Screen Recording Software Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

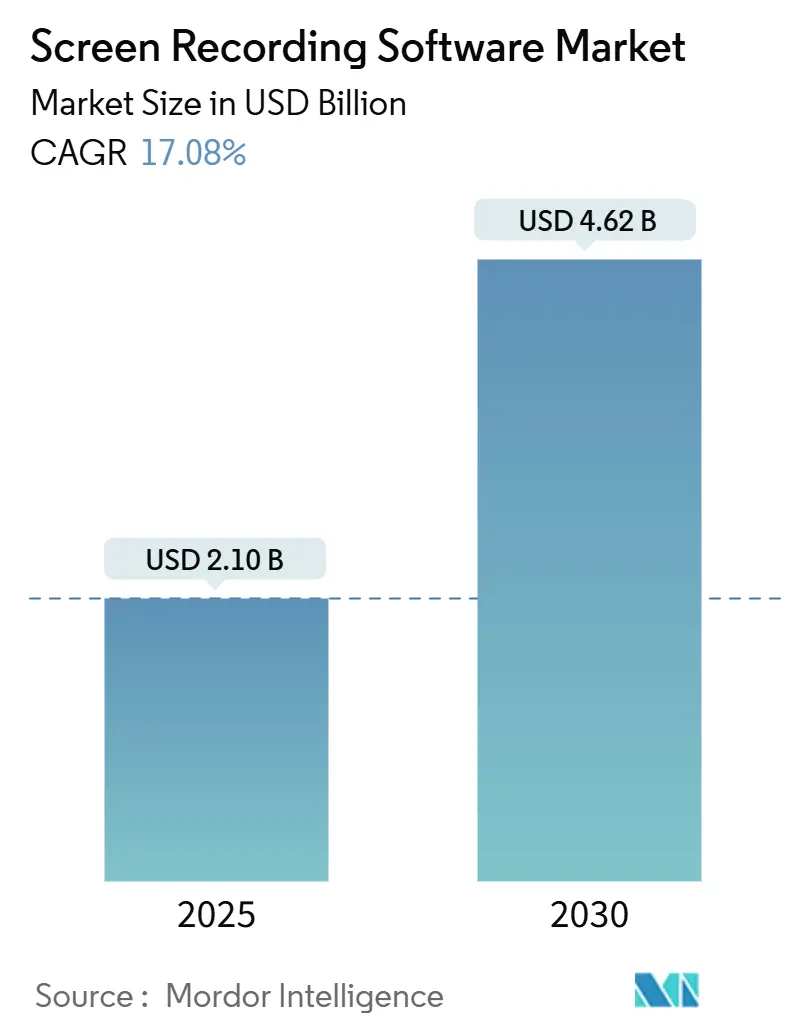

| Market Size (2025) | USD 2.10 Billion |

| Market Size (2030) | USD 4.62 Billion |

| Growth Rate (2025 - 2030) | 17.08% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

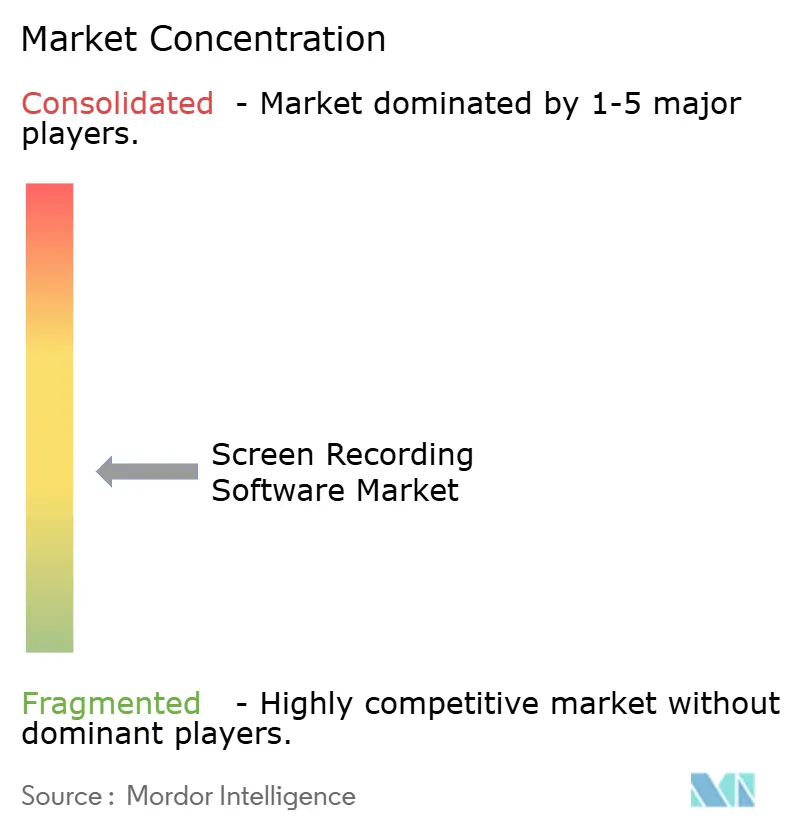

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Screen Recording Software Market Analysis by Mordor Intelligence

The screen recording software market size stands at USD 2.10 billion in 2025 and is projected to climb to USD 4.62 billion by 2030, reflecting a 17.08% CAGR across the forecast horizon. Three forces sustain this trajectory, including hybrid work that makes asynchronous video essential, AI features that eliminate editing skill barriers, and platform consolidation, such as Atlassian’s USD 975 million acquisition of Loom. Vendors now differentiate with enterprise-grade compliance, cloud-native storage, and vertical integrations that built-in OS tools lack. Yet basic recording baked into Windows 11 and macOS Sequoia is compressing the entry-level license pool, pushing suppliers upmarket toward regulated industries. This competitive pivot accelerates AI-centric roadmaps, fosters deeper identity-provider ties, and drives a clear shift to browser-based deployment, reducing IT overhead.

Key Report Takeaways

- By product type, desktop and laptop software led the screen recording software market with a 54.12% share in 2024. Cloud-native platforms are projected to expand at a 19.15% CAGR through 2030.

- By deployment mode, cloud-based offerings commanded a 3.32% share in 2024. On-premises solutions serving data-restricted buyers are expected to post a 19.3% CAGR to 2030.

- By operating system, Windows retained a 49.56% share in 2024. Android is forecasted to grow at 18.76% through 2030, driven by mobile creator adoption in the Asia Pacific.

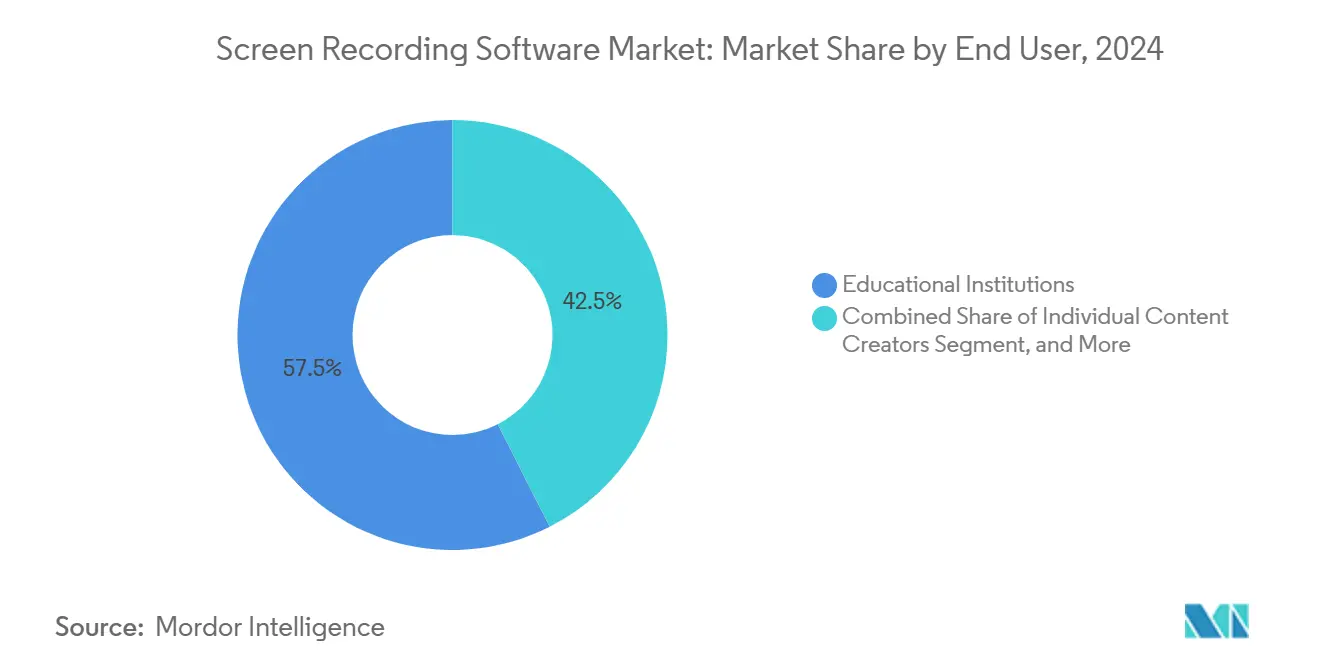

- By end user, educational institutions captured 57.48% revenue in 2024. Large enterprises are expected to grow at a 19.12% CAGR as video-first support reduces resolution times.

- By application, training, and onboarding held a 40.29% share in 2024. Customer support and troubleshooting is projected to grow at 18.69% to 2030.

- By geography, North America led with 38.46% share in 2024. Asia Pacific is forecast to advance at 19.36% CAGR through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Screen Recording Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Remote Work and E-Learning Adoption | +3.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Expansion of the Creator Economy and User-Generated Video | +3.2% | Global, led by Asia Pacific and North America | Long term (≥ 4 years) |

| Proliferation of Freemium SaaS Models Driving SME Uptake | +2.9% | Global, strongest in Asia Pacific and South America | Short term (≤ 2 years) |

| AI-Enabled Auto-Editing and Transcription Tools | +3.5% | North America and Europe, expanding to Asia Pacific | Medium term (2-4 years) |

| Regulatory Push for Secure Recording in Compliance-Intensive Sectors | +2.1% | North America and Europe, selective adoption in Middle East | Long term (≥ 4 years) |

| Emerging Demand for AR/VR Session Capture Capabilities | +1.6% | North America and Europe, pilot deployments in Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Remote Work and E-Learning Adoption

Screen recording shifted from a contingency tool to an everyday utility once work-from-home models became permanent. Vimeo reported a 65% surge in corporate video creation since 2023; yet, 57% of firms still lack a coherent video strategy. Universities retained pandemic lecture-capture rigs because recordings aid accessibility, accommodate working students, and build reusable content libraries. The University of Nevada, Las Vegas, installed 200 Pearl Nexus units across campuses in 2024, demonstrating a capital commitment to video-first pedagogy. Asynchronous clips now replace many live meetings, enabling teams in distant time zones to exchange knowledge without scheduling friction. This habit underpins the long-run demand curve for the screen recording software market.

Expansion of the Creator Economy and User-Generated Video

User-generated content matured into a dependable income stream. Vidyard logged 943,305 videos in 2024, a 88% increase, while the average creator published 37 clips, proving that video is a daily workflow. Mobile apps, such as XRecorder, have exceeded 100 million installs, attracting smartphone-first creators who lack desktop editors. TechSmith research shows 83% of learners prefer video for step-by-step guidance, pushing demand for frictionless recording-to-publish pipelines. As sponsor revenue and platform payouts scale, creators invest in pro-grade tools with premium analytics, propelling the screen recording software market ahead of general productivity averages.

Proliferation of Freemium SaaS Models Driving SME Uptake

Freemium tiers have erased price barriers for smaller organizations. Loom grew to 25 million users and USD 50 million annual recurring revenue by letting staff share watermarked clips that attracted colleagues, creating viral loops. SMEs test value-like lower support ticket volume before upgrading. Vimeo found the typical company now juggles five video tools, so niche SaaS vendors exploit integration agility rather than chase monolithic replacements. This low-risk entry accelerates user counts and underpins double-digit revenue growth.

AI-Enabled Auto-Editing and Transcription Tools

Artificial intelligence removes post-production bottlenecks. TechSmith embedded AI Dynamic Captions and one-click noise removal in Camtasia 2025, bringing studio-level polish to non-experts. Wondershare’s Filmora v14 auto-translates speech and adjusts lip sync for localized output. With speech-to-text engines achieving sub-5% error rates, enterprises can index recordings and search moments buried in thousands of hours, making video knowledge bases a practical solution. AI boosts adoption among business units that have been deterred by editing complexity, thereby strengthening the growth curve of the screen recording software market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Built-In OS Recording Features Erode Paid Adoption | -2.3% | Global, most pronounced in consumer and SME segments | Short term (≤ 2 years) |

| High Bandwidth and Cloud-Storage Cost Pressures | -1.8% | Global, acute in regions with metered data plans | Medium term (2-4 years) |

| Heightened Data-Privacy and Consent Compliance Burden | -1.4% | Europe and North America, emerging in Asia Pacific | Long term (≥ 4 years) |

| Antitrust Scrutiny of Platform Bundling and Algorithmic Pricing | -0.9% | North America and Europe, regulatory focus on tech giants | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Built-In OS Recording Features Erode Paid Adoption

Windows 11’s Snipping Tool and macOS’s Screenshot app now record screens with voiceover, meeting the basic needs for quick bug demos or walkthroughs.[1]Apple, “macOS Sequoia Screen Recording Guide,” apple.com Their ubiquity compresses entry-level demand, forcing vendors to justify subscriptions through cloud collaboration, analytics, and compliance. The effect is sharpest among consumers and budget-conscious SMEs that view advanced editing as a nice-to-have. Vendors are responding by moving upmarket, bundling identity-provider hooks and security certifications, but the near-term drag on unit growth is clear.

High Bandwidth and Cloud-Storage Cost Pressures

A one-hour 1080p clip can exceed 1 GB; storing thousands of drives on AWS S3 incurs a monthly bill of USD 0.023/GB, plus egress fees.[2]Amazon Web Services, “Amazon S3 Pricing,” aws.amazon.com Emerging-market users on metered data plans are hesitant to upload footage, which slows mobile SaaS adoption. Vendors deploy variable-bitrate encoding and on-device caching, yet these add engineering expense and split the user experience. Institutions on tight budgets must choose between shorter retention windows and higher cloud invoices, tempering volume growth even as demand remains high.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cloud-Native Platforms Gain Ground

The screen recording software market size for SaaS offerings is forecast to expand at 18.24% CAGR, nearly double that of perpetual-license desktop tools. Desktop and laptop software retains a 54.12% share of total installations because many IT departments standardized on Camtasia or Captivate years ago, valuing offline editing and multi-track control for high-resolution tutorials. SaaS vendors are courting these holdouts with downloadable recorders that sync to the cloud after capture, blending traditional fidelity with modern collaboration.

Desktop revenue is expected to plateau as perpetual upgrades migrate to subscription plans. Yet production houses requiring 4K capture and offline rendering will keep desktop SKUs relevant. Meanwhile, mobile apps form the fastest-growing sub-niche as smartphone creators record social-media snippets in a single tap. XRecorder’s install base above 100 million evidences a low-friction mobile opportunity. In the long term, the proliferation of progressive web apps could converge mobile and desktop UX within the browser, further skewing adoption toward cloud-native designs.

By Deployment Mode: Cloud Dominance Reflects Hybrid Collaboration

Cloud installations command over a 60% share because hybrid teams expect files to sync instantly, and admins favor single sign-on with Okta or Azure Active Directory. The screen recording software market share for cloud deployment reached 63.32% in 2024, and usage-based pricing enables SMEs to scale without upfront server costs. Organizations in healthcare or finance that require data residency still maintain on-premises nodes for raw video storage, but metadata is increasingly stored in the vendor cloud for indexing. Vendors with ISO 27001 and SOC 2 attestations win cautious buyers who need audit trails.

On-premises licenses decline to niche status yet remain sticky due to procurement cycles and sunk infrastructure. Hybrid modes, such as local capture with optional cloud publish, offer a migration path, allowing risk-averse enterprises to experiment before making a full transition. Over the period to 2030, the on-premises CAGR is forecasted at low single digits, primarily driven by replacement sales.

By Operating System: Windows Leads, Android Accelerates

Windows machines account for 49.56% of active licenses, powered by global enterprise desktop dominance. macOS remains influential among creative professionals, but its volume is smaller. Linux garners open-source enthusiasts who rely on OBS Studio. The screen recording software market size for Android is expected to triple by 2030 as mobile creators in India, Indonesia, and Vietnam increasingly produce tutorial and gaming content. Android’s 18.76% CAGR outpaces every desktop OS, reflecting the ubiquity of smartphones. iOS grows modestly due to device price ceilings in emerging markets, yet it enjoys a high ARPU because Apple users tend to buy premium apps.

Cross-platform toolkits such as Electron and Flutter now let vendors push simultaneous Windows, macOS, and Linux updates, narrowing feature gaps. Mobile-first vendors reciprocate by adding desktop viewers, hinting at a converged future where OS distinctions fade behind browser-centric workflows.

By End User: Education Dominates, Enterprises Accelerate

Higher-education institutions drove 57.48% of 2024 revenue as they embedded lecture capture into classroom design and accessibility mandates. This cohort values reliability and closed-caption accuracy more than flashy editing. The screen recording software market's contribution from large enterprises is forecast to rise swiftly, adding USD 0.7 billion in incremental revenue by 2030 as departments leverage video for support tickets and compliance evidence. SMEs enjoy freemium offerings, but churn remains high until workflows mature.

Use within individual creators numerically dwarfs institutional seats yet monetizes poorly; most creators rely on free tiers or open-source OBS. Vendors are increasingly funneling these users into affiliate programs that reward paid conversions, thereby converting volume into enterprise penetration through bottom-up adoption.

By Application: Training Holds but Customer Support Rises

Training and onboarding remain the core workflow, with a 40.29% share in 2024, as firms replace static PDFs with walk-through videos. Customer support outpaces all other segments at an 18.69% CAGR to 2030, as clips reduce back-and-forth emails. The screen recording software market size for support applications is forecast to surpass USD 1 billion mid-decade. Live streaming and gaming remain vibrant, but revenue is skewed toward tipping and sponsorship, rather than vendor subscription models. Product marketing and demos continue to grow steadily as SaaS sellers embed videos in outbound emails and LinkedIn messages.

In the longer term, AI analytics that flag when viewers pause or exit will enable trainers and support managers to refine content, thereby reinforcing ROI and justifying higher license tiers.

Geography Analysis

North America generated 38.46% of 2024 revenue and remains the premium ARPU region, thanks to early SaaS adoption and deep pockets in the enterprise sector. The screen recording software market size in the United States benefited from bundled sales of video capabilities with collaboration suites, snowballing renewals. Canada follows with government e-learning grants, while Mexico’s near-shoring boom drives the development of bilingual training content.

The Asia Pacific region registers the highest momentum, with a forecasted CAGR of 19.36%. India’s smartphone base surpasses 1 billion lines, fueling mobile tutorial demand, while Indonesia and Vietnam display similar patterns. Chinese creators monetize through Bilibili and Xiaohongshu, spurring localized app innovation. Regional data legislation is lighter than in Europe, easing cloud adoption. Sub-USD 10 monthly plans align with purchasing power, making freemium upsells effective.

Europe grows modestly because GDPR consent prompts add friction, yet sectors such as automotive and pharmaceuticals adopt screen recording for compliance documentation.[3]GDPR.eu, “Fines and Penalties,” gdpr.eu Vendors offer EU-hosted servers to win deals. The Middle East and Africa remain nascent but pilot projects in Saudi Arabia’s Vision 2030 schools and South Africa’s universities indicate latent potential once broadband costs drop. South America’s progress hinges on fiber rollout; Brazilian SMEs flock to free tiers until economic stability improves, creating a lagged monetization curve.

Competitive Landscape

Market fragmentation prevails, with no vendor holding more than a 15% share. TechSmith serves every Fortune 500 member with Camtasia and Snagit, leveraging direct sales and education discounts. Adobe competes in learning authoring with Captivate, which is bundled with Creative Cloud. Wondershare Filmora targets prosumers with frequent AI feature drops. Atlassian’s Loom acquisition integrates recording into Jira and Confluence, instantly exposing 25 million users to its stack. Microsoft and Google threaten paid incumbents by introducing baseline capture capabilities within Teams and Workspace, although the current feature depth lags behind that of third-party specialists.

Open-source OBS Studio dominates live streaming, siphoning price-sensitive gamers. Vertical-focused entrants pursue HIPAA or FERPA certifications, commanding premium pricing where compliance fines far exceed license costs.

Emerging players tackle AR/VR capture, relying on headset manufacturers as channel partners. Security certifications-ISO 27001, SOC 2 Type II-now figure prominently in RFPs, turning compliance into a moat for well-capitalized vendors.

Screen Recording Software Industry Leaders

TechSmith Corporation

Adobe Inc.

Wondershare Technology Group Co., Ltd.

Loom, Inc.

Screencastify, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: OBS Studio 32.0 shipped the Plugin Manager and NVIDIA RTX real-time filters.

- February 2025: TechSmith launched Camtasia 2025, featuring AI Dynamic Captions and single-window recording.

- January 2025: TechSmith has issued Camtasia 2025.0.3, which includes AI noise removal and Rev Media transcription ordering.

- January 2024: Atlassian finalized Loom acquisition for USD 975 million.

Global Screen Recording Software Market Report Scope

| Desktop/Laptop Software |

| Mobile Apps |

| Cloud-Native SaaS Platforms |

| On-Premises |

| Cloud-Based |

| Windows |

| macOS |

| Linux |

| iOS |

| Android |

| Individual Content Creators |

| Educational Institutions |

| Small and Medium Enterprises |

| Large Enterprises |

| Training and Onboarding |

| Live Streaming and Gaming |

| Product Demonstrations and Marketing |

| Customer Support and Troubleshooting |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Product Type | Desktop/Laptop Software | |

| Mobile Apps | ||

| Cloud-Native SaaS Platforms | ||

| By Deployment Mode | On-Premises | |

| Cloud-Based | ||

| By Operating System | Windows | |

| macOS | ||

| Linux | ||

| iOS | ||

| Android | ||

| By End User | Individual Content Creators | |

| Educational Institutions | ||

| Small and Medium Enterprises | ||

| Large Enterprises | ||

| By Application | Training and Onboarding | |

| Live Streaming and Gaming | ||

| Product Demonstrations and Marketing | ||

| Customer Support and Troubleshooting | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How big is the screen recording software market in 2025?

The screen recording software market size is valued at USD 2.10 billion in 2025.

What is the expected growth rate for screen-recording tools through 2030?

Market revenue is forecast to rise at a 17.08% CAGR, reaching USD 4.62 billion by 2030.

Which deployment model grows fastest?

Cloud-based deployment shows an 18.24% CAGR because teams favor browser access and scalable storage.

Which region offers the highest future upside?

Asia Pacific leads with a 19.36% CAGR thanks to smartphone proliferation and creator-economy monetization.

What application area will outpace others?

Customer support and troubleshooting is projected to expand at 18.69% as firms swap text tickets for video guides.

Who are the leading vendors?

TechSmith, Adobe, Wondershare, Atlassian’s Loom, and Microsoft are among the notable players, with no single firm exceeding 15% share.

Page last updated on: