Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

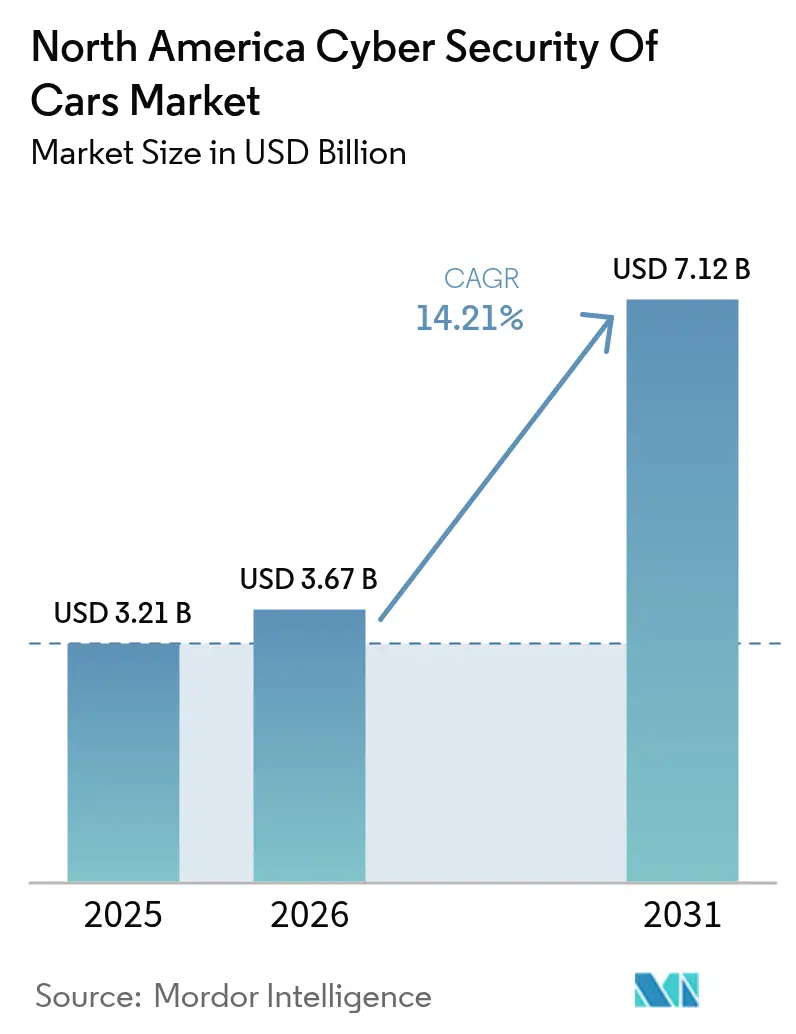

| Base Year Market Size (2025) | USD 3.21 Billion |

| Market Size (2026) | USD 3.67 Billion |

| Market Size (2031) | USD 7.12 Billion |

| Growth Rate (2026 - 2031) | 14.21% CAGR |

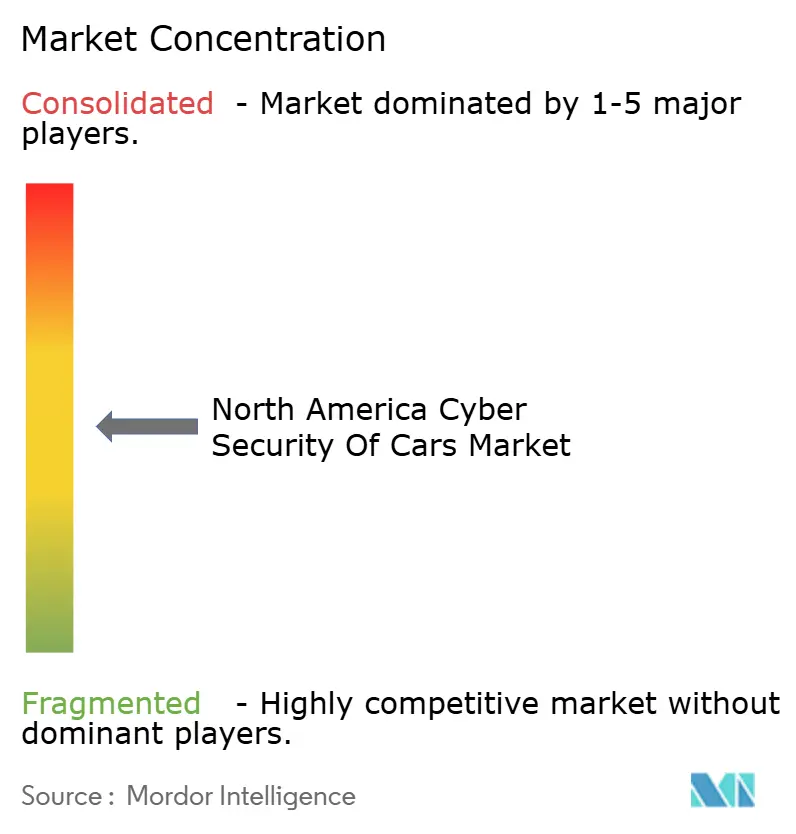

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Cybersecurity of Cars Market Analysis by Mordor Intelligence

The North America Cybersecurity of Cars Market size was valued at USD 3.21 billion in 2025 and estimated to grow from USD 3.67 billion in 2026 to reach USD 7.12 billion by 2031, at a CAGR of 14.21% during the forecast period (2026-2031). This rapid expansion reflects the region’s transition toward software-defined vehicles, mounting enforcement of UN Regulation R155 and ISO 21434, and a sharp rise in over-the-air update programs that expose both revenue potential and new attack vectors. Automakers continue reallocating capital toward centralized computing, 5G-enabled V2X communications, and digital-key ecosystems that demand end-to-end protection. Federal funding exceeding USD 13 billion for civilian agencies underscores the U.S. commitment to hardening critical mobility infrastructure [1]U.S. Department of Energy, “Securing EV Charging Infrastructure Part 1: Why Cybersecurity Matters,” energy.gov. Canada’s pending motor-vehicle safety reforms and Mexico’s evolving USMCA obligations introduce additional momentum and complexity across the North America Cybersecurity of Cars Market.

Key Report Takeaways

- By solution type, software-based platforms led with 39.65% revenue share in 2025, while professional and managed services are advancing at a 15.33% CAGR through 2031.

- By security domain, network security accounted for 34.78% of the North America cybersecurity of cars market share in 2025, and cloud/backend security is projected to expand at a 15.92% CAGR to 2031.

- By vehicle type, passenger cars held a 58.61% share of the North America cybersecurity of cars market size in 2025, whereas autonomous and robo-taxis are set to grow at an 17.64% CAGR.

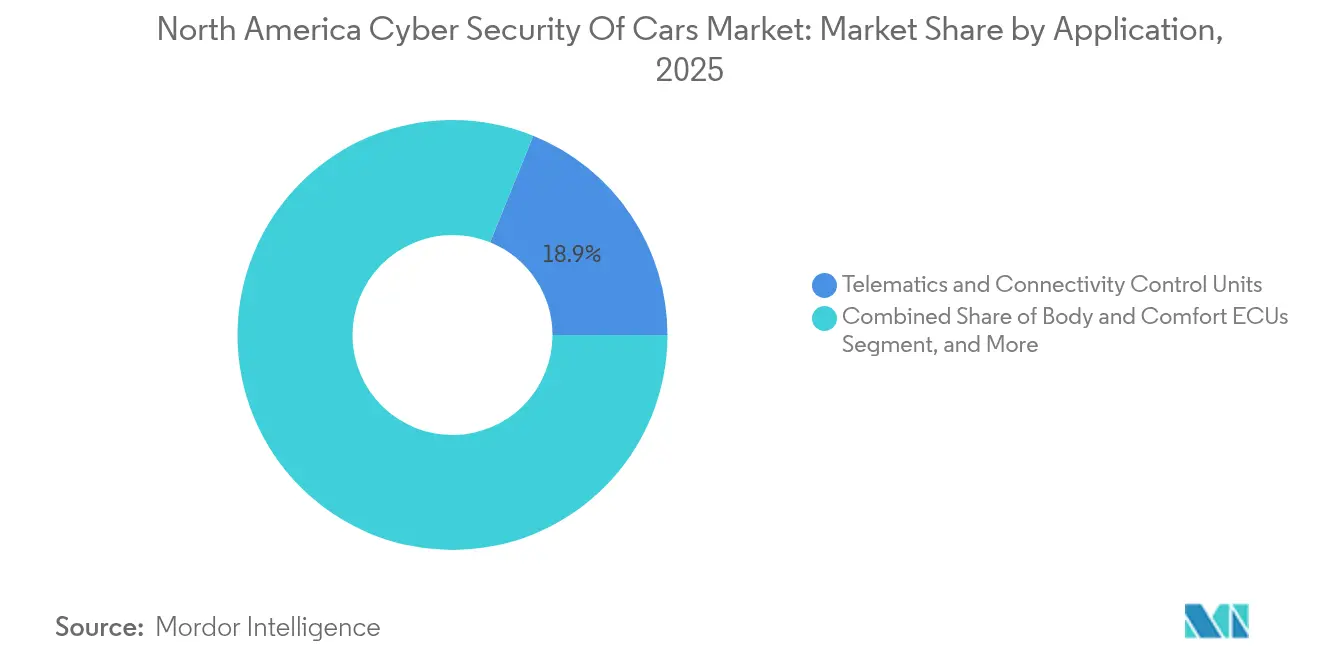

- By application, telematics and connectivity control units commanded 18.87% of 2025 revenue, and ADAS and autonomous driving systems are on track for a 16.74% CAGR through 2031.

- By deployment mode, on-board (edge) solutions represented 54.63% of revenue in 2025, and off-board / cloud deployments are forecast to rise at a 16.71% CAGR.

- By geography, the United States dominated with a 77.05% share in 2025, while Canada is forecast to post the fastest 17.58% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Cybersecurity of Cars Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| UN R155 / ISO 21434 compliance | +2.8% | North America and Global | Short term (≤ 2 years) |

| OTA software-update surge | +2.1% | United States, Canada | Medium term (2-4 years) |

| Connected-car parc growth and 5G / V2X roll-out | +1.9% | Core North America, spill-over Mexico | Medium term (2-4 years) |

| Digital-key ecosystem expansion | +1.4% | United States, early Canada | Short term (≤ 2 years) |

| EV-charging-station attack surface | +1.2% | Urban North America | Medium term (2-4 years) |

| Software-defined vehicle revenue models | +1.6% | Global, North America leadership | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

UN R155 / ISO 21434 compliance deadlines

Mandatory enforcement beginning July 2024 forced OEMs to certify cybersecurity management systems, software-update processes, and continuous vulnerability monitoring. Automakers responded by embedding “security-by-design” procurement across their tier-one supply networks, accelerating demand for third-party audits and managed-service contracts [2]UL Solutions, “Cybersecurity Management System (CSMS),” ul.com . Suppliers unable to demonstrate process maturity face exclusion from new-vehicle programs, pushing professional-service uptake across the North America Cybersecurity of Cars Market.

Surge in OTA software-update adoption

More than 250 million vehicles are expected to support OTA functions by 2025, shifting recall mitigation from physical service campaigns to secure remote patching [3]HARMAN Automotive, “Refining Automotive OTA Deployment Strategies for a Direct Consumer Impact,” harman.com. Automakers rely on cryptographic authentication and dual-image fail-safe techniques to safeguard updates. The heightened cadence of software releases amplifies endpoint exposure, thereby elevating demand for endpoint-protection agents and cloud-based threat-intelligence aggregation throughout the North America Cybersecurity of Cars Market.

Growth of connected-car parc and 5G / V2X roll-out

5G capacity enables low-latency V2X messaging yet enlarges the potential surface for distributed denial-of-service and man-in-the-middle intrusions. The U.S. Department of Homeland Security classifies wireless assaults on vehicular comms among the most serious transportation threats, encouraging joint industry–government frameworks for secure spectrum use [4]U.S. Department of Homeland Security, “5G Impacts to Vehicles and Highway Infrastructure,” dhs.gov. Emerging AI-driven network sensors leverage 5G throughput to quarantine anomalies in real time across the North America Cybersecurity of Cars Market.

Rapid expansion of in-vehicle digital-key ecosystems

CCC-driven interoperability underpins a 21% annual rise in digital-key adoption, rewarding providers of public-key-infrastructure services and biometric credential storage. PKI-anchored smartphone access cuts relay-attack incidents and aligns with consumer demand for frictionless mobility, yet demands continual risk assessment as handset OS updates can weaken cryptographic policies across the North America Cybersecurity of Cars Market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented software supply chain | -1.8% | North America and Global | Medium term (2-4 years) |

| Threat landscape outpacing standards | -1.5% | Global, acute North America | Short term (≤ 2 years) |

| AUTOSAR-cyber talent scarcity | -1.3% | North America, specialized roles | Long term (≥ 4 years) |

| Limited CAN-FD bandwidth | -0.9% | Global, infrastructure dependent | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Highly fragmented software supply chain

Typical vehicles integrate hundreds of supplier modules, each with its own firmware lineage. The absence of comprehensive software bills of materials complicates patch orchestration, leaving latent vulnerabilities across multiple ECUs. Ransomware actors exploited third-party gateways, pushing North America’s disclosed automotive supply-chain-attack share to 58% in Q2 2024.

Evolving threat landscape outpacing standards

Financial damages from automotive cyber incidents climbed to USD 22.5 billion in 2024, outstripping the pace of regulatory updates. Quantum-ready encryption remains largely absent from production vehicles, creating a roadmap mismatch that exposes long-life platforms to future decryption attacks. Vendors emphasizing adaptive, policy-based defense tools gain strategic advantage within the North America Cybersecurity of Cars Market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Services Drive Professional Transformation

Software-centric platforms captured 39.65% of 2025 revenue as firewalls, intrusion-detection systems, and AI-based analytics became default requirements for connected vehicles. Professional and managed services, however, are forecast to grow 15.33% each year to 2031 as OEMs outsource threat monitoring and incident response functions that outpace in-house capability gaps. The North America Cybersecurity of Cars Market size for professional services is projected to nearly double by 2031. Severe workforce shortages push automakers toward subscription models that bundle security operations center access with compliance reporting.

Momentum in managed services also supports integration consulting, allowing suppliers to harmonize security controls across heterogeneous ECU stacks. Upstream Security’s cloud surveillance service already supports more than 25 million vehicles, illustrating a scalable blueprint that other providers emulate . Hardware security modules from NXP and Infineon add root-of-trust features that reduce on-vehicle compute costs, but integration success still depends on holistic vulnerability-management workflows delivered by external partners.

By Security Domain: Cloud Architecture Transformation

Network security led the market with a 34.78% share in 2025 as OEMs hardened CAN-FD and automotive Ethernet against packet spoofing. Cloud/backend security is expected to post the fastest 15.92% CAGR as centralized data lakes collect up to 40 terabytes per hour of fleet telemetry for real-time anomaly detection. The North America Cybersecurity of Cars Market share for cloud security climbs as domain controllers forward logs to hyperscaler environments that offer elastic compute for AI analytics.

Application-level countermeasures gain relevance as third-party infotainment and insurance applications penetrate in-vehicle ecosystems. Sandboxing and code-signing functionalities protect cockpit marketplaces such as HARMAN Ignite Store, while endpoint ECU security continues to address lightweight encryption for body-control and safety actuators. Identity-and-access-management subdomains show early traction as digital-service portfolios expand.

By Vehicle Type: Autonomous Systems Security Premium

Passenger cars delivered 58.61% of 2025 revenue, yet autonomous and robo-taxis are on a trajectory to grow 17.64% annually because redundant sensor suites and AI decision loops demand multi-layer defense. The North America Cybersecurity of Cars Market size for autonomous platforms is tied to project rollouts from Tesla, Cruise, and Waymo. These programs allocate higher security-spend per unit as functional-safety regulators expect resilient response even under active cyber breach scenarios.

Light commercial fleets adopt fleet-wide intrusion-detection as logistics operators cannot tolerate vehicle downtime. Heavy trucks integrate gateway segmentation to isolate infotainment from brake controllers. Standardization across these categories remains fragmented, yet drives cross-vertical productization among security vendors that package solutions for mixed asset portfolios.

By Application: ADAS Security Complexity

Telematics and connectivity control units generated 18.87% of 2025 revenue by acting as default ingress points for remote services. ADAS and autonomous driving systems are projected for a 16.74% CAGR as sensor fusion algorithms move to centralized processors. The North America Cybersecurity of Cars Market size allocated to ADAS layers will expand alongside Level 3–4 rollouts. Attack vectors include spoofed object-detection data, compelling OEMs to deploy real-time sensor integrity checks.

Infotainment and digital cockpits continue to gain features such as app stores and voice assistants, elevating sandboxing requirements. Powertrain / EV charging interfaces reveal emerging risk associated with bi-directional energy flows. Body-and-comfort controllers, while low power, are no longer ignored, as relay thieves pivot to interior CAN nodes once perimeter defenses strengthen.

By Deployment Mode: Edge Computing Security

On-board solutions held 54.63% revenue in 2025, leveraging real-time anomaly detection to protect latency-sensitive powertrain and braking functions. Off-board / cloud deployments are expected to advance 16.71% annually through 2031, driven by AI-driven fleet-wide correlation models such as Upstream’s Ocean AI engine. The hybrid approach dominates procurement, allocating signature-based intrusion prevention to edge gateways, while complex pattern matching and long-term forensics reside in the cloud. Automakers increasingly standardize MQTT or HTTPS telemetry pipelines so that domain-controller logs feed threat-intelligence dashboards in near real time. The North America Cybersecurity of Cars Market benefits from 5G network slicing that offers a secure baseline latency for security telemetry backhaul without congesting consumer infotainment traffic.

Geography Analysis

The United States captured 77.05% of revenue in 2025, reflecting dense OEM footprints, tier-one suppliers, and federal backing that totals more than USD 13 billion for civilian cybersecurity programs . Washington’s ban on Chinese and Russian connected-vehicle technology pushes domestic vendors to occupy supply gaps, while Detroit–Silicon Valley collaboration accelerates innovation pipelines. Leading platform providers such as HARMAN, BlackBerry QNX, and Continental calibrate their product roadmaps to align with U.S. National Highway Traffic Safety Administration guidance linking type-approval to ISO 21434 audit results.

Canada is forecast to grow 17.58% annually, supported by updated motor-vehicle safety standards and public-sector initiatives promoting zero-trust frameworks across transportation assets. Yet the nation wrestles with a shortage of up to 25,000 cybersecurity professionals, incentivizing OEMs to contract managed-service suppliers. Provincial investments in 5G corridors between Ontario and Québec further elevate network-security spending within the North America Cybersecurity of Cars Market.

Mexico’s regulatory path remains fluid as USMCA review approaches in 2026, possibly imposing stricter controls on foreign telematics modules. IMMEX compliance audits already pressure assemblers to document end-to-end security processes, prompting multinational tier-ones to pre-qualify suppliers on ISO 21434 readiness. Proposed semiconductor tariffs could shift electronics production inward, positioning domestic fabs to integrate secure microcontrollers that meet export-market demands.

Competitive Landscape

The marketplace shows moderate fragmentation, with global technology conglomerates contending alongside specialized startups. HARMAN leverages Samsung’s silicon supply and has open-sourced a connected-services stack through the Eclipse Foundation to accelerate ecosystem adoption. BlackBerry QNX pairs deterministic microkernel heritage with new partnerships involving Vector and TTTech to supply safety-certified middleware for zonal architectures.

Semiconductor heavyweights NXP and Infineon embed post-quantum cryptography and hardware root-of-trust into 16 nm microcontrollers, enabling secure boot at power-on while easing AUTOSAR integration. Upstream Security and VicOne champion cloud-native threat-intelligence networks that deliver fleet-wide analytics. Niche innovators such as RunSafe introduce binary-level moving-target defense, evidenced by BMW i Ventures’ investment that validates market appetite for firmware immunization.

Growth strategies hinge on ecosystem alliances, vertical acquisitions, and compliance consulting services. Vendors that combine AI analytics, standards mapping, and over-the-air remediation gain traction as OEMs seek single-pane solutions across development and operations. Competitive intensity is expected to rise once mandatory cybersecurity type-approval expands to legacy model updates, widening total addressable spend in the North America Cybersecurity of Cars Market.

North America Cybersecurity of Cars Industry Leaders

Harman International Industries Inc. (Samsung Electronics Co. Ltd.)

BlackBerry Ltd. (through QNX Software Systems)

Continental AG

Robert Bosch GmbH – ETAS / ESCRYPT

Aptiv PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: HARMAN became one of the first companies to open-source a complete connected-services platform through the Eclipse Foundation, enabling secure vehicle-to-cloud connectivity for large-scale software-defined vehicle deployments.

- January 2025: VicOne collaborated with Microsoft to provide automotive threat intelligence for software developers, integrating GitHub security analysis with VicOne’s xZETA platform.

- December 2024: Upstream Security partnered with Google Cloud to enhance defensive analytics for connected vehicles across North America.

- November 2024: VVDN Technologies signed an MOU with SecureThings.ai to strengthen ISO 21434 compliance services for connected-vehicle programs.

North America Cybersecurity of Cars Market Report Scope

The scope of the study characterizes the North American market for cybersecurity of cars, based on the type of solution, which includes software-based, hardware-based, professional service, Integration, and security that includes network security, application security, cloud security.

The study also includes the assessment of the impact of COVID-19 on the market.

By Solution Type

| Software-based |

| Hardware-based |

| Professional and Managed Services |

| Integration |

| Other Solutions |

By Security Domain

| Network Security |

| Application Security |

| Cloud/Backend Security |

| Endpoint ECU Security |

| Other Domains |

By Vehicle Type

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

| Autonomous and Robo-Taxis |

By Application

| Telematics and Connectivity Control Units |

| Infotainment and Digital Cockpit |

| ADAS and Autonomous Driving Systems |

| Powertrain / EV Charging Interfaces |

| Body and Comfort ECUs |

By Deployment Mode

| On-board (Edge) |

| Off-board / Cloud |

By Country

| United States |

| Canada |

| Mexico |

| By Solution Type | Software-based |

| Hardware-based | |

| Professional and Managed Services | |

| Integration | |

| Other Solutions | |

| By Security Domain | Network Security |

| Application Security | |

| Cloud/Backend Security | |

| Endpoint ECU Security | |

| Other Domains | |

| By Vehicle Type | Passenger Cars |

| Light Commercial Vehicles | |

| Heavy Commercial Vehicles | |

| Autonomous and Robo-Taxis | |

| By Application | Telematics and Connectivity Control Units |

| Infotainment and Digital Cockpit | |

| ADAS and Autonomous Driving Systems | |

| Powertrain / EV Charging Interfaces | |

| Body and Comfort ECUs | |

| By Deployment Mode | On-board (Edge) |

| Off-board / Cloud | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the expected value of the North America Cybersecurity of Cars Market by 2031?

It is projected to reach USD 7.12 billion by 2031, growing at a 14.21% CAGR.

Which solution type shows the fastest growth trajectory?

Professional and managed services are forecast to expand at 15.33% annually as OEMs outsource threat-monitoring and compliance functions.

How are UN R155 and ISO 21434 influencing procurement strategies?

These regulations make certified cybersecurity management systems mandatory, compelling suppliers to embed security-by-design practices to retain program eligibility.

Why is cloud / backend security gaining momentum?

Centralized domain-controller architectures off-load massive telemetry streams to hyperscaler environments, driving a 15.92% CAGR for cloud-focused controls.

Page last updated on: