UV Printers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

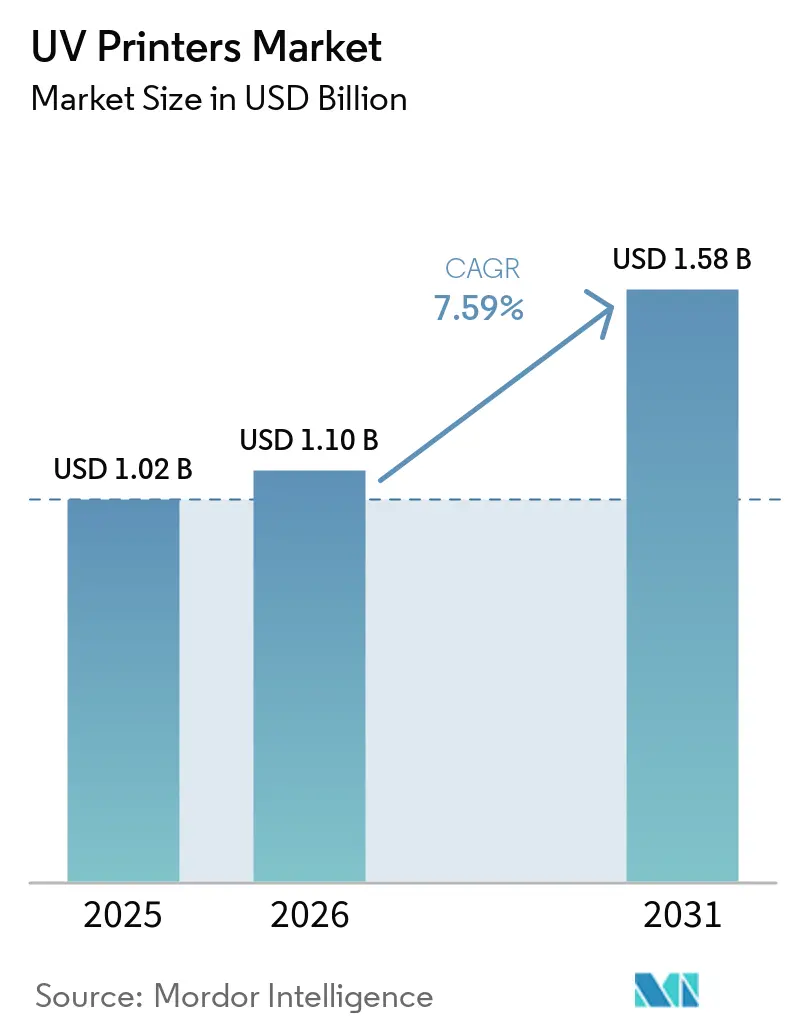

| Market Size (2026) | USD 1.10 Billion |

| Market Size (2031) | USD 1.58 Billion |

| Growth Rate (2026 - 2031) | 7.59% CAGR |

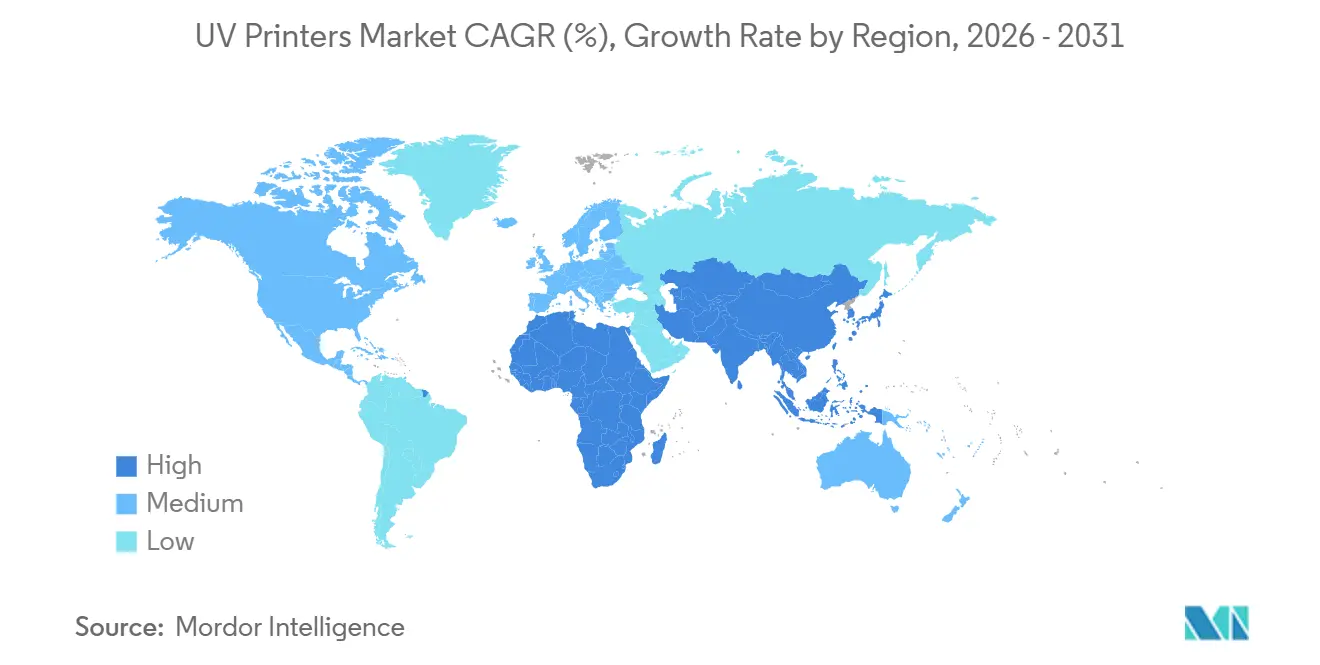

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

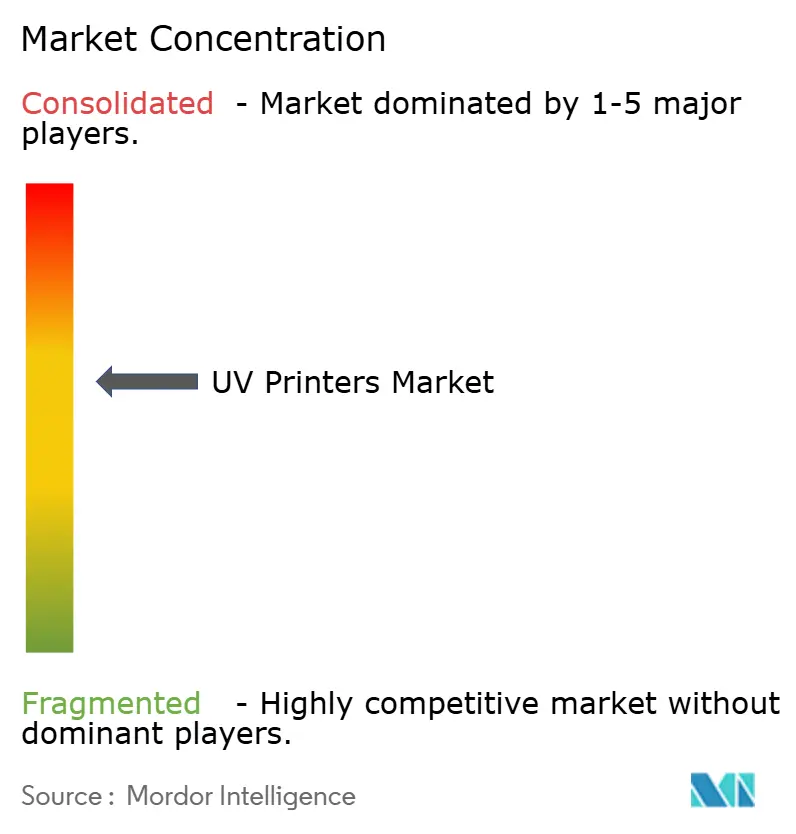

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UV Printers Market Analysis by Mordor Intelligence

The UV printers market size was valued at USD 1.02 billion in 2025 and is estimated to grow from USD 1.10 billion in 2026 to reach USD 1.58 billion by 2031, at a CAGR of 7.59% during the forecast period (2026-2031). Energy-saving UV LED curing, rising demand for short-run customized packaging, and the migration of industrial inkjet into electronics manufacturing are combining to keep replacement cycles brisk and capital expenditure resilient. Print service providers that consolidate flatbed and roll-to-roll work onto hybrid platforms are achieving higher asset utilization, while industrial OEMs are embedding flatbeds in automotive and consumer electronics lines to eliminate secondary finishing. At the same time, regulatory deadlines in North America and Europe are driving an accelerated switch to low-VOC, mercury-free chemistries, reinforcing UV LED’s position as the default investment choice. Heightened interest in direct-to-object printing for cylindrical substrates, bottles, and promotional items is opening lucrative niches for small-format units that fit storefronts and co-working spaces, further broadening the ultraviolet (UV) printers market.

Key Report Takeaways

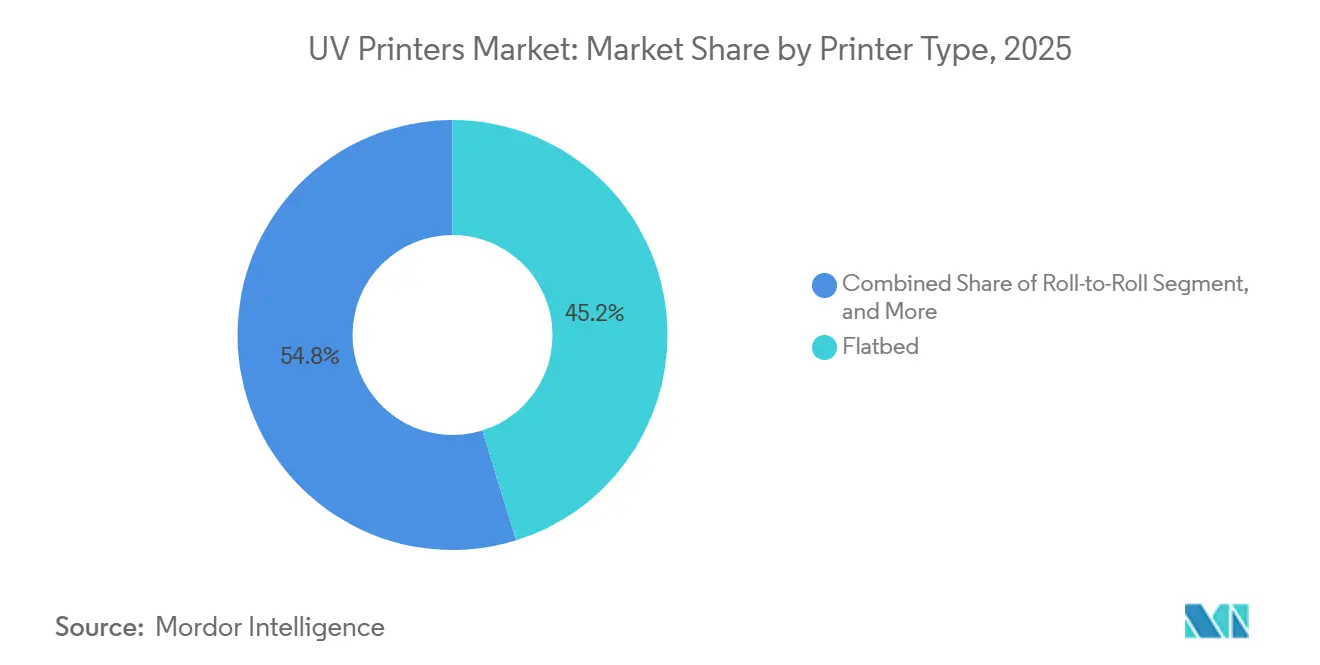

- By printer type, flatbed printers led with 45.21% of the UV printers market share in 2025, while hybrid configurations are projected to expand at a 7.86% CAGR through 2031.

- By format size, large-format systems captured 70.08% of the ultraviolet (UV) printer market share in 2025, and small- and medium-format systems are forecast to grow at a 7.65% CAGR through 2031.

- By ink source, UV-LED platforms dominated with 78.11% of the printers market share in 2025, and their installed base is expected to widen at a 7.88% CAGR over 2026-2031.

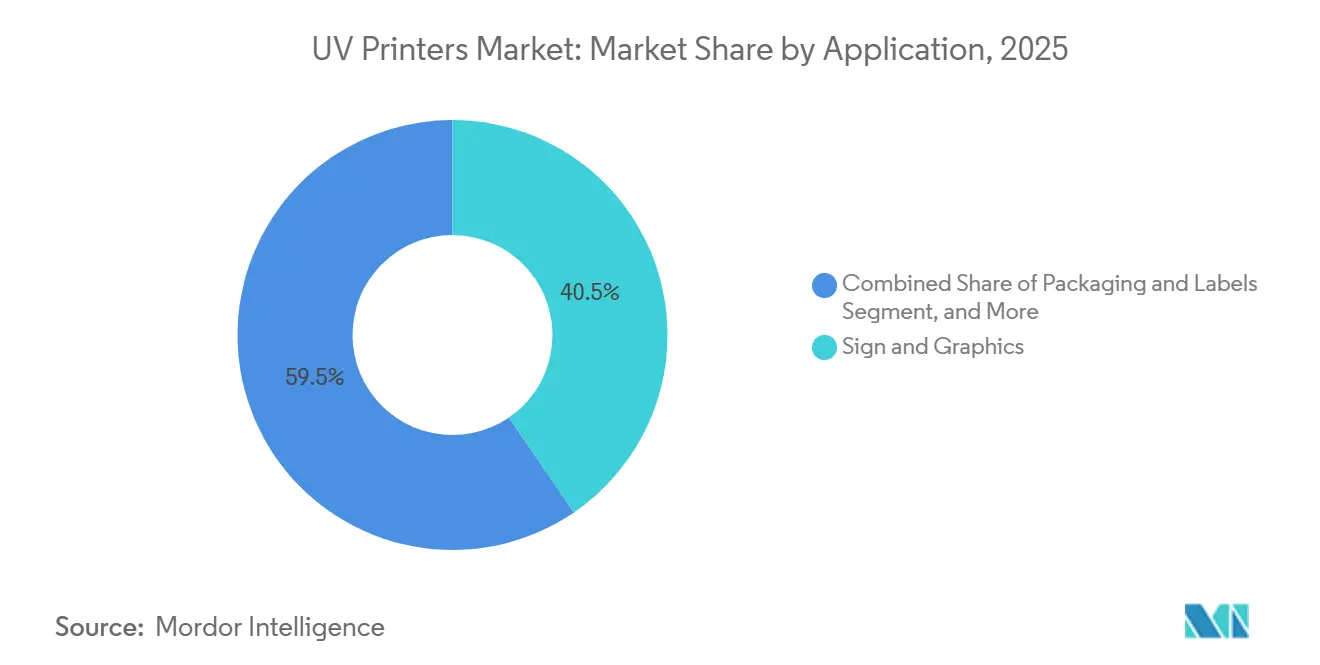

- By application, sign and graphics accounted for 40.45% of the UV printer market share in 2025; packaging and labels are set to grow at an 8.12% CAGR through 2031.

- By end user, print service providers accounted for 62.31% of the UV printer market share in 2025, while industrial OEMs recorded the fastest growth at an 8.28% CAGR through 2031.

- By geography, Asia-Pacific accounted for 38.43% of the UV printers market share in 2025, and Africa is projected to post the highest regional CAGR of 7.97% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global UV Printers Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption of UV LED-Curing Technology Reducing Operating Costs | +1.8% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Growing Demand for Short-Run Customized Packaging | +1.5% | Global, strongest in North America and Asia-Pacific | Short term (≤ 2 years) |

| Expansion of Industrial Inkjet Printing in Electronics Manufacturing | +1.3% | Asia-Pacific core, spillover to North America | Medium term (2-4 years) |

| Stringent Environmental Regulations Favoring Low-VOC UV Inks | +1.2% | Europe and North America, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Rising Investment in Direct-to-Object Printing for 3D Substrates | +0.9% | North America and Europe | Short term (≤ 2 years) |

| Accelerated Retail Rebranding Cycles Propelling Signage Replacement Rates | +0.7% | Global, concentrated in urban retail corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of UV LED-Curing Technology Reducing Operating Costs

Field measurements at a German print facility in 2024 showed UV LED arrays cutting energy use by 72.5% compared with mercury-arc lamps, with ROI within 18 months despite higher sticker prices.[1]IUV GmbH, “UV LED Curing Technology Energy Efficiency,” iuv.de Instant on-off switching removes costly warm-up cycles, while 20,000-hour diode life means bulb changes become irrelevant. The absence of ozone generation eliminates the need for exhaust ducting, which can add USD 5,000-USD 15,000 to a new shop's budget. LED’s cooler output protects thin films and foamed plastics from warping, widening the UV printers market into packaging segments once dominated by water-based or EB curing.

Growing Demand for Short-Run Customized Packaging

Plate costs of USD 800-USD 1,200 per SKU make analog flexography uneconomical below 1,000 units, pushing e-commerce brands toward digital UV lines capable of two-week turnarounds. ePac’s 2025 deal to install more than ten HP Indigo 200K presses exemplifies the rush to meet limited-edition and regional launch schedules. Variable data, QR codes, and personalized graphics add margin lift that offsets ink cost premiums, fuelling an expanding slice of the UV printers market.

Expansion of Industrial Inkjet Printing in Electronics Manufacturing

Japanese start-up Elephantech scaled a metal-inkjet PCB process to produce flexible circuits for automotive sensors without hazardous etching, reducing prototype cycles from 6 weeks to 48 hours. Austrian institute PROFACTOR subsequently demonstrated multi-material UV printing of silver nanoparticle inks and dielectrics, aligning UV inkjet with IoT module development. These breakthroughs encourage electronics OEMs to specify UV printers on research and development lines, deepening industrial penetration.

Stringent Environmental Regulations Favoring Low-VOC UV Inks

The US EPA hardened VOC limits to 25 g L⁻¹ for packaging inks in 2024, pushing converters toward UV LED systems that emit negligible VOCs after cure. Simultaneously, EU REACH bans on UV-328 and the pending April 2027 sunset for certain phosphine oxide initiators are driving rapid reformulation. Suppliers that validated compliant photoinitiator packages early secured multi-year deals with automotive and consumer electronics brands, reinforcing first-mover advantages.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Capital Expenditure for Wide and Superwide Format Printers | -1.4% | Global, acute in emerging markets and SME segments | Short term (≤ 2 years) |

| Limited Substrate Compatibility for Certain UV Ink Formulations | -0.8% | Global, concentrated in specialty applications | Medium term (2-4 years) |

| Supply Chain Volatility in UV LED Chips and Photoinitiators | -0.6% | Global, most severe in Europe and North America | Short term (≤ 2 years) |

| Skilled Operator Shortage Hindering Optimal Utilization | -0.5% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial Capital Expenditure for Wide and Superwide Format Printers

Production-class UV hybrids run USD 80,000-USD 250,000, an outlay that strains SMEs in regions where leasing penetration is below 20%. A 2025 MTU Tech analysis pegged the first-year cash requirement for a mid-range flatbed at USD 70,000, a level many shops earning under USD 200,000 annually cannot absorb.[2]MTU Tech, “UV Printer ROI: Calculating the Return on Your Investment,” mtutech.com Desktop units under USD 15,000 fill hobby niches but lack throughput, leaving a financing gap that slows the expansion of the ultraviolet (UV) printer market in developing economies.

Limited Substrate Compatibility for Certain UV Ink Formulations

PP and PE parts with surface energies below 38 mN m⁻¹ require corona treatment for ink adhesion, adding steps that erode UV’s time advantage. Glass presents the opposite hazard, which overly bonds and creates fracture risks during thermal cycling. Flexible textiles require costlier, stretchy chemistries that narrow color gamut while boosting ink budgets 20%-30%. Such material-specific hurdles complicate inventory and risk costly printhead contamination, tempering the addressable scope of the UV printers market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Printer Type: Hybrid Configurations Consolidate Workflows

Hybrid platforms pulled a 7.86% CAGR outlook because they let operators pivot between rigid and roll stock without unbolting media, raising uptime by 30% compared with two single-purpose units. Flatbeds with 45.21% share continued to dominate interiors and industrial décor, where 8-inch Z-clearance accommodates thick substrates, whereas roll-to-roll lines retained speed leadership on flexible banners. The UV printers market for flatbeds remains anchored by promotional products and rigid signage, but hybrids are winning new orders as PSPs retrofit floor plans for multifunction gear. Maintenance complexity does rise, servo-driven roll handlers and vacuum zones add USD 15,000-USD 25,000 to purchase price, yet surveys show faster payback when job mixes swing unpredictably.

The UV printers market also witnessed Turkish firm UVionArt demonstrate flatbeds printing of scratch-resistant architectural glass, highlighting how niche applications sustain demand for dedicated rigs. Conversely, soft-signage specialists still prefer continuous roll feeders for seamless 50-meter banners. A growing subset of packaging prototypers now uses hybrids to print both E-flute carton mock-ups and pressure-sensitive label stock in a single shift, slashing changeovers from 2 hours to 15 minutes. As automation levels climb, hybrids are expected to grab share from single-purpose systems without cannibalizing the high-end flatbed market.

By Format Size: Compact Platforms Unlock Direct-To-Object Revenues

Large-format units measuring 1.5 m or more in width accounted for 70.08% of 2025 sales, driven by transit advertising and building wraps. Yet small and medium formats are growing at 7.65% CAGR, propelled by front-of-house custom gift shops and in-store kiosks adopting desktop UV models that slide through a standard doorway. Roland’s LEF2-200 at USD 14,995 exemplifies this democratization, enabling single-operator stores to produce phone cases and trophies without rigging crews.[3]ABT Printing Solutions, “How Much Should You Pay for a UV Printer in 2025?” yourabt.com Direct-to-object capacity to decorate 32 tumblers in 10 minutes illustrates why compact rigs monetize high-margin personalization with minimal floor space.

Large-format lines maintain throughput economies, hitting 110 boards per hour on 4x8-foot sheets, keeping the cost per square meter below USD 5 at volumes above 500 m² per month. Mid-format bridges like Epson’s V7000 deliver large-board capability on single-phase power, making them suitable for suburban shops that lack three-phase service. Urban rent pressures tilt demand toward smaller footprints, so format choice increasingly aligns with real estate economics rather than with the application mix alone. Collectively, diversification by size segments keeps the ultraviolet (UV) printers market rolling across enterprise scales.

By Ink Source: UV-LED Supplants Mercury Across Install Base

LED curing captured 78.11% of the market in 2025 and is forecast to expand by 7.88% annually as mercury lamps are phased out under the Minamata Convention. Module prices fell 18% in 2024-2025, while bulb disposal fees climbed, flipping the total cost of ownership math. A five-year cost comparison by SENA showed LED workflows at USD 158,750 versus USD 337,500 for mercury, saving USD 178,750, even when hardware stickers cost 20% more. The UV printers market size tied to mercury systems now largely represents a replacement opportunity, with vendors dangling trade-in credits to accelerate switchovers.

LED’s cool spectral output lets converters tackle heat-sensitive films, while instant curing permits sheet stacking without inter-stage drying. Legacy varnish jobs requiring deep-ink films still rely on high-intensity mercury flashes, so niche applications remain. Nonetheless, the trajectory is decisive; module lifetimes four times longer than arc bulbs reduce unscheduled downtime, and the elimination of ozone simplifies local air-quality compliance, bedding in LED as the long-term default in the UV printers market.

By Application: Labels and Packaging Drive Future Volume

Signs and graphics accounted for 40.45% of revenue in 2025, yet packaging and labels are projected to grow at an 8.12% CAGR. Variable data, serialization, and SKU proliferation make UV inkjet’s plate-free economics irresistible for snack, coffee, and pet treat converters. Flexible films, once reliant on rotogravure, are now printed digitally in 5,000-unit bursts that ship within two weeks. Industrial manufacturing uses UV to decorate automotive dashboards and appliance fronts in-line, eliminating lamination steps that historically added 3 days of work-in-progress.

Electronics and PCB prototyping, though a small slice, captures outsized attention due to high-value functional layers printed in thicknesses under 10 µm by desktop systems such as BotFactory’s SV2. Interior décor gains from faux-wood and marble finishes inkjet-printed on MDF at one-third the cost of natural materials. Collectively, these diversifying use cases enlarge the UV printers market beyond its traditional signage core.

By End-User Industry: OEM Integration Accelerates

Print service providers still dominate with 62.31% share, aggregating varied customer needs across signage, décor, and promotional products. However, industrial OEMs integrating printers on assembly lines are clocking the fastest growth at 8.28% CAGR as they mark dashboards, electronics housings, and small appliances directly, trimming supply chain steps. A craft brewer that installed a cylindrical UV unit sold out a limited run of custom-printed bottles in two days, illustrating the pull of in-house control.

Corporate in-plant rooms increasingly rely on mid-format UV rigs to produce same-day marketing collateral, thereby eliminating delays associated with outsourcing and gaining greater internal agility. In response to this shift, print service providers (PSPs) have adapted by offering equipment-plus-service bundles. These bundles transfer operational risks away from small and medium-sized enterprises (SMEs) while ensuring PSPs retain a steady revenue stream through click-based consumable models. This hybrid approach has significantly expanded the ultraviolet (UV) printing market, serving both outsourcing and captive production needs.

Geography Analysis

Asia-Pacific generated 38.43% of global revenue in 2025, underpinned by China’s UV LED chip foundries, Japan’s high-precision printhead research and development, and India’s regulatory push against solvent emissions. China’s smartphone and automotive clusters value flatbeds that register layers within 100 µm on curved parts, anchoring demand for high-accuracy platforms. Mimaki’s May 2026 launch of the UJV200-160 with automatic dot adjustment targets PSPs seeking to widen material menus without adding headcount. Meanwhile, India’s Maharashtra and Gujarat states tightened VOC caps, prompting solvent shops to migrate to UV LED workflows free of exhaust ducting.

North America combines robust direct-to-object adoption with a pronounced skills gap; 95% of print shops report difficulty recruiting operators, prompting vendors to embed workflow automation and remote diagnostics. Ricoh’s March 2026 alliance with LogoJET leverages that need by bundling small-format DTO units into existing wide-format fleets.[4]Print and Promo Marketing, “Ricoh USA Partners With LogoJET,” printandpromomarketing.com Europe’s converters prioritize REACH-compliant inks, illustrated by Fotocenter.es installing Agfa’s Ciervo H2500 hybrid in January 2026 to future-proof personalized photo output. Canada, facing similar labor shortages, has seen service contracts eclipse hardware margins as suppliers offer uptime guarantees to offset operator deficits.

South America, the Middle East, and Africa deliver the fastest trajectories. Dubai and Abu Dhabi are positioning as exhibition graphics hubs, boosting hybrid printer imports, while South Africa and Egypt shift from solvent to UV to meet occupational exposure rules. Africa’s 7.97% CAGR benefits smaller sign shops upgrading to LED units that run on single-phase power, cutting hazardous-waste handling costs. Brazil’s flexible packaging lines embraced UV inkjet for food labels, capitalizing on rapid SKU turnover. Financing remains a constraint as equipment leasing penetration averages below 20%, so vendors offering deferred payment or ink-indexed leases are capturing share in the UV printers market.

Competitive Landscape

The market is moderately concentrated, with Japanese incumbents Mimaki, Epson, and Roland DG continuing to command premium slices through proprietary printhead technology and nationwide service infrastructures. European specialists Agfa, Durst, and swissQprint dominate high-speed industrial flatbeds aimed at packaging converters. Chinese challengers HandTop and Flora undercut mid-range pricing by 30%-40% by pairing Epson and Ricoh heads with value-engineered chassis, forcing incumbents to pivot toward software-led differentiation such as nozzle-fail compensation and predictive maintenance. Brother’s March 2026 purchase of Mutoh for USD 230 million signals accelerating consolidation as scale and vertical integration become competitive prerequisites.[5]World Imaging News, “Brother Industries Completes Acquisition of Mutoh Holdings,” worldimagingnews.com

Direct-to-object upstarts create fresh white space. LogoJET’s tie-up with Ricoh reframes small-format cylindrical printers as line extensions, not standalone niche gear, helping PSPs step into promotional goods without new operators. Suppliers bundling ISO-12647 color compliance, automated profiling, and application engineering labs achieve retention rates 20% higher than hardware-only sellers, underscoring the shift from iron-centric to solution-centric competition. Finance innovation also matters; trade-in credits for mercury rigs, ink-indexed leases, and click-charge consumable models lower adoption barriers, sustaining churn in the UV printers market even where capex appears daunting.

Mid-segment hybrids priced USD 50,000-USD 100,000 remain underserved, representing an opportunity for challengers able to balance throughput, versatility, and footprint. Workflow orchestration, not pure speed, is emerging as the decisive purchase criterion as PSPs juggle shorter runs, more substrates, and shrinking turnarounds. Consequently, software ecosystems, remote analytics, and subscription models will likely frame the next competitive battleground rather than incremental DPI gains.

UV Printers Industry Leaders

HP Inc.

Canon Inc.

Fujifilm Holdings Corporation

Mimaki Engineering Co., Ltd.

Seiko Epson Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Brother Industries finalized the USD 230 million takeover of Mutoh Holdings, absorbing VerteLith RIP and UV-LED know-how into a broader wide-format lineup.

- March 2026: Ricoh USA partnered with LogoJET to distribute direct-to-object UV systems across North America, tapping a segment forecast to climb 9.5% annually through 2030.

- March 2026: Polyplex Corporation acquired a 51% stake in TechNova Printrite for INR 621 million (USD 7.4 million) to strengthen its digital print media play and secure polyester film synergies.

- January 2026: Agfa Inkjet Solutions sold its 2.5-m Ciervo H2500 hybrid to Spain’s Fotocenter.es during C! Print Madrid, citing 169 m² h print speed and energy-efficient LED curing.

- September 2025: UK PSP PressOn replaced two aging hybrids with a Fujifilm Acuity Ultra Hybrid LED to raise speed, quality, and media versatility via Broadstairs-made Uvijet UH inks.

Global UV Printers Market Report Scope

The UV Printers Market comprises the global industry involved in the development, manufacturing, distribution, and deployment of ultraviolet (UV) curing-based digital printing systems used across commercial, industrial, and specialty printing applications. UV printers use UV-curable inks that harden instantly under ultraviolet light, enabling high-speed printing, enhanced durability, vibrant color output, and compatibility with a wide range of rigid and flexible substrates.

The UV Printers Market Report is Segmented by Printer Type (Flatbed, Roll-to-Roll, and Hybrid), Format Size (Small and Medium Format, and Large Format), Ink Source (UV-LED, and Mercury-Arc), Application (Sign and Graphics, Packaging and Labels, Industrial Manufacturing, Textile and Soft Signage, Interior Décor, and Electronics and PCB Prototyping), End-user Industry (Print Service Providers, In-house, and Industrial OEMs), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Flatbed |

| Roll-to-Roll |

| Hybrid |

| Small and Medium Format |

| Large Format |

| UV-LED |

| Mercury-Arc |

| Sign and Graphics |

| Packaging and Labels |

| Industrial Manufacturing |

| Textile and Soft Signage |

| Interior Décor |

| Electronics and PCB Prototyping |

| Print Service Providers (PSPs) |

| In-house |

| Industrial OEMs |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Israel | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Printer Type | Flatbed | |

| Roll-to-Roll | ||

| Hybrid | ||

| By Format Size | Small and Medium Format | |

| Large Format | ||

| By Ink Source | UV-LED | |

| Mercury-Arc | ||

| By Application | Sign and Graphics | |

| Packaging and Labels | ||

| Industrial Manufacturing | ||

| Textile and Soft Signage | ||

| Interior Décor | ||

| Electronics and PCB Prototyping | ||

| By End-user Industry | Print Service Providers (PSPs) | |

| In-house | ||

| Industrial OEMs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current UV printers market size and projected growth?

The UV printers market size stands at USD 1.10 billion in 2026 and is expected to reach USD 1.58 billion by 2031, expanding at a 7.59% CAGR (Mordor Intelligence).

Which printer type holds the largest share?

Flatbed units led the UV printers market share with 45.21% of 2025 revenue (Mordor Intelligence).

Why are UV-LED systems replacing mercury-arc lamps?

UV-LED arrays cut energy use by more than 70%, last up to 20,000 hours, and avoid mercury disposal, delivering lower total cost of ownership.

Which application segment is growing fastest?

Packaging and labels are forecast to grow at an 8.12% CAGR through 2031 as brands demand variable-data, short-run jobs (Mordor Intelligence).

How are hybrid printers changing buying decisions?

Hybrids combine flatbed and roll-to-roll jobs on one chassis, raising asset utilization by around 30% and cutting floor-space needs.

What regions are showing the highest CAGR?

Africa leads with a 7.97% CAGR to 2031, followed by strong gains in South America and the Middle East as solvent printers are replaced.

Page last updated on: