United States Pet Veterinary Diet Market Size and Share

Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

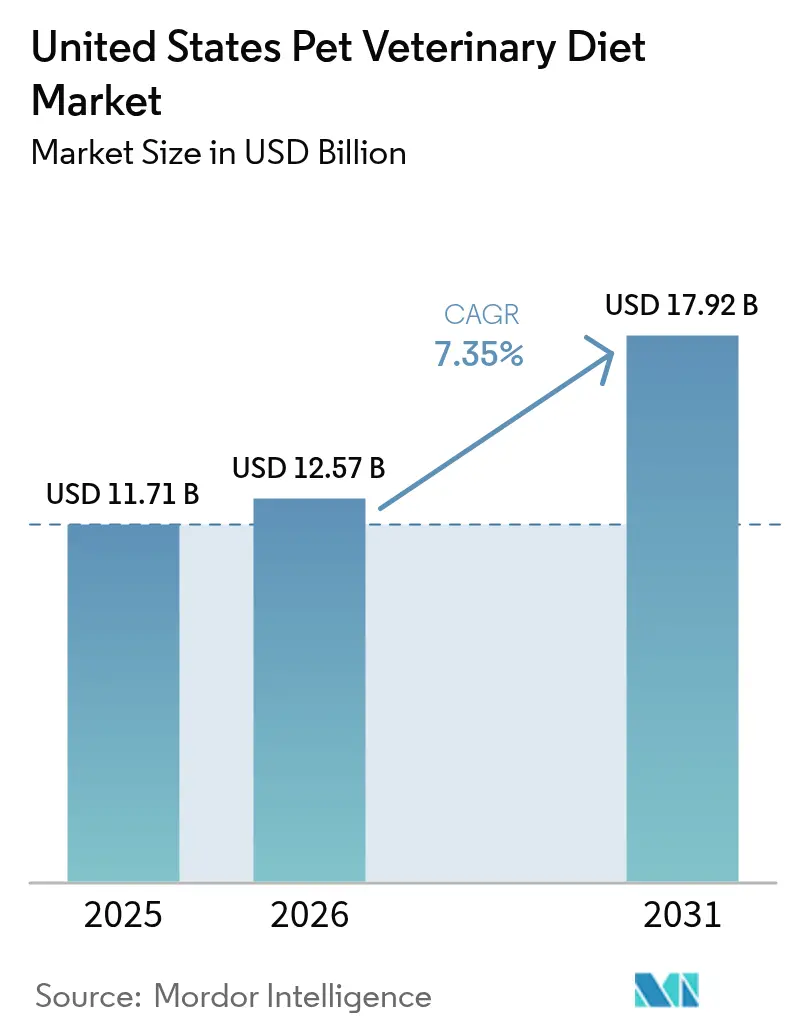

| Base Year Market Size (2025) | USD 11.71 Billion |

| Market Size (2026) | USD 12.57 Billion |

| Market Size (2031) | USD 17.92 Billion |

| Growth Rate (2026 - 2031) | 7.35% CAGR |

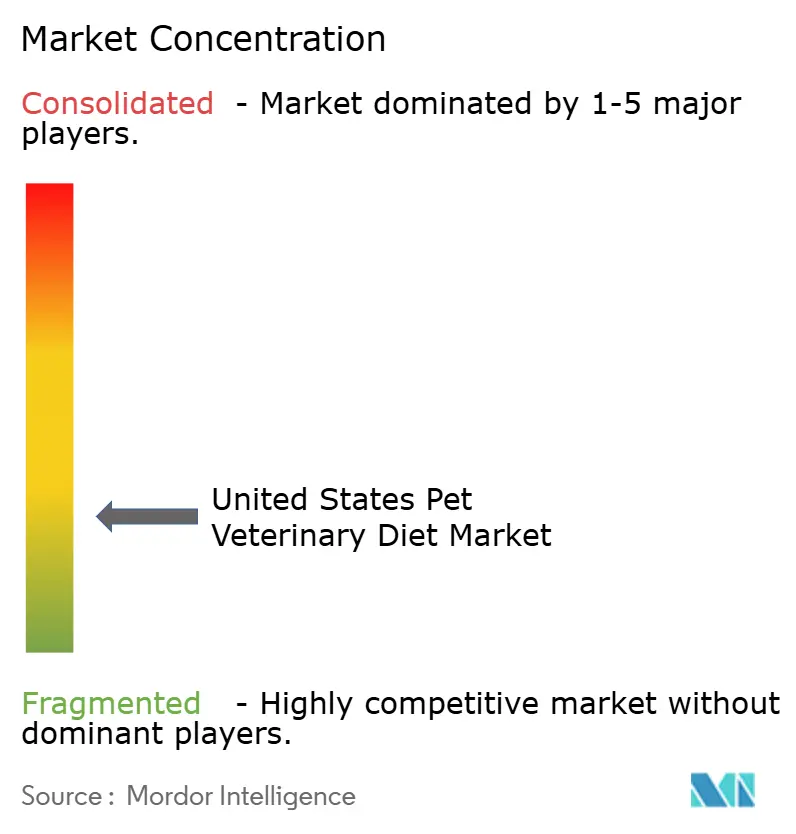

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Pet Veterinary Diet Market Analysis by Mordor Intelligence

The United States pet veterinary diet market size is expected to grow from USD 11.71 billion in 2025 to USD 12.57 billion in 2026 and is forecast to reach USD 17.92 billion by 2031 at 7.35% CAGR over 2026-2031. The growing prevalence of gastrointestinal disorders, wider pet insurance coverage, and algorithm-supported prescription tools within veterinary practices are driving demand for therapeutic diets. Premiumization remains steady despite inflation as owners prioritize clinically validated nutrition over conventional pet food. Digital fulfillment programs embedded in practice management software are boosting compliance, while tighter Food and Drug Administration (FDA) claim-validation rules are raising the innovation bar for manufacturers.

Key Report Takeaways

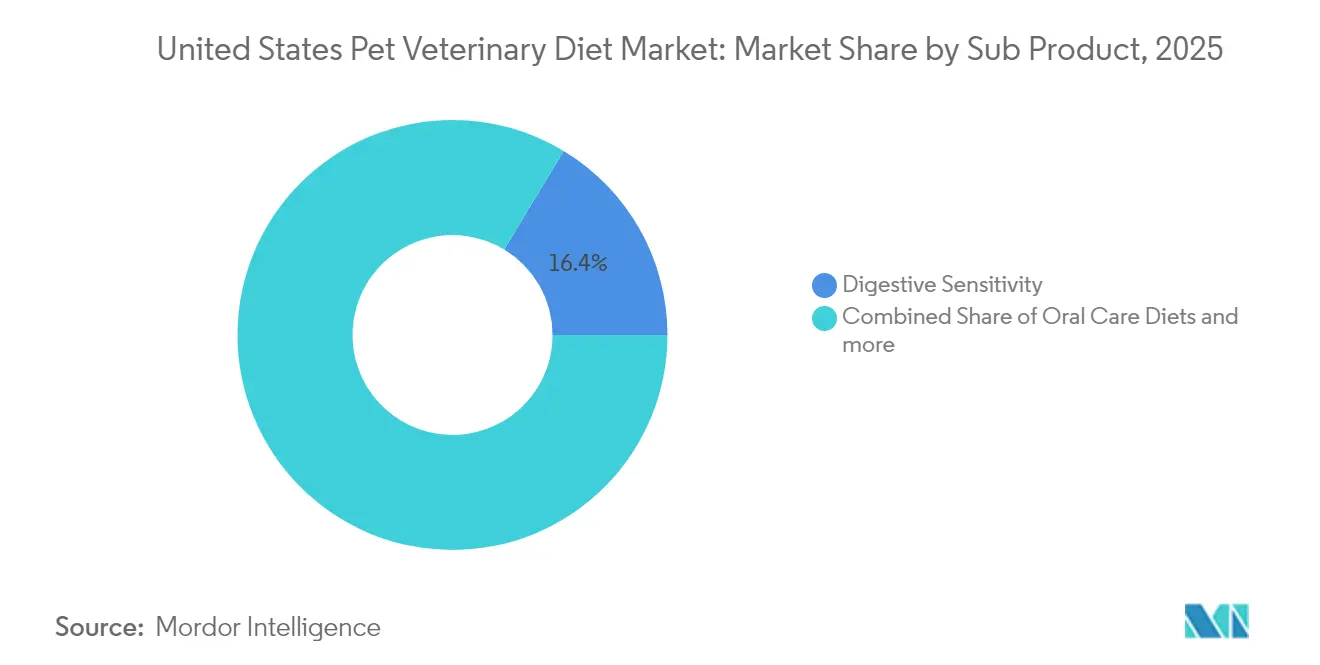

- By sub-product, digestive sensitivity diets captured 16.35% of the United States pet veterinary diet market share in 2025. Oral care diets are advancing at a 8.85% CAGR through 2031, the fastest pace among sub-product categories.

- By pet type, dogs held a 55.60% share of the United States pet veterinary diet market size in 2025 and are projected to expand at a 9.05% CAGR.

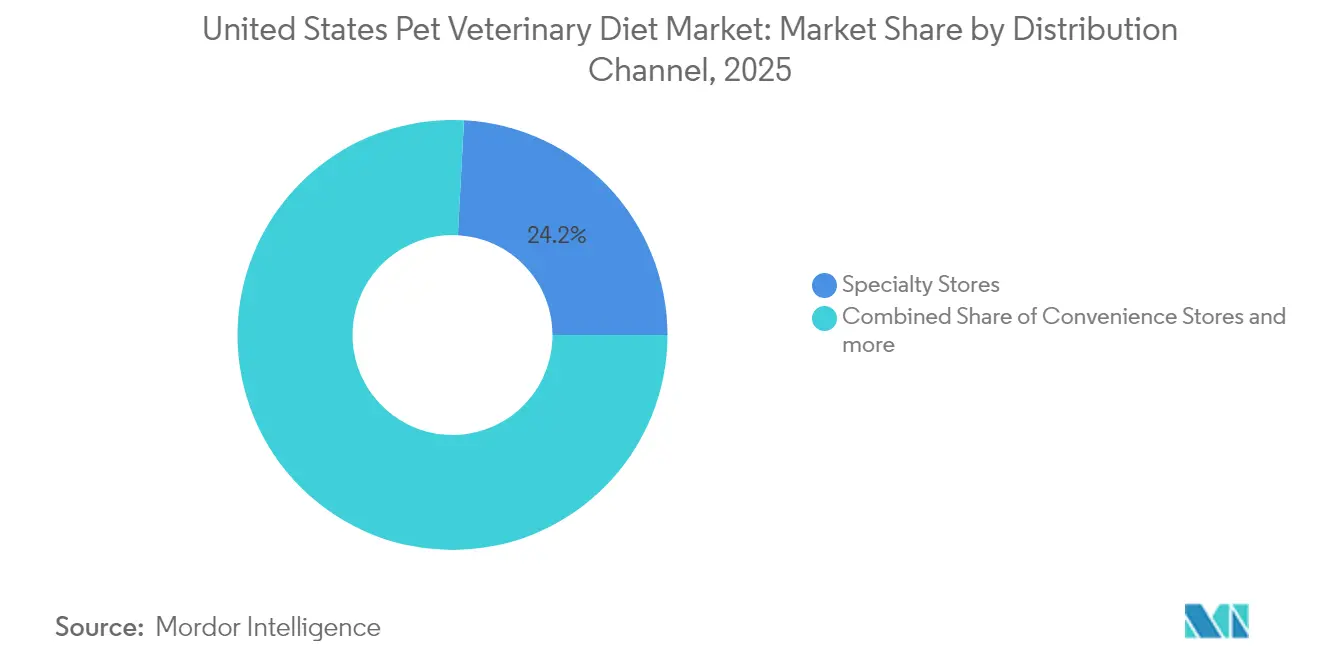

- By distribution channel, specialty stores led the distribution with a 24.15% of the United States pet veterinary diet market share in 2025, while convenience stores recorded the highest projected CAGR of 8.95% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Pet Veterinary Diet Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Gastrointestinal Disorders Lead Veterinary Diagnoses | +1.8% | National, with concentration in urban metropolitan areas | Medium term (2-4 years) |

| Rapid Premiumization in Pet Specialty Retail | +1.5% | National, strongest in Northeast and West Coast regions | Short term (≤ 2 years) |

| Veterinarian-Driven Subscription E-commerce Programs | +1.2% | National, with early adoption in tech-forward states | Medium term (2-4 years) |

| Algorithmic Diet-Matching Tools Inside Practice Software | +1.0% | National, concentrated in larger veterinary practices | Long term (≥ 4 years) |

| Probiotic Postbiotics Enabling Lower-Dose Drug Regimens | +0.9% | National, with veterinary research centers leading adoption | Long term (≥ 4 years) |

| Pet Insurance Chronic-Care Coverage Expansion | +0.8% | National, with higher penetration in higher-income demographics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Gastrointestinal Disorders Lead Veterinary Diagnoses

Gastrointestinal conditions accounted for 23% of all veterinary diagnoses in 2024, surpassing skin and ear infections as the primary health concern driving therapeutic nutrition prescriptions [1]Source: American Animal Hospital Association, “2024 Veterinary Diagnosis Trends Report,” aaha.org. Case numbers increased year-over-year, and hydrolyzed-protein prescription diets achieved a 67% symptom-resolution rate, compared to drug-only regimens. Center for Veterinary Medicine expanded therapeutic claim approvals for hydrolyzed protein and novel carbohydrate formulations, enabling more targeted dietary interventions for complex digestive disorders. Heightened clinical success continues to pull new owners toward diet-first interventions.

Rapid Premiumization in Pet Specialty Retail

Average selling prices for therapeutic diets in specialty outlets increased in 2024, as retailers paired exclusive formulations with personalized counseling. Independent specialty stores capture higher margins through exclusive distribution agreements with therapeutic diet manufacturers, while big-box retailers struggle to compete on specialized veterinary nutrition expertise. Premiumization extends beyond ingredient quality to encompass personalized nutrition consultations, subscription delivery services, and integration with veterinary practice management systems, enabling seamless prescription fulfillment.

Veterinarian-Driven Subscription E-commerce Programs

Subscription-based therapeutic diet delivery programs grew 45% in 2024, with veterinary practices partnering directly with manufacturers to provide automated prescription refills and dosage adjustments [2]Source: MJH Life Sciences, “Subscription Models in Veterinary Nutrition,” dvm360.com. Hill's Pet Nutrition, Royal Canin, and Purina Pro Plan Veterinary Diets launched practice-integrated platforms enabling veterinarians to monitor patient compliance and adjust therapeutic protocols remotely. These programs generate recurring revenue streams for veterinary practices while improving long-term adherence rates to diets for chronic conditions that require sustained nutritional management.

Algorithmic Diet-Matching Tools Inside Practice Software

Veterinary practice management software will integrate algorithmic diet-matching capabilities by 2024, enabling data-driven therapeutic nutrition recommendations based on patient history, breed characteristics, and diagnostic results. These tools analyze over 200 patient variables to recommend optimal therapeutic diet formulations, reducing prescription errors and improving treatment outcomes through precision nutrition protocols. Integration with laboratory diagnostic systems enables real-time diet adjustments based on blood chemistry panels and urinalysis results, particularly for renal and diabetic management programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Product Price Elasticity in Inflationary Cycles | -1.4% | National, with a higher impact in rural and lower-income areas | Short term (≤ 2 years) |

| Low Owner Compliance With Long-Term Diet Plans | -1.1% | National, with regional variations in pet healthcare attitudes | Medium term (2-4 years) |

| Growth of Compounded "Home-Cook Kits" in Tele-Vet Forums | -0.8% | National, concentrated in tech-savvy urban demographics | Medium term (2-4 years) |

| Phosphorus Sourcing Risk Due to European Union Fertilizer Directives | -0.6% | National supply chain impact from international sourcing dependencies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Product Price Elasticity in Inflationary Cycles

Therapeutic pet diet purchases demonstrate 23% price elasticity during inflationary periods, with consumers downgrading to lower-cost alternatives or extending feeding intervals to manage household budgets [3]Source: Bureau of Labor Statistics, “Consumer Price Index: Pets and Pet Products,” bls.gov. Rural markets exhibit higher sensitivity to price increases, with pet owners delaying therapeutic diet purchases when prices exceed USD 3.50 per pound, compared to metropolitan areas. Economic pressures force veterinarians to recommend generic therapeutic alternatives or combination approaches that mix prescription diets with conventional foods, potentially compromising treatment efficacy for chronic conditions that require strict dietary management.

Low Owner Compliance with Long-Term Diet Plans

Pet owner adherence to prescribed therapeutic diets averages 47% after six months, declining to 31% after one year due to concerns about palatability, convenience factors, and perceived cost burden. Compliance challenges intensify for multi-pet households where dietary separation proves difficult, as well as for conditions requiring permanent dietary modifications rather than short-term therapeutic interventions. Veterinary practices report that lack of owner education and follow-up support contributes to treatment failures, with 62% of therapeutic diet discontinuations occurring without veterinary consultation or alternative treatment planning.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub Product: Digestive Health Leads Therapeutic Innovation

Digestive sensitivity diets captured 16.35% of the United States pet veterinary diet market share in 2025, the largest slice among therapeutic categories. Their dominance stems from rising diagnoses of inflammatory bowel disease, food allergies, and microbiome imbalance that now prompt veterinarians to prescribe hydrolyzed-protein and novel-carbohydrate formulas as first-line interventions. Oral care diets are advancing at a 8.85% CAGR to 2031, buoyed by preventive dentistry programs that pair mechanical-abrasion kibble design with Food and Drug Administration (FDA)-approved enzymatic plaque reducers. Renal lines hold steady demand as aging pets with chronic kidney disease rely on phosphorus-restricted blends, while diabetes diets leverage controlled-release carbohydrates and soluble fiber to support insulin therapy.

Dermatology products target the elimination of allergenic proteins and incorporate omega-fatty acids for skin barrier repair. Obesity formulas deliver calorie-restricted yet nutrient-complete meals for sustainable weight control. Urinary tract blends regulate pH and mineral loads to curb stone formation. Cardiac, hepatic, and recovery formulas remain smaller but essential, supplying taurine, modified proteins, and elevated caloric density for complex medical cases. Continuous clinical trials and FDA claim expansions ensure high scientific rigor, keeping category innovation robust and reinforcing premium price positions within the United States pet veterinary diet market.

By Pets: Canine Spending Remains the Growth Anchor

Dogs accounted for 55.60% of the United States pet veterinary diet market size in 2025 and are projected to grow at a 9.05% CAGR through 2031, reflecting higher per-capita veterinary spending and widespread insurance adoption. Breed-specific research informs formulations for German Shepherd renal support, Bulldog digestive care, and Golden Retriever cardiac protection, while algorithmic diet-matching tools inside practice software fine-tune canine prescriptions. Routine wellness plans further embed therapeutic diets into daily care, reinforcing compliance and repeat purchasing.

Cats require specialized care from veterinarians, who address feline-specific issues such as urinary crystals, chronic kidney disease, and diabetes, which necessitate high-protein, amino-acid-balanced meals. Palatability science is crucial because flavor fatigue can quickly undermine adherence. Diet options for rabbits, birds, and exotics are rising as specialty veterinarians and tele-exotic platforms emerge. Manufacturers willing to invest in species-specific trials and FDA pathways can capture this underserved niche within the broader United States pet veterinary diet market.

By Distribution Channel: Expertise Drives Specialty Dominance

Specialty stores led 2025 distribution with 24.15% revenue, leveraging on-staff nutritionists and exclusive supplier ties that reinforce professional trust and allow premium pricing. Integrated prescription portals enable clinics to transmit diet authorizations directly to retail partners, streamlining pickup for clients. Convenience stores, although smaller today, are experiencing the fastest 8.95% CAGR through subscription lockers and automated refill kiosks that combine speed with compliance assurance.

Online portals are now closing gaps in rural therapy access through same-day shipment options. Supermarkets and hypermarkets remain constrained by prescription-only rules that require physical or digital vet authorization. Additional volume flows through veterinary clinic counters, farm stores, and wholesalers that supply shelters and research institutes, rounding out the distribution map of the United States pet veterinary diet market.

Geography Analysis

The United States pet veterinary diet market demonstrates regional variations driven by pet ownership density, veterinary infrastructure, and household income distributions across metropolitan and rural areas. The Northeast and West Coast regions are projected to lead market penetration in 2024, driven by higher per-capita veterinary spending and increased adoption of premium pet healthcare services. California, New York, and Massachusetts represent the largest state markets, driven by urban pet ownership patterns and established veterinary specialty practices offering advanced therapeutic nutrition programs.

The Midwestern and Southern states, together, reflect larger rural populations with different pet healthcare spending priorities and limited access to veterinary specialists. Texas, Florida, and Illinois emerge as growth leaders within these regions, benefiting from expanding suburban populations and increasing veterinary school graduate placement in underserved markets. Rural areas demonstrate higher price sensitivity for therapeutic diets but show improving compliance rates when supported by tele-veterinary consultation programs and subscription delivery services that overcome geographic barriers to specialized pet healthcare access.

Western mountain states and Plains regions represent a good combined share with variable growth patterns influenced by agricultural economies and seasonal population fluctuations in resort communities. FDA Center for Veterinary Medicine regional compliance programs ensure consistent therapeutic diet quality and safety standards across all geographic markets, while state veterinary licensing requirements create regulatory frameworks supporting prescription diet distribution through authorized channels only.

Competitive Landscape

The five largest suppliers, Mars Incorporated, General Mills Inc., Nestle (Purina), Schell & Kampeter Inc. (Diamond Pet Foods), and Colgate-Palmolive Company (Hill's Pet Nutrition Inc.), together accounted for a significant share of the revenue in 2024, establishing a low-concentration structure. Mars leverages Royal Canin research alliances to rapidly develop condition-specific launches, while Nestlé’s Purina Pro Plan platform integrates wellness supplements following its acquisition of VetriScience. Hill’s Pet Nutrition maintains its premium positioning through long-running partnerships with veterinary schools that yield continual formula updates.

Technology capabilities increasingly define competitive advantage. All leading firms are embedding algorithmic recommendation engines into cloud-based practice management systems, thereby deepening clinician loyalty and enhancing data capture. Direct-to-consumer subscription portals, launched in collaboration with clinics, are securing recurring revenue while adhering to Food and Drug Administration (FDA) prescription control rules. Smaller players, from Virbac to Farmina, compete in niche protein sources and certified organic claims, but their growth paths hinge on clinical trial funding and the depth of channel partnerships within the competitive framework of the United States pet veterinary diet market.

Strategic capacity expansions are underway. Mars Incorporated is investing USD 180 million in Kansas to add renal and cardiac diet lines. Hill’s deployed an AI-powered dosing engine across 2,000 practices to protect Science Diet’s leadership. Nestle (Purina) bolt-on acquisitions widen ingredient diversity and shorten innovation cycles, sustaining competitive intensity and margin defense.

United States Pet Veterinary Diet Industry Leaders

Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

General Mills Inc.

Mars Incorporated

Nestle (Purina)

Schell & Kampeter Inc. (Diamond Pet Foods)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2023: Colgate-Palmolive Company's pet care subsidiary Hill’s Pet Nutrition launched its new line of prescription diets to support pets diagnosed with cancer. This prescription line, Diet ONC Care, offers complete and balanced formulas in both dry and wet forms for cats and dogs.

- January 2023: Purina Pro Plan Veterinary Diets, a brand of Nestlé Purina PetCare, partnered with the American Veterinary Medical Foundation (AVMF) to help expand the AVMF Reaching Every Animal with Charitable Care (REACH) program. This program offers grants to veterinarians who provide immediate treatment for pets whose owners are experiencing financial hardship. This strategy helps increase the sales of veterinary diets.

- January 2023: Royal Canin, a subsidiary of Mars Incorporated, launched its new dog food line, SKINTOPIC, that can help manage canine atopic dermatitis.

United States Pet Veterinary Diet Market Report Scope

Diabetes, Digestive Sensitivity, Oral Care Diets, Renal, Urinary tract disease are covered as segments by Sub Product. Cats, Dogs are covered as segments by Pets. Convenience Stores, Online Channel, Specialty Stores, Supermarkets/Hypermarkets are covered as segments by Distribution Channel.| Derma Diets |

| Diabetes |

| Digestive Sensitivity |

| Obesity Diets |

| Oral Care Diets |

| Renal |

| Urinary tract disease |

| Other Veterinary Diets |

| Cats |

| Dogs |

| Other Pets |

| Convenience Stores |

| Online Channel |

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Other Channels |

| By Sub Product | Derma Diets |

| Diabetes | |

| Digestive Sensitivity | |

| Obesity Diets | |

| Oral Care Diets | |

| Renal | |

| Urinary tract disease | |

| Other Veterinary Diets | |

| Pets | Cats |

| Dogs | |

| Other Pets | |

| Distribution Channel | Convenience Stores |

| Online Channel | |

| Specialty Stores | |

| Supermarkets/Hypermarkets | |

| Other Channels |

Market Definition

- FUNCTIONS - Pet foods are usually intended to provide complete and balanced nutrition to the pet but are primarily used as functional products. The scope includes the food and supplements consumed by pets including veterinary diets. Supplements/nutraceuticals that are directly supplied to pets are considered within the scope.

- RESELLERS - Companies engaged in reselling of pet food without value addition have been excluded from the market scope, in order to avoid double counting.

- END CONSUMERS - Pet owners are considered to be the end-consumers in the market studied.

- DISTRIBUTION CHANNELS - Supermarkets/hypermarkets, specialty stores, convenience stores, online channels and other channels are considered within the scope. The stores which are exclusively providing pet related basic and custom products are considered within the scope of specialty stores.

| Keyword | Definition |

|---|---|

| Pet Food | The scope of pet food includes the food that is eatable by pets including food, treats, veterinary diets, and nutraceuticals/supplements. |

| Food | Food is animal feed intended for consumption by pets. It is formulated to provide essential nutrients and meet the dietary needs of various types of pets, including dogs, cats, and other animals. These are generally segmented into dry and wet pet foods. |

| Dry Pet Food | Dry pet foods may be extruded/baked (kibbles) or flaked. They have a lower moisture content, typically around 12-20%. |

| Wet Pet Food | Wet pet food, also known as canned pet food or moist pet food, generally has a higher moisture content compared to dry pet food, often ranging from 70-80%. |

| Kibbles | Kibbles are dry, processed pet food in small, bite-sized pieces or pellets. They are specifically formulated to provide balanced nutrition for various domestic animals, such as dogs, cats, and other animals. |

| Treats | Pet Treats are special food items or rewards given to pets, to show affection, and encourage good behavior. They are especially used during training. Pet treats are made from various combinations of meat or meat-derived materials with other ingredients. |

| Dental Treats | Pet dental treats are specialized treats that are formulated to promote good oral hygiene in pets. |

| Crunchy Treats | It is a type of pet treat that has a firm and crispy texture which can be a good source of nutrition for pets. |

| Soft and chewy treats | Soft and Chewy pet treats are a type of pet food product that is formulated to be easy to chewy and digest. They are usually made from soft and pliable ingredients, such as meat, poultry, or vegetables, that have been blended and formed into bite-sized pieces or strips. |

| Freeze-dried & Jerky Treats | Freeze-dried and jerky treats are snacks given to pets, that are prepared through a special preservation process, without damaging the nutritional content, resulting in long-lasting, nutrient-rich treats. |

| Urinary Tract Disease Diets | These are commercial diets that are specifically formulated to promote urinary health and reduce the risk of urinary tract infections and other urinary problems. |

| Renal Diets | These are specialized pet foods formulated to support the health of pets with kidney disease or renal insufficiency. |

| Digestive Sensitivity Diets | Digestive-sensitive diets are specially formulated to meet the nutritional needs of pets with digestive issues such as food intolerances, allergies, and sensitivities. These diets are designed to be easily digestible and to reduce the symptoms of digestive problems in pets. |

| Oral Care Diets | Oral care diets for pets are specially formulated diets produced to promote oral health and hygiene in pets. |

| Grain-Free Pet Food | Pet food that does not contain common grains like wheat, corn, or soy. Grain-free diets are often preferred by pet owners seeking alternative options or if their pets have specific dietary sensitivities. |

| Premium Pet Food | High-quality pet food formulated with superior ingredients often offers additional nutritional benefits compared to standard pet food. |

| Natural Pet Food | Pet food made from natural ingredients, with minimal processing and without artificial preservatives. |

| Organic Pet Food | Pet food is produced using organic ingredients, free from synthetic pesticides, hormones, and genetically modified organisms (GMOs). |

| Extrusion | A manufacturing process used to produce dry pet food, where ingredients are cooked, mixed, and shaped under high pressure and temperature. |

| Other Pets | Other pets include birds, fish, rabbits, hamsters, ferrets, and reptiles. |

| Palatability | The taste, texture, and aroma of pet food influence its appeal and acceptance by pets. |

| Complete and Balanced Pet Food | Pet food that provides all essential nutrients in appropriate proportions to meet the nutritional needs of pets without additional supplementation. |

| Preservatives | These are the substances that are added to pet food to extend its shelf life and prevent spoilage. |

| Nutraceuticals | Food products that offer health benefits beyond basic nutrition, often contain bioactive compounds with potential therapeutic effects. |

| Probiotics | Live beneficial bacteria that promote a healthy balance of gut flora, supporting digestive health and immune function in pets. |

| Antioxidants | Compounds that help neutralize harmful free radicals in the body, promoting cellular health and supporting the immune system in pets. |

| Shelf-Life | The duration of which pet food remains safe and nutritionally viable for consumption after its production date. |

| Prescription diet | Specialized pet food formulated to address specific medical conditions under veterinary supervision. |

| Allergen | A substance that can cause allergic reactions in some pets, leading to food allergies or sensitivities. |

| Canned food | Wet pet food that is packed in cans and contains higher moisture content than dry food. |

| Limited ingredient diet (LID) | Pet food formulated with a reduced number of ingredients to minimize potential allergens. |

| Guaranteed Analysis | The minimum or maximum levels of certain nutrients present in pet food. |

| Weight management | Pet food designed to help pets maintain a healthy weight or support weight loss efforts. |

| Other Nutraceuticals | It includes prebiotics, antioxidants, digestive fiber, enzymes, essential oils and herbs. |

| Other Veterinary Diets | It includes weight management diets, skin and coat health, cardiac care, and joint care. |

| Other Treats | It includes rawhides, mineral blocks, lickables, and catnips. |

| Other Dry Foods | It includes cereal flakes, mixers, meal toppers, freeze-dried foods, and air-dried foods. |

| Other Animals | It includes birds, fish, reptiles, and small animals (rabbits, ferrets, hamsters). |

| Other Distribution Channels | It includes veterinary clinics, local unregulated stores, and feed and farm stores. |

| Proteins and Peptides | Proteins are large molecules composed of basic units called amino acids which help in the growth and development of pets. Peptides are the short string of 2 to 50 amino acids. |

| Omega-3 fatty acids | Omega-3 fatty acids are essential polyunsaturated fats that play a crucial role in the overall health and well-being of Pets |

| Vitamins | Vitamins are the essential organic compounds that are essential for vital physiological functioning. |

| Minerals | Minerals are naturally occurring inorganic substances that are essential for various physiological functions in pets. |

| CKD | Chronic Kidney Disease |

| DHA | Docosahexaenoic Acid |

| EPA | Eicosapentaenoic Acid |

| ALA | Alpha-linolenic Acid |

| BHA | Butylated Hydroxyanisol |

| BHT | Butylated Hydroxytoluene |

| FLUTD | Feline Lower Urinary Tract Disease |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms