Automotive Start-Stop System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

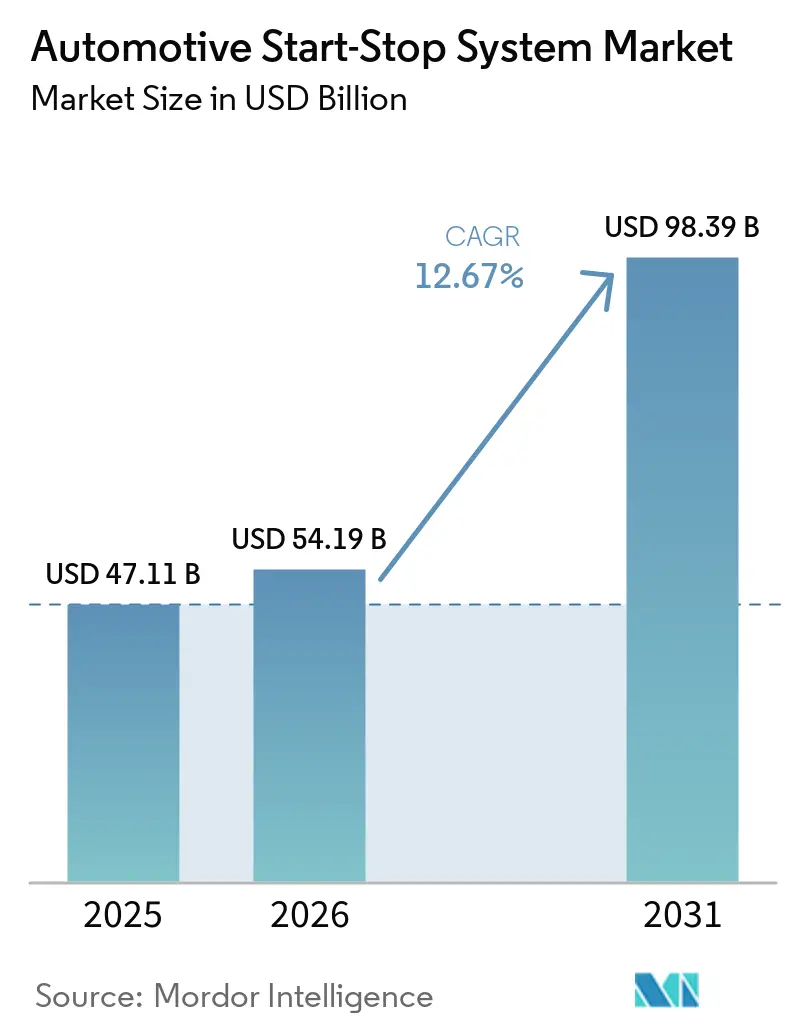

| Market Size (2026) | USD 54.19 Billion |

| Market Size (2031) | USD 98.39 Billion |

| Growth Rate (2026 - 2031) | 12.67% CAGR |

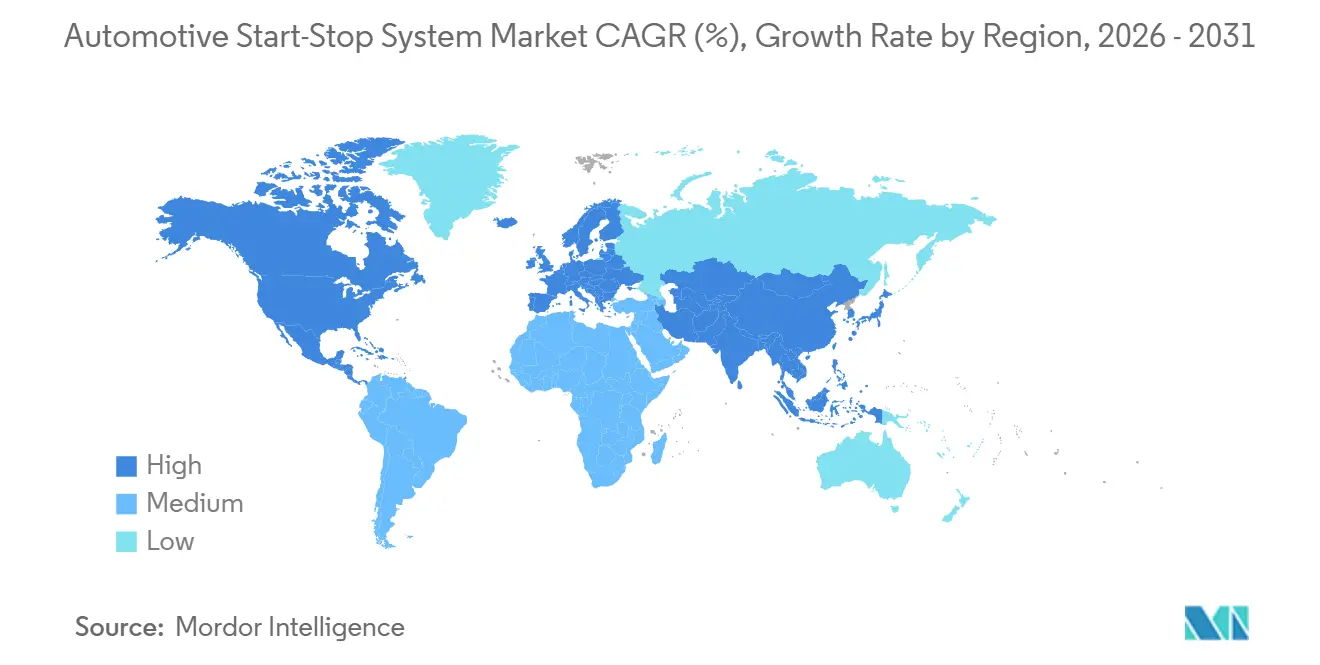

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Start-Stop System Market Analysis by Mordor Intelligence

The Automotive Start-Stop System Market size is projected to expand from USD 47.11 billion in 2025 and USD 54.19 billion in 2026 to USD 98.39 billion by 2031, registering a CAGR of 12.67% between 2026 to 2031.

Tightening fuel-economy and tail-pipe CO₂ rules on three continents compel original-equipment manufacturers (OEMs) to fit idle-reduction hardware across high-volume models. Micro-hybridization is being used as a low-cost bridge between internal-combustion and full battery-electric architectures, allowing carmakers to extract incremental efficiency gains while reusing legacy power-train assets. Component advances, in particular, high-cycle absorbed-glass-mat (AGM) batteries and edge-computing control units, are lifting real-world fuel savings and improving driver acceptance. As a result, the automotive start-stop system market continues to penetrate mass-market passenger cars, two-wheelers, and light commercial vehicles even as battery-electric vehicle (BEV) sales accelerate.

Key Report Takeaways

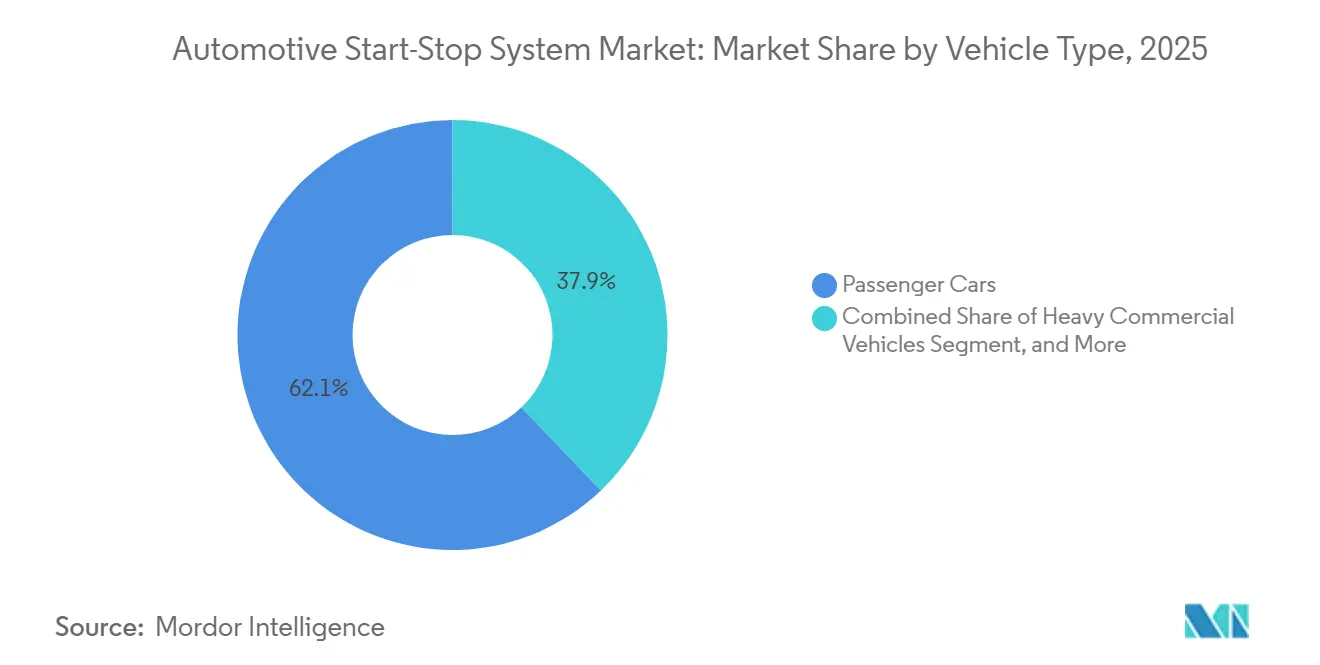

- By vehicle type, passenger cars led with 62.14% of the automotive start-stop system market share in 2025, while two-wheelers are projected to record the fastest 14.61% CAGR through 2031.

- By technology, belt-driven alternator starter commanded 38.42% share of the automotive start-stop system market size in 2025, whereas integrated starter generator is forecast to advance at an 16.13% CAGR over 2026-2031.

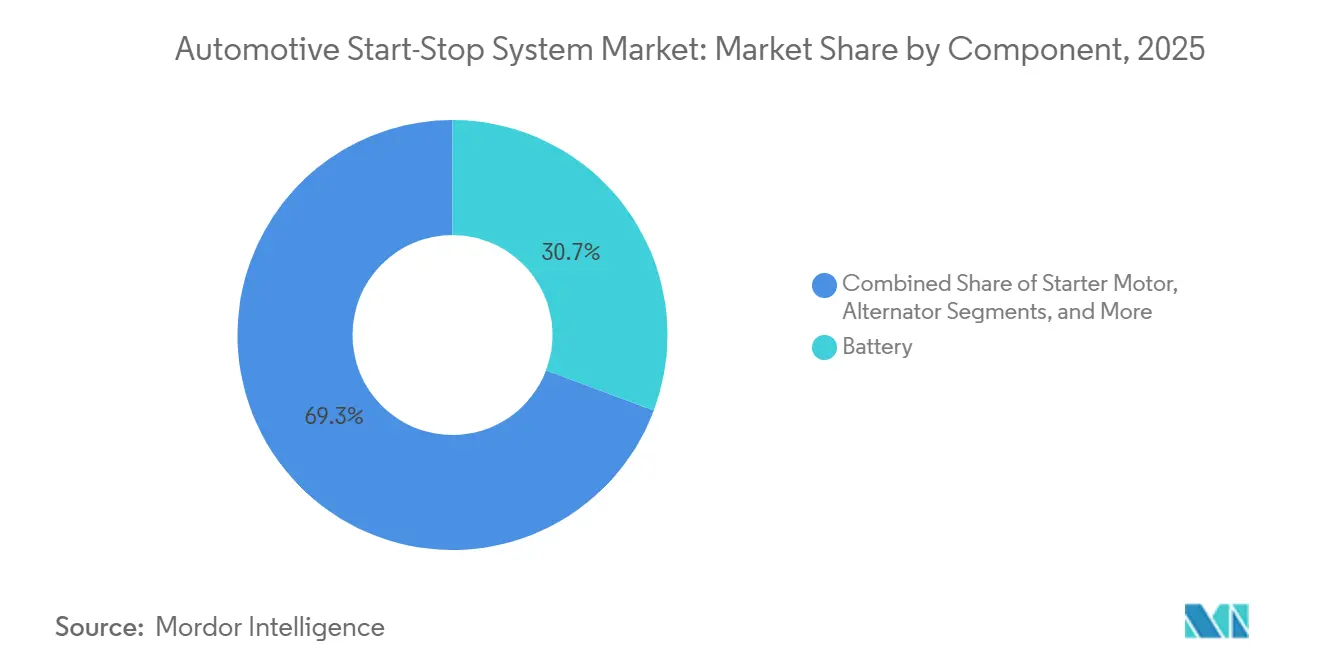

- By component, battery modules accounted for 30.72% of the automotive start-stop system market size in 2025, but control unit and sensors are set to expand at a 15.04% CAGR to 2031.

- By fuel type, gasoline engines held 57.11% share of the automotive start-stop system market size in 2025, yet hybrid powertrains, including 48-volt architectures, are projected to surge at a 16.82% CAGR during the same period.

- By geography, Europe commanded a 35.71% share in 2025; but Asia-Pacific is forecast to advance at an 14.23% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automotive Start-Stop System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened Corporate Average Fuel Economy and CO₂ Regulations | +3.2% | Global, with strongest enforcement in North America, European Union, China, India | Medium term (2-4 years) |

| OEM Integration of 48-Volt Mild-Hybrid Architectures | +2.8% | Europe, China, North America premium segments | Medium term (2-4 years) |

| Rising Demand for Micro-Hybrid Passenger Cars in Emerging Economies | +2.1% | Asia-Pacific (India, Indonesia, Thailand, Vietnam), Middle East, South America | Long term (≥ 4 years) |

| Continuous Decline in Lithium-Ion Battery USD per kWh Enhancing Durability | +1.6% | Global, with fastest adoption in China and Europe | Long term (≥ 4 years) |

| Adoption of Edge-AI Idle Prediction Algorithms to Minimize Restart Lag | +1.4% | North America, Europe, China (premium and near-premium segments) | Short term (≤ 2 years) |

| Insurance Telematics Incentives Favoring Idle-Reduction Technologies | +0.9% | North America commercial fleets, Europe fleet operators | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Heightened Corporate Average Fuel Economy and CO₂ Regulations

Regulatory stringency remains the single most potent lever for expansion in the automotive start-stop system market. The United States finalized corporate average fuel-economy targets that climb toward 50.4 miles per gallon by model year 2031, and penalties for non-compliance are set high enough to shift OEM product-planning budgets toward cost-effective idle-reduction content.[1]United States Environmental Protection Agency, “Corporate Average Fuel Economy Standards for Passenger Cars and Light Trucks for Model Years 2027 and Beyond,” federalregister.gov Europe’s revised passenger-van CO₂ performance standards require a 55% drop in fleet emissions by 2030 to 2034, cementing micro-hybrid demand as a compliance backstop when battery-electric deliveries miss plan.[2]United States Environmental Protection Agency, “Corporate Average Fuel Economy Standards for Passenger Cars and Light Trucks for Model Years 2027 and Beyond,” federalregister.gov Source: European Commission, “CO₂ Emission Performance Standards for Cars and Vans,” climate.ec.europa.eu Similar tightening is visible in India and Brazil, binding the technology to certification success in the next five-year product cycle. Collectively, these overlapping mandates provide an enduring compliance floor that supports long-run adoption.

OEM Integration of 48-Volt Mild-Hybrid Architectures

Automakers are migrating from 12-volt belt-starter packages to 48-volt integrated starter-generator (ISG) topologies that unlock regenerative braking and torque assist. MAHLE’s 48-volt belt-starter-generator delivers up to 15 kW of recuperation, saving 12-15% fuel in urban cycles.[3]MAHLE GmbH, “48 V Belt-Starter-Generator,” mahle.comSilicon-carbide power devices from STMicroelectronics and onsemi are cutting conversion losses by 30%, letting OEMs shrink under-hood packaging. These gains, matched with falling lithium-ion prices, make 48-volt the dominant bridge toward deeper electrification without incurring full BEV cost or charging-infrastructure risk.

Rising Demand for Micro-Hybrid Passenger Cars in Emerging Economies

Urban congestion and rising fuel bills in India, Indonesia, and Vietnam drive brisk uptake of idle-stop scooters and compact cars. Honda and TVS cite 7-15% real-world fuel savings from their idle-stop systems, strengthening the payback case for price-sensitive commuters. Brazil’s flex-fuel fleet is also adopting start-stop to meet PROCONVE L-8 standards, while Middle Eastern fuel-subsidy reforms make idle reduction a quick win for showroom efficiency labels. Because low-cost micro-hybrids align with disposable incomes and existing service networks, emerging regions will continue to anchor volume growth for the automotive start-stop system market.

Continuous Decline in Lithium-Ion Battery USD Per kWh Enhancing Durability

Pack prices dropped to roughly USD 115 per kWh in 2024, narrowing the cost gap between 12-volt AGM and higher-capacity 48-volt lithium-ion modules. Clarios has enhanced its VARTA AGM range, introducing carbon-infused plates that triple charge acceptance and extend the capacity of standard batteries. Parallel studies at Oak Ridge National Laboratory show 48-volt lithium packs lasting 3,000-5,000 deep cycles, translating to 10-12 years of service in mild-hybrid duty. As materials innovation trims costs and extends life, batteries shift from a maintenance headache to a durable asset, pushing the automotive start-stop system market deeper into commercial fleets and premium segments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Adoption of Battery-Electric Vehicles Cannibalizing Fitment | -2.4% | China, Europe, North America urban markets | Medium term (2-4 years) |

| Driver Discomfort From NVH During Heavy Stop-Start Cycles | -1.3% | Global, particularly dense urban markets in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Transition to Solid-State 12-Volt Batteries Necessitating Redesigns | -0.8% | Europe, North America premium segments | Long term (≥ 4 years) |

| Supply-Chain Fragility for Power MOSFETs and Relays | -0.7% | Global, with acute impact in 48-volt system production | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated Adoption of Battery-Electric Vehicles Cannibalizing Fitment

Rising BEV penetration directly shrinks the addressable pool for start-stop hardware. China’s new-energy vehicles accounted for 44.97% of all new automobile registrations in 2025, with BEVs forming about 70% of that mix. Harvard Business School research shows that the start-stop business case weakens as BEV total cost of ownership approaches parity with internal-combustion vehicles in markets with high fuel prices and dense charging grids. Premium segments convert first, chopping volume for 12-volt systems. While emerging economies and commercial fleets temper the impact, BEV growth remains the single largest structural headwind.

Driver Discomfort from NVH During Heavy Stop-Start Cycles

Frequent restart events can send 10-30 Hz torsional vibration through the driveline and spike cabin noise to 60-70 dBA, prompting many owners to disable the feature. Although dual-mass flywheels and active mounts cut vibration nearly in half, they add USD 80-120 per vehicle, a hurdle in cost-constrained segments. Bosch’s 2026 comfort-stop function leverages ADAS data and GPS to predict when not to shut the engine, lessening irritation without big hardware costs. Still, until predictive software proliferates and driver education improves, NVH will continue to cap real-world fuel-saving potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Two-Wheelers Accelerate As Urban Mobility Shifts

The automotive start-stop system market for passenger cars dominated in 2025, with a 62.14% share, as most global light-vehicle platforms standardized on idle-reduction to meet fleet targets. Urban motorists in India and Southeast Asia spend long stretches in stop-and-go traffic, making fuel savings from start-stop immediately tangible. Fleet operators in Europe and North America also add the technology to light vans to curb discretionary idling. Though heavy trucks lag in torque and accessory loads, niche applications such as refuse trucks are slowly adopting them.

Two-wheelers represent the fastest-growing segment, forecast to grow at a 14.61% CAGR through 2031, and are reshaping the automotive start-stop system market. Honda’s Idling Stop System restarts a scooter in 0.5 seconds, delivering double-digit fuel savings that resonate with price-sensitive commuters. TVS Motor has replicated the approach with its intelliGO starter, pushing penetration beyond premium bikes into mass-market city runabouts. Rising helmet-law enforcement and growing micro-mobility appetites further enlarge the pool of urban riders that value efficiency and low tail-pipe emissions. As two-wheeler output expands in India, Indonesia, and Vietnam, their share of overall system shipments will rise steadily.

By Technology: Integrated Starter-Generator Gains As 48-Volt Cascades

Belt-driven alternator starters enjoyed a robust 38.42% share of the automotive start-stop system market in 2025, driven by their favorable USD 200-300 bill-of-materials cost. It will continue to anchor entry-level micro-hybrids, particularly where 12-volt electrical architecture remains in place. Yet integrated starter-generator units are poised for double-digit growth as OEMs roll out 48-volt platforms across premium and, eventually, volume models. The switch unlocks energy recuperation, electric torque fill, and smoother restarts.

The integrated starter generator is set to post an 16.13% CAGR, capturing share in Europe and China first, then in North America. Valeo’s high-volume 48-volt program offers 15 kW recuperation, enough to power auxiliary compressors and let a small three-cylinder engine feel like a larger four-cylinder. Semiconductor advances, especially 750 V silicon-carbide MOSFETs from Infineon, are slashing thermal losses and enabling smaller converters, enabling packaging in compact sedans. Direct-starter solutions, though cheaper, lack these functional wins and are increasingly relegated to late-life platforms or markets with lenient standards.

By Component: Control Units Capture Value As Intelligence Migrates To Edge

Battery packs secured 30.72% share of the automotive start-stop system market size in 2025, reflecting their fundamental role in handling thousands of high-current restarts. AGM and enhanced flooded designs continue to improve through the use of carbon additives and smart charging algorithms, thereby limiting warranty claims. However, growth momentum is set to shift toward control units and sensor assemblies, whose revenue pool is forecast to grow at a 15.04% CAGR through 2031.

Edge-computing controllers now fuse ADAS signals, GPS, and cloud inputs to predict driver intent, avoiding unnecessary shutdowns at short red lights and steep driveways. Bosch’s comfort-stop illustrates how software can enhance perceived refinement without major mechanical upgrades. Sensors that monitor battery state, cabin climate, and traffic conditions feed these algorithms, creating an upsell path from basic voltage thresholds to predictive logic. As intelligence migrates to the edge, value pools tilt toward electronics and away from commoditized rotating hardware.

By Fuel Type: Hybrid Powertrains Lead As 48-Volt Bridges To Electrification

Gasoline units retained 57.11% share of the automotive start-stop system market size in 2025, but their growth is flattening as regulatory pressure pushes carmakers toward partial electrification. Diesels are trending lower in light-duty cars, although commercial fleets still embrace start-stop to curb idle fuel waste.

Hybrid powertrains, which bundle a 48-volt pack and an integrated starter generator, are forecast to soar at 16.82% CAGR, the fastest among fuel types. The architecture recovers braking energy, powers e-boosters, and eases compliance with real-world emissions testing requirements. Hyundai anticipates that one-third of its internal-combustion vehicles will feature 48-volt systems by 2028, a sign of mild-hybrid mainstreaming. Alternative fuels such as CNG and ethanol lag behind due to lower global volumes and calibration complexity, yet flex-fuel applications in Brazil highlight incremental CO₂ cuts when start-stop is paired with intelligent alternators.

Geography Analysis

In 2025, Europe secured 35.17% of the global automotive start-stop system market, solidifying its position as the leading regional market. This dominance stems from stringent EU CO₂ emission regulations, aggressive fleet efficiency mandates, and the widespread adoption of 48-volt mild-hybrid architectures in passenger vehicles. Even with the swift rise of battery-electric vehicles, start-stop systems remain prevalent on internal combustion and hybrid platforms, serving as a cost-effective compliance solution. Moreover, a robust Tier-1 supplier ecosystem in Germany, France, and other automotive hubs bolsters system integration capabilities and fuels strong aftermarket demand.

North America is a pivotal market for automotive start-stop systems, buoyed by tightening fuel-economy standards and their growing presence in light trucks, SUVs, and commercial fleets. Although historically lower fuel prices in the U.S. have tempered adoption rates compared to Europe, mounting regulatory pressures are now hastening their integration across OEM platforms. Additionally, the region's gradual pivot towards mild-hybrid powertrains is amplifying demand, especially in next-gen pickup and SUV models.

The Asia-Pacific region, marked by rapid urbanization and rising fuel costs, is witnessing a surge in demand for automotive start-stop systems. Countries like China, India, Japan, and those in Southeast Asia are tightening emissions regulations, further driving this trend. The region's large-scale production of compact and entry-level vehicles has led to widespread use of start-stop systems as a cost-effective solution for improving fuel efficiency. Furthermore, the increasing localization of battery and starter motor manufacturing is enhancing affordability, pushing deeper penetration into mass-market vehicle segments.

Furthermore, South America, the Middle East, and Africa form a smaller yet emerging market for automotive start-stop systems. Countries like Brazil, Saudi Arabia, and South Africa are emphasizing fuel efficiency, tightening regulations, and modernizing fleets. However, adoption remains constrained by economic volatility, harsh operating environments, and limited electrification infrastructure, which collectively slow large-scale penetration despite steady incremental demand.

Competitive Landscape

The automotive start-stop system market is moderately concentrated, with the top five Tier-1 suppliers, such as Bosch, Valeo, Denso, Continental, and BorgWarner, collectively holding a near 60% share through entrenched OEM contracts and global factories. Bosch differentiates through software, as seen in its 2026 comfort-stop, which locks in renewal business as new-vehicle launches shift to predictive control. Valeo leverages are scaled to offer remanufactured 48-volt units at 30-40% discounts, commanding the cost-sensitive aftermarket. Denso’s 2026 investment in iron-based amorphous alloy cores signals vertical integration into advanced materials for next-gen motor generators. [4]DENSO Corporation, “DENSO Invests in Next Core Technologies,” denso.com

Battery specialists are climbing the value chain. Clarios, Exide, and Johnson Controls embed LIN-bus diagnostics into AGM packs, letting OEMs harvest state-of-health data and schedule predictive maintenance. Solid-state pioneers such as Samsung SDI entered low-voltage mass production in late 2024, promising 25,000 life cycles but still grappling with validation costs. Semiconductor vendors Infineon and onsemi claim an increasing slice of system value by bundling silicon-carbide MOSFETs with reference designs for 48-volt DC-DC converters, bypassing traditional alternator makers.

White-space growth lies in two-wheelers and light commercial retrofits. Indian scooter makers source compact, silent-restart modules from local startups, threatening incumbents that lack low-power portfolios. As software moves center stage and new chemistries reach scale, competitive dynamics are poised to shift toward intellectual property depth and battery management know-how rather than mechanical prowess.

Automotive Start-Stop System Industry Leaders

Aisin Corporation

BorgWarner Inc.

DENSO Corporation

Valeo SA

Robert Bosch GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: DENSO Corporation invested in Next Core Technologies to co-develop iron-based amorphous alloy motor cores for next-generation starter-generators.

- November 2025: Robert Bosch GmbH launched its comfort-stop feature, which uses predictive algorithms to reduce unnecessary engine restarts in dense traffic.

- September 2025: Clarios expanded its VARTA AGM and EFB battery portfolio with new H3/L0 and H9/L6 sizes tailored for start-stop and mild-hybrid vehicles.

- August 2025: BorgWarner Inc. has begun supplying its start-stop systems to Renault for select models in Latin America, including the Captur and Duster equipped with 1.3L turbo engines.

Global Automotive Start-Stop System Market Report Scope

The Automotive Start-Stop System Market Report is Segmented by Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, and Two-Wheelers), Technology (Belt-Driven Alternator Starter, Integrated Starter Generator, and Direct Starter), Component (Battery, Starter Motor, Alternator, Control Unit and Sensors, and Other Components (Wiring Harness, and Relays), Fuel Type (Gasoline, Diesel, Hybrid Including 48-Volt, and Alternative Fuels Including (CNG, LPG, and Flex-Fuel), and Geography (North America, Europe, Asia-Pacific, Middle East, Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

| Two-Wheelers |

| Belt-Driven Alternator Starter (BDAS) |

| Integrated Starter Generator (ISG) |

| Direct Starter |

| Battery |

| Starter Motor |

| Alternator |

| Control Unit and Sensors |

| Other Components |

| Gasoline |

| Diesel |

| Hybrid (Incl. 48-V) |

| Alternative Fuel Types |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Heavy Commercial Vehicles | ||

| Two-Wheelers | ||

| By Technology | Belt-Driven Alternator Starter (BDAS) | |

| Integrated Starter Generator (ISG) | ||

| Direct Starter | ||

| By Component | Battery | |

| Starter Motor | ||

| Alternator | ||

| Control Unit and Sensors | ||

| Other Components | ||

| By Fuel Type | Gasoline | |

| Diesel | ||

| Hybrid (Incl. 48-V) | ||

| Alternative Fuel Types | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current automotive start-stop system market size, and how fast is it growing?

Mordor Intelligence values the automotive start-stop system market at USD 54.19 billion in 2026 and expects it to reach USD 98.39 billion by 2031, delivering a 12.67% CAGR.

Which vehicle category is expanding fastest in the automotive start-stop system market?

Two-wheelers are projected to grow at the highest 14.61% CAGR through 2031, driven by urbanization in Asia, which is driving demand for fuel-efficient scooters.

Which region generates the largest revenue?

Europe contributes 35.71% of global revenue and grows at 12.74% CAGR.

Why are 48-volt mild-hybrid systems important for start-stop technology?

A 48-volt architecture couples regenerative braking and torque assist with smoother, quicker restarts, thereby enhancing fuel savings and driver comfort while helping OEMs meet tightening CO₂ targets.

How do driver comfort features address noise and vibration during engine restarts?

Predictive algorithms, such as Bosch’s comfort-stop, analyze traffic data and prevent shutdowns when idle durations are too short, reducing cabin vibrations and minimizing manual deactivation of the system.

Page last updated on: