Natural Dog Treats Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

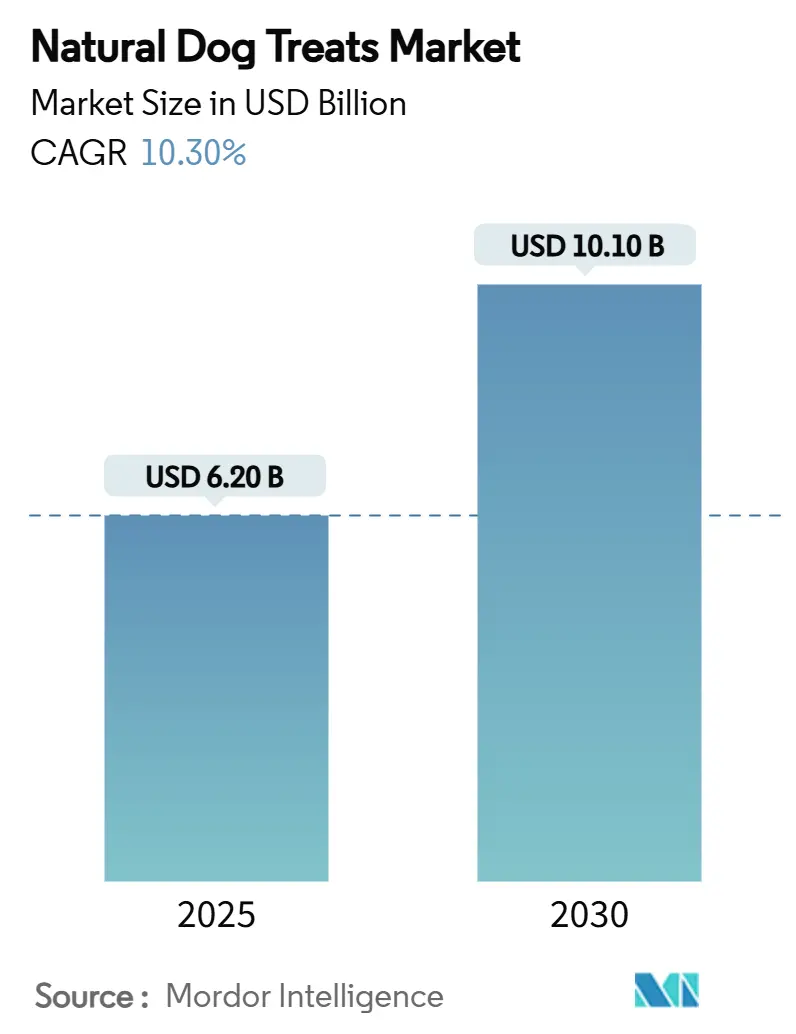

| Market Size (2025) | USD 6.20 Billion |

| Market Size (2030) | USD 10.10 Billion |

| Growth Rate (2025 - 2030) | 10.30% CAGR |

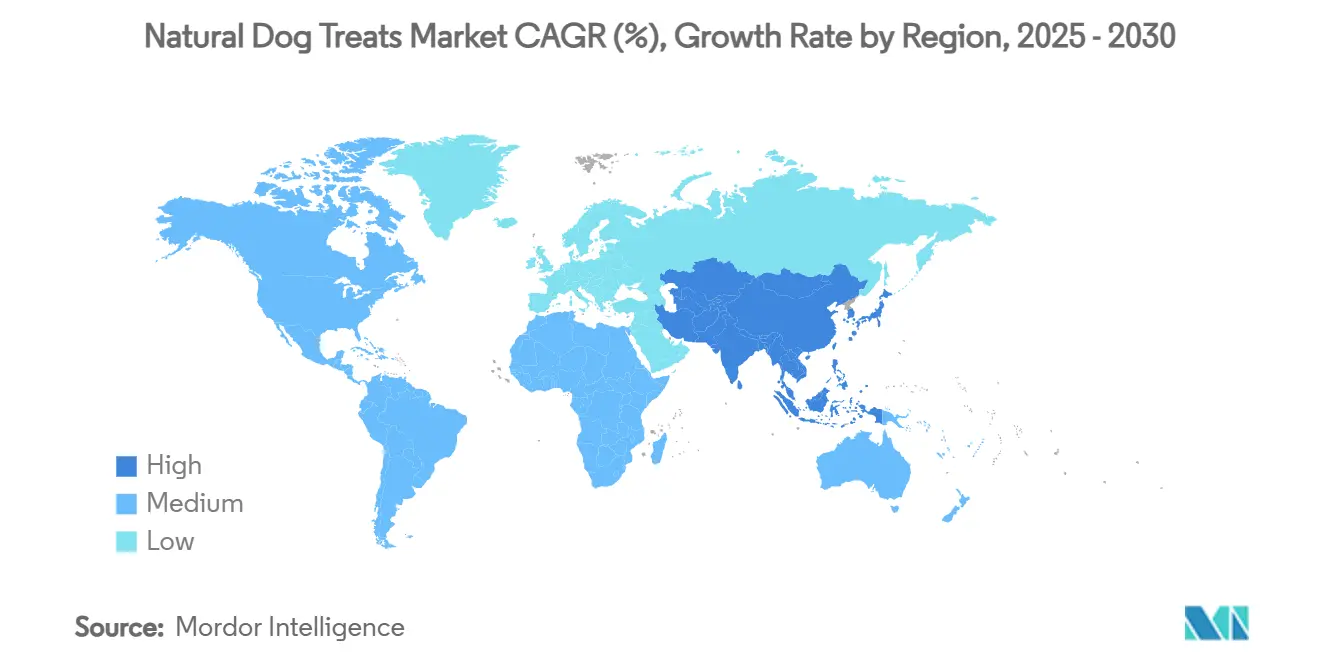

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Natural Dog Treats Market Analysis by Mordor Intelligence

The natural dog treats market size reached USD 6.2 billion in 2025 and is forecast to post a 10.3% CAGR, lifting revenues to USD 10.1 billion by 2030. Accelerated clean-label premiumization, the expansion of human-grade product mix, and increased e-commerce cold-chain capacity are widening household penetration while allowing producers to sustain premium price points. A shift toward functional formulations, validated by veterinarians, is unlocking new use-case opportunities, and sustainability mandates are encouraging brands to commercialize upcycled proteins and carbon-neutral packaging. Competitive intensity remains moderate, with the top five players holding the majority of revenue. However, new entrants are scaling direct-to-consumer niches in areas such as freeze-dried and personalized nutrition. Although inflation has squeezed discretionary spending in some segments, loyalty toward perceived higher-quality natural treats is insulating overall category demand in developed economies.

Key Report Takeaways

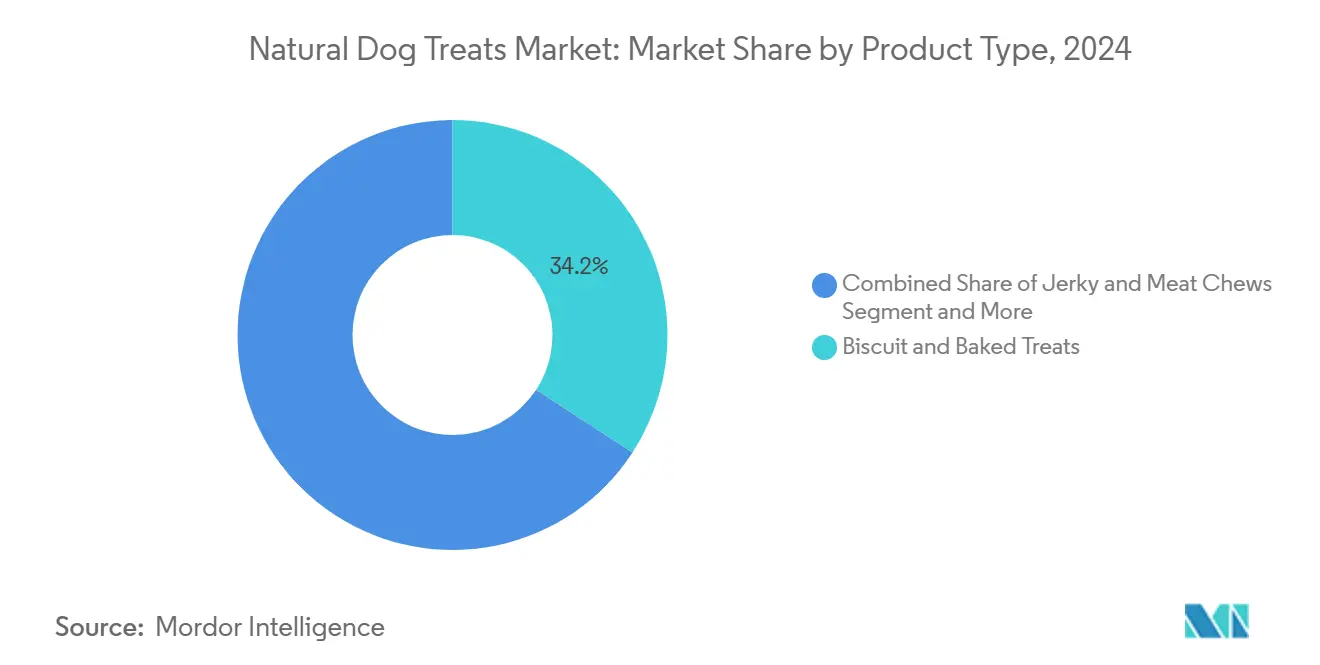

- By product type, biscuit and baked treats led with 34.2% revenue share in 2024, while freeze-dried and air-dried products are projected to expand at a 11.6% CAGR through 2030.

- By ingredient source, animal-based formulations accounted for 68.1% of the natural dog treats market share in 2024, whereas hybrid and upcycled alternatives are projected to grow at a 10.2% CAGR through 2030.

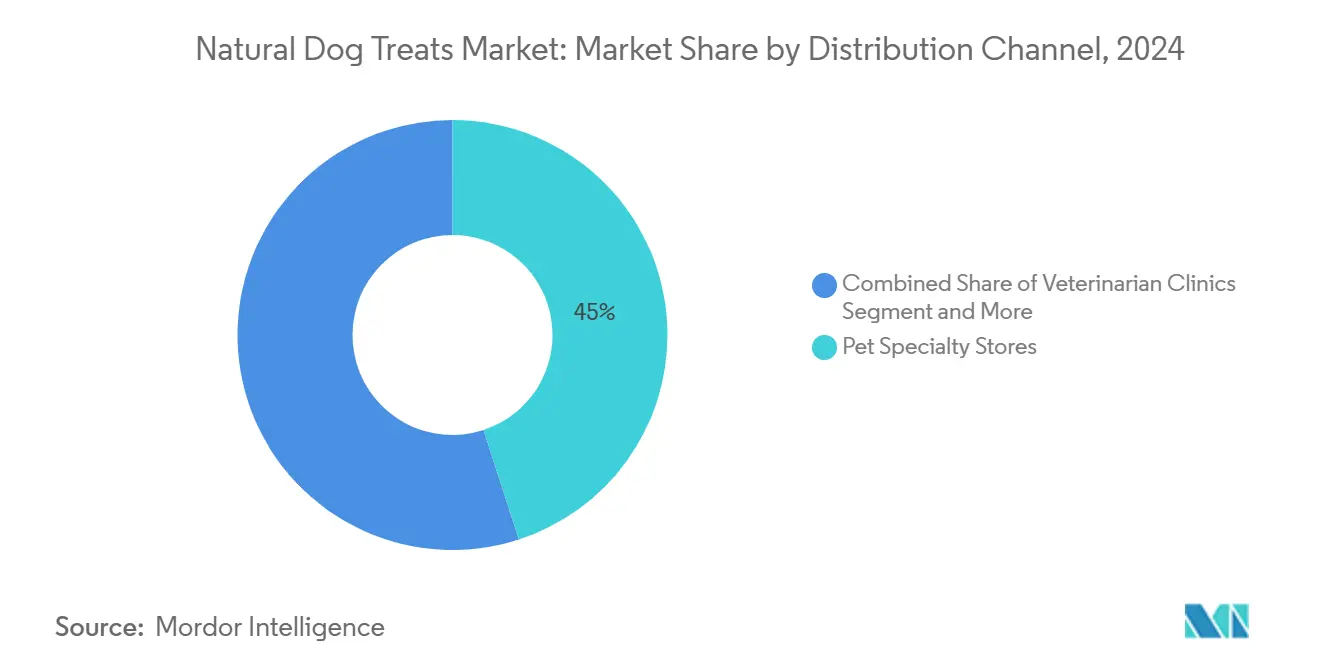

- By distribution channel, pet specialty stores accounted for 45.0% of the natural dog treats market size in 2024. However, online retailers are forecast to register a 13.1% CAGR, the fastest growth rate across all channels.

- By dog size, small breeds represented 40.0% of the 2024 value, while large breeds are the fastest-growing segment, with a 10.5% CAGR toward 2030.

- By geography, North America accounted for 37.5% of the natural dog treats market share in 2024, whereas the Asia-Pacific is the fastest-growing region with a 12.9% CAGR.

- The top five companies collectively controlled more than 50% of category sales in 2024, underscoring a moderately concentrated but innovation-friendly environment.

Global Natural Dog Treats Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Clean-label premiumization boom | +2.8% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Pet humanization influencing treat formats | +2.1% | Global, led by developed markets | Long term (≥4 years) |

| E-commerce expansion into fresh and frozen logistics | +1.9% | North America and Asia-Pacific | Short term (≤2 years) |

| Veterinarian endorsement of functional SKUs | +1.5% | Global, regulation-dependent regions | Medium term (2-4 years) |

| Upcycled coproduct adoption for sustainability | +1.2% | Europe and North America, expanding globally | Long term (≥4 years) |

| AI-guided personalized nutrition platforms | +0.8% | North America and select Asia-Pacific markets | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Clean-Label Premiumization Boom

Premium positioning has shifted from niche indulgence to baseline anticipation, as 30% of canine products now reside in the premium tier, and more than half of the 2024 European introductions featured “natural” cues. “Free-from” certifications lifted unit sales 24% last year, signaling that absence claims resonate as strongly as positive nutrition claims. Brands are reformulating to eliminate synthetic preservatives, prompting suppliers such as Kemin Industries, Inc., to commercialize buffered-vinegar systems that maintain shelf life without affecting palatability. Ingredient decks are shrinking as shoppers scrutinize label panels on mobile apps and anticipate single-protein transparency. Retailers are rewarding compliant suppliers with preferential shelf facings in premium sets that now out-earn mass tiers on a dollar-per-square-foot basis. The momentum suggests that “natural” will soon act as table stakes rather than a differentiator in most developed markets.

Pet Humanization Influencing Treat Formats

Over 70% of pet owners consider their pets as family members, leading to an increased demand for culinary-inspired treats that resemble human snacks. Kombucha-styled meal toppers, plant-based jerkies, and vitamin “bars” fit seamlessly into household pantry repertoires, expanding daily usage occasions. Functional soft chews aimed at anxiety, joint, and digestive issues posted double-digit sales growth as owners seek non-pharma interventions validated by veterinarians. Packaging now borrows resealable pouches and matte film finishes from the human snack aisle to convey freshness and upscale cues. Together, these trends are broadening price elasticity because owners equate quality time with premium treat rituals.

E-Commerce Expansion into Fresh and Frozen Logistics

Online turnover is forecast to climb at a faster growth rate as platforms perfect doorstep frozen delivery and auto-replenishment services. Yelloh’s Partner Picks network now places frozen natural treats within a 48-hour reach of 95% of the United States households, proving national scale is feasible. The average basket value online is 18% higher than in-store because recommendation engines bundle toppers, supplements, and accessories. Subscription programs reduce churn below 6% annually, locking in predictable cash flow for brands. Cold-chain advances such as compostable insulation and phase-change gel packs mitigate emissions concerns while preserving product integrity. The confluence of logistics reliability and AI merchandising is shifting category power toward digitally native labels.

Veterinarian Endorsement of Functional SKUs

Professional validation distinguishes premium Stock Keeping Units in a crowded market, with products bearing the Veterinary Oral Health Council seal commanding price premiums of 20% or more. Regulatory bodies now require documented surveys before a “vet recommended” label can appear, raising entry barriers and favoring Research and Development-centric companies. Clinics are turning into retail hubs for condition-specific snacks that complement prescribed diets, expanding average revenue per patient visit. Post-purchase compliance apps remind owners to dispense functional chews, driving higher consumption frequency than indulgent treats. With the increase in pet insurance adoption, coverage for clinically validated products may create a further boost in consumption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price sensitivity during global inflation cycles | -1.8% | Global, most acute in emerging markets | Short term (≤2 years) |

| Ingredient supply volatility | -1.4% | Global, supply-chain dependent regions | Medium term (2-4 years) |

| Stricter regulatory scrutiny of natural claims | -0.9% | North America and Europe, expanding globally | Medium term (2-4 years) |

| Cold-chain emissions pressure on ESG scores | -0.6% | Europe and North America, corporate focused | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Stricter Regulatory Scrutiny of Natural Claims

Association of American Feed Control Officials’ 2024 update mandates chemical-free processing documentation, compelling brands to audit every minor ingredient for compliance. The European Union regulators are drafting analogous measures under the Green Claims Initiative, which may prohibit vague “nature-inspired” wording without scientific substantiation. Compliance costs include laboratory analysis, legal review, and potential reformulation when synthetics hide in flavor carriers. Retailers have begun delisting products flagged for non-conformity to reduce liability. Transparent labels boost consumer trust, but transition missteps risk recalls and social-media backlash. The net effect is a higher operating bar that could squeeze smaller firms lacking regulatory expertise.

Cold-Chain Emissions Pressure on ESG Scores

Fresh and frozen fulfillment generates 2-3 times the carbon footprint of ambient shipments, putting brands under shareholder scrutiny to justify climate impact. Retailers in Europe now require Scope 3 emissions disclosures for private-label tenders, pushing suppliers to adopt renewable-energy warehouses and electric delivery fleets. Compostable insulation and dry-ice alternatives lower footprint but lift per-order cost by up to USD 0.60, challenging profitability on small baskets. Carbon offset programs fill the gap yet attract skepticism if not paired with direct reduction initiatives. Government incentives for refrigerated-truck electrification could ease the burden, but timelines remain uncertain. Brands lacking credible roadmaps may lose shelf space to room-temperature competitors perceived as greener.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Freeze-dried innovation disrupts traditional formats

Biscuit and baked items captured 34.2% of 2024 revenue, the largest share within the global natural dog treats market. Their longevity and easy portability make them staples for obedience training and casual snacking, especially among small-dog owners who favor bite-sized shapes. Freeze-dried and air-dried lines are projected to rise at a 11.6% CAGR. Growing penetration in Asia-Pacific e-commerce baskets suggests that the format’s appeal extends beyond Western markets. Jerky and meat chews hold strong with protein-centric buyers, but rising raw-material costs threaten margin stability. Brands incorporating regenerative-agriculture beef jerky are carving premium shelf slots by tying taste to environmental impact.

Consolidation is accelerating. Pure Treats acquired Bar W Foods and Eighteen Below Partners to secure a freeze-drying capacity and establish a United States Department of Agriculture-certified supply chain. New entrants are experimenting with sous-vide sticks that blend cooked-meat safety with raw-like texture, widening culinary diversity. Packaging innovation oxygen-barrier films with QR codes delivers freshness and traceability in one touchpoint. As manufacturing technology such as vacuum microwave dehydration matures, cost differentials versus baked treats are anticipated to narrow.

By Ingredient Source: Sustainability drives hybrid innovation

Animal-based recipes retained 68.1% of the global natural dog treats market share in 2024, capitalizing on consumer belief that canine biology demands meat-first nutrition. Grain-inclusive variants using heritage barleys are nevertheless reclaiming space as veterinarians caution against exotic-protein-linked DCM (Dilated Cardiomyopathy) cases. Hybrid and upcycled formulas sport the fastest trajectory at 10.2% CAGR. Upcycled seafood collagen chews carry joint-health claims, blending functionality with circular-economy messaging. Plant-centric innovations include spirulina-enriched crisps that deliver complete amino acid profiles while emitting a fraction of livestock greenhouse gases. Regulatory openings, such as the European Food Safety Authority's approval of mycelium protein, will catalyze Research and Development investment into fungal and microbial sources.

MicroHarvest’s microbial protein treats scored 10% higher palatability than poultry controls in companion-animal panels, debunking concerns about taste acceptance. Insect-based inputs such as black soldier fly are gaining GRAS (Generally Recognized As Safe) status in multiple jurisdictions, though scale remains regionally constrained. Co-branding with human-food upcycling initiatives, like breweries supplying spent grain, helps communicate provenance. As Scope 3 reporting tightens, ingredient origin will influence buyer decision matrices alongside flavor and price.

By Distribution Channel: Digital transformation accelerates market access

Pet specialty outlets held 45.0% of 2024 turnover, anchoring the natural dog treats market through expert advice and curated assortments. Grooming and veterinary services bundled within these stores create traffic loops that online rivals struggle to replicate. E-commerce is growing rapidly at a compound annual growth rate (CAGR) of 13.1%, as same-day delivery becomes increasingly common. Digital marketplaces enable long-tail assortment breadth, showcasing single-ingredient or hypoallergenic Stock Keeping Units that brick-and-mortar cannot stock. Social-commerce live streams drive impulse buys and harvest zero-party data for hyper-targeted retargeting. Supermarkets have improved natural sets with end-cap education, but remain primarily volume channels for mid-priced lines.

Mars, Incorporated's USD 1 billion analytics push aims to double online revenue by employing machine-learning models that predict replenishment timing down to the day. Veterinarian clinics are monetizing clinical credibility by stocking prescription-adjacent functional treats, capturing share from pet specialty. Click-and-collect hybrid models shorten last-mile emissions while sustaining impulse walk-in traffic. Amazon’s rollout of temperature-controlled lockers could remove remaining friction for frozen formats. Emerging markets in Southeast Asia demonstrate leapfrogging behavior, with over half of natural treat purchases already being made through mobile super-apps that integrate payment and delivery services.

By Dog Size: Large breed segment emerges as a growth driver

Small breeds represented 40.0% of 2024 sales, dominating the global natural dog treats market amid urban living patterns that favor compact companions. Owners prefer mini heart-shaped biscuits and low-calorie dental sticks tailored for smaller jaws. Large dogs show the sharpest momentum with a 10.5% CAGR as suburban migration increases yard space. Calorie-dense chews fortified with glucosamine mitigate joint stress in breeds exceeding 70 lbs, commanding price premiums of up to 25%. Breed-specific subscription boxes curate portion-controlled assortments, addressing overfeeding documented in 84% of Romanian households. Medium-sized dogs maintain a stable core, benefiting from crossover products that balance calorie content and chew durability.

Manufacturers are redesigning extrusion dies and freeze-drying grids to accommodate larger piece geometries without compromising structural integrity. Size-adapted QR codes on packs link to feeding calculators that adjust treat allowances based on body-condition-score inputs. Retail planograms segment by dog size to simplify navigation and minimize accidental mis-sizing purchases. Insurance providers increasingly require adherence to vet-approved feeding guidelines, further institutionalizing size-specific education. As canine obesity rises, functional treats with satiety fibers could gain traction across all sizes, but particularly in large breeds where metabolic stress is higher.

Geography Analysis

North America remains the largest regional market for natural dog treats, driven by high pet ownership and premium spending patterns. The region benefits from regulatory clarity under the Association of American Feed Control Officials labeling rules, which support consumer trust in “natural” claims and facilitate quicker market entry for new products. In Canada, similar trends are observed as retailers expand clean-label assortments and loyalty programs to meet the growing demand.

Asia-Pacific is experiencing significant growth in the natural dog treats market, fueled by increasing urbanization and smaller household sizes, particularly in countries like China, India, and Southeast Asia. Younger consumers, including Millennials and Generation Z, prioritize pet health and wellness, treating pets as family members. E-commerce platforms such as JD.com, Tmall, and Petoo play a crucial role in distributing premium treats across both urban and rural areas. Markets like India and key Southeast Asian countries, including Vietnam, Singapore, and Malaysia, are witnessing robust growth, supported by smartphone-based retail and social-commerce initiatives.[1]OpenGov Asia, "Vietnam and Thailand: SEA's Fastest-Growing E-Commerce Market," opengovasia.com

Europe, South America, the Middle East, and Africa together account for the remaining share with heterogeneous drivers. Europe enforces FEDIAF (European Pet Food Industry Federation) and the European Union Regulation 767/2009, which elevates documentation costs but also protects “natural” claims.[2]FEDIAF, “The safety of pet food,” FEDIAF.ORG Sustainability resonates strongly, with a significant portion of French shoppers favoring eco-centric labels. Brazil and Chile are prominent in South America, with Chile’s market driven by the growing middle class and increasing pet humanization. Expatriate populations contribute to the demand for premium products in the Gulf Cooperation Council, while the African market is still in its early stages but is gradually expanding alongside economic growth.

Competitive Landscape

The natural dog treats market remains moderately concentrated, with the five largest suppliers holding more than 50% revenue share in 2024, giving the category a balanced mix of scale efficiencies and innovation headroom. Mars, Incorporated, Nestle Purina (Nestle S.A.), Blue Buffalo Company, Ltd. (General Mills Inc.), Wellness Pet, LLC, and The J.M. Smucker Company wield extensive distribution, research budgets, and brand equity. Investment trends highlight a pivot to digital Mars, Incorporated, earmarking USD 1 billion for AI tools that power recipe optimization and predictive inventory, while Hill’s completed a USD 450 million smart factory outfitted with advanced automation.

Acquisitive activity is narrowing opportunities in the premium segment. Blue Buffalo Company, Ltd. (General Mills Inc.) has expanded its portfolio with the acquisition of Whitebridge Pet Brands, adding notable brands to its natural product lineup. Similarly, Pure Treats has enhanced its production capabilities through a strategic capacity deal, while SunRice Group has entered the Australian market through a significant acquisition. Venture capital is increasingly directed toward platforms emphasizing personalization and sustainability. Companies like the Chilean startup Tributo Natural are gaining traction by focusing on upcycled inputs and transparent sourcing practices.

Smaller challengers exploit e-commerce reach and social marketing to attract niche audiences. Brands such as Jack’s Premium use upcycled salmon skins to satisfy ethical protein demand while limiting raw material cost exposure. AI-based diagnostics from Ollie and DIG Labs integrate feeding guidance, creating high-switching-cost ecosystems. Competitive differentiation is increasingly anchored in credible functional claims and measurable ESG footprints.

Natural Dog Treats Industry Leaders

-

Mars, Incorporated

-

Nestlé Purina (Nestlé S.A.)

-

Blue Buffalo Company, Ltd. (General Mills Inc.)

-

Wellness Pet, LLC

-

The J.M. Smucker Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: J.M. Smucker is investing USD 52.6 million to upgrade its Milk-Bone manufacturing facility in Buffalo. The investment aims to expand production capacity and meet rising consumer demand. The facility upgrade includes modernizing equipment and improving production flow, while creating additional employment opportunities. The expansion aligns with increasing consumer preference for soft, natural dog treats and less processed pet snacks.

- January 2025: The Nutriment Company acquired The Dog's Butcher and Your Pet Nutrition, broadening its United Kingdom raw portfolio, including natural dog treats with over 100 locally sourced SKUs and veterinarian-designed supplements.

- December 2024: General Mills Inc. completed its USD 1.45 billion acquisition of Whitebridge Pet Brands' North American operations, which include Tiki Pets and Cloud Star brands. The acquisition expands General Mills Inc.' presence in the natural pet nutrition market, particularly within specialty retail and e-commerce segments.

- October 2024: Pure Treats Inc., the manufacturer of PureBites, acquired Bar W Foods and 18 Below Partners, which includes a United States Department of Agriculture-inspected, human-grade freeze-drying facility in Texas. The acquisition expands the company's capacity to produce minimally processed, raw treats and reinforces its position in the natural pet nutrition market.

Global Natural Dog Treats Market Report Scope

| Biscuit and Baked Treats |

| Jerky and Meat Chews |

| Functional Soft Chews |

| Freeze-dried and Air-dried Treats |

| Frozen and Refrigerated Treats |

| Animal-based |

| Plant-based |

| Hybrid/Upcycled |

| Pet Specialty Stores |

| Supermarkets and Hypermarkets |

| Veterinarian Clinics |

| Online Retailers |

| Small |

| Medium |

| Large |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Product Type | Biscuit and Baked Treats | |

| Jerky and Meat Chews | ||

| Functional Soft Chews | ||

| Freeze-dried and Air-dried Treats | ||

| Frozen and Refrigerated Treats | ||

| By Ingredient Source | Animal-based | |

| Plant-based | ||

| Hybrid/Upcycled | ||

| By Distribution Channel | Pet Specialty Stores | |

| Supermarkets and Hypermarkets | ||

| Veterinarian Clinics | ||

| Online Retailers | ||

| By Dog Size | Small | |

| Medium | ||

| Large | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the forecast value of global natural dog treats sales by 2030?

The category is anticipated to generate USD 10.1 billion in 2030, up from USD 6.2 billion in 2025.

Which product format is growing fastest in premium canine snacks?

Freeze-dried and air-dried treats are projected to rise at a 11.6% CAGR through 2030 due to raw-like positioning and nutrient retention.

How large is the online channel in natural treats?

Online retailers are on track to handle USD 4.6 billion by 2030, expanding at a 13.1% CAGR from their 2024 base.

Which region shows the quickest expansion?

Asia-Pacific leads growth, with freeze-dried and air-dried sales climbing at 12.9% CAGR amid rising disposable income and e-commerce adoption.

What share do upcycled or hybrid proteins hold today?

Hybrid and upcycled ingredients currently represent 10.2% of global revenue and are the fastest-growing ingredient category.

Page last updated on: