Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 88.25 Billion |

| Market Size (2031) | USD 162.16 Billion |

| Growth Rate (2026 - 2031) | 12.94% CAGR |

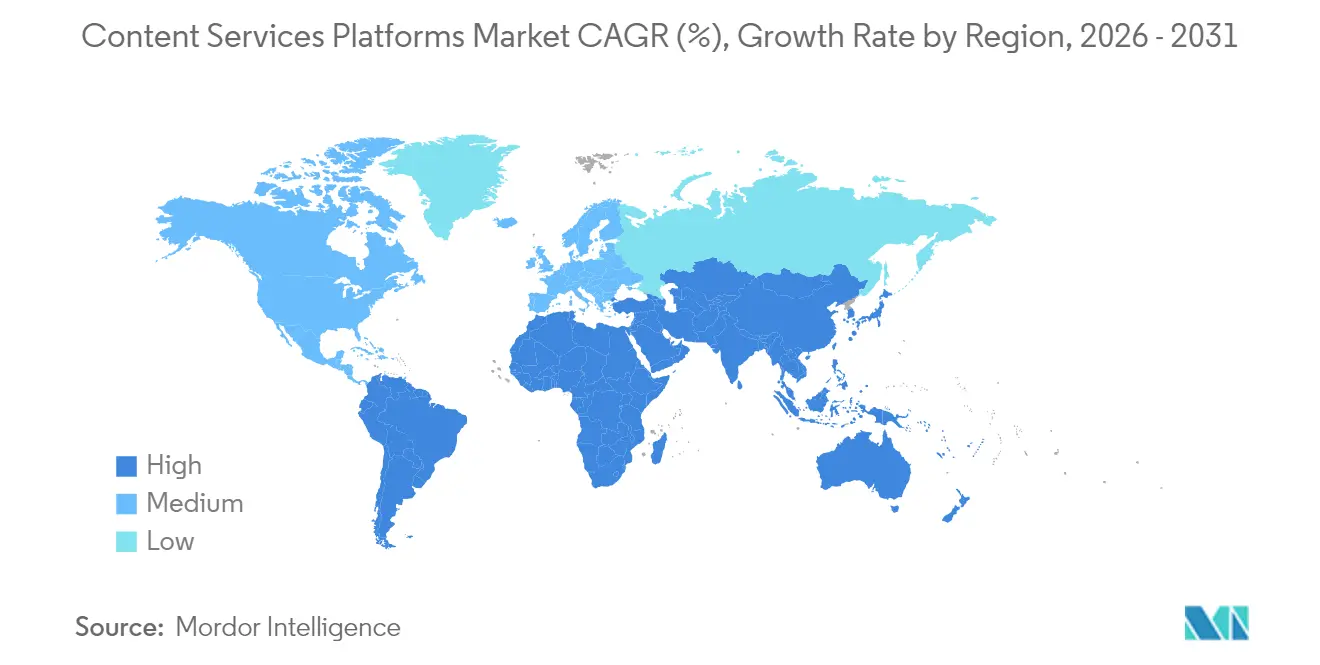

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

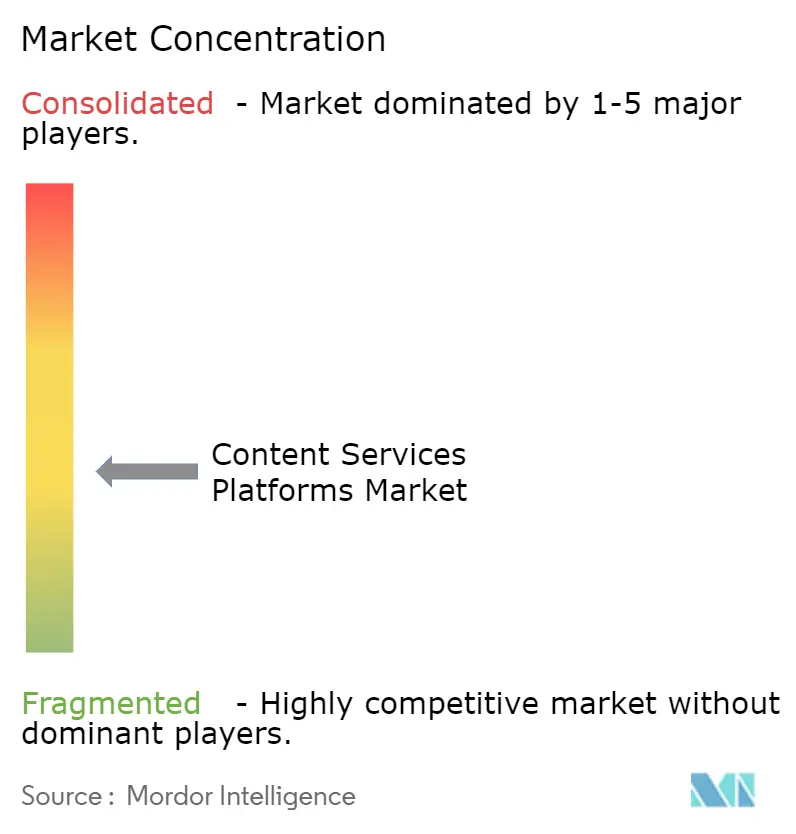

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Content Services Platforms Market Analysis by Mordor Intelligence

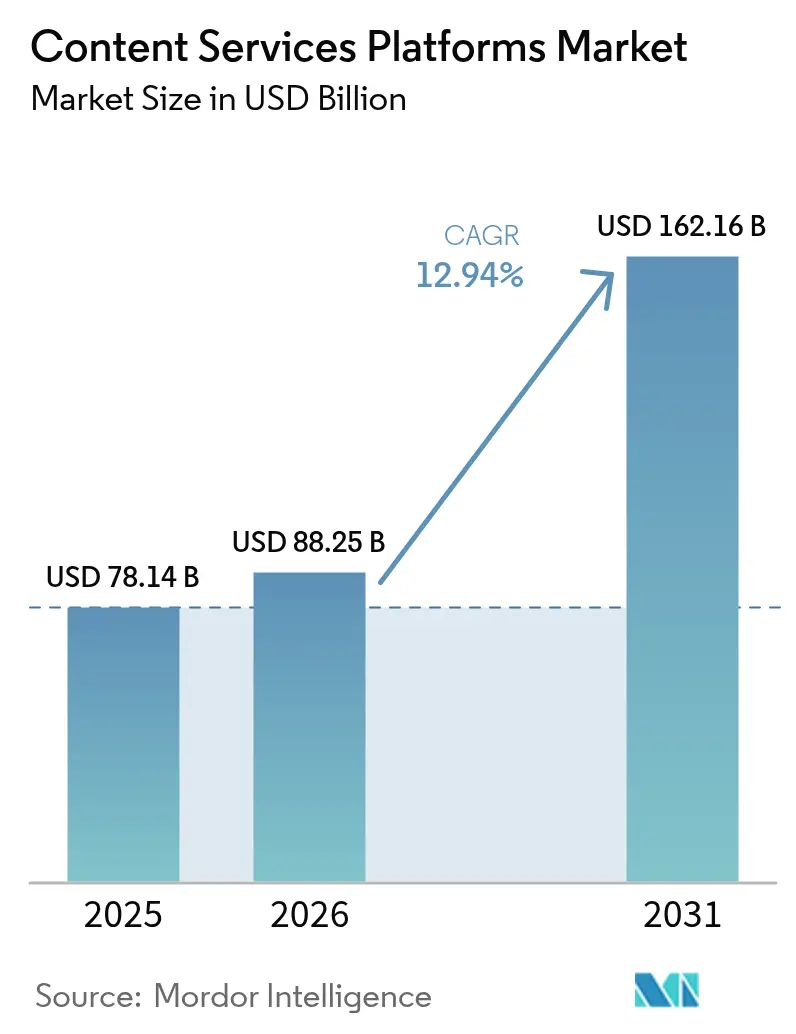

Content Services Platforms market size in 2026 is estimated at USD 88.25 billion, growing from 2025 value of USD 78.14 billion with 2031 projections showing USD 162.16 billion, growing at 12.94% CAGR over 2026-2031. The proliferation of cloud-native architectures, the expansion of AI capabilities, and stringent regulatory frameworks are driving enterprises to modernize their document ecosystems. Rapid cloud adoption shortens implementation cycles, while generative AI automates tasks ranging from classification to contract drafting, thereby lowering operating costs for both large enterprises and fast-growing SMEs. Competitive dynamics are constantly shifting as leading vendors bundle AI with existing productivity suites and independent specialists differentiate themselves through verticalized offerings and low-code accelerators. Finally, persistent cybersecurity threats and legacy integration hurdles temper near-term adoption yet spur demand for secure, API-first platforms.

Key Report Takeaways

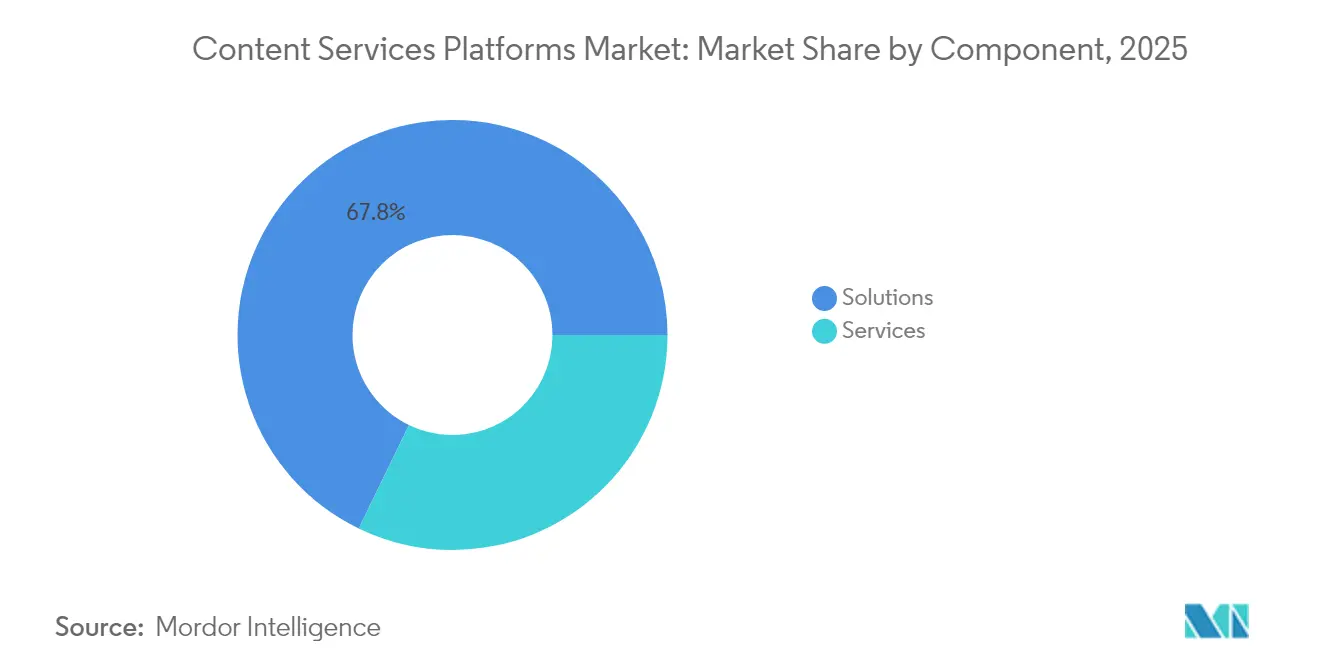

- By component, solutions led with 67.82% revenue share in 2025; services are projected to expand at a 17.12% CAGR through 2031.

- By deployment model, the cloud segment captured 78.05% of the content services platforms market share in 2025, and register a CAGR of 19.21% CAGR through 2031.

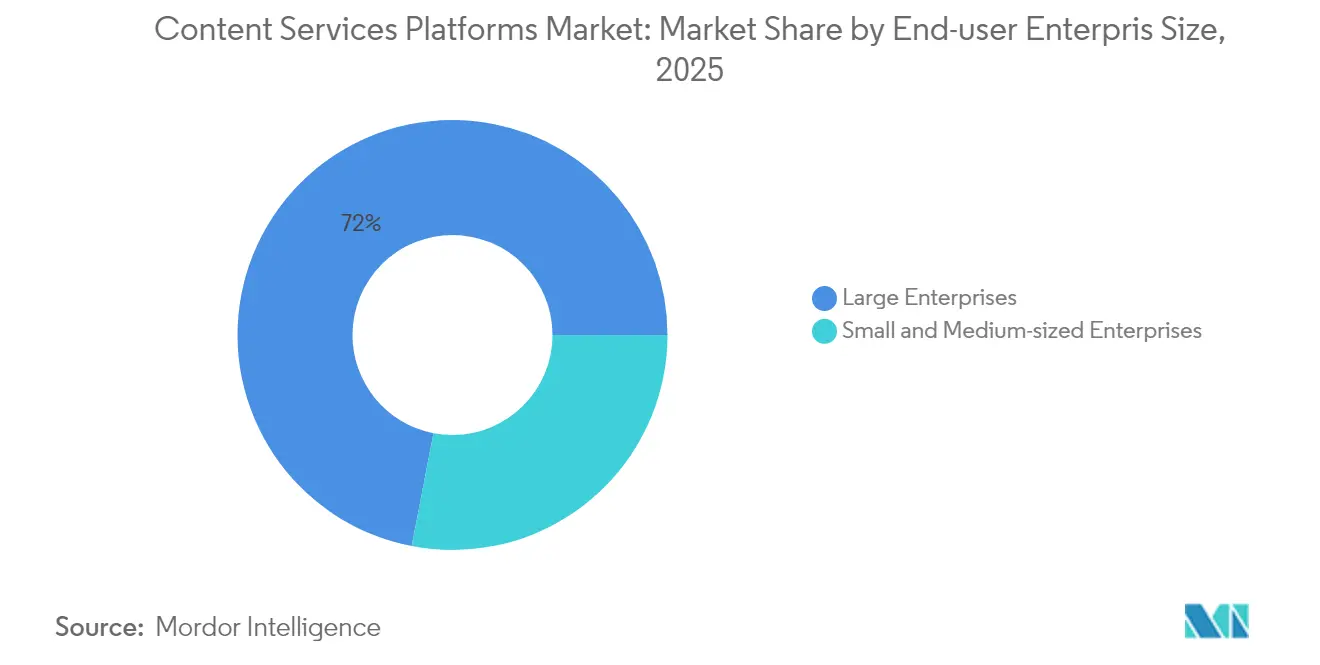

- By enterprise size, large organizations held 71.96% of the content services platforms market share in 2025; SMEs are set to grow fastest at a 14.49% CAGR.

- By end-user vertical, BFSI commanded 25.62% share of the content services platforms market size in 2025, whereas healthcare and life sciences are primed for a 15.08% CAGR over the period.

- By geography, North America contributed 38.05% share of the content services platforms market size in 2025; Asia-Pacific is anticipated to record the highest regional CAGR of 13.88% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Content Services Platforms Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-native adoption momentum | +3.2% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Surging unstructured data volumes | +2.8% | Global, with Asia-Pacific growth edge | Long term (≥ 4 years) |

| Heightened regulatory-compliance pressure | +2.1% | North America and EU now, widening to Asia-Pacific | Short term (≤ 2 years) |

| Generative-AI powered autonomous workflows | +1.9% | Global, early movers in developed markets | Medium term (2-4 years) |

| Low-code accelerators for CSP rollout | +1.4% | Global, highly attractive to SMEs | Short term (≤ 2 years) |

| M&A-driven platform consolidation | +1.1% | Global, centered on North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cloud-Native Adoption Momentum

Enterprises migrating to cloud-native platforms gain scalability and unified access while reducing infrastructure costs by up to 40% through exemplars such as Microsoft SharePoint Online and OneDrive[1]Microsoft Corporation, “Microsoft 365 SharePoint Collaboration Solutions,” Microsoft.com. Remote work trends amplify demand because API-first architectures handle distributed collaboration with minimal latency. Mid-market firms, once priced out of robust document management solutions, now deploy feature-rich SaaS offerings without the need for capital-intensive servers. Cloud providers’ continuous delivery enables quarterly AI feature refreshes, ensuring compliance with frameworks such as SOC 2 and ISO 27001, which increasingly prioritize full-stack cloud solutions. Disaster recovery built into hyperscale data centers further encourages wholesale retirement of aging on-premises repositories.

Surging Unstructured Data Volumes

Video meetings, IoT sensors, and omnichannel customer touchpoints are expected to inflate unstructured data to an estimated 80% of enterprise totals by 2025, overwhelming traditional file shares. Modern platforms integrate NLP and computer vision, transforming contracts, emails, and images into searchable intelligence, enabling healthcare providers to maintain HIPAA compliance while surfacing valuable clinical insights[2]Adobe Inc., “Document Cloud for Business Enterprise Solutions,” Adobe.com. Automated tagging, versioning, and retention schedules help satisfy audit demands in litigation-heavy sectors. As data footprints swell, algorithmic classification limits storage spend by moving obsolete records to cold tiers and preventing the proliferation of duplicative content.

Heightened Regulatory-Compliance Pressure

GDPR, CCPA, and the European Union’s DORA mandate real-time evidence of operational resilience, compelling financial institutions to document every process in machine-readable form[3]European Banking Authority, “Digital Operational Resilience Act Implementation,” Eba.europa.eu . Fines reaching 4% of global revenue have recast compliance from a cost center to a boardroom priority. Leading platforms now embed policy engines that classify sensitive material on ingestion, mask personal identifiers, and log immutable audit trails. Multi-jurisdictional rule libraries reduce manual review workloads for global enterprises navigating overlapping privacy statutes, accelerating ROI, and justifying premium subscription tiers.

Generative-AI Powered Autonomous Content Workflows

Integrations, such as Adobe Document Cloud with generative AIs, reduce legal review cycles by 60% through automatic clause extraction, risk flagging, and suggested redlines. Beyond contracts, LLM-based copilots draft marketing collateral, translate technical manuals, and recommend next-best actions, fostering continuous knowledge reuse. Workflow bots escalate exceptions, while adaptive prompts fine-tune responses to corporate tone, reducing desk-to-decision lag times for professional services, banking, and government agencies

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy and cyber-security concerns | -1.8% | Global, acute in regulated verticals | Short term (≤ 2 years) |

| Legacy-system integration complexity | -1.5% | North America and Europe, mature IT estates | Medium term (2-4 years) |

| Hyperscaler bundling squeezing independents | -1.2% | Global, mid-market focus | Medium term (2-4 years) |

| Scarcity of AI-taxonomy skillsets | -0.9% | Global, sharper in emerging regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy and Cyber-Security Concerns

The 2024 Change Healthcare breach, exposing records of over 100 million patients, heightened scrutiny of cloud repositories[4]U.S. Department of Health and Human Services, “HHS Releases Comprehensive Cybersecurity Strategy,” Hhs.gov. Regulated sectors now demand zero-trust postures, field-level encryption, and regional data residency, which elongate vendor evaluations and raise deployment costs. “Right to be forgotten” clauses force platforms to automate granular deletion across distributed caches, adding architectural complexity. Boards allocate larger cyber budgets, yet the specter of reputational damage continues to sustain cautious rollouts, especially in defense and public safety domains.

Legacy-System Integration Complexity

Fortune 1000 firms often run decades-old workflow engines with undocumented business rules, creating brittle dependencies when modern APIs interface with COBOL and mainframe data stores. Projects routinely overrun schedules as teams uncover incompatible metadata schemas or hidden VBA scripts. Regulated industries keep hybrid stacks alive to preserve validated records, elevating support overhead. Consequently, some enterprises postpone migrations until end-of-life deadlines loom or budget cycles can absorb extensive refactoring.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Accelerate Despite Solutions Dominance

Solutions maintain a commanding market leadership position with a 67.82% share in 2025, encompassing document management, workflow automation, data capture, and security governance modules that form the core functionality of content services platforms. However, services represent the fastest-growing component, with a 17.12% CAGR through 2031, driven by increasing demand for specialized integration, consulting, and support capabilities as organizations deploy AI-powered content workflows. Integration and deployment services, particularly those involved in connecting modern content platforms with legacy enterprise systems, benefit from the complexity of this task. Meanwhile, consulting services expand as organizations require expertise in AI taxonomy development and regulatory compliance frameworks.

Document and records management solutions dominate the software segment, providing foundational capabilities for content storage, version control, and lifecycle management that remain essential across all industry verticals. Workflow management and case management solutions show strong growth as organizations automate manual processes and implement intelligent routing based on content analysis and business rules. Information security and governance solutions gain prominence as data protection regulations intensify and organizations require sophisticated policy enforcement capabilities that can adapt to evolving compliance requirements across global markets.

By Deployment Model: Cloud Supremacy Accelerates

Cloud deployment models are expected to command a 78.05% market share in 2025 and maintain the strongest growth trajectory at a 19.21% CAGR through 2031, reflecting an enterprise preference for scalable, cost-effective solutions that eliminate infrastructure management overhead. The cloud advantage intensifies as vendors integrate advanced AI capabilities that require significant computational resources and frequent model updates that are impractical for on-premises deployments. Box Inc.'s Multi-tenant SaaS architectures enable rapid feature rollouts and automatic security updates, reducing the IT burden while providing access to cutting-edge functionality, including generative AI, advanced analytics, and intelligent automation.

On-premises deployments persist in highly regulated industries and government agencies where data sovereignty requirements mandate local control over sensitive content repositories. However, even traditional on-premises customers are increasingly adopting hybrid architectures that leverage cloud services for non-sensitive content while maintaining critical data within their private infrastructure. The deployment model choice often correlates with organizational size, as large enterprises with dedicated IT resources maintain on-premises capabilities while small and medium enterprises overwhelmingly prefer cloud solutions that provide enterprise-grade functionality without requiring specialized technical expertise.

By End-user Enterprise Size: SME Growth Outpaces Large Enterprise Stability

Large enterprises account for a 71.96% market share in 2025, leveraging content services platforms to manage complex, multi-departmental workflows that span global operations and require sophisticated integration with enterprise resource planning, customer relationship management, and business intelligence systems. These organizations typically deploy comprehensive solutions that include advanced security features, custom workflow engines, and extensive API integrations, supporting thousands of concurrent users across diverse geographic locations. Large enterprise adoption focuses on replacing legacy systems with modern platforms that can scale to support digital transformation initiatives while maintaining regulatory compliance across multiple jurisdictions.

Small and medium-sized enterprises represent the fastest-growing segment, with a 14.49% CAGR through 2031, benefiting from cloud-based deployment models that provide enterprise-grade functionality at accessible price points, without requiring significant upfront investment or specialized IT resources. SME adoption accelerates as vendors introduce simplified onboarding processes, pre-configured industry templates, and low-code customization tools that enable rapid deployment and user adoption. This segment particularly values integrated solutions that combine content management with collaboration, communication, and basic workflow automation capabilities within unified platforms that reduce complexity and total cost of ownership.

By End-user Industry Vertical: Healthcare Disrupts BFSI Leadership

The Banking, Financial Services, and Insurance sector maintains the largest industry share at 25.62% in 2025, driven by stringent regulatory requirements, including Basel III, Dodd-Frank, and MiFID II, which mandate comprehensive documentation, audit trails, and risk management processes. Financial institutions leverage content services platforms for loan processing, compliance reporting, customer onboarding, and regulatory filing automation that reduces operational risk while improving processing efficiency. The sector's mature adoption reflects an early recognition that content management has a direct impact on regulatory compliance costs and operational efficiency in highly regulated environments.

Healthcare and Life Sciences emerge as the fastest-growing vertical, with a 15.08% CAGR through 2031, driven by digital health initiatives, patient data management requirements, and clinical research automation that necessitate sophisticated content governance and interoperability capabilities. The sector benefits from AI-powered capabilities that can analyze medical imaging, extract insights from clinical notes, and automate regulatory submissions while maintaining HIPAA compliance and patient privacy protections. Government and public sector adoption accelerates as digital transformation initiatives modernize citizen services and internal operations, while transportation and logistics organizations implement content platforms to manage supply chain documentation, regulatory compliance, and operational efficiency requirements across global networks.

Geography Analysis

North America generated 38.05% of global revenue in 2025, primarily driven by the United States, where cloud-first mandates and aggressive AI adoption are fueling high-value projects. Deep partner ecosystems enable Fortune 500 firms to integrate content intelligence into their ERP, CRM, and analytics stacks, while federal data-governance directives expand public-sector adoption. Canadian financial institutions are embracing platforms for anti-money laundering documentation, and Mexico’s export manufacturers are digitizing quality records to meet U.S. import audits.

Europe sustains solid momentum as GDPR fines motivate enterprises to automate data-subject-access workflows and deletion procedures. Germany leads industrial deployments aligned with Industry 4.0, whereas the United Kingdom’s City institutions prioritize real-time regulatory filings. France’s digital-services agenda injects demand for sovereign-cloud options, and the Nordics favor carbon-neutral data centers, influencing vendor hosting roadmaps. The region’s multilingual landscape further boosts AI-driven translation and summarization modules.

Asia-Pacific, projected to grow at 13.88% CAGR, benefits from ambitious national digitization programs, expanding broadband and mobile penetration. China’s “Made in China 2025” policy accelerates smart-factory rollouts that embed quality-control documentation in unified repositories. India’s public-sector initiatives, under the Digital India umbrella, foster e-governance platforms built on localized content taxonomies. Japan’s aging workforce spurs automation of knowledge capture, while Australia and Singapore serve as regional hubs for multinational compliance operations. This momentum is expected to narrow the gap with North America by 2030, further elevating the content services platforms market profile in emerging economies.

Regulatory Landscape

Content services platforms operate under converging privacy, resilience, and AI transparency rules that influence how enterprise content is captured, stored, processed, and audited across jurisdictions. In the European Union, obligations linked to the Digital Services Act (DSA, Regulation (EU) 2022/2065) raise transparency expectations for content governance, while the EU AI Act (Regulation (EU) 2024/1689) introduces specific transparency requirements for certain AI systems, including disclosures and machine-readable labeling for AI-generated or manipulated content. Those obligations, referenced as starting from 2 August 2026, create design and governance requirements for platforms embedding generative AI in content workflows.

Sector and process requirements also reinforce auditability and retention controls. Under the Digital Operational Resilience Act framework (including Regulation (EU) 2024/1773), financial entities must manage ICT third-party risk for critical functions with contractual and monitoring requirements that increase demand for immutable logs, evidence collection, and vendor oversight within CSP deployments. In the United States, the Department of Justice ADA Title II web accessibility rule anchors WCAG 2.1 Level AA as the standard for state and local government digital services, with extended compliance timelines (April 26, 2027 for larger entities and April 26, 2028 for smaller ones). This pushes CSP user experiences, portals, and document delivery journeys toward accessibility-by-design, especially in public sector and citizen-service use cases.

Value Chain Analysis

The value chain starts with core platform vendors delivering content repositories, workflow/case management, capture, and governance layers, and then extends into hyperscaler infrastructure, AI services, and enterprise application ecosystems. Cloud infrastructure providers supply compute, storage, security tooling, and regional hosting options that underpin SaaS and private cloud deployments, while AI model and orchestration components increasingly sit alongside the CSP to enable classification, summarization, and agent-driven task execution. Partnerships illustrate this coupling, such as Hyland collaborating with Microsoft Azure (June 2026) to run the Hyland Content Innovation Cloud with joint go-to-market motions, reinforcing the role of hyperscaler marketplaces, co-sell programs, and cloud architectures in how CSP capabilities are packaged and procured.

Downstream, systems integrators, consultants, and managed service providers handle migrations, taxonomy development, ERP/CRM/HCM connectivity, and the operationalization of governance and security controls, aligning with the market's faster services growth. Interoperability and federation services have become a delivery layer as enterprises keep multiple repositories and hybrid stacks, limiting the need for full migrations while improving access for AI and search across silos. Tooling and standards for connecting AI agents to enterprise systems are also emerging as connective tissue in the ecosystem, supported by industry emphasis on open interfaces such as the Model Context Protocol discussed in enterprise forums (for example, Doxis Summit 2026 in Munich), which supports safer retrieval and action on governed enterprise content.

Competitive Landscape

The content services platforms market remains moderately concentrated, with OpenText, Microsoft, IBM, and Adobe leading, yet none exceeding a 15% share. These incumbents differentiate through end-to-end suites that bundle AI search, records management, and low-code workflow builders. Box, Hyland, and M-Files defend share by targeting line-of-business buyers, offering rapid configuration and transparent pricing.

Hyperscalers such as Microsoft, Amazon, and Google are increasingly influential: their ability to embed content services into cloud infrastructure credits lowers effective ownership costs and tilts RFPs toward bundled solutions. Independent vendors respond by deepening vertical IP-for example, Hyland’s healthcare imaging connectors-and forging strategic alliances that certify interoperability in multicloud estates.

M&A activity is brisk: OpenText’s absorption of Micro Focus assets consolidates aging Documentum customers under one roof, while Box acquires niche AI players to fortify summarization and translation pipelines. Patent races in large-language-model tuning highlight the strategic importance of proprietary data, as vendors pool anonymized customer content to train domain-specific models. Continuous R&D investments, measured at 12-17% of revenue among top players, signal a long-term technology arms race destined to reshape provider hierarchies within the content services platforms market.

Content Services Platforms Industry Leaders

IBM Corporation

Microsoft Corporation

Box Inc.

Oracle Corporation

OpenText Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

AI transparency and auditability requirements create a product whitespace around enterprise-grade provenance, labeling, and governance for generated content. The EU AI Act transparency obligations referenced to start from 2 August 2026 raise the need for machine-readable marking, disclosure workflows, and policy enforcement that can be applied across documents, knowledge bases, and collaboration content. Vendors that embed labeling, retention, and immutable audit trails directly into authoring, review, and publishing pipelines can position CSP deployments as compliance-enabling infrastructure rather than add-on repositories.

Public sector and regulated-industry procurement is also tightening around data safeguarding for LLM-enabled workflows, favoring CSP architectures that support data residency, encryption, and controlled agent access. A visible 2026 signal is the US General Services Administration proposing a GSAR clause (June 2026) to safeguard government data processed in large language model AI systems, reinforcing demand for controllable connectors, governed retrieval, and policy-based restrictions on what agents can access and output. At the same time, the market is shifting from isolated AI pilots toward agentic workflows that plan and act on content-centric tasks, supported by vendor moves such as Box Automate and the Box Agent (April 2026) and integrations that standardize agent-to-content connectivity (for example, the Box MCP server becoming available in the IBM watsonx Orchestrate agent catalog in May 2026). This supports opportunities for CSPs that can federate content across multiple repositories without forcing immediate full migrations.

Recent Industry Developments

- June 2026: IBM released IBM Content Cortex Essentials Edition as an AI-native content services platform positioned for agentic content automation and as an evolution path for FileNet Content Manager and Content Manager Enterprise Edition. The release reinforces the shift from traditional ECM toward AI-driven orchestration, with content treated as a governed substrate for autonomous workflows across enterprise systems.

- May 2026: OpenText released Core Content Management 26.2, adding an AI-to-AI integration between Microsoft Copilot and OpenText Content Aviator. This tightens how content services are consumed inside everyday productivity workflows and increases competitive pressure on standalone CSP vendors to match embedded, suite-led experiences.

- April 2026: Box launched Box Automate and announced general availability of the Box Agent to route work across humans and AI agents using Box-managed content. By productizing agentic workflow orchestration on top of its content layer, Box expanded its platform positioning beyond storage and collaboration into end-to-end automation for unstructured processes.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers software platforms that let organizations store, govern, search, secure, and deliver enterprise content across multiple repositories and business applications.

Scope exclusions: We exclude general-purpose collaboration tools that do not provide core content services functions like governance, records retention, and content lifecycle controls.

Segmentation Overview

- By Component

- Solutions / Software

- Document and Records Management

- Data Capture

- Workflow Management

- Information Security and Governance

- Case Management

- Other Solutions / Software

- Services

- Integration and Deployment

- Consulting

- Support and Maintenance

- Solutions / Software

- By Deployment Model

- On-Premises

- Cloud

- By End-user Enterprise Size

- Small and Medium-sized Enterprises

- Large Enterprises

- By End-user Industry Vertical

- Banking, Financial Services and Insurance (BFSI)

- Government and Public Sector

- Healthcare and Life Sciences

- Information Technology and elecom

- Transportation and Logistics

- Other End-user Industry Verticals

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market context and to build a clean set of demand and supply signals for content services platforms. We reviewed public sources such as US SEC filings, the US Bureau of Labor Statistics, the US Census Bureau, NIST publications on information security, and OECD digital economy indicators, which helped us track IT spend direction and compliance priorities.

We also read vendor annual reports, investor presentations, product documentation, and reputable press coverage to map platform feature boundaries and typical buying cycles. Patent databases were checked to understand which functions are actively being developed, including content intelligence and automation for classification. The desk sources listed here are illustrative, and we used additional public and paid sources to collect data, validate assumptions, and address open questions.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with platform vendors, implementation partners, IT and security leaders, and content governance owners across major regions. These discussions helped confirm what is counted as platform revenue versus adjacent tools, and they refined inputs such as cloud migration pace, average contract values, and renewal behavior.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 12% | APAC: 45% |

| Mid tier: 53% | Functional/Unit leaders: 40% | EMEA: 34% |

| Smaller Players: 15% | Managers: 48% | Americas: 21% |

Market-Sizing & Forecasting

Our sizing uses a top-down approach where enterprise software and IT services spending is reconstructed by region, then filtered through indicators that reflect content services platform adoption. The filtered demand pool is converted into market value using pricing and deployment mix checks, followed by adjustments where adoption is uneven across industries.

To keep totals realistic, we corroborate top-down outputs with selective bottom-up approximations, including sampled average subscription and maintenance values, partner channel checks, and a limited roll-up of reported platform revenue where disclosures are clear. Inputs used in the model include cloud versus on-premises deployment mix, regulated content and records requirements, growth in digital documents and content workflows, cybersecurity and identity-control needs tied to content access, and the pace of repository modernization programs. Where bottom-up inputs were missing, we used ranges agreed during interviews and applied them only after they matched regional demand signals.

Forecasts were built using scenario analysis, since spending shifts are tied to macro IT budgets and enterprise migration timelines. In each scenario, variables such as cloud adoption rates, security and compliance spend, and enterprise digitization initiatives were moved together, then reviewed with expert feedback before finalizing the yearly curve.

Data Validation & Update Cycle

Validation was handled through multiple checks so the final number is consistent with how the market behaves in practice. We compared outputs against independent signals such as enterprise software spend direction, public revenue trends in content-centric software lines, and region-level cloud migration indicators, then reworked outliers before sign-off.

Before release, the model is reviewed step by step by another analyst to catch unit errors, mismatched year conversions, and unusual price or volume jumps. If a material variance shows up, we re-contact sources to confirm what changed, including pricing resets, bundling shifts, or regulation-driven demand. Reports are refreshed annually, with interim updates when major events could change adoption or vendor revenue reporting, and a final pre-delivery pass is completed to keep the latest information in view.

Mordor Intelligence's Content Service Platforms Market Size Versus Other Published Estimates

Published market sizes for content services platforms can vary even when the topic label appears similar. Differences usually come from which revenue streams are counted, which years are treated as the base, how cloud subscriptions are annualized, and how quickly assumptions are refreshed.

Workflow automation suites and adjacent content creation tools are common add-ons in enterprise deals, but Mordor Intelligence keeps those revenues outside the content services platforms scope unless they are sold and used as core content repository and governance functions. When some estimates bundle broader digital workplace software, the total moves up quickly, and when currency timing and ASP escalation are handled differently, the curve can shift as well.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 88.25 B (2026) | |

| Global Consultancy A | USD 66.90 B (2024) | Uses an earlier base year and often treats broader enterprise content management and related services as part of the platform total, which can shift the year-to-year comparability versus a platform-only view. |

| Trade Journal B | USD 56.27 B (2025) | Leans on a narrower regional coverage and may apply conservative pricing progression for subscriptions, which can keep the near-term value lower even if adoption growth is similar. |

The spread in the table is mainly explained by scope bundling and timing, not by a disagreement that platforms are growing. By keeping inputs tied to observable adoption signals and by checking pricing and deployment mix with interviews, the estimate stays traceable to repeatable steps that a reader can follow.

Key Questions Answered in the Report

How large is the content services platforms market in 2026?

The content services platforms market size is valued at USD 88.25 billion in 2026, with a projected 12.94% CAGR to 2031.

Which deployment model is growing fastest?

Cloud platforms are advancing at 19.21% CAGR, reflecting enterprise preference for scalable SaaS and integrated AI.

Why are SMEs adopting content services now?

Subscription pricing, low-code templates and bundled AI search reduce barriers, lifting SME growth to 14.49% CAGR through 2031.

What sector leads adoption today?

BFSI maintains the largest share at 25.62% thanks to stringent documentation and risk-management mandates.

Which region will outpace others by 2031?

Asia-Pacific is forecast for a 13.88% regional CAGR, driven by government digitization and manufacturing modernization efforts.

Page last updated on: