Vehicle Anti-Theft System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

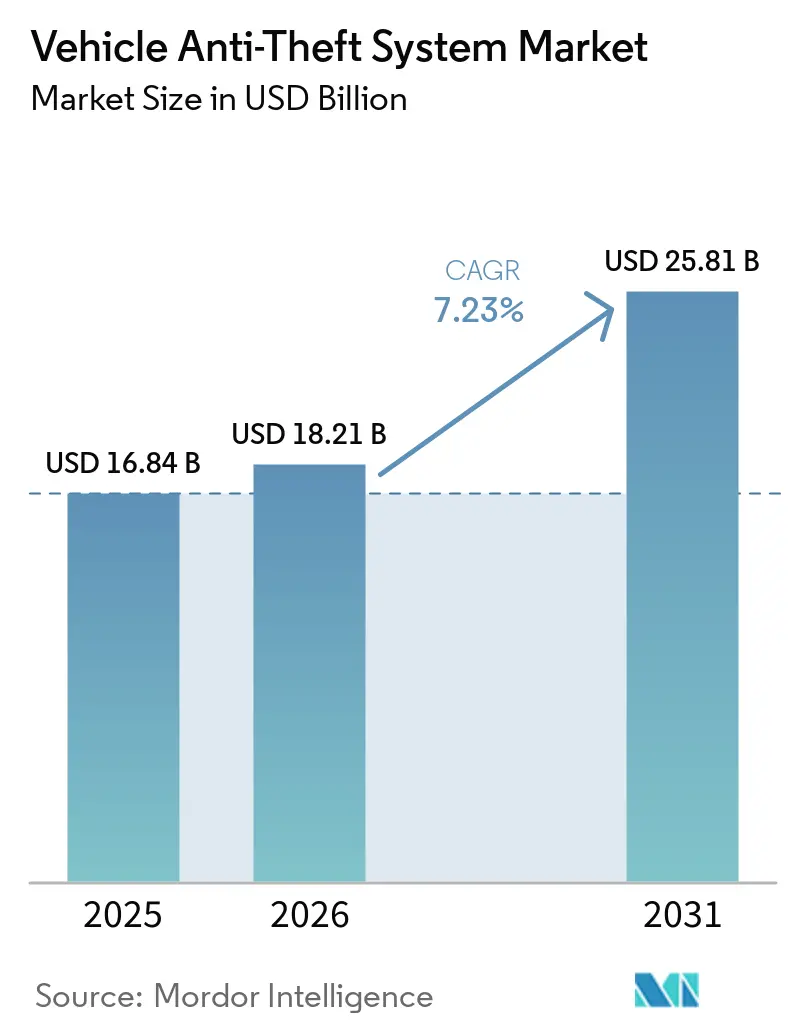

| Market Size (2026) | USD 18.21 Billion |

| Market Size (2031) | USD 25.81 Billion |

| Growth Rate (2026 - 2031) | 7.23% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vehicle Anti-Theft System Market Analysis by Mordor Intelligence

The vehicle anti-theft system market size was valued at USD 16.84 billion in 2025 and estimated to grow from USD 18.21 billion in 2026 to reach USD 25.81 billion by 2031, at a CAGR of 7.23% during the forecast period (2026-2031). Escalating relay and CAN-bus injection attacks are pushing automakers to replace legacy RFID keys with ultra-wideband (UWB) digital-key architectures, while governments tighten immobilizer mandates across Asia-Pacific and Europe. Insurance-premium discounts of 5%-25% in 12 US states are steering buyers toward factory-installed immobilizers and telematics, especially within commercial-vehicle fleets. At the same time, AI-driven anomaly-detection platforms such as Geotab and Samsara are creating a parallel layer of security that appeals to logistics operators seeking to reduce theft and crash losses. Competitive dynamics are intensifying as tier-1 suppliers co-develop UWB keys with smartphone OEMs, and regional specialists leverage aftermarket certification to serve price-sensitive niches in two-wheelers and construction equipment.

Key Report Takeaways

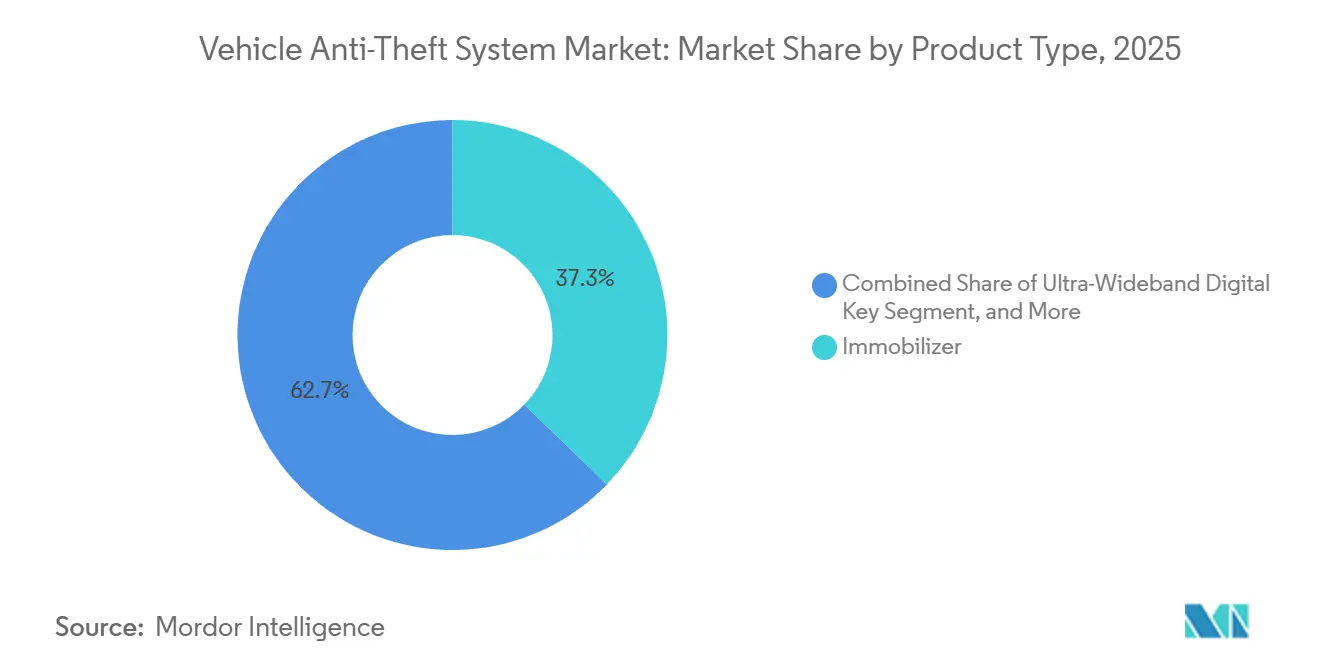

- By product type, immobilizers led with 37.25% of the vehicle anti-theft system market share in 2025, whereas UWB digital keys are projected to record the fastest 8.11% CAGR through 2031.

- By 2025, RFID transponders captured 45.16% of the market, while UWB technology is forecast to grow at a 7.56% CAGR through 2031.

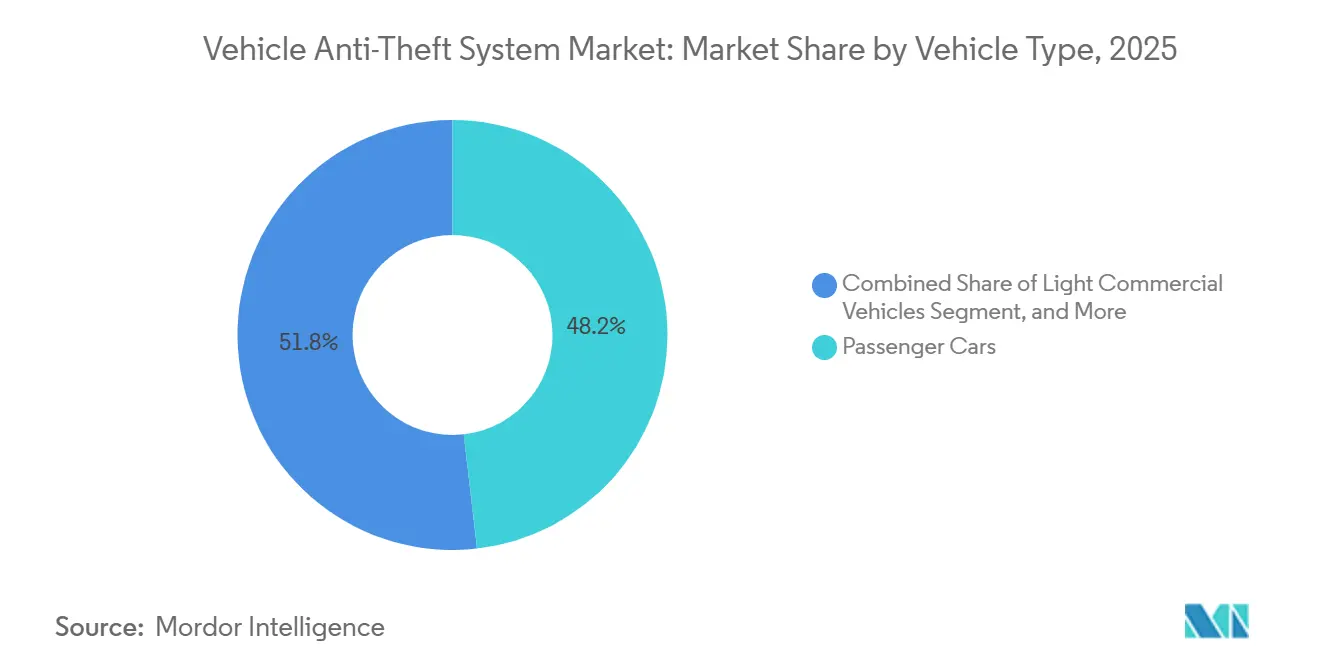

- By vehicle type, passenger cars accounted for 48.19% of the market in 2025, whereas two-wheelers and powersports are set to grow at a 7.96% CAGR across 2026-2031.

- By sales channel, OEM-installed solutions held a 64.53% market share in 2025 and are anticipated to expand at an 8.04% CAGR through 2031.

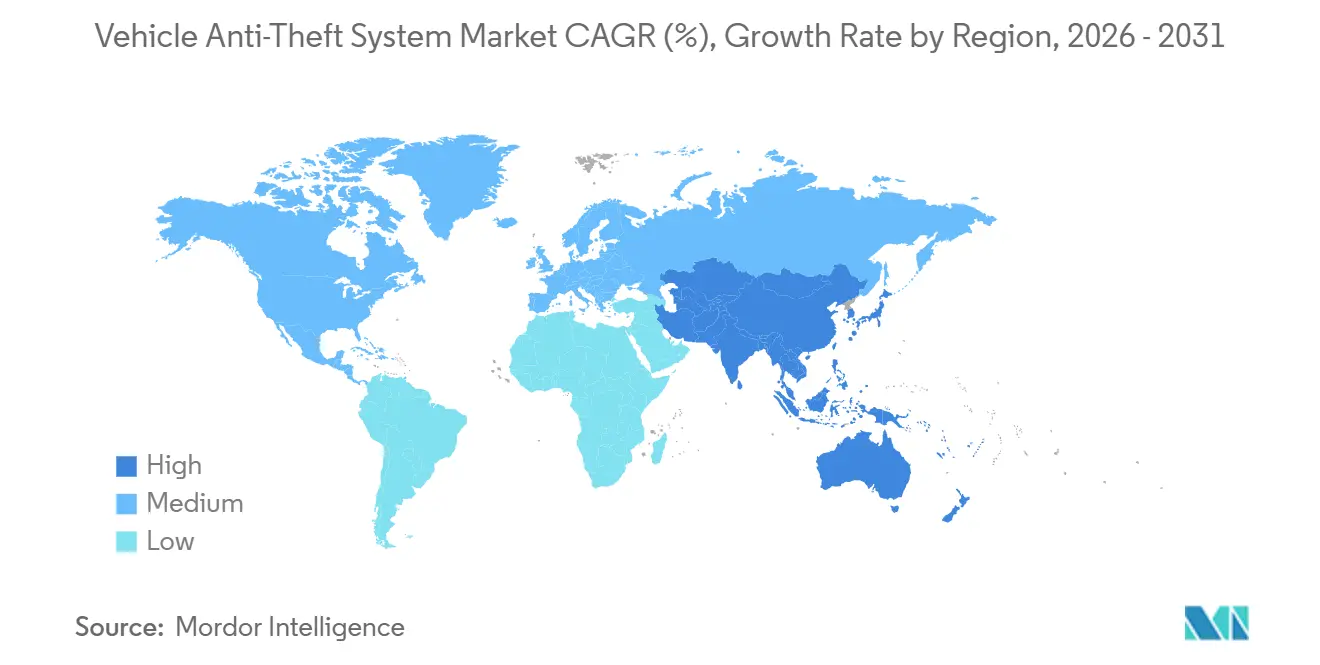

- By region, Asia-Pacific accounted for 35.34% of vehicle anti-theft system sales in 2025 and is poised to grow at a 7.74% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Vehicle Anti-Theft System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Vehicle-Theft Incidents | +1.8% | Global, spikes in North America, South America, and Asia-Pacific | Short term (≤ 2 years) |

| Government Mandates Making Immobilizers Compulsory | +1.5% | Asia-Pacific, South America, Europe | Medium term (2-4 years) |

| OEM Integration of Smart Keys and Connected Security | +1.3% | North America and Europe luxury segments, expanding to the Asia-Pacific | Medium term (2-4 years) |

| Insurance Premium Discounts for Certified Systems | +0.9% | North America, Europe, and emerging Asia-Pacific | Short term (≤ 2 years) |

| Ultra-Wideband Digital-Key Ecosystems | +0.7% | North America and Europe luxury segments, pilot Asia-Pacific | Long term (≥ 4 years) |

| AI-Driven Telematics Anomaly Detection for Fleets | +0.6% | Global commercial fleets, strongest in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Global Vehicle-Theft Incidents

Organized crime rings intensified relay and CAN-bus attacks during 2025-2026, with Rio de Janeiro logging 5,344 thefts in the first two months of 2026 and India recording 224,187 motorcycle thefts in 2023.[1]National Insurance Crime Bureau, “2025 National Auto Theft Statistics,” nicb.org The United States reported 659,880 thefts in 2025, yet specific brands without immobilizers saw disproportionate losses. Meanwhile, affordable dark-web relay devices priced below EUR 200 (USD 213) are spreading across Europe, widening pressure on OEMs to layer on immobilizers with GPS tracking and biometric authentication.[2]UK Home Office, “Crime in England and Wales 2025,” homeoffice.gov.uk

Government Mandates Making Immobilizers Compulsory

India’s AIS-140 regulation now extends to all passenger vehicles with engine capacities exceeding 1,500 cc, aiming to enhance vehicle safety and monitoring systems. Meanwhile, China’s GB 44495-2024 mandates comprehensive cybersecurity audits and the implementation of encrypted immobilizers across approximately 28 million vehicles annually, reflecting the country's focus on automotive cybersecurity. Brazil continues to enforce its long-standing Contran rules, while Europe’s Type Approval Regulation (EU) 2018/858 imposes stringent compliance requirements on manufacturers. These evolving regulations are significantly compressing original equipment manufacturers' (OEMs) development cycles, driving tier-1 suppliers to expedite the launch of ultra-wideband (UWB) key solutions and encrypted modules to meet the growing demand for secure and compliant automotive technologies.[3]European Data Protection Board, “Guidelines on Vehicle Data Processing,” edpb.europa.eu

OEM Integration of Smart Keys and Connected Security

BMW’s UWB-enabled Digital Key Plus on the iX, Hyundai’s face-recognition entry on the Genesis GV60, and Tesla’s planned facial unlock for Model S/X illustrate a significant shift toward advanced biometric and relay-attack-resistant access technologies. These innovations highlight the automotive industry's focus on enhancing vehicle security and user convenience. The integration of such technologies at the factory level not only provides a seamless user experience but also enables over-the-air (OTA) software updates. This capability ensures that vulnerabilities can be addressed and patched more efficiently compared to traditional aftermarket retrofits, thereby improving the overall security framework of modern vehicles.

Insurance Premium Discounts for Certified Systems

Thatcham’s revised five-star rating system and US state-level regulations have introduced significant cost-saving opportunities for vehicle owners and fleet operators. These measures provide 5%-30% premium savings for vehicles equipped with approved immobilizers, GPS trackers, or AI-based telematics systems, directly linking regulatory compliance to tangible consumer economic benefits.[4]Thatcham Research, “Vehicle Security Ratings 2025,” thatcham.org For instance, fleets that adopt advanced platforms such as Geotab or Samsara not only experience reduced loss ratios from enhanced vehicle tracking and monitoring but also qualify for substantial insurance rebates, further incentivizing their integration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront and Replacement Cost of Advanced Systems | -1.4% | Global, more pronounced in emerging markets | Short term (≤ 2 years) |

| Cybersecurity and Data Privacy Vulnerabilities | -0.8% | Global, with regulatory focus in Europe and North America | Medium term (2-4 years) |

| Sophisticated Relay/CAN Bus Injection Attacks | -0.6% | Global, concentrated in developed markets with keyless systems | Short term (≤ 2 years) |

| Aftermarket Installation Quality Variability | -0.5% | Global, particularly in regions with limited certified installers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront and Replacement Cost of Advanced Systems

Biometric entry systems, which add USD 300-800 at the factory and even higher costs in the aftermarket, are becoming a significant consideration for manufacturers and consumers alike. However, the high replacement cost of a lost smart key, which can reach up to USD 600 plus dealer programming fees, has discouraged adoption, particularly in price-sensitive Asia-Pacific markets. Additionally, fleet telematics hardware and associated subscription fees can increase three-year ownership costs by up to USD 2,300 per vehicle. This cost burden has slowed the adoption of telematics solutions, especially among small logistics operators who often operate on tight budgets and prioritize cost-efficiency.

Cyber-Security and Data-Privacy Vulnerabilities

In 2025, relay devices successfully bypassed immobilizers on several Toyota and Lexus models, leading to the urgent deployment of over-the-air patches to address the vulnerabilities. This incident highlighted the growing sophistication of cyber threats in the automotive sector. Furthermore, the upcoming ISO/SAE 21434 compliance deadline in Europe, set for July 2026, mandates that original equipment manufacturers (OEMs) implement comprehensive lifecycle-wide threat management systems. However, the significant investment required, ranging from USD 5 to 20 million per platform, has caused delays in the rollout of these measures, particularly in emerging markets where resources are limited.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Immobilizers Retain Scale While UWB Keys Gain Premium Traction

Immobilizers dominated the vehicle anti-theft system market, accounting for 37.25% of 2025 revenue, driven by their near-universal fitment across Europe and expanding mandates in India. These systems have become a standard feature in many vehicles, driven by stringent regulations and increasing consumer demand for enhanced vehicle security. However, the market is witnessing a shift as Ultra-Wideband (UWB) digital keys are gaining traction, growing at a compound annual growth rate (CAGR) of 8.11%. This growth is attributed to the increasing focus of original equipment manufacturers (OEMs) on developing relay-attack-resistant technologies. For instance, BMW's time-of-flight authentication technology has been designed to limit signal amplification to less than 10 cm, effectively addressing a critical vulnerability in fixed-frequency RFID keys. This innovation highlights the industry's commitment to advancing security measures in response to evolving threats.

Aftermarket alarms remain popular in North America, particularly among consumers seeking additional layers of security for their vehicles. However, the growing trend toward factory-installed immobilizer-plus-alarm packages is gradually eroding demand for standalone aftermarket alarm systems. Despite this, traditional security measures like steering-column locks have made a notable comeback. For example, Hyundai distributed 62,000 steering-column locks to owners of vehicles prone to USB-ignition bypass attacks. This move underscores the enduring relevance of low-tech hardware solutions in addressing specific vulnerabilities and maintaining public trust in vehicle security systems.

By Technology: RFID Maturity versus UWB Innovation

RFID transponders accounted for 45.16% of the revenue in 2025, serving as the primary immobilizer technology in the automotive market. These transponders operate on a static-frequency architecture, which, while effective, is vulnerable to relay amplification attacks. Such attacks exploit the static nature of the frequency, posing significant security risks to vehicles. Despite these challenges, RFID transponders remain a popular choice due to their affordability and compatibility with existing vehicle systems. Their widespread adoption underscores the need to develop enhanced security measures to mitigate risks and maintain consumer trust in this technology.

The ultra-wideband (UWB) market is growing at a CAGR of 7.56%, and its technology has introduced a new layer of security and convenience in the automotive sector. UWB operates by registering nanosecond-level time-of-flight measurements, enabling smartphones to function as secure digital keys. By 2025, this innovative feature is expected to be integrated into 18 different vehicle model lines, offering enhanced security and user convenience. Additionally, cellular-linked GPS trackers have become a critical tool for fleet management, processing trillions of data points to support theft recovery and predictive maintenance. However, biometric modules, which offer advanced security features, remain confined to luxury vehicle trims due to their high production costs, limiting their broader adoption.

By Vehicle Type: Two-Wheelers Outpace Passenger-Car Growth

Passenger cars accounted for 48.19% of the market demand in 2025, driven by the widespread adoption of immobilizer systems. The high penetration of these systems in passenger vehicles highlights their importance in enhancing vehicle security and reducing theft incidents. As the automotive industry continues to prioritize safety and security features, passenger cars are expected to maintain their dominance in the market. Additionally, the increasing integration of advanced technologies, such as GPS trackers and RFID-based systems, further supports the growth of this segment. These advancements cater to the rising consumer demand for enhanced vehicle safety and theft prevention measures.

The two-wheeler segment is projected to outpace the overall vehicle anti-theft system market CAGR, with an anticipated growth rate of 7.96%. This growth is primarily attributed to regulatory mandates in Indian states requiring RFID registration and GPS trackers for two-wheelers above 150 cc. Such regulations aim to improve vehicle tracking and reduce theft incidents in the region. Furthermore, the construction equipment sector presents a significant opportunity, as theft in this segment exceeds USD 1.5 billion annually. This highlights the demand for ruggedized immobilizers and geofencing solutions tailored to the unique requirements of construction equipment. These developments underscore the growing need for advanced anti-theft systems across various vehicle categories.

By Sales Channel: OEM Lead Widens as Software Locks-in Revenue

OEM solutions captured 64.53% of the market share in 2025, driven by insurance incentives and the growing adoption of over-the-air upgradability. These solutions have been expanding faster, with a CAGR of 8.04%, compared to the broader vehicle anti-theft system market. Minda Corporation, for instance, recorded a 18% year-on-year increase in passive-entry contracts, highlighting the potential for suppliers as OEMs transition their mid-tier portfolios to keyless-entry systems. OEMs' integration of advanced technologies has also enhanced the reliability and efficiency of these systems, further solidifying their dominance in the market. Additionally, the ability to offer seamless upgrades and enhanced security features has made OEM solutions a preferred choice among consumers and insurers alike.

Despite the dominance of OEM solutions, aftermarket channels continue to thrive in regions where Contran enforcement remains weak. These channels cater to a significant portion of the market, especially in areas where cost-sensitive consumers seek affordable alternatives. However, the variability in quality among aftermarket products has raised concerns, with 18% of retrofits reportedly turning off factory-installed alarms. This has prompted insurers to implement stricter certification requirements for installers to ensure the reliability of aftermarket solutions. The demand for aftermarket systems remains robust, particularly in emerging markets, but addressing quality issues will be critical for sustained growth in this segment.

Geography Analysis

Asia-Pacific led the vehicle anti-theft system market with 35.34% revenue share in 2025 and is projected to grow at a 7.74% CAGR through 2031. India’s AIS-140 GPS mandate and China’s January 2026 cybersecurity rules compel encrypted immobilizers across 28 million new vehicles annually, lifting demand for OEM modules and certified aftermarket trackers. Rising motorcycle theft, especially in Maharashtra and Karnataka, is accelerating sales of two-wheeler telematics. Additionally, the increasing adoption of connected vehicle technologies in the region is driving the integration of advanced anti-theft systems. Japan and South Korea maintain over 90% immobilizer penetration, yet now roll out patches to counter relay exploits. Furthermore, government initiatives promoting vehicle safety and security are expected to bolster the market growth in the region.

Europe maintains strict immobilizer compliance under Regulation (EU) 2018/858, yet theft patterns diverge. The United Kingdom cut theft by 11.36% to 90,625 incidents in 2025, while the Netherlands saw a 12% increase as inexpensive relay tools circulated online. The European Commission’s 2025 proposal to mandate biometrics on autonomous-ready models by 2028 positions suppliers such as Continental and Valeo for new contracts. Additionally, the growing adoption of electric vehicles in the region is expected to create opportunities for advanced anti-theft systems. The growing adoption of telematics and connected vehicle technologies is also driving market growth. Moreover, collaborations between automakers and technology providers are fostering innovation in anti-theft solutions tailored to European regulations and consumer preferences.

North America recorded 659,880 thefts in 2025, a 23% decline, yet Hyundai and Kia models without immobilizers remained vulnerable, prompting free steering-lock campaigns and software updates. The region's focus on advanced driver assistance systems (ADAS) and connected vehicle technologies is driving the adoption of integrated anti-theft solutions. South America faces surging pick-up theft, with Rio de Janeiro up 5% year-on-year and pick-up trucks up 12.2%. The increasing availability of affordable aftermarket anti-theft devices is also influencing the market in the region. Middle East and Africa remain nascent but register growing demand for GPS-mandated commercial-vehicle trackers under Gulf Cooperation Council safety rules. Additionally, rising vehicle ownership and the expansion of logistics and transportation sectors in these regions are expected to drive the adoption of anti-theft systems.

Competitive Landscape

The vehicle anti-theft system market demonstrates moderate concentration, with the top seven tier-1 suppliers Continental, Bosch, Valeo, Denso, HELLA, Tokai Rika, and Lear accounting for approximately 55%-60% of OEM shipments. Continental experienced a 14% increase in revenue from passive-entry systems and immobilizers in 2025, driven by stricter regulatory requirements in Europe and China. These regulations have pushed automakers to adopt advanced anti-theft technologies, creating growth opportunities for established players. Bosch has capitalized on hardware security modules compliant with ISO/SAE 21434 standards, securing ultra-wideband (UWB) key orders from major automakers like Mercedes-Benz and Volkswagen. This alignment with industry standards has strengthened Bosch's market position. Valeo, through its January 2026 partnership with Hero MotoCorp, has expanded its presence in the rapidly growing two-wheeler segment, further diversifying its portfolio and tapping into emerging markets with high growth potential.

Regional players also play a significant role in shaping the competitive landscape. Minda Corporation, for instance, has set an ambitious target of achieving USD 2.1 billion in revenue by fiscal 2030. The company leverages its 320 patents and 32 manufacturing facilities across Asia to meet both OEM and aftermarket demand. Its focus on innovation and regional expertise has allowed it to maintain a competitive edge in the market. Scorpion Automotive, a European specialist, focuses on Thatcham-approved alarms, which are highly regarded for their reliability and compliance with insurance standards. Meanwhile, Directed LLC benefits from US insurance rebates on its GPS-enabled Viper trackers, which are gaining traction among consumers for their advanced tracking capabilities and integration with modern vehicle systems. These regional players contribute to the market's diversity and cater to specific consumer needs.

Emerging disruptors are also reshaping the market dynamics. Companies like Geotab and Samsara are integrating artificial intelligence (AI) into their solutions to detect unauthorized engine starts and geofence breaches, reducing fleet theft losses by up to 75%. These innovations are particularly appealing to fleet operators, who face significant financial losses due to vehicle theft. Additionally, smartphone manufacturers such as Apple, Samsung, Xiaomi, and Huawei are entering the space through the Car Connectivity Consortium. These companies are embedding UWB radios in their handsets, enabling smartphones to function as car keys. While this adds convenience for consumers, proprietary OEM authentication systems ensure that automakers retain control over the broader ecosystem.

Vehicle Anti-Theft System Industry Leaders

Continental AG

Robert Bosch GmbH

Valeo SE

Denso Corporation

Tokai Rika Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Valeo partnered with Hero MotoCorp to integrate GPS tracking and motion-sensor alarms on premium motorcycles priced above INR 150,000 (USD 1,800).

- January 2026: Tesla announced facial-recognition entry for Model S and Model X variants, scheduled for late-2026 launch.

- January 2026: Valeo and Kapsch TrafficCom agreed to deploy vehicle-to-infrastructure tolling systems incorporating passive keyless entry and GPS tracking.

- January 2026: China enforced GB 45672-2025, mandating real-time crash and location data transmission via 5G on all new passenger cars.

Global Vehicle Anti-Theft System Market Report Scope

The Vehicle Anti-Theft System Market encompasses electronic, electromechanical, and software-based security solutions designed to deter unauthorized vehicle access, operation, or theft. These systems include immobilizers with cryptographic key authentication, GPS tracking, and telematics for real-time monitoring and recovery; alarm systems with sensors for motion/shock detection; biometric access controls; steering locks; central locking mechanisms; and connected platforms that integrate multiple features via mobile apps.

The Vehicle Anti-Theft System Market Report is Segmented by Product Type (Alarm, Immobilizer, Steering-Wheel/Column Lock, Passive Keyless Entry, Biometric Capture Device, GPS/GSM Tracking System, Ultra-Wideband Digital Key), Technology (RFID, GPS/GNSS, GSM/LTE/5G, Bluetooth/BLE, Ultra-Wideband (UWB), and Biometric), Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Two-Wheelers and Powersports, and Off-Road and Construction Equipment), Sales Channel (OEM-Installed, and Aftermarket), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

| Alarm |

| Immobilizer |

| Steering-Wheel / Column Lock |

| Passive Keyless Entry |

| Biometric Capture Device |

| GPS / GSM Tracking System |

| Ultra-Wideband Digital Key |

| RFID |

| GPS / GNSS |

| GSM / LTE / 5G |

| Bluetooth / BLE |

| Ultra-Wideband (UWB) |

| Biometric (Fingerprint / Facial) |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

| Two-Wheelers and Powersports |

| Off-Road and Construction Equipment |

| OEM-Installed |

| Aftermarket |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Product Type | Alarm | ||

| Immobilizer | |||

| Steering-Wheel / Column Lock | |||

| Passive Keyless Entry | |||

| Biometric Capture Device | |||

| GPS / GSM Tracking System | |||

| Ultra-Wideband Digital Key | |||

| By Technology | RFID | ||

| GPS / GNSS | |||

| GSM / LTE / 5G | |||

| Bluetooth / BLE | |||

| Ultra-Wideband (UWB) | |||

| Biometric (Fingerprint / Facial) | |||

| By Vehicle Type | Passenger Cars | ||

| Light Commercial Vehicles | |||

| Heavy Commercial Vehicles | |||

| Two-Wheelers and Powersports | |||

| Off-Road and Construction Equipment | |||

| By Sales Channel | OEM-Installed | ||

| Aftermarket | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the projected value of the vehicle anti-theft system market by 2031?

The market is forecast to reach USD 25.81 billion by 2031.

Which product category currently leads global demand?

Immobilizers held the largest 37.25% share in 2025 owing to broad regulatory mandates.

Why are ultra-wideband digital keys gaining traction?

UWB keys resist relay attacks by measuring signal time-of-flight, prompting faster OEM adoption in premium segments.

How do insurance incentives influence anti-theft adoption?

Certified immobilizers and AI-powered telematics can cut premiums by 5%-30%, accelerating factory integration and fleet retrofits.

Which region is expected to post the fastest growth?

Asia-Pacific is set for a 7.74% CAGR through 2031, driven by Indian and Chinese security regulations.

How concentrated is supplier competition in this space?

The top seven tier-1 suppliers control about 55%-60% of shipments, reflecting moderate concentration and active regional competition.

Page last updated on: