Enterprise Video Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 28.98 Billion |

| Market Size (2031) | USD 46.93 Billion |

| Growth Rate (2026 - 2031) | 10.12% CAGR |

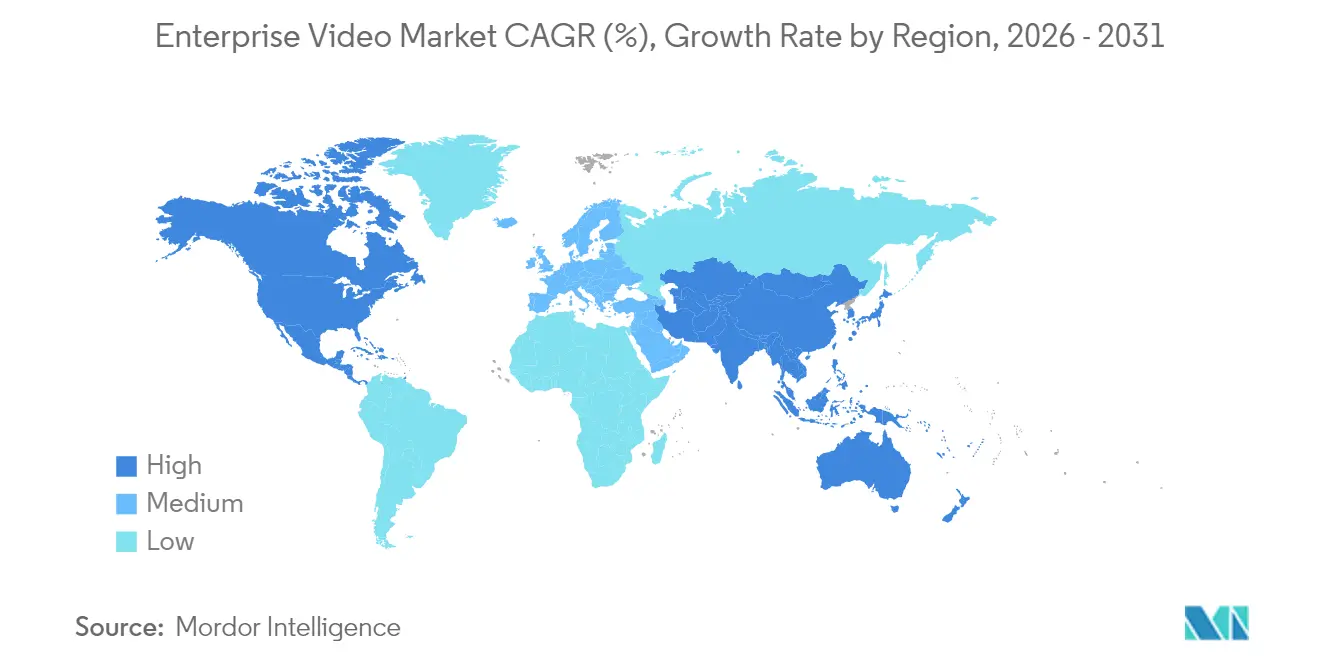

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

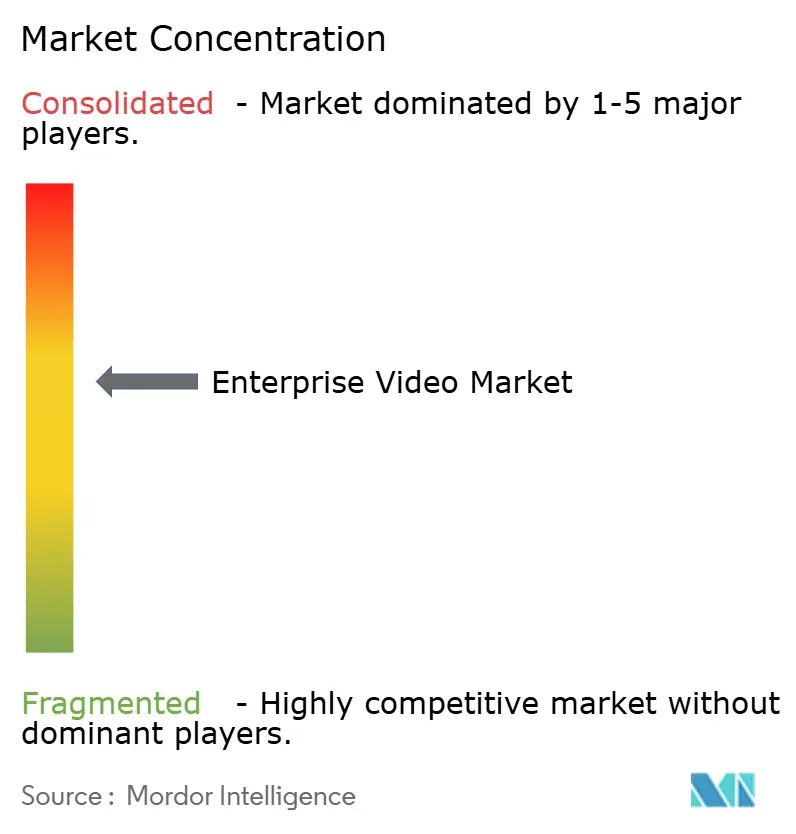

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Enterprise Video Market Analysis by Mordor Intelligence

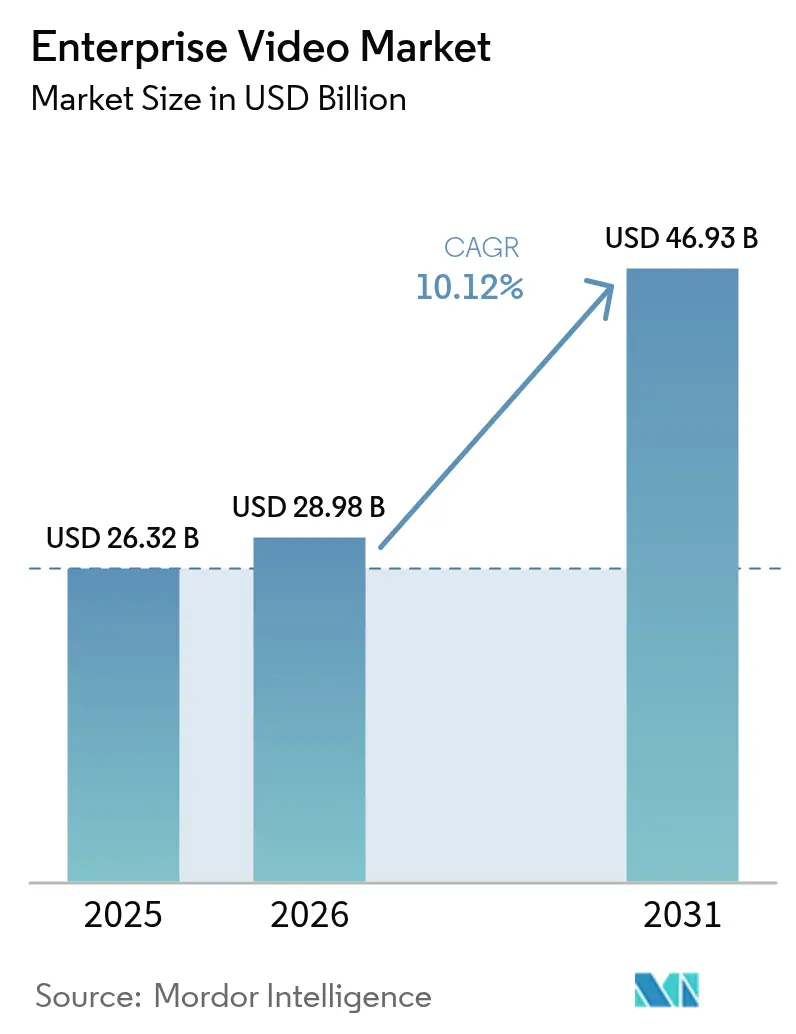

The enterprise video market size is expected to grow from USD 26.32 billion in 2025 to USD 28.98 billion in 2026 and is forecast to reach USD 46.93 billion by 2031 at 10.12% CAGR over 2026-2031. The expansion reflects the shift from video as a meeting tool to a mission-critical infrastructure that supports workflow automation, data-driven decision making, and global collaboration. Cloud-native platforms, AI-powered analytics, and private 5G networks are improving scalability, caption accuracy, and sub-25 millisecond end-to-end latency, which together elevate user expectations for always-on, ultra-responsive experiences[1]Ericsson AB, “Private 5G Networks Enable Sub-25 ms Latency,” ericsson.com. Rising hybrid-work norms continue to anchor budget allocations for video, while vendor consolidation—illustrated by the Brightcove acquisition—signals a platform race toward full-stack offerings. Concurrently, mounting cybersecurity insurance premiums and skills shortages in video-workflow orchestration temper adoption curves for some late-moving enterprises.

Key Report Takeaways

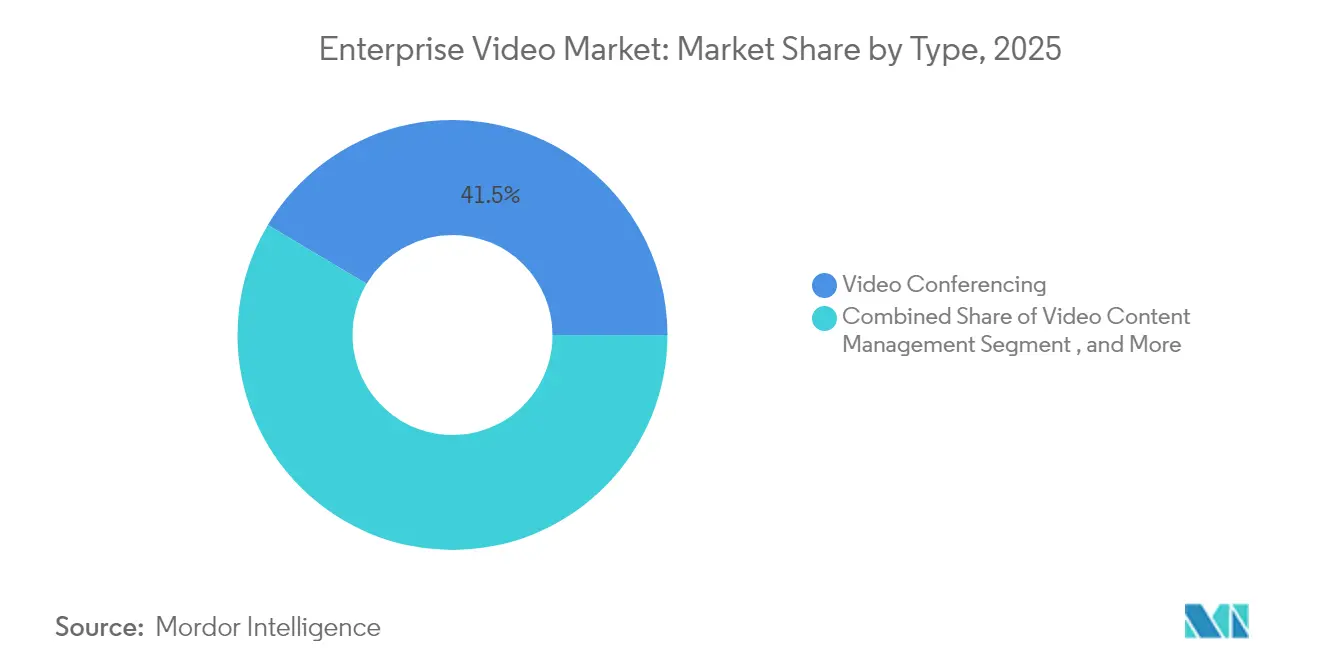

- By type, Video Conferencing led with 41.45% of enterprise video market share in 2025; Video Analytics is projected to register an 18.2% CAGR through 2031.

- By component, Software accounted for 50.92% of enterprise video market size in 2025; Services is set to advance at a 14.05% CAGR to 2031.

- By deployment mode, On-Premises held 56.35% share of the enterprise video market in 2025; Cloud deployment is predicted to expand at a 12.9% CAGR.

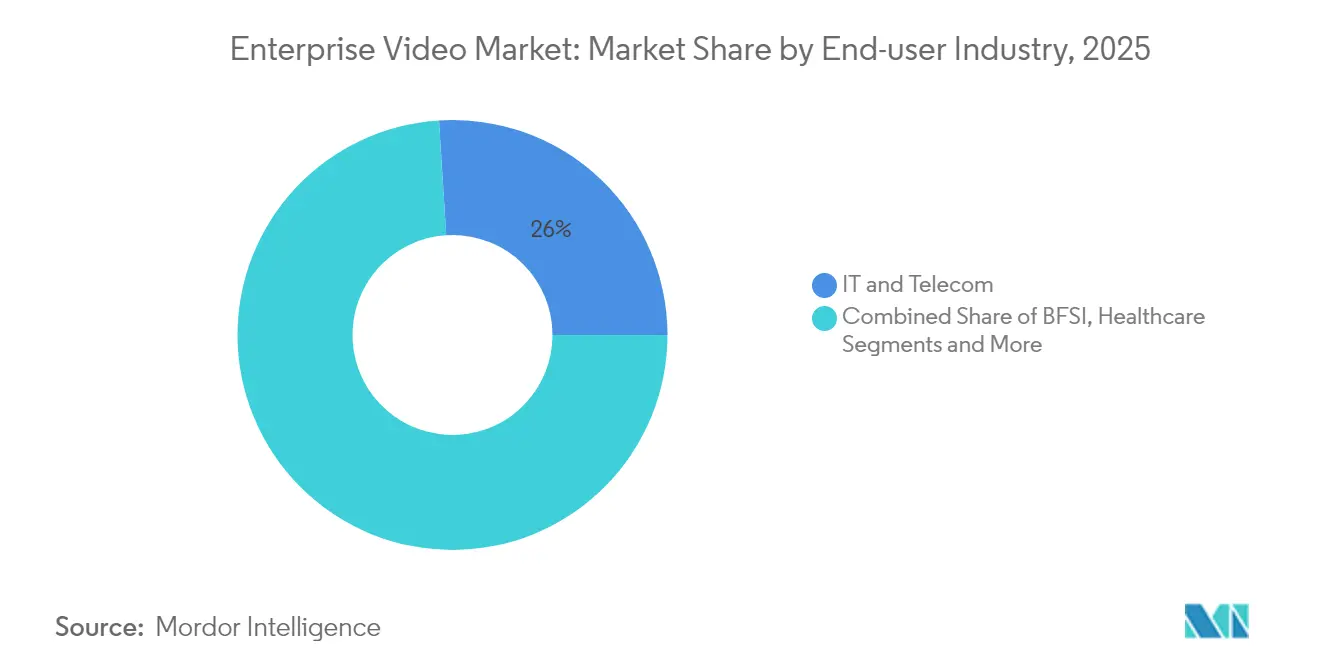

- By end-user industry, IT and Telecommunications captured 26.00% revenue share in 2025, while Healthcare is forecast to grow at a 15.9% CAGR.

- By organization size, Large Enterprises commanded 63.60% share of the enterprise video market size in 2025; Small and Medium Enterprises are growing fastest at a 13.7% CAGR.

- By geography, North America held 34.05% share in 2025; Asia-Pacific is the fastest-growing region with a 12.6% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Enterprise Video Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-first video architecture adoption | +2.1% | Global, with North America and EU leading | Medium term (2-4 years) |

| AI-powered live-caption accuracy breakthroughs | +1.8% | Global, with Asia-Pacific showing rapid adoption | Short term (≤ 2 years) |

| Growth of hybrid and remote workforces | +2.4% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| BYOD proliferation across enterprises | +1.3% | North America and EU primarily | Medium term (2-4 years) |

| Low-latency 5G private networks in campuses | +1.6% | Asia-Pacific core, spill-over to North America | Long term (≥ 4 years) |

| Compliance-driven demand for secure archival | +1.1% | Global, with a regulatory focus in EU and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cloud-first video architecture adoption

The migration to cloud-native stacks enables elastic scaling, API-driven integrations, and global content distribution at lower upfront cost. Enterprises retain sensitive archives on-premises yet push compute-heavy analytics to public clouds, reducing local hardware refresh cycles. Multi-cloud routing safeguards against vendor lock-in and latency variation, and it lets IT teams match diverse workloads with the optimal cost-performance region. Even so, “cloud-exit” strategies are surfacing as some firms rebalance spend toward private infrastructure when monthly egress fees outweigh elasticity benefits.

AI-powered live-caption accuracy breakthroughs

Automatic speech recognition models now deliver up to 98% precision under favorable acoustics, lifting video accessibility beyond regulatory compliance into a productivity advantage. Rich language support—spanning 140 tongues—facilitates cross-border collaboration while searchable transcripts unlock evergreen knowledge repositories. Enterprises embed these AI captions directly in content management systems to raise engagement metrics and speed content localization. The advance also fuels inclusive hiring practices because Deaf and hard-of-hearing employees access meetings in real time without third-party captioners.

Growth of hybrid and remote workforces

Office-attendance expectations have stabilized at two to three days per week in many developed economies, cementing video as the connective tissue across distributed teams. Companywide town halls, onboarding modules, and customer demos increasingly stream through centralized video portals rather than siloed conferencing links. Performance dashboards track view-through rates, speaker effectiveness, and knowledge-retention scores, making video a measurable productivity input instead of a sunk cost.

BYOD proliferation across enterprises

Two-thirds of enterprises plan to implement Bring Your Own Meeting workflows by 2025, empowering employees to host sessions from any preferred application while using installed conference-room fixtures. This trend pushes vendors to ship hardware-agnostic SDKs and to harden device-certificate management layers that secure personal laptops and smartphones. Network administrators, in turn, lean on role-based access controls and zero-trust verification to prevent rogue devices from exposing corporate video archives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High total cost of ultra-low-latency infrastructure | -1.4% | Global, with higher impact in emerging markets | Short term (≤ 2 years) |

| Inter-country data-sovereignty barriers | -0.9% | Global, with EU and Asia-Pacific regulatory focus | Long term (≥ 4 years) |

| IT staff skill shortages in video-workflow orchestration | -1.2% | Global, acute in North America and EU | Medium term (2-4 years) |

| Rising cyber-insurance premiums on video breaches | -0.8% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High total cost of ultra-low-latency infrastructure

Enterprises seeking sub-25 millisecond round-trip performance must invest in private 5G, edge CDN nodes, and GPU-accelerated encoders. Capital plans frequently exceed budget allocations, as hyperscalers earmark USD 75 billion in 2025 capex for AI and networking backbones that downstream customers must partially absorb. LED video walls alone range between USD 380 and USD 1,200 per ft², making large-format displays viable only for cash-rich organizations. Ongoing operational costs—from on-call engineers to redundancy circuits—further widen total cost of ownership.

IT staff skill shortages in video-workflow orchestration

Modern ecosystems demand professionals proficient in container orchestration, AI inference tuning, and compliance auditing. The labor pool remains thin, forcing CIOs to outsource management to specialist providers, which in turn propels the 14.2% CAGR in the Services segment. Talent gaps slow deployment timelines and elevate configuration errors that can trigger privacy breaches or performance bottlenecks. Upskilling initiatives have begun; however, certification programs lag behind the pace of toolchain updates, so skill availability will remain a mid-term constraint.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Analytics-led Innovation Shapes Growth

The Video Conferencing segment delivered USD 10.91 billion and held 41.45% of enterprise video market share in 2025, reflecting its entrenchment as the default collaboration medium. Video Analytics, though smaller in absolute value, is projected to outpace all other categories at an 18.2% CAGR, adding more than USD 4 billion to enterprise video market size by 2031. This momentum stems from AI engines that detect anomalies, extract metadata, and trigger workflow automations across security, manufacturing, and retail settings.

Adoption patterns reveal convergence between once-distinct categories. Conferencing vendors bundle analytics for speaker sentiment, while content-management platforms embed live-stream modules to support hybrid events. AI video generators, such as Google’s Veo 3, blur production and distribution boundaries by enabling non-specialists to create branded assets in seconds. The result is a mosaic ecosystem where enterprises choose flexible modules that integrate through open APIs rather than monolithic suites, a dynamic that further accelerates innovation cycles within the enterprise video market.

By Component: Services Outpace Software

Software products retained 50.92% share of enterprise video market size in 2025, underpinning meeting, streaming, and archival functions. Yet the Services category will rise fastest at a 14.05% CAGR. Outsourced orchestration, 24/7 monitoring SLAs, and AI tuning services appeal to organizations lacking in-house expertise. Hardware remains essential for encoding, room endpoints, and edge caching, but value is migrating to software-defined components pre-installed on commodity devices.

Bundled “video-as-a-service” offerings illustrate the shift. Providers supply managed encoder racks, transcoding software, and analytics dashboards under a predictable monthly fee, bundling proactive maintenance and feature updates. This model lowers total cost of ownership and supports SMEs that previously could not justify dedicated video teams. As a result, service providers are rapidly expanding consulting arms, certification programs, and managed eCDN portfolios, defending margins as pure software licensing becomes price-competitive.

By Deployment Mode: Cloud Adoption Accelerates but Hybrid Persists

Cloud deployments are forecast to climb at a 12.9% CAGR, narrowing the gap with on-premises setups that still accounted for 56.35% of enterprise video market share in 2025. Drivers include rapid provisioning, elastic transcode, and simplified global access control. Industry-specific compliance prompts hybrid topologies, where sensitive footage remains in sovereign data centers while less critical workloads execute in multi-cloud clusters.

Enterprises increasingly route traffic among multiple hyperscalers to minimize egress fees and to position content closer to local audiences. However, cost spikes and data-gravity challenges have spurred selective “cloud repatriation,” leading to edge-heavy private clouds optimized for latency-sensitive applications. Decision frameworks now weigh workload type, audience geography, and regulatory posture, producing a spectrum of deployment mixes rather than a binary cloud/on-premises dichotomy inside the enterprise video market.

By End-User Industry: Healthcare Leads the Upswing

IT and Telecommunications remained the largest contributor with 26.00% revenue share in 2025, but Healthcare is set to log a 15.9% CAGR, the steepest across all verticals. Telehealth consults, surgical training simulations, and remote patient monitoring drive continuous streaming demand, while privacy laws accelerate investment in encrypted archival and audit-trail capabilities. Banks follow closely, harnessing secure video rooms for wealth-management advisory and post-trade compliance evidence.

Manufacturers deploy machine-vision analytics to reduce defect rates and machine downtime, integrating video alerts into MES dashboards. Retailers stream personalized shopping assistance from live agents, turning browsing sessions into high-conversion sales funnels. Education continues migrating to asynchronous video libraries that boost knowledge retention and cater to flexible study schedules. Each vertical imposes unique compliance, latency, and integration constraints that spur niche solution development within the enterprise video market.

By Organization Size: Democratization Spurs SME Uptake

Large Enterprises generated nearly two-thirds of 2025 revenue, leveraging expansive budgets for multi-tenant eCDN deployments and global content redundancies. Small and Medium Enterprises, however, exhibit a 13.7% CAGR as barrier-lowering SaaS license tiers and freemium models unlock entry. The pay-as-you-grow pricing model lets SMEs add features—AI captions, live translation, NDI routing—only when ROI becomes apparent.

Bundled support packages replace fractional IT hires, while drag-and-drop studio interfaces eliminate video-editing complexity. SMEs also exploit public marketplaces that integrate video APIs into CRM and ERP workflows with minimal code. Consequently, feature parity between tiers is compressing, nudging vendors to differentiate via industry templates, advanced compliance collections, and regional data-sovereignty assurances rather than raw functionality counts.

Geography Analysis

North America secured 34.05% of enterprise video market share in 2025 on the back of expansive broadband penetration, early SaaS adoption, and robust federal investment in telework infrastructure. Growth is moderating as large enterprises optimize existing deployments, prioritizing AI add-ons and advanced analytics rather than net-new seat licenses. Even so, edge acceleration nodes around tier-2 cities extend low-latency streaming into under-served areas, preserving incremental revenue.

Asia-Pacific is the fastest-growing territory, registering a 12.6% CAGR as mobile broadband upgrades and 5G private-network pilots proliferate. Indigenous champions—Tencent Meeting in China and Itochu-backed EasyRooms in Japan—tailor interfaces, compliance modules, and language packs to local norms. Government digitalization programs and manufacturing modernization efforts underpin demand for inspection-grade video analytics, further bolstering regional uptake within the enterprise video market.

Europe follows a steady trajectory shaped by GDPR compliance mandates. Enterprises gravitate toward vendors offering in-region data centers and stringent privacy certifications, driving cooperation between U.S. platforms and EU-based cloud hosts. South America plus the Middle East and Africa represent emerging footholds where cloud-first strategies leapfrog legacy on-premises rollouts. Telco partnerships that bundle video suites with high-speed connectivity lower adoption hurdles for mid-market firms across these regions.

Competitive Landscape

The enterprise video market features moderate concentration and is tilting toward consolidation. Bending Spoons’ USD 233 million bid for Brightcove underscores a strategic pivot by mobile-first developers seeking end-to-end video distribution playbooks. Simultaneously, longstanding vendors like Cisco and Microsoft double down on AI copilots, marrying communication, workflow automation, and analytics under unified interfaces.

Differentiation pivots on AI breadth. Kaltura’s Work Genie layers generative content snippets atop traditional portals, while Vbrick’s Universal eCDN melds bandwidth conservation with zero-touch edge deployment. Start-ups focus on specialty segments: device-embedded video analytics for manufacturing, covert watermarking for media rights, or ultra-low-bitrate codecs for bandwidth-constrained geographies.

Strategic partnerships are paramount. Hardware firms partner with caption API start-ups, and cloud providers court system integrators that embed video into line-of-business suites. No single player can execute across codecs, compliance frameworks, and edge architectures, driving multi-layer alliances that knit together a holistic value proposition for customers of the enterprise video market.

Enterprise Video Industry Leaders

Microsoft Corporation

Cisco Systems, Inc.

Zoom Video Communications, Inc.

Adobe Inc.

Google LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Google launched Veo 3, enabling Gemini users in 159 countries to generate photorealistic videos from text or images.

- May 2025: XTM International acquired TXTOmedia to bolster multilingual video automation.

- April 2025: Cvent bought Prismm to enhance spatial design for hybrid events.

- April 2025: Adobe introduced Clip Maker, Generate Video, and Dynamic Animation in Adobe Express.

Global Enterprise Video Market Report Scope

The enterprise video market issegmented by type, components, end-user industry, and geography.By type, the market studied is segmented into video conferencing, video content management, webcasting, and others. By components, the market studied is segmented into hardware and software. Integrated solutions offered by vendors are also considered in the scope of the study. By end-user industry, the market studied is segmented into BFSI, IT & telecommunications, retail, healthcare, public sector & education, and media & entertainment, and others.

| Video Conferencing |

| Video Content Management |

| Webcasting and Live Streaming |

| Video Analytics |

| Other Types |

| Hardware |

| Software |

| Services |

| On-Premises |

| Cloud |

| BFSI |

| Healthcare |

| IT and Telecommunications |

| Retail and E-commerce |

| Education |

| Government and Public Sector |

| Manufacturing |

| Media and Entertainment |

| Others |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordics | ||

| Rest of Europe | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| By Type | Video Conferencing | ||

| Video Content Management | |||

| Webcasting and Live Streaming | |||

| Video Analytics | |||

| Other Types | |||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Deployment Mode | On-Premises | ||

| Cloud | |||

| By End-user Industry | BFSI | ||

| Healthcare | |||

| IT and Telecommunications | |||

| Retail and E-commerce | |||

| Education | |||

| Government and Public Sector | |||

| Manufacturing | |||

| Media and Entertainment | |||

| Others | |||

| By Organization Size | Small and Medium Enterprises (SMEs) | ||

| Large Enterprises | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Nordics | |||

| Rest of Europe | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| ASEAN | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia-Pacific | |||

Key Questions Answered in the Report

What is the current size of the enterprise video market?

The enterprise video market stands at USD 28.98 billion in 2026.

How fast is the enterprise video market expected to grow?

It is forecast to expand at a 10.12% CAGR, reaching USD 46.93 billion by 2031 over 2026-2031.

Which enterprise video segment is growing the fastest?

Video Analytics leads with an anticipated 18.2% CAGR through 2031, reflecting demand for AI-driven insights.

Why is Healthcare the fastest-growing user industry?

Telemedicine, strict patient-data regulations, and rising remote-care adoption give Healthcare a projected 15.9% CAGR.

Page last updated on: