

| Market Size (2031) | USD 590.39 Million |

| Growth Rate (2026 - 2031) | 5.57% CAGR |

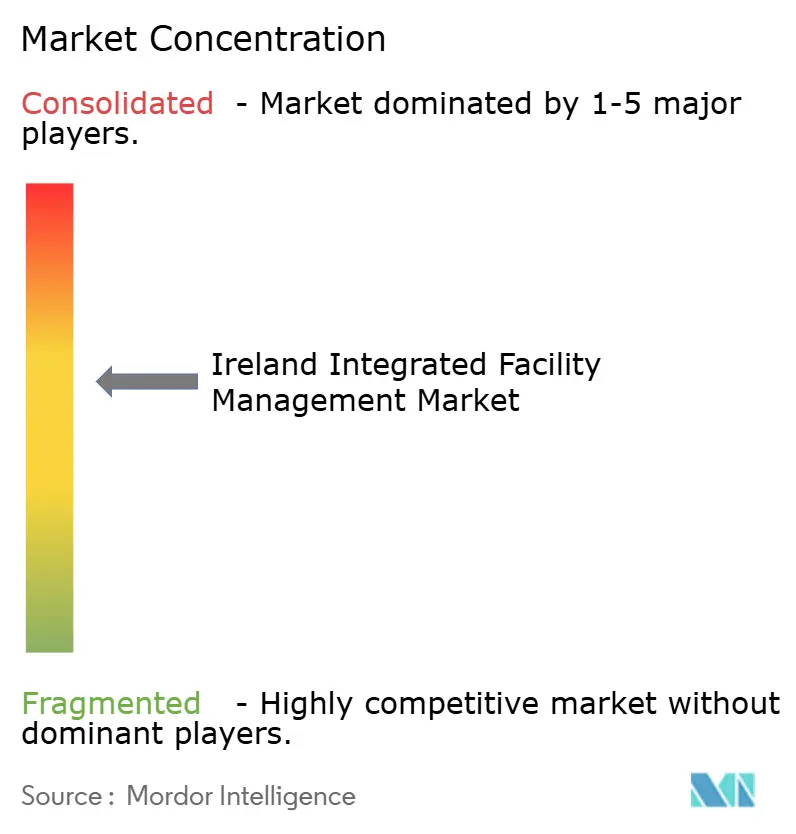

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ireland Integrated Facility Management Market Analysis by Mordor Intelligence

The Ireland Integrated Facility Management Market size is expected to grow from USD 420.17 million in 2025 to USD 450.64 million in 2026 and is forecast to reach USD 590.39 million by 2031 at 5.57% CAGR over 2026-2031.

The Ireland integrated facility management (IFM) market is now moving into a steadier phase after the outsourcing surge seen between 2021 and 2023, with demand shifting toward multi-service contracts that are judged on outcomes, service continuity, and measurable performance rather than only on price. Ireland’s economic base continues to support this model because the country hosts 9 of the world’s top 10 pharmaceutical companies and remains a key European base for technology, BFSI, and life sciences occupiers, which creates a stronger starting point for integrated contracts than for loosely bundled service models. Medical and pharmaceutical products accounted for 53% of Ireland’s total goods exports in 2025, while pharmaceutical exports reached EUR 99.9 billion (USD 109.0 billion), in 2024, and that concentration keeps technical maintenance demand unusually strong for a market of this size. Public capital spending also supports the Ireland IFM market, with Budget 2026 allocating EUR 19.1 billion (USD 20.8 billion) in capital expenditure and the National Development Plan Review 2025 committing EUR 102.4 billion (USD 111.6 billion) across 2026 to 2030, which steadily converts new hospitals, schools, transport assets, and public buildings into long-cycle service opportunities. At the same time, labor shortages, wage pressure, and the shift toward self-delivery have made scale more valuable. Larger providers are using acquisition-led expansion to improve technical depth and protect margins in the Ireland integrated facility management market.

Key Report Takeaways

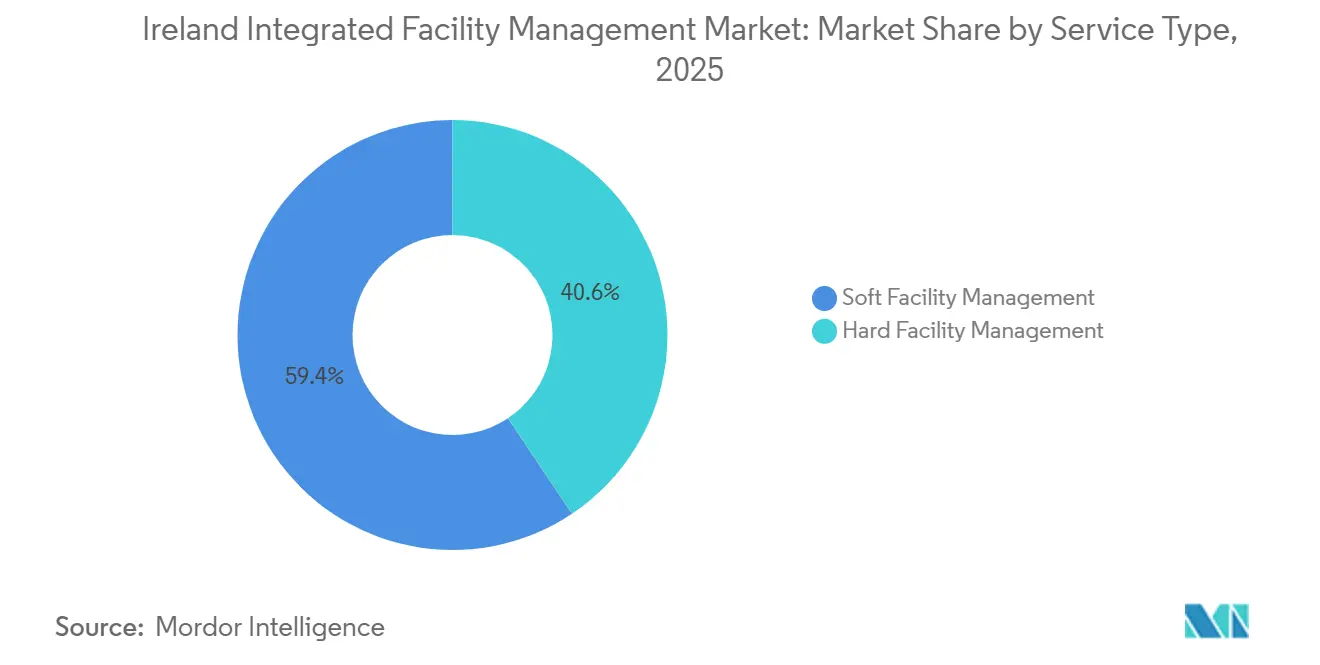

- By service type, soft facility management led with 59.37% of the Ireland integrated facility management market share in 2025, while hard facility management recorded the highest projected CAGR of 6.83% through 2031.

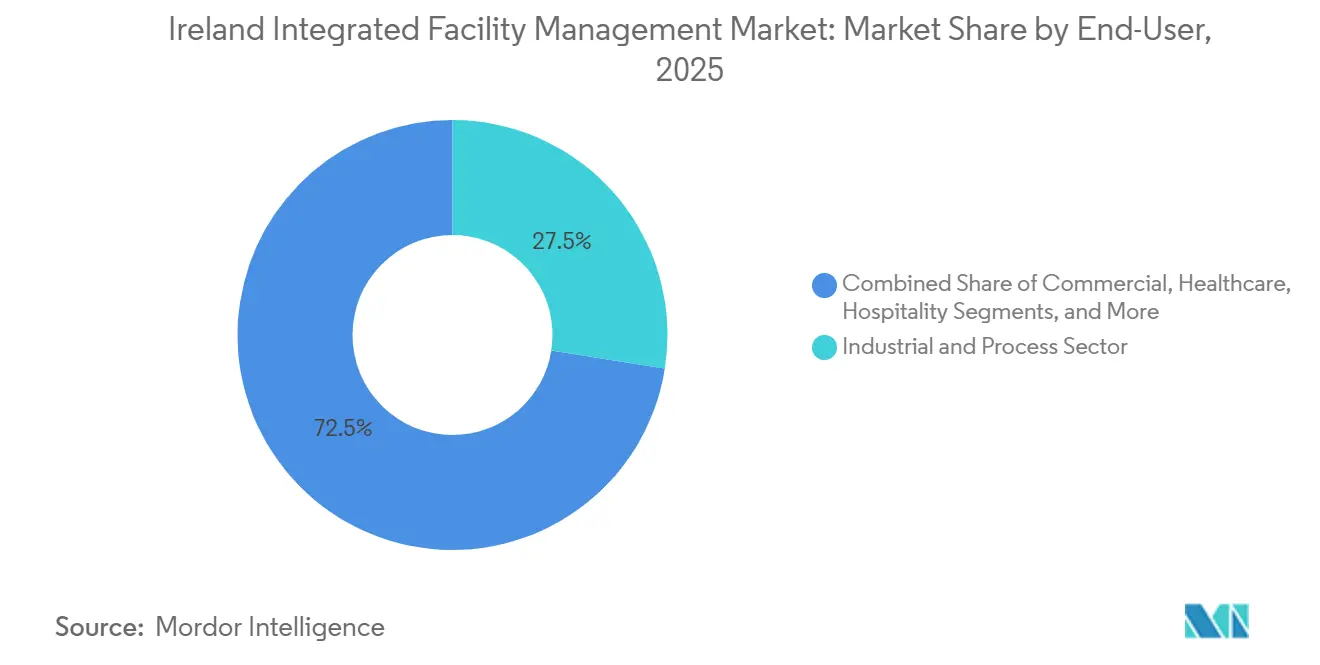

- By end-user, the industrial and process sector held 27.49% of the Ireland integrated facility management (IFM) market share in 2025, while commercial end-users posted the fastest projected CAGR of 6.73% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Ireland Integrated Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Adoption Of Integrated Services For Cost Optimization | +0.7% | Ireland-wide, most pronounced in Dublin, Cork, and Galway pharmaceutical and commercial corridors | Short term (≤ 2 years) |

| Growing Demand For Energy-Efficient And Sustainable Buildings | +0.6% | Ireland-wide, with early gains in Dublin Docklands commercial stock and pharmaceutical campuses across Leinster and Munster | Medium term (2-4 years) |

| Rising Outsourcing Trend Among Ireland Corporates | +0.4% | National, concentrated in technology and BFSI sectors in Dublin and Cork | Short term (≤ 2 years) |

| Significant Infrastructure Projects Linking Large-Scale IFM | +0.3% | National, with early gains in Dublin, Cork, and Galway | Long term (≥ 4 years) |

| Expansion Of Co-Invested Real Estate And Commerce Delivery Optimization | +0.3% | Dublin, Cork, and Limerick commercial and logistics real estate hubs | Medium term (2-4 years) |

| Landmark Economy Data Guiding IFM Customer Procurement Decisions | +0.2% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Adoption of Integrated Services for Cost Optimization

The Ireland integrated facility management market is benefiting from the shift toward single-provider contracts because these models reduce the coordination burden that comes from managing many specialist vendors at once. This was visible in July 2025 when the Medical Council of Ireland moved from more than 32 separate suppliers to one total facilities management structure, which removed duplication in oversight and created a more unified service model.[1]OCS, “July 2025 Publication Cited In Draft,” OCS CBRE reported a 10% reduction in cost per technical work order under its integrated delivery model, which gives procurement teams a direct cost case for consolidation rather than a general efficiency claim.[2]CBRE, “2026 Publication Cited In Draft,” CBRE For occupiers with multiple sites in Dublin, Cork, and Galway, unified reporting, common SLAs, and single-invoice billing reduce the internal workload associated with hard and soft service delivery.[3]FM Services Group, “April 2026 Publication Cited In Draft,” FM Services Group The effect becomes stronger once service providers are embedded into ERP and IWMS systems because contract transitions become more complex and retention naturally improves. Rising labour, energy, and material costs since 2022 have strengthened this pattern further because scaled providers are better placed to absorb inflation through purchasing leverage and workforce planning than fragmented single-service operators.

Growing Demand for Energy-Efficient and Sustainable Buildings

The Ireland integrated facility management market is also being shaped by tighter building energy and sustainability requirements that are moving from optional standards to contract-level expectations. Ireland is transposing the recast Energy Performance of Buildings Directive through the Energy Performance of Buildings Bill, which was listed for priority drafting in the first half of 2026, and this is widening the operational scope expected from FM partners. Providers that can deliver HVAC optimization, BMS upgrades, solar PV integration, and audit-ready energy documentation are now better positioned in tender evaluations because these capabilities directly support compliance and reporting requirements. Budget 2026 allocated EUR 558 million (USD 614 million), to the Sustainable Energy Authority of Ireland for retrofit schemes, which creates a clear delivery route for technically capable operators working across public and residential assets. Apleona stated in January 2026 that more than 80% of Ireland’s 2050 building stock is already built, which means the practical decarbonization task now lies in operating efficiency rather than replacement of the full asset base. This raises the value of IFM contracts that combine retrofit work with ongoing performance management, while buildings with LEED, BREEAM, or BREEAM In-Use credentials require providers that can maintain and demonstrate those standards year after year.

Rising Outsourcing Trend Among Ireland Corporates

The Ireland integrated facility management market continues to gain support from a corporate base that prefers to keep facilities expertise outside core operating teams. Multinational employers in Ireland often follow parent-company models that favour lean internal staffing, and ISS’s position across technology, manufacturing, and life sciences illustrates how outsourcing can lower fixed-cost exposure while giving clients access to specialist training, technology, and tools. The internal capability gap is also widening because experienced facilities professionals have been retiring since 2024, while building systems are becoming more complex through wider use of BMS, IoT monitoring, and GMP-driven documentation standards. Cedefop’s 2025 Ireland Skills Forecast showed strong shortage pressure in service management roles, which adds replacement demand to an already tight labour environment and makes in-house FM teams harder to sustain. Apleona stated in December 2025 that outsourcing in Ireland is most developed in pharmaceutical, technology, finance, and manufacturing settings, while healthcare, education, and the public sector appear to be the next wave of adoption. That public and institutional shift is starting to show in practice because the publication of IDA Ireland’s EUR 20 million (USD 22.0 million), tender in March 2026 signals that long-cycle outsourced IFM models are moving into areas that were previously served through more fragmented internal arrangements.

Significant Infrastructure Projects Linking Large-Scale IFM

The Ireland integrated facility management market is also supported by an infrastructure program that steadily turns capital projects into operating assets that need professional management for many years after handover. The Accelerating Infrastructure Report and Action Plan, published in December 2025, identified 30 actions to remove delivery barriers for nationally significant projects across transport, healthcare, housing, and energy, which expands the pipeline of future FM assets. Projects moving through procurement or construction in 2026 include MetroLink, Cork Area Commuter Rail Phase 1, the National Maternity Hospital, and more than 300 school building projects scheduled for completion in 2026 and 2027. Data centers form a separate source of demand because they require permanent hard FM coverage, and PwC Ireland projected EUR 71.8 billion (USD 78.3 billion), in digital infrastructure investment through 2050 as AI workloads and hyperscaler activity expand. Hospitals, data centers, and education campuses all move into long operating cycles once commissioned, and that gives integrated providers a recurring revenue base that extends far beyond the original construction phase. This is why large contractors are building technical teams before project completion so they can move from asset delivery into full-service facility management without a long transition period.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tight Labor Market Driving Wage Inflation | -0.5% | Ireland-wide, most acute in Dublin and Cork where competing infrastructure and pharmaceutical construction programs absorb skilled trades | Short term (≤ 2 years) |

| Cost And Uncertainty For Corporate CAPEX | -0.3% | National, particularly affecting multinational occupiers managing global balance sheets under macroeconomic uncertainty | Medium term (2-4 years) |

| Challenges In Attracting Foreign Investments In Certain Regions | -0.2% | Predominantly the Border Region and secondary urban centers outside the Dublin-Cork-Galway triangle | Long term (≥ 4 years) |

| High Public Procurement Rules Inhibiting Innovation | -0.1% | National, concentrated in government and institutional segments reliant on OGP framework agreements | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tight Labor Market Driving Wage Inflation

The Ireland integrated facility management market faces one of its clearest limits in the form of a tight labour market for technical building roles. Facilities management and construction are drawing from the same pool of mechanical, electrical, and HVAC engineers, and the Department of Enterprise, Trade, and Employment formally recognized this pressure when it included several engineering roles on the updated Critical Skills Occupations List in September 2024. Morgan McKinley reported that Facilities Technician salaries in Dublin ranged from EUR 50,000 to EUR 55,000 (USD 54,500 - USD 59,950) in 2026, while professionals with more than 5 years of experience could command EUR 55,000 to EUR 60,000 (USD 59,950 - USD 65,400), and that raises cost pressure in hard FM, where labor represents most of the service cost. Indeed, Hiring Lab reported 4.6% year-on-year wage growth in December 2024, while the Irish Fiscal Advisory Council recorded a construction workforce of 177,000 in early 2025, indicating that competition for qualified trades remained intense. In response, providers are favoring self-delivery employment models over heavier subcontracting because direct employment offers tighter cost control and more reliable access to specialist skills. This also helps explain the acquisition activity seen between 2024 and 2026, because directly employed engineering capacity has become a strategic asset rather than merely an operating preference in the Ireland integrated facility management market.

Cost And Uncertainty for Corporate CAPEX

Cost pressure around corporate capital spending also slows parts of the Ireland integrated facility management market, especially in the commercial segment where multinational occupiers make portfolio decisions against global budget constraints. Since 2024, hybrid work has led some firms to rework office footprints rather than simply renew existing space, resulting in shorter contract terms, more flexible scopes, and delayed service upgrades. KPMG noted in its Ireland Infrastructure Outlook 2026 that funding and affordability were broad constraints across transport, housing, and commercial real estate development, which, in turn, indirectly affects the pace at which new buildings enter full FM operation. Currency movements also affect the economics for USD-reporting multinationals with EUR-denominated Irish operations because a stronger EUR can raise the reported cost of local FM commitments. Providers have responded by offering modular scopes and outcome-based pricing, which helps sustain renewal activity but can reduce the pace of entirely new contract formation. The result is not a collapse in demand because facilities budgets remain necessary, but rather a slower expansion path for some occupiers while they reassess space needs and investment timing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard FM Accelerates as Technical Complexity Deepens

Soft facility management (FM) accounted for 59.37% of the Ireland integrated facility management market size in 2025, supported by Ireland’s concentration of offices, retail assets, institutions, and hospitality sites where cleaning, catering, security, and workplace services make up a large share of contract scope. The catering and hospitality component is gaining greater weight in integrated contracts, as shown by the Central Bank of Ireland’s June 2025 award of a EUR 28.5 million (USD 31.1 million) contract to Sodexo Ireland, which included digital cashless payment capability within the service model rather than as a separate procurement line. Soft FM still leads in scale, but the growth pattern in the Ireland integrated facility management industry is now tilting toward technical services because buildings are becoming more regulated, more data-driven, and more complex to operate. Hard FM is forecast to grow at a 6.83% CAGR from 2026 to 2031, and that pace is tied to GMP-compliant pharmaceutical maintenance, critical systems support in data centers, and wider use of BMS-led building control in the Ireland integrated facility management market. ISO 41001 is also becoming more visible in Irish tender criteria, which raises the qualification threshold for both hard and soft service providers and favours operators that can show stronger governance, audit readiness, and service integration.

Within Hard FM, asset management and IoT-enabled monitoring are expected to expand faster than traditional planned preventive maintenance because clients increasingly want live performance data, early fault detection, and documented service histories. That requirement is especially important in pharmaceutical facilities, where maintenance records need to stand up to FDA and EMA audit expectations and where lower-capability operators are less likely to qualify for campus-wide contracts. Apleona’s January 2026 partnership with the Tim Kelly Group added 190 mechanical and electrical technicians and strengthened its self-delivery position in pharmaceutical, manufacturing, and public sector settings, which directly matches this technical demand pattern. Within Soft FM, the security services segment is also becoming more integrated, with remote monitoring, Alarm Receiving Centre operations, and related systems moving into broader IFM platforms rather than remaining standalone contracts. OCS Ireland’s acquisition of Top Security in 2025, which brought more than 300 employees into the business and lifted its Irish workforce to nearly 4,000, shows how security capability is being folded into wider service offers to deepen technical scope and improve contract stickiness.

By End-User: Commercial Growth Offsets Industrial Dominance

The Industrial and Process Sector held 31.52% of the Ireland integrated facility management market size in 2025, reflecting the unusually high concentration of pharmaceutical and MedTech production sites across Cork, Kildare, Waterford, Galway, and Limerick. Pharmaceutical exports reached EUR 99.9 billion (USD 109.0 billion), in 2024, which confirms the economic weight of these facilities and explains why industrial sites generate more hard service demand than their number alone would suggest. Even with that lead, the fastest expansion is expected in commercial occupiers, where the Ireland integrated facility management market size for commercial end-users is projected to rise at a 3.49% CAGR through 2031 as occupiers deepen contract scope around energy management, carbon reporting support, and workplace experience. This pattern reflects a more selective office strategy rather than simple expansion because some companies are using fewer sites but demanding more integrated service coverage in the Grade A spaces they keep. CBRE’s Ireland Real Estate Market Outlook 2026 noted continued demand for best-in-class space from technology and financial services occupiers, with sustainability features and digital amenities now treated as baseline requirements rather than premium extras.

Hospitality remains an important part of the demand mix, especially in Dublin, Killarney, Galway, and Shannon Airport areas where tourism-linked assets support service needs in food management, grounds care, and facility technology. Institutional and public infrastructure occupiers are still earlier in the adoption curve, but momentum is rising as fragmented in-house delivery gives way to consolidated outsourced models. The Medical Council of Ireland contract awarded to OCS in July 2025 and the publication of IDA Ireland’s EUR 20 million (USD 22.0 million), integrated FM tender in March 2026 both point to a more formal procurement approach in public and quasi-public settings. Healthcare is also becoming more important because Budget 2026 allocated EUR 1.56 billion (USD 1.72 billion), to health infrastructure, supporting hospital completion, acute bed additions, and primary care expansion that will require professional operation from day one. The Other End-User Industries group, which includes multi-unit residential and utilities, is still at an earlier stage, but it is starting to build relevance as housing delivery scales and owner-management companies need more formal building management arrangements.

Geography Analysis

The Ireland integrated facility management market is concentrated along a coastal economic corridor led by Dublin and extending through Cork, Limerick, Galway, and Waterford. Dublin remains the main center because it holds the largest stock of Grade A commercial real estate, which supports high volumes of Soft FM across offices, institutions, and mixed-use assets. Technology and BFSI occupiers continue to anchor demand in the Docklands, Grand Canal Dock, Sandyford, IFSC, and Blanchardstown business estates, where multi-site service needs are common. This concentration gives providers access to dense contract clusters, shorter mobilization distances, and higher-value multi-service mandates. Budget 2026 also allocated EUR 8.87 billion (USD 9.8 billion), to housing capital, and EUR 3.98 billion (USD 4.4 billion), to transport capital, meaning the stock of FM-relevant assets around Dublin will keep widening as new communities and transport facilities come into operation.

Outside Dublin, Cork, Limerick, Galway, and Waterford represent the growth frontier of the Ireland integrated facility management market because these cities sit at the center of the state’s regional development strategy. Project Ireland 2040 targeted at least 50% population growth by 2040 for these cities, which supports a broader long-term case for office, industrial, healthcare, education, and residential asset growth. Hard FM demand is especially strong in regional industrial clusters, including pharmaceutical operations in Cork, the Limerick-Shannon corridor, and Galway’s MedTech base. The National Development Plan Review 2025 committed EUR 102.4 billion (USD 111.6 billion), across 2026 to 2030, and regional transport and healthcare spending within that program will gradually convert into long-term service opportunities across all provinces. Apleona’s Tim Kelly Group partnership, which added teams in Ballinrobe, Galway, and Letterkenny, also shows that providers are expanding coverage into western and northern areas rather than building only within the Dublin-Cork pair.

The regional picture is less favorable in border areas and smaller urban centers, where lower multinational density and slower commercial development constrain contract size and timing. KPMG identified the Atlantic Economic Corridor road network and Ceannt Quarter in Galway as catalysts for future demand in secondary locations, but conversion from project delivery to operating contracts is expected to take longer in these markets. The National Broadband Plan should support more distributed workplace activity over time, which may create incremental soft service demand in regional business parks and government offices. Even so, compliance under Health and Safety Authority rules and Building Regulations Technical Guidance Documents is consistent across the country, which favours providers with national compliance systems and makes scale an advantage even in smaller locations.

Competitive Landscape

The Ireland integrated facility management market is moderately concentrated in the large-contract segment, where Apleona, CBRE GWS, ISS Ireland, Sodexo Ireland, Bidvest Noonan, OCS Ireland, Mitie Ireland, and ABM Ireland account for a large share of complex multi-site opportunities. Competition is increasingly shaped by self-delivery because clients want fewer subcontracting layers, more direct control of technical labor, and clearer accountability across hard and soft service lines. Apleona illustrates this pattern well because its 3 Irish acquisitions since 2022, culminating in the Tim Kelly Group partnership completed in January 2026, were aimed at reducing dependence on subcontracted technical work and expanding direct engineering capacity. The result was an Irish workforce of nearly 3,000 people, providing the company with stronger coverage in installation, maintenance, and project delivery. In the Ireland integrated facility management market, that kind of scale matters because labour shortages, compliance needs, and technical specialization are making service continuity as important as price in tender decisions.

CBRE is competing through performance contracting rather than only labour scale, and its CORE model reported a 10% reduction in cost per technical work order and a 29% reduction in energy consumption in the managed Irish portfolio. That approach matters because large occupiers now want measurable operating outcomes linked to energy, maintenance efficiency, and workplace performance, not only a bundled service menu. ABM is following a parallel route through targeted expansion, with its June 2025 acquisition of LMC FM strengthening nationwide coverage and its Galway healthcare mobilization showing deeper sector reach. OCS has also expanded its platform through the integration of security capability, while Bidvest Noonan has used robotics and water-saving technologies to differentiate itself on innovation in large campus settings. Across the Ireland integrated facility management market, predictive maintenance tools, connected HVAC and BMS systems, and CMMS platforms are no longer niche differentiators because they are becoming standard expectations in larger procurement exercises.

There is still room for smaller and mid-sized providers, especially in the space between single-site local contracts and very large multinational portfolios. Companies such as Sensori FM, FLEXÉIR Facilities Services, and Bidvest Noonan are targeting mid-market clients that operate several facilities but may not attract the full attention of the largest global players. Their advantage often comes from sector focus, local responsiveness, and a willingness to customize service design for contract sizes that fall below the main targets of the biggest providers. At the same time, public procurement rules and OGP framework requirements favour well-established firms with stronger financial reporting, transfer experience, and compliance records, which protects incumbents in institutional renewals. This creates a two-tier market structure in which strategic integrated mandates continue to consolidate among scaled operators, while selected domestic and specialist firms compete more actively in regional and mid-value contracts.

Ireland Integrated Facility Management Industry Leaders

ISS A/S

Sodexo SA

CBRE Group Inc.

Aramark Corporation

Mitie Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: IDA Ireland published a tender for an integrated FM services contract covering its Irish and international office portfolio, valued at EUR 20 million (USD 22.0 million), with a 4-year initial term and a maximum 7-year life. Services include mechanical, electrical, cleaning, grounds maintenance, catering, and helpdesk functions, representing a significant institutional shift toward bundled professional IFM delivery.

- January 2026: Apleona completed its partnership with Tim Kelly Group, a County Mayo-based mechanical and electrical systems provider employing 190 specialist technicians across pharmaceutical, manufacturing, commercial, and public sector clients. This is Apleona’s third sizeable investment in Ireland since 2022, following Acacia and Neylons, and it extends its self-delivery capability into mechanical and electrical installation and project delivery. Financial terms were not disclosed.

- October 2025: Bidvest Noonan extended its multi-year FM partnership with University College Dublin for the 330-hectare Belfield campus, covering cleaning and outdoor grounds maintenance across academic buildings, laboratories, the National Virus Reference Laboratory, and event spaces. The extension incorporates robotic cleaning systems and water-saving technology, establishing innovation capability as a decisive factor in contract renewal.

- July 2025: OCS mobilized Phase 1 of a two-year Total Facilities Management contract with the Medical Council of Ireland, consolidating more than 32 previously separate suppliers into a single integrated delivery structure encompassing cleaning, security, mechanical and electrical maintenance, life safety systems, BMS management, CCTV monitoring, and keyholding services.

Ireland Integrated Facility Management Market Report Scope

Ireland Integrated Facility Management Market Report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, Fire Systems and Safety, and Other Hard Facility Management Services], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and Other Soft Facility Management Services]), End User (Commercial (includes BFSI, IT and Telecom, Retail and Warehouses, etc.), Hospitality (includes Eateries, Restaurants and Large-Scale Hotels), Institutional and Public Infrastructure (includes Government Establishments, Education, Transportation such as Airports and Railways, etc.), Healthcare (includes Public and Private Healthcare Facilities), Industrial and Process Sector (includes Manufacturing, Energy including Oil and Gas Exploration, Mining, etc.), and Other End-User Industries (Multi-House Residential, Entertainment, Sports and Leisure)). The Market Forecasts are Provided in Terms of Value (USD).

| Hard Facility Management | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft Facility Management | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management Services |

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process Sector |

| Other End-user Industries |

| By Service Type | Hard Facility Management | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft Facility Management | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management Services | ||

| By End-user Industry | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process Sector | ||

| Other End-user Industries | ||

Key Questions Answered in the Report

What is the size of Ireland integrated facility management market in 2026?

The Ireland integrated facility management market stood at USD 450.64 Million in 2026 and is projected to reach USD 590.39 Million by 2031 at a 5.57% CAGR.

Which service category leads demand in Ireland?

Soft FM was the largest service category in 2025 with 59.37% share, supported by high demand from offices, institutions, retail assets, and hospitality sites.

Which part of the business is growing fastest through 2031?

Hard FM is the fastest-growing service type with a 6.83% CAGR, driven by pharmaceutical maintenance, data center systems support, and more complex building operations.

Which end-user group contributes the most revenue?

The Industrial and Process Sector led in 2025 with 27.49% share because Ireland’s pharmaceutical and MedTech base creates strong hard service demand across major production clusters.

Why are more occupiers moving to integrated contracts in Ireland?

Clients are consolidating services to reduce coordination effort, improve reporting, standardize SLAs, and access technical capabilities in energy management, compliance, and digital building operations.

What are the main risks affecting providers in Ireland?

The main constraints are wage inflation, competition for engineers and technicians, and delayed capital decisions among commercial occupiers adjusting office portfolios and project timing.

Page last updated on: