Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

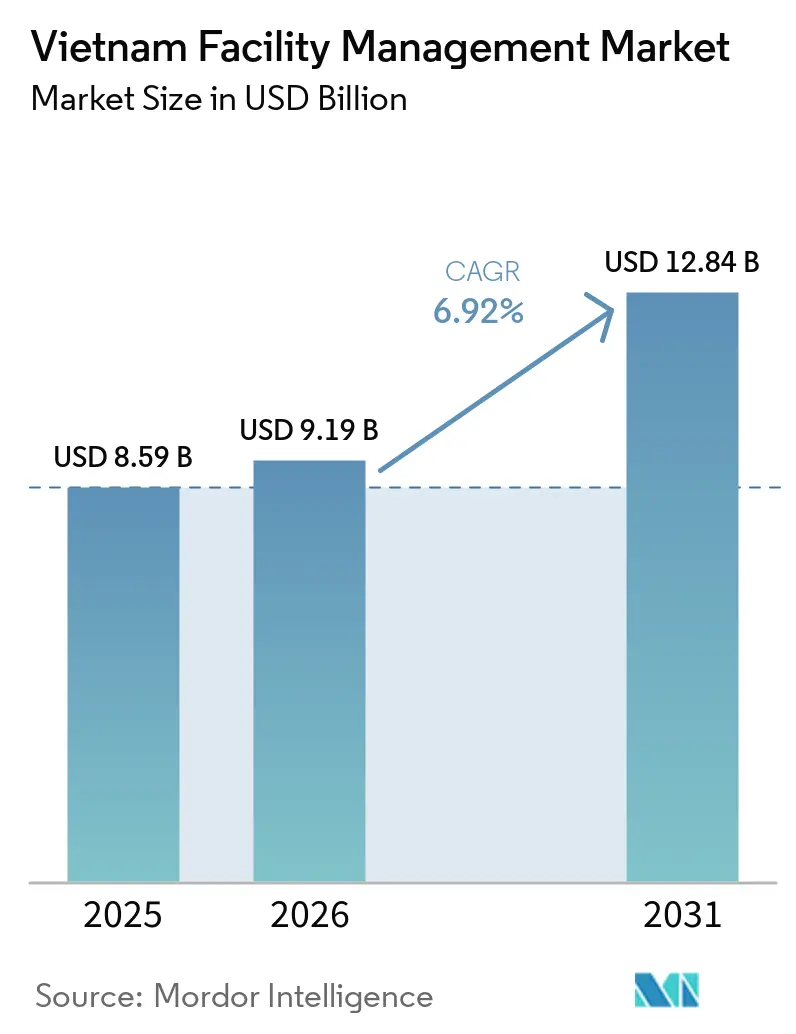

| Base Year Market Size (2025) | USD 8.59 Billion |

| Market Size (2026) | USD 9.19 Billion |

| Market Size (2031) | USD 12.84 Billion |

| Growth Rate (2026 - 2031) | 6.92% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Facility Management Market Analysis by Mordor Intelligence

The Vietnam facility management market size was valued at USD 8.59 billion in 2025 and estimated to grow from USD 9.19 billion in 2026 to reach USD 12.84 billion by 2031, at a CAGR of 6.92% during the forecast period (2026-2031). Rapid industrialization, the China-plus-one relocation wave, and a surge in Grade-A office completions are expanding the addressable base of commercial, industrial, and public-infrastructure assets that must run around the clock. The Vietnam facility management market is benefiting from state infrastructure programs that stipulate lifecycle operations in public-private concessions, while growing foreign direct investment is pushing landlords to adopt international service standards. Demand is shifting from single-service contracts toward bundled and integrated models because asset owners want cost certainty, uptime guarantees, and ESG reporting. Technology adoption, especially IoT monitoring and AI energy optimization, is moving from pilot to early scale, positioning digitally capable providers for outsized gains in the Vietnam facility management market.

Key Report Takeaways

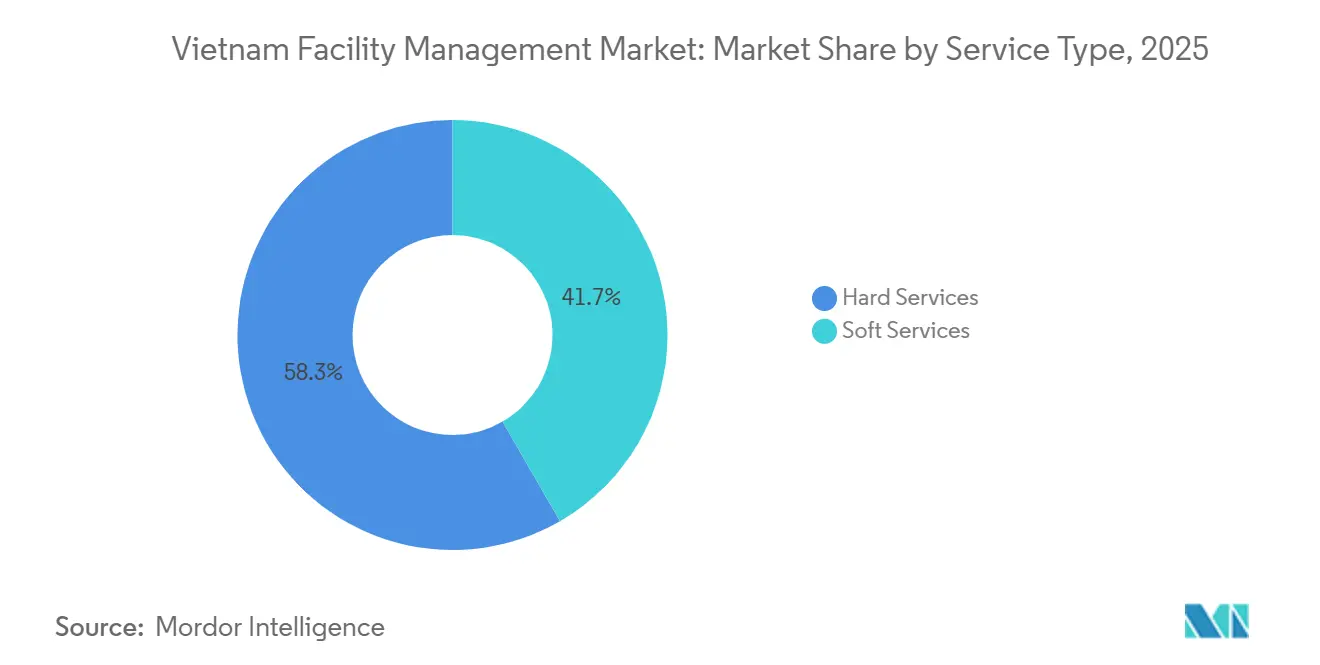

- By service type, hard services led with 58.34% of the Vietnam facility management market share in 2025. Soft Services is advancing at a 7.32% CAGR through 2031, the fastest pace among service types.

- By offering type, in-house teams controlled 53.67% of the Vietnam facility management market size in 2025, but Outsourced Facility Management is projected to expand at a 7.46% CAGR to 2031.

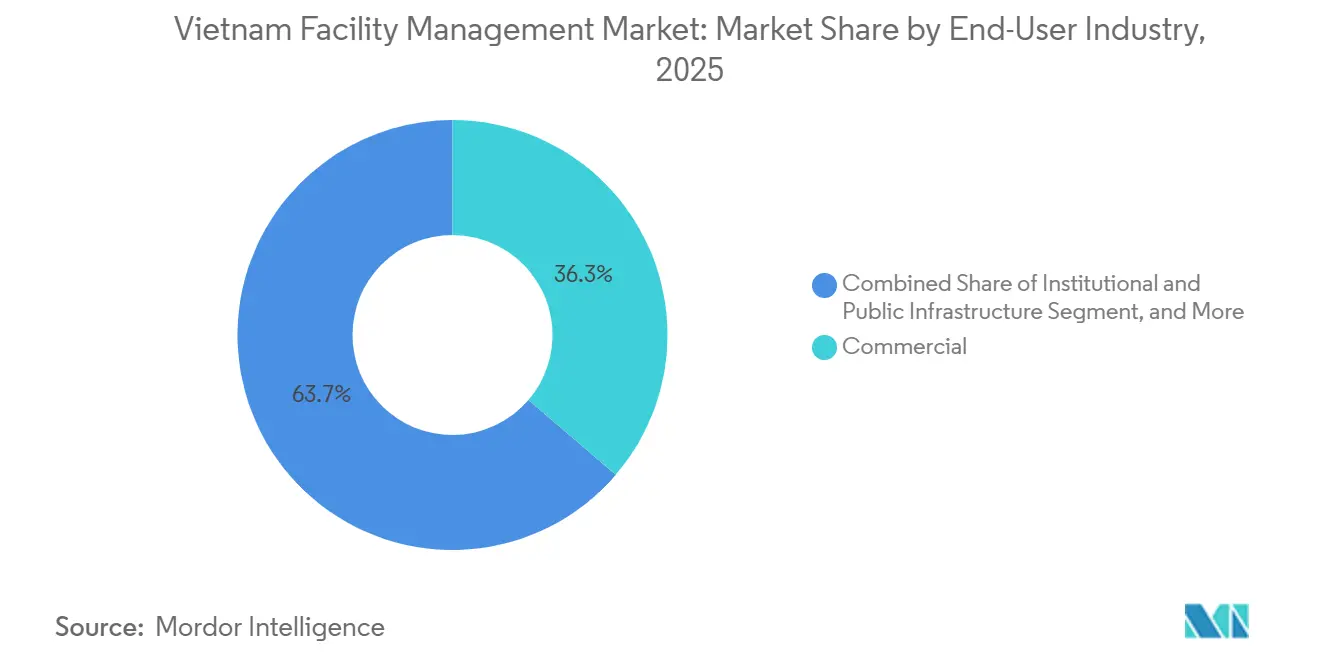

- By end-user Industry, commercial real estate captured 36.27% of total spending in 2025, whereas Institutional and Public Infrastructure is forecast to post the quickest growth at 7.28% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Grade-A Office and Mixed-Use Real Estate Stock | +1.8% | National, concentrated in Ho Chi Minh City, Hanoi, Da Nang | Medium term (2-4 years) |

| Manufacturing and Logistics Growth via China+1 and FTAs | +1.5% | Binh Duong, Dong Nai, Bac Ninh, Hai Phong industrial corridors | Long term (≥ 4 years) |

| Hyperscale Data-Center Build-Out Driving Critical-Environment FM | +1.2% | Ho Chi Minh City, Hanoi, spillover to Binh Duong | Short term (≤ 2 years) |

| Government Smart-City and Infrastructure PPP Initiatives | +1.0% | National, early gains in Ho Chi Minh City, Hanoi, Da Nang | Long term (≥ 4 years) |

| Cost-Optimization Outsourcing Trend in State and Private Enterprises | +0.9% | National, led by state-owned enterprises in Hanoi, Ho Chi Minh City | Medium term (2-4 years) |

| Green-Building, Energy-Efficiency Certification Demand – LOTUS, EDGE | +0.6% | National, early adoption in Ho Chi Minh City, Hanoi Grade-A towers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Grade-A Office and Mixed-Use Real Estate Stock

Grade-A inventory in Ho Chi Minh City and Hanoi climbed 18% between 2024 and 2025, adding more than 1.2 million m² of premium space that requires sophisticated mechanical, electrical, and plumbing upkeep, tenant-experience services, and stringent life-safety compliance.[1]CBRE Vietnam, “Vietnam Real Estate Market Outlook Q4 2025,” CBRE, cbre.com.vn Developers now pre-negotiate five-to-ten-year integrated contracts, often linking payment to LEED or LOTUS certification milestones that deliver 10%-15% rental premiums. Mixed-use schemes such as Vinhomes Golden River bundle residential concierge, retail area maintenance, and office hard services in a single scope, which favors providers able to manage multifaceted assets. New completions in Da Nang are targeting regional headquarters relocations, stretching the Vietnam facility management market beyond the Hanoi–Ho Chi Minh City corridor. As stock ages, demand will intensify for predictive maintenance, façade refurbishment, and elevator modernization.

Manufacturing and Logistics Growth via China + 1 and FTAs

Foreign capital of USD 22.8 billion flowed into manufacturing in 2025, stimulating the build-out of 15 million m² of factories and logistics hubs across Binh Duong, Bac Ninh, and Hai Phong.[2]Ministry of Planning and Investment, “Foreign Direct Investment Report 2025,” mpi.gov.vn Semiconductor assembly, battery production, and textile finishing lines all mandate ISO-class cleanrooms, hazardous-waste handling, and 24/7 HVAC monitoring, expanding the hard-services wallet within the Vietnam facility management market. Industrial-park operators bundle security, landscaping, and wastewater treatment into leases, effectively outsourcing operations from day one. Reduced tariffs under RCEP and the EU-Vietnam Free Trade Agreement lock in long-run export competitiveness, ensuring a steady stream of facilities that will require uptime guarantees above 98% and environmental compliance audits.[3]Savills Vietnam, “Vietnam Property Market Overview 2025,” Savills, savills.com.vn

Hyperscale Data-Center Build-Out Driving Critical-Environment FM

Data-center capacity is rising 25% a year as cloud and telecom providers race to serve Vietnam’s booming digital economy. The newly commissioned 30-MW Viettel IDC site and the upcoming 20-MW CMC Telecom campus both specify 99.99% uptime, demanding redundant chillers, N+1 power, and real-time BMS integration. AI-enabled cooling optimization and waste-heat recovery are moving from concept to procurement requirements, rewarding FM firms that can blend operational engineering with data science. Each additional megawatt adds roughly USD 1.5 million in annual facility-services revenue, making hyperscale projects a high-margin niche inside the Vietnam facility management market.

Government Smart-City and Infrastructure PPP Initiatives

Twenty-four municipalities are piloting smart-city programs under the National Digital Transformation agenda, with USD 67 billion earmarked through 2030 for metros, airports, and IoT-enabled civic buildings.[4]Ministry of Construction, “National Digital Transformation Program Progress Report 2025,” moc.gov.vn accelerating Vietnam Infrastructure development. PPP concessions transfer 15-to-25-year operations risk to private consortia, embedding outcome-based key-performance indicators such as 95% equipment availability and 24-hour fault response. FM providers that can deploy digital work-order platforms, mobile field-service tools, and ESG dashboards are positioned to win these long-tail contracts. Early metro lines in Ho Chi Minh City and Hanoi already require station cleaning, escalator upkeep, and HVAC servicing, anchoring multi-decade recurring revenue in the Vietnam facility management market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-Labor Shortage and High Turnover in FM Workforce | -0.8% | National, acute in Ho Chi Minh City, Hanoi technical roles | Short term (≤ 2 years) |

| Price-Focused Procurement Undercutting Service Quality | -0.6% | National, prevalent in state-owned enterprise and local developer tenders | Medium term (2-4 years) |

| Absence of Unified FM Licensing and Standards Causing Fragmentation | -0.4% | National, regulatory gaps across provinces | Long term (≥ 4 years) |

| Cyber-Physical Security Concerns Slowing IoT, BMS Adoption | -0.3% | Ho Chi Minh City, Hanoi, industrial parks with foreign investment | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Skilled-Labour Shortage and High Turnover in FM Workforce

Annual turnover tops 30% for BMS operators, HVAC technicians, and fire-safety specialists, inflating recruitment costs and lengthening contract mobilization by up to three months. Only 12% of workers hold recognized FM certifications, forcing service providers to run in-house academies that add 8%-12% to labor expense. English-language gaps hinder knowledge transfer from multinational clients, slowing adoption of global best practices. Unless vocational curricula incorporate FM modules and tax incentives encourage upskilling, constrained talent will limit the Vietnam facility management market’s ability to absorb sophisticated technologies.

Price-Focused Procurement Undercutting Service Quality

Sixty-eight percent of public-sector tenders award contracts primarily on price, driving margins to break-even levels and encouraging deferral of preventive maintenance, spare-parts stocking, and staff training. Healthcare and institutional assets are especially vulnerable, as infection-control lapses or equipment downtime have direct safety implications. The race to the bottom deters international firms from bidding, leaving asset owners with limited access to technology-backed solutions. Without procurement reform that weights lifecycle value, the Vietnam facility management market risks commoditization and slower digital transformation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Services Anchor Revenue, Soft Services Accelerate

Hard Services accounted for 58.34% of the Vietnam facility management market in 2025, a share underpinned by mechanically intensive buildings and stringent safety regulations that require quarterly inspections and annual system recertification. Heating, ventilation, and air-conditioning dominates spend because Vietnam’s tropical climate forces continuous cooling in offices, malls, and hyperscale data centers. Fire-system upgrades, elevator refurbishment, and façade maintenance are rising as first-generation Grade-A towers built between 2010 and 2015 now require lifecycle overhauls. Asset-management advisory is gaining favor among REITs and institutional landlords that need data-driven capital planning to defend yields, further cementing the revenue base for hard-service specialists across the Vietnam facility management market.

Soft Services represent a smaller dollar pool but expand at a 7.32% CAGR, driven by corporate hygiene mandates and the formalization of cleaning and security roles. International hospitality chains and JCI-accredited hospitals compel providers to meet documented audit trails, chemical-handling standards, and infection-control checklists, displacing informal labor pools. Office catering rebounds in tandem with workplace re-occupancy, and industrial campuses are outsourcing meal programs to manage worker retention. Landscaping and waste-management contracts are increasingly tied to LOTUS green-building points, transforming previously low-margin tasks into value-added deliverables within the Vietnam facility management market size for soft services.

By Offering Type: Outsourcing Gains Momentum

In-house operations still held 53.67% of spending in 2025, a legacy of state-owned enterprises that historically retained direct control over buildings. Rising labor costs, regulatory complexity, and tenant expectations for digital service delivery are exposing the inefficiencies of self-performing models. Pilot outsourcing programs in telecoms, energy, and transport are already unlocking 15%-25% cost savings, signaling the start of a wider realignment.

Outsourced facility management is projected to post a 7.46% CAGR to 2031, with bundled and integrated models taking the largest incremental share. Single-service cleaning or security contracts dominate small assets but are ceding ground to bundled scopes that simplify procurement and align accountability. Integrated facility management commands 20%-30% price premiums yet delivers quantifiable uptime gains, energy savings, and ESG disclosures, making it the preferred model for multinationals and data-center operators. Draft licensing rules that differentiate single, bundled, and integrated providers could formalize this segmentation and lift professional standards across the Vietnam facility management market.

By End-User Industry: Commercial Leads, Institutional Accelerates

Commercial real estate absorbed 36.27% of expenditures in 2025 thanks to 5.2 million m² of Grade-A office stock, premium retail malls, and proliferating coworking sites. Integrated contracts covering HVAC zoning, life-safety compliance, and tenant-experience technology average USD 18-22 per m² annually, keeping the segment the largest contributor to the Vietnam facility management market size. Hotel pipelines expanded 12% in 2025, spurring demand for white-glove guest-room maintenance, food-safety auditing, and utility cost optimization that fits strict brand standards.

Institutional and Public Infrastructure spending is rising fastest at a 7.28% CAGR as metros, airports, and smart-city precincts shift to performance-based operating models under long-term PPP concessions. Healthcare facilities add complexity through infection control and hazardous-waste handling, accelerating outsourcing among hospitals chasing international accreditation. Industrial and process plants in Binh Duong, Dong Nai, and Bac Ninh remain the second-largest users, relying on ISO 14001 environmental programs and 24/7 critical-equipment monitoring to protect export supply chains that anchor the Vietnam facility management market share in manufacturing corridors.

Geography Analysis

Ho Chi Minh City and Hanoi together generate roughly 65% of national revenue, reflecting their dominance in premium office stock, multinational occupiers, and public-infrastructure rollouts. Ho Chi Minh City delivered more than 700,000 m² of new space between 2024 and 2025, and the metro, airport expansion, and Thu Thiem new-urban projects create continuous demand for mechanical upkeep, station cleaning, and life-safety compliance contracts. Hanoi mirrors this trajectory with 500,000 m² of new Grade-A offices and major concessions covering Metro Line 3 and Noi Bai Airport Terminal 2, embedding multidecade FM workloads tied to stringent performance benchmarks across the Vietnam facility management market.

Da Nang is emerging as a tertiary hub where Grade-A stock grew 25% in 2025, supported by a smart-city master plan that features IoT-enabled municipal buildings and energy-efficient street lighting. Industrial zones in Binh Duong, Dong Nai, and Bac Ninh register the highest growth rates as electronics and automotive clusters relocate under China-plus-one strategies.

Hai Phong’s logistics and cold-chain boom, fueled by a 40% expansion in warehouse capacity in 2025, adds refrigeration maintenance and automated material-handling support to the service mix. Government regional development plans targeting the Central Highlands and Mekong Delta could widen the geographic footprint of the Vietnam facility management market, although those regions currently contribute less than 10% of turnover.

Competitive Landscape

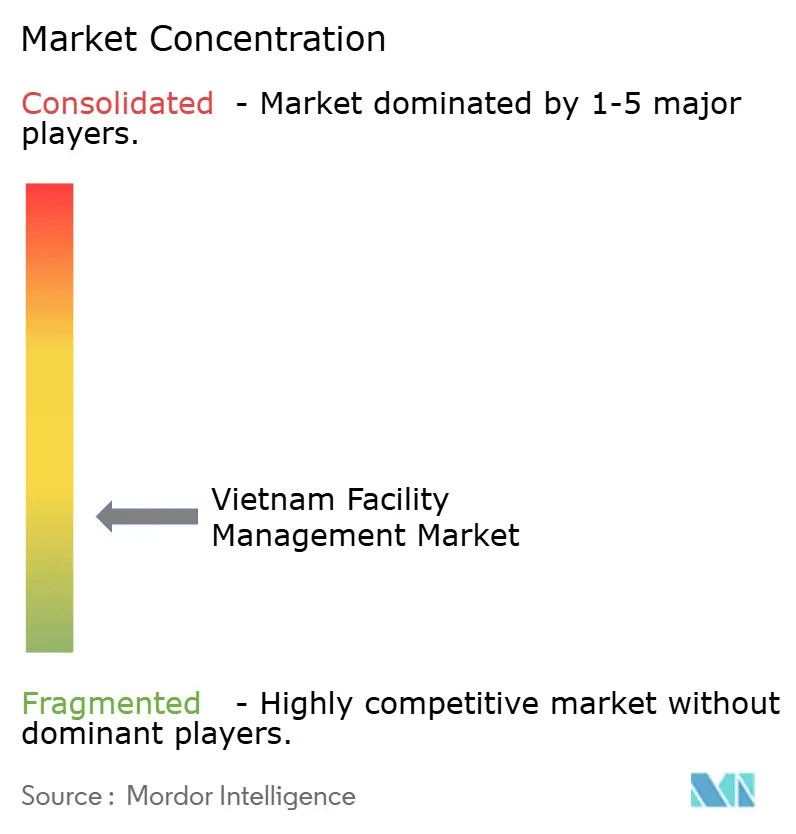

The top ten providers command about 45% of the Vietnam facility management market, indicating moderate concentration that still leaves maneuvering room for regional specialists and technology disruptors. Global incumbents such as Sodexo, CBRE, JLL, and Savills leverage integrated platforms, global procurement scale, and ESG reporting to win multiyear contracts in Grade-A offices, hyperscale data centers, and PPP concessions. Domestic challengers like RCR Vietnam, Vintek, and VSIP Facility Management compete effectively in industrial parks and mixed-use schemes where local permitting knowledge, cost structures, and language alignment resonate with asset owners.

Technology differentiation is accelerating: IoT sensors, AI-based energy analytics, and blockchain compliance logs are now mandatory in select hyperscale and smart-building RFPs. Providers that adopt ISO 41001 management systems and tiered digital toolsets are edging ahead in tenders that score bidders on measurable uptime, sustainability outcomes, and tenant satisfaction.

White-space remains in outcome-based contracting, which ties fees to performance metrics instead of labor hours; early adopters in data centers and smart offices are setting precedents likely to spill into industrial and healthcare estates. Venture-backed SaaS platforms that match owners with vetted subcontractors are gaining curiosity but face licensing ambiguity, meaning incumbents that integrate such tools into existing workflows may capture the next layer of value in the Vietnam facility management market.

Vietnam Facility Management Industry Leaders

RCR Vietnam

Sodexo Vietnam

ATALIAN Global Services Vietnam

Thainam Facility Services

TKT Cleaning

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: CBRE Vietnam secured a seven-year integrated contract for the 250,000 m² Vinhomes Golden River complex, bundling IoT-enabled MEP maintenance with ESG reporting aligned to LEED Gold targets.

- December 2025: JLL Vietnam partnered with CMC Telecom to run a 20-MW Tier III data center in Hanoi, including AI-driven cooling optimization and 24/7 critical monitoring, with handover slated for Q3 2026.

- November 2025: Sodexo Vietnam won a five-year catering and facility-support deal at Samsung Electronics’ Bac Ninh campus, serving 15,000 employees in cleanroom conditions.

- October 2025: ATALIAN Global Services bought 60% of TKT Cleaning, adding 2,000 personnel and strengthening bundled soft-service offerings.

Vietnam Facility Management Market Report Scope

Facility management (FM) is a profession that incorporates many disciplines to ensure functionality, safety, comfort, and efficiency of the built environment by integrating people, process, place, and technology. FMs contribute to the business's bottom line through their responsibility for often maintaining an organization's most significant and most valuable assets, such as property, equipment, buildings, and other environments that house personnel, productivity, inventory, and other elements of the operation. The objective of professional FM as an interdisciplinary business function is to coordinate the demand and supply of facilities and services in both public and private organizations.

The Vietnam Facility Management Market Report is Segmented by Service Type (Hard Services including Asset Management, MEP and HVAC Services, Fire Systems and Safety, Other Hard Facility Management Services; Soft Services including Office Support and Security, Cleaning Services, Catering Services, Other Soft Facility Management Services), Offering Type (In-house, Outsourced including Single Facility Management, Bundled Facility Management, Integrated Facility Management), End-User Industry (Commercial, Hospitality, Institutional and Public Infrastructure, Healthcare, Industrial and Process, Other End-User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management Services |

By Offering Type

| In-house | |

| Outsourced | Single Facility Management |

| Bundled Facility Management | |

| Integrated Facility Management |

By End-User Industry

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process |

| Other End-User Industries |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management Services | ||

| By Offering Type | In-house | |

| Outsourced | Single Facility Management | |

| Bundled Facility Management | ||

| Integrated Facility Management | ||

| By End-User Industry | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

How fast is the Vietnam facility management market expected to grow between 2026 and 2031?

The sector is projected to advance at a 6.92% CAGR, enlarging from USD 9.19 billion in 2026 to USD 12.84 billion by 2031.

Which service type holds the largest revenue share today?

Hard Services lead with 58.34% of market spending because mechanically intensive buildings and strict safety rules require frequent technical maintenance.

What segment is expanding at the quickest rate?

Outsourced Facility Management is forecast to grow at a 7.46% CAGR as state-owned enterprises and multinationals turn to bundled and integrated contracts for cost savings and uptime guarantees.

Why are data centers significant for facility management providers?

Each additional megawatt of capacity delivers around USD 1.5 million in annual FM fees, while Tier III and Tier IV uptime targets demand specialist skill sets and digital monitoring tools.

Which cities generate most of the demand?

Ho Chi Minh City and Hanoi jointly account for about 65% of national revenue because of their concentration of Grade-A offices, infrastructure projects, and multinational tenants.

What are the main hurdles facing service providers?

Acute shortages of certified technicians and lowest-bid procurement practices tighten margins, slow technology adoption, and threaten service-quality consistency.

Page last updated on: