Video Streaming Infrastructure Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

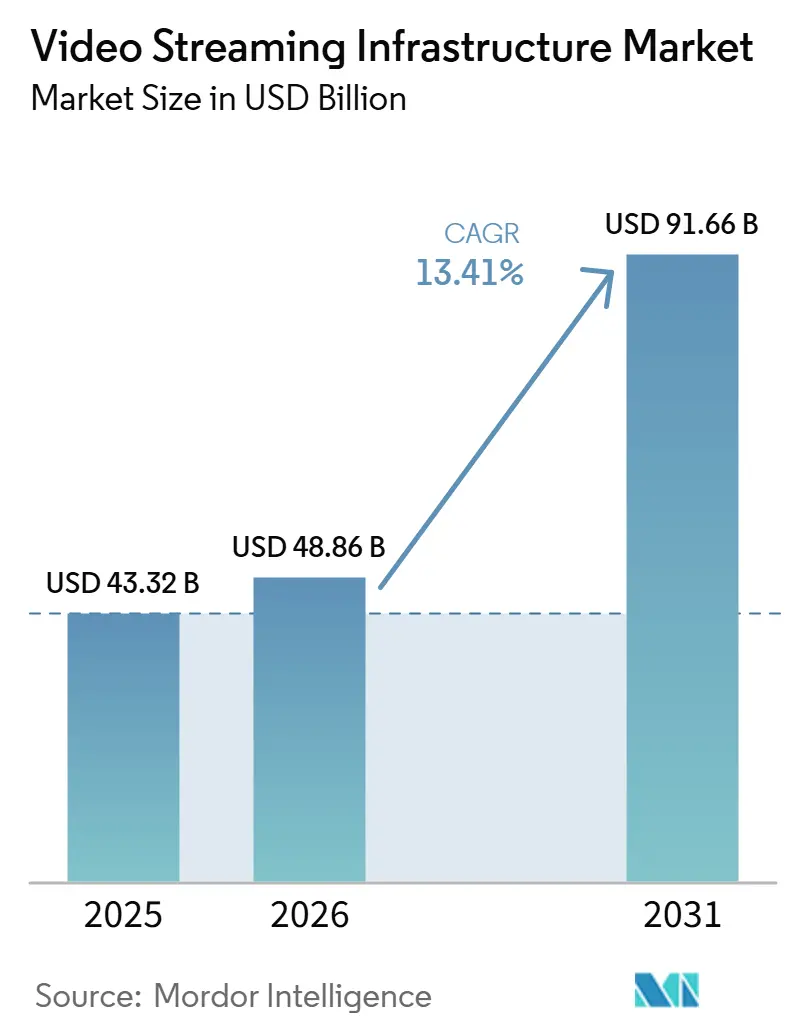

| Market Size (2026) | USD 48.86 Billion |

| Market Size (2031) | USD 91.66 Billion |

| Growth Rate (2026 - 2031) | 13.41% CAGR |

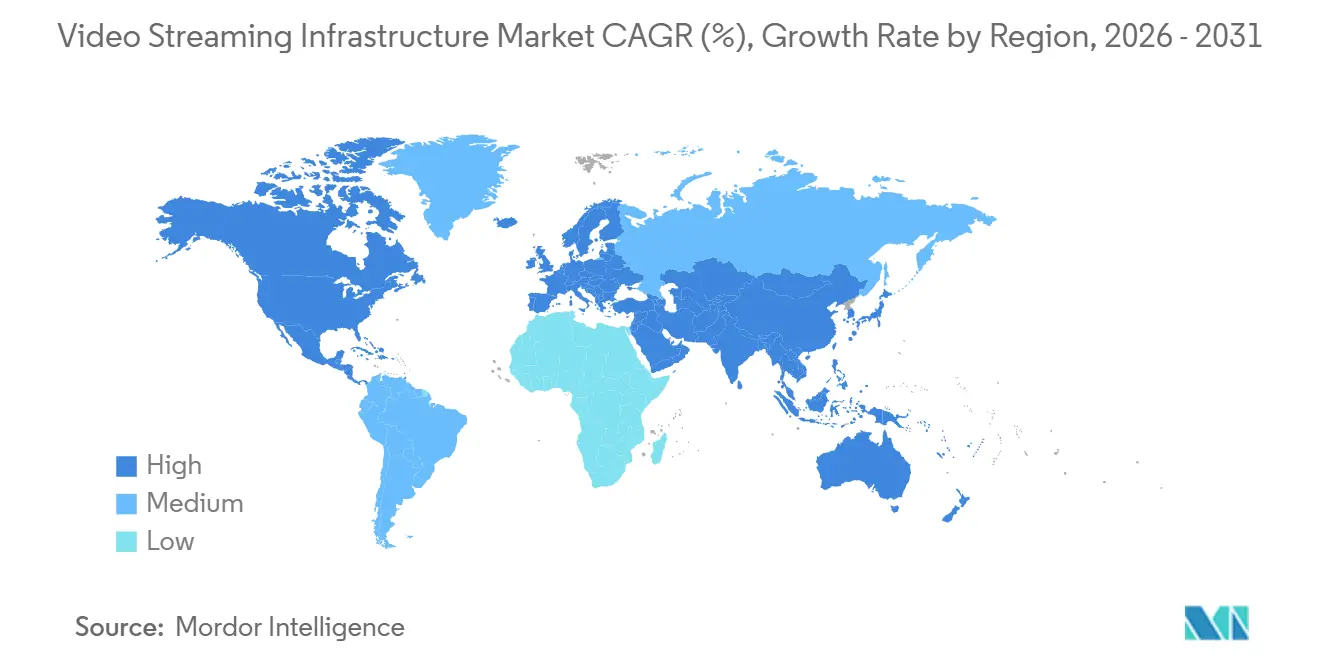

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Video Streaming Infrastructure Market Analysis by Mordor Intelligence

The Video streaming infrastructure market size was valued at USD 43.32 billion in 2025 and estimated to grow from USD 48.86 billion in 2026 to reach USD 91.66 billion by 2031, at a CAGR of 13.41% during the forecast period (2026-2031). The Video streaming infrastructure market is expanding because audiences continue shifting from linear television toward on-demand and live digital viewing, which keeps raising the need for reliable, scalable, and low-latency delivery systems. Investment is also moving deeper into cloud-based media orchestration, encoding, transcoding, CDN density, and quality monitoring, because operators now need performance control across larger video libraries and more frequent traffic spikes. Competitive activity remains strong as hyperscalers bundle more services into unified platforms, while specialist vendors defend their position through low-latency delivery, codec efficiency, piracy control, and event-grade reliability. The Video streaming infrastructure market is also gaining support from hybrid deployment strategies, where broadcasters keep latency-sensitive workloads on site and move orchestration, metadata, and analytics into cloud environments. The Video streaming infrastructure market still faces cost and compliance pressure from rising transcoding loads, fragmented device compatibility, weak metadata quality, and data residency requirements, yet these same constraints are creating new openings for regional edge nodes, workflow automation, and managed infrastructure services.

Key Report Takeaways

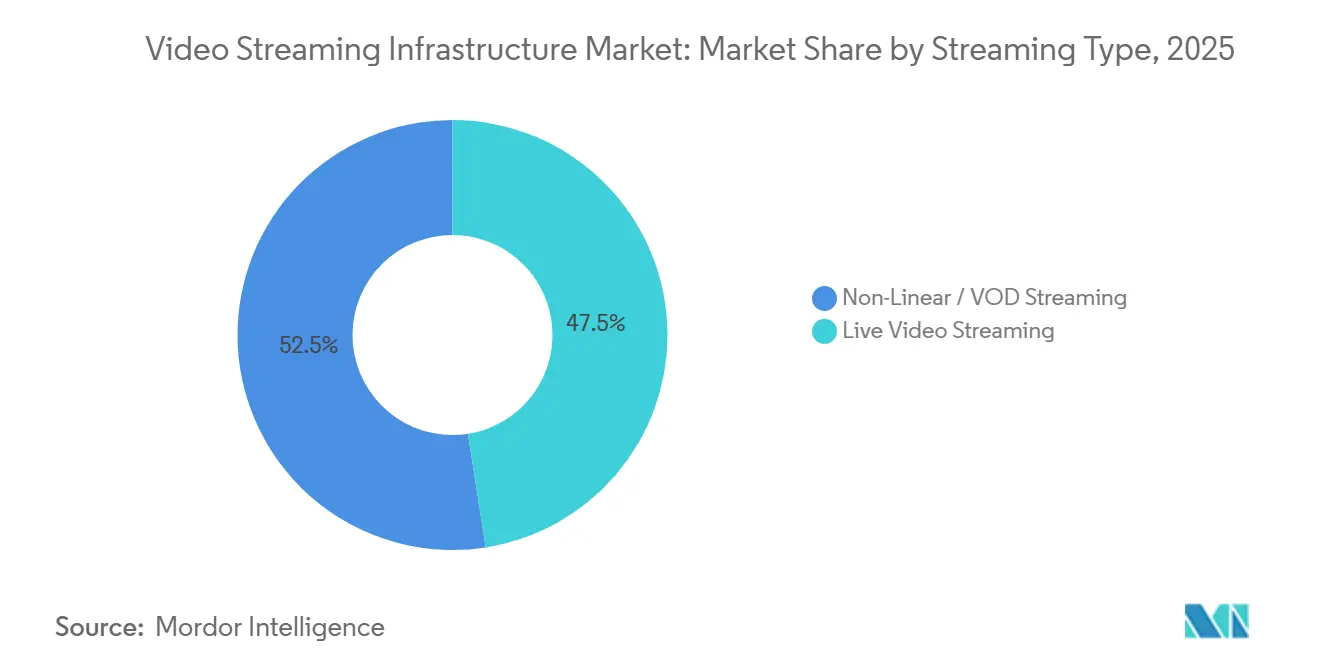

- By streaming type, Non-Linear and VOD streaming held 52.47% share in the video streaming infrastructure market in 2025, while Live video streaming is projected to expand at 17.33% CAGR through 2031.

- By component, Software held 51.87% share in the video streaming infrastructure market in 2025, while Services is projected to expand at 15.24% CAGR through 2031.

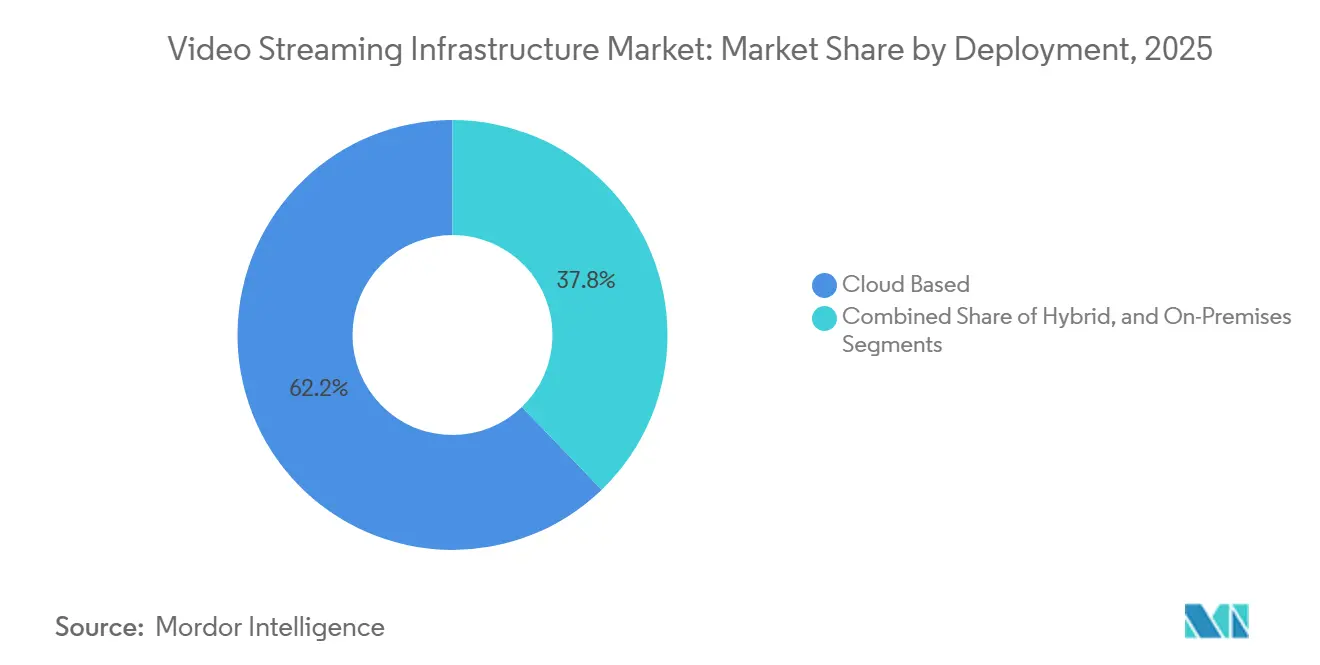

- By deployment, Cloud-based held 62.21% share in the video streaming infrastructure market in 2025, while Hybrid is projected to expand at 16.21% CAGR through 2031.

- By end user, Media and entertainment held 39.94% share in the video streaming infrastructure market in 2025, while Sports and live events is projected to expand at 17.85% CAGR through 2031.

- By geography, North America held 36.63% share in the video streaming infrastructure market in 2025, while Asia-Pacific is projected to expand at 15.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Video Streaming Infrastructure Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Low-Latency Live Events | +2.8% | Global, with concentrated impact in North America, Europe, and APAC | Short term (≤ 2 years) |

| AI-Based Video Workflow Automation and Localization | +2.3% | Global, highest adoption in North America and APAC | Medium term (2-4 years) |

| Expanding CDN and Edge Compute Capacity for Peak Traffic Delivery | +2.1% | Global, highest density in North America, Europe, and APAC core, with spillover to Middle East and Africa | Short term (≤ 2 years) |

| Cloud-Native Streaming Operations Reducing Capex Burden | +1.9% | Global, accelerated adoption in APAC and Middle East and Africa | Medium term (2-4 years) |

| Ad-Supported and Hybrid Monetization Expanding Delivery Volumes | +1.5% | North America and Europe primary, with spillover to South America and APAC | Medium term (2-4 years) |

| 5G Multicast and Broadcast Streaming Use Cases | +0.9% | Europe, APAC, and emerging Middle East and Africa markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Low-Latency Live Events

Live sports and premium event delivery remain the most immediate reason for new infrastructure spending across the Video streaming infrastructure market. Rights holders now need systems that can support very large concurrent audiences while keeping picture quality stable and delay tightly controlled. Lenovo said its FIFA World Cup 2026 deployment used near real-time AI-powered infrastructure and on-premise edge computing because cloud-only delivery did not meet broadcast-grade latency needs. MainStreaming also expanded the DAZN Edge footprint ahead of the FIFA Club World Cup 2025, showing that leading sports platforms are investing in private edge capacity rather than relying only on third-party CDN coverage. Akamai Media Services Live 5 then pushed low-latency HLS delivery toward a 5 to 7 second baseline, which makes higher performance expectations harder to avoid in future sports rights contracts.

AI-Based Video Workflow Automation and Localization

AI-led automation is lowering the time and labor needed to prepare, label, localize, and publish video at scale, which is raising the operating range of the Video streaming infrastructure market. That matters because content owners now need more versions of the same asset across languages, platforms, formats, and monetization models. Brightcove added automated metadata creation, caption generation, AI translation, audio dubbing, and 4K UHD live streaming with delays as low as 8 seconds in its July 2025 platform update. Wowza launched its Video Intelligence Framework in April 2026 to generate real-time metadata, clips, alerts, and machine-readable event signals inside live workflows, which reduces post-stream processing delays and manual handoffs.[1]Wowza Media Systems, “Wowza Launches Video Intelligence Framework,” Wowza, wowza.com As these tools become standard, smaller broadcasters can expand into multi-language catalogues faster because localization and metadata work no longer require the same manual overhead that once limited international scaling.

Expanding CDN And Edge Compute Capacity for Peak Traffic Delivery

The Video streaming infrastructure market is moving from static caching toward edge environments that can also process media tasks closer to the viewer. This shift is important because the same platform now often needs to handle delivery, playback intelligence, ad insertion, and workload balancing during the same traffic burst. Akamai and Bitmovin launched Akamai Adaptive Media Player 2 in October 2025, combining playback, analytics, and delivery tools to improve OTT and direct-to-consumer performance under heavier usage conditions.[2]Akamai Technologies, Inc. and Bitmovin Inc., “Akamai Adaptive Media Player 2, Bitmovin and Akamai Set New Streaming Standard,” Akamai, akamai.com The AVIA 2026 Asia Video Industry Report also noted that long-haul, centralized CDN models can create congestion during national live events, which is pushing operators toward ISP-embedded caching and more distributed traffic management. As this model spreads, ISPs are becoming more active commercial partners in video delivery because better caching placement now has a direct effect on service quality and cost control.

Cloud-Native Streaming Operations Reducing Capex Burden

Cloud-native operations are helping the Video streaming infrastructure market attract buyers that want flexibility without carrying large, fixed hardware investments. Media companies are under pressure to align spending with actual usage, especially when audience spikes are event driven and hard to predict. Harmonic extended its hybrid streaming platform in April 2026 with cloud-native deployment on Red Hat OpenShift and Model Context Protocol support for AI application connectivity, which shows how orchestration is shifting into more modular environments. Bitmovin’s May 2026 agreement with MUBI showed the same direction, replacing a legacy on-premises encoding stack with cloud-based VOD encoding through AWS Marketplace and a multi-codec workflow built around AVC, HEVC, and AV1. The practical result is that cloud migration is no longer only a cost decision, because buyers also want elastic computing for AI inference, faster codec updates, and simpler platform operations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Bandwidth and Transcoding Cost Burden | -1.8% | Global, most acute in North America and APAC high-volume markets | Short term (≤ 2 years) |

| Fragmented Device, Codec, and Player Compatibility | -1.3% | Global, most complex in APAC and Middle East and Africa with diverse device ecosystems | Medium term (2-4 years) |

| Privacy, Rights, and Data Residency Constraints | -1.0% | Europe and North America primarily, expanding to APAC and Middle East | Long term (≥ 4 years) |

| Peak-Time Quality of Service Instability in Emerging Networks | -0.7% | APAC developing markets, South America, and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Bandwidth and Transcoding Cost Burden

The cost side of the Video streaming infrastructure market is rising because better compression is coming with heavier compute requirements and more complex delivery stacks. Operators now need to support more formats, higher resolutions, and more frequent concurrency peaks at the same time that monetization models are still shifting. Meta Engineering said in June 2026 that adopting AV1 for real-time communication at scale required significant computational investment, even though the codec improved bandwidth efficiency. Bitmovin’s work with MUBI also reflected this pressure, because a cloud-based multi-codec workflow can be easier to scale than refreshing owned encoding hardware for AVC, HEVC, and AV1 support.[3]Bitmovin Inc., “Bitmovin Powers Global Film Streaming Platform, MUBI,” Bitmovin, bitmovin.com These cost pressures weigh most heavily on mid-tier operators, which face the same resolution and codec expectations as top-tier platforms but do not have the same pricing leverage or installed scale.

Fragmented Device, Codec, And Player Compatibility

Compatibility remains a stubborn drag on the Video streaming infrastructure market because every new code or delivery improvement still has to work across uneven device estates. Large smart TVs, legacy set-top boxes, streaming sticks, and mobile phones do not move to new decode standards at the same speed. Meta Engineering noted in September 2025 that software AV1 decoding on mobile devices can hurt battery performance, which keeps mobile support more difficult than large-screen support in many real-world use cases.[4]Meta Engineering, “Adopting AV1 for Real-Time Communication (RTC) at Scale,” Meta Engineering, engineering.fb.com Bitmovin said its automated testing infrastructure processed more than 1 million tests per week to identify playback issues across device and codec combinations, which shows how much operational effort this fragmentation creates. As long as older devices remain active, platforms will keep carrying overlapping encoding ladders, fallback logic, and player validation work that do not decline as quickly as vendors would like.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Streaming Type: Non-Linear and VOD streaming Commands Scale, Live Video Accelerates

Non-Linear and VOD streaming held 52.47% share in 2025, which confirms that on-demand viewing remained the largest current use case inside the Video streaming infrastructure market. VOD demand favors deep caching, efficient encoding, and stable adaptive bitrate delivery because viewers expect consistent performance across large catalogues and repeated sessions. In this segment, scale comes less from one-time traffic bursts and more from how efficiently platforms can serve a wide content library across many devices and access networks. That makes cost control and playback consistency more important than ultra-low delay in many VOD-heavy deployments. VOD therefore keeps anchoring baseline infrastructure spending even as newer workloads attract more growth attention.

Live video streaming was the faster-moving side of this segment and is projected to expand at 17.33% CAGR from 2026 to 2031. The growth is tied to sports rights migration, larger virtual event calendars, and stronger direct-to-consumer ambitions from content owners that want a direct billing and advertising relationship. Live delivery needs real-time encoding, tighter latency control, rapid concurrency scaling, and stronger observability than the VOD model usually requires. Many operators are also linking live and on-demand workflows so recorded streams become replay assets within minutes, which reduces the need for separate pipeline designs. That blending of formats means the video streaming infrastructure industry is increasingly building around unified operations rather than isolated VOD and live systems.

By Component: Software Anchors Revenue, Services Drive Growth

Software accounted for 51.87% share in 2025 and encoding and transcoding represented 31.13% of the software sub-segment, showing how central compute-heavy processing remained to platform economics. This made software the anchor of recurring control in the Video streaming infrastructure market because encoding logic, orchestration, playback intelligence, and monitoring all sites close to daily operations. Video analytics and quality-of-experience monitoring is also projected to grow at 15.89% CAGR by 2031, as operators move from reactive troubleshooting toward predictive performance management. That shift matters because viewer churn, ad delivery failure, and latency spikes now have direct revenue consequences in both subscription and ad-supported models. Software vendors with strong observability and workflow automation are therefore gaining more influence over buying decisions.

Services is the fastest-growing top-level component and is projected to expand at 15.24% CAGR from 2026 to 2031. Comcast Technology Solutions launched Comcast Media360 in April 2025 as a managed service that combines video management, OTT delivery, and social media distribution in one operating model. This service-led pattern reflects a broader preference for operating flexibility, because buyers increasingly want outcomes and uptime rather than more owned hardware. Hardware still has a role in specialized environments, but its relative position is weakening as more functions move into software-defined or managed environments. Across the video streaming infrastructure industry, the center of value is shifting toward platforms and service layers that can keep media operations running with less internal operational strain.

By Deployment: Cloud Leads, Hybrid Architecture Closes the Gap

Cloud-based deployment held 62.21% share in 2025, which means it accounted for the largest portion of current spending in the Video streaming infrastructure market. Its lead came from elastic scaling, easier geographic reach, and the ability to expand capacity without long hardware procurement cycles. This model suits broadcasters, OTT platforms, and enterprises that face variable traffic and need quick rollout across multiple regions. It also supports faster codec changes and integrated analytics because these capabilities can be updated centrally across a wider installed base. For many buyers, cloud adoption has moved from a pilot choice to a standard operating approach.

Hybrid deployment is projected to expand at 16.21% CAGR from 2026 to 2031, and the video streaming infrastructure market size for this deployment model is growing because operators want both control and flexibility. Broadcasters and telcos are keeping latency-sensitive production and deterministic encoding closer to owned environments while moving orchestration, metadata workflows, and analytics into cloud layers. Harmonic’s April 2026 update showed how hybrid stacks are evolving, combining cloud-native deployment with AI connectivity while still serving broadcast-grade workflows. Hybrid adoption is also being reinforced by sovereignty and localization demands, because some operators need regional processing nodes even when centralized delivery would be cheaper. That keeps hybrid architecture positioned as a practical long-run model rather than a short transitional phase.

By End User: Media And Entertainment Anchors Spend, Sports Races Ahead

Media and entertainment held 39.94% of the video streaming infrastructure market share in 2025, making it the largest current end-user group. This leadership reflects the ongoing modernization of legacy broadcast systems, streaming-native platforms, studio operations, and post-production workflows into more cloud-aware video environments. These companies require infrastructure not only for content delivery but also for packaging, rights management, archive access, metadata handling, and monetization support. The size of this installed base provides the video streaming infrastructure market with a stable revenue anchor even as newer buyer segments continue to expand. It also results in long-term vendor relationships that often span multiple products and extended operating cycles.

Sports and live events are projected to expand at a 17.85% CAGR from 2026 to 2031, making it the fastest-growing end-user segment. This growth reflects the increasing shift toward direct-to-consumer streaming models and high-concurrency global event delivery. Enterprise, education, telecom, and government segments also remain significant contributors, driven by demand for secure webcasting, internal video communication, and regulated digital workflows. At the same time, vendors are increasingly extending their offerings beyond core streaming infrastructure into broader AI-driven digital experience platforms, expanding their role across the video value chain.

Geography Analysis

North America held 36.63% of the video streaming infrastructure market share in 2025, maintaining its position as the largest regional revenue contributor. The region benefits from mature subscription habits, strong digital advertising depth, dense data center coverage, and a large base of premium video services. The United States remains the main demand center because it combines sports, media, enterprise, and platform scale in one market. Canada and Mexico also contribute demand through bilingual and cross-border content needs, which increase the importance of localization and workflow flexibility. Even with a mature base, the video streaming infrastructure market in North America still has room to expand through hybrid operations, event streaming, and broader AI-driven media workflows.

Europe remains an important region in the video streaming infrastructure market because its streaming transition is shaped by both content economics and regulatory compliance. Demand patterns are fragmented across the region because national broadcast systems, rights structures, and monetization models still vary widely by country. This makes multi-country rollout more complex and encourages vendors to offer more modular deployment and workflow options. Data residency and data transfer requirements also influence infrastructure topology, supporting continued demand for regional processing nodes and localized delivery design. In the Middle East and Africa, Gulf markets are investing more actively in digital media systems, while several Sub-Saharan markets still face network quality limitations that can slow near-term deployment, even as mobile video demand continues to rise.

Asia-Pacific is projected to expand at a 15.98% CAGR from 2026 to 2031, making it the fastest-growing geography in the video streaming infrastructure market. The region is being driven by mobile-first consumption habits, strong demand for local premium content, and heavy live-streaming traffic across large user bases. AVIA reports that the regional online video sector reached USD 70 billion in revenue by the end of 2025, highlighting the scale already supporting new delivery investments. AVIA also identifies India as a global reference point for mobile-first live delivery architecture, underscoring why the region is setting important performance benchmarks for future deployments.

Competitive Landscape

The video streaming infrastructure market remained moderately fragmented in 2026, with hyperscalers, specialist software vendors, edge delivery firms, and managed service providers all competing across different layers. AWS, Microsoft Azure, and Google Cloud hold a structural advantage in cloud deployment because they can bundle storage, CDN, transcoding, analytics, and global infrastructure within a broad service portfolio. That scale creates pricing pressure in more standardized workflow categories, especially where delivery and encoding functions are already mature. However, the market still leaves room for specialists because latency, piracy control, event reliability, and codec performance are not fully commoditized. Buyers continue to distribute spending across multiple vendors when no single platform can meet all operational and contractual requirements.

Consolidation is reshaping the video streaming infrastructure market as vendors aim to combine broadcast-grade tools with cloud-native delivery capabilities. Harmonic completed the divestiture of its video business to MediaKind in June 2026 for USD 145 million, strengthening MediaKind’s end-to-end position across broadcast and OTT delivery. Fox Corporation also announced plans to acquire Roku in June 2026, linking premium content and sports rights with a connected TV platform that reaches 100 million global streaming households. These developments reflect a growing connection between infrastructure strategy, distribution control, ad monetization, and household reach. They also suggest that ownership of the user relationship is becoming almost as important as control of the underlying delivery stack.

Strategic differentiation in the video streaming infrastructure market is now centered on AI integration, workflow depth, and edge specialization. Bitmovin’s Q1 2026 product roadmap introduced AI-based scene detection for smarter SCTE marker insertion, HDR10+ encoding support, and enhanced workflow observability, reflecting how software vendors are strengthening their technical differentiation. Synamedia and SoFast have also focused on simplifying the launch process for FAST, Pay TV, and VOD services, highlighting how time-to-market has become as important a competitive factor as infrastructure scale. Emerging 5G multicast and broadcast standards could further expand opportunities over time, as 3GPP Release 19 provides a clearer path toward stadium-scale and event-scale delivery models with lower incremental cost per viewer.

Video Streaming Infrastructure Industry Leaders

Amazon Web Services, Inc.

Akamai Technologies, Inc.

Microsoft Corporation

Cisco Systems, Inc.

Alphabet Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: MediaKind completed the USD 145 million acquisition of Harmonic Inc.'s Video Business, combining Harmonic's broadcast-grade encoding technology with MediaKind's cloud streaming platform. The transaction positions MediaKind as a strengthened end-to-end video delivery vendor for both broadcast and OTT clients globally.

- June 2026: Fox Corporation announced a definitive agreement to acquire Roku, Inc. for approximately USD 22 billion in a combination of cash and Fox Class A common stock, uniting Fox's sports, news, and Tubi FAST service with Roku's connected TV platform and its direct relationship with 100 million global streaming households. The transaction is expected to close in the first half of 2027, pending regulatory and shareholder approvals.

- May 2026: Bitmovin announced a strategic agreement with MUBI, the global film streaming platform, to replace MUBI's legacy on-premises encoding stack with Bitmovin's VOD Encoder via AWS Marketplace, supporting 3-pass encoding, UHD, and a multi-codec strategy spanning AVC, HEVC, and AV1.

- April 2026: Wowza Media Systems launched the Video Intelligence Framework, enabling organizations to apply AI directly inside live streaming workflows to generate real-time metadata, clips, and machine-readable event signals without separate post-stream processing pipelines

Global Video Streaming Infrastructure Market Report Scope

The Video Streaming Infrastructure Market Report is Segmented by Streaming Type (Live Video Streaming, and Non-Linear / VOD Streaming), Component (Software, Services, and Hardware), Deployment (Cloud-Based, On-Premises, and Hybrid), End User (Media and Entertainment, Sports and Live Events, Telecommunications, Enterprises, Education, Government and Public Sector, and More), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Live Video Streaming |

| Non-Linear / VOD Streaming |

| Software | Encoding and Transcoding Solutions |

| Video Player Solutions | |

| Video Analytics and QoE Monitoring | |

| Media Workflow Orchestration | |

| Other Software Components | |

| Services | |

| Hardware |

| Cloud-based |

| On-Premises |

| Hybrid |

| Media and Entertainment |

| Sports and Live Events |

| Telecommunications |

| Enterprises |

| Education |

| Government and Public Sector |

| Other End Users |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Qatar | ||

| Turkey | ||

| Rest of the Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Streaming Type | Live Video Streaming | ||

| Non-Linear / VOD Streaming | |||

| By Component | Software | Encoding and Transcoding Solutions | |

| Video Player Solutions | |||

| Video Analytics and QoE Monitoring | |||

| Media Workflow Orchestration | |||

| Other Software Components | |||

| Services | |||

| Hardware | |||

| By Deployment | Cloud-based | ||

| On-Premises | |||

| Hybrid | |||

| By End User | Media and Entertainment | ||

| Sports and Live Events | |||

| Telecommunications | |||

| Enterprises | |||

| Education | |||

| Government and Public Sector | |||

| Other End Users | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Qatar | |||

| Turkey | |||

| Rest of the Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current and forecast value of video streaming infrastructure?

The Video streaming infrastructure market was valued at USD 43.32 billion in 2025, stands at USD 48.86 billion in 2026, and is forecast to reach USD 91.66 billion by 2031 at a 13.41% CAGR.

Which content format drives the largest current demand?

Non-Linear and VOD led with 52.47% share in 2025, showing that on-demand viewing still generates the broadest base of infrastructure spending.

Which deployment model is growing the fastest?

Hybrid deployment is projected to expand at 16.21% CAGR through 2031 because many operators want cloud flexibility while keeping latency-sensitive functions closer to owned environments.

Why are sports platforms investing more heavily in delivery systems?

Sports and live events is the fastest-growing end-user segment at 17.85% CAGR, and rights holders increasingly want direct-to-consumer control, better latency, and stronger event reliability.

Which region offers the strongest growth opportunity?

Asia-Pacific is forecast to grow at 15.98% CAGR through 2031, supported by mobile-first viewing habits, large live audiences, and rising premium online video revenue.

What is the main operational challenge for providers today?

The biggest pressure comes from rising transcoding and bandwidth costs, along with codec and device fragmentation that forces platforms to support multiple delivery profiles at the same time.

Page last updated on: