Automotive Cybersecurity Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

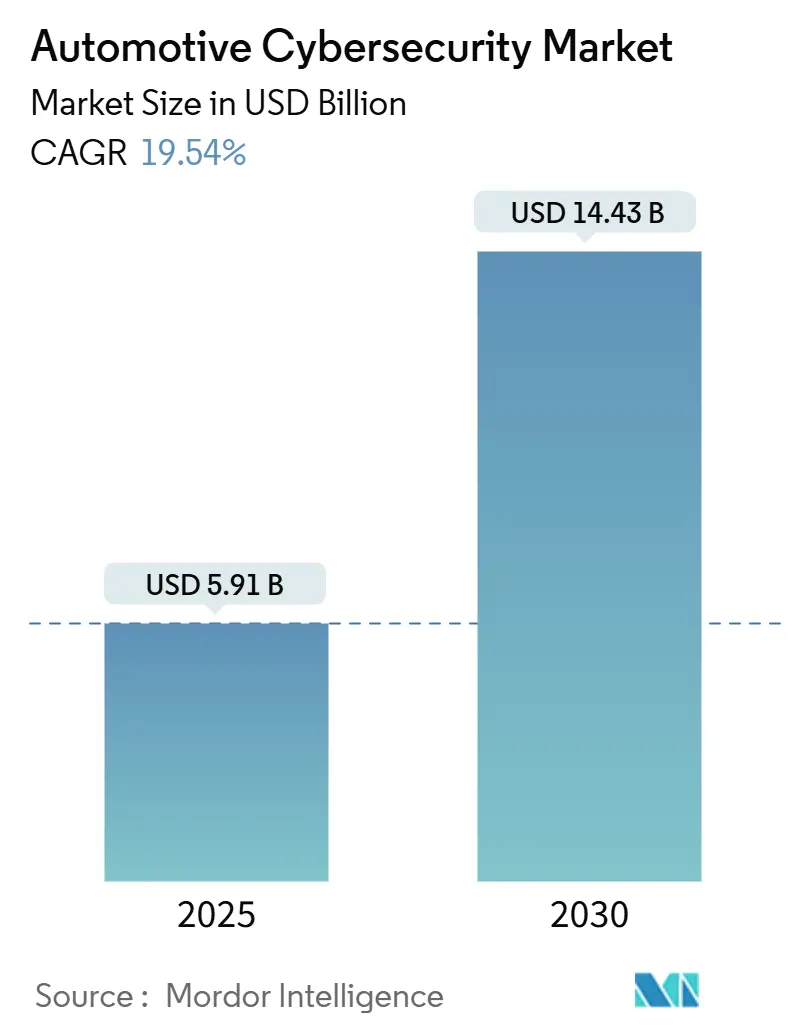

| Market Size (2025) | USD 5.91 Billion |

| Market Size (2030) | USD 14.43 Billion |

| Growth Rate (2025 - 2030) | 19.54% CAGR |

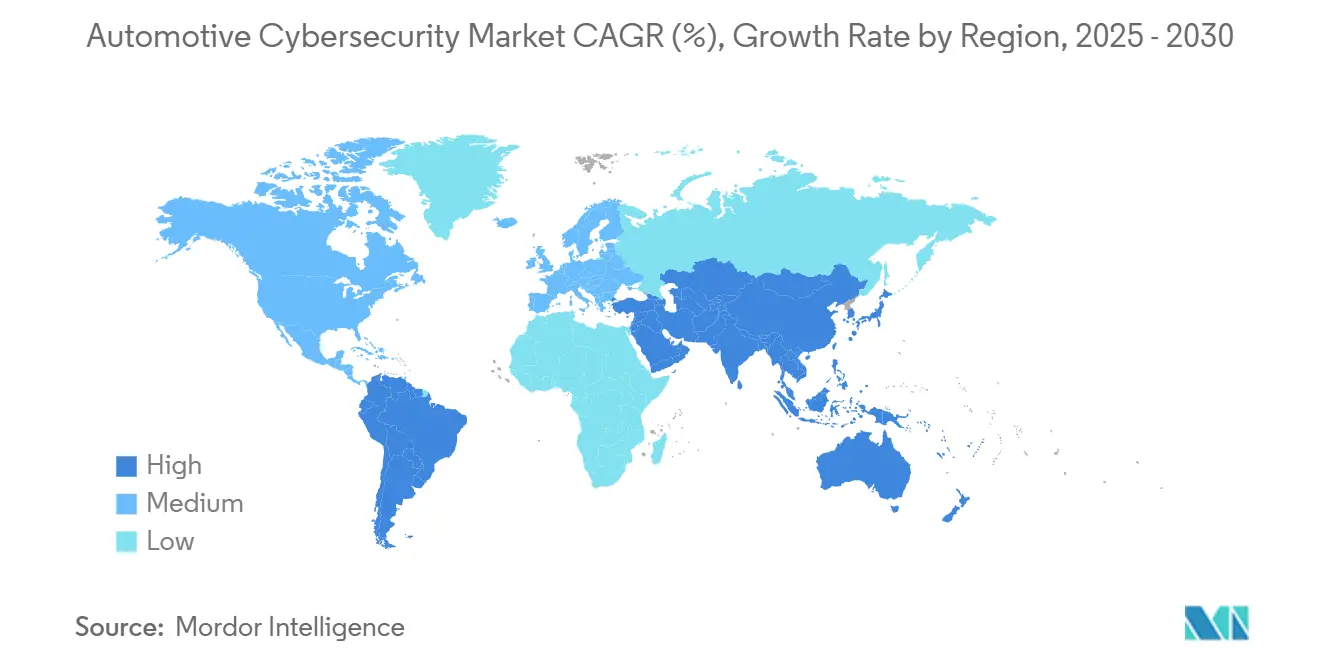

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

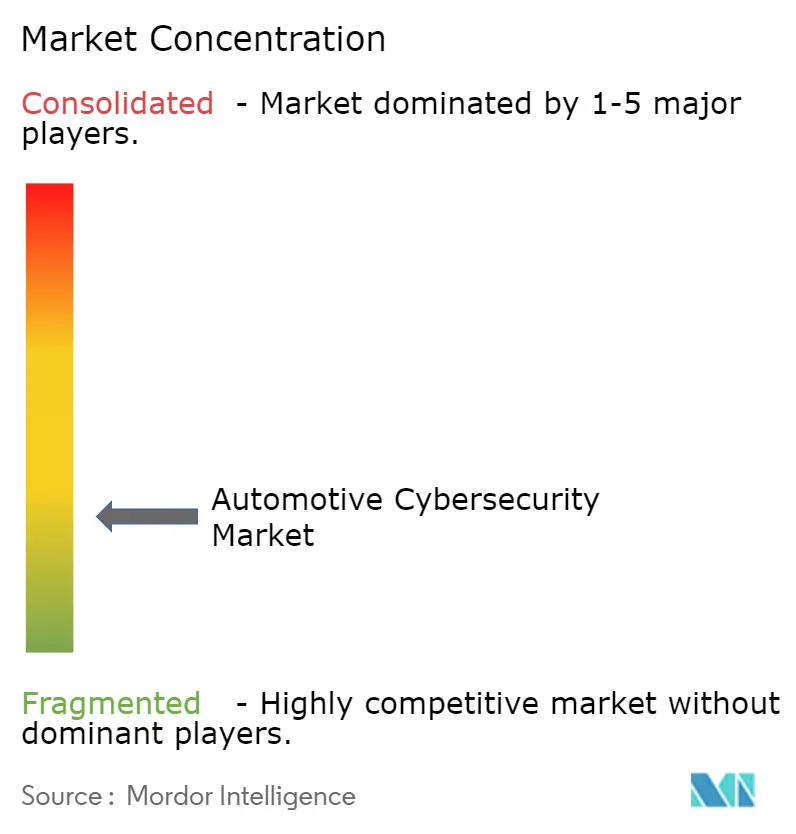

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Cybersecurity Market Analysis by Mordor Intelligence

The Automotive Cybersecurity Market size is estimated at USD 5.91 billion in 2025, and is expected to reach USD 14.43 billion by 2030, at a CAGR of 19.54% during the forecast period (2025-2030).

Strong regulatory enforcement, the proliferation of electronic control units (ECUs), and the shift toward software-defined vehicles continue to widen the attack surface, prompting original equipment manufacturers (OEMs) to redesign security architectures. Consolidation of multiple vehicle functions into high-performance domain controllers concentrates cyber-risk and accelerates demand for end-to-end cyber-protection platforms. UNECE WP.29 regulations now require cybersecurity management systems for type approval in 54 countries, creating a compliance-driven purchasing cycle that favours vendors offering lifecycle monitoring and incident-response capabilities.[1]United Nations Economic Commission for Europe, “UN Regulation 155 – Cyber Security and Cyber Security Management System,” unece.org Cloud-delivered analytics further reshape the automotive cybersecurity market as real-time fleet monitoring becomes indispensable for over-the-air (OTA) updates and threat intelligence. Meanwhile, persistent skills shortages inside OEM engineering teams create white space for managed security service providers able to bundle hardware, software, and 24 × 7 monitoring.

Key Report Takeaways

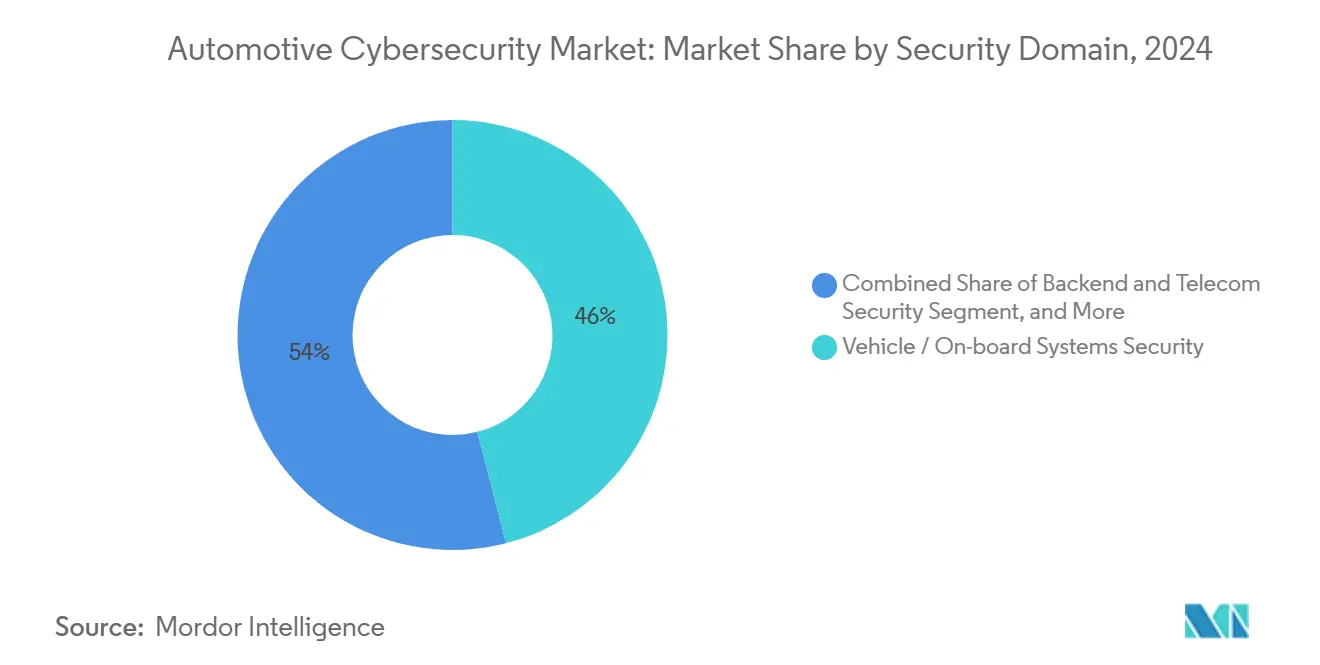

- By security domain, Vehicle/On-board Systems Security led with 46.0% revenue share of the automotive cybersecurity market in 2024, whereas Production (OT and IIoT) Security is projected to expand at a 25.0% CAGR through 2030.

- By deployment model, on-premises solutions accounted for 48.1% automotive cybersecurity market share in 2024, while cloud-based platforms are forecast to register a 26.8% CAGR to 2030.

- By solution type, Embedded Security Software accounted for 37.5% share of the automotive cybersecurity market size in 2024, while Cloud-based Security Platforms are projected to register a 25.44% CAGR through 2030.

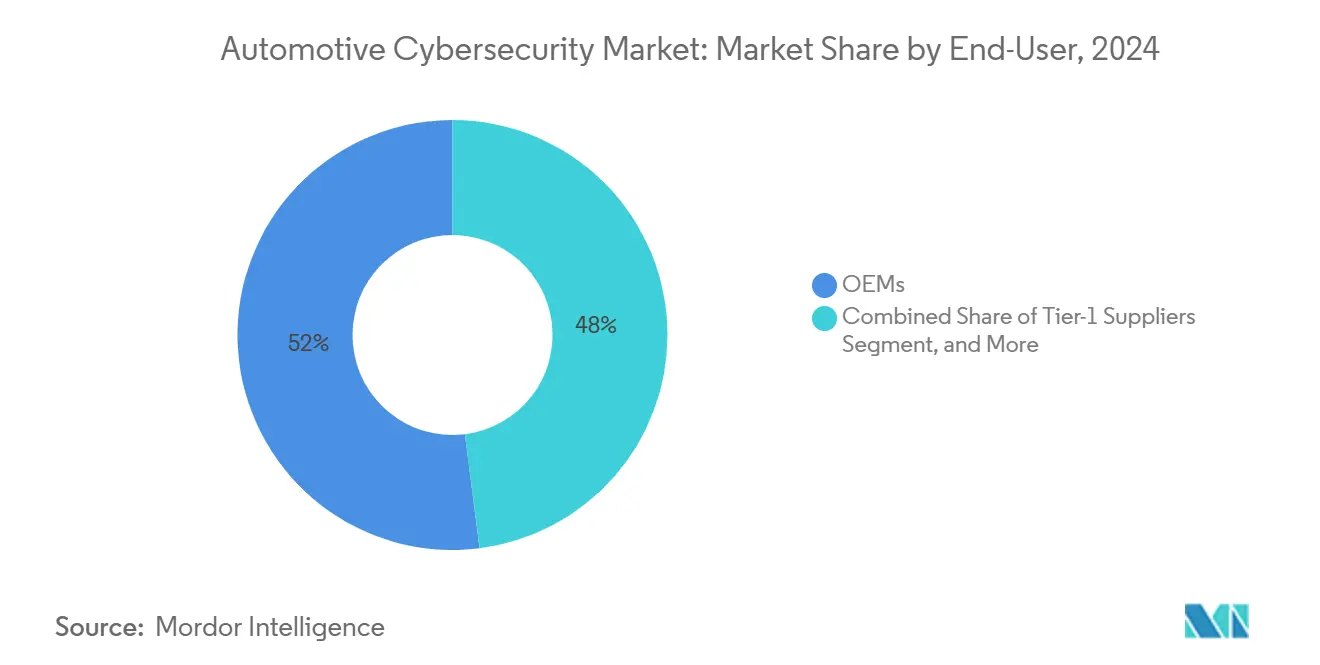

- By end user, OEMs commanded 52.0% of the automotive cybersecurity market size in 2024, whereas smart-factory operators will grow fastest at 24.1% CAGR between 2025 and 2030.

- By geography, Europe captured 34.0% of automotive cybersecurity market share in 2024 and Asia-Pacific is set to post a 25.8% CAGR through 2030.

Global Automotive Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| UNECE WP.29 mandatory compliance deadlines (2024+) | +4.80% | Global, with strongest enforcement in EU, Japan, South Korea | Short term (≤ 2 years) |

| Surging ECU and OTA update attack-surface | +5.20% | Global, with highest exposure in North America and Europe | Medium term (2-4 years) |

| OEM shift to centralized SDVs (software-defined vehicles) | +4.10% | Global, led by premium brands in North America and Europe | Medium term (2-4 years) |

| Growing EV charging-infrastructure vulnerabilities (under-reported) | +2.90% | APAC core, spill-over to North America and Europe | Long term (≥ 4 years) |

| Insurance premium discounts for cyber-secured fleets (under-reported) | +2.40% | North America and Europe, emerging in APAC | Long term (≥ 4 years) |

| AI-powered threat detection and automated response systems adoption | +1.80% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

UNECE WP.29 Mandatory Compliance Deadlines Drive Market Acceleration

The July 2024 enforcement of Regulation No. 155 obliges automakers to install cybersecurity management systems that span design, production, and post-production monitoring.[2]TÜV SÜD, “Mandatory Digital Shield for All New Cars,” tuvsud.com Type approval now hinges on documented risk assessments and validated countermeasures, prompting every OEM and tier-1 supplier to embed security-by-design practices. The regulation’s scope covers passenger cars, light commercial vehicles, two-wheelers exceeding 25 km/h, and even trailers, broadening the total addressable portion of the automotive cybersecurity market. Laboratories accredited under WP.29 have reported double-digit increases in testing backlogs, a signal that compliance spending is advancing quickly toward full-vehicle and fleet-wide monitoring subscriptions.

Surging ECU and OTA Update Attack Surfaces Expand the Threat Landscape

Modern vehicles ship with more than 100 million lines of code across upwards of 100 ECUs, raising the probability of exploitable bugs.[3]Magna International, “Cybersecurity in the Automotive Industry,” magna.com OTA capabilities, while crucial for feature deployment, expose remote services that attackers can weaponize unless authentication and encryption are rigorously enforced. As vehicle-to-everything (V2X) interfaces proliferate, automakers must validate third-party software libraries and continuously patch vulnerabilities that appear after vehicles have entered service. Global recall data indicate that software faults already account for an increasing share of safety notices, reinforcing the necessity of embedded intrusion detection and encrypted firmware delivery.

OEM Shift to Centralized Software-Defined Vehicles Reshapes Security Architecture

Centralized computing platforms collapse historically discrete controllers into a handful of high-performance chips, making any single exploitable weakness a systemic threat. Upstream’s 2025 Automotive Cybersecurity Report notes that 92% of observed attacks were executed remotely, underscoring why perimeter-only defenses are no longer adequate. As the automotive cybersecurity market expands, DevSecOps adoption inside engineering organizations is accelerating so that security validation keeps pace with weekly, not annual, software drops. Machine-learning-powered threat detection tailored for Controller Area Network (CAN) and Automotive Ethernet traffic is rapidly displacing static code-review regimes.

Growing EV Charging Infrastructure Vulnerabilities Create Systemic Risks

Independent audits of Open Charge Point Protocol (OCPP) implementations show exploitable defaults that could enable denial-of-service or malicious firmware flash at public chargers. Because chargers link payment, vehicle battery management, and grid load-balancing systems, compromise can ripple far beyond individual cars. With national charging rollouts prioritizing speed over hardening, governments are beginning to classify charging networks as critical infrastructure, foreshadowing tighter standards and new spending streams for specialized operational-technology (OT) security suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Long homologation cycles vs. rapid threat evolution | -3.20% | Global, most pronounced in highly regulated markets | Medium term (2-4 years) |

| Shortage of automotive-grade cyber talent | -2.80% | Global, acute in North America and Europe | Long term (≥ 4 years) |

| High up-front cost for legacy platform retrofit (under-reported) | -2.10% | Global, particularly impacting Tier-1 suppliers and aftermarket | Medium term (2-4 years) |

| Liability-allocation ambiguity across value-chain (under-reported) | -1.60% | Global, with regulatory uncertainty in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Long Homologation Cycles Constrain Rapid Threat Response

Vehicle type approval commonly spans 18–24 months, during which novel exploits routinely outpace design mitigations. Although ISO/SAE 21434 formalizes a risk-based approach, regulatory sign-off still depends on static documentation snapshots. Consequently, OEMs must architect post-production update pipelines that preserve safety certifications while enabling swift patch deployment—a technical and procedural balancing act that can delay fleet-wide remediation.

Shortage of Automotive-Grade Cybersecurity Talent Dampens Market Momentum

Domain convergence forces cybersecurity engineers to master functional safety standards, in-vehicle networking protocols, and real-time operating systems. Continental AG reports multi-quarter lead times to fill senior embedded-security positions, even as vehicle programs compress software release cadences. In response, vendors of managed detection and response (MDR) services are emphasizing turnkey offerings that offset head-count constraints for OEMs and tier-1 suppliers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Security Domain: Vehicle Systems Retain Primacy While Production Security Accelerates

The automotive cybersecurity market size allocated to Vehicle/On-board Systems Security amounted to 46.0% in 2024, reflecting immediate regulatory pressure to safeguard powertrain, chassis, and advanced driver-assistance functions. Central gateway encryption, secure boot, and in-vehicle intrusion detection now form the baseline stack across new platforms. Alongside, back-end and telecom security spending are rising as data-lake analytics link vehicle-side logs to centralized security operations centers.

Production (OT and IIoT) Security is forecast to record a 25.0% CAGR to 2030, the fastest among all domains. Smart-factory rollouts blend robot controllers, programmable logic controllers, and industrial Ethernet—the convergence invites ransomware operators who increasingly pivot from IT to OT targets. Fortinet telemetry shows manufacturing to be among the top three industries hit by OT-specific malware in 2024. Automakers therefore invest in segmentation policies, zero-trust access, and digital twins that stress-test plant networks before commissioning.

By Solution Type: Embedded Software Dominates as Cloud Platforms Surge

Embedded security software captured 37.5% revenue in 2024 on the strength of host-based firewalls, secure hypervisors, and cryptographic key-stores that remain operative even without cellular coverage. Hardware security modules (HSMs) are tile-mapped onto system-on-chips to secure bootloaders and sign OTA updates. Simultaneously, managed security services gain relevance where budget holders prefer predictable operating expenditure to scaling in-house security operations centers.

Cloud-based security platforms will expand at a 25.44% CAGR through 2030 as fleet-level anomaly detection relies on deep-learning models processing petabytes of telematics data. Cloud4C observes that software-defined vehicle programs now budget more for cloud-native security analytics than for traditional endpoint tools. Unified dashboards that correlate vehicle, charger, and supply-chain alerts offer value not attainable via siloed embedded agents alone.

By End User: OEMs Dominate While Smart-Factory Operators Drive Growth

OEMs held 52.0% of automotive cybersecurity market share in 2024 because liability and brand reputation sit squarely with vehicle makers under WP.29. They bundle encryption, intrusion detection, and digital-twin-based validation during new platform launches. Tier-1 suppliers follow suit as contract renewals increasingly specify cybersecurity maturity metrics.

Smart-factory operators will grow revenue at 24.1% CAGR to 2030, propelled by high-speed 5G private networks that stretch the threat perimeter from enterprise IT to production robots. Fusion Worldwide notes semiconductor shortages have sharpened awareness of plant downtime costs, accelerating OT-centric security investment.

By Deployment: On-Premises Control Remains but Cloud Momentum Builds

On-premises installations account for 48.1% of spending, favoured for development toolchains, build servers, and proprietary data that OEMs are reluctant to route through shared infrastructure. Webroot analysis points out that local deployments facilitate deterministic latency and diagnostic access during vehicle validation.

Yet cloud deployment is racing ahead at 26.8% CAGR, enabled by elasticity that aligns with fluctuating OTA traffic and by cross-OEM threat-intelligence exchanges. Hybrid modes—edge analytics inside the vehicle, policy orchestration in the cloud—are emerging as the architecture of choice for 2026-model-year platforms.

Geography Analysis

Europe generated 34.0% of the automotive cybersecurity market revenue in 2024, underpinned by the European Union’s blanket enforcement of WP.29 for every new vehicle category. Germany’s cluster of premium brands accelerates pilot adoption of vehicle security operations centers (VSOCs), while the United Kingdom leverages deep infosec capabilities to incubate cyber-risk pools and insurance offerings. Cross-border regulatory alignment lets suppliers certify once and deploy across the entire bloc, trimming go-to-market timelines.

Asia-Pacific is projected to post a 25.8% CAGR through 2030 as China scales battery-electric vehicle exports and Japan integrates high-bandwidth in-vehicle infotainment that necessitates hardened backend gateways. Battery-swap ecosystems, particularly in China, create new authentication challenges now being addressed by home-grown HSM vendors. South Korea’s nationwide 5G coverage catalyses V2X pilots that depend on low-latency certificate management—a sub-segment attracting fresh investment from local telecom operators.

Within the global Automotive Cybersecurity Market, North America continues to exert influence influential through regulatory committees shaping over-the-air update guidelines and cybersecurity labelling schemes. OEM–technology-company alliances headquartered in the United States drive patents around ML-based intrusion detection, while Canada’s manufacturing corridor aligns federal R and D tax credits with vehicle-security prototypes. Mexico’s export-oriented assembly plants adopt OT micro-segmentation to secure production lines that feed USMCA trade flows.

Mordor Intelligence provides coverage of the automotive cybersecurity market across other key regional markets, including Europe, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The automotive cybersecurity market is moderately fragmented as legacy tier-1 suppliers intersect with niche cybersecurity start-ups and hyperscale cloud providers. Continental AG and Robert Bosch GmbH integrate cryptographic keys and secure boot at the silicon level, while Argus Cyber Security and Karamba Security focus on lightweight, host-based intrusion-prevention modules tailored for resource-constrained ECUs. Technology giants enter via acquisition: BlackBerry Limited leverages QNX real-time OS ubiquity to pivot Cylance’s AI defenses into vehicle domains, whereas Intel Corporation extends silicon-root-of-trust capabilities inherited from Mobileye across automated-driving stacks.

Strategic partnerships define go-to-market playbooks. Upstream Security teamed with OTORIO in 2025 to merge fleet-centric data lakes with plant-floor threat-hunting, delivering continuous coverage from design through decommissioning.[4] BMW i Ventures’ USD 12 million placement in RunSafe Security exemplifies OEM venture capital’s role in hardening supply-chain binaries. Cadence Design Systems planned Secure-IC acquisition points to growing demand for pre-silicon side-channel-resistant IP blocks inside next-generation domain controllers.

Managed security services gain traction where talent shortages pinch. HSB’s “Cyber for Auto” policy bundles insurance with continuous VSOC monitoring, appealing to smaller fleet operators that lack in-house analysts. Cloud hyperscalers, notably Google Cloud, cement positions by offering AI-driven log-analysis pipelines that ingest petabyte-scale telemetry from mixed-brand fleets.

Automotive Cybersecurity Industry Leaders

Harman International Industries, Incorporated

Continental AG

Aptiv PLC

BlackBerry Limited

NXP Semiconductors N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Upstream Security partnered with OTORIO to provide unified protection spanning vehicle and factory ecosystems.

- February 2025: NCC Group joined Auto-ISAC as a strategic partner to expand threat-intelligence sharing for connected vehicles.

- February 2025: Upstream Security launched Ocean AI to automate investigation and response workflows for automotive VSOCs.

- January 2025: Cadence Design Systems announced its intent to acquire Secure-IC, bringing embedded security IP to automotive semiconductor customers.

Global Automotive Cybersecurity Market Report Scope

| Vehicle / On-board Systems Security |

| Backend and Telecom Security |

| Production (OT and IIoT) Security |

| Supply-Chain and Logistics Security |

| Hardware Security Modules (HSM) |

| Embedded Security Software |

| Managed Security Services |

| Cloud-based Security Platforms |

| Security Testing and Audit Tools |

| OEMs |

| Tier-1 Suppliers |

| After-market Service Providers |

| Fleet and Mobility Operators |

| Smart-Factory Operators |

| On-Premise |

| Cloud |

| Hybrid |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Security Domain | Vehicle / On-board Systems Security | |

| Backend and Telecom Security | ||

| Production (OT and IIoT) Security | ||

| Supply-Chain and Logistics Security | ||

| By Solution Type | Hardware Security Modules (HSM) | |

| Embedded Security Software | ||

| Managed Security Services | ||

| Cloud-based Security Platforms | ||

| Security Testing and Audit Tools | ||

| By End User | OEMs | |

| Tier-1 Suppliers | ||

| After-market Service Providers | ||

| Fleet and Mobility Operators | ||

| Smart-Factory Operators | ||

| By Deployment | On-Premise | |

| Cloud | ||

| Hybrid | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value and expected growth of the automotive cybersecurity market?

The automotive cybersecurity market size reached USD 5.91 billion in 2025 and is projected to hit USD 14.43 billion by 2030, posting a 19.54% CAGR.

Which security domain holds the largest revenue share?

Vehicle/On-board Systems Security accounted for 46.0% of global spending in 2024.

Which region is expanding fastest in automotive cybersecurity market?

Asia-Pacific is forecast to grow at 25.8% CAGR through 2030, driven by electric-vehicle adoption and 5G-based connectivity programs.

How do UNECE WP.29 regulations influence purchasing decisions?

Starting July 2024, every new vehicle sold in 54 countries must pass cybersecurity audits, prompting OEMs to prioritize lifecycle monitoring and incident-response solutions.

Why are cloud-based platforms gaining traction in vehicle security?

Fleet-wide anomaly detection and AI-driven threat analytics require elastic compute power that on-premise hardware cannot provide cost-effectively, fueling a 26.8% CAGR for cloud deployments.

What strategies help OEMs address the cybersecurity talent gap?

Many automakers partner with managed security service providers and utilize DevSecOps toolchains to compensate for limited in-house expertise, ensuring continuous compliance and faster patch cycles.

Page last updated on: