Webcams Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

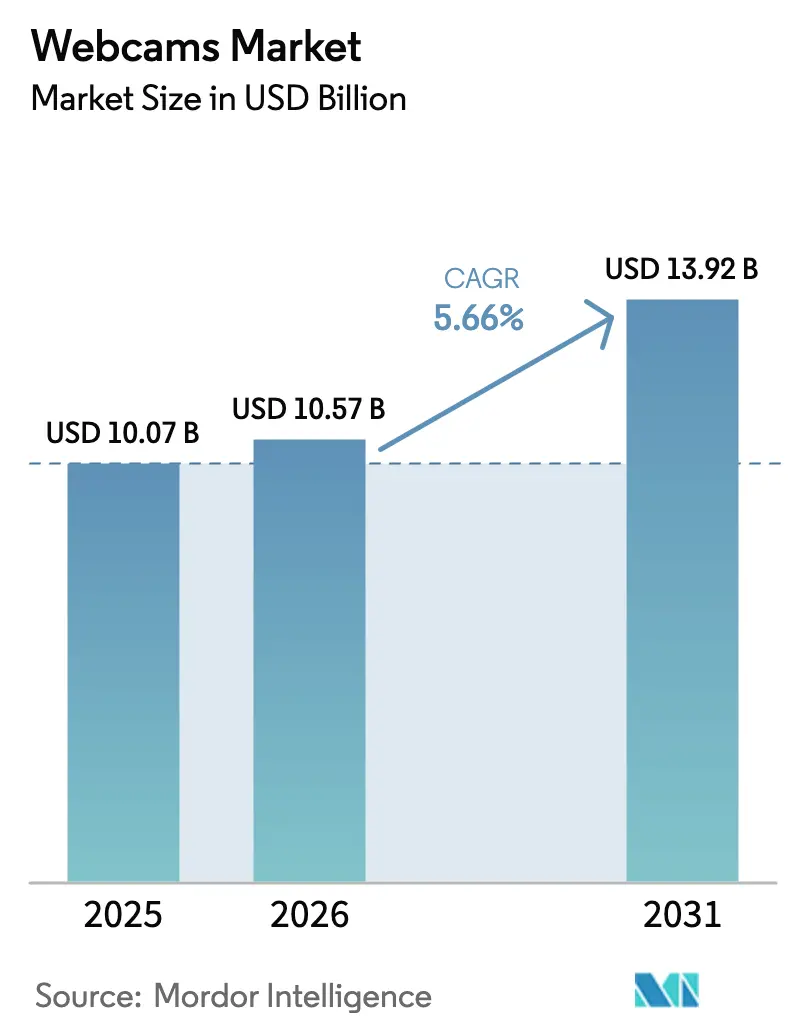

| Market Size (2026) | USD 10.57 Billion |

| Market Size (2031) | USD 13.92 Billion |

| Growth Rate (2026 - 2031) | 5.66% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

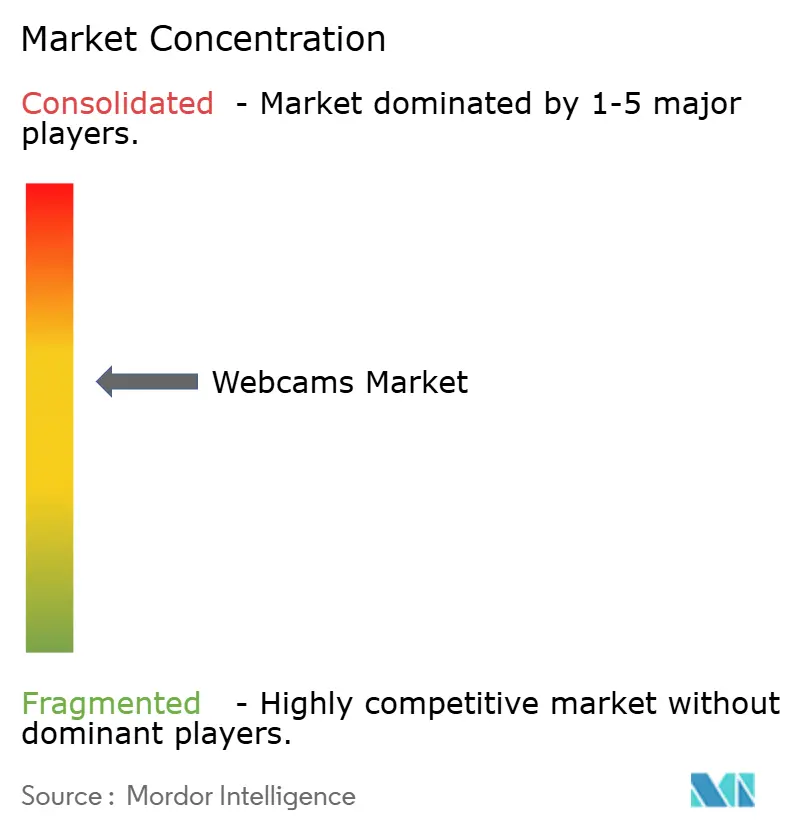

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Webcams Market Analysis by Mordor Intelligence

The webcams market size was valued at USD 10.07 billion in 2025 and is estimated to grow from USD 10.57 billion in 2026 to reach USD 13.92 billion by 2031, reflecting a 5.66% CAGR over the forecast period (2026-2031). Several converging forces drive this expansion, including corporate commitments to hybrid work, the surge in live streaming, falling average selling prices, and the rapid integration of AI-powered imaging features. Enterprise buyers now standardize on external 4K units for conference rooms and executive offices, while healthcare providers adopt diagnostic-grade cameras to support tele-medicine. At the same time, prosumer creators view high-resolution webcams as foundational studio tools, lifting volume demand even as margins compress. Component miniaturization and supply-chain normalization further reduce price barriers, enabling small and medium enterprises to refresh legacy 720p devices in bulk.

Key Report Takeaways

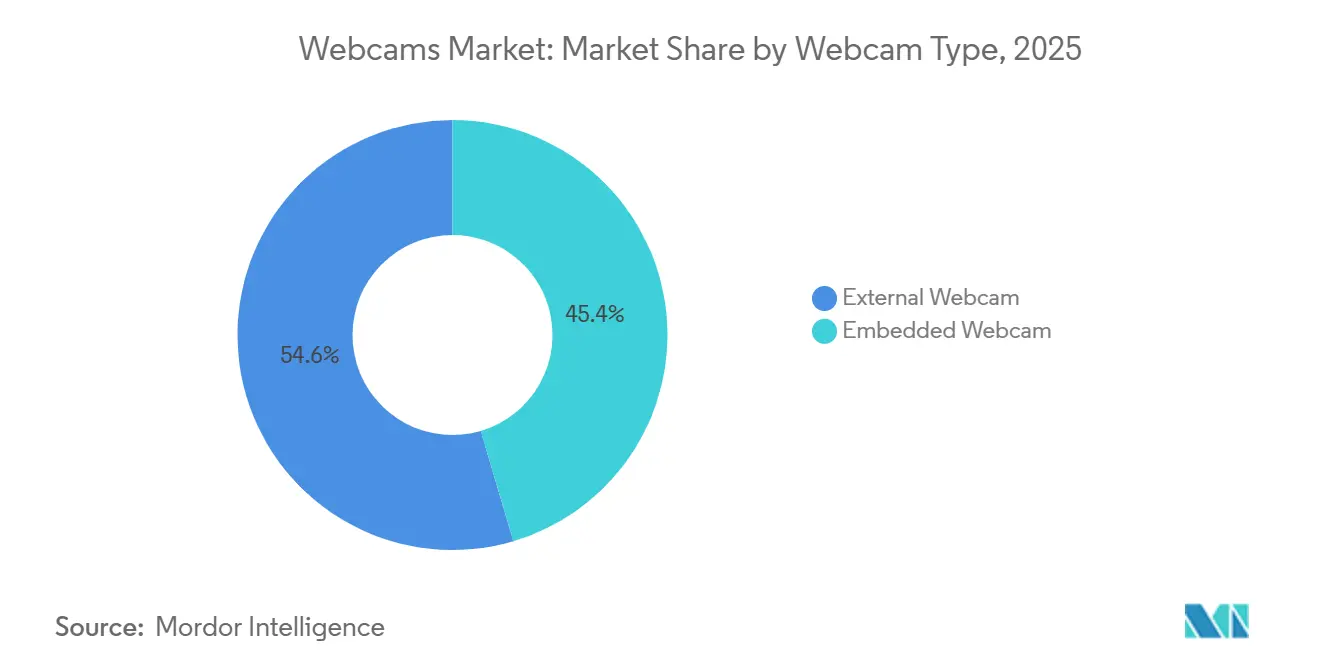

- By webcam type, external units led with 54.57% of the webcam market share in 2025, and the segment is forecast to expand at a 6.68% CAGR through 2031.

- By sensor resolution, Full HD commanded 45.72% of the webcam market size in 2025, while 4K UHD is advancing at a 6.02% CAGR through 2031.

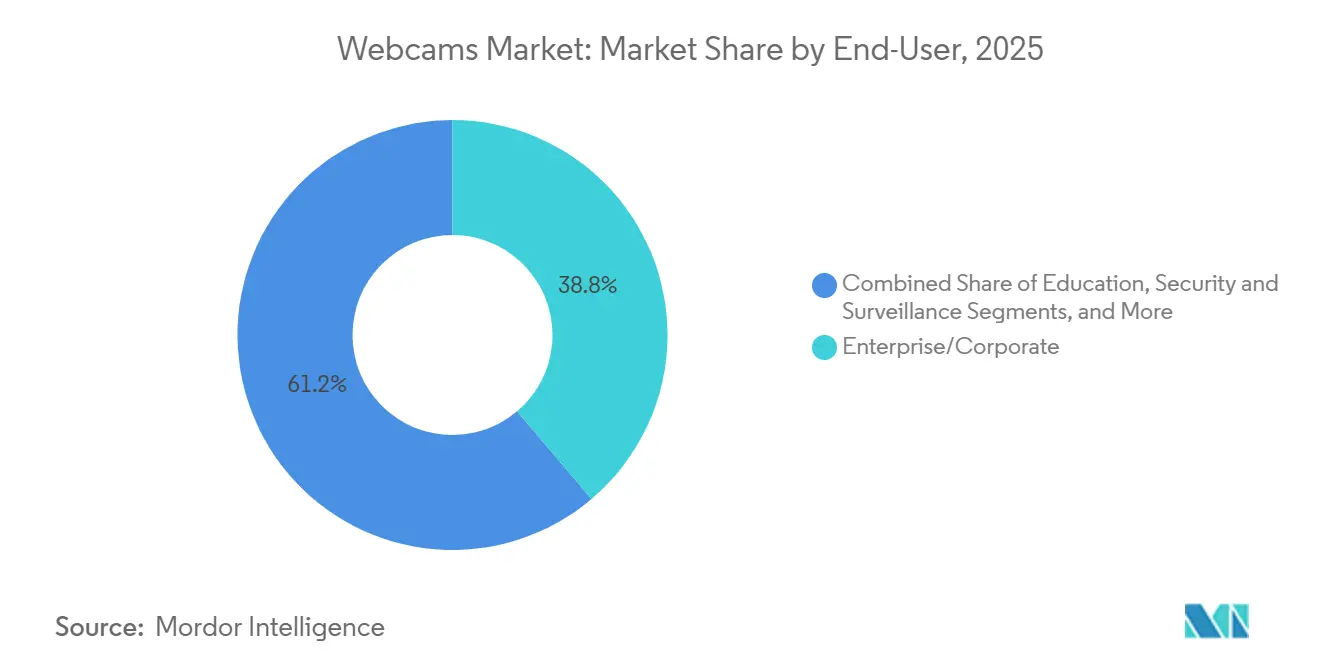

- By end-user, enterprise and corporate buyers held a 38.82% share in 2025, whereas the healthcare sector is growing fastest at a 5.91% CAGR to 2031.

- By distribution channel, online sales accounted for 55.47% of revenue in 2025 and are projected to grow at a 6.24% CAGR through 2031.

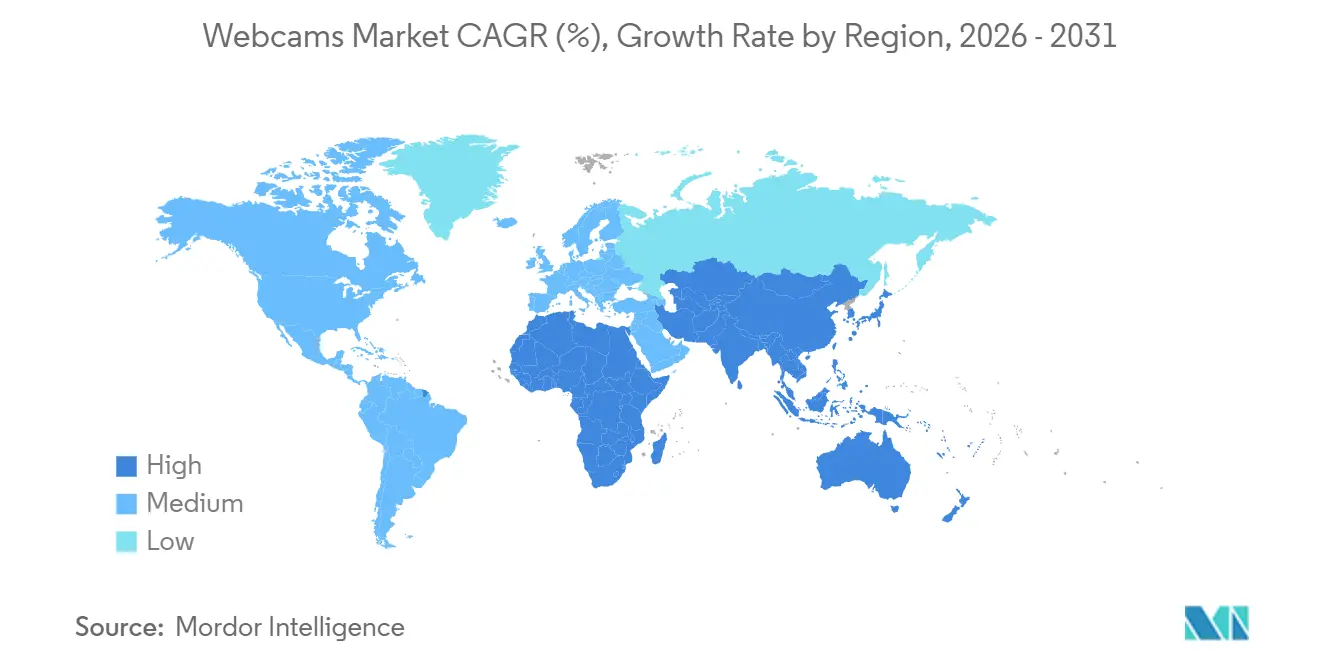

- By geography, the Asia-Pacific region accounted for 36.64% of 2025 revenue, while the Middle East will be the fastest-growing regions at a 6.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Webcams Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exploding adoption of enterprise video-conferencing solutions | +1.8% | Global, with concentration in North America, Europe, and Asia-Pacific urban centers | Medium term (2-4 years) |

| Hybrid and remote work models normalizing webcam usage | +1.5% | Global, led by North America and Europe, expanding to Asia-Pacific and Middle East | Long term (≥ 4 years) |

| Accelerating growth of live-streaming and content-creator economy | +1.2% | Global, with highest intensity in North America, Europe, and Asia-Pacific (Japan, South Korea) | Medium term (2-4 years) |

| Rapid decline in ASPs of HD and FHD webcams | +0.9% | Global, most pronounced in Asia-Pacific manufacturing hubs and emerging markets | Short term (≤ 2 years) |

| AI-enabled smart webcams fueling prosumer upgrade cycles | +1.4% | North America, Europe, and Asia-Pacific developed markets | Medium term (2-4 years) |

| Tele-health demand for 4K and 8K clinical-grade cameras | +0.7% | North America and Europe, with emerging adoption in Asia-Pacific and Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Exploding Adoption of Enterprise Video-Conferencing Solutions

Corporate video-conferencing suites transitioned from convenience tools to mission-critical infrastructure in 2025. Zoom reported 4,274 customers producing more than USD 100,000 in annual recurring revenue, a cohort that standardizes on external 4K webcams to ensure board-level image fidelity. Large employers upgraded 27%-35% of meeting spaces in 2025, replacing embedded laptop cameras that lack optical zoom and low-light prowess. Persistent meeting friction, averaging 6 minutes of lost productivity per session, accelerated these deployments, especially for Microsoft Teams Rooms and Zoom Rooms. The shift toward asynchronous video messaging further amplifies demand, as employees need dedicated webcams to record polished content. Collectively, these factors lift enterprise volume shipments and reinforce premium certification ecosystems.

Hybrid and Remote Work Models Normalizing Webcam Usage

Hybrid schedules hardened into the dominant employment pattern in 2025, with 28% of United States staff working partly from home and 9% fully remote. The Bureau of Labor Statistics counted 35.5 million U.S. teleworkers, a 5.1 million rise from 2024. Similar adoption is visible in the United Kingdom, where 45% of employees now split time between office and home, and in the Middle East, where 81% of professionals secured remote-work approval. Because technology quality ranks among the top five contributors to job satisfaction for 85% of hybrid workers, enterprises budget for professional-grade webcams across home offices. This structural shift elevates webcams from optional peripherals to essential productivity assets, anchoring long-run demand across regions.

AI-enabled Smart Webcams Fueling Prosumer Upgrade Cycles

Machine-learning features once exclusive to USD 1,000 conference systems now ship in sub-USD 200 consumer devices. Logitech’s MX Brio incorporates auto-framing, computational lighting, and an overhead document mode; Microsoft’s IntelliFrame dynamically centers meeting participants without manual pan-tilt-zoom. HP, Razer, and Dell add AI facial tracking and noise reduction, compressing the performance gap between webcams and interchangeable-lens cameras. Prosumer creators, remote executives, and online educators perceive these upgrades as productivity investments, triggering replacement cycles every two to three years. As AI feature parity spreads, differentiation shifts toward sensor size, optics, and software ecosystems.

Accelerating Growth of Live-Streaming and Content-Creator Economy

Advertising spend on creator channels reached USD 37.1 billion in 2025, up 26%, as brands used AI to find niche influencers.[2]Interactive Advertising Bureau, “2025 Creator Economy Benchmarking Report,” iab.com Live-streaming platforms logged 29.7 billion hours watched in Q1 2025; YouTube Live captured roughly half that time, TikTok Live exceeded 8 billion hours, and Twitch maintained 140 million monthly active users. Creators demand 4K60 webcams capable of sustained bit-rates without thermal throttling or compression artifacts. Virtual events and hybrid conferences additionally require broadcast-grade video for panelists and keynote speakers. These cross-segment dynamics elevate the webcams market as a foundational layer of the global creator economy.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Widespread availability of embedded laptop and mobile cameras | -0.8% | Global, with highest penetration in developed markets (North America, Europe, Asia-Pacific) | Long term (≥ 4 years) |

| Persistent privacy and cyber-security concerns (webcam hacking) | -0.6% | Global, with heightened awareness in North America and Europe | Medium term (2-4 years) |

| CMOS sensor supply-chain volatility impacting inventories | -0.4% | Global, most acute in Asia-Pacific manufacturing hubs (China, Taiwan, South Korea) | Short term (≤ 2 years) |

| Compliance costs from stricter e-waste and RoHS regulations | -0.3% | Europe, North America, with expanding reach to Asia-Pacific and Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Privacy and Cyber-Security Concerns (Webcam Hacking)

Seventy-five percent of consumers worry about unauthorized camera access, and 61% physically cover webcams when idle. The FBI’s 2024 advisory cited malware that activates webcams without LED indicators, while high-severity vulnerabilities such as CVE-2024-5028 and CVE-2024-31320 affected flagship devices.[3]CVE Program, “CVE-2024-5028 and CVE-2024-31320,” cve.mitre.org Live exploits at Pwn2Own reinforced the perception that manufacturers prioritize features over security audits. This mistrust dampens impulse purchases and elongates replacement intervals as buyers await clearer regulatory safeguards. The forthcoming EU Cyber Resilience Act could restore confidence but will add compliance costs for smaller brands.

CMOS Sensor Supply-Chain Volatility Impacting Inventories

Lead times for CMOS image sensors peaked at 26 weeks in 2022 before easing to 8-12 weeks by 2024, yet supplier concentration remains a critical risk. Sony maintains 42% share of global output, followed by ON Semi, Samsung, and OmniVision. Disruptions in any one fab cascade through webcam OEMs that rely on advanced 4K and 8K nodes. Smaller brands struggle to secure priority allocation, often carrying excess safety stock or absorbing stockouts. Dual-sourcing agreements and long-term purchase commitments mitigate but do not eliminate the threat, especially as automotive and smartphone segments compete for the same high-resolution wafers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Webcam Type: External Units Dominate Professional Deployments

External models captured 54.57% revenue in 2025 and are projected to advance at a 6.68% CAGR through 2031, highlighting their dominance in professional deployments. This leadership reflects enterprise and healthcare users who require modular cameras with eye-level mounting, superior optics, and interchangeable lenses. External devices integrate seamlessly with conferencing platforms and allow straightforward cable management, boosting installation speed in huddle rooms and tele-medicine carts. Vendors increasingly bundle 4K sensors, beamforming microphones, and integrated speakers, reducing component sprawl and IT overhead. While embedded laptop cameras ship in 95% of new notebooks, their fixed angles and small sensors limit suitability for boardroom settings. As hybrid policies mature, many professionals add an external unit at home even when their laptops include 1080p webcams, ensuring consistent image quality across workspaces. Rapid price declines below USD 100 for Full HD and under USD 200 for 4K enable budget-constrained SMEs to adopt external solutions at scale, thereby reinforcing the dominance of this category within the webcams market.

Despite embedded cameras’ ubiquity, their revenue share trails units shipped because costs are subsumed into broader device bills of material. Consumer video calling, online education, and casual gaming continue to rely on embedded hardware, but these contexts rarely justify standalone purchases. In contrast, healthcare organizations specify external 4K cameras to satisfy diagnostic accuracy guidelines, and content creators favor flexible tripods and ring-light mounts that laptop lids cannot match. The balancing act between embedded convenience and external performance should continue, yet external unit innovation-such as AI-directed framing and optical zoom-positions the segment to preserve leadership within the webcams market across the forecast horizon.

By Sensor Resolution: 4K UHD Becomes the Aspirational Standard

Full HD resolution accounted for 45.72% of 2025 revenue, benefiting from decade-long platform standardization and a sub-USD 100 price point. Nonetheless, 4K UHD is the fastest-growing tier, registering a 6.02% CAGR through 2031 as creators, clinicians, and executives upgrade. High pixel density enables lossless digital pan-tilt-zoom, critical for multi-person framing and tight crop shots during live streams, thereby linking resolution improvements to AI feature efficacy. Retail availability of 4K60 models, such as Elgato Facecam Pro and Logitech MX Brio, has lowered entry thresholds for prosumers who view visual quality as a competitive differentiator. Healthcare buyers adopt 4K cameras to future-proof against evolving telehealth guidelines, while 8K remains niche due to bandwidth constraints and limited platform support.

Looking forward, falling bit-rate demands from advanced codecs mean 4K adoption will accelerate even among bandwidth-restricted users. Content platforms such as YouTube and Twitch have enabled 4K streaming, incentivizing creators to migrate from 1080p. Enterprises experimenting with immersive collaboration solutions also benefit, as 4K webcams capture finer spatial detail for AR overlays. Although 1080p models will maintain relevance in budget segments, shipment mix will increasingly tilt toward 4K, cementing this resolution as the new baseline of the webcams market.

By End-User: Healthcare Ascends as the Fastest-Growing Vertical

Corporate and enterprise customers commanded 38.82% revenue in 2025, underpinned by global hybrid work policies and ongoing meeting-room upgrades. Yet healthcare providers represent the most dynamic opportunity, expanding at 5.91% CAGR through 2031. Regulatory endorsements for virtual diagnostics and reimbursable tele-medicine encourage hospitals and clinics to install 4K webcams that capture dermatological detail and nuanced patient cues. HIPAA-compliant devices with encrypted streams and physical shutters address privacy mandates, allowing providers to satisfy both clinical and security criteria. Meanwhile, consumer and residential users sustain steady but slower growth as embedded laptop cameras suffice for casual communication.

Educational institutions often procure rugged Full HD webcams in bulk to facilitate hybrid classrooms, whereas creators invest USD 200-400 in 4K units featuring large sensors and AI exposure control. Security and surveillance overlap remains limited because dedicated IP cameras offer specialized weatherproofing and power options. Still, as health systems integrate virtual care into standard practice, webcam vendors that tailor firmware, privacy features, and medical-grade certifications will capture this accelerating slice of the webcams market.

By Distribution Channel: E-Commerce Consolidates Majority Share

Online channels accounted for 55.47% of 2025 sales, rising on the back of vendor storefronts, marketplace platforms, and software-centric subscription bundles. Procurement teams favor e-commerce for transparent pricing, configuration flexibility, and rapid fulfillment, while creators rely on customer reviews and detailed spec sheets when selecting high-resolution models. Value-added resellers layer services such as installation and multi-year maintenance atop web-based portals, merging digital ordering convenience with on-site support. Subscription refresh programs dispatched through vendor dashboards further cement the digital route to market.

Brick-and-mortar retailers retain relevance for hands-on testing, impulse purchases, and immediate replacement needs, especially among consumers wary of counterfeit products. However, shrinking shelf space and the shift toward higher-margin product lines diminish in-store webcam assortments. Absent experiential demos or exclusive launches, offline share is expected to erode steadily. As a result, online dominance appears durable, ensuring that the e-commerce ecosystem remains a strategic battleground for differentiation within the webcams market.

Geography Analysis

Asia-Pacific accounted for 36.64% of global revenue in 2025, driven by China’s manufacturing scale, India’s IT services boom, and Japan’s early embrace of AI-enabled conference systems. Rapid urbanization and government digitization programs are accelerating corporate video adoption, while CMOS sensor clusters in Taiwan and South Korea are streamlining component logistics. Enterprises such as Japan Radio Company standardized 77 Logitech-equipped rooms within a single quarter, evidencing deployment velocity. Simultaneously, cultural comfort with camera-based identification- highlighted by Panasonic’s facial recognition rollout at Expo 2025 Osaka- reduces privacy-driven resistance, reinforcing regional demand.

The Middle East is the fastest-rising region, with a 6.12% CAGR, propelled by multinational headquarters relocating to Dubai and Riyadh and by government mandates for digital service delivery. Broadband penetration surpasses 98% in the United Arab Emirates and approaches that level in Saudi Arabia, creating a digitally literate workforce. Survey results show that 81% of Middle Eastern professionals received their employer's approval for remote work, lifting per-capita webcam adoption.

North America and Europe remain mature yet vibrant upgrade markets. The United States added 5.1 million teleworkers in 2025, and the United Kingdom reported 45% hybrid work penetration. Replacement cycles now pivot toward 4K60 capability and AI-enabled framing, sustaining mid-single-digit growth rates. Strict compliance regimes, such as the EU’s WEEE and RoHS directives, elevate operating costs for smaller brands, thereby consolidating share with established vendors. South American demand, led by Brazil and Argentina, skews value-oriented, focusing on prior-generation or refurbished models to offset import tariffs and currency volatility. Collectively, these regional dynamics ensure geographically diversified expansion for the webcams market.

Competitive Landscape

The webcam industry hosts a moderately concentrated field in which Logitech controls an estimated 30%-35% of shipments through its Rally, Brio, and MX lines. Microsoft, HP, Dell, and Lenovo leverage integrated hardware-software ecosystems to penetrate enterprise accounts, bundling certified devices with collaboration suites. Razer, Elgato, and Anker compete aggressively in the live-streaming niche, differentiating with large sensors, high frame rates, and streamer-oriented software overlays. Patent filings emphasize AI-driven framing, low-light enhancement, and background segmentation, underscoring a collective pivot toward computational imaging.

Component ownership influences competitive resilience. Logitech’s long-standing partnership with Sony for STARVIS sensors secures supply at advantaged pricing, while Razer experiments with sensor fusion to merge CMOS and depth data for green-screen-free background removal. Standards bodies such as the USB-IF and VESA establish a floor for 4K60 transmission bandwidth, compelling each vendor to meet increasingly stringent technical baselines. Smaller innovators, including Huddly and AVer, carve out huddle-room share with ultra-wide 150-degree fields of view and modular microphone arrays, though scale constraints limit their foothold. Ongoing AI feature parity threatens to commoditize mid-tier models, likely catalyzing consolidation or vertical integration plays as stakeholders seek unique defensible assets within the webcams market.

Webcams Industry Leaders

Logitech International S.A.

Microsoft Corporation

Lenovo Group Limited

HP Inc.

Dell Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Logitech released the MX Brio 4K webcam priced at USD 199.99, featuring AI image enhancement and an overhead document mode, positioning it for hybrid executives and content creators.

- November 2025: HP introduced the 950 4K Streaming Webcam with AI face tracking and auto-framing for enterprise plug-and-play scenarios.

- October 2025: Razer launched the Kiyo Pro Ultra, integrating Sony’s STARVIS 2 sensor and F1.7 aperture for low-light 4K30 capture.

- September 2025: Microsoft rolled out IntelliFrame to Teams Rooms certified devices, delivering cloud-driven dynamic framing to existing Logitech hardware.

- August 2025: Anker unveiled the AnkerWork B600 video bar, combining a 2K webcam, quad-microphone array, and AI framing in a single USB-C unit.

Global Webcams Market Report Scope

The Webcams Market Report is Segmented by Webcams Type (External, and Embedded), by Sensor Resolution (HD Greater than 720p, Full HD 1080p, 4K UHD, 8K and Others), by End-User (Consumer/Residential, Enterprise/Corporate, Healthcare and Tele-Medicine, Education, Broadcasting and Content Creation, and Security and Surveillance), by Distribution Channel (Online, and Offline), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| External Webcams |

| Embedded Webcams |

| HD (Greater than 720p) |

| Full HD (1080p) |

| 4K UHD |

| 8K and Above |

| Consumer/Residential |

| Enterprise/Corporate |

| Healthcare and Tele-Medicine |

| Education |

| Broadcasting and Content Creation |

| Security and Surveillance |

| Online (E-Commerce, Direct) |

| Offline (Retail Chains, Value-Added Resellers) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Webcams Type | External Webcams | |

| Embedded Webcams | ||

| By Sensor Resolution | HD (Greater than 720p) | |

| Full HD (1080p) | ||

| 4K UHD | ||

| 8K and Above | ||

| By End-User | Consumer/Residential | |

| Enterprise/Corporate | ||

| Healthcare and Tele-Medicine | ||

| Education | ||

| Broadcasting and Content Creation | ||

| Security and Surveillance | ||

| By Distribution Channel | Online (E-Commerce, Direct) | |

| Offline (Retail Chains, Value-Added Resellers) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the webcam market in 2026 and what growth is expected by 2031?

The webcams market size is USD 10.57 billion in 2026 and is projected to reach USD 13.92 billion by 2031, representing a 5.66% CAGR.

Which webcam type currently leads global revenue?

External units hold the lead, capturing 54.57% of 2025 revenue due to superior optics and flexible positioning.

Why is healthcare the fastest-growing vertical for webcams?

Tele-medicine reimbursement, diagnostic-grade 4K requirements, and HIPAA-compliant encryption drive a 5.91% CAGR for healthcare purchases.

What regions are forecast to post the highest growth rates?

The Middle East and Africa region is projected to expand at 6.12% CAGR through 2031, outpacing other geographies.

How are AI features reshaping webcam upgrades?

Auto-framing, speaker tracking, and computational lighting have migrated into sub-USD 200 models, prompting shorter replacement cycles among creators and remote executives.

Which companies dominate the competitive landscape?

Logitech leads with around one-third of shipments, while Microsoft, HP, Dell, Razer, and Elgato share the remainder of a moderately concentrated field.

Page last updated on: