Singapore Integrated Facility Management Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

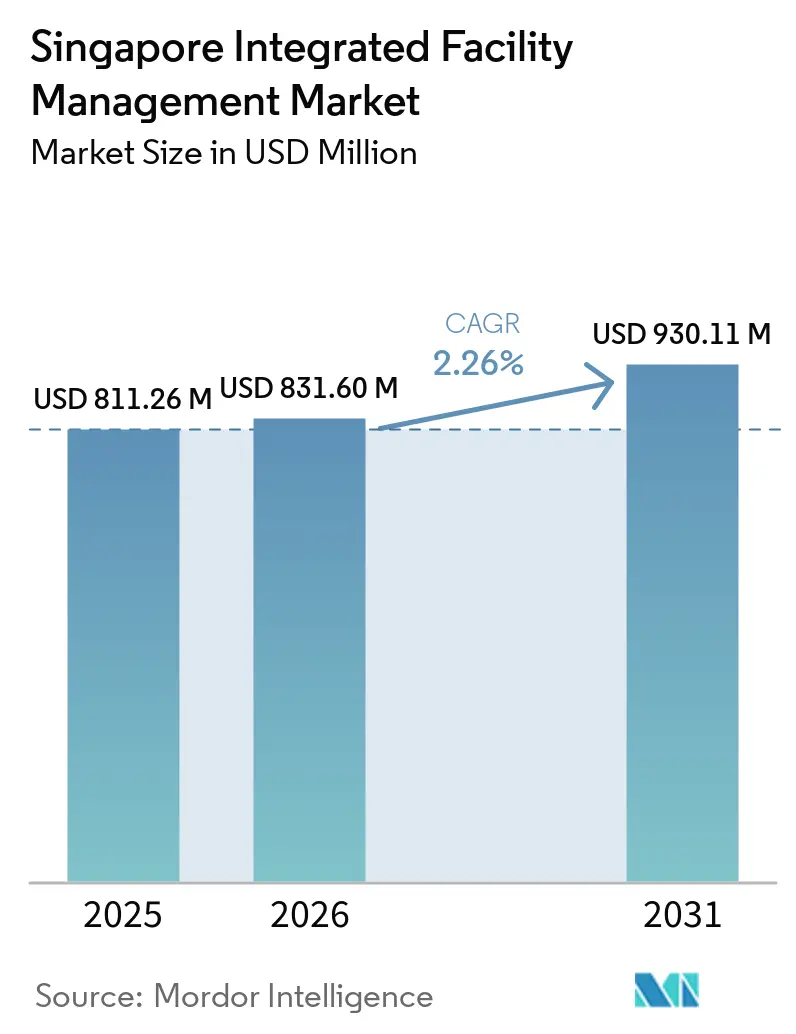

| Base Year Market Size (2025) | USD 811.26 Million |

| Market Size (2026) | USD 831.60 Million |

| Market Size (2031) | USD 930.11 Million |

| Growth Rate (2026 - 2031) | 2.26% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Singapore Integrated Facility Management Market Analysis by Mordor Intelligence

The Singapore Integrated Facility Management Market size is projected to expand from USD 811.26 million in 2025 and USD 831.60 million in 2026 to USD 930.11 million by 2031, registering a CAGR of 2.26% between 2026 to 2031.

The Singapore integrated facility management (IFM( market is moving on steady demand rather than rapid expansion, as building owners shift toward outcome-based contracts that combine compliance, energy performance, and day-to-day service delivery under one provider. Mandatory energy rules, higher carbon costs, and annual building data submissions are also changing the role of providers, as technical operators with verified energy management capability are now treated as compliance partners rather than solely as operating vendors. Competition remains split between multinational operators with strong digital systems and local firms that remain competitive through public-sector familiarity, accredited work heads, and established relationships in regulated tenders. At the same time, selective in-house control over building management systems for sensitive assets is limiting full outsourcing in certain technical areas, keeping the Singapore IFM market on a measured growth path. The result is that value in the Singapore integrated facility management market is shifting away from labour volume toward analytics, energy savings, automation, and deeper integrated service.

Key Report Takeaways

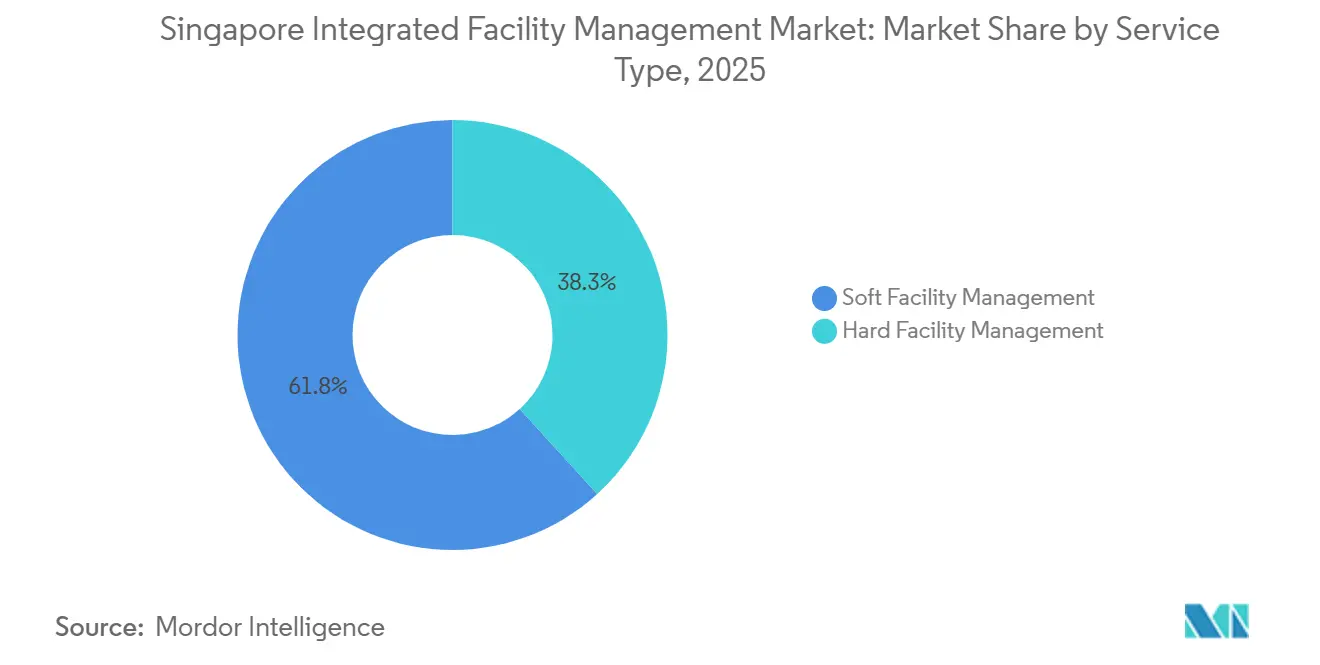

- By Service Type, Soft Facility Management held 61.75% of the revenue share of the Singapore integrated facility management market in 2025, while Hard Facility Management recorded the fastest projected CAGR of 2.88% through 2031.

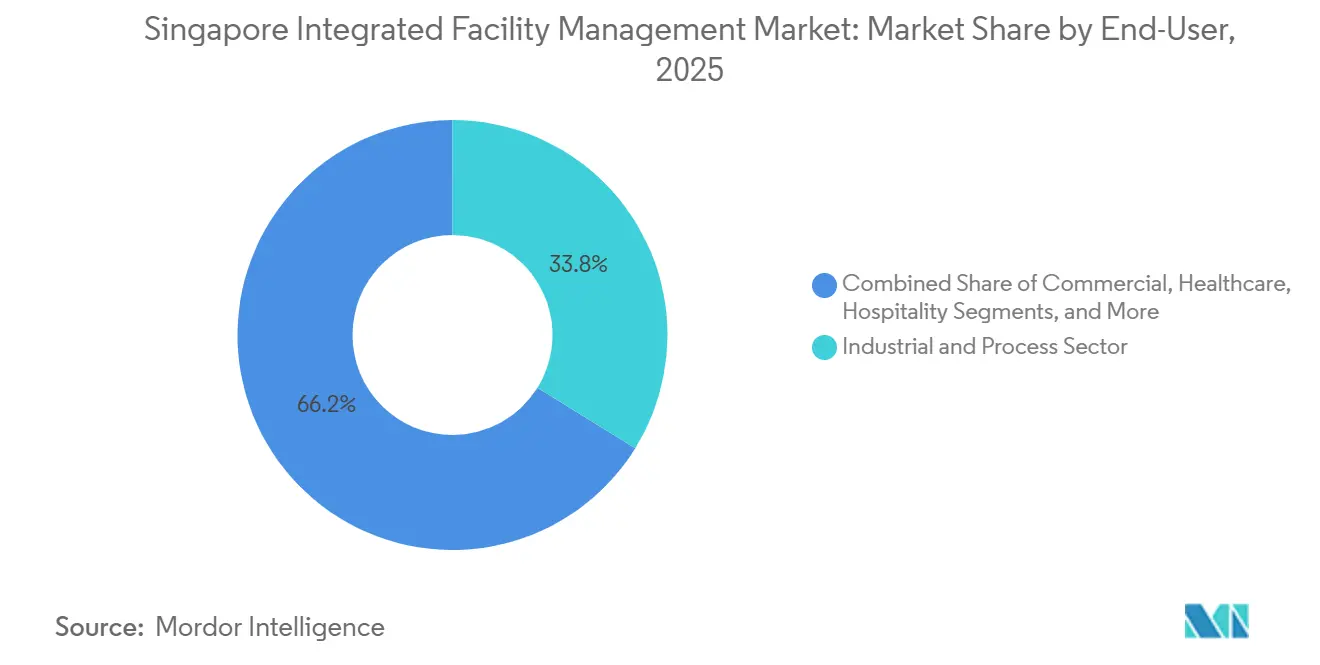

- By End-User, Industrial accounted for 33.84% of the value of the Singapore integrated facility management (IFM) market in 2025, while Commercial posted the highest projected CAGR of 3.01% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Singapore Integrated Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Government Push for Smart Green Buildings | +0.5% | Singapore-wide, concentrated in CBD, institutional campuses, and healthcare clusters | Short term (≤2 years) |

| Mandatory Preventive Maintenance Requirements and HSE Regulations | +0.4% | Singapore-wide, the highest density in commercial, healthcare, and industrial buildings ≥ 5,000 m² GFA | Short term (≤2 years) |

| Corporate ESG Push Driving Outsourcing of Facility Services | +0.4% | Singapore-wide, strongest in MNC-tenanted Grade A offices and REIT-managed portfolios | Medium term (2-4 years) |

| AI and IoT Integration for Predictive Maintenance | +0.3% | Singapore-wide, concentrated in industrial, datacenter, and transport infrastructure assets | Medium term (2-4 years) |

| Process Digitalization and Regulatory Compliance for Shared Services | +0.2% | Singapore-wide, accelerated by BCA FM01 and SIFMA accreditation requirements | Medium term (2-4 years) |

| Shift Toward Integrated In-House IFM Solutions in Asia | +0.2% | Singapore-wide, strongest in government agencies and data-center operators | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing Government Push for Smart Green Buildings

The Singapore integrated facility management market is benefiting from the government’s direct push to improve the energy performance of existing buildings. Singapore’s building sector accounted for more than 20% of national carbon emissions, which keeps energy efficiency high on the policy agenda and supports long-term demand for technical service providers that can deliver measurable outcomes.[1]Building and Construction Authority, “Environmental Sustainability Measures for Existing Buildings,” Building and Construction Authority, bca.gov.sg The Building Control (Environmental Sustainability Measures for Existing Buildings) (Amendment) Regulations 2025 took effect on September 30, 2025, and imposed Energy Use Intensity thresholds of 200 kWh/m²/year for offices, 495 kWh/m²/year for retail, and 360 kWh/m²/year for hospitals.[2]Attorney-General’s Chambers Singapore, “Building Control (Environmental Sustainability Measures for Existing Buildings) (Amendment) Regulations 2025,” Singapore Statutes Online, sso.agc.gov.sg Buildings that exceed those thresholds must appoint a qualified energy auditor, submit an Energy Efficiency Improvement Plan, and deliver a 10% reduction within 3 years, which expands the technical scope of FM contracts and supports recurring specialist work. The Green Mark Incentive Scheme for Existing Buildings 2.0 also lowers the financial barrier for retrofit activity by co-funding up to 50% of retrofit capital expenditure, which makes performance-linked FM contracts easier for owners to adopt. Singapore had greened 61% of its building stock by May 2026, and the remaining gap to the 80% target by 2030 leaves a clear near-term pipeline for retrofit-linked service mandates in the Singapore integrated facility management (IFM) market.[3]COP30 Singapore Pavilion, “Singapore Green Building Progress and Building Stock Target,” COP30 Singapore Pavilion, cop.gov.sg

Mandatory Preventive Maintenance Requirements and HSE Regulations

The Singapore IFM market also benefits from a stringent regulatory environment that makes preventive maintenance difficult to defer. Building owners must manage overlapping obligations covering workplace safety, fire safety certification, lift servicing, escalator servicing, and cooling system maintenance, which increases the appeal of a single integrated provider that can coordinate those routines under one operating model. The BCA FM01 work head framework narrows the eligible pool for public sector maintenance contracts because M1-grade applicants must hold SGD 2 million (USD 1.5 million) in paid-up capital and at least SGD 40 million (USD 30 million) in a verified IFM project track record. That screening effect supports margin discipline for larger accredited operators in the Singapore integrated facility management market, especially where clients value reliability over lowest-cost bidding. Government tender requirements also reinforce that pattern because operators that cannot meet recognized safety standards are less likely to qualify for high-value preventive maintenance work. In practice, this turns compliance calendars into a recurring revenue base for established firms that can handle multiple regulators, technical trades, and reporting obligations without disruption.

Corporate ESG Push Driving Outsourcing of Facility Services

The Singapore integrated facility management (IFM) market is also being pushed by the closer link between corporate sustainability reporting and day-to-day facility operations. Singapore Exchange sustainability reporting requirements have made emissions tracking, resource use, and operating transparency more important for listed companies and real estate portfolios. That shift is changing bid requirements, since providers are increasingly expected to show live energy dashboards, waste tracking capability, water monitoring, and recognized environmental management systems alongside standard safety credentials. Large office and mixed-use portfolios are responding by moving from narrow service packages toward multi-year integrated contracts that can absorb reporting, operational control, and performance verification within one structure. OCS Singapore’s published ESG blueprint for commercial buildings showed how inspection discipline, energy monitoring, and material conservation are being positioned as the delivery mechanism for ESG commitments rather than a supporting back-office task. This strengthens the role of integrated providers in the Singapore integrated facility management market because contracts increasingly sit closer to board-level reporting and tenant accountability than they did a few years ago.

AI And IoT Integration for Predictive Maintenance

Digital tools are reshaping the Singapore IFM market, especially in technical assets where downtime carries high operating and compliance costs. Smart building systems, connected sensors, and building management platforms are allowing providers to move from fixed maintenance schedules toward fault prediction, condition monitoring, and faster escalation of equipment problems. This matters most in industrial sites, transport facilities, and data-center assets where uptime, response time, and documented service history influence contract renewal. Primustech’s April 2026 launch of AiBE, a large language model trained for facility management workflows, showed that the local market is moving beyond isolated sensor deployments toward wider integration across SOP management, BMS and CMMS workflows, and tenant service functions. As these systems mature, the Singapore integrated facility management market is likely to reward operators that can blend field execution with usable digital intelligence rather than those that only add dashboards on top of traditional labour models. The same trend is also raising expectations around data quality, response coordination, and asset-level visibility across large portfolios.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Qualified FM Workforce Limiting Service Scalability | -0.5% | Singapore-wide, most acute in industrial zones and healthcare facilities requiring certified M&E technicians | Short term (≤2 years) |

| Data Privacy and Cybersecurity Risks in Smart Building Systems | -0.3% | Singapore-wide, concentrated in data centers, government buildings, and critical infrastructure | Medium term (2-4 years) |

| Cybersecurity and Regulatory Compliance Complexity | -0.2% | Singapore-wide, the highest exposure in OT-connected facilities in energy, transport, and healthcare | Medium term (2-4 years) |

| Workforce Mobility Constraints and Talent Retention Challenges | -0.2% | Singapore-wide, intensified by foreign worker quota restrictions in cleaning and maintenance trades | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Shortage Of Qualified FM Workforce Limiting Service Scalability

Labor remains the clearest structural limit on how fast the Singapore integrated facility management (IFM) market can scale. Singapore’s labour market recorded a vacancy-to-unemployed ratio of 1.58 in December 2025, and 24.3% of employers reported skills gaps that increased workloads and affected service quality. In facility management, the pressure is sharper because labour accounts for 40% to 50% of operating costs, and many hard FM contracts require certified technicians, mechanical engineers, and energy auditors who are not easy to replace. The aging domestic technical workforce and weaker entry of younger workers into trade roles are adding to the problem, while foreign worker limits make large-scale staffing responses difficult. That combination restrains how much new business providers can absorb, even when demand is present, because contract mobilization depends on qualified people rather than only sales capacity. BCA Academy’s specialist training programs support the medium-term pipeline, but they do not fully relieve the near-term staffing constraint facing the Singapore integrated facility management market.

Data Privacy and Cybersecurity Risks in Smart Building Systems

As the Singapore integrated facility management market becomes increasingly digital, cybersecurity risk is becoming an operational issue rather than a separate IT concern. Building management systems, IoT devices, cloud-based dashboards, and tenant-facing platforms create larger attack surfaces for operators managing critical facilities and sensitive client data. Singapore recorded 159 ransomware cases in 2024, up 21% year over year, with manufacturing and professional services among the most targeted sectors, both of which are important end-user groups for outsourced FM. The compliance burden is also rising because operators handling tenant information, access credentials, and building sensor data must align with the Personal Data Protection Act and the OT Cybersecurity Masterplan 2024. That pushes investment needs upward in network segmentation, multi-factor authentication, device lifecycle management, and vulnerability control, which is harder for mid-sized firms to absorb. The result is a market where digital capability helps providers win work, but weak cyber controls can also shut them out of smart-building and critical-infrastructure mandates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard FM's Compliance-Driven Acceleration Narrows the Gap with Soft FM

Hard Facility Management (FM) is the fastest-growing service line in the Singapore integrated facility management (IFM) market, with the Singapore IFM market size for this segment set to rise at a 2.88% CAGR from 2026 to 2031. That pace is tied to the September 2025 MEI regime, which turns energy performance from a discretionary upgrade topic into a timed compliance requirement for large buildings above 5,000 m² gross floor area. Once buildings cross prescribed energy intensity thresholds, owners must engage qualified specialists and document improvement actions, which gives hard FM providers a recurring role in audits, mechanical optimization, system tuning, and follow-up reporting. KONE’s connected elevator services in Singapore, which improved proactive fault identification by 70% and reduced callouts by 40% in the first 2 years of deployment, show how technical operators are moving from scheduled visits toward continuous monitoring contracts that increase revenue per asset. The Singapore integrated facility management industry also benefits from local operating conditions because high humidity and long annual cooling hours make HVAC upkeep difficult to defer without affecting comfort, efficiency, and building compliance.

Soft FM remained the volume leader and held 61.75% of the Singapore IFM market share in 2025. Its lead reflects the breadth of work covered across cleaning, security, landscaping, pest control, concierge, and related site services that appear in almost every asset class. In the Singapore integrated facility management industry, this service group remains deeply embedded in commercial buildings, public spaces, logistics facilities, and hygiene-sensitive environments that require steady execution every day. The cost profile is changing, however, because wage regulation in cleaning and security is pushing operators to defend margins through robotics, process redesign, and outcome-based pricing rather than through higher labour deployment alone. OCS Singapore’s November 2024 arrangement with SoftBank Robotics and the Environmental Services Industry Transformation Map 2025 both point in that direction, with productivity, automation, and labour efficiency shaping the next phase of competition in soft FM.

By End-User: Industrial Sector Anchors Scale While Commercial Drives Forward Velocity

The industrial segment accounted for 33.84% of the Singapore integrated facility management market size in 2025, making it the largest end-user group by value. This position is rooted in the continuous operating requirements of semiconductor plants, logistics warehouses, workshops, technology parks, and other facilities where equipment uptime and safe plant conditions are closely tied to production continuity. Industrial zones such as Jurong, Tuas, and Woodlands create dense clusters of technical assets, which helps service providers build route efficiency and specialist teams around repeatable MEP, fire-safety, and environmental service routines. JLL reported that Singapore’s All Industrial Rental Index rose 2.4% year over year in 4Q 2025, while electronics and semiconductor indicators pointed to healthier business conditions, which supports stable utilization of industrial real estate and steady demand for outsourced operations. OCS’s management of a 22,500 sqm Tier-III data center through a single-vendor IFM model also shows how industrial-type mandates in and around Singapore increasingly favour consolidated governance over fragmented specialist contracting.

Commercial real estate is the faster-moving segment in the Singapore IFM market, projected to expand at a 3.01% CAGR through 2031. Grade A offices, retail plazas, and mixed-use assets are shifting from transactional cleaning and maintenance packages toward bundled contracts that combine occupancy support, energy reporting, asset care, and tenant-facing service metrics within one agreement. That transition is strongest in REIT-managed and institutionally owned portfolios where owners can evaluate providers on total operating outcomes rather than line-by-line staffing schedules. The Singapore integrated facility management industry is also seeing support from public sector, healthcare, and institutional assets, which may be smaller than industrial and commercial in share but provide stable, multi-year demand with higher compliance intensity. Hospitals, clinics, nursing homes, and education campuses especially favour operators that can combine infection control routines, planned maintenance discipline, and regulated reporting under one management layer. This means the commercial segment is driving forward momentum, while government, healthcare, and institutional accounts remain important anchors for recurring revenue and operating credibility.

Geography Analysis

The Singapore integrated facility management market is forecast to expand at a 2.3% CAGR through 2031, and that growth is concentrated within a compact national footprint where different districts create distinct service needs. The city-state’s small land area allows providers to serve commercial, industrial, healthcare, institutional, and transport assets under one regulatory system, which improves route density and makes integrated service deployment more efficient than in larger regional markets. Singapore had greened 61% of its building stock by May 2026 and was targeting 80% coverage by 2030, which keeps retrofit activity and compliance-linked operating demand visible across the local building base.

The Central Business District and the Marina Bay corridor form the core zone for commercially structured IFM contracts in Singapore. This cluster has a high concentration of Grade A office towers, mixed-use assets, transit-linked buildings, and dense tenant populations, which makes service-level performance, energy reporting, and real-time issue resolution central to contract design. Providers competing in this part of the Singapore integrated facility management (IFM) market usually need strong digital workflows because owners and tenants expect measurable outcomes instead of labour-based reporting. The western belt around Jurong Lake District, Jurong Island, Tuas, Pioneer, and nearby logistics nodes carries the strongest technical bias, with hard FM demand driven by petrochemicals, semiconductors, warehousing, and other uptime-sensitive operations. These assets rely on continuous mechanical, electrical, chilled water, fire-safety, and compliance oversight, so the service mix in the west tends to be more engineering-intensive than in the office-led core.

The northern and eastern corridors are becoming more important to the Singapore IFM market as digital infrastructure and advanced industrial activity spread outward. Seletar Aerospace Park, Changi Business Park, Woodlands Regional Centre, and the data-center zones along the east coast are creating a wider set of mandates tied to aerospace support, digital operations, and high-specification technical environments. JTC’s Open Digital Platform at Punggol Digital District is particularly important because it provides a working model for smart estate management that links infrastructure, analytics, and operating response in one ecosystem. As that template broadens, providers that can scale across CBD office portfolios, western industrial assets, and emerging digital districts will be better placed to capture the next wave of integrated mandates in the Singapore integrated facility management market.

Competitive Landscape

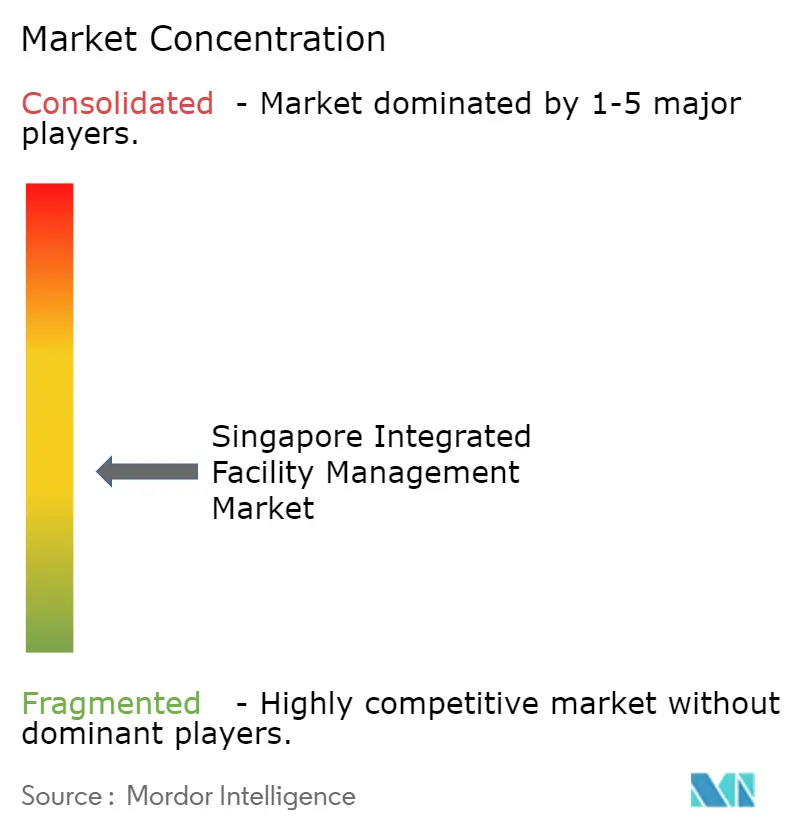

The Singapore integrated facility management market remains moderately fragmented, with large multinational firms competing for broad portfolio mandates while hundreds of local providers stay active in single-service and subcontracted scopes. This structure reflects the coexistence of high-entry technical work, where accreditations and capital matter, and labour-led routine work, where local familiarity and price responsiveness still carry weight. Larger operators are taking share where clients want one contract, one operating dashboard, and one accountable party across cleaning, maintenance, engineering, security, and tenant services. Smaller firms remain relevant in niche packages, but the balance is moving toward providers that can combine digital visibility, accredited delivery, and scale across multiple sites. The Singapore integrated facility management (IFM) market is therefore not consolidating rapidly, but it is becoming more selective in the parts of the value chain tied to energy compliance, smart buildings, and public tenders.

A large part of the competitive moat now comes from compliance-based filters. SIFMA’s CFMC accreditation framework, BCA’s FM01 work head grading, and the link between certification status and grant eligibility under GMIS-EB 2.0 make it harder for smaller uncertified operators to compete for complex integrated work. That matters because buyers in the Singapore IFM market are increasingly screening providers before price discussions begin, especially in government-linked assets and institutional portfolios. Multinational operators also compete through proprietary digital platforms that help them win outcome-based deals where response time, asset health data, and performance guarantees matter more than headcount promises. This has widened the gap between firms that can fund automation, cyber controls, and specialist talent and firms that still depend on labour-heavy service models.

Strategic moves by leading players show where competition is headed. Certis expanded its digital operating stack in 2026 through partnerships with Ensign InfoSecurity, FieldAI, Nuvola Media, and H2O.ai, which strengthened its position in robotics, consolidated dashboards, and AI-enabled service orchestration for complex facilities. Keppel secured more than USD 7.1 billion in long-term contracted revenue for decarbonization and sustainability solutions in February 2026, including work linked to Singapore’s first fully integrated thermal grid serving more than 25 developments, which reinforces its role in long-duration energy-linked facility infrastructure. ISS also renewed and expanded a Southeast Asia public healthcare contract valued at DKK 1.0 billion, equivalent to USD 145 million, over 5 years from July 2025, showing the continuing importance of large regional framework contracts in healthcare-linked operations. At the same time, in-house control over sensitive BMS and OT systems in government and data-center environments is creating room for hybrid FM models, where providers supply analytics, field support, and certified manpower while the client retains direct control over the most sensitive systems.

Singapore Integrated Facility Management Industry Leaders

C&W Services (S) Pte. Ltd.

ISS A/S

CBM Pte. Ltd.

ENGIE Services Singapore Pte. Ltd.

CBRE Group, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Certis Group partnered with Ensign InfoSecurity to strengthen cybersecurity governance in AI-driven robotic deployments. This collaboration directly addresses the escalating OT security risk in IoT-connected IFM operations, where compromised building management systems can expose critical infrastructure to ransomware and state-sponsored intrusion.

- April 2026: Primustech launched AiBE, the first large language model, LLM, specifically trained for facility management, as reported by the Business Times. AiBE integrates three modules, Scholar, for document and SOP management, Operator, for BMS and CMMS integration and cross-building analytics, and Dweller, for tenant service management, directly targeting Singapore's chronic problem of FM knowledge loss as experienced technicians age out of the workforce.

- February 2026: Keppel is locked in over USD 7.1 billion in long-term contracted revenue for decarbonization and sustainability solutions after securing USD 600 million in new contracts. Singapore-specific awards included the development of the country's first fully integrated thermal grid linking the Fusionopolis 2A, Biopolis, and Mediapolis chilled-water plants, serving more than 25 developments, a contract structure that embeds Keppel as an essential FM infrastructure partner for Singapore's largest research and biomedical precinct for over a decade.

- February 2026: Certis Group and FieldAI, US, formed a strategic partnership to deploy autonomous robotics in security and facilities operations, integrating FieldAI's AI autonomy stack with the Certis Mozart™ orchestration platform. FieldAI opened a Singapore office to support deployment, targeting public infrastructure, transport hubs, commercial facilities, and industrial sites.

Singapore Integrated Facility Management Market Report Scope

The Singapore Integrated Facility Management Market Report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, Fire Systems and Safety, and Other Hard Facility Management Services], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and Other Soft Facility Management Services]), End User (Commercial (includes BFSI, IT and Telecom, Retail and Warehouses, etc.), Hospitality (includes Eateries, Restaurants and Large-Scale Hotels), Institutional and Public Infrastructure (includes Government Establishments, Education, Transportation such as Airports and Railways, etc.), Healthcare (includes Public and Private Healthcare Facilities), Industrial and Process Sector (includes Manufacturing, Energy including Oil and Gas Exploration, Mining, etc.), and Other End-User Industries (Multi-House Residential, Entertainment, Sports and Leisure)). The Market Forecasts are Provided in Terms of Value (USD).

| Hard Facility Management | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft Facility Management | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management Services |

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process Sector |

| Other End-User Industries |

| By Service Type | Hard Facility Management | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft Facility Management | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management Services | ||

| By End User Industry | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process Sector | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

What is the current size of the Singapore integrated facility management market?

The Singapore integrated facility management market was valued at USD 811.6 million in 2025, reached USD 831.6 million in 2026, and is projected to reach USD 930.1 million by 2031 at a 2.26% CAGR.

Which service category leads demand in Singapore integrated facility management?

Soft FM remained the largest service category in 2025 with a 61.75% revenue share, supported by broad use across offices, industrial sites, retail assets, and public facilities.

Why is hard FM growing faster in Singapore?

Hard FM is projected to grow at 2.88% CAGR through 2031 because energy rules, preventive maintenance requirements, and uptime needs are increasing demand for engineering-led technical services.

Which end-user group contributes the most revenue in Singapore?

Industrial facilities led in 2025 with a 33.84% share, backed by semiconductor plants, logistics hubs, technology parks, and other sites that need continuous MEP and fire-safety support.

What is driving outsourcing decisions among Singapore building owners?

Owners are moving toward integrated outsourcing because energy compliance, carbon reporting, sustainability targets, and multi-regulator maintenance obligations are easier to manage through outcome-based IFM contracts.

What is the main risk facing providers in Singapore integrated facility management?

The biggest risk is limited service scalability due to a shortage of qualified technical labor, while cybersecurity requirements are also becoming more important as building systems become more connected.

Page last updated on: