Pet Food Preservatives Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 360 Million |

| Market Size (2030) | USD 534 Million |

| Growth Rate (2025 - 2030) | 6.10% CAGR |

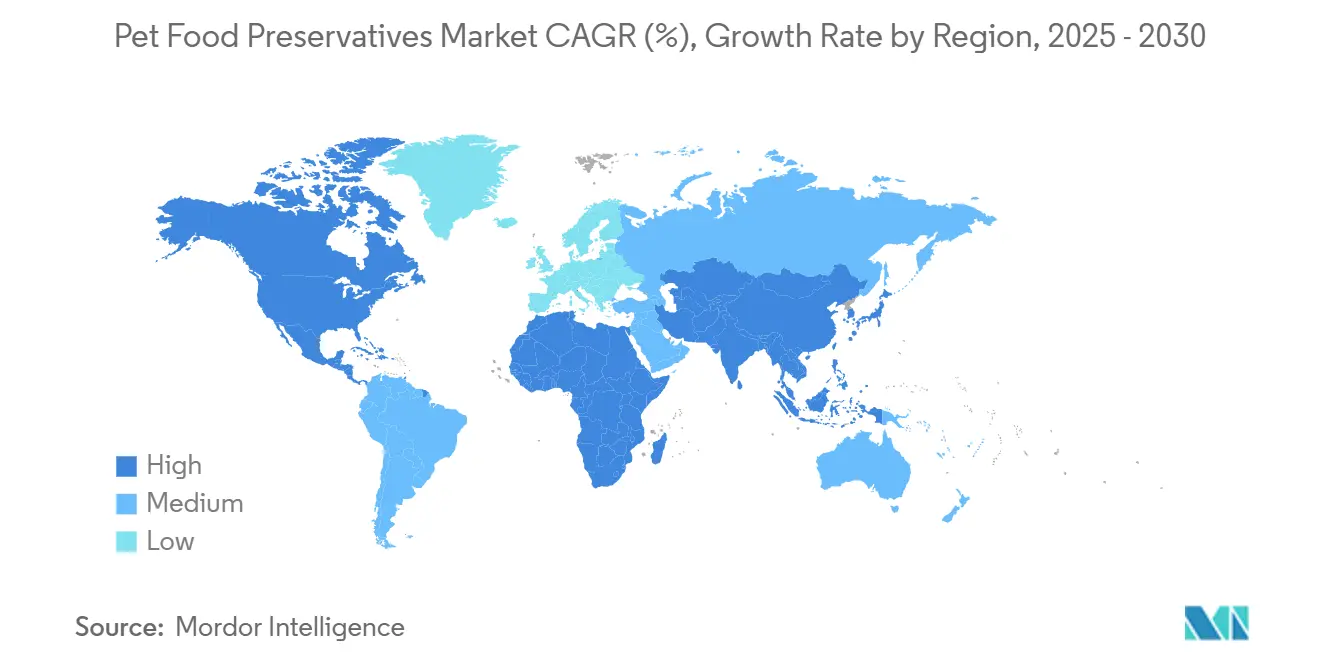

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

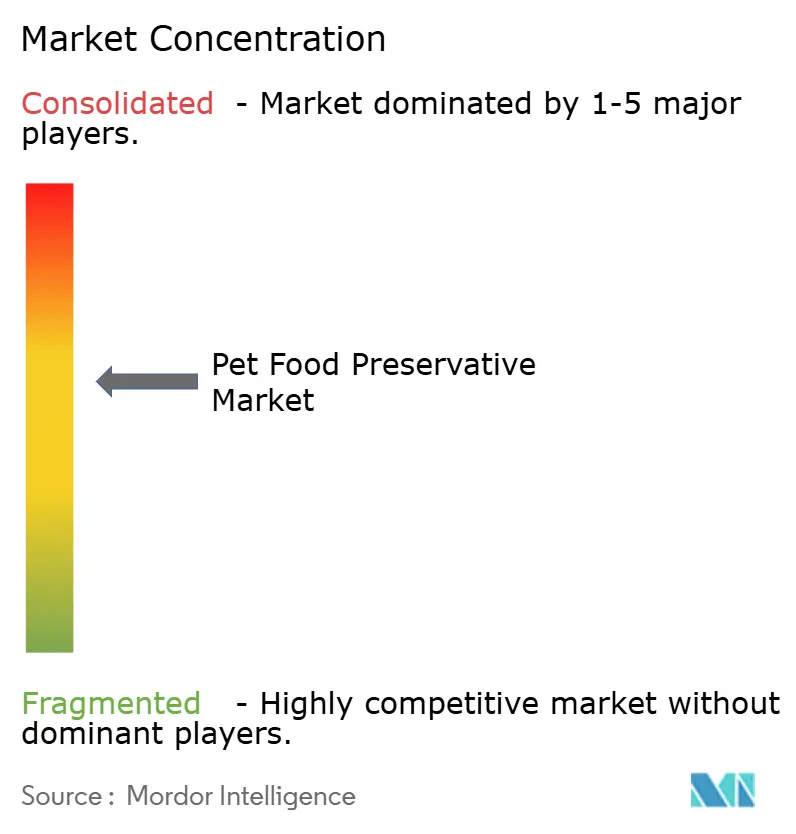

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pet Food Preservatives Market Analysis by Mordor Intelligence

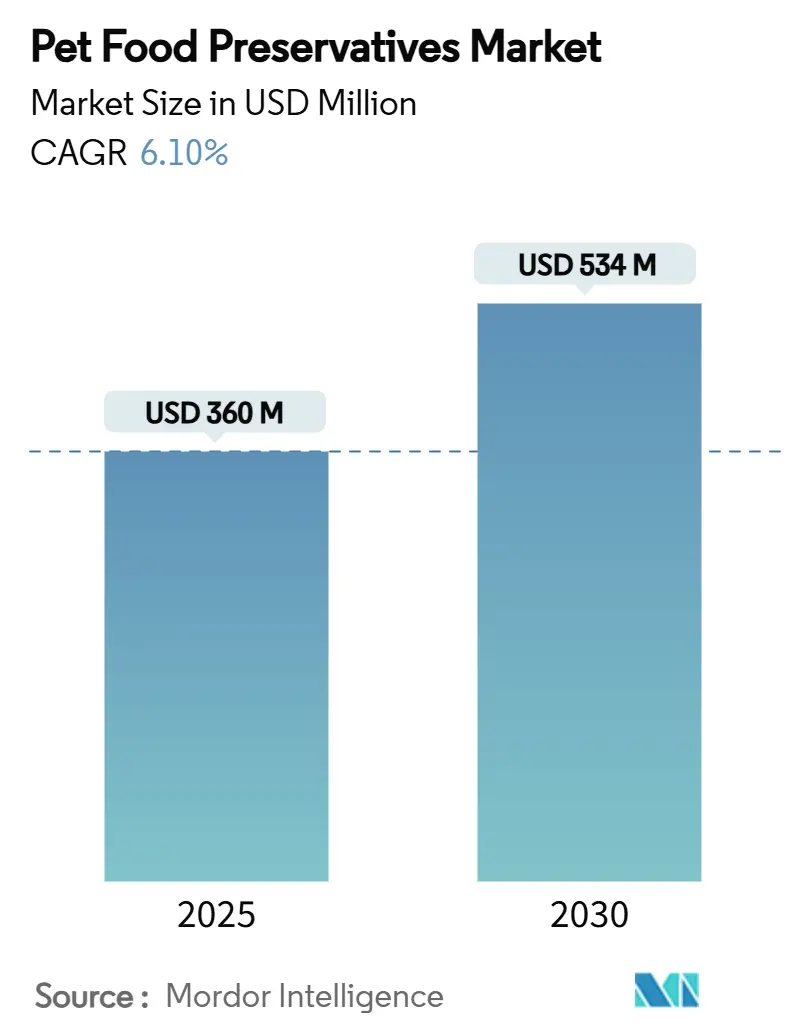

The pet food preservative market size is estimated at USD 360 million in 2025 and is projected to reach USD 534 million by 2030, registering a 6.1% CAGR over the forecast period. The expansion reflects the industry’s effort to meet rising consumer expectations for clean-label products while preserving feed safety and palatability. Demand for natural preservation systems based on rosemary extract, mixed tocopherols, and botanical antioxidants is intensifying as pet owners look for ingredient transparency that mirrors human food trends. North America retains market leadership due to its entrenched regulatory structures and high pet ownership rates, whereas the Asia-Pacific region records the fastest regional growth, driven by urbanization and premiumization. The pet food preservative market continues to balance cost-effective synthetic solutions with steady adoption of natural alternatives.

Key Report Takeaways

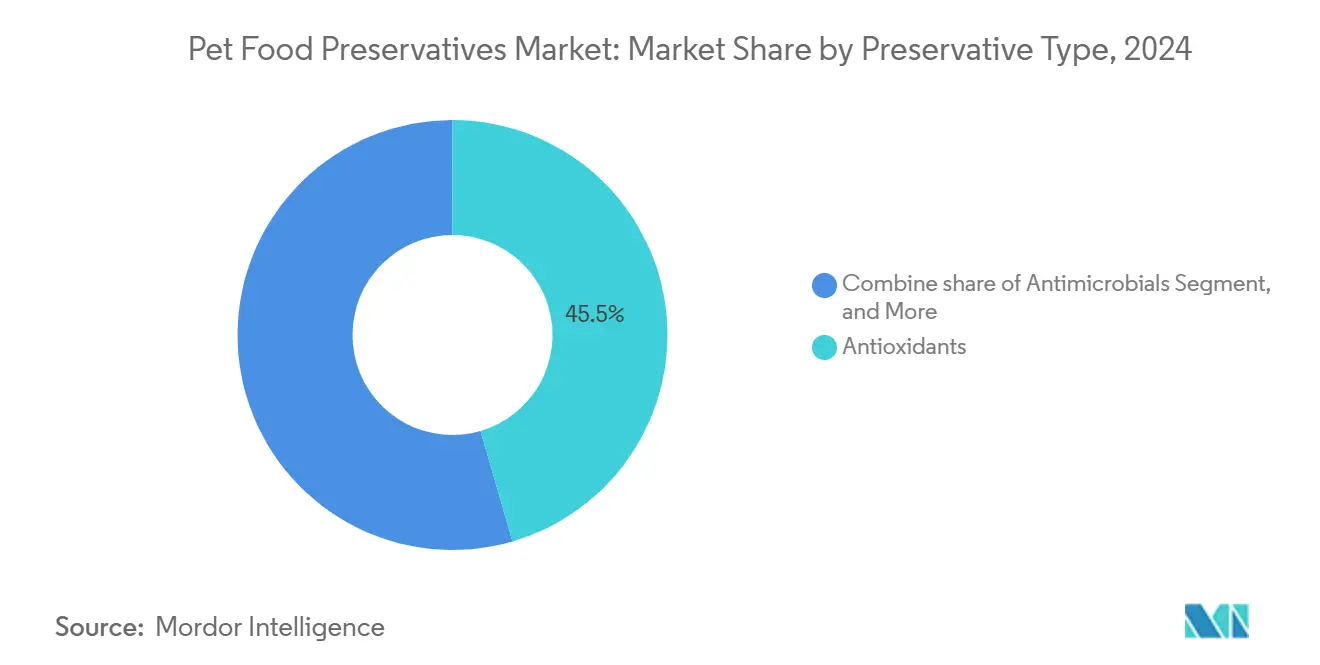

- By preservative type, antioxidants led with 45.5% pet food preservatives market size in 2024, and enzymatic preservatives posted the fastest growth at 9.0% CAGR to 2030

- By pet type, dog food commanded 56.9% of the pet food preservative market share in 2024, while the cat segment posts the fastest growth at 7.5% CAGR to 2030.

- By source, synthetic formulations retained 64.0% share of the pet food preservative market in 2024, but natural alternatives are projected to narrow the gap with a 9.0% CAGR.

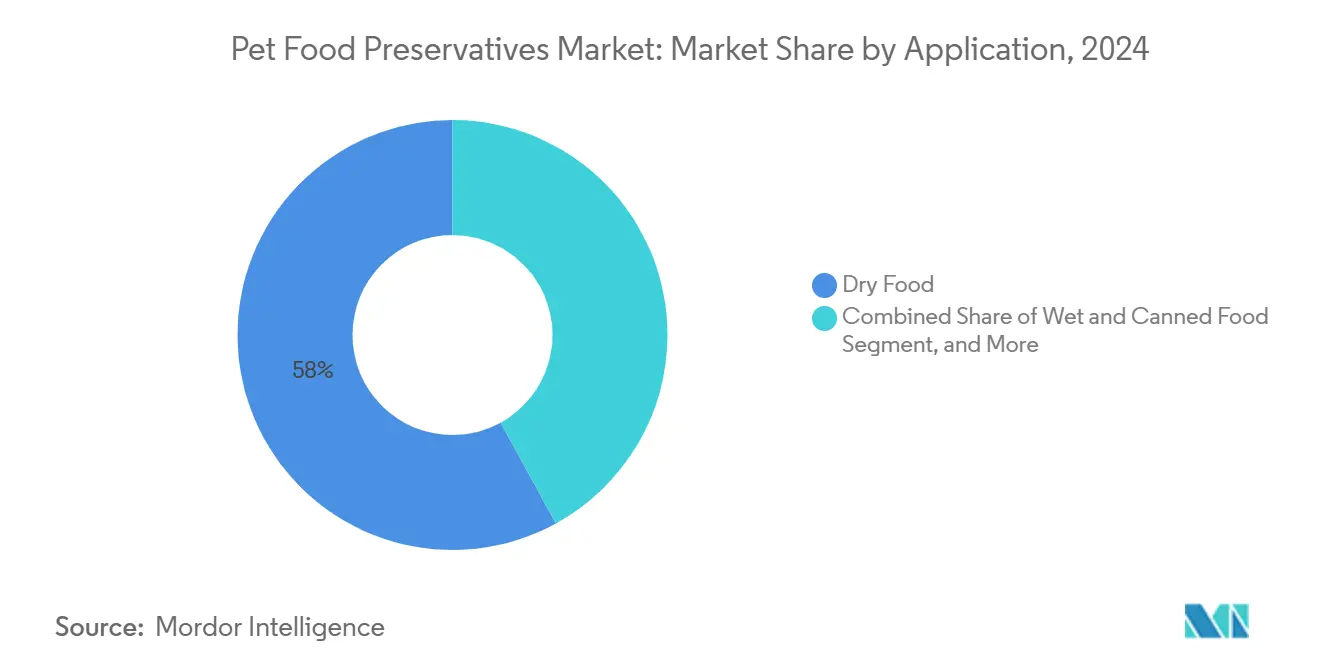

- By application, dry food captured 58% of the pet food preservative market size in 2024, whereas wet and canned formats are projected to register the highest CAGR at 8.2% through 2030.

- By geography, North America maintained a 38% share of the pet food preservative market size in 2024, and Asia-Pacific remains the fastest-growing region at 7.1% CAGR.

Global Pet Food Preservatives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Clean-label demand for preservative-free claims | +1.2% | Global with peaks in North America and Europe | Medium term (2–4 years) |

| Shift toward wet and fresh pet food formats | +0.9% | Global, strongest in developed markets | Long term (≥ 4 years) |

| Rising premiumization and functional nutrition additives | +0.8% | North America, Europe, urban Asia–Pacific | Medium term (2–4 years) |

| Retail private-label expansion needs cost-effective shelf life | +0.6% | North America and Europe | Short term (≤ 2 years) |

| Regulatory pressure limiting antibiotics as preservatives | +0.7% | Global, led by the European | Long term (≥ 4 years) |

| AI-enabled formulation for multi-hurdle preservation | +0.4% | Technology-ready developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Clean-Label Demand for Preservative-Free Claims

Consumers scrutinize ingredient panels for synthetic additives such as BHA, BHT, and ethoxyquin, accelerating the shift toward plant-based antioxidants like rosemary extract, mixed tocopherols, and green tea polyphenols. Kemin’s expansion of its NATUROX portfolio, along with FDA (Food and Drug Administration) clearance for VERDILOX rosemary extract, illustrates supplier response. European Commission authorization of rosemary extract as a feed additive validates the regulatory path for botanical solutions. Natural options often carry a two- to three-times price premium over synthetics, pressuring manufacturers to balance cost and label transparency. Brands that justify these premiums through wellness claims gain an edge in the pet food preservative market.

Shift Toward Wet And Fresh Pet Food Requiring Stronger Preservation

High-moisture diets foster microbial growth, requiring multi-hurdle strategies that blend antimicrobials, pH control, and water-activity management. Corbion’s PURAC Petfood 88 lactic acid system offers Salmonella mitigation tailored for wet formats. Fresh pet food expanded 30% in 2024 versus 2.4% for overall dog food, underscoring the opportunity. Brands deploy high-pressure processing and modified atmosphere packaging to secure shelf stability without undermining fresh positioning.

Rising Premiumization and Functional Nutrition Additives

Preservatives now serve dual roles: extending shelf life and delivering health benefits. Tocopherols and plant polyphenols double as antioxidants that support senior pets by mitigating oxidative stress. Hill’s Pet Nutrition showcased ActivBiome+ technology, integrating prebiotic blends with antioxidant systems to promote gut health. Functional preservation underpins premium price positioning and enlarges margins in the pet food preservative market.

Retail Private-Label Expansion Needs Cost-Effective Shelf-Life Solutions

Big-box and grocery chains increase their own-label penetration and push suppliers for cost-optimized preservation solutions that can meet strict quality audits. Synthetic antioxidants remain prevalent for budget lines because they deliver high performance at low inclusion rates. Nevertheless, economical mixed-tocopherol blends are surfacing, proving that even discount tiers aim to borrow cues from the wider clean-label shift.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Natural preservative cost volatility | -1.1% | Global, hardest for price-sensitive markets | Short term (≤ 2 years) |

| Allergy concerns around synthetic antioxidants | -0.7% | Developed regions with high consumer awareness | Medium term (2–4 years) |

| Stringent approval timelines for novel preservatives | -0.8% | Global, greatest in Europe and United States | Long term (≥ 4 years) |

| Supply chain fragility for rosemary and tocopherol crops | -0.9% | Global, due to concentrated source regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Natural Preservative Cost Volatility

Rosemary extract prices swing with Mediterranean crop yields, and tocopherol values track vegetable-oil markets. BASF’s July 2024 force majeure on vitamin E highlighted how single-site outages shock an already tight supply base [1]Source: BASF, “Company Information,” basf.com. Margins tighten for smaller brands lacking procurement leverage. Premium positioning remains the main offset, but sustained price spikes risk slowing natural adoption in the pet food preservative market.

Allergy Concerns Around Synthetic Antioxidants

Published toxicology studies link high exposure to BHA and BHT with hepatic stress and dermatitis in companion animals. Rising veterinary awareness is prompting reformulations, especially at the mid and high ends, where owners are more willing to pay for “free-from” labels. Regulatory reviews by the European Food Safety Authority add urgency for proactive ingredient substitution. Major United States pet retailers have begun enforcing internal ingredient blacklists that include BHA and BHT, prompting private-label suppliers to switch to natural alternatives. Pet insurance data indicate an 8% rise in dermatitis claims for dogs in 2024, a trend veterinarians partly attribute to dietary exposure to synthetic antioxidants. In response, ingredient vendors are promoting mixed-tocopherol systems that deliver oxidation control comparable to BHA and BHT at inclusion rates below 300 ppm, giving formulators a label-friendly path to maintain shelf life.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Preservative Type: Antioxidants anchor market strength while botanicals surge

Antioxidants accounted for 45.5% of the pet food preservatives market size in 2024, holding the largest share of the pet food preservative market. Lipid-rich premium diets demand robust oxidation control to safeguard omega-3 and other high-value fats. BHA, BHT, and ethoxyquin dominate the cost-sensitive dry kibble market, whereas tocopherols and rosemary offer a cleaner-label alternative for ultra-premium products.

The antimicrobial segment focuses on organic acids, including lactic, propionic, and sorbic acid, which target mold and bacterial spoilage in high-moisture diets. Corbion’s Certeza mold inhibitor demonstrates efficacy without compromising taste. Mold inhibitor adoption rises where long ocean freight spans require extended shelf stability. Enzymatic systems, although niche today, appeal to formulators seeking label simplicity, exhibiting a 9.0% CAGR growth to 2030. The lactoperoxidase system, which leverages natural enzymes and hydrogen peroxide, reflects early-stage yet promising innovation.

By Pet Type: Dogs dominate, but feline momentum accelerates

Dog diets accounted for 56.9% of the pet food preservative market share in 2024, driven by large population bases and rising pet ownership. In 2024, according to the Pet Product Association, around 68 million households in the United States own at least one dog [2]Source: American Pet Products Association, “2024–2025 National Pet Owners Survey Statistics,” americanpetproducts.org. Owners show a higher propensity to pay for vitamin-E-enriched solutions aimed at joint and coat health. Cat food, at a faster 7.5% CAGR, benefits from premium wet formats where oxidative stability in high-fat recipes is critical.

Other companion animals, such as rabbits, birds, and reptiles, constitute a small but rising niche. Species-specific sensitivities shape preservative selection, for instance, birds’ intolerance to propylene glycol. Suppliers creating micro-batch additives for exotics penetrate a greenfield sub-segment of the pet food preservative market.

By Source: Synthetic resilience meets natural ascendancy

Synthetic solutions still deliver 64.0% of 2024 revenue, owing to consistent performance and broad approval. Inclusion rates of 150 ppm deliver two-year shelf stability in dry kibble, a benchmark difficult for natural extracts to match at parity cost. The natural tier closes performance gaps through synergistic blends that combine tocopherols with chelators, such as citric acid.

Natural options are likely to grow 9.0% annually as scale economies emerge and raw material sourcing improves transparency. Novozymes’ flavor-enhancing enzyme line showcases how enzymatic systems unite preservation with palatability, underscoring functional convergence.

By Application: Dry food scale contrasts with wet food innovation.

Dry food remains the workhorse, absorbing 58% of the pet food preservative market size in 2024 because of its long shelf life and global shipment volumes. Synthetic antioxidants excel here due to heat stability during extrusion. Wet and canned diets, though smaller in volume, spur the highest R&D spending as producers strive to protect high-moisture products without high salt or sugar loads, registering the highest projected CAGR at 8.2% through 2030. Modified atmosphere packaging paired with lactic acid is becoming standard in new wet launches.

Frozen and refrigerated formats see double-digit growth driven by the humanization trend and direct-to-consumer delivery. Cold chain reliance reduces chemical preservative load but increases logistical complexity. In treats and snacks, sensory quality rules, Kemin’s PET-OX and PARAMEGA lines are engineered to maintain aroma and texture, an area where plant antioxidants deliver marketing appeal.

Geography Analysis

North America commanded 38% of the pet food preservative market size in 2024, backed by high disposable income and regulatory clarity. The United States shows brisk uptake of natural solutions, while Canada’s aligned feed standards streamline cross-border launches. Large-scale facilities, such as ADM’s new wet plant in Yecapixtla, Mexico, help regional brands localize supply and cut import reliance.

Asia-Pacific grows at 7.1% CAGR, the highest worldwide. Rising pet ownership in China and India catalyzes demand for cost-efficient oxidation control as local manufacturers move toward FSSC 22000 certification. According to the Asia Pet Research Institute, China was home to 187 million pet dogs and cats in 2024 [3]Source: Asia Pet Research Institute, “2024 China Pet Industry White Paper,” asiapet.org. China’s pet food sales reached USD 27 billion in 2024, setting the stage for preservative upgrades in domestic formulations. Japan and South Korea spearhead premiumization and thus natural antioxidant adoption.

Europe maintains steady gains supported by stringent EFSA (European Food Safety Authority) oversight that historically favors well-documented ingredients. Germany and the United Kingdom drive clean-label innovation, whereas Eastern European countries remain price sensitive. The European Union's approval of rosemary as a feed additive positions European producers to capitalize on export opportunities when other regions harmonize their regulations.

Competitive Landscape

The pet food preservative market exhibits moderate concentration. Top players include Kemin Industries, Inc., Cargill Incorporated, Corbion N.V., BASF SE, and DSM-Firmenich AG, with numerous regional specialists also thriving in the botanicals and enzymes sectors. Kemin couples its synthetic mainstays with the NATUROX natural range, utilizing vertical integration from raw herb procurement to final blend. Cargill leverages its agricultural supply reach to integrate tocopherols and emerging postbiotics.

Strategic moves center on M&A and capability expansion. Camlin Fine Sciences purchased Vitafor to boost natural antioxidant manufacturing capacity and geographic spread. White-space investment flows into AI-driven formulation services and specialty enzymatic solutions, where know-how is a durable moat. Sustainability and traceability remain differentiators as retailers audit supply chains deeper than ever.

Companies are heavily investing in research and development to create specialized pet food preservatives. Operational agility has become crucial as manufacturers expand their production capabilities through new facility construction and existing plant upgrades across multiple regions. Strategic moves predominantly focus on strengthening distribution networks through partnerships with retailers and e-commerce platforms, while also developing direct-to-consumer channels. Geographic expansion remains a key priority, with companies establishing a manufacturing presence in emerging markets and acquiring local brands to gain market access.

Pet Food Preservatives Industry Leaders

BASF SE

Corbion N.V.

DSM-Firmenich AG

Cargill, Incorporated

Kemin Industries, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: ADM’s USD 39 million investment in a wet pet food plant in Yecapixtla, Mexico, boosts local production of high-moisture formulas and drives additional demand for multi-hurdle preservatives that secure shelf life during regional distribution.

- February 2025: The Nutriment Company’s acquisition of Spain-based Puromenu broadens its reach in Europe’s fresh and raw diet segment, a category that depends on sophisticated antimicrobial and antioxidant systems to maintain safety across chilled supply chains.

- January 2025: BENEO released a tailored syrup as BeneoCarb S for pet food, broadening formulators’ options in preservation-friendly carbohydrates.

Global Pet Food Preservatives Market Report Scope

| Antioxidants |

| Antimicrobials |

| Mold Inhibitors |

| Enzymatic Preservatives |

| Dog |

| Cat |

| Other Companion Animals |

| Synthetic |

| Natural |

| Dry Food |

| Wet and Canned Food |

| Frozen and Refrigerated Food |

| Treats and Snacks |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Preservative Type | Antioxidants | |

| Antimicrobials | ||

| Mold Inhibitors | ||

| Enzymatic Preservatives | ||

| By Pet Type | Dog | |

| Cat | ||

| Other Companion Animals | ||

| By Source | Synthetic | |

| Natural | ||

| By Application | Dry Food | |

| Wet and Canned Food | ||

| Frozen and Refrigerated Food | ||

| Treats and Snacks | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How fast is the pet food preservative market anticipated to grow through 2030?

The market is forecasted to advance at a 6.1% CAGR over the forecast period, is projected to reach USD 534 million by 2030, and is likely to register USD 360 million in 2025.

Which region is registering the quickest rise in preservative demand?

Asia-Pacific posts the highest regional CAGR at 7.1% thanks to urbanization and premium pet ownership growth.

What preservative type currently commands the largest revenue share?

Antioxidants lead with 45.5% of 2024 sales because of their effectiveness in preventing lipid oxidation in fat-rich diets.

How concentrated is supplier power in this space?

The top five companies capture about 56% of revenue, reflecting moderate concentration and ongoing room for niche entrants.

What manufacturing technologies are enabling cleaner labels?

AI-driven formulation tools, high-pressure processing, and multi-hurdle systems integrating organic acids and plant antioxidants are key enablers.

Page last updated on: