Vegan Dog Food Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

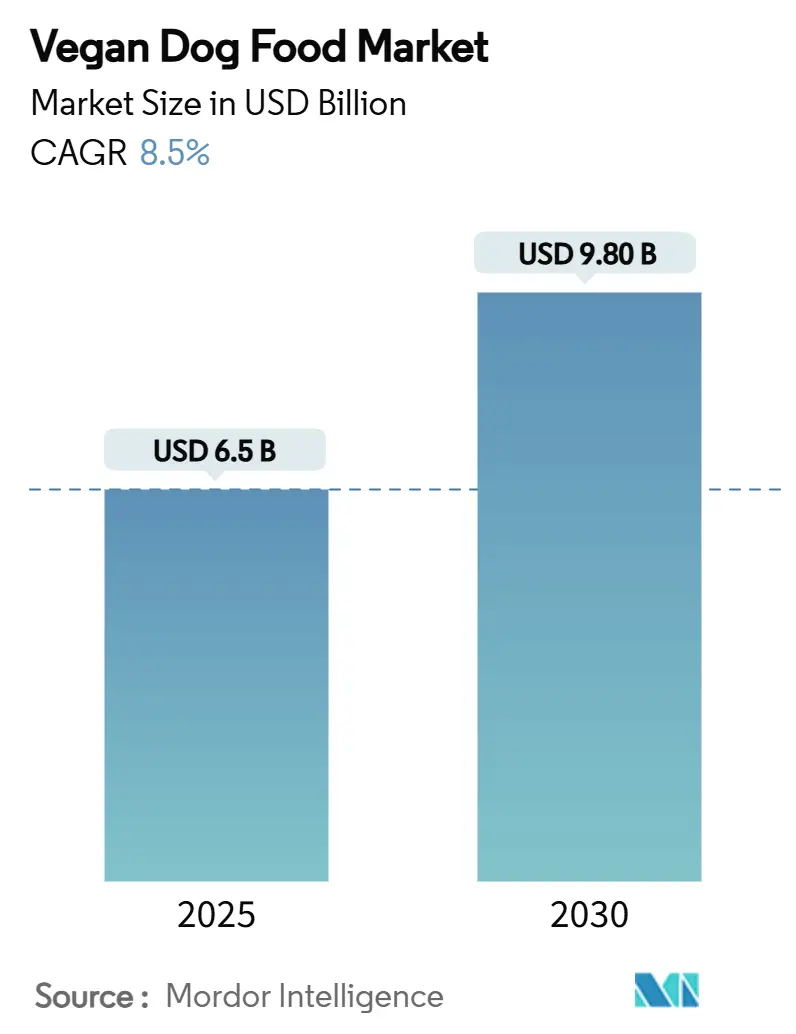

| Market Size (2025) | USD 6.5 Billion |

| Market Size (2030) | USD 9.80 Billion |

| Growth Rate (2025 - 2030) | 8.50% CAGR |

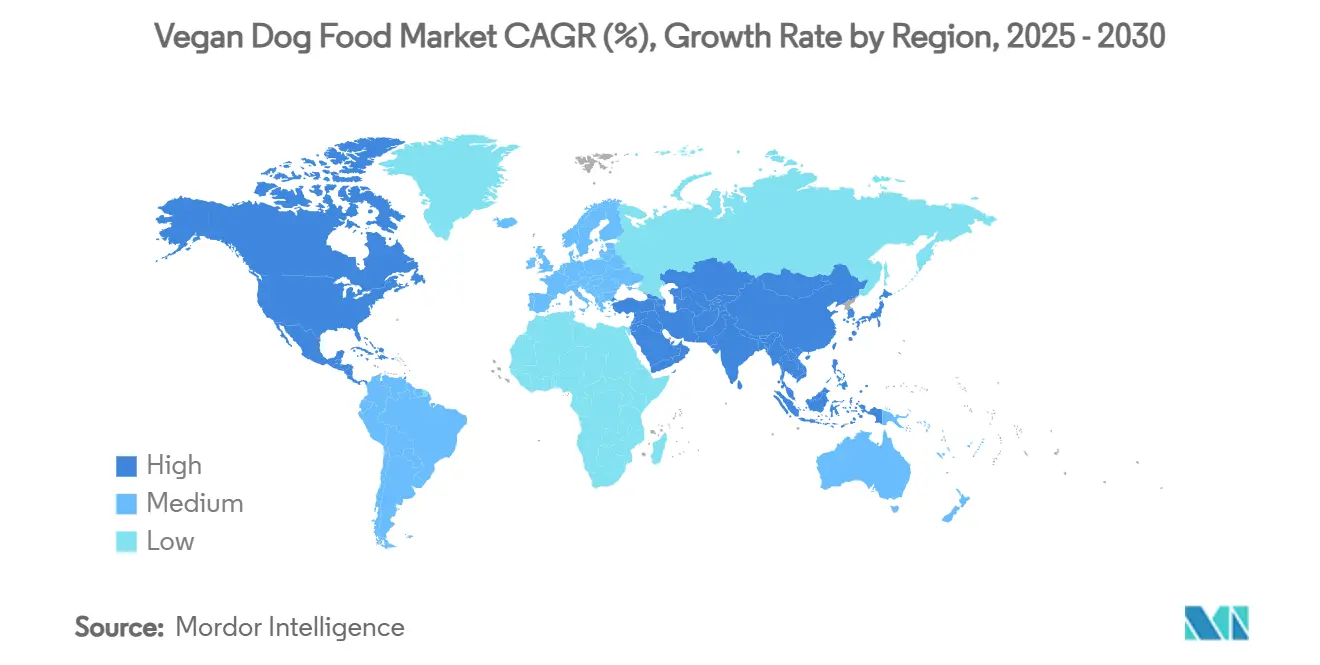

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vegan Dog Food Market Analysis by Mordor Intelligence

The vegan dog food market size reached USD 6.5 billion in 2025 and is on course to climb to USD 9.8 billion by 2030, reflecting an 8.5% CAGR over the review period. Accelerating mainstream adoption stems from shifting owner values, expanding veterinary acceptance, and tightening sustainability rules that favor plant-based formulations. Precision-fermentation breakthroughs are beginning to close historic price gaps, while online channels give niche brands direct paths to early adopters. The level of competition in the market is relatively moderate, as the leading suppliers collectively account for a small portion of global sales. This situation creates opportunities for new entrants to offer differentiated products. However, the vulnerabilities in the supply chain for essential amino acids underscore the importance of having backup sources and establishing long-term contracts for securing supplies.

Key Report Takeaways

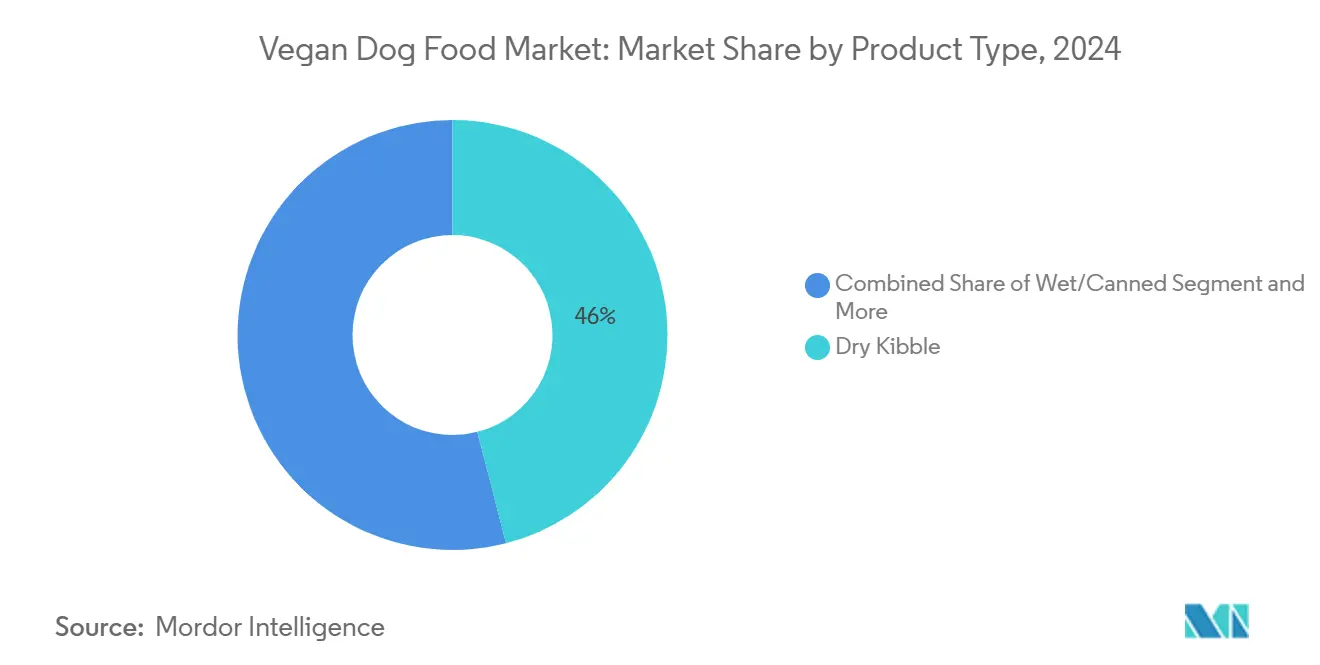

- By product type, dry kibble led with a 46% revenue share in 2024, while supplements posted the fastest growth at a 12.6% CAGR to 2030.

- By ingredient source, soy-based recipes captured 38% of the vegan dog food market share in 2024, whereas fermentation-derived proteins are projected to expand at a 14.2% CAGR through 2030.

- By life stage, adult diets accounted for 52% of the vegan dog food market size in 2024, and senior formulas are projected to advance at a 10.8% CAGR during the forecast horizon.

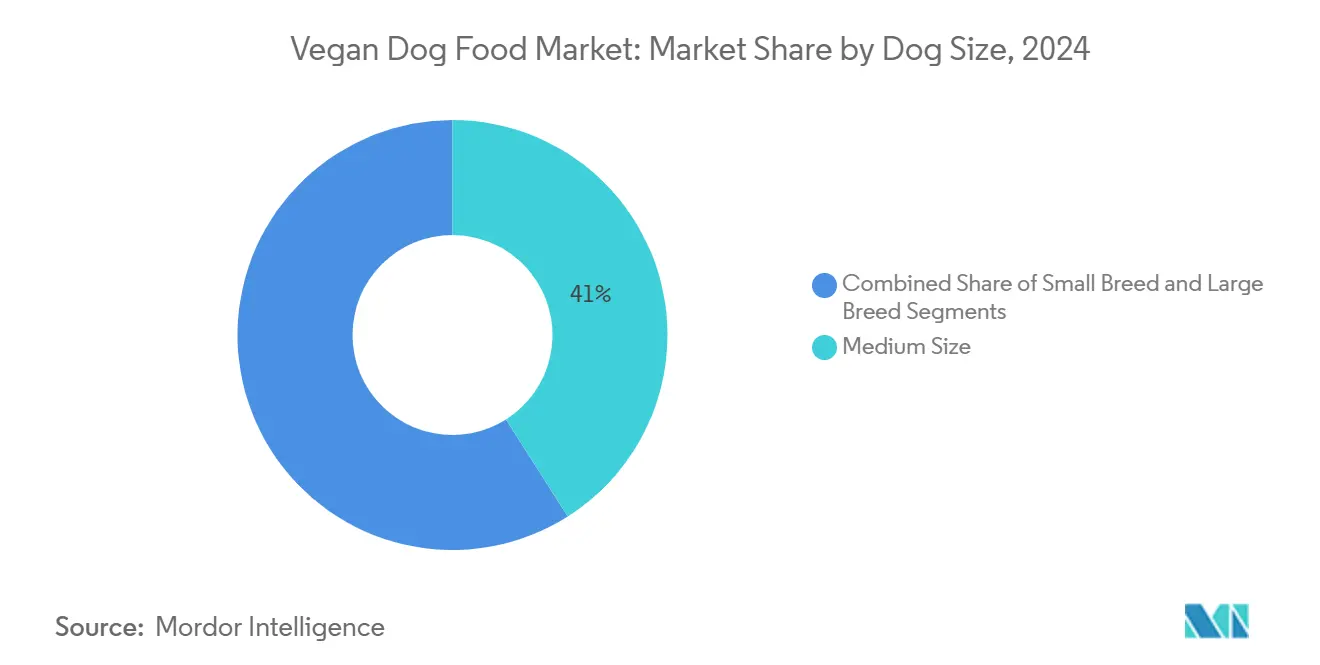

- By dog size, medium breeds held 41% of 2024 sales, and small-breed products recorded the highest projected 11.3% CAGR to 2030.

- By distribution channel, supermarkets represented 49% of global turnover in 2024, whereas online retail is forecast to grow at an 18.4% CAGR to 2030.

- By geography, Europe dominated with a 34% share in 2024, while Asia-Pacific is anticipated to surge at a 12.9% CAGR through 2030.

- The top five companies accounted for 35% share of global revenue, signaling a moderate level of market concentration.

Global Vegan Dog Food Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising vegan and flexitarian pet-owner base | +1.8% | Global, pronounced in North America, Europe | Medium term (2-4 years) |

| Pet humanization driving premium spend | +1.5% | Global, Asia-Pacific urban hubs lead | Long term (≥ 4 years) |

| Environmental sustainability mandates | +1.2% | Europe, North America, expanding in Asia-Pacific | Long term (≥ 4 years) |

| Veterinary endorsement of hypoallergenic plant diets | +1.0% | North America, Europe, and emerging in Asia-Pacific | Medium term (2-4 years) |

| Precision-fermented proteins lowering cost of amino-acid supplementation | +0.8% | Global, production clusters in North America and Europe | Medium term (2-4 years) |

| Carbon-footprint labeling rules for pet food SKUs | +0.6% | Europe in front, North America following | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Vegan and Flexitarian Pet-Owner Base

Surging interest in meat-free living now extends to household animals, creating a durable demand curve for the vegan dog food market. Survey data show that many veterinarians already see clients feeding plant-based diets, citing welfare and ecological motives. Millennials and Generation Z dominate new pet acquisitions, and these cohorts display a higher propensity to align pet feeding with personal ethics. Social media amplifies success stories, lowering perceived switching risks and energizing word-of-mouth marketing. The trend concentrates in dense urban centers where retail assortment, logistics convenience, and environmental consciousness converge.

Environmental Sustainability Mandates

Legislators in Europe and North America are embedding carbon-disclosure rules into product labeling, a shift that structurally advantages the vegan dog food market. The European Union’s Product Environmental Footprint methodology now covers pet food life-cycle impacts, compelling meat-based brands to quantify high-emission profiles [1]Source: UK Pet Food, “Environmental Impacts of Pet Food,” ukpetfood.org. Scientific modeling shows plant-only dog diets could free land greater than the combined territory of Mexico and Germany. Grocery buyers and specialty retailers respond by expanding shelf allocation to low-impact SKUs, reinforcing the growth loop. Compliance investments required for footprint audits create additional barriers for small conventional manufacturers, indirectly boosting vegan entrants that start with inherently lower emissions.

Veterinary endorsement of hypoallergenic plant diets

Clinical acceptance crossed a tipping point when the British Veterinary Association formally ended its opposition to vegan canine diets in July 2024 [2]Source: British Veterinary Association, “Policy on Vegan Diets for Dogs,” bva.co.uk. Longitudinal research in PLOS ONE confirmed maintenance of normal hematological parameters after 12 months on commercial plant-based formulas [3]Source: Linde et al., “One-Year Plant-Based Diet Study in Dogs,” plosone.org . For dogs with chronic food allergies, veterinarians now prescribe vegan rotations as first-line therapy, shifting the category from niche to therapeutic. Trade media highlight success stories, reinforcing practitioner comfort and spurring continuing-education modules on plant-based nutrition. Brand owners leverage endorsements to earn shelf positioning in veterinary clinics and pet pharmacies.

Precision-Fermented Proteins Lowering Cost of Amino-Acid Supplementation

Amino-acid parity with meat historically required expensive synthetic additives that inflated retail prices. Bond Pet Foods shipped animal-identical fermented proteins to Hill’s Pet Nutrition in February 2024, proving industrial scalability. FeedKind Pet protein, launched in Europe in 2024, provides complete amino profiles while using minimal water and land resources. As fermentation capacity builds, analysts project ingredient costs to fall by 20-30%, pushing vegan dog food closer to conventional price points. The technology also mitigates taurine and methionine supply shocks by creating regional production redundancies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Perceived nutritional adequacy risk | −1.4% | Global, strongest in mature pet-food zones | Medium term (2-4 years) |

| Premium pricing versus conventional dog food | −1.1% | Global, price-sensitive economies are most hit | Short term (≤ 2 years) |

| Palatability and taste-acceptance challenges | −0.9% | Global, varies with regional preferences | Medium term (2-4 years) |

| Limited global taurine/methionine supply chain for vegan formulations | −0.7% | Global, concentrated in chemical clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Perceived Nutritional Adequacy Risk

Decades of meat-centric marketing leave many owners skeptical that plant-based recipes meet canine dietary standards. Even with robust clinical evidence, the absence of immediate visual feedback on internal health metrics fuels caution. Brands counteract the restraint through transparent publication of digestibility studies, FEDIAF compliance badges, and third-party certifications. Educational campaigns featuring board-certified nutritionists help demystify protein bioavailability. As time goes on, ongoing peer-reviewed studies are expected to diminish the perception gap.

Premium Pricing Versus Conventional Dog Food

Vegan formats still retail at two to four times the price of economy meat-based kibble. Inflationary pressures amplify sticker shock, especially among single-income households. Manufacturers pursue value engineering by integrating co-product streams and scaling fermentation inputs. Subscription programs that smooth monthly costs gain traction among digitally native shoppers. Price parity remains a medium-term milestone that will determine how far beyond affluent early adopters the vegan dog food market can penetrate.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dry Kibble Dominance Drives Innovation

Dry kibble retained 46% of 2024 sales within the vegan dog food market because of cost-efficient mass manufacturing and broad supermarket shelf presence. Brands exploit existing extrusion lines, making plant-based switchover economically feasible for co-packers. Flavor coatings meet taste expectations, maintaining repeat purchase rates close to those of meat-based products. Wet and canned variants, though smaller, grow steadily as owners seek texture variety.

Supplements, registering the segment-high 12.6% CAGR, mirror human functional-food trends. Formulators bundle joint-care actives such as glucosamine with algae-derived omega-3s, creating cross-category upsell opportunities. Direct-to-consumer delivery makes replenishment easy, while veterinary clinics stock therapeutic chews for specific conditions. Success in the segment signals that ancillary products can scale faster than staple diets when positioned around discrete health outcomes.

By Ingredient Source: Fermentation Disrupts Traditional Proteins

Soy-based recipes held 38% of the vegan dog food market share in 2024, due to established supply networks and complete amino profiles. Critics of soy’s allergen potential accelerate demand for pea and lentil blends that offer similar protein densities with cleaner labels.

Fermentation-derived ingredients are projected to achieve the highest CAGR of 14.2%, representing a key area of innovation during the forecast period. Companies like Bond Pet Foods deliver chicken-identical keratin proteins without involving animals, letting manufacturers meet essential amino-acid ratios while cutting land use by more than 90%. Regulatory green lights in the European Union ease inclusion in commercial formulas, and early consumer studies show no palatability penalty. As capacities scale, cost curves will tighten, reinforcing ingredient diversity.

By Life Stage: Adult Segment Stability Contrasts Senior Growth

Adult formulations represented 52% of 2024 turnover, reflecting the largest cohort in the global dog population and the baseline from which owners experiment with diet swaps. Marketing focuses on everyday vitality, skin-and-coat shine, and weight management, mirroring mainstream wellness cues.

Senior recipes, growing at 10.8% CAGR, capitalize on evidence that plant-based diets reduce inflammatory biomarkers and support renal health [4]Source: Veterinary Sciences Journal, “Plant Extracts Enhance Canine Health,” veterinarysciences.org . Brands include lower-calorie, high-fiber matrices to aid weight control, and joint-support botanicals tackle age-related mobility decline. Packaging highlights softer kibble textures and smaller pellet sizes to accommodate dental wear.

By Dog Size: Medium Breeds Lead While Small Breeds Accelerate

Medium-sized dogs captured 41% of 2024 sales due to balanced energy demands that align with standard vegan formulations. This demographic skews toward urban households that value eco-friendly claims and possess disposable income to trial premium diets.

Small breeds are experiencing the highest growth rate at 11.3% CAGR as apartment living becomes more popular worldwide. Owners typically purchase smaller bag sizes but spend more per kilogram, pushing average revenue per pet higher than larger breeds. Product managers tailor nutrient density and kibble diameter to miniature jaws, while treat lines spotlight weight-control features to prevent calorie overfeeding.

By Distribution Channel: Online Surge Challenges Retail Dominance

Brick-and-mortar supermarkets controlled 49% of global volume in 2024, offering shoppers one-stop convenience and impulse display endcaps. Merchandising partnerships secure eye-level facings and in-aisle education signage.

Online retail expands at an 18.4% CAGR, driven by algorithmic recommendations, same-day shipping, and auto-replenishment subscriptions. Native-digital brands leverage direct data feedback loops to shorten innovation cycles, releasing limited-edition flavors tested through controlled cohorts. Retailers respond by launching marketplace models that aggregate third-party vegan listings, blurring channel boundaries.

Geography Analysis

Europe held 34% of 2024 revenue, benefiting from stringent environmental benchmarks and harmonized nutritional standards. The European Union’s Regulation 2023/2419 on organic pet food catalyzed retailer assortment shifts toward plant-based SKUs. Germany anchors continental momentum through supermarket listings of VEGDOG and private-label vegan lines, while the United Kingdom spearheads fermented-protein R&D via public-private incubators. Italy’s pet-food turnover surpassed EUR 3 billion (USD 3.2 billion) in 2023, marking double-digit dog-food expansion that feeds directly into premium vegan sublines.

North America experienced significant growth driven by initial-stage venture capital and enthusiastic support from advocates in the veterinary field. The United States saw Wild Earth reach 11% domestic share before its 2025 bankruptcy, underscoring both potential scale and capital risk. Canadian ingredient self-sufficiency improves as Louis Dreyfus Company builds a pea-protein complex in Saskatchewan in 2024, lessening reliance on the United States or Chinese concentrates. Regulatory modernization via the PURR Act could accelerate novel-ingredient clearances while diluting decentralized state oversight, creating a fluid compliance landscape.

Asia-Pacific posts the fastest 12.9% CAGR to 2030 on the back of rising disposable incomes and intense pet humanization. Chinese e-commerce giants host dedicated vegan pet-food sections, and livestream demos illustrate feeding trials to skeptics. Singapore-based manufacturers pioneer insect-based and tofu-by-product blends aimed at eco-conscious urbanites. Vietnam’s dog-food category saw 57.6% market contribution inside overall pet-food spending, and government free-trade commitments ease ingredient imports. Regional barriers include limited cold-chain logistics for wet vegan diets and nutritional label harmonization gaps.

Competitive Landscape

The vegan dog food market remains moderately fragmented as the top five companies control 35% of global revenue, which leaves meaningful growth space for well-funded challengers. V-Dog stands out with its multichannel presence that spans grocery, specialty, and e-commerce shelves. European producer Benevo follows with export-focused manufacturing that reaches more than 30 countries and benefits from rising private-label demand in German supermarkets.

Leading companies are first establishing strong regional foundations before scaling internationally. Vegdog reflects this strategy through its strong presence in supermarkets across Germany and Austria. In August 2025, OMNI gained traction in the United Kingdom market through innovative subscription models and veterinary partnerships.

White-space opportunities exist in the area of precision fermentation, with companies like Bond Pet Foods partnering with major manufacturers like Hill's Pet Nutrition to supply fermented animal proteins that maintain nutritional profiles while reducing costs in 2024. Emerging players are gaining momentum, including Czech startup Bene Meat Technologies, which achieved EU registration for cultivated pet food, and Calysta's FeedKind Pet protein, which offers scalable fermentation-based alternatives. Technology adoption is centered around improving production efficiency and developing new ingredients, with leading companies using unique product formulations, targeted retail collaborations, and subscription models to stay ahead in an increasingly competitive and fast-changing market.

Vegan Dog Food Industry Leaders

V-Dog

Benevo

Vegdog(Younikat GmbH)

Halo Pets (Garden of Vegan)

Omni Pet Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Marsapet introduced MicroBell, the first complete diet to use FeedKind Pet protein. The product carries vegan accreditation and targets allergy-prone dogs.

- November 2024: Palak Jain has launched India’s first vegan pet food brand, "Paws for Greens", pioneering a plant-based dog food option. The initiative promotes sustainable and cruelty-free nutrition, marking a milestone in India’s pet care industry.

- July 2024: The British Veterinary Association officially reversed its opposition to nutritionally adequate vegan dog diets, citing new scientific data.

Global Vegan Dog Food Market Report Scope

| Dry Kibble |

| Wet/Canned |

| Treats and Chews |

| Supplements |

| Soy-based |

| Pea and Legume-based |

| Potato and Grain-based |

| Algae and Fermentation-derived Proteins |

| Puppy |

| Adult |

| Senior |

| Small Breed |

| Medium Breed |

| Large Breed |

| Supermarkets and Hypermarkets |

| Specialty Pet Stores |

| Online Retail |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Product Type | Dry Kibble | |

| Wet/Canned | ||

| Treats and Chews | ||

| Supplements | ||

| By Ingredient Source | Soy-based | |

| Pea and Legume-based | ||

| Potato and Grain-based | ||

| Algae and Fermentation-derived Proteins | ||

| By Life Stage | Puppy | |

| Adult | ||

| Senior | ||

| By Dog Size | Small Breed | |

| Medium Breed | ||

| Large Breed | ||

| By Distribution Channel | Supermarkets and Hypermarkets | |

| Specialty Pet Stores | ||

| Online Retail | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the vegan dog food market and forecasted market size?

The vegan dog food market size reached USD 6.5 billion in 2025 and is projected to hit USD 9.8 billion by 2030.

Which region leads global sales?

Europe commanded the largest 2024 share at 34%, propelled by strict environmental rules and high consumer awareness.

Which product segment is expanding most rapidly?

Supplements show the highest forecast growth at a 12.6% CAGR through 2030, reflecting owner interest in functional add-ons.

How competitive is the market?

The top five companies hold 35% of worldwide revenue, resulting in moderate concentration and significant white-space for new entrants.

Are vegan diets clinically safe for dogs?

Peer-reviewed studies and veterinary association endorsements confirm that properly formulated vegan diets maintain normal health markers over extended periods.

What technological advances are lowering costs?

Precision fermentation produces complete animal-identical proteins, reducing reliance on costly synthetic amino acids and narrowing price gaps with conventional kibble.

Page last updated on: