Vehicle Occupancy Detection System Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

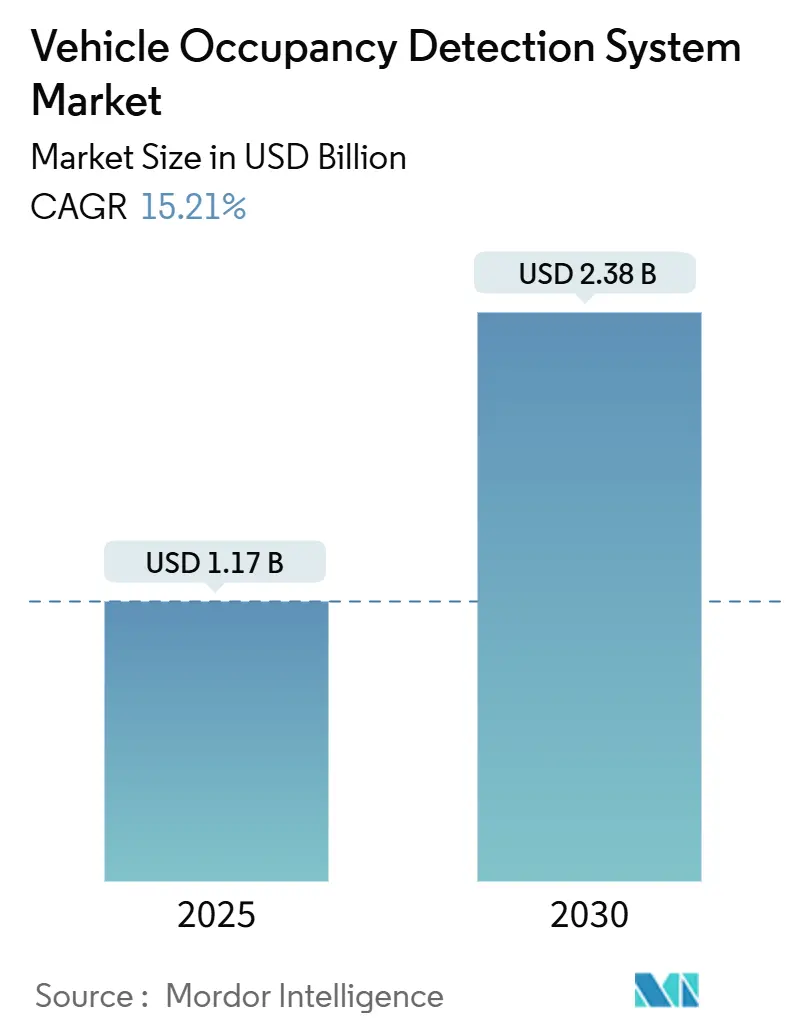

| Market Size (2025) | USD 1.17 Billion |

| Market Size (2030) | USD 2.38 Billion |

| Growth Rate (2025 - 2030) | 15.21% CAGR |

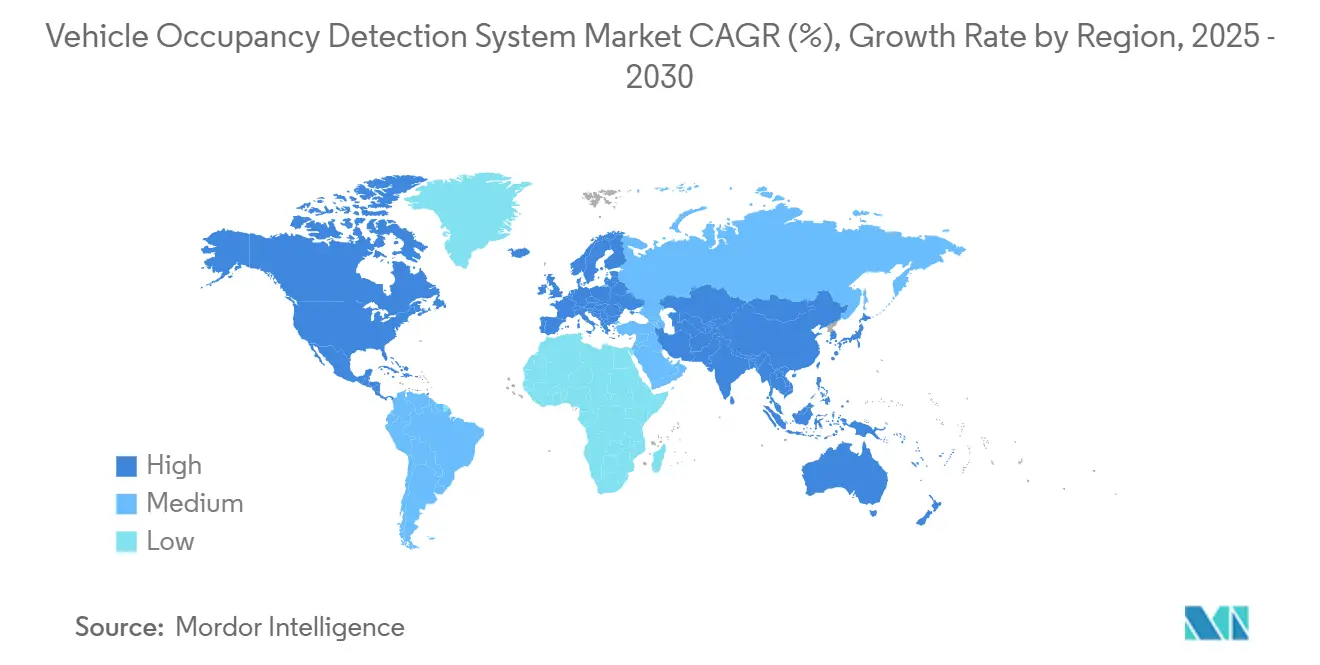

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

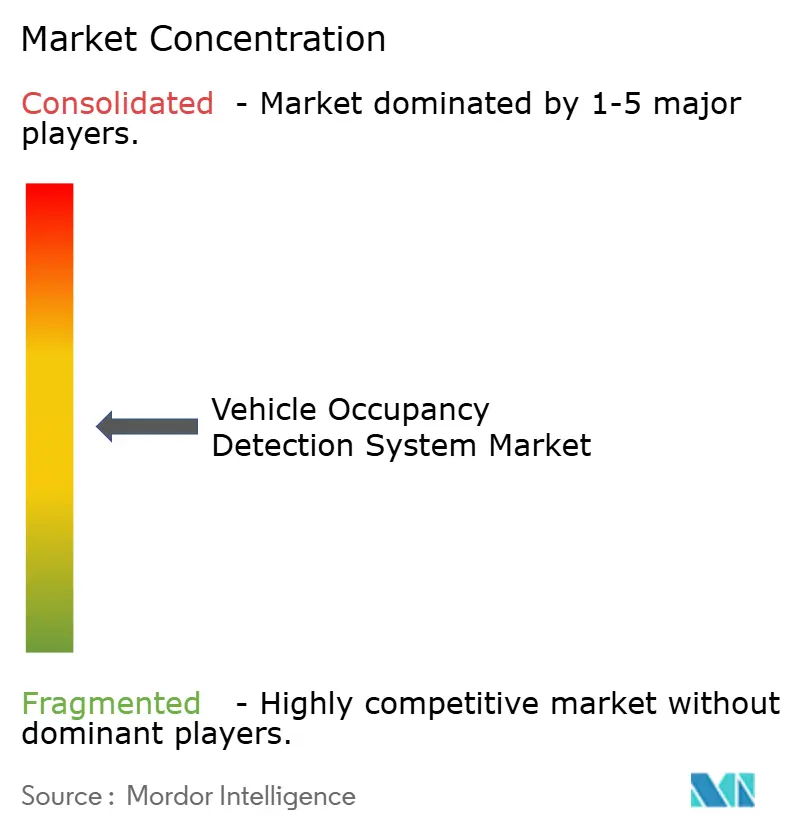

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vehicle Occupancy Detection System Market Analysis by Mordor Intelligence

The vehicle occupancy detection system market size stood at USD 1.17 billion in 2025 and is projected to reach USD 2.38 billion by 2030, advancing at a 15.21% CAGR. Strong regulatory pressure in the United States, the European Union, and China accelerates standard fitment, while artificial-intelligence-driven sensor fusion unlocks use cases that extend beyond basic seat presence alerts. Automakers are shifting toward software-defined platforms that allow over-the-air activation of safety features, effectively turning what was once a premium option into default equipment across new models. Falling radar and infrared component costs are lowering the price threshold for mid-range vehicles, and insurers are beginning to monetize occupant data through usage-based policies that reward safer family travel. These intertwined forces keep the vehicle occupancy detection system market on a steep upward trajectory despite privacy-related headwinds in several jurisdictions.

Key Report Takeaways

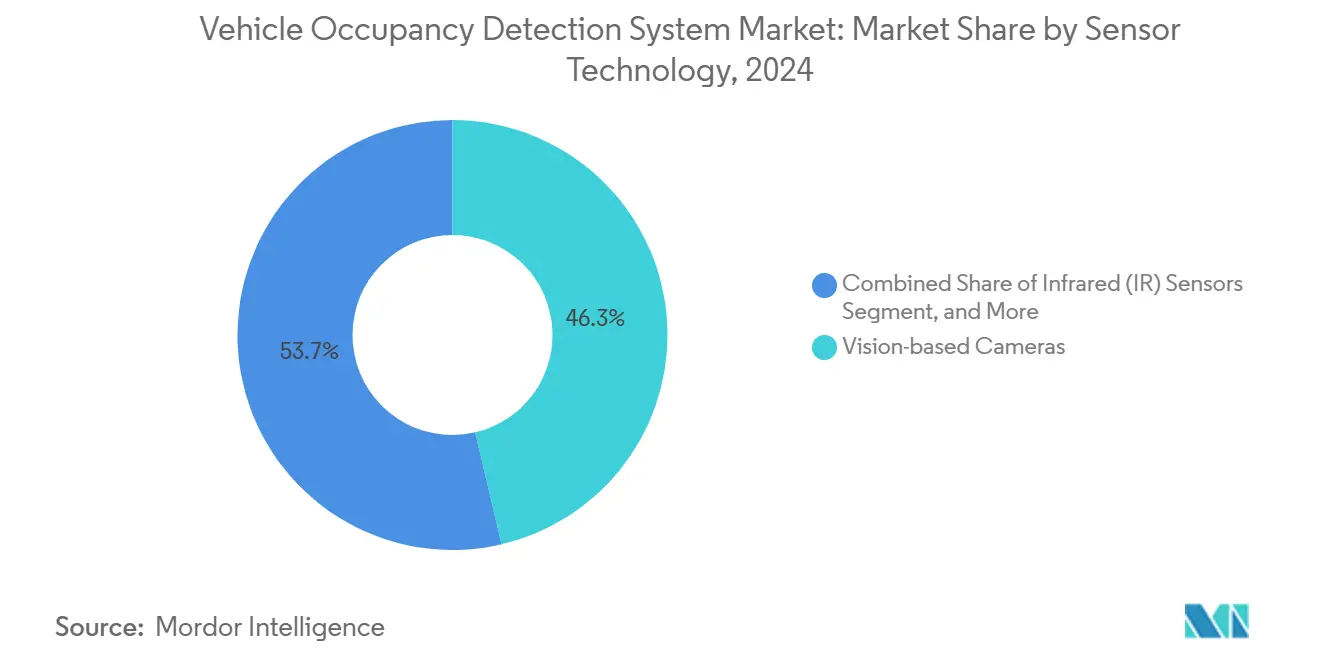

- By sensor technology, vision-based cameras led with a 46.34% revenue share in 2024, while infrared sensors are forecast to grow at an 18.54% CAGR through 2030.

- By vehicle type, passenger cars accounted for 65.53% of the vehicle occupancy detection system market share in 2024, and they remain the fastest-expanding category at a 17.46% CAGR to 2030.

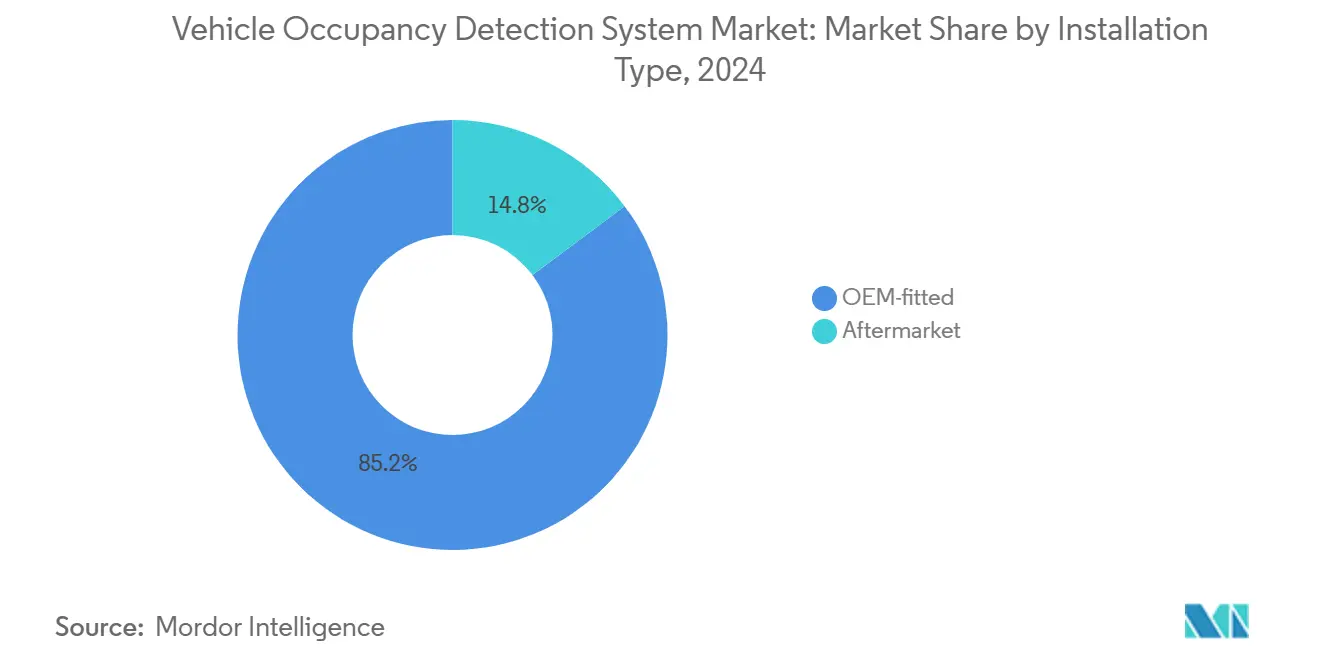

- By installation type, OEM-fitted systems dominated with 85.23% share in 2024; this channel is projected to advance at a 16.43% CAGR over the forecast period.

- By detection mode, seat occupancy remained the largest at 54.21% in 2024, whereas comprehensive cabin-presence solutions are poised for the quickest climb at a 16.88% CAGR to 2030.

- By geography, Asia-Pacific captured 40.12% share in 2024 and is projected to post the highest 18.96% CAGR through 2030, fueled by China NCAP’s 2024 driver-monitoring mandate.

Global Vehicle Occupancy Detection System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-powered multi-modal sensor fusion improves detection accuracy | +2.8% | Global with early adoption in North America and EU | Medium term (2-4 years) |

| Mandated rear-seat occupancy alerts in U.S. and EU regulations | +3.2% | North America and EU; expanding to Asia-Pacific | Short term (≤ 2 years) |

| Insurance telematics discount programs linked to occupancy data | +1.4% | North America core; spreading to EU and Asia-Pacific | Medium term (2-4 years) |

| Surge in robotaxi R&D requiring real-time cabin analytics | +2.1% | Asia-Pacific core; spill-over to North America | Long term (≥ 4 years) |

| Cost decline in 60 GHz radar chipsets | +1.8% | Global | Short term (≤ 2 years) |

| OEM shift to software-defined vehicles enabling OTA activation | +2.3% | Global; early gains in North America, EU, China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

AI-powered multi-modal sensor fusion improves detection accuracy

Machine-learning algorithms that blend camera, radar, and infrared inputs now reach over 95% detection accuracy in real-time cabin assessments. Fusing complementary signals slashes false-positives by 40% compared with vision-only configurations, especially in low-light or high-glare situations. Automakers use these robust data streams to tailor airbag deployment, adaptive HVAC, and smart-restraint logic around each occupant’s position and size. Continuous over-the-air model re-training allows region-specific optimization without hardware refresh, ensuring performance remains high across varied demographic profiles. The resulting gains in reliability underpin regulatory acceptance and reinforce consumer trust, propelling the vehicle occupancy detection system market forward.

Mandated rear-seat occupancy alerts in U.S. and EU regulations

NHTSA’s December 2024 final rule compels every light vehicle sold after September 2027 to include rear-seat occupancy detection, instantly expanding the addressable U.S. fleet by millions of units per year. [1]National Highway Traffic Safety Administration, “Final Rule Seat Belt Use Warning System for Rear Seats,” nhtsa.gov Parallel EU measures that took effect in July 2024 link five-star Euro NCAP ratings to sophisticated occupant-monitoring performance. [2]European Commission, “Mandatory Drivers Assistance Systems Expected to Help Save Over 25,000 Lives by 2038,” ec.europa.eu These synchronized policies compress OEM development timelines and make compliance non-negotiable, triggering bulk orders for sensor suites and embedded AI processors. The regulation-driven surge strengthens the vehicle occupancy detection system market even during cyclical downturns in overall vehicle sales.

Insurance telematics discount programs linked to occupancy data

Programs such as AAA OnBoard now integrate live occupancy feeds with driving-behavior metrics to shape individualized premiums, offering discounts up to 30% for families that demonstrate safe habits. Occupancy context clarifies risk profiles by distinguishing high-risk solo night drives from routine school runs, thereby enhancing actuarial accuracy. Automakers profit by licensing anonymized datasets to insurers, opening recurring revenue beyond initial hardware sales. The feedback loop encourages wider adoption, adding a financial incentive atop safety and compliance motivations that already sustain the vehicle occupancy detection system market.

Surge in robotaxi R&D requiring real-time cabin analytics

As Level 4 and Level 5 pilots proliferate, fleet developers demand non-intrusive yet comprehensive solutions capable of spotting medical emergencies, vandalism, or abandoned property without a driver present. Toyota’s 2025 Sienna radar implementation illustrates how incumbent OEMs adapt child-presence logic for autonomous contexts. Real-time cabin analytics also feed utilization algorithms that maximize earnings per mile through dynamic dispatch. These new functional layers widen market boundaries beyond conventional passenger vehicles into shared-mobility fleets, strengthening long-run demand for vehicle occupancy detection system market solutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy compliance costs (GDPR, CPRA) | -1.6% | EU and California core; expanding globally | Short term (≤ 2 years) |

| High false-positive rates in vision-only systems under low light | -1.2% | Global | Medium term (2-4 years) |

| Limited standardization across regional safety bodies | -0.8% | Global with regional variations | Long term (≥ 4 years) |

| Customer reluctance due to in-cabin camera concerns | -1.4% | North America and EU primarily | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-privacy compliance costs (GDPR, CPRA)

Honda’s USD 632,500 California settlement in March 2025 underscores the rising legal exposure tied to connected-vehicle data collection. [3]California Privacy Protection Agency, “Honda Settles With CPPA Over Privacy Violations,” cppa.ca.gov To satisfy GDPR’s data-minimization clause, many OEMs now restructure algorithms so raw imagery never leaves the edge device, pushing up development budgets and silicon requirements. Ongoing audits and double-opt-in consent flows add operational overhead that erodes near-term margins. Such complexities temporarily temper rollout velocity yet ultimately favor vendors capable of delivering privacy-by-design architectures, reshaping competitive dynamics inside the vehicle occupancy detection system market.

High false-positive rates in vision-only systems under low light

Camera-exclusive solutions still struggle with blur, low signal-to-noise ratios, and LED flicker when ambient illumination dips below 5 lux. False alerts undermine driver trust and can even disable safety functions. OEMs respond by adding infrared or radar layers, which raises hardware cost and lengthens validation cycles. These engineering detours delay deployments but also amplify long-term demand for hybrid stacks, reinforcing the strategic shift toward multi-modal sensor fusion within the vehicle occupancy detection system market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sensor Technology: Multi-modal integration unlocks scale

Vision-based cameras commanded 46.34% of the vehicle occupancy detection system market size in 2024, cementing their role as the baseline sensor for occupant recognition. Infrared devices, however, outpace overall growth, charting an 18.54% CAGR as OEMs seek privacy-preserving detection under low-light or covered-face conditions. Industry collaboration between image-sensor suppliers and processor vendors reduces latency so alerts trigger under 300 milliseconds, meeting Euro NCAP recommendations. Cost-down roadmaps for 60 GHz radar and the launch of single-package RGB-IR chips further validate the multi-sensor route and expand addressable trim lines inside the vehicle occupancy detection system market.

AI-optimized sensor gateways now permit on-chip fusion, eliminating the need for discrete domain controllers and trimming wiring weight by up to 2 kilograms per vehicle. Vehicle-secure operating systems push detection results onto CAN-FD or Ethernet-AVB backbones for use in adaptive airbag or ride-share billing modules. These developments transform occupant sensing from a standalone peripheral into a core node within the software-defined architecture that powers the broader vehicle occupancy detection system market.

By Vehicle Type: Passenger cars dominate, robotaxis soar

Passenger cars captured 65.53% of vehicle occupancy detection system market share in 2024 thanks to family-safety priorities and imminent U.S. compliance deadlines. Compact SUVs in particular exhibit high installation rates because their flat rooflines simplify camera placement. Light commercial vans follow, propelled by fleet insurers that offer lower premiums if smart-cabin functionality is active. Heavy trucks lean on driver-fatigue modules that repurpose occupancy cameras, but stricter hours-of-service audits could lift adoption toward the decade’s end.

Autonomous shuttles, though currently niche, log the highest growth slope as Level 4 pilots convert simulation learnings into fleet orders. In unmanned vehicles, detection algorithms must recognize obstructed passengers, unattended pets, and even contraband, triggering tiered response protocols. These advanced requirements ensure multi-modal stacks remain non-negotiable, extending the customer base and revenue potential of the vehicle occupancy detection system market.

By Installation Type: OEM fitment is default

Factory-installed solutions accounted for 85.23% of the vehicle occupancy detection system market size in 2024 and will expand at 16.43% CAGR because only OEM channels can meet functional-safety (ASIL-B or above) calibration demands. Automakers embed occupancy classifiers within restraint ECU firmware to control multi-stage airbags, making post-sale retrofits infeasible. Over-the-air unlocking models, however, introduce new monetization layers by letting consumers subscribe to Child-Presence Detection Plus or biometric ID packages whenever they choose.

Aftermarket kits focus on fleet dashboards that visualize seat-belt compliance or passenger counts to optimize route planning. Yet legal barriers against modifying certified restraint systems restrict aftermarket penetration, reinforcing OEM supremacy and sustaining volume growth for the vehicle occupancy detection system market.

By Detection Mode: From seats to full-cabin intelligence

Seat-specific weight and pressure mats still delivered 54.21% revenue in 2024, but cabin-wide presence analytics are rising at a 16.88% CAGR as regulations expand beyond simple binary status. Next-generation sensors classify occupants by age, posture, and gaze direction, feeding adaptive restraint algorithms. Biometrics such as iris-or face-print enable secure payment authorization, turning the cabin into a multifactor authentication zone.

The wider data set exposes secondary revenue vectors—media personalization, ride-share fraud alerts, or in-vehicle commerce—that lift ROI for OEMs and encourage higher option-take rates. Together, these dynamics reinforce the technology roadmap for comprehensive systems, ensuring sustained expansion of the vehicle occupancy detection system market.

Geography Analysis

Asia-Pacific held 40.12% of the vehicle occupancy detection system market in 2024 and is projected to log an 18.96% CAGR through 2030 as China’s NCAP criteria extend occupant-monitoring coverage to every mainstream segment. Domestic suppliers, backed by policy incentives, ramp volume production of CMOS-IR hybrids to serve local brands, while multinationals localize ECU software to comply with data-export restrictions. Japanese regulation now classifies occupancy detectors as serviceable electronic-control devices, boosting aftermarket inspection demand and creating a pull-through effect on spare-parts sales.

North America ranks second, driven by federal mandates and a mature insurance ecosystem that values telematics-enriched underwriting. U.S. automakers quickly expand camera-radar combos into entry-level trims to meet the 2027 rear-seat reminder deadline, increasing factory throughput. Canadian assembly plants follow identical specifications to preserve cross-border homologation, while Mexican facilities leverage new sensor-pack sourcing deals to remain cost-competitive. These integrated supply chains give the region scale, strengthening its contribution to the vehicle occupancy detection system market.

Europe shows steady gains as advanced-driver-assistance rules entered force in 2024, binding five-star safety ratings to occupant-monitoring excellence. Germany’s premium brands accelerate multi-sensor adoption, whereas smaller volume automakers rely on turnkey modules from Tier-1s to hit compliance targets. GDPR complexities stimulate local edge-processing innovation, and several start-ups now offer encrypted-memory radar chips to tap this niche. Collectively, these forces guarantee Europe a firm 25%-plus revenue slice of the global vehicle occupancy detection system market by mid-decade.

Competitive Landscape

The vehicle occupancy detection system market displays moderate concentration as the top five Tier-1 suppliers aggregate roughly 62% of 2024 sales value. Bosch deepens its generative-AI partnership with Microsoft to compress algorithm-training cycles and deliver turnkey perception stacks. Continental expands aftermarket lines, offering plug-and-play radar units that integrate via CAN into existing seat-belt warning modules. ZF merges its chassis and active-safety divisions, leveraging brake-by-wire orders to cross-sell in-cabin sensing packages.

Component specialists sharpen differentiation through sensor innovation: OMNIVISION’s RGB-IR global-shutter chip cuts part count by 30%, while Infineon’s 60 GHz radar MMIC drives down cost for entry-segment trims. Software-first players such as Smart Eye and Aptiv promote cloud-trained classifiers that adapt to new geopolitical privacy laws via over-the-air patches. Patent activity remains brisk; Tesla’s mixed weight-presence algorithm filing hints at fresh logic to improve small-child identification without camera input. Taken together, these moves reveal a race to own the fusion layer that will decide long-term leadership inside the vehicle occupancy detection system market.

Vehicle Occupancy Detection System Industry Leaders

Bosch GmbH

Continental AG

Denso Corporation

ZF Friedrichshafen AG

Aptiv Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: FORVIA and Smart Eye unveiled an iris-and-facial biometric authentication module that leverages existing driver-monitoring cameras to authorize in-car purchases.

- March 2025: California Privacy Protection Agency fined Honda USD 632,500 for connected-car data-privacy violations, highlighting regulatory scrutiny over occupant-data pipelines.

- January 2025: Aalto University introduced a more responsive 1.55 µm infrared photodiode that boosts automotive IR detection by 35%.

- December 2024: NHTSA issued its final seat-belt reminder rule mandating rear-seat occupancy alerts by Sep 2027.

Global Vehicle Occupancy Detection System Market Report Scope

| Vision-based Cameras |

| Ultrasonic Sensors |

| Millimetre-wave Radar (24/60 GHz) |

| Pressure and Weight Sensors |

| Infrared (IR) Sensors |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

| Robo-taxis and Autonomous Shuttles |

| OEM-fitted |

| Aftermarket |

| Seat Occupancy Detection |

| Cabin Occupancy / Presence Detection |

| Child Left-Behind Detection |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Sensor Technology | Vision-based Cameras | ||

| Ultrasonic Sensors | |||

| Millimetre-wave Radar (24/60 GHz) | |||

| Pressure and Weight Sensors | |||

| Infrared (IR) Sensors | |||

| By Vehicle Type | Passenger Cars | ||

| Light Commercial Vehicles | |||

| Heavy Commercial Vehicles | |||

| Robo-taxis and Autonomous Shuttles | |||

| By Installation Type | OEM-fitted | ||

| Aftermarket | |||

| By Detection Mode | Seat Occupancy Detection | ||

| Cabin Occupancy / Presence Detection | |||

| Child Left-Behind Detection | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Netherlands | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How large is the vehicle occupancy detection system market in 2025?

The vehicle occupancy detection system market size reached USD 1.17 billion in 2025 and is on track to hit USD 2.38 billion by 2030.

What regulations are driving rapid adoption?

NHTSA’s rear-seat reminder mandate effective September 2027 and the EU’s July 2024 advanced-driver-assistance requirements compel standard integration in new vehicles.

Which sensor type is growing fastest?

Infrared sensors are expanding at an 18.54% CAGR because they perform well in low-light and protect passenger privacy.

Why is Asia-Pacific leading the market?

China’s 2024 NCAP update and Japan’s new maintenance rules create large-scale compliance demand, giving Asia-Pacific a 40.12% share and the highest regional growth rate.

How are insurers using occupancy data?

Programs like AAA OnBoard blend occupant information with driving metrics to refine risk scoring and deliver premium discounts up to 30%.

Can aftermarket kits be installed easily?

Aftermarket solutions exist but remain limited to non-safety fleet analytics because regulatory rules often forbid modifying factory-calibrated restraint systems.

Page last updated on: