Vegan Cat Food Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

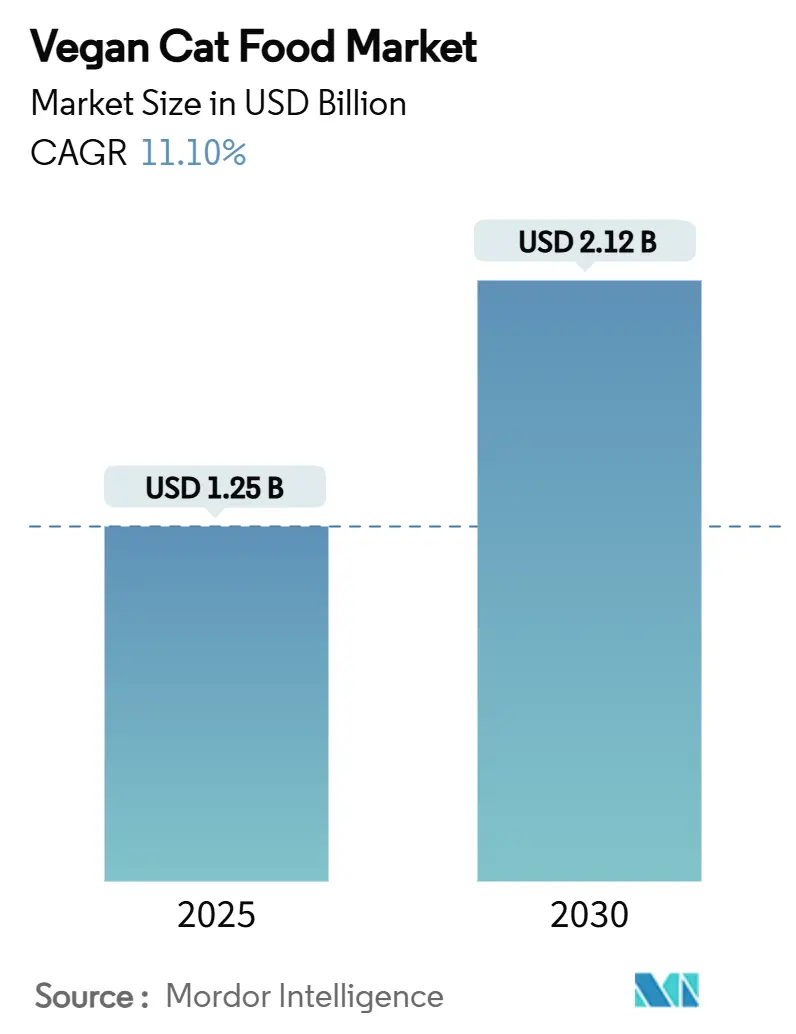

| Market Size (2025) | USD 1.25 Billion |

| Market Size (2030) | USD 2.12 Billion |

| Growth Rate (2025 - 2030) | 11.10% CAGR |

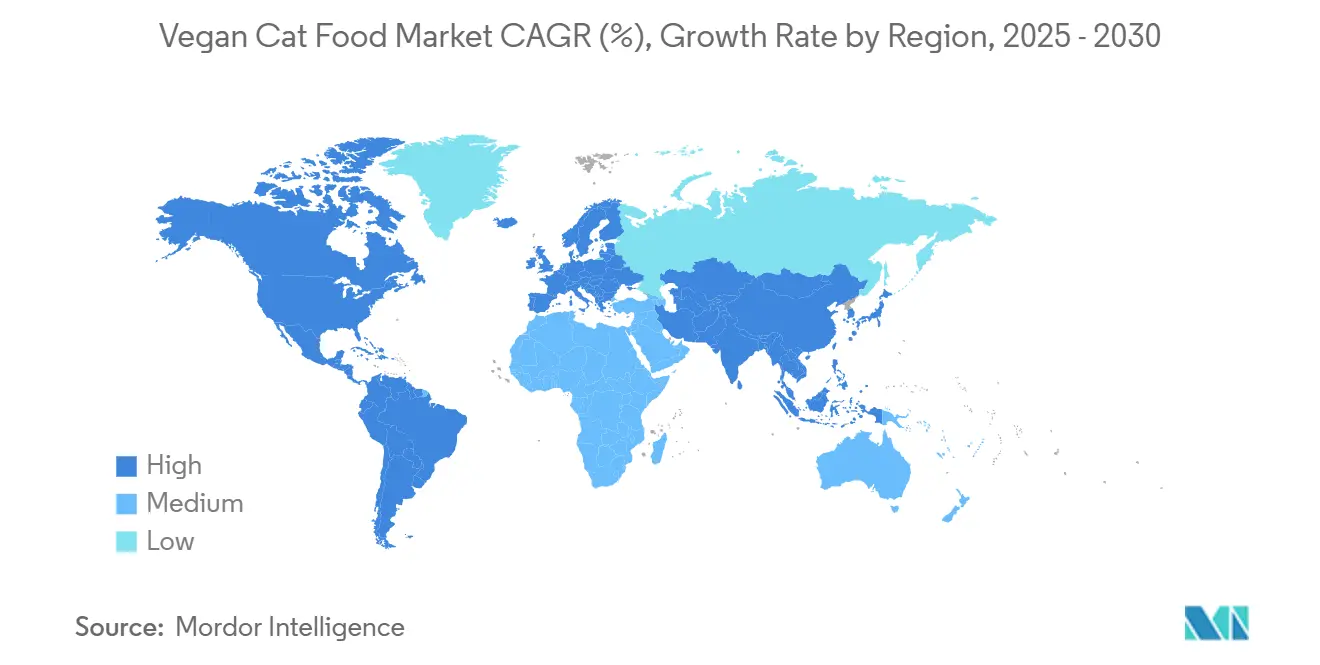

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Vegan Cat Food Market Analysis by Mordor Intelligence

The vegan cat food market size reached USD 1.25 billion in 2025 and is projected to expand to USD 2.12 billion by 2030, reflecting an 11.1% CAGR through the forecast period. Rising pet humanization, accelerating climate-related supply risks for animal proteins, and rapid product innovation in synthetic taurine and precision fermentation underpin this trajectory. Dry kibble holds the largest revenue share, yet online retail and freeze-dried formats lead growth as subscription services, transparent sourcing claims, and fresh-food positioning gain traction. North America remains the largest regional market, while Asia-Pacific records the fastest gains on the back of expanding middle-class pet ownership and pervasive e-commerce adoption. Moderate industry concentration persists because early European pioneers coexist with venture-backed disruptors and fast-moving consumer-goods entrants seeking sustainable growth avenues.

Key Report Takeaways

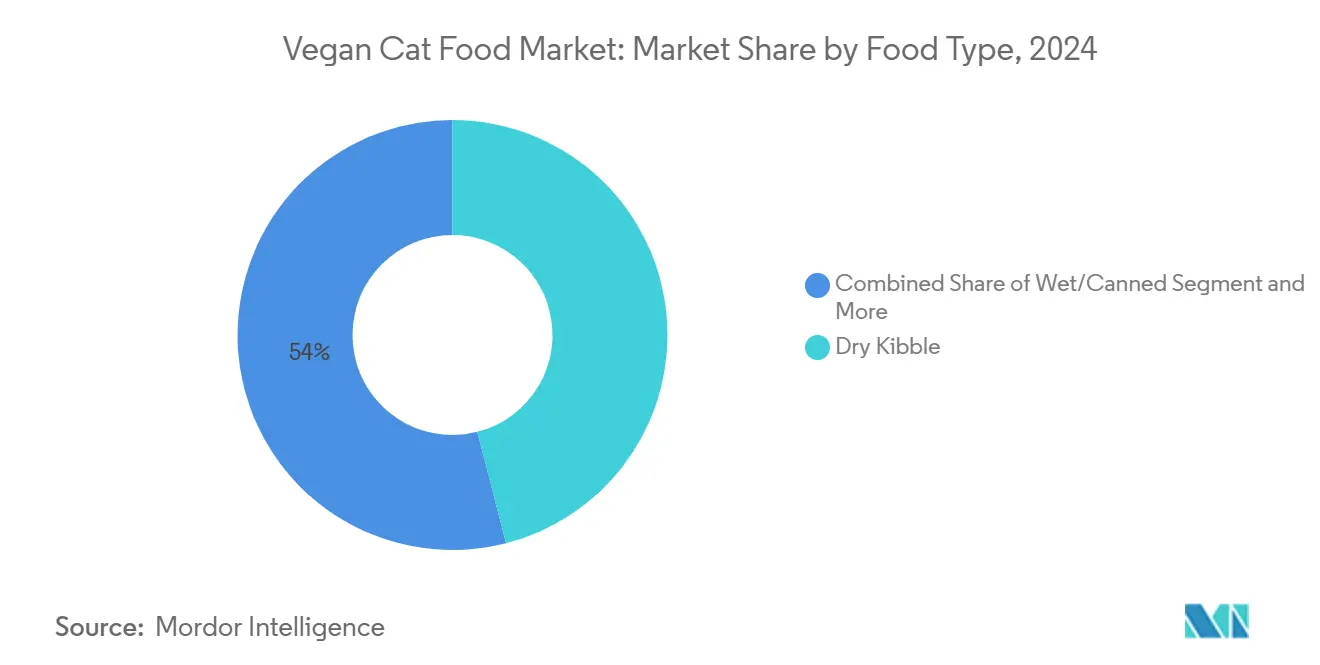

- By food type, dry kibble led with 46.0% of the vegan cat food market share in 2024, while wet and canned alternatives are set to post a 7.2% CAGR to 2030.

- By protein source, soybean held 31.0% share of the vegan cat food market size in 2024, and pea and lentil proteins are forecast to expand at a 10.2% CAGR through 2030.

- By form, extruded accounted for 48.5% of the vegan cat food market size in 2024, and freeze-dried products are advancing at an 11.4% CAGR.

- By life stage, adult formulations dominated with 62.0% revenue share in 2024, while kitten diets are projected to rise at a 9.1% CAGR to 2030.

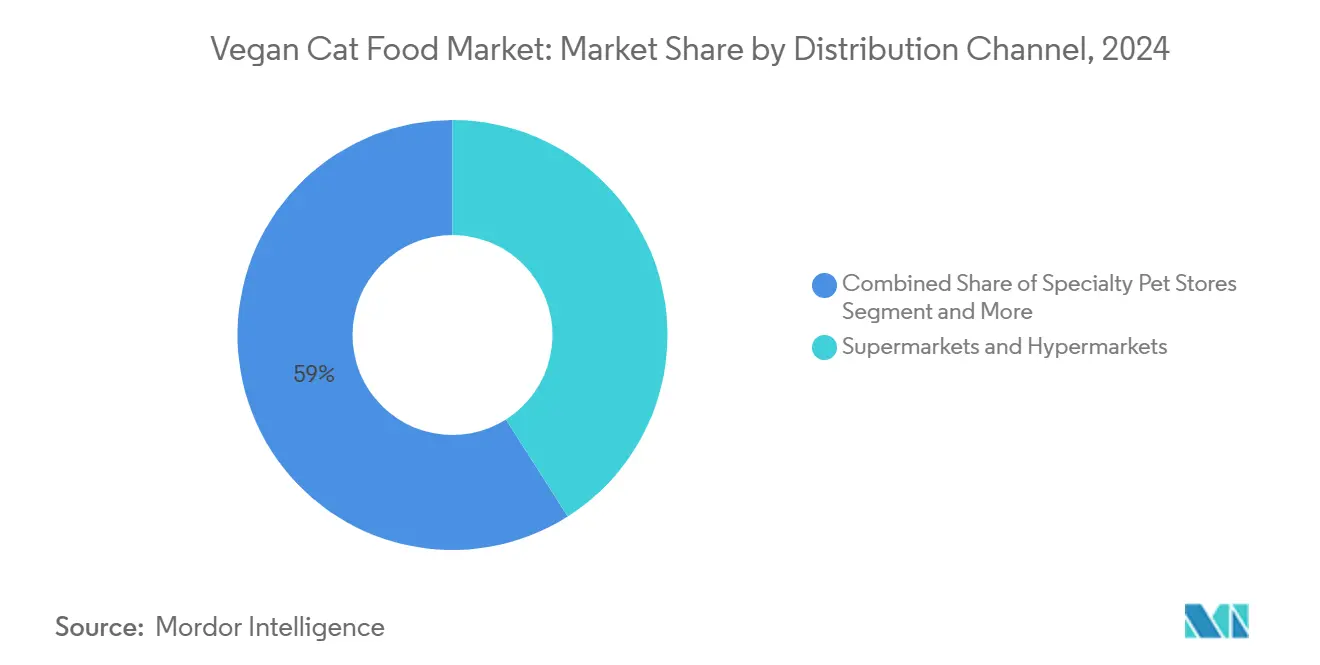

- By distribution channel, supermarkets and hypermarkets held a 41.0% share of the vegan cat food market size in 2024, while online retail is growing at a 13.8% CAGR.

- By geography, North America held about a 44.5% share, and the Asia-Pacific region is projected to grow fastest at a CAGR of 11.5% during the forecast period.

Global Vegan Cat Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pet humanization drives sustainable diets | +3.2% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Vegan consumer influence on pet choices | +2.8% | North America, Europe, and urban Asia-Pacific | Short term (≤2 years) |

| Zoonotic disease risk perception | +2.1% | Global, heightened in post-pandemic markets | Medium term (2-4 years) |

| Climate-driven meat supply volatility | +1.9% | Global, and supply-constrained regions | Long term (≥4 years) |

| Synthetic taurine eliminates nutrient gaps | +1.5% | Global, and technology-dependent markets | Medium term (2-4 years) |

| Carbon-footprint disclosure mandates | +1.3% | Europe expanding to North America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Vegan Consumer Influence on Pet Nutrition Choices

Rising plant-based lifestyles translate directly into pet feeding habits, with 20% of cat owners contemplating vegan transitions for sustainability reasons. Social media accelerates peer-to-peer education, amplifying brand trials and fostering communities that exchange feeding success stories. Brands that publish laboratory nutrient analyses, Association of American Feed Control Officials (AAFCO) compliance evidence, and veterinarian testimonials secure stronger engagement levels than conventional marketing tactics. The behavioural shift enlarges the addressable base for complete vegan diets across urban markets in the United States, Germany, and Japan.

Zoonotic Disease Risk Perception

Public awareness of zoonotic outbreaks propels interest in diets free from livestock inputs, perceived as safer and more hygienic. Plant-based alternatives help pet owners mitigate concerns over bacterial contamination and antibiotic residues linked to animal proteins. Companies leverage this perception in risk-averse marketing messages while regulators encourage diversified protein sources to bolster food-system resilience. The driver remains particularly influential in Asia-Pacific markets where pandemic memory is recent and acute.

Synthetic Taurine Eliminates Nutrient Gaps

WACKER’s fermentation-based taurine delivers a non-synthetic solution that satisfies obligate-carnivore requirements without petroleum derivatives. Parallel United States Department of Agriculture (USDA) funded research accelerates scalability and cost reduction, widening access for medium-sized formulators [1]Source: National Institute of Food and Agriculture, “Phase II: Microbial Fermentation of Taurine,” nifa.usda.gov . As achieving complete nutrient profiles becomes increasingly feasible, professional skepticism continues to diminish. This paves the way for greater product diversification, including tailored formulas for kittens and senior cats.

Carbon-Footprint Disclosure Mandates

European legislation requires manufacturers to quantify and publish their greenhouse-gas footprints, highlighting the high emissions intensity of meat-based recipes. [2]Source: European Commission, "Commission Delegated Regulation (EU) 2023/2772 of 31 July 2023 Supplementing Directive (EU) 2022/2464 of the European Parliament and of the Council as Regards Sustainability Reporting Standards," europa.eu As a result, plant-based products are gaining traction not only as compliance-friendly solutions but also as strategic marketing differentiators. This shift is increasingly influencing Research and Development investment priorities and guiding retailer shelf space decisions. Meanwhile, North American regulators are advancing toward similar transparency frameworks, signaling a likely ripple effect that could reshape global formulation strategies and accelerate sustainability-driven innovation across the pet food sector.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nutritional adequacy skepticism | −2.8% | Global, and strongest in veterinary communities | Medium term (2-4 years) |

| Premium pricing gap vs. conventional food | −2.3% | Price-sensitive markets, and emerging economies | Short term (≤2 years) |

| Palatability challenges | −1.9% | Global, and varies by regional taste | Medium term (2-4 years) |

| Dependence on imported plant proteins | −1.5% | Import-dependent markets | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Nutritional Adequacy Skepticism

Professional associations caution that long-term evidence for vegan feline diets remains limited, prompting conservative feeding recommendations. The British Veterinary Association’s 2024 report calls for rigorous trials before routine endorsement [3]Source: British Veterinary Association, “BVA Companion Animal Feeding Working Group Report,” bva.co.uk . Peer-reviewed studies demonstrating comparable or improved health outcomes gradually shift opinions, yet a broad consensus will require multi-year longitudinal data. Investment in independent research and continuing-education outreach can narrow the trust gap and speed clinical acceptance.

Palatability Challenges

Cats exhibit strong sensory preferences; aroma and mouthfeel deviations from meat can depress acceptance, leading to waste and consumer dissatisfaction. Advances in extrusion, flavor masking, and lipid micro-encapsulation have improved acceptance scores, yet consistent palatability parity remains elusive. Brands experimenting with cultivated chicken flavors or algal oils seek to replicate organoleptic cues without compromising vegan claims, though regulatory clearance and cost hurdles persist.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Food Type: Dry Kibble Retains Leadership While Wet and Fresh Gain Momentum

The dry-kibble segment commanded 46.0% of the vegan cat food market share in 2024, supported by price advantage, shelf stability, and widespread distribution. Wet and canned lines, backed by hydration benefits, are forecast to outpace at a 7.2% CAGR, reflecting enhanced texture technologies and broadened flavor ranges that narrow historical acceptance gaps. Treats and snacks, buoyed by humanization trends, show a robust growth as owners reward pets with functional or indulgent extras.

Over the outlook period, manufacturers are fine-tuning extrusion settings and optimizing protein blends to improve palatability, ensuring dry products retain relevance as premium wet and fresh offerings gain traction. The vegan cat food segment for fresh, refrigerated meals is projected to post double-digit growth, though cold-chain logistics continue to limit widespread adoption. Consumers are increasingly rotating between formats, driving cross-category purchases and boosting overall per-capita spending in the category.

By Protein Source: Pea Protein Innovation Underpins Category Growth

Soybean recipes retained 31.0% of the vegan cat food market size in 2024, aided by cost efficiency and complete amino-acid profiles. Pea and lentil protein, delivering hypoallergenic positioning and non-GMO claims, is gearing up for a 10.2% CAGR as new fractionation plants remove supply bottlenecks. Wheat and potato proteins remain important secondary options, but allergen concerns and carbohydrate perceptions cap their upside.

Precision-fermentation ingredients are entering commercial pipelines, delivering designer proteins with enhanced digestibility and functional benefits. These innovative inputs command premium pricing while aligning with carbon-reduction and sustainability narratives. Simultaneously, supply-chain diversification helps mitigate exposure to tariff fluctuations and geopolitical risks. However, persistent resin shortages and rising energy costs, particularly in Europe, may intermittently constrain production capacity and delay scale-up timelines for next-generation vegan cat food formulations.

By Form: Freeze-Dried Formats Capture Premium Shelf Space

Extruded vegan cat food constituted 48.5% of the vegan cat food market share in 2024 on the back of efficient throughput and low moisture content. Freeze-dried products, combining raw-like nutrition with ambient storage, are slated for an 11.4% CAGR as specialty retailers allocate more facings to ultra-premium SKUs. Canned and pate offerings are projected to grow steadily, benefitting from elevated palatability and moisture delivery.

Investment in high-pressure processing and gentle dehydration techniques helps preserve vitamin integrity, enhancing the nutritional appeal of premium formats. However, cost-of-goods sold remains about 25–30% higher than traditional kibble, constraining adoption among lower-income consumer segments. Emerging innovations in continuous freeze-drying technology are projected to reduce this cost gap after 2027, potentially expanding access and driving broader market acceptance of nutrient-dense, minimally processed vegan cat food options.

By Distribution Channel: Digital Ecosystems Redefine Market Access

Supermarkets and hypermarkets remained the top outlet with 41.0% of the vegan cat food market size in 2024, yet online retail is on course for a 13.8% CAGR as subscription programs and auto-replenishment reduce churn. Specialty pet stores grow closely as online retail channels, leveraging staff expertise and curated assortments to educate first-time buyers. Veterinary clinics add credibility, though slower growth reflects limited shelf space and higher product-turn requirements.

Direct-to-consumer brands leverage first-party data to fine-tune formulations, strengthen customer loyalty, and integrate tele-nutrition services for added value. At the same time, logistics partners are expanding cold-chain infrastructure to accommodate the growing demand for fresh, perishable offerings. Omnichannel retailers are also piloting click-and-collect models, seamlessly blending in-store experiences with digital convenience to meet evolving consumer expectations and enhance accessibility across multiple touchpoints.

By Life Stage: Specialized Kitten Diets Present Formulation Challenges

Adult maintenance diets accounted for 62.0% of the vegan cat food market size in 2024, reflecting broad applicability and established nutrient-validation datasets. Kitten formulas, requiring higher taurine, DHA, and lysine levels, will expand at a 9.1% CAGR as synthetic-nutrient availability and clinical data ease formulation complexity. Senior products projected to rise steadily, addressing joint and renal health with algae-derived omega-3 oils.

Targeted functional claims such as immune support, hairball control, and digestive health help differentiate product offerings and justify premium pricing. Brands that invest in and document life-stage-specific feeding trials build greater credibility with veterinarians and discerning consumers alike. This evidence-based approach not only reinforces brand trust but also accelerates penetration into specialized segments, paving the way for tailored formulations that address distinct health and nutritional needs across feline life stages.

Geography Analysis

North America generated the highest regional revenue, accounting for approximately 44.5% of the vegan cat food market share in 2024, driven by a mature premium pet food culture, regulatory clarity from the Association of American Feed Control Officials (AAFCO), and strong e-commerce infrastructure. The market is projected to expand steadily, supported by rising subscription adoption and growing endorsements from veterinary professionals. Resilient consumer spending continues to reinforce category momentum, even as broader inflationary pressures ease.

Asia-Pacific emerges as the key demand hotspot, projected to grow at a steep 11.5% CAGR. This is fueled by rising disposable incomes, a growing millennial middle class, and widespread digital commerce adoption, all contributing to rapid premiumisation. Supportive government initiatives around alternative protein infrastructure and positive cultural perceptions of novel ingredients are further accelerating uptake in the region.

Europe ranks second in growth, supported by high consumer awareness of plant-based diets and progressive policy frameworks, including strict organic-labelling standards. Advancements in pet-focused cultivated protein and eco-labelling schemes enhance the region’s innovation landscape. First-mover brands and specialty retailers play a key role in educating consumers on nutritional adequacy and environmental benefits.

Competitive Landscape

The vegan cat food market demonstrates moderate concentration. Companies such as Ami Planet Srl and Veggieanimals leverage strong formulation consistency, established distribution networks, and a history of consumer trust to maintain a competitive advantage. These brands are often perceived as pioneers in the segment, focusing on ingredient integrity, palatability, and compliance with feline nutritional requirements. Their portfolios typically include dry and wet formats, positioned to meet the needs of ethically conscious pet owners seeking fully plant-based solutions.

Compassion Circle, Inc. has earned sustained loyalty through its long-standing VegeCat offerings, formulated for nutritional adequacy and supported by a niche but committed consumer base. Similarly, VGRRR Pet Food Inc. is expanding its market presence with proprietary blends focused on digestibility and essential amino acid profiles tailored to feline health. Additional players contributing to the market's evolution include Wysong, Vitaveg, Nature’s HUG Pet Food Inc., and Vegan Pet.

Wysong continues to enhance its Vegan line with a focus on preserving nutrient integrity through careful processing techniques. Vitaveg is developing limited-ingredient recipes that emphasize purity and functional nutrition. Nature’s HUG differentiates itself with clean-label positioning and alternative protein sources that reduce environmental impact. Vegan Pet, a longstanding brand in the space, maintains relevance through consistent product quality and veterinarian-informed formulations. Strategic collaborations with ingredient suppliers, veterinary advisors, and fulfillment partners remain essential for product validation, speed-to-market, and long-term consumer trust.

Vegan Cat Food Industry Leaders

-

Amì Planet Srl

-

Veggieanimals

-

VGRRR

-

Nature’s HUG Pet Food Inc.

-

Benevo (Vegeco Ltd)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Prefera Petfood acquired British vegan pet food startup THE PACK. This move strengthens Prefera’s position in climate-smart and low-carbon cat food and brings together THE PACK’s expertise in plant-based formulations with Prefera’s manufacturing and scale.

- August 2024: Wild Earth introduced its first nutritionally complete vegan wet cat food, branded as Unicorn Pâté, formulated without animal proteins yet meeting Association of American Feed Control Officials (AAFCO) standards. The product includes lentils, peas, sweet potato, and microalgae, supplemented with taurine and essential nutrients to meet feline health requirements

- October 2023: CULT Food Science's Noochies brand introduced freeze-dried vegan cat treats that incorporate proprietary nutritional yeast, enhancing both palatability and nutritional completeness.

Global Vegan Cat Food Market Report Scope

| Dry Kibble |

| Wet/Canned |

| Treats and Snacks |

| Soybean |

| Pea and Lentil Protein |

| Potato, Wheat and Other Cereals |

| Extruded |

| Canned |

| Freeze-Dried/Dehydrated |

| Kitten |

| Adult |

| Senior |

| Supermarkets and Hypermarkets |

| Specialty Pet Stores |

| Veterinary Clinics |

| Online Retail |

| Other Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Food Type | Dry Kibble | |

| Wet/Canned | ||

| Treats and Snacks | ||

| By Protein Source | Soybean | |

| Pea and Lentil Protein | ||

| Potato, Wheat and Other Cereals | ||

| By Form | Extruded | |

| Canned | ||

| Freeze-Dried/Dehydrated | ||

| By Life Stage | Kitten | |

| Adult | ||

| Senior | ||

| By Distribution Channel | Supermarkets and Hypermarkets | |

| Specialty Pet Stores | ||

| Veterinary Clinics | ||

| Online Retail | ||

| Other Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the vegan cat food market?

The market generated USD 1.25 billion in 2025 and is projected to climb to USD 2.12 billion by 2030.

Which product format is expanding most rapidly?

Freeze-dried vegan cat food is set to rise at an 11.4% CAGR, reflecting premiumization and minimal-processing appeal.

Why is taurine crucial in vegan cat food?

Taurine is essential for feline health; fermentation-based synthetic taurine now enables nutritionally complete plant-based diets.

How significant is online retail for sales?

Online channels are posting a 13.8% CAGR as subscription models and direct-to-consumer platforms gain traction.

Page last updated on: