Video Interviewing Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

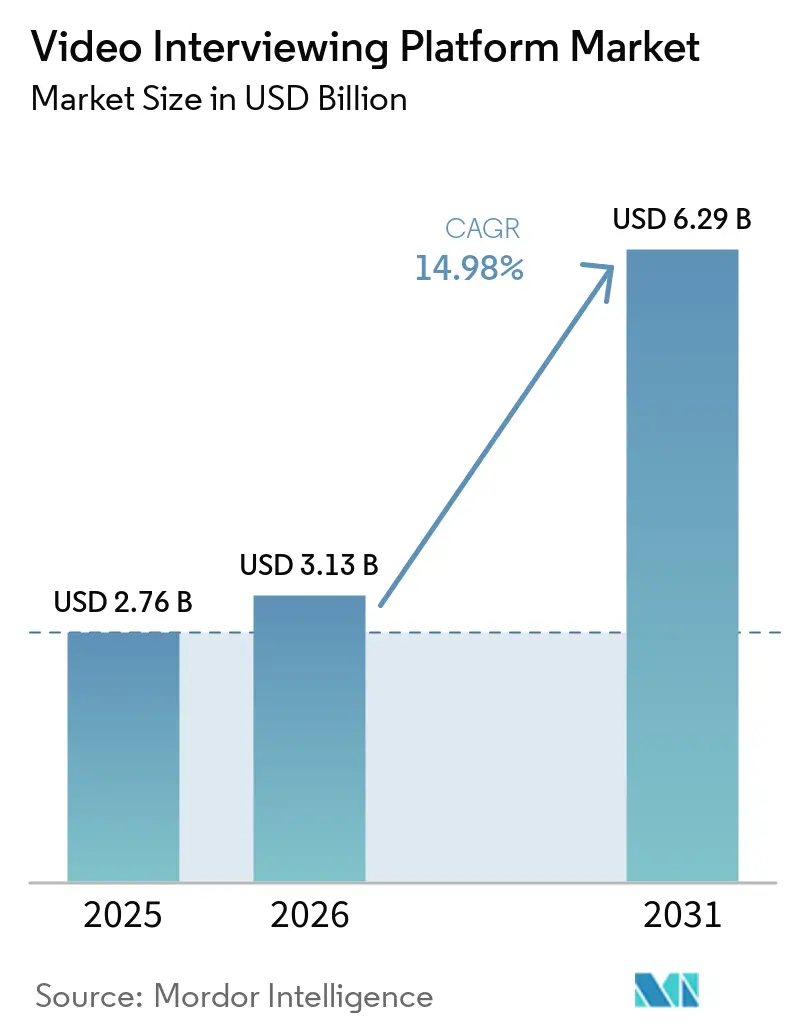

| Market Size (2026) | USD 3.13 Billion |

| Market Size (2031) | USD 6.29 Billion |

| Growth Rate (2026 - 2031) | 14.98% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Video Interviewing Platform Market Analysis by Mordor Intelligence

The Video Interviewing Platform Market size was valued at USD 2.76 billion in 2025 and estimated to grow from USD 3.13 billion in 2026 to reach USD 6.29 billion by 2031, at a CAGR of 14.98% during the forecast period (2026-2031). The current expansion of the video interviewing platform market is tied to a more permanent reset in hiring operations, because hybrid and distributed work now sit inside long-term talent acquisition design rather than short-term contingency planning. Buyer behavior also shows that the video interviewing platform market has moved deeper into the core HR stack, with procurement teams favoring multi-year renewals, tighter applicant-tracking integrations, and broader workflow coverage rather than point solutions. AI-assisted evaluation is expanding the role of these tools beyond interview scheduling and recording to structured review, guided scoring, and faster handoffs across hiring teams. Compliance pressure is reinforcing the same direction, as employers increasingly want auditable workflows, documented human oversight, and defensible assessment records that can withstand internal review and external scrutiny. Vendor strategy in the video interviewing platform market is therefore shifting toward end-to-end hiring ownership, which explains the rise in platform acquisitions, deeper ecosystem partnerships, and product development centered on explainability and workflow control.

Key Report Takeaways

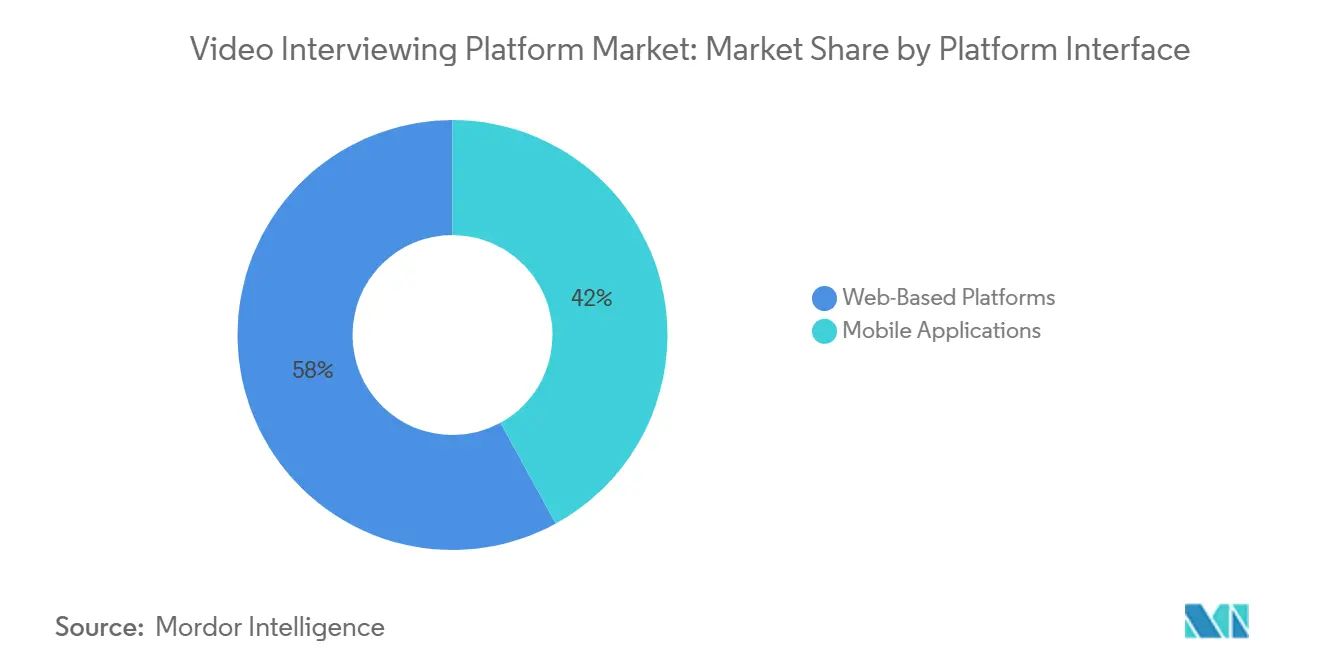

- By platform interface, web-based platforms led with 57.98% revenue share in 2025, while mobile applications are projected to expand at a 15.37% CAGR through 2031.

- By deployment model, cloud-based deployment held 61.24% of the market in 2025 and is also expected to advance at a 14.88% CAGR through 2031.

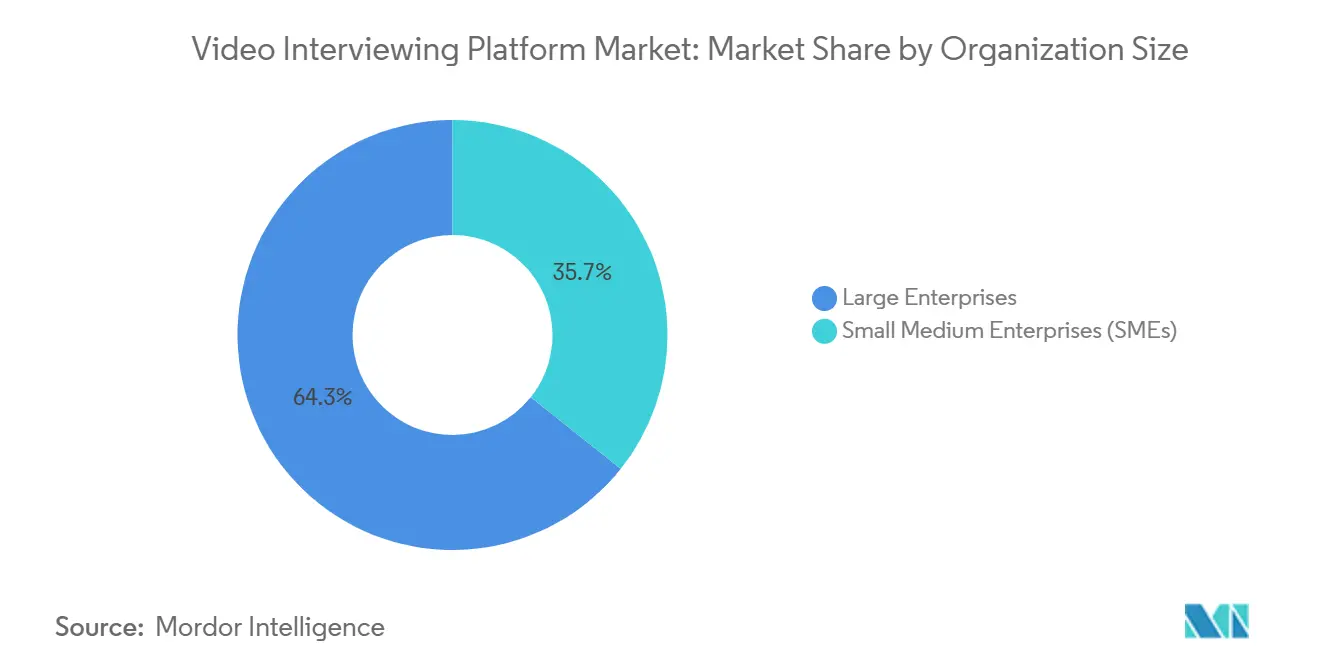

- By organization size, large enterprises held 64.31% of the video interviewing platform market share in 2025, while SMEs are projected to grow at a 16.43% CAGR through 2031.

- By end-user industry, IT and Telecom accounted for 23.71% of the market in 2025, while healthcare and life sciences are expected to expand at a 16.11% CAGR through 2031.

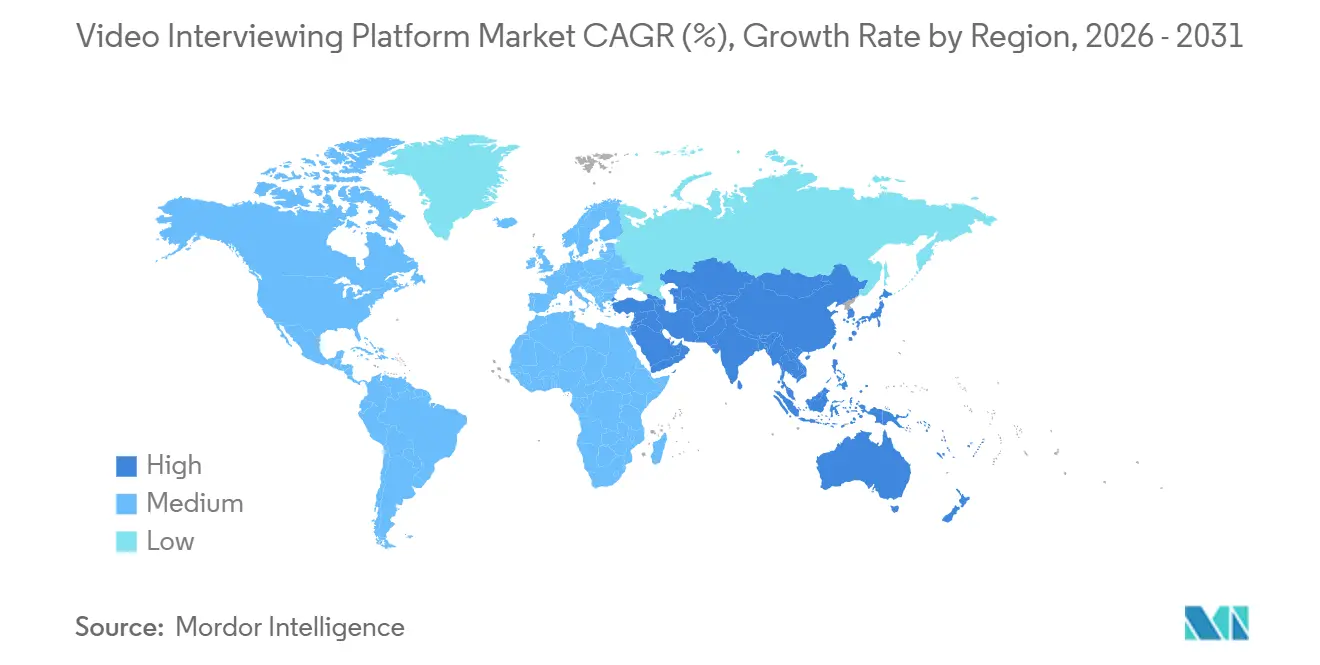

- By geography, North America held 44.36% of revenue in 2025, while Asia-Pacific is projected to expand at an 15.93% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Video Interviewing Platform Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Enterprise Shift to Structured Remote Hiring | +3.5% | Global, with strongest pull in North America and Western Europe | Short term (≤ 2 years) |

| Demand For Faster Screening and Lower Time-To-Hire | +3.0% | Global | Short term (≤ 2 years) |

| ATS And HRIS Integration as a Buying Prerequisite | +2.5% | North America and EU | Medium term (2-4 years) |

| Adoption of AI-Assisted Summaries and Interview Intelligence | +2.2% | North America and EU, spill-over to Asia-Pacific | Medium term (2-4 years) |

| Demand For Audit-Ready Human Oversight Workflows | +1.5% | EU and North America | Medium term (2-4 years) |

| Growth of Cross-Border and Multilingual Hiring Programs | +1.2% | Asia-Pacific core, spill-over to Middle East, Africa, and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Enterprise Shift To Structured Remote Hiring

The video interviewing platform market is being lifted by the steady move from informal virtual interviewing to structured remote hiring systems that employers can apply consistently across large candidate pools. Distributed work has made location-flexible recruiting normal, and that has pushed employers to standardize questions, evaluation criteria, and evidence capture instead of depending on live calls that vary by interviewer and time slot. Large organizations now want every candidate to move through the same process, which makes structured video workflows more useful in regulated sectors and multi-site hiring programs. In recent years, employers have increasingly adopted artificial intelligence in recruitment, with numerous organizations integrating AI into their hiring processes. This trend reflects a broader transition toward a more structured and technology-driven recruitment framework, where automation, candidate intelligence, and predictive analytics have become integral to talent acquisition strategies. This shift is changing what buyers expect from the video interviewing platform market, because the requirement is no longer basic video connectivity but a system that can hold rubrics, preserve records, and support repeatable evaluation. Vendors that cannot deliver standardized workflows at enterprise scale are losing relevance as the video interviewing platform market moves toward process control and auditability instead of simple interview convenience

Demand For Faster Screening and Lower Time-To-Hire

The video interviewing platform market is also benefiting from employer pressure to reduce early-stage screening delays, especially where hard-to-fill roles attract multiple competing offers. Asynchronous interviewing separates recruiter availability from candidate availability, which lets teams review more applicants in parallel and move stronger candidates forward before interest fades. That scheduling flexibility matters most in technology, healthcare, and other labor-tight fields where speed often determines whether an employer even reaches the offer stage. SmartRecruiters reported in its 2025-2026 recruiting benchmarks that structured scorecard adoption is now close to universal among high-performing hiring teams, which shows how standardization and speed are increasingly linked in modern recruitment operations. The commercial effect is broader than calendar efficiency, because a faster first screen improves response momentum, reduces idle time between steps, and helps recruiters coordinate decisions across several stakeholders with less friction. As the video interviewing platform market matures, vendors that combine async screening with built-in review structure and AI-assisted summaries are closing the remaining time gaps that manual note-taking and unstructured review still create.

ATS And HRIS Integration as a Buying Prerequisite

Enterprise demand in the video interviewing platform market increasingly depends on whether a platform can connect cleanly to the systems that already run recruiting and onboarding. Procurement teams now expect interview invitations, candidate status updates, score capture, and downstream hiring triggers to flow between the interviewing platform and the system of record without manual re-entry. This expectation reflects a more mature view of HR technology, where disconnected tools create compliance risk, weak reporting, and extra recruiter workload even when the stand-alone product itself performs well. The practical result is that platforms without pre-built connectors or strong APIs are often screened out before commercial discussions move very far. HireVue’s entry into the Workday AI Agent Partner Network in January 2026 showed how leading vendors are moving from peripheral interview tools to embedded workflow participants inside the core HR environment. That kind of system-level placement raises the entry barrier across the video interviewing platform market, particularly for smaller vendors that do not have the engineering depth, partner relationships, or service capacity needed to support complex enterprise integrations.

Adoption Of AI-Assisted Summaries And Interview Intelligence

AI-assisted review is becoming a baseline expectation in the video interviewing platform market, as employers want less time spent watching full recordings and more clarity on the moments that matter for job-relevant evaluation. The focus is shifting from generic automation to interview intelligence that can surface important responses, summarize evidence, and support more consistent reviewer decisions. HireVue’s Interview Insights launch in October 2025 reflected this change, as it was designed to highlight interview moments tied to job-related skills so managers could review large candidate volumes more efficiently.[1]HireVue, “HireVue Launches Interview Insights,” HireVue, hirevue.com VidCruiter added another layer in May 2026 with AI Interview Scoring, tying evaluation to client-approved rubrics and maintaining a full audit trail, which addresses buyer concerns around explainability and defensibility. That matters because regulators and enterprise buyers are no longer treating explainability as a premium feature, they are treating it as a condition for purchase in any system that touches employment decisions. As a result, the video interviewing platform market is favoring vendors whose AI features remain transparent, reviewable, and directly connected to human-approved scoring logic rather than opaque black-box outputs.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising AI Hiring Compliance and Bias Audit Burden | -1.8% | North America and EU | Short term (≤ 2 years) |

| Integration Complexity With Legacy HR Tech Stacks | -1.5% | Global, acute in Asia-Pacific and South America | Medium term (2-4 years) |

| Candidate Drop-Off From One-Way Interview Fatigue | -1.0% | Global | Short term (≤ 2 years) |

| Reliability Gaps in Low-Bandwidth and Low-Device-Quality Environments | -0.7% | Africa, South Asia, Southeast Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising AI Hiring Compliance And Bias Audit Burden

Compliance pressure is one of the clearest checks on the video interviewing platform market, especially for buyers and vendors operating across North America and Europe. New York City’s Local Law 144 requires annual independent bias audits for automated employment decision tools, public disclosure of results, and advance notice to candidates, which has made governance and documentation part of normal platform review.[2]New York City Department of Consumer and Worker Protection, “Automated Employment Decision Tools,” NYC Government, nyc.gov The EU AI Act adds another layer, because recruitment systems classified as high-risk AI must meet conformity, documentation, and post-market monitoring obligations that became fully applicable in August 2026. These rules do not stop adoption, but they do lengthen procurement reviews and raise the threshold for product defensibility, especially when smaller vendors cannot show mature governance controls. Buyers now expect audit logs, human review checkpoints, rubric-linked scoring, and clear accountability inside the product rather than in separate policy documents. The restraint on the video interviewing platform market, therefore, comes less from regulatory prohibition and more from the rising cost and complexity of proving that a hiring system is safe, explainable, and fit for employment use.

Integration Complexity With Legacy HR Tech Stacks

The video interviewing platform market also faces friction when employers try to connect modern interview tools to older HR technology environments that were not built for real-time interoperability. Many mid-enterprise, public-sector, and highly regulated organizations still rely on legacy HRIS and ATS configurations that make new workflow connections slower, riskier, and more expensive than software demos suggest. In these cases, the challenge is rarely whether integration is technically possible, it is whether the organization is willing to absorb the development effort, testing burden, and governance review that come with exposing older systems to third-party workflows. This slows deployments and can move buyers toward larger vendors that offer managed services, stronger connector libraries, and more implementation support. The problem is especially relevant where local enterprises are modernizing unevenly, because the video interviewing platform market may be ready for API-led workflows while the buyer’s broader HR architecture is not. Smaller vendors often lose these deals not because their interview product is weak, but because buyers view integration risk as more important than feature strength once the platform must sit inside an older and more sensitive HR stack.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform Interface: Web Access Holds The Core Position While Mobile Reshapes Candidate Behavior

Web-based platforms held 57.98% of the market in 2025, which kept browser access as the main operating model across the video interviewing platform market. That lead reflects the preference of enterprise recruiters and hiring managers for desktop review environments that fit existing ATS workflows and do not require additional device-level installation. Browser delivery also aligns better with internal IT policies, because many large organizations place tighter controls on app installation across managed devices. In that sense, web access remains the stable operating center of the video interviewing platform market even as buyer expectations around automation and compliance continue to rise. The format is especially useful for recruiter-side review, panel coordination, and evaluation record keeping, where screen size, multitasking, and reporting visibility matter more than portability.

Mobile, however, is reshaping the candidate side of the video interviewing platform market at a faster pace, and mobile applications are projected to grow at a 15.37% CAGR through 2031. That growth reflects the rising share of frontline, hourly, and distributed hiring programs where candidates increasingly default to smartphones for job search activity and first-stage screening. The important shift is not simply that interviews can happen on smaller screens, it is that completion rates depend more heavily on mobile-friendly recording, short load times, and minimal sign-in friction. Platforms that reduce app-download requirements and offer smooth in-browser capture are better positioned for candidate populations that do not sit at desks or have easy access to laptops. This has created a structural asymmetry in the video interviewing platform industry, because recruiter workflows still lean toward web access while candidate experience is increasingly shaped by mobile-first design choices.

By Deployment Model: Cloud Delivery Remains The Default Architecture

Cloud-based deployment accounted for 61.24% of the market in 2025, giving it the largest position in the video interviewing platform market by deployment model. The same segment is also projected to grow at a 14.88% CAGR through 2031, which shows that cloud adoption is still widening rather than simply defending an installed base. Buyers continue to prefer cloud delivery because it avoids hardware provisioning, shortens upgrade cycles, and supports pricing models that can flex with hiring volume. Those advantages matter when recruitment demand changes quickly across seasons, projects, or expansion phases. Cloud architecture also makes it easier for vendors in the video interviewing platform market to push new AI features, workflow adjustments, and compliance controls without waiting for a customer-side upgrade cycle.

Hybrid deployment still has a place in highly regulated environments where data residency concerns or internal governance rules complicate full migration to the cloud. On-premises models remain relevant in parts of government and defense-related hiring, but they are losing momentum in new buying decisions across the broader video interviewing platform market. The real competitive divide is now less about where software is hosted and more about how well that hosting model supports ecosystem participation. HireVue’s Workday partnership in 2026 showed that cloud-native design increasingly serves as the base requirement for deeper orchestration across connected HR workflows.[3]HireVue, “HireVue Joins Workday AI Agent Partner Network,” HireVue, hirevue.com As that pattern spreads, vendors with cloud-first products will continue to hold the stronger position because they can move faster on integration, automation, and regional compliance configuration than deployment models built around older infrastructure.

By Organization Size: Large Enterprises Lead While SMEs Expand More Quickly

Large enterprises held 64.31% of the video interviewing platform market share in 2025, which underlines how strongly the category has been shaped by scale hiring economics. Large employers were earlier adopters because the value of structured video workflows becomes more visible when thousands of interviews, multiple geographies, and several review layers sit inside the same recruiting system. That scale gives enterprise buyers more reason to invest in compliance controls, integration depth, and global deployment standards that smaller hiring teams may not need at the outset. As a result, the premium end of the video interviewing platform market remains anchored by enterprise procurement patterns, longer contracts, and broader workflow expectations. The segment’s weight is therefore tied to both budget capacity and the operational complexity of large hiring programs.

SMEs are still the faster-growth group, with a 16.43% CAGR projected through 2031, and that is broadening the demand base of the video interviewing platform market. Affordable pricing models, self-serve onboarding, and packaged templates have reduced the barrier for sub-500-headcount organizations that want structure without enterprise implementation effort. The buying logic is different in this part of the video interviewing platform market, because speed to deploy and candidate simplicity often matter more than deep configuration or multinational governance. Phenom’s embedding of video assessments inside a broader talent experience environment illustrates how vendors are capturing this demand by making video screening one step in a wider automation flow rather than a stand-alone product.

By End-User Industry: IT And Telecom Leads While Healthcare And Life Sciences Accelerate

IT and Telecom held the largest end-user share at 23.71% in 2025, making it the clearest anchor vertical in the video interviewing platform market. The sector moved early because remote and hybrid work fit its operating model, and because technology employers often need structured ways to evaluate communication, problem framing, and role fit across global candidate pools. Video interviewing also suits the pace of technology hiring, where cross-time-zone screening and high application volumes can overwhelm live scheduling. This has kept IT and Telecom at the center of the video interviewing platform market even as other sectors have deepened adoption. The segment remains important not only for current demand but also for shaping feature expectations around workflow speed, evaluation consistency, and international hiring coverage.

Healthcare and life sciences are projected to grow at a 16.11% CAGR through 2031, which makes them the fastest-expanding vertical in the video interviewing platform market. Persistent staffing pressure across clinical and allied health roles is pushing recruiters toward tools that can screen larger candidate flows without adding equivalent recruiter headcount. Asynchronous interview formats are particularly useful here because candidates often respond outside normal office hours and cannot easily coordinate live screens during shift-based work cycles. That dynamic has made mobile compatibility, short response workflows, and clear handoff between recruiters and hiring managers especially important in healthcare hiring. The same pattern is widening adoption across BFSI, staffing and recruiting, retail and e-commerce, government, manufacturing, education, and other verticals, although these segments still sit behind the leading role of IT and Telecom and the faster acceleration now visible in healthcare and life sciences.

Geography Analysis

North America held 44.36% of the video interviewing platform market share in 2025, and that lead came from early enterprise adoption, a deep vendor base, and more developed employer familiarity with digital hiring tools. The United States remains the center of regional demand because technology, financial services, and healthcare employers have made time-to-hire reduction and structured remote screening part of normal talent acquisition practice. Canada is moving on a similar enterprise adoption path, while Mexico is benefiting from hiring growth tied to nearshore manufacturing and technology services that increasingly rely on remote pre-screening. Regulatory clarity also strengthens North America’s position, because employers there are becoming more practiced at evaluating bias audit, notice, and governance requirements in AI-assisted hiring systems. Europe remains the second-largest region in the video interviewing platform market, with strong adoption in Germany, the United Kingdom, and France, where enterprise talent acquisition teams have matured into more video-first workflows.

Europe’s path is being shaped as much by compliance architecture as by demand expansion. GDPR obligations influence how platforms handle consent, storage, retention, and processing across recorded interview workflows, which affects both vendor design and buyer selection. The EU AI Act is now further tightening expectations around employment-related AI by making explainability, documentation, and monitoring central to market access for higher-risk systems.[4]European Parliament and Council, “Regulation (EU) 2024/1689,” EUR-Lex, eur-lex.europa.eu These conditions are pushing the video interviewing platform market in Europe toward vendors that can combine strong workflow capability with credible governance controls. Regional growth is also being helped by localization of language support, pricing, and compliance features that make adoption easier beyond the largest Western European economies.

Asia-Pacific is projected to advance at a 15.93% CAGR, making it the fastest-growing regional block in the video interviewing platform market through 2031. Growth is being supported by India’s scale of graduate and professional hiring, Southeast Asia’s rising adoption of cloud HR tools, and stronger interest in multilingual workflows for cross-border recruitment. Markets such as Singapore, Indonesia, and Vietnam are benefiting from the need to manage distributed hiring programs more efficiently, while Australia, New Zealand, Japan, South Korea, and China broaden the region’s demand base through different mixes of enterprise modernization and AI adoption. South America, the Middle East, and Africa remain smaller in absolute terms, but the video interviewing platform market is expanding there as employers digitize recruitment and seek more consistent screening across language, location, and infrastructure gaps. Brazil and Argentina lead South American demand, the United Arab Emirates and Saudi Arabia are investing in AI-enabled HR systems, and parts of Africa are showing early adoption even though bandwidth quality and device limitations still restrain broader rollout.

Competitive Landscape

The video interviewing platform market is moderately consolidated at the enterprise end, where HireVue, iCIMS, and Radancy continue to hold the strongest presence in large-account mandates. Their advantage comes less from video functionality alone and more from how well they support integration, workflow coverage, and compliance expectations inside larger HR environments. In the current video interviewing platform market, procurement decisions are increasingly shaped by whether a vendor can sit inside the broader hiring process instead of standing next to it as a separate tool. That is why ecosystem depth now matters more than simple feature comparison in top-tier enterprise deals. Buyers want a platform that can manage candidate engagement, interview structure, evaluation records, and downstream workflow movement in one connected environment.

Recent strategic moves make that direction clear. HireVue acquired the technology behind Hireguide in March 2026 to accelerate agentic AI hiring and extend its reach earlier in the funnel through voice-based interviewer agents. Radancy acquired myInterview in September 2025 to add AI-powered candidate and recruiter agents to its talent acquisition cloud, which strengthened its position around fuller workflow ownership. iCIMS also expanded its platform in March 2026 with iCIMS Frontline AI and broader automation updates, which showed that enterprise suites are pushing harder into frontline recruitment workflows that overlap with the video interviewing platform market.

Mid-market competition remains more fragmented, and that is where specialist vendors such as VidCruiter, Spark Hire, Willo Technologies, Talview, Recright, Jobma, and Wamly are creating room through faster deployment and more focused product choices. VidCruiter’s May 2026 AI Interview Scoring launch is a strong example, because it was built around explainable, rubric-linked, auditable evaluation rather than opaque automation. Spark Hire and Willo are also competing by keeping implementation lighter and candidate interaction simpler, which helps them appeal to growing SME demand and to employers that want quicker rollout. The video interviewing platform market is also seeing pressure from general HR platforms that now embed video interviewing natively, which narrows the stand-alone differentiation available to pure-play vendors. At the same time, adjacent assessment providers such as TestGorilla and Cangrade do not materially define this competitive set because their core value lies in testing and predictive fit rather than structured or asynchronous video interviewing workflows. This combination of top-tier consolidation and mid-tier fragmentation means the video interviewing platform market is likely to remain strategically crowded, even as acquisitions and platform bundling reduce the number of independent paths to enterprise scale.

Video Interviewing Platform Industry Leaders

HireVue, Inc.

Employ, Inc.

VidCruiter Inc.

Spark Hire, Inc.

interviewstream, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: VidCruiter launched AI Interview Scoring, providing consistent, explainable, and fully auditable scoring for pre-recorded video interview responses using client-approved rubrics. The capability complements the company's broader AI suite, including AI Interview Notes and AI Fraud Detection, positioning it as a defensible AI hiring stack for compliance-sensitive enterprise buyers.

- March 2026: iCIMS expanded its enterprise talent acquisition platform with iCIMS Frontline AI, a purpose-built hiring solution targeting frontline talent recruitment. The Spring 2026 release also included hiring automation enhancements, an AI sourcing agent, and interview scheduling version 2 with cross-calendar support, addressing recruiter productivity at scale.

- March 2026: HireVue acquired the technology behind Hireguide, a company specializing in agentic AI for hiring. The integration accelerates HireVue's deployment of voice-based AI interviewer agents capable of qualifying candidates earlier in the hiring funnel than traditional video screening, adding richer candidate signal than resume screening or text-based bots.

- February 2026: HireVue launched Assessment Builder, enabling organizations to construct role-specific, performance-predictive hiring assessments in minutes without specialist psychometrics expertise. The product targets lower-volume roles typically excluded from validated assessment programs, extending skills-based hiring infrastructure to the full organizational roster.

Global Video Interviewing Platform Market Report Scope

A Video Interviewing Platform is a digital tool that allows organizations to conduct, manage, and assess job interviews remotely through video technology. These platforms optimize the recruitment process by providing features such as live video interviews, pre-recorded (on-demand) responses, candidate assessments, and integration with applicant tracking systems (ATS).

The Video Interviewing Platform Market is Segmented by Platform Interface (Web-Based Platforms, and Mobile Applications), Deployment Model (Cloud-Based, On-premises, and Hybrid), Organization Size (SMEs, and Large Enterprises), End-user Industry (IT and Telecom, BFSI, Healthcare, Retail, Staffing, Education, Government, Manufacturing, and Other End-user Industries), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Web-Based Platforms |

| Mobile Applications |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Small Medium Enterprises (SMEs) |

| Large Enterprises |

| IT and Telecom |

| BFSI |

| Healthcare and Life Sciences |

| Retail and E-Commerce |

| Staffing and Recruiting |

| Education and University Admissions |

| Government and Public Sector |

| Manufacturing |

| Other End-User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Israel | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Platform Interface | Web-Based Platforms | |

| Mobile Applications | ||

| By Deployment Model | Cloud-Based | |

| On-Premises | ||

| Hybrid | ||

| By Organization Size | Small Medium Enterprises (SMEs) | |

| Large Enterprises | ||

| By End-User Industry | IT and Telecom | |

| BFSI | ||

| Healthcare and Life Sciences | ||

| Retail and E-Commerce | ||

| Staffing and Recruiting | ||

| Education and University Admissions | ||

| Government and Public Sector | ||

| Manufacturing | ||

| Other End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the 2026 size of the video interviewing platform space, and how fast is it expected to grow?

The Video Interviewing Platform Market stands at USD 3.13 billion in 2026 and is projected to reach USD 6.29 billion by 2031 at a CAGR of 14.98%.

Which platform interface leads today, and which one is growing faster?

Web-based access led with 57.98% share in 2025 because recruiters still prefer browser-led workflows, while mobile applications are projected to grow faster at a 15.37% CAGR through 2031.

Why are enterprises investing more in video interviewing tools now than in the pandemic period?

Buyers now treat these platforms as core HR infrastructure rather than temporary remote hiring tools. Demand is being driven by structured workflows, AI-assisted review, deeper ATS integration, and stronger compliance requirements.

Which deployment model is winning, and why does it matter?

Cloud deployment led with 61.24% share in 2025 and is also the fastest-growing model at 14.88% CAGR. It matters because cloud systems support faster upgrades, flexible pricing, and better integration with broader HR platforms.

Which customer group offers the biggest revenue base, and which offers the best growth outlook?

Large enterprises accounted for 64.31% of demand in 2025, making them the main revenue anchor. SMEs are growing faster at a 16.43% CAGR as self-serve and lower-cost tools reduce adoption barriers.

Which regions and end-user sectors are shaping future demand most strongly?

North America held 44.36% share in 2025, while Asia-Pacific is growing fastest at a 15.93% CAGR. By end user, IT and Telecom led with 23.71% share in 2025, while healthcare and life sciences are growing fastest at 16.11% CAGR.

Page last updated on: