China Integrated Facility Management Market Size and Share

Market Overview

| Study Period | 2024 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

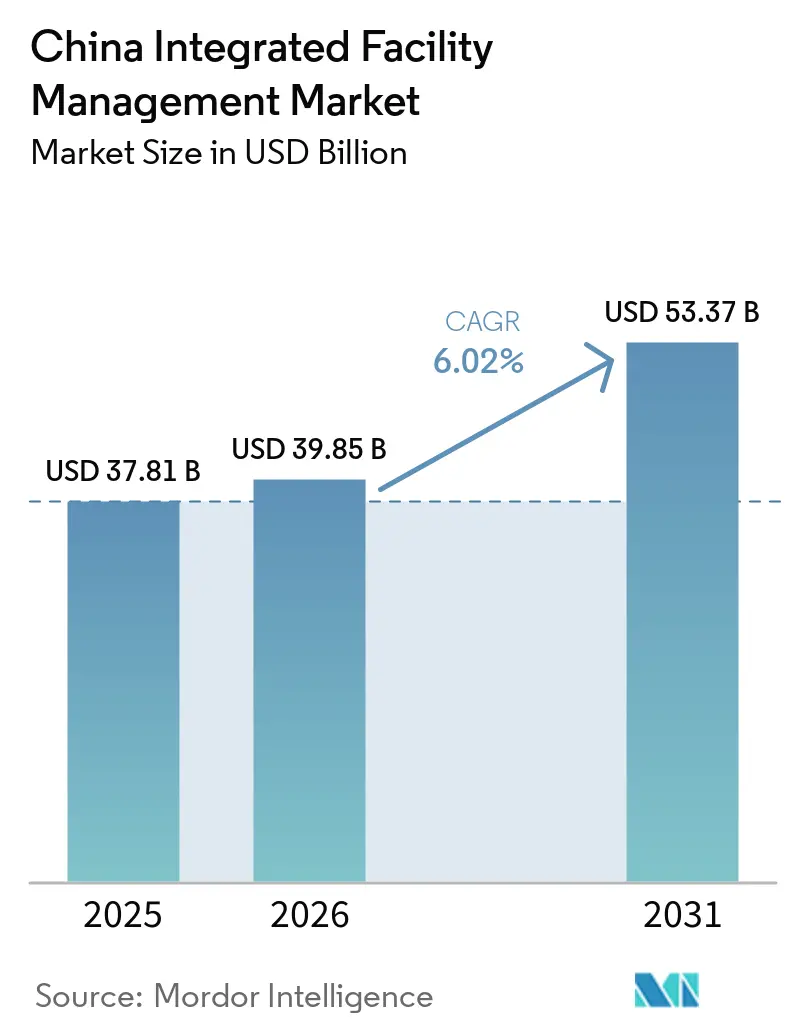

| Base Year Market Size (2025) | USD 37.81 Billion |

| Market Size (2026) | USD 39.85 Billion |

| Market Size (2031) | USD 53.37 Billion |

| Growth Rate (2026 - 2031) | 6.02% CAGR |

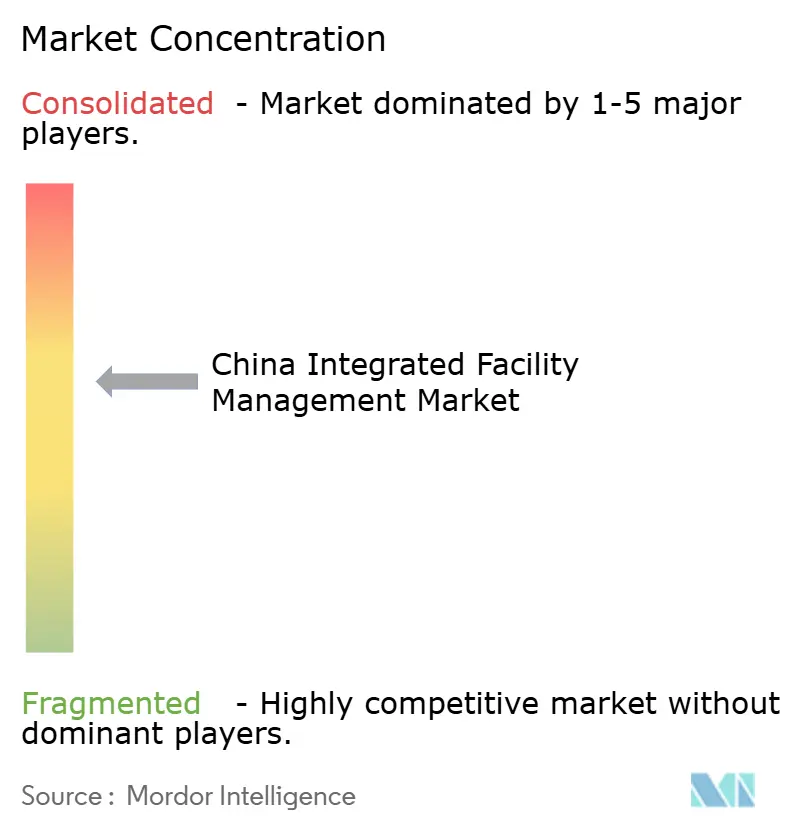

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Integrated Facility Management Market Analysis by Mordor Intelligence

The China Integrated Facility Management Market size was valued at USD 37.81 billion in 2025 and is estimated to grow from USD 39.85 billion in 2026 to reach USD 53.37 billion by 2031, at a CAGR of 6.02% during the forecast period (2026-2031).

The China integrated facility management (IFM) market is being supported by low outsourcing penetration, which leaves room for steady structural gains as more occupiers move away from in-house teams. Energy compliance is also changing the scope of work, because facility operators now need stronger monitoring, maintenance, and reporting capabilities across building systems. Demand is also widening across commercial campuses, industrial parks, logistics hubs, and data-intensive assets, which gives the China IFM market a broader base than a pure office-led cycle. Competitive activity remains active, with international firms defending large accounts and domestic providers expanding through specialization, technology deployment, and selective consolidation. Even with pressure from the property debt cycle on new supply and renovation pipelines, the China integrated facility management market still benefits from long-duration demand tied to outsourced operations, energy management, and service integration.

Key Report Takeaways

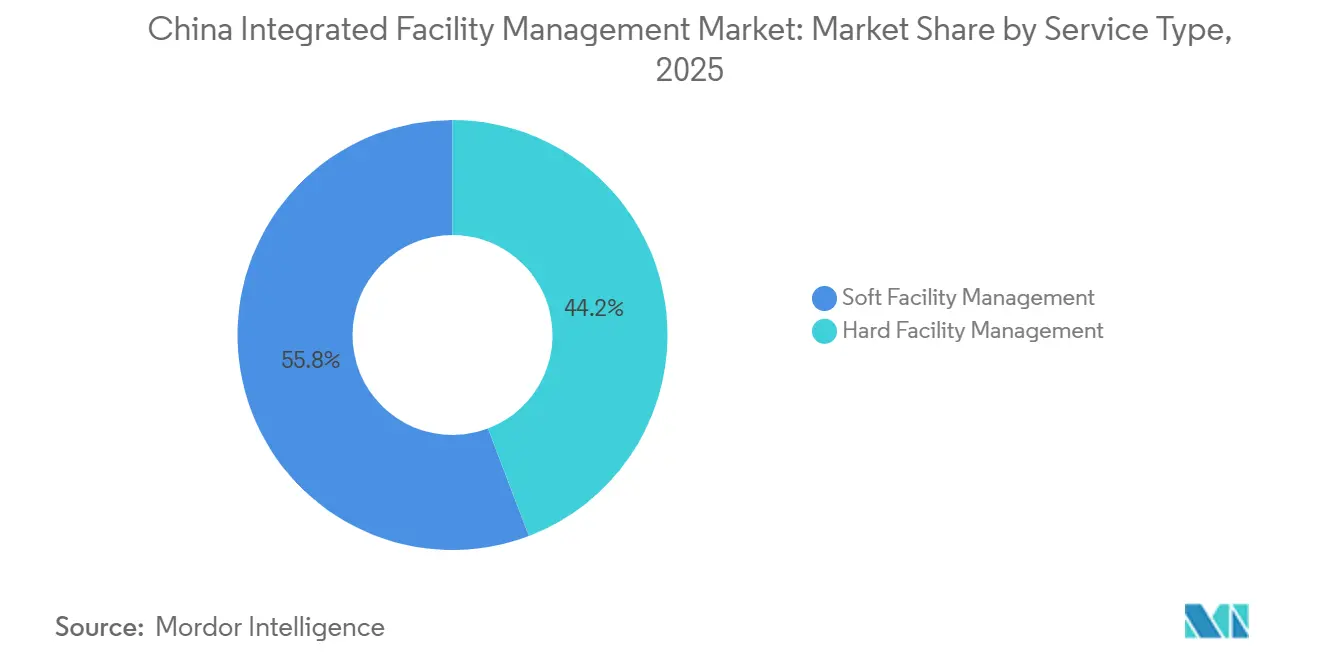

- By service type, Soft FM held 55.78% revenue share of the China integrated facility management market in 2025, while Hard FM is projected to expand at a 6.73% CAGR through 2031.

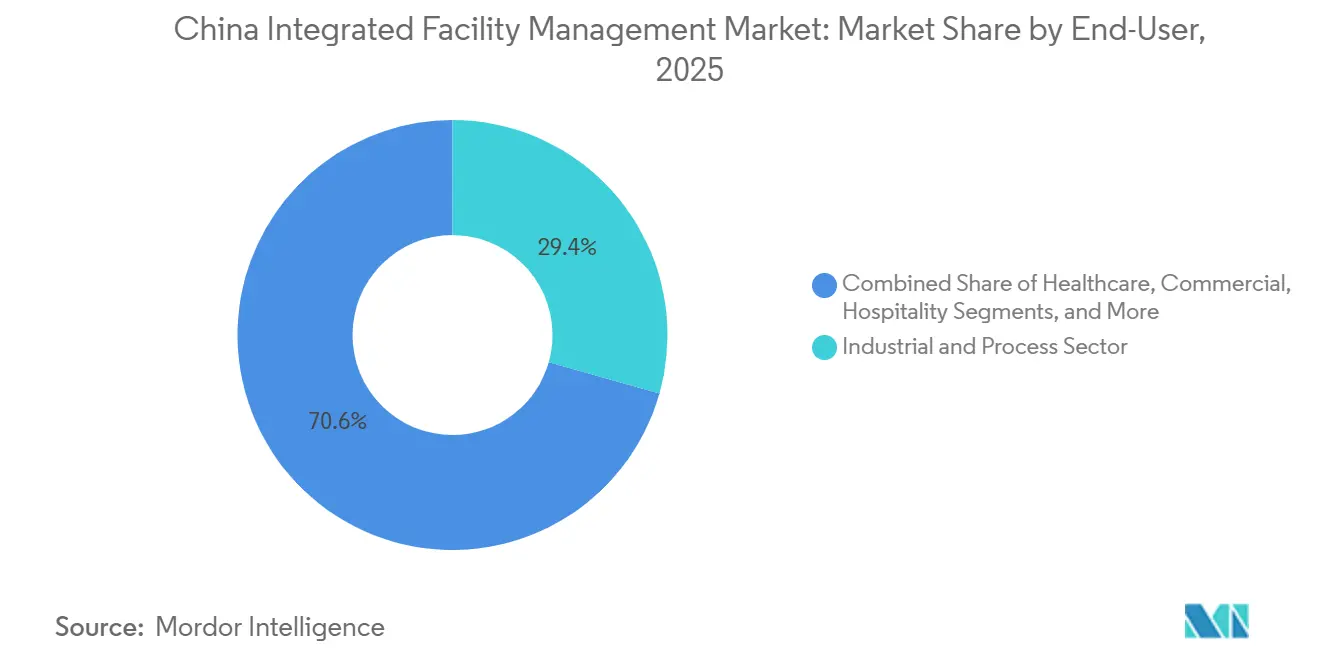

- By end-user, industrial and manufacturing held 29.38% revenue share of the China integrated facility management (IFM) market in 2025, while commercial is forecast to grow at a 6.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Integrated Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Growth of Real Estate, Office, and Data Centre Industries | +1.5% | National, concentrated in Yangtze River Delta, Greater Bay Area, and Beijing-Tianjin corridor | Short term (≤2 years) |

| Rising Outsourcing of Third-Party FM Services in China | +1.4% | National, strongest in Tier-1 and new first-tier cities, emerging in Tier-2 cities | Medium term (2-4 years) |

| Mandate of Energy Efficiency and Focus on Sustainable Solutions | +0.9% | National, accelerated in Shanghai, Shenzhen, and Zhejiang under provincial green FM standards | Medium term (2-4 years) |

| Acceleration of Urbanization and Growth of Real Estate Sector in China | +0.8% | National, with higher impact in Tier-2 and Tier-3 cities undergoing rapid urban expansion | Long term (≥4 years) |

| Improvement in Digital and Smart Solutions, Industry 4.0 Era | +0.6% | National, concentrated in smart-city pilot municipalities including Shenzhen and Hangzhou | Medium term (2-4 years) |

| Advancing Connectivity and Integration of Automation in Healthcare and Industrial Parks | +0.4% | National, concentrated in healthcare clusters and high-tech special economic zones | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rapid Growth of Real Estate, Office, And Data Centre Industries

Data centers are creating a distinct stream of demand in the China integrated facility management market because they need uninterrupted engineering support, tighter response windows, and stronger performance validation. This is different from conventional office facilities, where the service mix is broader, but the engineering threshold is often lower. The Data Center Green Development Action Plan set requirements around lower power usage effectiveness and rising renewable energy use, which has increased the need for energy management, cooling optimization, and electrical system oversight within hard FM services.[1]National Development and Reform Commission, “Data Center Green Development Action Plan,” National Development and Reform Commission, ndrc.gov.cn Office parks and corporate campuses continue to add to this demand channel, especially where technology, intelligent manufacturing, and new energy firms need stable and bundled support services. Providers that can handle specialized testing, cooling, compliance, and account management are therefore gaining stronger contract positions in the China integrated facility management (IFM) market.

Rising Outsourcing of Third-Party FM Services in China

The China integrated facility management market is also benefiting from a gradual shift toward third-party delivery, as occupiers seek clearer accountability and better service integration. This shift is visible in large enterprise portfolios, where providers are being asked to combine workplace services, maintenance, digital tools, and performance reporting within a single operating model. Recent product and contract launches show how outsourcing is moving beyond labour substitution and toward a platform-based operating approach.[2]JLL, “JLL Property Assistant,” JLL, jll.com Digital twin monitoring is also being used to support cleaning, maintenance, landscaping, and hygiene under one service structure.[3]Aden Group, “TotalEnergies China Headquarters Digital Twin Deployment,” Aden Group, adengroup.com As more occupiers seek bundled execution instead of fragmented procurement, the China IFM market is likely to reward vendors that can combine site delivery, digital visibility, and national account management.

Mandate of Energy Efficiency and Focus on Sustainable Solutions

Energy performance is becoming one of the strongest structural supports for the China integrated facility management market because building operations now sit closer to compliance and carbon targets. China’s buildings account for a significant share of national electricity use, which turns energy management from a cost-saving tool into an operating requirement with wider policy relevance.[4]Arm, “China Buildings and Electricity Use Under The Dual Carbon Framework,” Arm Newsroom, arm.com The Energy Law that took effect in January 2025 increased the need for monitoring systems, measurable conservation practices, and clearer accountability around facility energy performance, which expands the role of engineering-led FM services. In practice, this is pushing clients to combine maintenance, energy tracking, and operational reporting under one contract instead of treating them as separate tasks. That change strengthens the case for integrated delivery and gives the China integrated facility management (IFM) market a durable growth path in assets where efficiency, uptime, and reporting matter at the same time.

Acceleration Of Urbanization and Growth of Real Estate Sector in China

Urban expansion continues to widen the serviceable base for the China integrated facility management market, especially outside the most mature city clusters. This matters because Tier-2 and Tier-3 cities still have room for stronger formalization in outsourced building operations, particularly where non-residential assets are growing faster than local technical supply. Urban renewal also supports demand because aging properties need retrofits, maintenance planning, and system upgrades even when greenfield construction is softer. The geographic spread of newly secured third-party floor area across many cities shows that institutional and commercial demand is broadening geographically.[5]China Overseas Property Holdings, “2025 Interim Report,” China Overseas Property Holdings, copl.com.hk As this pattern spreads across more secondary cities, the China IFM market should gain from a wider mix of office, public, industrial, and mixed-use assets that require formal service delivery.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of Standardization in Pricing, Referencing, and Contracts | -0.7% | National, most acute in Tier-2 and Tier-3 cities where local vendors dominate procurement | Long term (≥4 years) |

| Complex Legal Requirements from National and State-Level Regulations | -0.6% | National, compliance burden amplified in special economic zones and regulated sectors | Medium term (2-4 years) |

| Lack of Large-Scale Procurement, Investment, and Pricing Norms | -0.4% | National, impacts mid-tier and smaller enterprises without formalized procurement frameworks | Medium term (2-4 years) |

| Low Compliance and High Variability in Enforcement of Rules and Regulations | -0.3% | National, concentrated in industrial zones and mixed-use developments with multi-jurisdictional oversight | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Lack Of Standardization in Pricing, Referencing, And Contracts

A lack of standard pricing and contract structures still slows the China integrated facility management (IFM) market because it keeps many tenders focused on lowest-cost selection. That approach makes it harder for buyers to distinguish between basic labour supply and genuinely integrated delivery with technical depth. When procurement leans too heavily on price, providers with stronger engineering or digital capability can struggle to defend margins even when their service quality is higher. This also creates weaker renewal dynamics, because clients may see inconsistent outcomes when contracts are awarded without clear quality benchmarks. Until contract templates, service definitions, and performance baselines become more consistent, the China integrated facility management market will continue to face friction in value-based procurement.

Complex Legal Requirements from National and State-Level Regulations

The legal framework around facilities services is becoming more demanding, and that raises execution costs across the China IFM market. Providers need to deal with overlapping rules on property management, labour, safety, energy, data handling, and environmental compliance, and those requirements do not always move at the same pace across cities. This burden is easier for large providers to absorb because they can spread compliance investment across a broader managed area and a deeper client base. Smaller regional firms often face greater pressure, especially when they try to expand into regulated sectors or multi-city accounts with higher documentation needs. Over time this will improve operating discipline, but in the near term it still acts as a brake on margin expansion and wider capability investment in the China integrated facility management market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Soft FM Leads While Hard FM Gains Speed Through Engineering Needs

Soft Facility Management (FM) held 55.78% of China integrated facility management (IFM) market share in 2025, which kept it as the largest service group across commercial, institutional, and campus environments. Cleaning, catering, and office support remained the most widely outsourced activities because they are visible, repetitive, and easier for occupiers to centralize under one vendor. This part of the China IFM market also benefits from the spread of larger enterprise campuses, where employers need consistent support services across more complex sites. As contracts become broader, clients are increasingly bundling front-of-house support, cleaning, workplace services, and selected compliance tasks into one package rather than sourcing them separately. That shift supports stable demand for Soft FM even as the service mix becomes more data-aware and process-driven.

Hard FM is the fastest-growing service category, with the China integrated facility management market size for this segment advancing at a 6.73% CAGR from 2026 to 2031. The growth is being driven by asset management, MEP services, HVAC oversight, and other engineering-intensive work tied to uptime, safety, and energy control. Data center policy has added to this demand because operators need tighter oversight of cooling, electrical systems, and performance tracking under formal efficiency targets. Fire systems and safety services are also becoming more specialized as clients look for documented maintenance, audit trails, and better fault response across mission-critical sites. Within the China integrated facility management industry, this leaves hard FM well placed to capture a larger share of new integrated contracts where technical assurance matters as much as routine service coverage.

By End-User: Industrial And Manufacturing Provide the Base While Commercial Moves Faster

Industrial and manufacturing accounted for 29.38% of China IFM market share in 2025, making it the largest end-user group. Large factory parks, semiconductor facilities, logistics hubs, and production campuses need permanent technical coverage, and that gives this segment a dependable volume base. Service failure in these sites can interrupt production, weaken safety outcomes, or raise energy losses, which is why buyers often place a premium on reliability and engineering competence. The China integrated facility management market, therefore, sees strong demand from industrial clients for predictive maintenance, utility management, cleanroom support, and disciplined contractor control. This makes industrial and manufacturing a stable anchor for providers that want longer-duration contracts and deeper site-level integration.

Commercial is the fastest-growing end-user segment, and the China integrated facility management (IFM) market size for this group is set to expand at a 6.55% CAGR through 2031. Office owners, retail operators, and mixed-use landlords are moving away from fragmented service buying and are showing stronger interest in performance-linked bundled contracts. Commercial clients are increasingly looking for real-time operating visibility alongside routine FM execution. Broader enterprise contracts also reflect a preference for integrated operating models that can align facilities management, workplace experience, and digital support. Commercial demand should therefore remain a faster-growth pocket of the China integrated facility management market as landlords try to improve tenant retention, operating control, and reporting quality.

Geography Analysis

Geographic market share figures were not disclosed, but demand in the China integrated facility management market remained most concentrated in the Yangtze River Delta, the Greater Bay Area, and the Beijing-Tianjin corridor in 2025. These clusters have the deepest base of office parks, commercial campuses, data centers, and industrial assets that can support integrated contracts. They also tend to carry tighter service expectations, which benefits providers with national account structures and stronger engineering depth. The data center buildout has further reinforced these geographies because mission-critical sites are more likely to require integrated energy, cooling, and maintenance support under formal efficiency targets. As a result, the China integrated facility management (IFM) market continues to draw its highest-value opportunities from city clusters where technical compliance and asset intensity are both high.

Tier-1 and new first-tier cities remain the most mature outsourcing zones, but the next layer of growth is moving into Tier-2 cities where formal integrated delivery is still less penetrated. This is important because many local providers in those markets remain smaller in scale and narrower in capability. That leaves room for regional expansion by firms that can bring standardized processes, digital monitoring, and broader service bundles. The expansion of independent third-party area across a large number of cities supports the view that demand is widening beyond a handful of coastal centers. The China integrated facility management market is therefore becoming more geographically dispersed even while premium contracts remain concentrated in the most developed urban corridors.

Shanghai, Shenzhen, and Zhejiang stand out in the China IFM market because green standards and smart building activity are pushing a more advanced mix of energy and digital services. Shenzhen and Hangzhou also fit the profile of smart-city municipalities where data-led operations can move faster from pilot use into larger service contracts. Industrial zones and healthcare clusters add another layer of geographic diversity, since they require stricter operating discipline than conventional office stock. This means future growth will come from a mix of mature coastal clusters, emerging secondary cities, and specialized non-residential zones rather than from any single building category or region alone.

Competitive Landscape

The China integrated facility management market had moderate concentration at the top in 2025, with Sodexo, JLL, CBRE, and Mitie together accounting for 30% of revenue while the rest was spread across a large and fragmented supplier base. This structure creates strong competition for national and multinational accounts, but it also leaves clear whitespace for providers that can scale beyond local delivery. The main dividing line is no longer basic service coverage alone. Buyers are increasingly comparing digital visibility, engineering competence, ESG reporting support, and the ability to manage multi-site portfolios with consistent standards. That change is raising the bar across the China integrated facility management (IFM) market and making sub-scale competition harder in larger tenders.

Strategic moves since 2025 show how leading companies are responding. Sodexo completed the acquisition of Compass Group’s mainland China subsidiaries in January 2025, which expanded its catering-led integrated FM footprint and strengthened client access in corporate and hospitality settings. JLL launched JLL Property Assistant in May 2025, adding an AI-enabled natural-language interface that connects facility operations with existing real estate systems for faster decision support. Aden Services also began managing TotalEnergies’ 35,000-square-meter China headquarters in June 2025 with a digital twin platform, showing how providers are using software visibility to support routine site execution. These actions point to a common pattern in the China IFM market, where technology is being used to deepen stickiness, improve reporting, and widen the range of services held within one contract.

Company positioning is also being shaped by the mix of property types each provider serves. Firms with heavy exposure to residential property management face tighter fee pressure and slower value expansion than those with stronger commercial, industrial, healthcare, or public-sector portfolios. Diversification across third-party clients in telecom, education, transportation hubs, and healthcare shows the importance of broadening beyond a narrow property base. Large enterprise accounts also highlight that clients now expect workplace, facilities, and digital support to be aligned rather than purchased in isolation. In this environment, the China integrated facility management market should continue to favour providers that combine service breadth with specialized engineering, digital tools, and the balance sheet to support larger accounts.

China Integrated Facility Management Industry Leaders

CBRE Group, Inc.

Jones Lang LaSalle Incorporated

Cushman & Wakefield plc

ISS A/S

Sodexo S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Commercial property operators across Shenzhen, Shanghai, and Beijing increased investment in ESG-linked facility upgrades, including carbon-monitoring platforms, intelligent lighting systems, and energy-efficient HVAC modernization programs, strengthening demand for integrated facility management providers with green-building compliance capabilities.

- April 2026: China’s hyperscale data-center expansion continued to support demand for technical integrated facility management services, particularly across Beijing, Shanghai, Guangzhou, and western computing hub regions, where operators increased investment in predictive maintenance, cooling optimization, and critical power infrastructure management.

- March 2026: Chinese facility management providers expanded AI-enabled building management deployments across Grade A commercial properties, integrating IoT sensors, centralized control platforms, and cloud-based maintenance systems to improve energy efficiency and reduce operational downtime.

- February 2026: State-owned enterprises and public infrastructure operators in China increasingly shifted toward bundled integrated facility management contracts instead of fragmented single-service outsourcing models, supporting wider adoption of centralized workplace management, technical maintenance, and sustainability-focused operations frameworks.

China Integrated Facility Management Market Report Scope

The China Integrated Facility Management Market Report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, Fire Systems and Safety, and Other Hard Facility Management Services], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and Other Soft Facility Management Services]), End User (Commercial (includes BFSI, IT and Telecom, Retail and Warehouses, etc.), Hospitality (includes Eateries, Restaurants and Large-Scale Hotels), Institutional and Public Infrastructure (includes Government Establishments, Education, Transportation such as Airports and Railways, etc.), Healthcare (includes Public and Private Healthcare Facilities), Industrial and Process Sector (includes Manufacturing, Energy including Oil and Gas Exploration, Mining, etc.), and Other End-User Industries (Multi-House Residential, Entertainment, Sports and Leisure)). The Market Forecasts are Provided in Terms of Value (USD).

| Hard Facility Management | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft Facility Management | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management Services |

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process Sector |

| Other End-User Industries |

| By Service Type | Hard Facility Management | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft Facility Management | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management Services | ||

| By End-User Industry | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process Sector | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

What is the current size and outlook for integrated facility management in China?

The China integrated facility management market was valued at USD 37.81 billion in 2025, stood at USD 39.85 billion in 2026, and is projected to reach USD 53.37 billion by 2031 at a 6.02% CAGR.

Which service segment leads revenue generation in China?

Soft FM led with a 55.78% revenue share in 2025 because cleaning, catering, and office support remained the most widely outsourced services across campuses and commercial properties.

Which service category is growing the fastest through 2031?

Hard FM is expected to expand at a 6.73% CAGR through 2031, supported by stronger demand for MEP, HVAC, safety, and energy-management services.

Which end-user group contributes the most demand?

Industrial and manufacturing held the largest revenue share at 29.38% in 2025, supported by factory parks, logistics hubs, and production sites that need permanent technical coverage.

Why is the commercial segment growing faster than other end users?

Commercial is projected to grow at a 6.55% CAGR through 2031 because landlords and operators are moving from single-service buying to bundled contracts with stronger reporting and operating control.

How concentrated is competition among facility management providers in China?

Competition remains moderate, with the top 4 international players holding 30% of revenue in 2025, which leaves substantial room for domestic specialists and regional operators.

Page last updated on: