Dog Food Topper Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

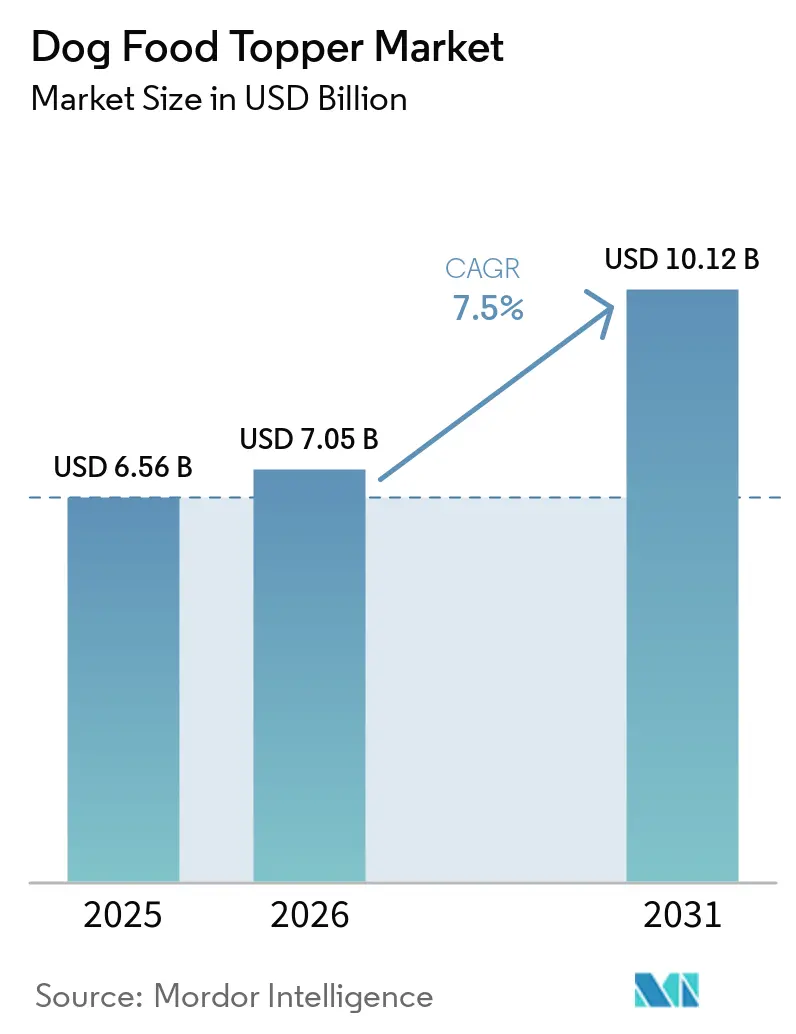

| Market Size (2026) | USD 7.05 Billion |

| Market Size (2031) | USD 10.12 Billion |

| Growth Rate (2026 - 2031) | 7.50% CAGR |

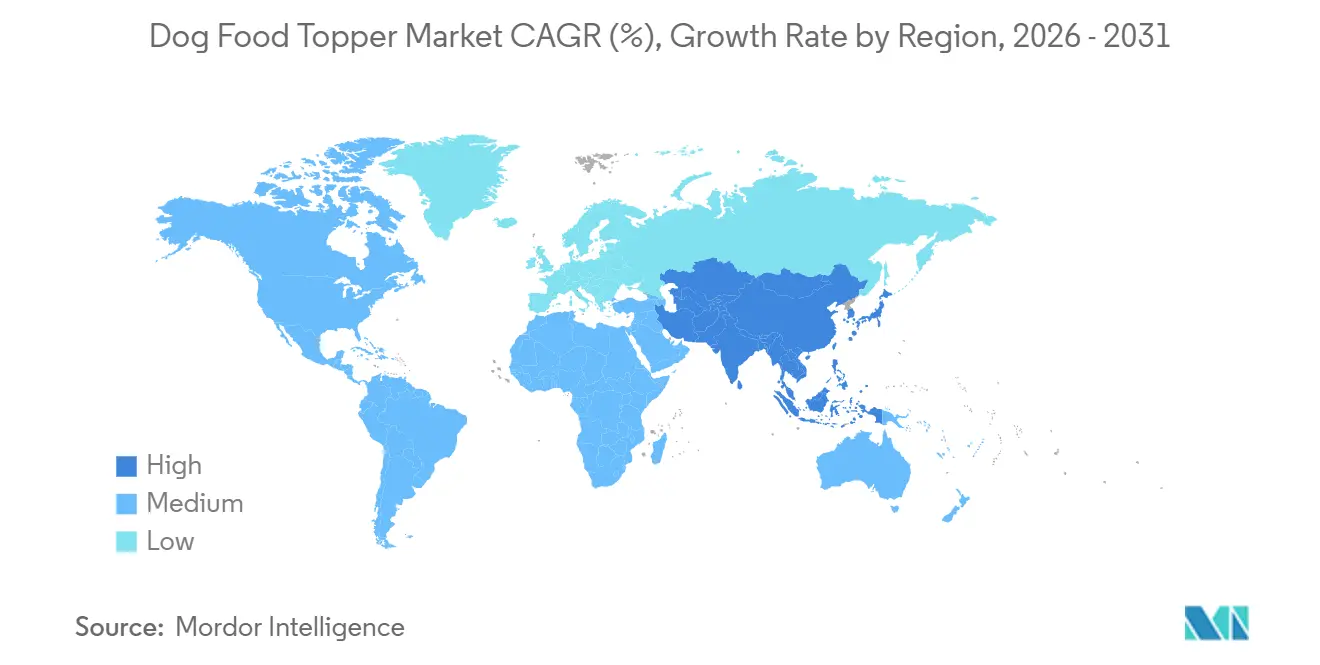

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dog Food Topper Market Analysis by Mordor Intelligence

The Dog Food Topper Market size was valued at USD 6.56 billion in 2025 and is estimated to grow from USD 7.05 billion in 2026 to reach USD 10.12 billion by 2031, at a CAGR of 7.5% during the forecast period (2026-2031). Pet owners are increasingly adding functional layers to traditional kibble rather than replacing entire meals, enabling personalization without altering established feeding routines. While dry and freeze-dried formats continue to dominate, the growing preference for liquid and fresh toppers highlights the importance of perceived freshness over shelf-life convenience. Ingredient innovation is expanding beyond traditional meats to include insects and fermentation-derived postbiotics, combining sustainability with nutritional benefits. Additionally, digital subscriptions, social commerce, and AI-driven nutrition tools are influencing brand strategies. However, fragmented regulations and high cold-chain logistics costs are moderating the market's growth pace.

Key Report Takeaways

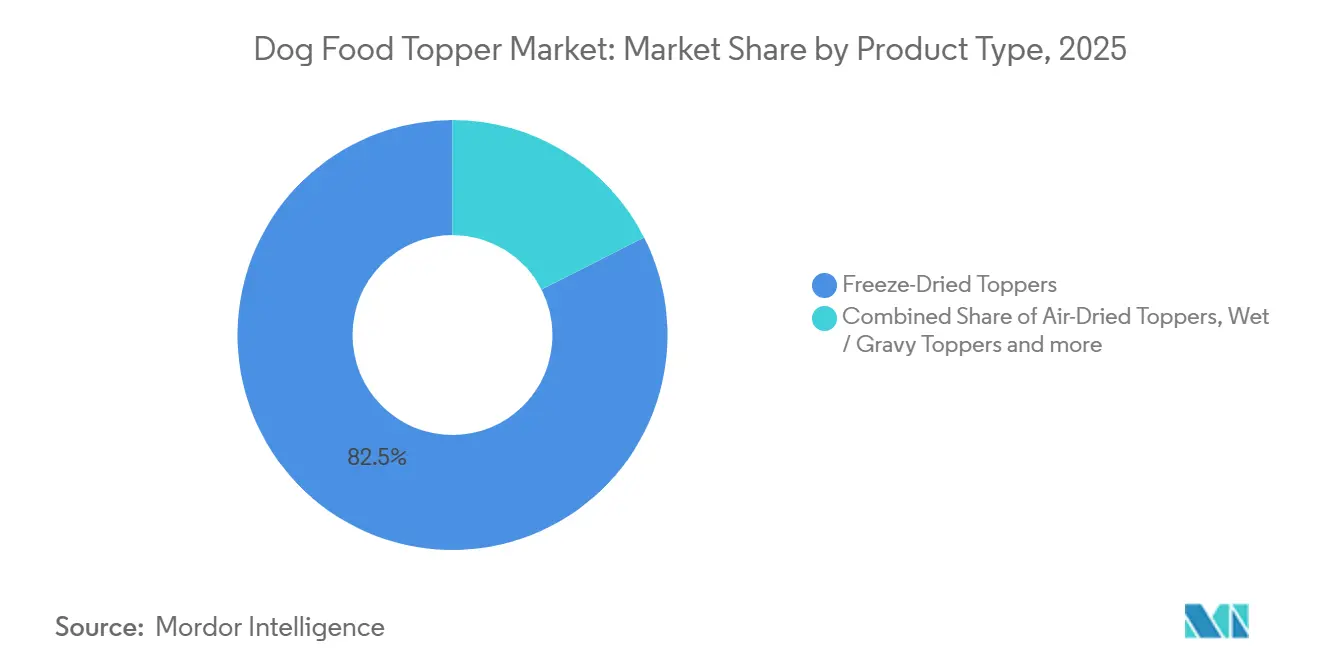

- By product type, freeze-dried toppers accounted for the largest 82.5% of the market share in 2025, and the market size is projected to achieve the fastest growth with a CAGR of 12.0% from 2026 to 2031.

- By ingredient source, animal-based proteins dominated with the largest 71.0% market share in 2025, while the insect-based proteins market size is anticipated to grow at the fastest CAGR of 14.5% from 2026 to 2031.

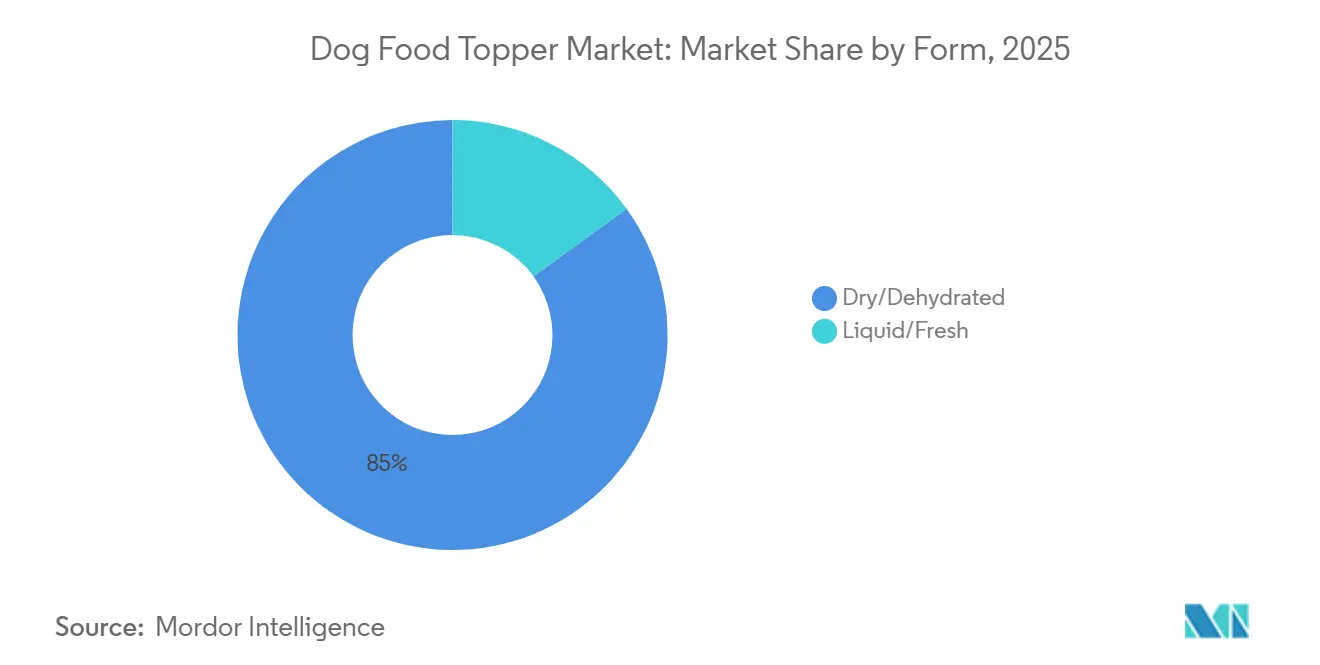

- By form, dry/dehydrated form held the largest 85% of the dog food topper market share in 2025. The liquid/fresh form market size is projected to grow at the fastest CAGR of 10.3% from 2026 to 2031.

- By distribution channel, pet specialty stores accounted for the largest 23.9% of the dog food topper market share in 2025. The online retail and direct-to-consumer market size is forecast to expand at the fastest CAGR of 18.0% from 2026 to 2031.

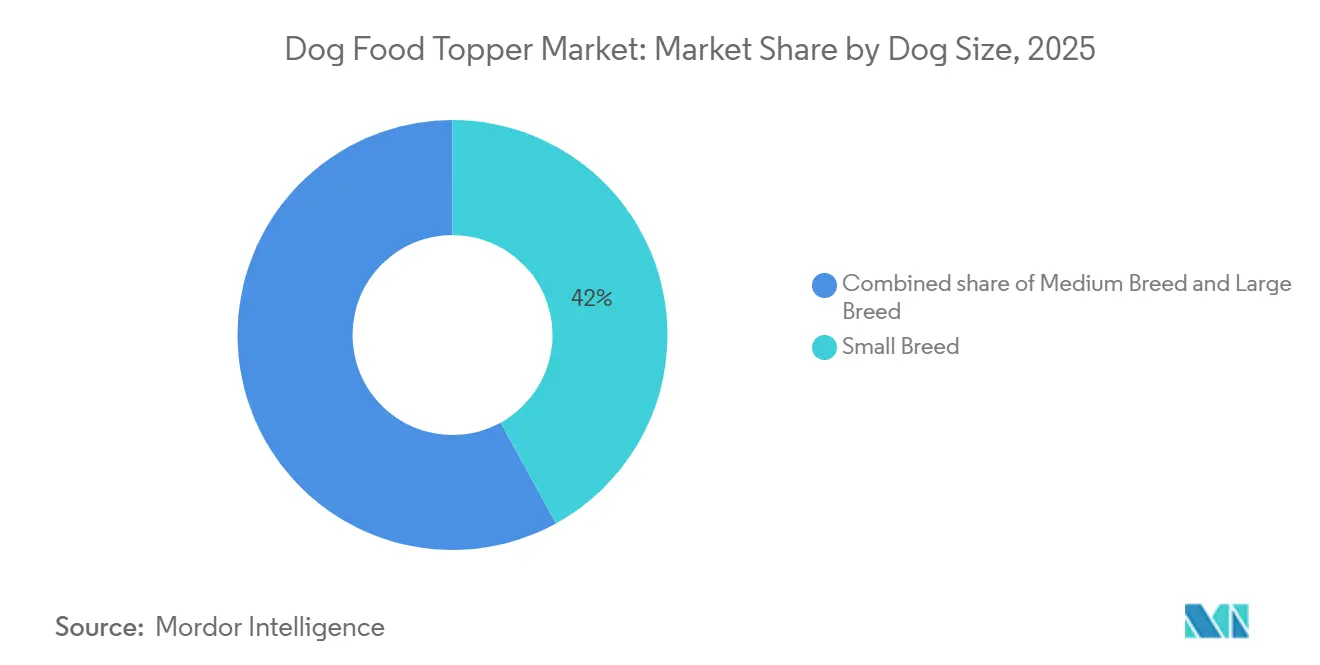

- By dog size, small breeds accounted for the largest 42.0% of the dog food topper market share in 2025, and the market size is projected to grow at the fastest CAGR of 9.0% from 2026 to 2031.

- By geography, North America led the market with a 38.0% of the dog food topper market share in 2025, while the Asia-Pacific market size is projected to grow at the fastest CAGR of 11% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Dog Food Topper Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumization of pet diets | +1.8% | Global, led by North America and Europe | Medium term (2-4 years) |

| Surge in freeze-dried and raw-inspired formats | +1.5% | North America, Europe, and Asia-Pacific urban centers | Short term (≤ 2 years) |

| Rising pet obesity driving functional toppers | +1.2% | North America and Europe | Medium term (2-4 years) |

| Growing adoption of direct-to-consumer subscription models | +1.4% | Global, core in North America and Asia-Pacific | Short term (≤ 2 years) |

| AI-enabled personalized nutrition algorithms | +0.9% | North America, Europe, and early Asia-Pacific adoption | Long term (≥ 4 years) |

| Fermentation-derived postbiotic additions for gut health | +0.7% | Global, regulatory momentum in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Premiumization of Pet Diets

Pet owners are allocating more resources to premium dog food toppers that prioritize human-grade ingredients, transparency, and functional health benefits, driven by the rising trend of pet humanization. Millennials and Generation Z together represent approximately 57% of pet ownership, playing a significant role in driving demand for high-quality and specialized pet nutrition products. [1]Source: American Pet Products Association (APPA), Pet Ownership Statistics; Pet Age, Gen Z and Millennial Pet Ownership Trends, petage.com. Brands are focusing on aspects such as product provenance, recyclable packaging, and visible ingredient inclusions to enhance feeding experiences. The willingness to pay a premium stems from the perception of customization while retaining core kibble products. Growth is most rapid in North America and Europe, with a rising trend in the Asia-Pacific region as urban consumers adopt premium human-food-inspired habits.

Surge in Freeze-Dried and Raw-Inspired Formats

Freeze-dried toppers have transitioned from niche treats to mainstream enhancements, offering raw-like nutrition without the need for refrigeration. These toppers appeal to pet owners due to their ability to retain nutrients and provide texture variety, which encourages repeat purchases. Additionally, air-dried hybrid options are gaining traction as they help reduce energy costs during production. The increasing availability of these formats in mass retail stores highlights their growing acceptance among consumers. This trend is significantly contributing to the expansion of the dog food topper market, as more pet owners seek convenient and nutritious meal enhancements for their pets.

Rising Pet Obesity Driving Functional Toppers

The growing prevalence of pet obesity is driving demand for functional toppers containing ingredients like glucosamine, omega-3 fatty acids, and fiber to aid in weight management and joint health. According to the Association for Pet Obesity Prevention, around 59% of dogs in the United States were classified as overweight or obese in 2022, underscoring the magnitude of the issue and the need for specialized nutritional solutions. Veterinarians frequently recommend functional toppers as an effective method to enhance diet quality without altering the primary food, allowing for controlled portion sizes and additional health benefits.

Growing Adoption of Direct-to-Consumer Subscription Models

Direct online sales offer recurring revenue, detailed data insights, and improved profit margins for challenger brands. The global direct-to-consumer pet food market is fueled by increasing consumer demand for convenience, customization, and premium-quality pet food options. Subscription models are particularly suited for lightweight freeze-dried or powdered toppers, which are cost-effective to ship. These products not only reduce shipping expenses but also align with the preferences of pet owners seeking practical and nutritious feeding solutions for their pets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pricing premium versus conventional kibble | −1.1% | Global, highest price sensitivity in emerging markets | Short term (≤ 2 years) |

| Regulatory uncertainty on novel ingredients | −0.8% | Europe, Asia-Pacific, select South American markets | Medium term (2-4 years) |

| Cold-chain cost for fresh/liquid toppers | −0.6% | Global, infrastructure gaps in Asia-Pacific and Africa | Medium term (2-4 years) |

| Limited palatability data for insect protein | −0.5% | Global, strongest resistance in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Pricing Premium versus Conventional Kibble

The price disparity between premium dog food toppers and conventional kibble remains a significant restraint in the dog food topper market. Toppers are often considerably more expensive than traditional dry kibble, limiting both trial and repeat purchases among cost-sensitive households. According to the American Pet Products Association, U.S. pet food spending surpassed USD 64 billion in 2023, but a large portion of this spending is still directed toward conventional dry food due to its affordability [2]Source: American Pet Products Association (APPA), “U.S. Pet Industry Reaches $147 Billion in Sales in 2023,” americanpetproducts.org. While toppers are marketed as premium dietary additions for pets, their high cost poses a barrier to broader adoption.

Regulatory Uncertainty on Novel Ingredients

Insects, cultivated meat, and specific postbiotics face varying approval timelines across different regions, which slows down product rollouts and creates an advantage for companies with significant compliance resources. These delays often result from complex regulatory frameworks and differing safety standards in each market. To navigate these challenges, brands typically adopt a phased approach by launching their products in the United States first, where regulatory pathways may be more streamlined. Once approvals are obtained in other regions, they expand their operations, ensuring compliance with local regulations and minimizing potential risks associated with premature market entry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Freeze-Dried Leads Premium Adoption

Freeze-dried toppers accounted for the largest 82.5% of the dog food topper market share in 2025, and the market size is projected to achieve the fastest growth with a CAGR of 12.0% from 2026 to 2031. This segment benefits from attributes such as raw-like nutrition, ambient storage, and ease of functional fortification. Hybrid air-dried inclusions offer reduced processing energy requirements and expanded pricing options. Liquid gravies and bone broths' growth is driven by their hydration and joint support benefits, although their reliance on refrigeration limits their market penetration. Powdered seasonings provide a cost-effective entry point but require consumer education on proper reconstitution methods.

Freeze-dried brands are differentiating through protein variety and visible chunks designed to appeal to canine sensory preferences. Examples include West Paw’s postbiotic-fortified cubes and Stella and Chewy’s raw-coated kibble, reflecting the trend of combining health benefits with enhanced texture. Liquid product lines focus on ingredients such as collagen, glucosamine, and electrolytes, while innovations like bone broth drum-pouch packaging improve shelf visibility. As manufacturers continue to innovate, format selection increasingly emphasizes balancing freshness perception, cost efficiency, and shipping durability, contributing to greater competitive diversity within the dog food topper market.

By Ingredient Source: Insects Accelerate Share Gains

Animal-based proteins accounted for the largest 71.0% of the dog food topper market share in 2025, while the insect-based proteins market size is anticipated to grow at the fastest CAGR of 14.5% from 2026 to 2031, following the approval of dried mealworm meal in the United States. Key drivers of this growth include rising consumer interest, environmental benefits, and high digestibility. These factors are encouraging experimentation within the market. Meanwhile, plant-based proteins address hypoallergenic needs but require amino acid fortification to meet nutritional standards, limiting their standalone use in dog food toppers.

Ynsect's expansion initiatives in France and Mexico, along with Tyson's investment in Protix, are contributing to increased insect protein availability. Research highlights that black soldier fly larvae have limitations in palatability at higher inclusion levels, guiding blend ratios in formulations. Manufacturers are strategically integrating insect, animal, and plant-based ingredients to achieve a balance between flavor, cost, and sustainability. This strategy addresses consumer preferences while enhancing the resilience of raw material sourcing, ensuring a stable supply and adaptability in the evolving dog food topper market.

By Form: Liquids Rise Despite Cold-Chain Barriers

Dry/dehydrated form held the largest 85% of the dog food topper market share in 2025. This highlights the ongoing preference for convenience, ambient storage, and easy integration with existing kibble, as noted by. Retail offerings prominently feature freeze-dried cubes, seasoning powders, and raw-coated kibble, which enable premium positioning without requiring refrigeration. Attributes such as visible inclusions, crunchy textures, and human-grade labeling enhance perceived value while maintaining a competitive cost per serving. This market dominance also provides manufacturers with scale efficiencies, supporting investments in emerging fresh and liquid topper formats globally.

The liquid/fresh forms market size is projected to grow at the fastest CAGR of 10.3% from 2026 to 2031. This growth is driven by increasing demand for hydration, enhanced aroma, and soft textures that appeal to senior or selective dogs. General Mills’ upcoming refrigerated Blue Buffalo Company, Ltd. range in 2026 reflects confidence in chilled offerings, despite the added costs associated with cold-chain logistics. To address economic challenges, brands are introducing shelf-stable bone-broth pouches, concentrated drizzles, and functional beverages enriched with collagen, electrolytes, and postbiotics.

By Distribution Channel: Digital Disrupts Margin Models

Pet speciality stores accounted for the largest 23.9% of the dog food topper market share in 2025, highlighting the role of knowledgeable staff and curated product assortments in driving premium product discovery. Features such as in-store tastings and transparent packaging enable customers to evaluate texture, aroma, and ingredient quality directly, fostering trust in innovative products like insect-based proteins or postbiotic-coated options. Additionally, shelf arrangements often position toppers near treats rather than base diets, creating an impulse-buy area that increases basket value.

The online retail and direct-to-consumer channels market size is forecast to expand at the fastest CAGR of 18.0% from 2026 to 2031, making it the fastest-expanding distribution channel. Subscription bundles streamline product replenishment while generating first-party data that companies use to develop personalized promotions and dynamic product formulations. Social commerce, often driven by pet influencers, reduces advertising costs and appeals to millennials and Generation Z consumers who prioritize convenience through doorstep delivery.

By Dog Size: Small Breeds Propel Premium Spend

Small breeds accounted for the largest 42.0% of the dog food topper market share in 2025, emphasizing their significance as a focus area for premium product innovation. Their lower calorie requirements make per-meal topper spending more manageable, allowing owners to select options such as freeze-dried inclusions, collagen broths, or insect proteins without surpassing budget limitations. This trend corresponds with broader pet ownership patterns, as the American Veterinary Medical Association reported that the U.S. dog population reached approximately 87.3 million in 2025, with an average of 1.6 dogs per household [3]Source: American Veterinary Medical Association (AVMA), “U.S. Pet Ownership Statistics / Pet Ownership and Demographics Sourcebook,” avma.org.. This indicates a substantial base of pet owners adopting portion-controlled and premium feeding solutions.

The market size for small breed is projected to grow at the fastest CAGR of 9.0% from 2026 to 2031, outpacing the growth rates of medium and large breeds and reinforcing their importance in growth strategies. Brands are focusing on developing lower-density topper formulations enriched with omega-3 fatty acids, joint supplements, and postbiotics to align with veterinary recommendations for weight management and gut health. Shopping applications with portion calculators simplify compliance by converting body-weight goals into precise topper quantities. While medium-sized dogs exhibit steady adoption of toppers, large breeds tend to prefer value-sized tubs.

Geography Analysis

North America led the market with a 38.0% of the dog food topper market share in 2025, driven by advanced pet humanization trends and higher disposable income levels. Pet owners in the region increasingly treat their pets as family members, leading to a growing demand for premium and specialized dog food toppers. The region is witnessing increased adoption of direct-to-consumer subscriptions and freeze-dried formats, as consumers prioritize convenience, shelf stability, and functional benefits such as enhanced nutrition and digestibility. North America is leading the way in testing fresh and cultivated meat toppers, supported by clear regulations that encourage innovation.

The Asia-Pacific market size is projected to register the fastest CAGR of 11% from 2026 to 2031, fueled by urban millennials in countries like China and Japan who align their pets' diets with personal wellness trends. This demographic is increasingly willing to spend on high-quality, health-focused pet food products, reflecting their own lifestyle choices. The rising adoption of e-commerce platforms has simplified access to dog food toppers, offering a wide range of options to consumers in both urban and rural areas. However, fragmented regulations surrounding insects and cultivated proteins necessitate localized compliance strategies, as brands must navigate varying legal frameworks across countries.

Europe's stringent novel-food regulations are shaping a cautious approach to the introduction of insect-based and cell-based ingredients. These regulations ensure consumer safety but also slow down the pace of innovation in the market. Sustainability labels and organic certifications strongly appeal to consumers, as environmental concerns and ethical considerations increasingly influence purchasing decisions. This has driven demand for low-carbon protein options, such as insect-based and plant-based toppers, which align with the region's focus on reducing environmental impact.

Competitive Landscape

The dog food topper market was moderately concentrated in 2025, with the top five key players including Mars, Incorporated, Nestle Purina PetCare Company, WellPet LLC, Blue Buffalo Company, Ltd., and Stella & Chewy's, LLC. These companies maintain diverse product portfolios, including dry, freeze-dried, and emerging liquid toppers. Mars, Incorporated utilizes its extensive pet-care infrastructure to enhance shelf placement for products with functional benefits, while Nestle Purina PetCare Company’s 9 Square Ventures focuses on early-stage technologies, such as AI-driven personalization, to sustain innovation.

Opportunities are emerging in areas such as AI-enabled personalized nutrition, cultivated meat toppers, and hybrid formats that combine freeze-dried inclusions with extruded kibble, offering raw-like attributes without the need for cold-chain logistics. Smaller competitors are challenging established players by adopting direct-to-consumer models, which eliminate retailer margin pressures and enable the collection of first-party data. This approach allows for faster adjustments to formulations and packaging based on consumer feedback.

Competitive intensity is highest in North America and Europe, where retail shelf space is limited, and digital marketing costs are increasing. In contrast, the Asia-Pacific region presents growth opportunities for brands capable of navigating complex regulatory environments and establishing local distribution partnerships. Market consolidation is projected as larger companies acquire digitally native brands to gain access to innovation and direct-to-consumer capabilities. Meanwhile, smaller players are focusing on niche markets, emphasizing novel proteins, functional benefits, and sustainability-focused narratives.

Dog Food Topper Industry Leaders

Mars, Incorporated

Nestle Purina PetCare Company

WellPet LLC

Blue Buffalo Company, Ltd.

Stella & Chewy's, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Stella & Chewy's, LLC's introduced over 80 SKUs, including meals, toppers, freeze-dried raw-coated kibble, and treats, across PetSmart stores nationwide in the United States. This expansion aims to provide a wider variety of high-quality pet food options to customers, catering to diverse dietary needs and preferences for pets.

- May 2025: Natoo Pet Foods Ltd. expanded its Meal Topper range by introducing four new flavors, including Salmon with Pumpkin in Broth and Chicken with Carrot and Brown Rice. This expansion addresses the increasing demand for premium and functional toppers that enhance flavor while offering additional nutritional benefits. Ingredients such as pumpkin and brown rice are included to support digestive health, appealing to pet owners seeking healthier and more varied feeding options.

- May 2024: Mars, Incorporated has announced an investment exceeding €130 million (USD 141.2 million) in its manufacturing operations in France. This investment is aimed at increasing production capacity and fostering innovation in pet nutrition, particularly in premium and functional products. The initiative is projected to improve supply capabilities and facilitate the development of value-added products, such as specialized dog food toppers, aligning with the rising preference for high-quality and customized pet diets.

Global Dog Food Topper Market Report Scope

Dog food toppers are supplementary products added to a dog's regular meals to enhance flavor, texture, and nutritional value. These products aim to improve palatability, address specific health requirements, and promote better eating habits without substituting the primary diet. The dog food topper market report is segmented by product type (freeze-dried toppers, air-dried toppers, wet/gravy toppers, bone broth toppers, powdered/seasoning toppers, and functional and supplement-infused toppers), by ingredient source (animal-based protein, plant-based protein, insect-based protein, and mixed/hybrid proteins), by form (dry/dehydrated and liquid/fresh), by distribution channel (supermarkets and hypermarkets, pet specialty stores, veterinary clinics, and online retail and direct-to-consumer), by dog size (small breed, medium breed, and large breed), and by geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The market forecasts are provided in terms of value (USD).

| Freeze-Dried Toppers |

| Air-Dried Toppers |

| Wet/Gravy Toppers |

| Bone Broth Toppers |

| Powdered/Seasoning Toppers |

| Functional and Supplement-Infused Toppers |

| Animal-Based Protein |

| Plant-Based Protein |

| Insect-Based Protein |

| Mixed/Hybrid Proteins |

| Dry/Dehydrated |

| Liquid/Fresh |

| Supermarkets and Hypermarkets |

| Pet Specialty Stores |

| Veterinary Clinics |

| Online Retail and Direct-to-Consumer |

| Small Breed |

| Medium Breed |

| Large Breed |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Product Type | Freeze-Dried Toppers | |

| Air-Dried Toppers | ||

| Wet/Gravy Toppers | ||

| Bone Broth Toppers | ||

| Powdered/Seasoning Toppers | ||

| Functional and Supplement-Infused Toppers | ||

| By Ingredient Source | Animal-Based Protein | |

| Plant-Based Protein | ||

| Insect-Based Protein | ||

| Mixed/Hybrid Proteins | ||

| By Form | Dry/Dehydrated | |

| Liquid/Fresh | ||

| By Distribution Channel | Supermarkets and Hypermarkets | |

| Pet Specialty Stores | ||

| Veterinary Clinics | ||

| Online Retail and Direct-to-Consumer | ||

| By Dog Size | Small Breed | |

| Medium Breed | ||

| Large Breed | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How fast will the dog food topper market grow through 2031?

It is forecast to advance at a fastest 7.5% CAGR between 2026 and 2031 to reach to reach USD 10.12 billion by 2031 as owners layer functional additions onto core kibble.

Which product format is gaining the most share?

Freeze-dried toppers are expanding at fastest 12.0% CAGR from 2026 to 2031 because they deliver raw-like nutrition without refrigeration.

What drives insect protein adoption in canine toppers?

Association of American Feed Control Officials approval, 80%-plus digestibility, and lower environmental impact support a fastest 14.5% CAGR from 2026 to 2031 for insect proteins.

Why are small-breed dogs important for premium toppers?

Lower calorie needs make premium servings affordable, so small dogs account for 42.0% of consumption and grow at 9.0% CAGR.

How is e-commerce reshaping channel dynamics?

Online and direct-to-consumer sales are growing at a fastest 18.0% CAGR from 2026 to 2031 by offering subscriptions, data insights, and bypassing retailer fees.

Page last updated on: