Automatic Emergency Braking Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 73.12 Billion |

| Market Size (2030) | USD 99.43 Billion |

| Growth Rate (2025 - 2030) | 6.34% CAGR |

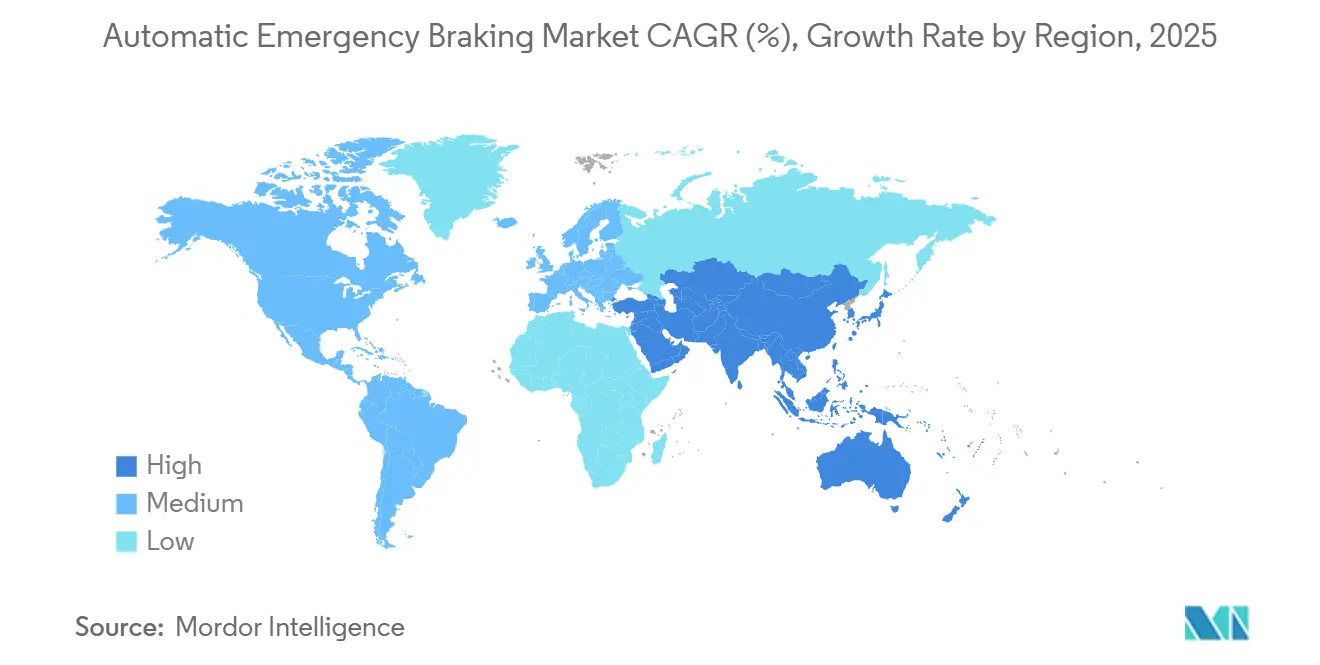

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automatic Emergency Braking Market Analysis by Mordor Intelligence

The automatic emergency braking market size reached USD 73.12 billion in 2025 and is forecast to expand at a 6.34% CAGR, pushing the value to USD 99.43 billion by 2030. The upward trajectory is anchored in synchronized regulatory mandates that compel every light vehicle in the United States, China, Europe, India, and other major regions to install compliant AEB systems within the next five years. Rapid electric-vehicle penetration, falling sensor prices, and intensifying NCAP safety assessments are accelerating technology diffusion, while looming cybersecurity requirements and high retrofit costs keep adoption asymmetrical across vehicle classes. Competitive intensity is rising as Tier-1 suppliers bundle radar, camera, and emerging LiDAR units into modular sensor-fusion suites designed for over-the-air updates. These forces collectively position the automatic emergency braking market as a linchpin for Level 2+ driver assistance rollouts and a critical gateway to autonomous driving.

Key Report Takeaways

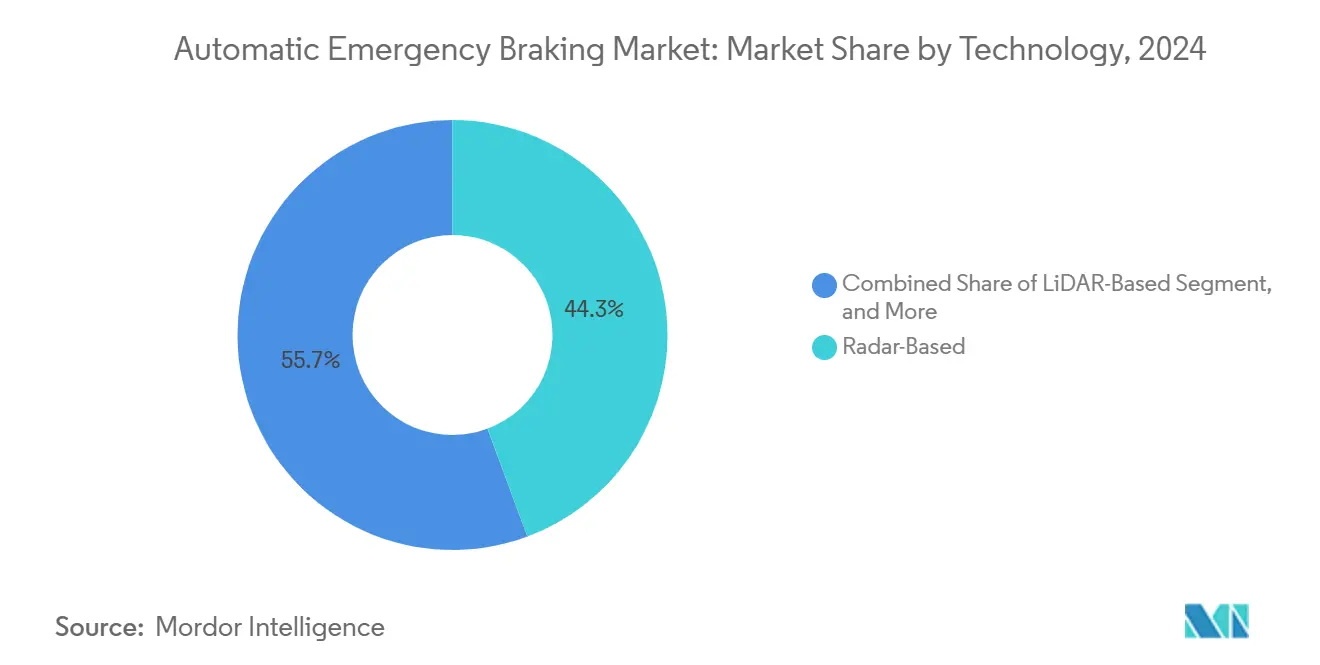

- By technology, radar-based solutions led with 44.32% automatic emergency braking market share in 2024, while sensor-fusion platforms anchored by solid-state LiDAR are projected to post the fastest 6.68% CAGR through 2030.

- By vehicle type, passenger cars accounted for 69.13% of the automatic emergency braking market size in 2024, whereas electric cars are poised for the quickest 6.82% CAGR to 2030.

- By operating speed, low-speed systems below 40 km/h held a 52.87% automatic emergency braking market share in 2024; pedestrian-detection solutions aimed at vulnerable road users are forecast to grow at an 8.57% CAGR.

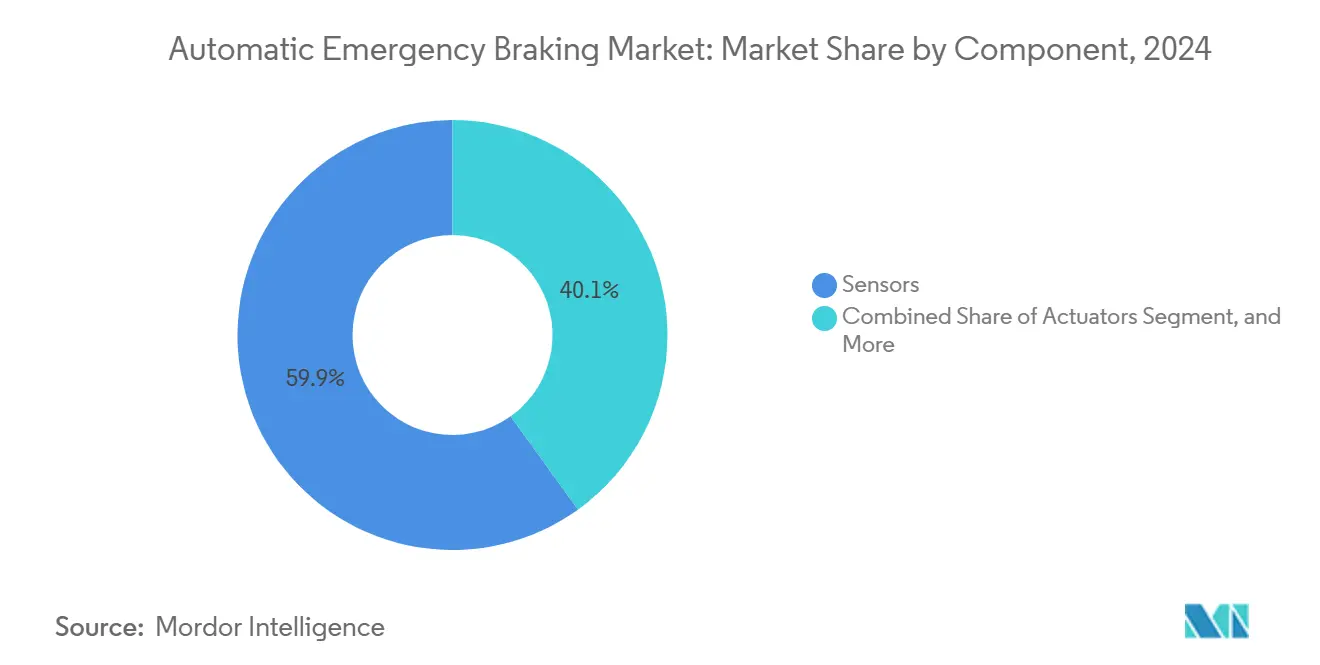

- By component, sensors captured 59.91% of the automatic emergency braking market size in 2024, even as software and algorithms are set to expand at a 7.46% CAGR through 2030.

- By sales channel, OEM-fitted units dominated with an 85.32% share in 2024; the aftermarket retrofit channel is expected to rise at an 8.83% CAGR as fleets update legacy vehicles.

- By geography, Asia-Pacific commanded a 42.30% automatic emergency braking market share in 2024 and is projected to maintain the highest 7.91% CAGR to 2030.

Global Automatic Emergency Braking Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory mandates for AEBS fitment in Euro NCAP and NHTSA programs | +1.8% | North America and Europe | Medium term (2-4 years) |

| Inclusion of AEB in UN-ECE R152 regulation | +1.2% | Europe and Asia-Pacific | Long term (≥ 4 years) |

| Falling radar–camera sensor cost curve | +0.9% | Global, manufacturing in Asia-Pacific | Short term (≤ 2 years) |

| Growing NCAP star-rating influence on OEM sales mix | +0.7% | Global | Medium term (2-4 years) |

| Usage-based-insurance discounts tied to AEB activation data | +0.4% | North America and Europe | Medium term (2-4 years) |

| V2X-enabled predictive braking algorithms in robo-taxis | +0.3% | Urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory mandates for AEBS fitment in Euro NCAP and NHTSA programs

Coordinated rule-making has eliminated the fragmented compliance landscape that once allowed automakers to time-shift rollouts. NHTSA’s FMVSS 127 obliges every light vehicle under 10,000 lb sold after September 2029 to avoid frontal impacts up to 62 mph and detect pedestrians up to 40 mph. Similar Euro NCAP 2026 protocols integrate more robust pedestrian tests, while China’s C-NCAP 2024 rules push AEB into mainstream models. The harmonization compresses development cycles, raises performance baselines, and keeps suppliers locked into multiyear capacity-build plans. As OEMs converge on common test matrices, the automatic emergency braking market can scale sensor-fusion architectures across global platforms without major redesigns, boosting volumes and lowering unit costs.

Inclusion of AEB in UN-ECE R152 regulation

UN-ECE R152 standardizes core functional requirements ranging from sensor redundancy to minimum deceleration curves across 50 contracting parties.[1]United Nations Economic Commission for Europe, “Regulation No. 152—Uniform provisions concerning the approval of vehicles with regard to the Advanced Emergency Braking System,” unece.orgSuppliers now design a single reference system that satisfies homologation in Europe, Asia, and parts of South America, trimming validation expense and certification lead time. Early compliance deadlines in the EU have compelled German and French OEMs to commercialize high-spec camera–radar modules two years ahead of Asian rivals, temporarily tilting competitive dynamics. The regulation’s alignment with ISO 26262 and ISO/SAE 21434 embeds functional-safety and cybersecurity provisions, forcing chipmakers and software houses to co-develop secure boot loaders and encrypted firmware pipelines. Robust global rules thus underpin the automatic emergency braking industry’s shift toward high-integrity electronic architectures.

Falling radar–camera sensor cost curve

Volume production, package miniaturization, and semiconductor localization in China and South Korea have slashed 77 GHz radar prices by close to 35% since 2022. Front-view camera modules incorporating new 3-µm pixel CMOS sensors and on-board AI accelerators now retail well below USD 50 in 50-k piece lots. The cost drop lets automakers move AEB from optional to standard equipment, raising fitment rates in compact and mid-range vehicles. Lower hardware expense also frees margin for software-defined upgrades, enabling over-the-air performance boosts long after sale. This economics pivot underlies the predicted uptick in the automatic emergency braking market size through 2030.

Growing NCAP star-rating influence on OEM sales mix

Euro NCAP, US NCAP, and China’s C-NCAP collectively cover more than 70% of global light-vehicle demand, and each program now assigns multiple star points to robust AEB capability. Dealership data show that a five-star rating can lift residual values by up to 9%, directly influencing consumer purchasing decisions. Automakers, therefore, tune algorithms for edge-case pedestrian scenarios and false-positive rejection to secure top grades. The competitive push to outperform baseline regulations raises the functional ceiling, ensuring that premium features soon trickle down to volume segments, which enlarges the automatic emergency braking market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sensor performance degradation in snow, fog, and glare | -0.8% | Northern regions, mountainous zones | Short term (≤ 2 years) |

| High total-cost-of-ownership for heavy trucks | -0.6% | Global commercial fleets | Medium term (2-4 years) |

| Cyber-attacks on brake ECUs causing functional-safety risk | -0.4% | Connected-vehicle markets | Long term (≥ 4 years) |

| Phantom braking events eroding consumer trust | -0.5% | Early-adoption markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Sensor performance degradation in snow, fog, and glare

Camera-only systems can lose object-recognition fidelity when lens temperature drops below -10 °C or when direct glare saturates image sensors. Millimeter-wave radar struggles with multi-path reflections off wet asphalt, while LiDAR faces signal-to-noise penalties in dense fog. These environmental constraints force conservative tuning that elongates minimum trigger distances, sometimes reducing crash-avoidance effectiveness by 15%. Tier-1s are testing hydrophobic coatings, lens heaters, and AI-driven fog-penetration filters, but the engineered fixes add cost and complexity. Until those upgrades become mainstream, winter markets in Canada, Scandinavia, and northern Japan will trail global average fitment, tempering overall automatic emergency braking market growth.

Phantom braking events eroding consumer trust

False-positive AEB activations remain headline risks for OEMs. Litigation against major brands in 2024–2025 highlighted sudden decelerations triggered by overhead highway signs or oncoming shadows, leading to rear-end crashes.[2]Repairer Driven News Staff, “Litigation Over Phantom Braking Spurs Scrutiny of AEB Algorithms,” repairerdrivennews.com Social-media amplification damages brand perception and slows optional-package uptake in early-adopter regions. To rebuild confidence, suppliers are refining sensor-fusion weighting strategies and integrating driver-monitoring cameras that allow predictive threshold adjustment based on driver attention state. The extra validation burden lengthens software release cycles, though continuous fleet-learning loops promise gradual mitigation of phantom-brake events.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Sensor-fusion platforms cement leadership

Radar-centric designs held a 44.32% automatic emergency braking market share in 2024, reflecting durable performance across weather conditions and low per-unit cost. The automatic emergency braking market size for radar-based modules is projected to hit USD 31.4 billion by 2030. In parallel, the LiDAR-assisted segment is predicted to log a 6.68% CAGR as solid-state beam-steering units drop below USD 300. OEM demand is pivoting toward three-sensor fusion combining radar, camera, and LiDAR inputs within centralized domain controllers-to create redundancy and raise detection reliability above 99.5% in mixed traffic.

Tier-1s such as Bosch and ZF ship integrated perception stacks that execute physics-based tracking and AI classification on single-box ECUs. Mobileye’s SuperVision anchors Level 2+ programs by blending eight cameras with front-corner radar, yielding 360-degree situational coverage. These advancements shorten emergency-brake latency to under 150 ms and open cloud-update pathways for performance tuning. As sensor-fusion economies scale, system-level costs are forecast to fall 12% between 2025 and 2028, reinforcing the segment’s dominant role.

By Vehicle Type: Commercial mandates reshape demand

Passenger cars represented a 69.13% automatic emergency braking market size in 2024, owing to high volume and early regulatory targeting. Yet electric cars will surge at a 6.82% CAGR to 2030 because regenerative braking complicates torque coordination and makes advanced AEB algorithms mandatory. Light commercial vehicles gain traction under fleet-safety policies, while heavy-duty trucks confront unit-cost barriers that slow penetration.

India’s rule requiring AEB for buses and trucks from April 2026 adds 1.5 million incremental units to annual demand. Fleets in North America and Europe tie usage-based insurance rebates to real-time AEB activation metrics, driving retrofit programs for vans and tractors. Suppliers now market modular, brake-by-wire controllers that meet both light-duty and heavy-duty hydraulic specifications, lowering engineering overhead and smoothing adoption curves.

By Operating Speed: Pedestrian focus accelerates growth

Low-speed AEB below 40 km/h accounted for a 52.87% automatic emergency braking market share in 2024, as city driving sees the highest collision frequency. Vulnerable-road-user detection modules, which cover pedestrian and cyclist scenarios, are projected to grow at an 8.57% CAGR through 2030, adding over USD 6 billion to the automatic emergency braking market size.

NHTSA now mandates pedestrian detection up to 40 mph, pushing suppliers toward higher-resolution image sensors and improved night-vision algorithms. Euro NCAP 2026 tests add crossing-child and turning-vehicle cases, raising accuracy demands under occlusion. Vendors use AI-accelerated silicon and synthetic-data training to distinguish human profiles in cluttered urban scenes. The segment expansion catalyzes investment in wide-field imaging radar, which mitigates camera blackout during glare events.

By Component: Software commands premium value

Hardware still dominates bill-of-materials cost, with sensors holding a 59.91% share of the automatic emergency braking market size in 2024. However, software and algorithms will outpace every other component at 7.46% CAGR because over-the-air upgradability lets OEMs monetize post-sale feature unlocks.

Volkswagen’s 2025 partnership with Valeo and Mobileye packages a unified perception stack and remote-update pipeline across future MQB cars.[3]Volkswagen Group, “Volkswagen, Valeo and Mobileye to Enhance Driver Assistance in Future Vehicles,” volkswagengroup.com Such architectures push compute density toward zonal gateways and migrate braking logic to central drive computers. Suppliers differentiate through closed-loop fleet-learning networks that refine braking thresholds across millions of vehicle miles, offering OEMs recurring revenue for algorithm-subscription tiers.

By Sales Channel: Aftermarket retrofit gains momentum

Factory-installed systems controlled 85.32% of 2024 shipments, yet the aftermarket retrofit segment is on track for an 8.83% CAGR as governments extend AEB mandates to existing fleets. Retrofit kits integrate forward-camera pods, radar or LiDAR units, and stand-alone ECUs that piggyback on CAN buses without re-flashing the original brake controller.

Bendix targets Class 8 trucks with a roof-mounted radar kit that ties into air-brake modulators, while Mobileye offers camera-only consumer units for cars built since 2015. Fleet operators weigh kit cost against projected liability reduction, and insurers increasingly subsidize installation. Standardized mounting brackets and pre-calibrated sensor packages are shrinking installation time below three hours, feeding volume growth.

Geography Analysis

Asia-Pacific dominated the automatic emergency braking market with a 42.30% share in 2024 and is forecast to register a 7.91% CAGR through 2030. China’s 2024 C-NCAP upgrade made AEB mandatory for 70% of models sold, driving local sensor suppliers to triple production capacity. Government incentives for electric cars, which require seamless integration between regenerative braking and emergency braking, further accelerate regional adoption. India’s commercial-vehicle mandate multiplies demand in a fleet base exceeding 5 million trucks, while Japanese and South Korean OEMs leverage mature ADAS ecosystems to meet stricter pedestrian standards.

North America trails in installed base but benefits from the definitive FMVSS 127 deadline in September 2029. The United States alone represents over 15 million annual vehicle sales; mandatory AEB fitment will add roughly 18 million cumulative units between 2026 and 2030. Canadian regulatory alignment ensures cross-border model parity, and Mexican assembly plants supply cost-competitive modules for regional OEMs. Fleet insurers in the United States already offer premium discounts up to 12% for verified AEB activation data, encouraging early adoption across rental and ride-hail operators.

Europe continues to set engineering benchmarks through Euro NCAP’s evolving star-rating tests, even as overall volume growth lags Asia. German premium brands embed redundant sensor suites to secure five-star scores, while French suppliers advance mid-range models with cost-optimized radar-camera fusion. Post-Brexit, the United Kingdom mirrors EU safety rules, keeping the supply chain integrated. Eastern Europe shows emerging growth as regional governments harmonize vehicle safety inspections with EU directives, unlocking latent automatic emergency braking market demand.

Competitive Landscape

Tier-1 suppliers such as Bosch, Continental, ZF, and Valeo anchor the competitive field, holding long-standing OEM relationships and end-to-end integration skills. Bosch leads global radar production capacity, while Continental leverages high-precision camera perception through its ASIL-D-rated domain controllers. ZF advances brake-by-wire actuators, and Valeo pairs them with LiDAR modules co-developed with Mobileye. These incumbents bundle sensor, ECU, and algorithm offerings, reducing OEM sourcing complexity.

Strategic alliances redefine the market. Volkswagen, Valeo, and Mobileye combine hardware depth with AI expertise to accelerate Level 2+ functions. Hyundai Mobis partners with domestic chipmakers to tailor radar SoCs, ensuring localized supply resilience. Semiconductor vendors such as Texas Instruments and NXP embed hardware security modules directly into ADAS microcontrollers to counter rising cyber-attack risk. Start-ups focus on software-only stacks that leverage vehicle camera feeds and cloud compute-an asset-light model poised to capture retrofit demand.

Consolidation is ongoing. Over the past 18 months, six notable acquisitions have centered on LiDAR firmware, prediction algorithms, and low-power radar front-ends. Patent filings highlight predictive braking, cross-traffic monitoring, and sensor self-diagnostics as hot spots. Given that the top five suppliers are estimated to control roughly 65% of revenue, bargaining power remains balanced: OEMs enjoy multiple qualified sources, yet second-tier suppliers struggle with capital outlays for new 10-nm radar chip fabs.

Automatic Emergency Braking Industry Leaders

Robert Bosch GmbH

Continental AG

ZF Friedrichshafen AG

DENSO Corporation

Hyundai Mobis Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Hyundai Mobis unveiled autonomous rear-end collision avoidance tailored for electric vehicles, achieving coordinated friction-regenerative brake control.

- June 2025: NHTSA finalized FMVSS 127, mandating AEB on all light vehicles by Sep 2029 with pedestrian detection up to 40 mph.

- May 2025: India’s Ministry of Road Transport confirmed ADAS mandates including AEB for ≥ 8-passenger vehicles from Apr 2026.

- April 2025: Nexteer launched brake-by-wire hardware offering sub-100 ms pressure buildup for emergency maneuvers.

Global Automatic Emergency Braking Market Report Scope

| Camera-Based |

| Radar-Based |

| LiDAR-Based |

| Sensor Fusion |

| Ultrasonic |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Trucks and Buses |

| Off-Highway and Special Vehicles |

| Low-Speed (< 40 km/h) |

| High-Speed (> 40 km/h) |

| Vulnerable-Road-User (Pedestrian/Cyclist) |

| Sensors |

| Electronic Control Units |

| Actuators |

| Software and Algorithms |

| OEM-Fitted |

| Aftermarket Retrofit |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Technology (Sensor Type) | Camera-Based | ||

| Radar-Based | |||

| LiDAR-Based | |||

| Sensor Fusion | |||

| Ultrasonic | |||

| By Vehicle Type | Passenger Cars | ||

| Light Commercial Vehicles | |||

| Heavy Trucks and Buses | |||

| Off-Highway and Special Vehicles | |||

| By Operating Speed | Low-Speed (< 40 km/h) | ||

| High-Speed (> 40 km/h) | |||

| Vulnerable-Road-User (Pedestrian/Cyclist) | |||

| By Component | Sensors | ||

| Electronic Control Units | |||

| Actuators | |||

| Software and Algorithms | |||

| By Sales Channel | OEM-Fitted | ||

| Aftermarket Retrofit | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How large is the automatic emergency braking market in 2025?

The automatic emergency braking market size reached USD 73.12 billion in 2025.

What CAGR is forecast for automatic emergency braking through 2030?

A 6.34% CAGR is projected, taking the market to USD 99.43 billion by 2030.

Why is Asia-Pacific the leading region?

Asia-Pacific leads because China mandated AEB under 2024 C-NCAP rules and India requires it for commercial vehicles from 2026, together driving the region’s 42.30% share in 2024.

Which technology segment grows fastest?

Sensor-fusion systems anchored by solid-state LiDAR are forecast to post the fastest 6.68% CAGR as falling hardware prices support broad integration.

How will U.S. regulation affect demand?

FMVSS 127 makes AEB compulsory for every light vehicle sold after September 2029, adding tens of millions of units and sharply lifting North American demand.

Does software now add more value than hardware?

Yes; software and algorithm revenue is set for a 7.46% CAGR as over-the-air updates enable continuous performance gains and new revenue streams.

Page last updated on: