Market Overview

| Study Period | 2020 - 2031 |

|---|---|

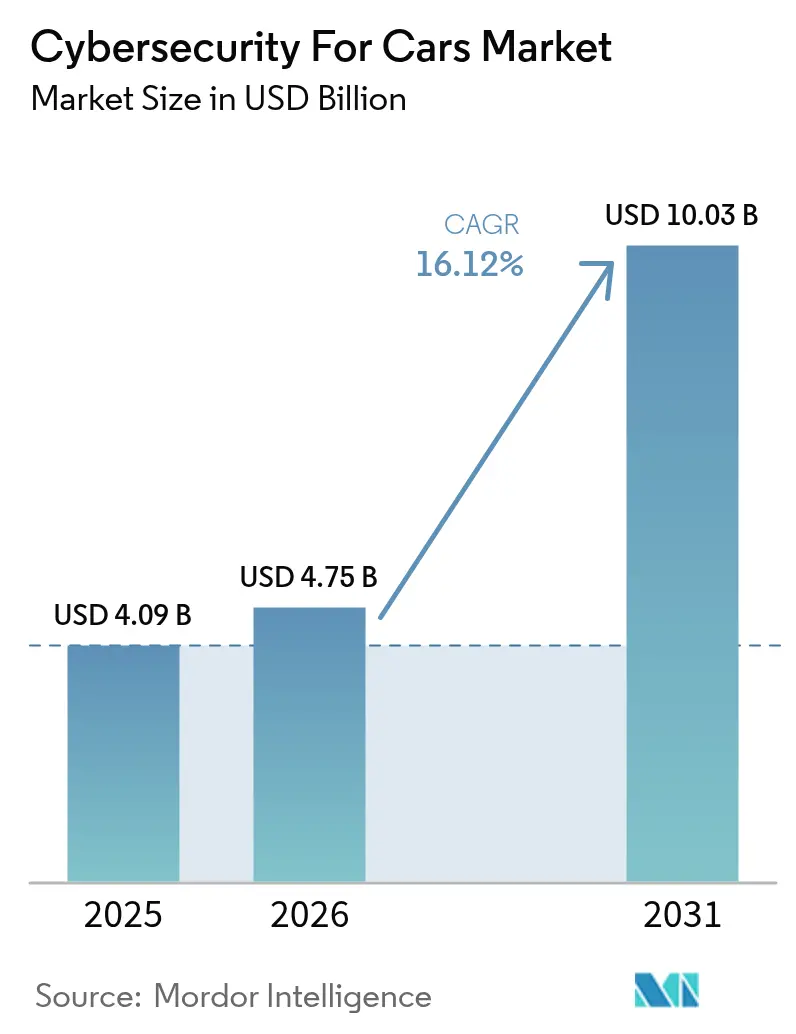

| Market Size (2026) | USD 4.75 Billion |

| Market Size (2031) | USD 10.03 Billion |

| Growth Rate (2026 - 2031) | 16.12% CAGR |

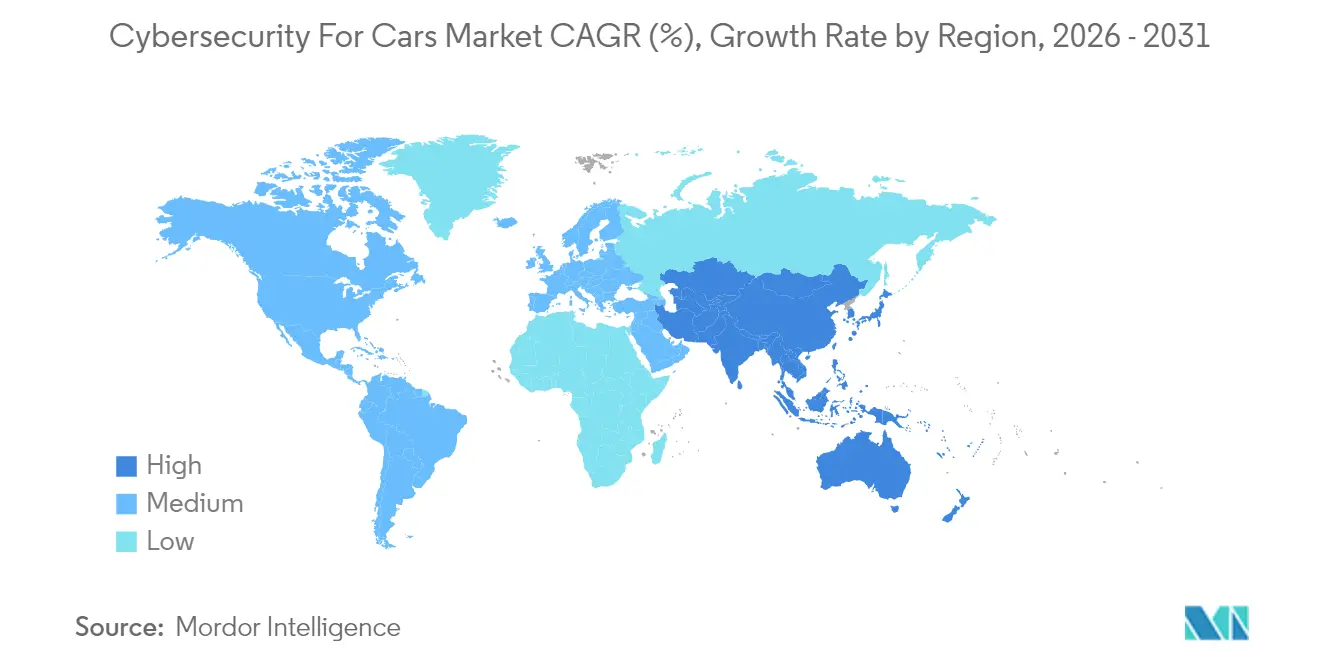

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cybersecurity For Cars Market Analysis by Mordor Intelligence

Cybersecurity For Cars Market size in 2026 is estimated at USD 4.75 billion, growing from 2025 value of USD 4.09 billion with 2031 projections showing USD 10.03 billion, growing at 16.12% CAGR over 2026-2031. Rapid vehicle digitalization, growing regulatory scrutiny, and wider 5G/V2X roll-outs are reshaping competitive strategies and opening new service-led revenue pools. Manufacturers race to certify Cybersecurity Management Systems before UNECE R155/R156 audits, while cloud-native security platforms gain traction as software-defined vehicles demand continuous protection. Simultaneously, electric-vehicle adoption, bidirectional charging, and sensor-rich ADAS features multiply the attack surface, attracting specialized solution vendors that promise real-time threat intelligence and automated response. OEMs also eye monetization of over-the-air security updates and usage-based insurance programs that reward certified cyber-hardening, partially offsetting high integration costs.

Key Report Takeaways

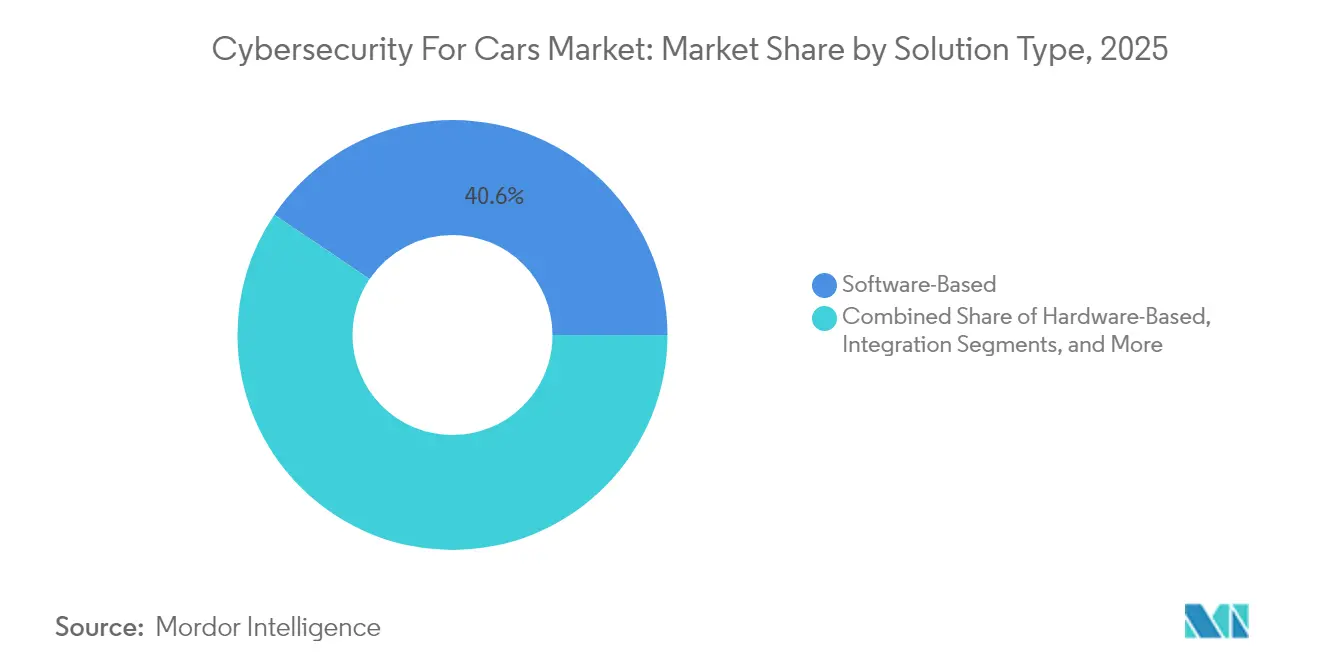

- By solution type, software-based offerings led with 40.55% revenue share in 2025, while professional services are forecast to register the fastest 19.1% CAGR to 2031.

- By security type, endpoint security accounted for 29.62% of the cybersecurity for cars market share in 2025, whereas cloud security is projected to climb at 20.6% CAGR through 2031.

- By vehicle type, passenger cars represented 56.48% of demand in 2025; the cybersecurity for cars market size for electric vehicles is set to expand at 21% CAGR between 2026-2031.

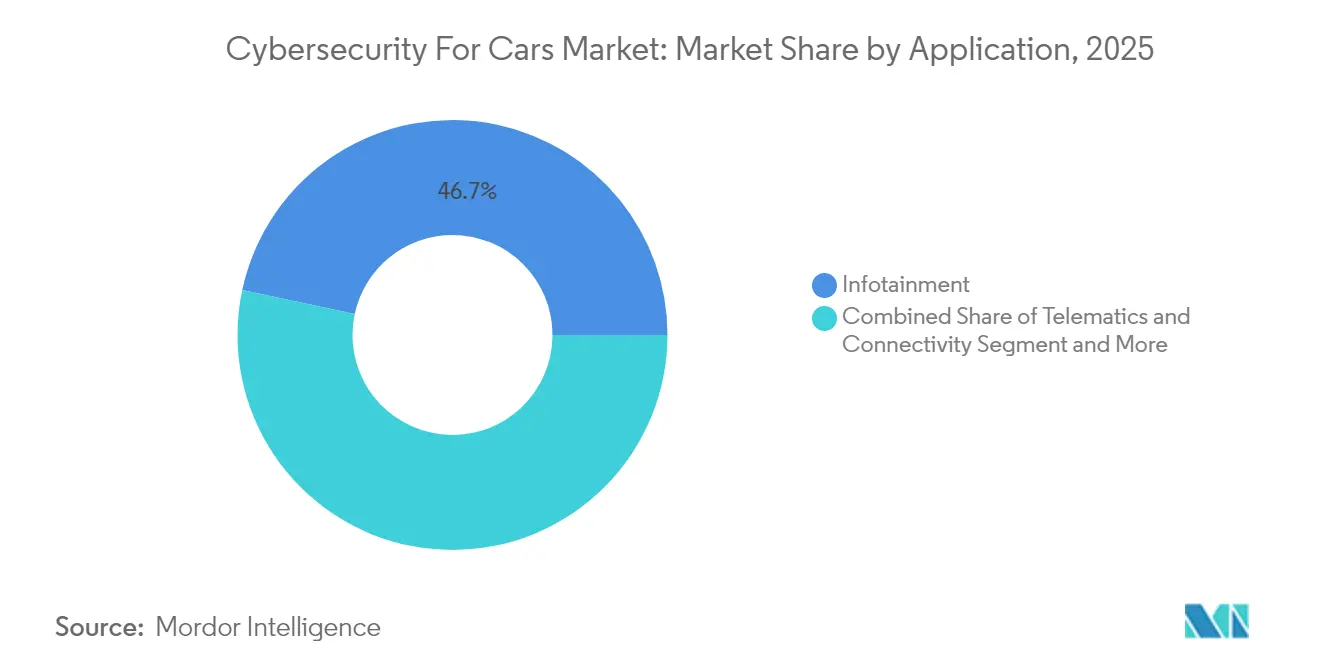

- By application, infotainment systems captured 46.65% of the cybersecurity for cars market size in 2025, while ADAS and safety applications are expected to grow at a 20.9% CAGR through 2031.

- By form type, in-vehicle embedded solutions dominated with 57.41% revenue share in 2025, and external cloud services are projected to post the highest 22.9% CAGR to 2031.

- By geography, Asia-Pacific led with 35.12% revenue share in 2025 and is anticipated to register the fastest 19.5% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cybersecurity For Cars Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory mandates (UNECE R155/R156, ISO 21434) compliance wave | +4.2% | Global; early adoption in EU and Japan | Medium term (2-4 years) |

| Rapid growth in connected-vehicle fleet and 5G/V2X roll-outs | +3.8% | APAC core; spill-over to North America and EU | Short term (≤ 2 years) |

| ADAS/autonomous feature proliferation elevating cyber-risk | +3.1% | North America and EU leading; APAC following | Medium term (2-4 years) |

| Vehicle-to-Grid (V2G) bidirectional charging | +2.4% | EU and California early markets; expanding globally | Long term (≥ 4 years) |

| Usage-based-insurance discounts for certified cyber-hardening | +1.8% | North America and EU mature insurance markets | Medium term (2-4 years) |

| OEM monetization of OTA security updates | +1.3% | Global; premium segments first | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory mandates drive fundamental change

Global homologation now hinges on demonstrating end-to-end security. UNECE R155 alone creates a USD 2.1 billion compliance opportunity by 2030 as OEMs must track 69 attack vectors and prove continuous monitoring throughout vehicle lifecycles. [1]VicOne, “UN R155,” vicone.com ISO/SAE 21434 hardcodes cybersecurity engineering into concept and decommission phases, prompting carmakers to expand specialist teams. Similar rules emerge in Japan and the United States, eliminating first-mover disadvantages and standardizing baselines worldwide.

Connected-vehicle fleet expansion multiplies attack surfaces

Modern cars host up to 150 ECUs and 100 million lines of code—volumes that could triple by 2030, stressing legacy defenses. Backend servers already account for 43% of incidents, and 95% of attacks originate remotely. [2]Automotive IQ, “UNECE R155/R156 Compliance,” automotive-iq.com 5G-based V2X exchanges add high-bandwidth vectors exposing telematics gateways, while ransomware targeting dealership IT highlights supply-chain vulnerabilities beyond the vehicle perimeter.

ADAS proliferation elevates safety-critical risks

AI-driven perception stacks introduce adversarial-learning weaknesses that may misread traffic signs, with researchers cataloging 115 threats in driver monitoring alone. Sensor spoofing against radar and ultrasonic modules underscores the need for multi-layered protection spanning silicon, middleware, and cloud analytics, spurring demand for specialized runtime intrusion detection.

Vehicle-to-Grid integration creates bidirectional pathways

Only 12% of CCS chargers currently support TLS, leaving most deployments open to man-in-the-middle exploits. Vulnerabilities such as CVE-2024-37310 inside open-source charging firmware expose entire EV fleets and potentially the grid. Regulators and utilities now view automotive security as a critical infrastructure risk.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High integration cost and legacy E/E architectures | -2.8% | Global; established OEMs most affected | Short term (≤ 2 years) |

| Fragmented standards and certification overload | -1.9% | Global; regional variations | Medium term (2-4 years) |

| Acute shortage of automotive-grade cyber-talent | -2.1% | North America and EU | Medium term (2-4 years) |

| Post-warranty liability for long-life vehicles | -1.4% | Global; regulatory uncertainty | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy architecture integration costs constrain adoption

Retrofitting 150-plus ECUs in legacy platforms can add 15-20% to vehicle development budgets. Continental’s 2022 breach illustrated supplier-network exposure and forced expensive architecture reviews. Such financial drag delays roll-outs among volume brands, even as compliance deadlines loom.

Automotive cybersecurity talent shortage limits execution

Roles demand deep knowledge of CAN, FlexRay, ISO 26262, and real-time constraints that few traditional IT security professionals possess. Smaller suppliers struggle to match salary offers from tech firms, widening the skills gap just as demand spikes. Investments like BMW i Ventures’ USD 12 million in RunSafe Security reflect efforts to backfill capabilities across the supply chain.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Professional services outpace as compliance complexities surge

Software-based platforms held 40.55% of 2025 revenue, underscoring their centrality in a software-defined vehicle era where embedded firewalls, secure firmware, and runtime intrusion detection converge. Consulting-led offerings, however, are on a 19.1% CAGR ascent as OEMs outsource gap analyses, threat modeling, and audit preparation to specialist advisors. The cybersecurity for cars market increasingly rewards vendors capable of bundling continuous monitoring with UNECE R155 documentation support, a capability visible in HARMAN’s end-to-end WP.29 packages.

Professional services also orchestrate multi-vendor integration when hardware security modules, PKI suites, and cloud SOC platforms must interoperate inside tight development timelines. Such cross-domain coordination positions service providers as primary gatekeepers of compliance roadmaps, shifting revenue toward recurring assessment and managed-detection contracts. Consequently, the cybersecurity for cars market is witnessing alliances where software licensors embed service retainer clauses to secure lifetime margins.

By Security Type: Cloud security accelerates while endpoint remains essential

Endpoint controls retained a 29.62% share in 2025 because cryptographic keys, secure boot, and ECU-level firewalls remain foundational. Yet cloud defenses are racing ahead at 20.6% CAGR as automakers shift data lakes, OTA orchestration, and fleet analytics off-board. The cybersecurity for cars market size for cloud protection is swelling each quarter, buoyed by collaborations such as Upstream’s tie-up with Google Cloud. Incident lessons from the 2024 Volkswagen data breach showed that insufficient encryption of telemetry can cascade into reputational damage.

Network-layer segmentation and TLS v1.3 upgrades ride parallel with cloud growth, while application-centric hardening becomes imperative as vehicles download microservices weekly. Wireless security remains the final mile, guarding 5G links that now underpin platooning and V2I signalling. As virtual ECUs offload tasks to the edge, hybrid architectures combining in-vehicle enforcement with remote AI-assisted analytics form the emerging blueprint across the cybersecurity for cars market.

By Vehicle Type: Electric-vehicle focus intensifies protective spend

Passenger cars still anchor revenue, accounting for 56.48% of demand in 2025, yet electric vehicles represent the fastest-growing slice at 21% CAGR. Their dependence on battery management systems, high-voltage controllers, and V2G interfaces expands both threat vectors and regulatory scrutiny, enlarging the cybersecurity for cars market size earmarked for EV protection. Studies revealing low TLS adoption among public chargers and disclosures such as CVE-2024-37310 have sharpened OEM and utility focus on end-to-end encryption, firmware signing, and anomaly scoring.

Commercial fleets increasingly procure telematics with built-in intrusion-prevention to avoid cargo disruptions, while heavy trucks integrate secure gateways that isolate safety-critical brake controllers from infotainment head-units. These differing risk profiles sustain multi-tier demand, ensuring the cybersecurity for cars market continues to fragment by propulsion type and duty cycle.

By Application: ADAS and safety spend gains momentum

Infotainment held the largest slice at 46.65% in 2025 because audio-video domains remain an easy phishing and ransomware target. However, security outlays around ADAS and safety systems are rising at 20.9% CAGR as lidar fusion, automated lane-keep, and driver monitoring migrate into higher SAE automation levels. This pivot moves the cybersecurity for cars market share toward functions that can physically endanger occupants if compromised. The STRIDE-mapped catalogue of 115 threats against driver monitoring systems underscores the urgency.

Telematics remains the connective tissue between vehicle and cloud, making secure MQTT brokering and certificate rotation key purchase criteria. Powertrain controllers, once isolated, now expose APIs for regenerative-braking updates, demanding signed firmware and runtime integrity checks. Charging infrastructure security rounds out the stack, especially in regions deploying bidirectional energy services.

By Form Type: External cloud services reshape architectures

In-vehicle embedded solutions stayed dominant with a 57.41% share in 2025, driven by real-time needs such as secure boot and cryptographic seed-key routines. Yet, external cloud services exhibit a 22.9% CAGR as automakers centralize threat intelligence, vulnerability scanning, and fleetwide policy management. Upstream’s Ocean AI illustrates how aggregated telemetry enables machine-learning models that predict and neutralize complex, multi-vehicle attacks. The cybersecurity for cars market thus evolves toward a dual-plane model: embedded enforcement for milliseconds-level reactions, and cloud orchestration for situational awareness and over-the-air patching.

Microsoft’s integration of VicOne threat feeds into GitHub workflows shows dev-sec-ops convergence, tightening feedback loops between software releases and field monitoring. As continuous delivery culture takes hold, cloud-native SOCs become indispensable to maintain compliance and performance metrics.

Geography Analysis

Asia-Pacific commanded 35.12% revenue in 2025 and is projected to grow at 19.5% CAGR, making it the fastest-advancing geography within the cybersecurity for cars market. China’s scaling of connected-EV production fuels large-scale procurement of V2G-ready PKI and ECU hardening suites, while Japan’s early alignment with UNECE rules accelerates supplier certification programs. South Korea’s 5G highways amplify demand for real-time over-the-air patching technologies, and India’s emergent export ambitions trigger investments in ISO 21434 compliance tooling. Collectively, these dynamics push regional vendors to deliver low-latency cloud SOC services hosted within data-residency-compliant zones.

North America represents a mature yet evolving arena where premium vehicle trims and robust insurance ecosystems encourage cybersecurity monetization. The United States Connected Vehicles Rule, effective March 2025, forces OEMs to audit supply chains for sanctioned components, redirecting procurement toward domestic chipsets and security modules. Canada’s tier-one suppliers leverage proximity and regulatory alignment to integrate secure Ethernet backbones, while Mexico’s assembly plants adopt managed-security services to counter rising ransomware aimed at just-in-time logistics. Europe remains a regulatory trendsetter and R&D hub. Germany hosts flagship suppliers such as Bosch ETAS and Continental, although the latter’s prior breach highlighted vulnerabilities in centralized architecture. France and the United Kingdom channel public grants into quantum-safe automotive cryptography, while the ENX VCS audit framework overlays ISO 21434 to standardize supplier assessments. Eastern European engineering hubs contribute competitive talent, though war-related cyber sanctions reshape sourcing strategies.

Competitive Landscape

The cybersecurity for cars market features moderate fragmentation where established tier-one suppliers intersect with security pure-plays. Continental, Bosch ETAS, DENSO, and NXP leverage deep vehicle integration to embed hardware-root-of-trust and secure gateway offerings. Upstream, VicOne, and Argus supply AI-driven SOC platforms and threat intelligence that complement in-vehicle defenses, enabling OEMs to monitor fleets in real time. Semiconductor leaders Infineon and Renesas bundle secure microcontrollers with automotive Ethernet switch silicon, targeting domain controller architectures.

Strategic partnerships define go-to-market execution. Infineon’s USD 2.5 billion acquisition of Marvell’s Automotive Ethernet business broadens its portfolio into high-bandwidth networking essential for ADAS domain controls. [5]Infineon Technologies, “Infineon Further Strengthens Its Number One Position in Automotive Microcontrollers,” infineon.com VicOne’s integration with Microsoft’s developer tools accelerates secure-coding adoption, tightening the loop between design and field feedback. Upstream’s Ocean AI brings automated root-cause investigation, lowering SOC response times. Meanwhile, automakers invest directly: BMW i Ventures’ stake in RunSafe Security secures software immunization IP across its supply base. Competitive intensity is expected to rise as quantum-resistant cryptography and AI-generated code defense emerge as next battlegrounds.

Cybersecurity For Cars Industry Leaders

Continental AG

Harman International

Bosch ETAS GmbH

Infineon Technologies AG

NXP Semiconductors NV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Infineon Technologies closed the USD 2.5 billion acquisition of Marvell’s Automotive Ethernet unit to fuse high-bandwidth networking with secure microcontrollers.

- March 2025: The United States Connected Vehicles Rule took effect, restricting Chinese and Russian components and mandating supply-chain disclosure filings.

- February 2025: VicOne and Microsoft integrated automotive threat intelligence into GitHub Advanced Security, expanding secure-by-design tooling.

- February 2025: Upstream Security launched Ocean AI to automate multi-vehicle attack investigation and mitigation.

- January 2025: Infineon created the SURF business unit to consolidate sensor and RF development for secure ADAS applications.

- December 2024: Upstream partnered with Google Cloud to scale global automotive SOC services.

- September 2024: BMW i Ventures invested USD 12 million in RunSafe Security to harden supply-chain software.

- September 2024: Toyota Tsusho joined forces with Keyfactor to deploy global PKI services for connected vehicles.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the car cybersecurity market as all hardware, software, and managed services that prevent, detect, and respond to unauthorized digital access or manipulation of on-road passenger and light commercial vehicles, including over-the-air update infrastructure and V2X communication links.

Scope Exclusion: After-sales antivirus apps for personal mobile devices and broader enterprise cyber tools that never interface with in-vehicle networks sit outside this assessment.

Segmentation Overview

- By Solution Type

- Software-Based

- Hardware-Based

- Professional Services

- Integration

- Other Solutions

- By Security Type

- Network Security

- Application Security

- Cloud Security

- Endpoint Security

- Wireless Security

- By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- Electric Vehicles (BEV/HEV/PHEV)

- By Application

- Infotainment

- Telematics and Connectivity

- Powertrain/Propulsion Control

- ADAS and Safety

- Charging Infrastructure and V2G

- By Form Type

- In-Vehicle (Embedded)

- External Cloud Services

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Malaysia

- Singapore

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed Tier-1 security suppliers, vehicle-software architects, and fleet managers across North America, Europe, and Asia Pacific. Those conversations clarified typical security spend per connected vehicle, regional compliance timetables, and the pace at which OEMs bundle endpoint versus cloud defenses, letting us reconcile desk estimates with market reality.

Desk Research

We began with traffic-accident records and connected-car parc counts from bodies such as UNECE, NHTSA, ACEA, and Japan's MLIT, which outline the regulatory baseline that drives security spend. Patent families retrieved through Questel helped us map new intrusion-detection IP, while import-export values from Volza and customs dashboards revealed cross-border ECU flows. Company 10-Ks, investor decks, and trade journals then provided average selling prices and attach-rate commentary. These examples are illustrative; many other open and paid sources supported data collection and fact-checking.

Market-Sizing & Forecasting

We applied a top-down build that starts with connected-vehicle stock by region, multiplies by average cybersecurity outlay per vehicle, and is subsequently cross-checked through sampled supplier revenue roll-ups. Key variables like connected-car penetration, UNECE R155 certification deadlines, ECUs per vehicle, OTA update adoption, EV sales, and 5G-V2X rollout feed a multivariate regression to project demand through 2030. Bottom-up gaps, where supplier disclosure is thin, are bridged with channel checks and ASP benchmarks shared in confidence during primary research.

Data Validation & Update Cycle

Outputs run through variance checks against historic spend ratios and peer indices, then a second analyst reviews anomalies before sign-off. Reports refresh each year, with interim updates triggered by material policy changes or major cyber incidents, ensuring clients receive the latest calibrated view.

Why Mordor's Cybersecurity For Cars Baseline Is Dependable

Published estimates often differ because firms pick dissimilar system boundaries, pricing tiers, and refresh cadences. We ground our baseline in connected-car counts and live regulatory milestones, which keeps our totals representative yet conservative.

Key gap drivers include whether ADAS software warranties are priced in, how aggressively future OTA volumes are assumed, and the currency conversion point each publisher freezes. Rivals that rely mainly on supplier surveys or dated OEM lists miss late-cycle compliance spend, whereas Mordor's rolling update schedule captures it.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.09 B | Mordor Intelligence | - |

| USD 3.24 B | Regional Consultancy A | excludes cloud-based threat-monitoring fees |

| USD 3.87 B | Trade Journal B | relies on 2023 ASPs without FX normalization |

| USD 3.40 B | Global Consultancy C | omits ADAS cybersecurity retrofits in post-sale market |

Taken together, the comparison shows that when scope and price levers shift, totals swing widely. By tying every assumption to transparent vehicle counts, rule deadlines, and validated spend curves, Mordor Intelligence delivers the dependable baseline decision-makers need.

Key Questions Answered in the Report

What is driving the rapid growth of the cybersecurity for cars market?

Mandatory UNECE R155/R156 regulations, 5G-enabled connectivity, and the migration to software-defined vehicles have increased attack surfaces and forced OEMs to invest in continuous protection, supporting a 16.12% CAGR through 2031.

How large is the cybersecurity for cars market size today?

The cybersecurity for cars market size reached USD 4.75 billion in 2026 and is forecast to grow to USD 10.03 billion by 2031.

Which region leads the cybersecurity for cars market?

Asia-Pacific leads with 35.12% revenue share in 2025, propelled by China’s connected-EV production and Japan’s early regulatory adoption.

Why is cloud security gaining prominence in automotive cybersecurity?

OTA updates, remote diagnostics, and fleet analytics increasingly rely on cloud services, making cloud security the fastest-growing segment at 20.6% CAGR.

What is the biggest challenge for OEMs implementing cybersecurity measures?

High integration costs for legacy E/E architectures and a shortage of automotive-grade cyber-talent jointly restrict rollout speed, together depressing projected CAGR by roughly 5 percentage points.

How are OEMs monetizing cybersecurity investments?

Automakers now charge subscription fees for over-the-air security updates and partner with insurers to offer usage-based premiums tied to certified cyber-hardening, creating new recurring revenue streams.

Page last updated on: