United States Integrated Facility Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

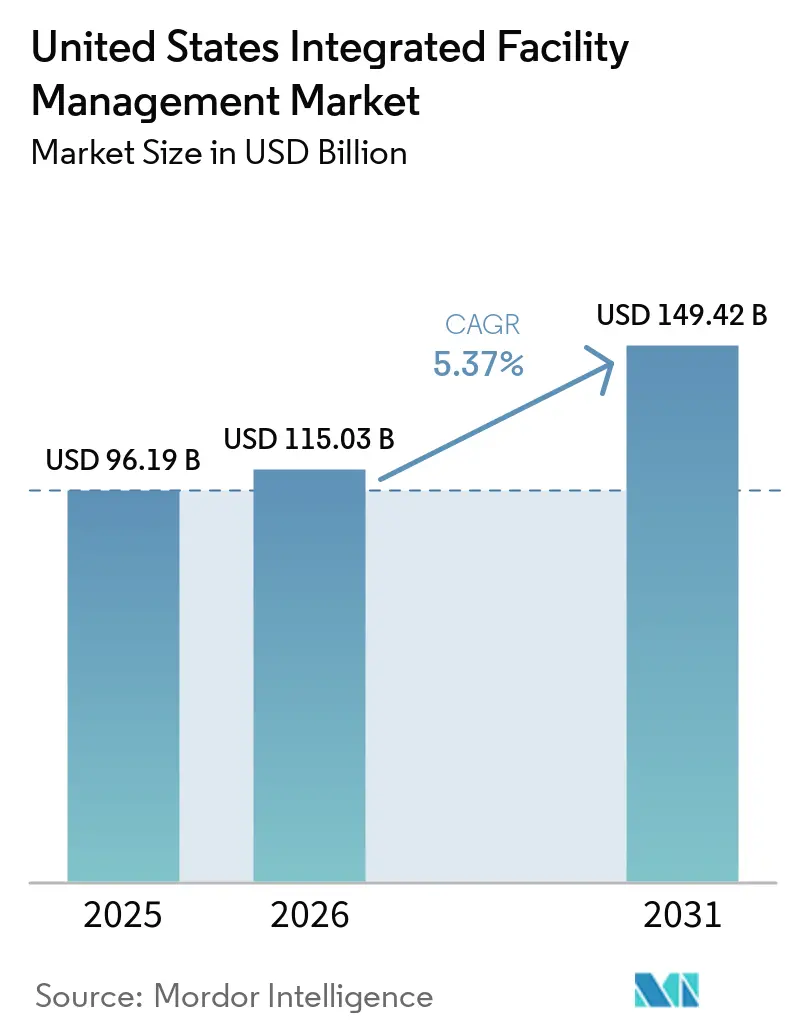

| Base Year Market Size (2025) | USD 96.19 Billion |

| Market Size (2026) | USD 115.03 Billion |

| Market Size (2031) | USD 149.42 Billion |

| Growth Rate (2026 - 2031) | 5.37% CAGR |

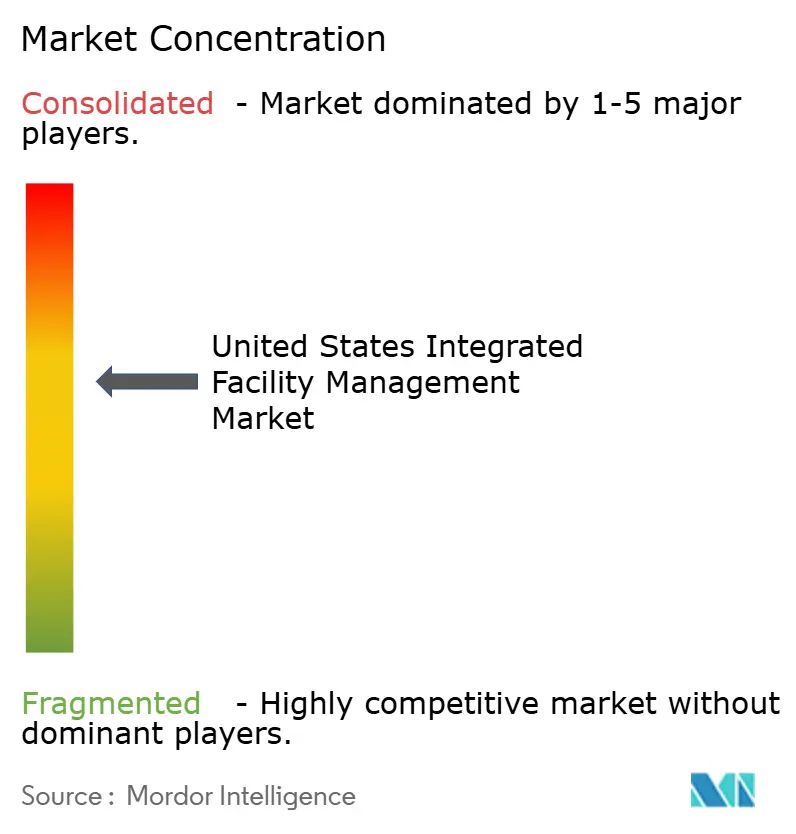

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Integrated Facility Management Market Analysis by Mordor Intelligence

The United States integrated facility management market size was valued at USD 96.19 billion in 2025 and estimated to grow from USD 115.03 billion in 2026 to reach USD 149.42 billion by 2031, at a CAGR of 5.37% during the forecast period 2026-2031. The United States integrated facility management (IFM) market is being supported by steady demand for bundled service delivery across commercial, industrial, and institutional real estate, where buyers increasingly prefer single-vendor accountability over multi-provider coordination. Operating complexity is rising as buildings add more digital controls, connected devices, and performance tracking layers, which makes separate service contracts harder and more expensive to manage. Real estate portfolios are also being reshaped, with occupiers reducing excess space while investing more heavily in better assets, and that has strengthened the case for integrated service models at the executive level. Growth is also being reinforced by tighter energy compliance needs, uneven workplace occupancy patterns, and a clear move toward performance-led contracts that tie service delivery to uptime, efficiency, and experience outcomes. At the same time, cyber risk in connected building systems and shortages in technical labor are raising delivery costs, which is pushing larger providers with stronger platforms and staffing depth into a more favorable competitive position in the US IFM mark.

Key Report Takeaways

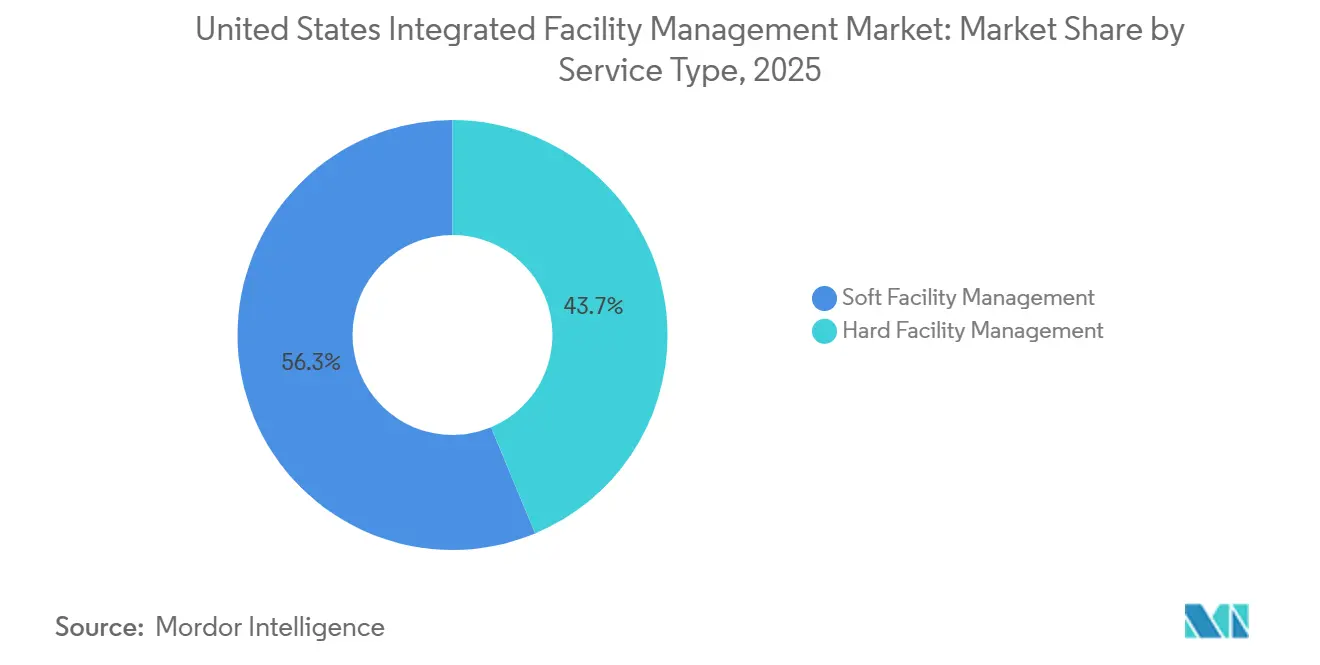

- By service type, soft facility management segment held 56.28% share of revenue in 2025, while hard facility management segment in the United States integrated facility management market is projected to expand at a 5.37% CAGR through 2031.

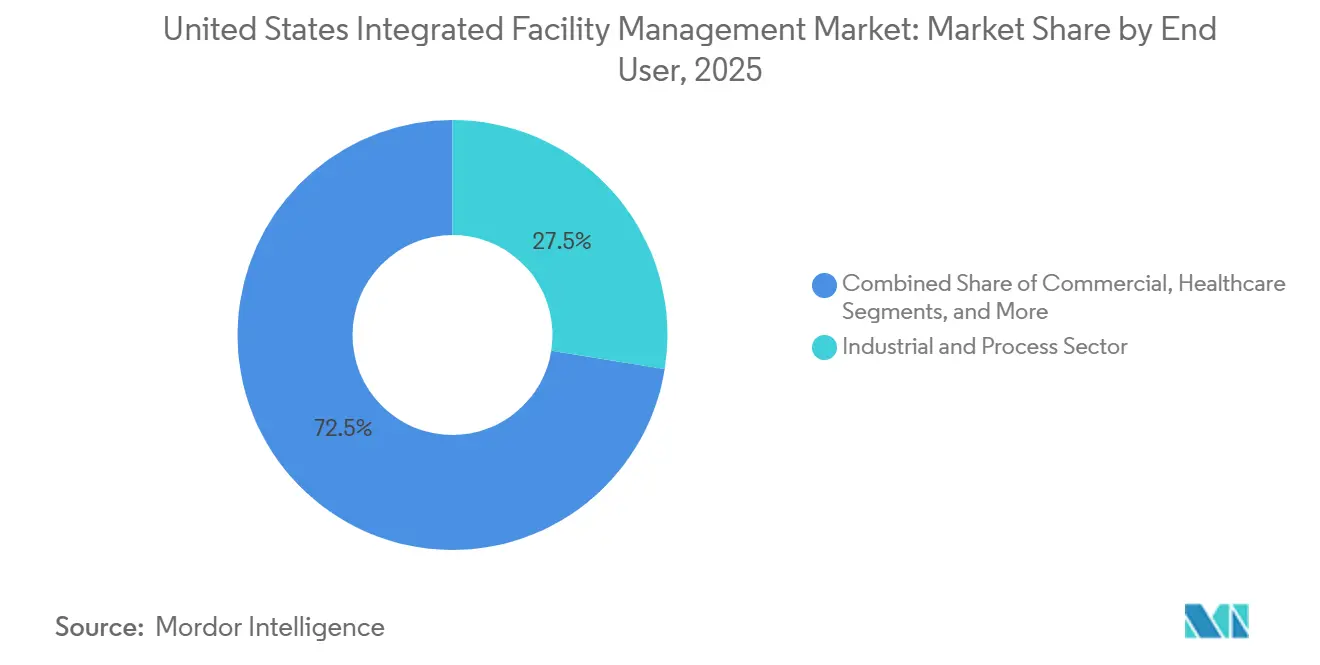

- By end user, the industrial and process segment held 27.53% share in 2025, while the commercial segment in the United States integrated facility management marketis projected to grow at a 6.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Integrated Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Smart, Connected Buildings | +1.2% | National, with concentrated early uptake in coastal metros including New York City, San Francisco, Chicago, and Seattle | Medium term (2-4 years) |

| Rising Outsourcing to Control Operating Expenditure | +1.0% | National, with strongest adoption in Sunbelt commercial corridors including Dallas, Phoenix, and Miami | Short term (≤ 2 years) |

| Increasing Emphasis on Energy-Efficient Operations | +0.9% | National, with regulatory influence spreading from California, New York, and Washington state | Medium term (2-4 years) |

| Accelerated Post-Pandemic Hybrid Workplace Adoption | +0.7% | National, with the largest effect in major CBD office markets including New York City, Chicago, Los Angeles, and Washington, D.C. | Short term (≤ 2 years) |

| Federal Push for Carbon-Neutral Government Facilities | +0.6% | National, concentrated in federal building hubs including Washington, D.C. metro, Atlanta, and Chicago | Long term (≥ 4 years) |

| Emergence of Data-Driven Predictive Maintenance | +0.5% | National, with strongest uptake in data center corridors including Northern Virginia, Phoenix, and Dallas, and in life sciences clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Smart, Connected Buildings

Smart building infrastructure is becoming a core operating layer in the United States integrated facility management market, rather than a separate technology upgrade. Smart-building node installations are projected to reach 115 million in 2026, which means more facilities are sending live operating data into day-to-day service workflows. That data now supports real-time HVAC optimization, occupancy-linked energy control, and predictive fault detection, which reduces the need for large manual inspection teams. As a result, many contracts are shifting away from labor-hour commitments and toward uptime, comfort, and energy-performance targets, which tends to favor larger vendors with stronger digital platforms. JLL reported that 28% of FM organizations embedded AI in operations in 2025, while the figure reached 46% among enterprises with more than 100,000 employees, and 92% had already piloted AI tools in real estate or FM functions.[1]JLL, “Global State Of FM Report 2025,” JLL, jll.com Johnson Controls reinforced that direction in April 2026 when it acquired Nantum AI to strengthen autonomous HVAC control, with the company pointing to energy savings above 10% per building.

Rising Outsourcing to Control Operating Expenditure

Cost pressure has become one of the clearest reasons buyers are moving deeper into the United States IFM market. JLL found in 2025 that 84% of CRE and FM leaders identified escalating costs and budget constraints as a top concern, while 81% said cost efficiency was a leading priority for the following year. That pressure matters most in first-time outsourcing, where organizations are moving from in-house delivery into bundled or fully integrated contracts and creating new addressable demand. IFMA reported a net 19% point shift toward greater outsourcing in its Q4 2025 FM Market Pulse, with utilities, healthcare, and professional services showing especially strong movement. Buyers are also becoming more selective in how they choose vendors, and JLL said 78% of organizations ranked deep business understanding as the top selection factor rather than the lowest unit rate. That preference supports longer contract relationships because providers that understand operations, compliance, and occupancy patterns are harder to replace once the service model is embedded.

Increasing Emphasis on Energy-Efficient Operations

Energy performance is moving into the center of the United States integrated facility management market because clients increasingly want operating savings that can be measured and reported. The U.S. Department of Energy Clean Energy Rule requires a 90% reduction in on-site fossil fuel-generated energy consumption for qualifying new federal construction from fiscal year 2025.[2]U.S. Department of Energy, “Clean Energy For New Federal Buildings And Major Renovations Of Federal Buildings,” Federal Register, federalregister.gov The same rule raises that requirement to a 100% reduction from fiscal year 2030, which extends the retrofit and compliance pipeline well beyond a single budget cycle. Federal procurement is also shaped by 10 CFR Part 436, where energy savings performance contracts are embedded as a recognized route for agencies to pursue long-term efficiency upgrades. Pressure is not limited to federal buildings because state-level building performance standards in California, New York, and Washington are also pushing private portfolios toward retrofit activity and tighter energy tracking. This is changing large RFPs because energy transparency and commissioning capability are becoming part of provider qualification, not just a value-added feature after the award.

Accelerated Post-Pandemic Hybrid Workplace Adoption

Hybrid work has changed the service profile of the United States IFM market, even where total occupied space has stopped expanding. A 2025 CBRE and CoreNet Global survey of 198 real estate professionals found that more than half planned to increase in-office attendance, which pointed to a more active workplace strategy rather than a simple retreat from office use. That shift is raising service intensity per square foot because occupiers are spending more on scheduling tools, air quality monitoring, workplace hospitality, and asset quality to support return-to-office goals. Facilities are also dealing with an uneven weekly occupancy curve, where Tuesday through Thursday demand peaks create staffing and service challenges that fixed single-shift models do not handle well. Eptura reported that only 4% of organizations had fully integrated workplace technology systems, while the average organization was still managing 17 separate platforms.[3]“Workplace Index,” Eptura, eptura.com That fragmentation gives integrated providers a clear contract upgrade opportunity because workplace systems, service delivery, and operating data still sit in too many disconnected layers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Vendor Landscape Limiting Standardization | -0.8% | National, most pronounced in multi-market portfolios spanning Southeast and Midwest secondary cities | Long term (≥ 4 years) |

| Shortage of Skilled MEP and HVAC Technicians | -0.7% | National, acute in Sunbelt high-growth metros including Austin, Phoenix, and Charlotte, and in rural and suburban markets | Medium term (2-4 years) |

| High Cybersecurity Risk in IoT-Enabled FM Platforms | -0.5% | National, concentrated in digitally advanced markets and in federal and defense facilities | Medium term (2-4 years) |

| Inflation-Driven Contract Cost Volatility | -0.4% | National, with the most visible pressure in high-wage and high-construction-cost metros including New York City, San Francisco, and Boston | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Vendor Landscape Limiting Standardization

Fragmentation remains a structural drag on the United States integrated facility management market because service delivery becomes harder to standardize when multiple vendors, systems, and local practices overlap. The problem becomes more severe in large portfolios where cleaning, security, engineering, catering, and workplace systems are still procured or tracked separately. Each additional interface increases the risk of inconsistent logs, delayed work orders, incomplete data transfers, and limited visibility into service-level compliance. International Facility Management Association has also emphasized the importance of integrated KPI visibility and audit traceability in modern FM operations, particularly as regulatory and internal reporting requirements continue to increase. As a result, fragmentation is no longer just an administrative challenge because it directly impacts cost control, operational performance tracking, and audit defensibility across large enterprise accounts.

Shortage Of Skilled MEP And HVAC Technicians

Technical labor shortages are constraining the United States integrated facility management market at the point where demand is strongest, especially in Hard FM and critical asset support. SMACNA reported that around 110,000 HVAC technician positions were unfilled in 2025, which shows how severe the staffing gap had become across the country.[4]Sheet Metal And Air Conditioning Contractors' National Association, “Beat the HVAC Technician Shortage” SMACNA, smacna.org The U.S. Bureau of Labor Statistics also recorded an average of 42,500 HVAC job openings each year over the prior decade, which indicates that the shortage is not a temporary issue. That pressure is most visible in MEP and HVAC delivery because providers need certified technicians to handle compliance-heavy work, and those roles are difficult to replace quickly. CBRE identified labor shortages as a top procurement risk for FM leaders, with wage competition from construction and energy employers making the talent problem harder to absorb. Larger providers are therefore in a stronger position because they can spread wage pressure across bigger contract bases, recruit nationally, and protect service levels more effectively than smaller firms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Soft FM Holds The Lead While Hard FM Expands Faster

Soft facility management segment held 56.28% of the United States integrated facility management market share in 2025, which made it the largest service category by revenue. In the United States IFM industry, that lead reflects the broad role of office support, security, cleaning, catering, and workplace experience services across outsourced contracts. These activities are now treated as a core part of occupier value rather than a peripheral support layer, especially in commercial and institutional settings where user experience matters more. Hard facility management segment, which covers asset management, MEP and HVAC services, fire systems and safety, and other technical functions, is projected to expand at a 5.83% CAGR through 2031. The US IFM market size for technical services is rising faster because energy rules, aging mechanical systems, and connected building controls are all pushing more work into non-discretionary maintenance budgets.

That split shows why soft services still drive volume while hard services often drive stickier contract economics and stronger margins. Within Hard FM, MEP and HVAC remain the most capacity-constrained areas because technician shortages are limiting how much of the available demand providers can actually serve. Within Soft FM, security is moving through a technology-led upgrade cycle as AI-enabled access control, remote monitoring, and integrated visitor systems replace older guard-heavy models in many buildings. That upgrade changes site economics because digital layers can improve oversight and standardization without relying on the same staffing mix used in legacy contracts. Johnson Controls' acquisition of Nantum AI in April 2026 captured the broader direction of travel, where analytics, building controls, and hard-services delivery are converging into a more differentiated technical offer.

By End User: Industrial Assets Anchor Revenue While Commercial Outsourcing Builds Momentum

The industrial and process segment accounted for 27.53% of the United States integrated facility management market share in 2025, which made it the largest end-user category. Its position is tied to cleanrooms, semiconductor fabrication facilities, pharmaceutical production, and food processing environments that require specialized technical coverage and strict operating discipline. Semiconductor onshoring is adding to that demand because new fab projects in Arizona, Texas, Ohio, and New York need both early operational support and long-duration service contracts once production starts. ABM's completion of the WGNSTAR acquisition in February 2026 directly reflected that opportunity, since the target specialized in cleanroom operations and production tool management for chip manufacturing environments. Healthcare is also proving attractive for larger providers, and Aramark's March 2026 Penn Medicine win showed how large and complex integrated contracts can become in multisite hospital systems.

The commercial segment is projected to grow at a 6.01% CAGR through 2031, which makes it the fastest-growing end-user group in the United States integrated facility management IFM market. The United States IFM market size for commercial accounts is benefiting from first-time outsourcing by mid-market occupiers that are reworking office footprints around hybrid attendance patterns. Hospitality, healthcare, institutional and public infrastructure, and other end users each bring a different contract mix, but all of them are placing more value on bundled delivery and more accountable operating models. Public infrastructure demand is also supported by federal modernization and energy performance contracting frameworks that favor long-term operational partnerships. This broader end-user spread matters because it lowers the market's dependence on any single real estate cycle and gives providers more ways to balance exposure across sectors.

Geography Analysis

The United States integrated facility management market was valued at USD 96.19 billion in 2025, and the country remains the sole geographic scope of this study. Demand patterns still vary widely by regional industry mix, the age of building stock, local regulation, and population movement. The Northeast held the largest regional revenue position, supported by dense urban portfolios, higher asset quality standards, and a heavy concentration of large commercial and institutional properties. Local rules such as New York City's Local Law 97 have also raised compliance expectations for larger buildings, which adds to the appeal of integrated delivery and stronger energy-management capability. Older building stock across cities such as New York, Boston, Philadelphia, and Washington, D.C. also creates recurring demand for complex MEP Services in U.S, which gives experienced multi-trade providers a structural edge.

Federal demand adds another stable layer in the Northeast and Mid-Atlantic because the government spends an estimated USD 8.1 billion each year on owned and leased office space, with a heavy concentration around the Washington, D.C. metro area. The Southeast is the fastest-growing regional pocket of the US IFM market, driven by population inflows into Florida, North Carolina, Georgia, and Tennessee. Those migration patterns are expanding commercial, healthcare, education, and public-service footprints that need more formalized facility support. Industrial relocation is also supporting the region because automotive plants, semiconductor suppliers, and distribution hubs are creating fresh multisite FM opportunities. The Southwest, especially Arizona and Texas, is becoming a specialized corridor for semiconductor fabrication and hyperscale data centers that require precision thermal management and clean environment support.

Johnson Controls' February 2026 agreement to acquire Alloy Enterprises showed how important liquid cooling and advanced thermal management have become in this part of the country, with the company pointing to thermal efficiency gains of up to 35% and pressure-drop reductions of up to 75%. The Midwest presents a mixed picture because office FM demand remains softer in Chicago and several other large cities, while industrial and renewable-energy work is providing a steadier base. California and the Pacific Northwest continue to lead in AI-enabled energy controls and advanced sustainability reporting, which keeps the western states at the front of technology-led FM adoption. Those western markets are also setting operating and compliance practices that many other regions tend to follow with a 2-3-year lag.

Competitive Landscape

The United States integrated facility management market is moderately concentrated at the top, with the 5 largest providers holding an estimated combined revenue share of 45-50%. CBRE, JLL, and Cushman and Wakefield hold strong positions in corporate real estate-linked contracts, where portfolio relationships and multi-site account infrastructure matter in large bids. ABM Industries and EMCOR Group are more prominent in engineering-heavy and technical service environments, where hard-services depth is often more important than real estate platform scale. EMCOR's revenue base illustrates how large the technical side of the market has become, with the company reporting USD 14.57 billion in fiscal 2024 revenue and projecting USD 16.1-16.9 billion for 2025. Even so, the provider field below the first tier remains fragmented, which leaves meaningful room for further consolidation.

A clear strategic theme in the United States IFM market is the convergence of building technology and service delivery. Honeywell's June 2024 completion of the USD 4.95 billion acquisition of Carrier's Global Access Solutions business showed that OEM and controls companies are moving deeper into security, access, and intelligent building infrastructure. FM providers are responding by building their own operating platforms so they can retain contracts, deepen scope, and prove performance more directly. ABM's Connect platform, which brings together IoT sensors, robotics, AI, and operating data, received an Edison Award in April 2026 and highlighted how providers are competing on technology capability as well as labor delivery. Cyber readiness is also becoming more important in federal and defense-linked procurement, where NIST-aligned practices are increasingly relevant for connected building environments.

White space is still most visible in semiconductor fabs, life sciences facilities, and hyperscale data centers, where demand is rising faster than the supply of specialized technical support. Mid-market first-time outsourcing is another opening because regional providers are still winning early contracts that larger operators may try to consolidate later through M&A. Outcome-based contracts are also reshaping competition because providers with stronger energy, uptime, and analytics records can defend premium pricing more easily. ABM's WGNSTAR acquisition and Johnson Controls' Nantum AI deal both point to the same direction of travel, where growth is moving toward cleanroom operations, predictive controls, and higher-value technical niches rather than standard labor-only delivery.

United States Integrated Facility Management Industry Leaders

CBRE Group, Inc.

Jones Lang LaSalle Incorporated (JLL)

Cushman & Wakefield plc

ABM Industries Inc.

ISS A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Johnson Controls acquired Nantum AI, a New York-based company specializing in AI algorithms for real-time HVAC optimization. Nantum's technology adjusted airflow based on occupancy data to deliver reported energy savings exceeding 10% per building. The acquisition expanded Johnson Controls' OpenBlue digital ecosystem with autonomous air-side and water-side control capability, with the first combined offering in pilot at higher education and healthcare campuses.

- April 2026: ABM was selected by Vanderbilt University to deliver end-to-end operational services at the institution's new 150,000-square-foot NYC campus at the General Theological Seminary in Manhattan, covering cleaning, maintenance, engineering services, subcontract oversight, HVAC, fire/life safety, elevators, pest control, and event coordination. ABM serves over 200 colleges and universities.

- March 2026: Aramark secured a multi-service agreement across Penn Medicine's 4,000-bed, seven-hospital system, described by the company as the largest single contract in its history, integrating AI-driven operational platforms and support services across all 7 hospitals.

- March 2026: ABM announced a multi-year partnership with the Philadelphia Phillies to deliver fully integrated facility engineering, maintenance, and cleaning services at Citizens Bank Park, utilizing the ABM Performance Solutions technology-enabled platform. The contract extended ABM's MLB footprint to 10 teams.

United States Integrated Facility Management Market Report Scope

The United States Integrated Facility Management Market Report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, Fire Systems and Safety, and Other Hard Facility Management Services], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and Other Soft Facility Management Services]), End User (Commercial [includes BFSI, IT and Telecom, Retail and Warehouses, etc.], Hospitality [includes Eateries, Restaurants and Large-Scale Hotels], Institutional and Public Infrastructure [includes Government Establishments, Education, Transportation such as Airports and Railways, etc.], Healthcare [includes Public and Private Healthcare Facilities], Industrial and Process Sector [includes Manufacturing, Energy including Oil and Gas Exploration, Mining, etc.], and Other End-User Industries [includes Multi-House Residential, Entertainment, Sports and Leisure]). The Market Forecasts are Provided in Terms of Value (USD).

| Hard Facility Management | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft FM | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management Services |

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process Sector |

| Other End-User Industries |

| By Service Type | Hard Facility Management | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft FM | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management Services | ||

| By End User | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process Sector | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

What is driving growth in United States integrated facility management services?

Growth is being supported by single-vendor outsourcing, smart-building adoption, tighter energy compliance, and hybrid workplace operating needs. The market is expected to rise from USD 115.03 billion in 2026 to USD 149.42 billion by 2031 at a 5.37% CAGR.

Why does Soft FM remain the largest service category in the United States?

Soft facility management segment held 56.28% share in 2025 because cleaning, security, catering, office support, and workplace experience services are widely embedded across outsourced contracts.

Why is Hard facility management segment growing faster than other service areas?

Hard FM is projected to grow at a 5.83% CAGR through 2031 because aging MEP systems, energy targets, and connected building controls are increasing technical maintenance needs.

Which end users create the strongest demand for integrated facility management in the United States?

Industrial and process assets led with a 27.53% share in 2025, while commercial accounts are growing fastest at a 6.0% CAGR as more mid-market occupiers move into first-time outsourcing.

What are the biggest risks providers need to manage?

The main pressures are fragmented vendor ecosystems, technical labor shortages, cyber exposure in connected buildings, and contract cost volatility. Technician shortages are especially important in HVAC and MEP services.

How concentrated is the competitive landscape in the United States?

The top 5 providers hold an estimated 45-50% combined revenue share, so the upper tier is meaningful but the broader provider base is still fragmented enough to leave room for consolidation.

Page last updated on: