Inkjet Printing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

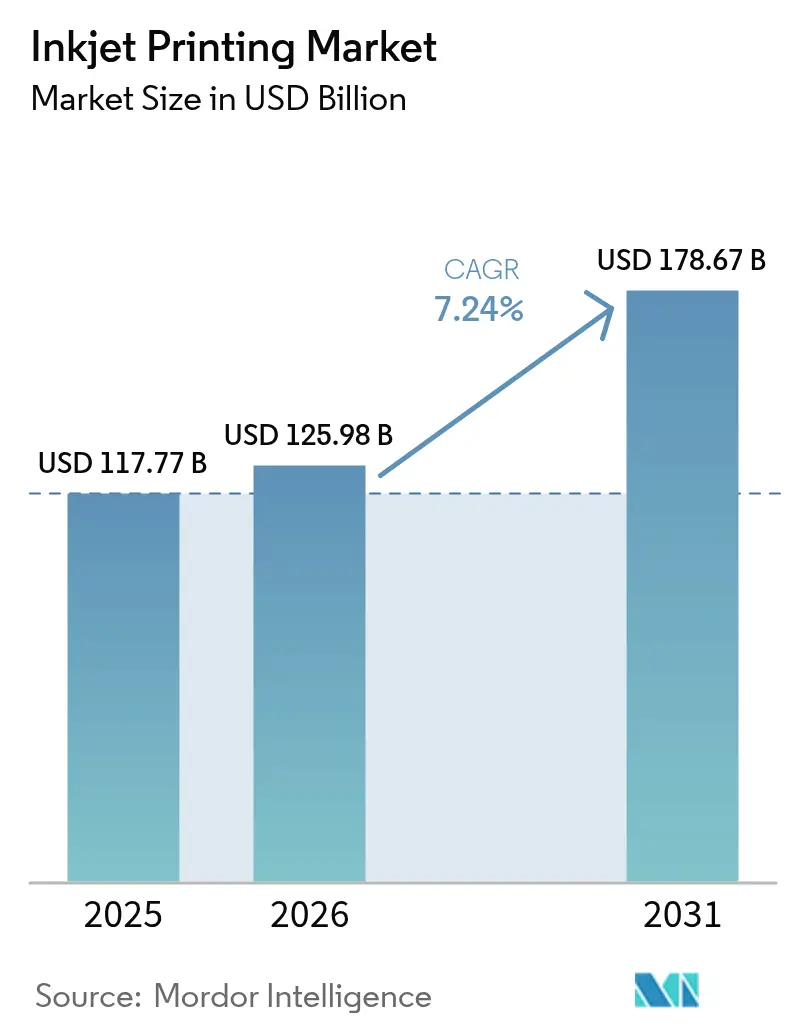

| Market Size (2026) | USD 125.98 Billion |

| Market Size (2031) | USD 178.67 Billion |

| Growth Rate (2026 - 2031) | 7.24% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Inkjet Printing Market Analysis by Mordor Intelligence

The inkjet printing market size was valued at USD 117.77 billion in 2025 and is estimated to grow from USD 125.98 billion in 2026 to reach USD 178.67 billion by 2031, at a CAGR of 7.24% during the forecast period (2026-2031). A clear shift from offset and flexographic systems toward agile digital workflows underpins this expansion. Brand owners worldwide now require shorter production runs, late-stage customization, and serialized data on every unit, all of which favor drop-on-demand and continuous inkjet architectures. Single-pass presses that exceed 300 meters per minute have narrowed the historical cost-per-impression gap with flexo, compressing payback periods for capital equipment. At the same time, cloud-based color management platforms automate substrate profiling and predictive maintenance, further lowering the total cost of ownership. Supply-side risks linked to piezoelectric ceramics persist, yet buyer willingness to pay for variable data, quick turnround, and sustainable inks continues to outweigh those headwinds.

Key Report Takeaways

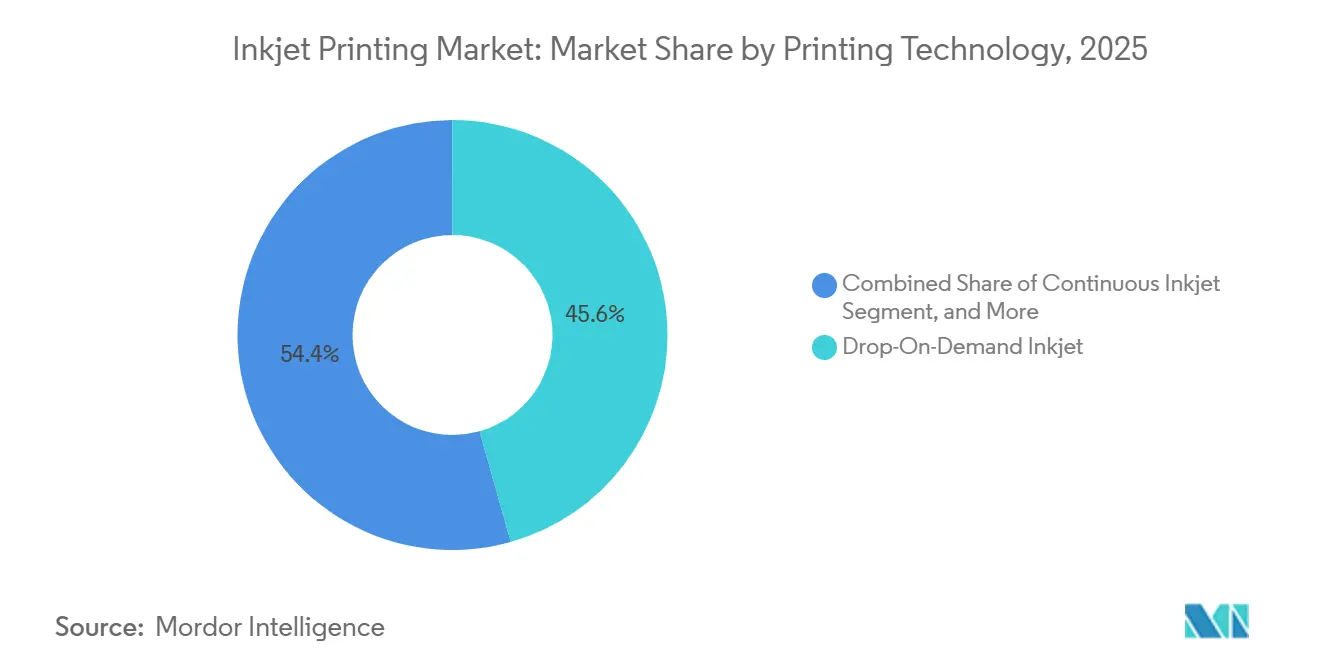

- By printing technology, drop-on-demand captured 45.63% of the share in 2025, whereas continuous inkjet is projected to expand at an 8.45% CAGR through 2031.

- By ink type, aqueous formulations accounted for 34.77% of the market share in 2025, while the latex chemistries segment is forecast to grow at an 8.23% CAGR.

- By component, printers represented 50.68% of the share in 2025, yet the software and services segment is set to climb at an 8.77% CAGR.

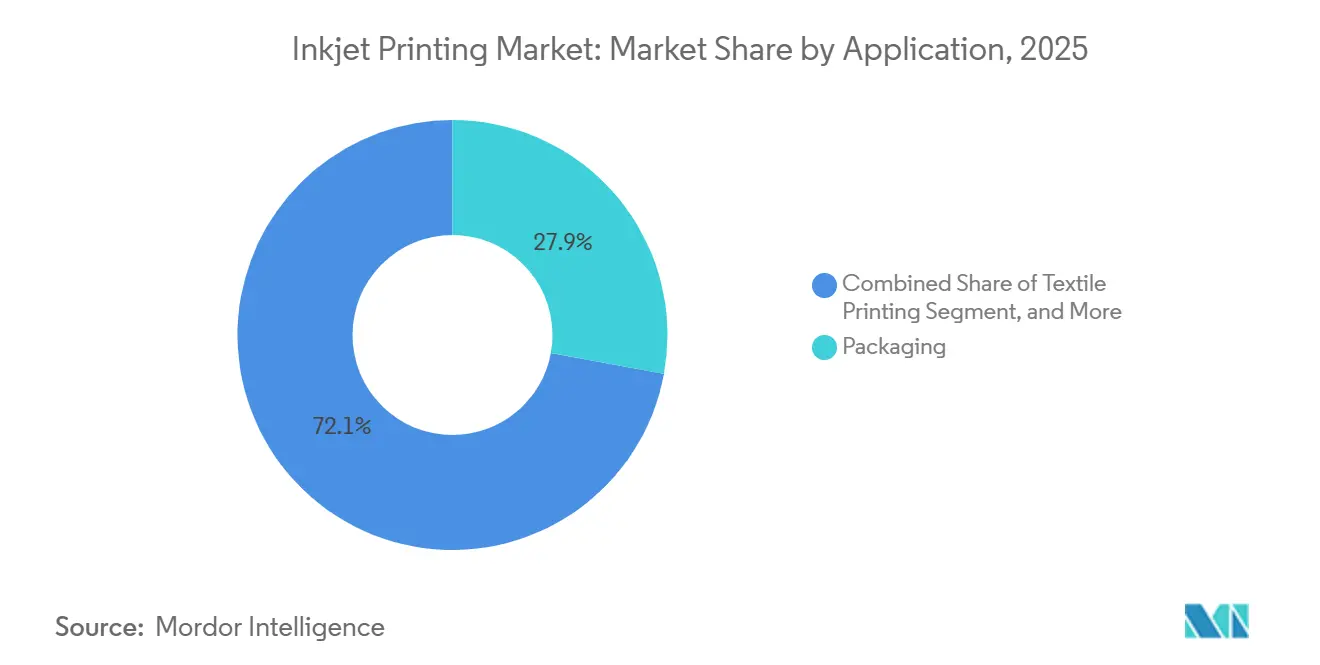

- By application, packaging accounted for 27.88% of the share in 2025, whereas textile printing is poised to surge at a 9.12% CAGR.

- By substrate material, paper and paperboard held 40.71% of the share in 2025, but the textile substrates segment is expected to rise at a 9.24% CAGR.

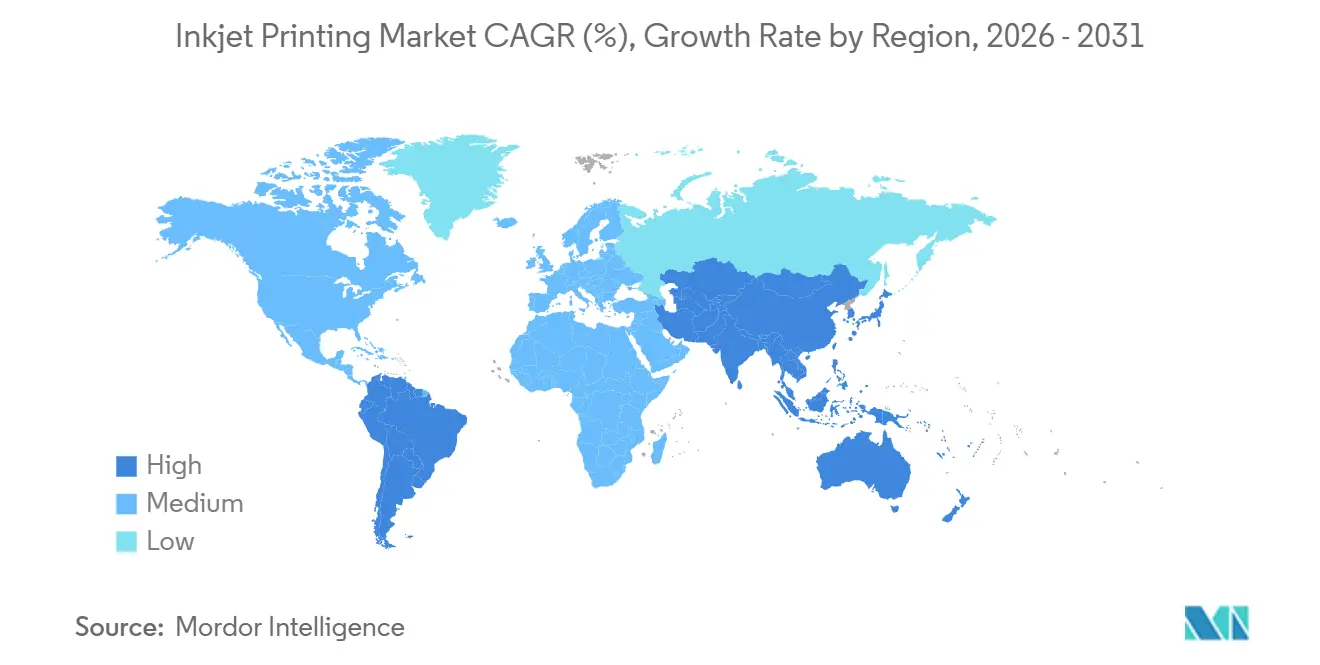

- By geography, Asia-Pacific led with a 39.87% share in 2025, and South America is anticipated to rise at a 9.09% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Inkjet Printing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-Driven Packaging Demand from FMCG and Food Sectors | +1.8% | Global, Asia-Pacific and Europe concentration | Medium term (2-4 years) |

| Proliferation of Short-Run, On-Demand Publishing | +1.2% | North America and Europe | Short term (≤ 2 years) |

| Growth of Industrial Décor and Direct-to-Shape Printing | +1.0% | Global, early gains in North America and Asia-Pacific | Medium term (2-4 years) |

| Advent of Single-Pass, High-Speed Inkjet Presses | +1.5% | Global, early adoption in Europe and North America | Long term (≥ 4 years) |

| Shift Toward Decentralized Micro-Factories Enabling Just-in-Time Customization | +0.9% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Rapid Adoption of Enzyme-Based Colorants for Biodegradable Textiles | +0.6% | Europe and North America, spillover to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-Driven Packaging Demand from FMCG and Food Sectors

Serialized QR codes, batch identifiers, and allergen warnings are now standard on primary packaging, a requirement amplified by European carbon disclosure rules due by 2027.[1]HP Inc., “HP Indigo Digital Presses,” hp.com Regional converters deploy digital presses that swap artwork without plate changes, letting brands pilot limited-edition flavors without holding excess inventory.[2]Domino Printing Sciences, “Thermal Inkjet Modules for Flexible Packaging,” domino-printing.com Contracts such as HP Inc.’s USD 50 million Indigo deal with ePac Holdings illustrate the scale of investment. In dairy and snack categories, shelf-life pressure makes frequent label changes unavoidable, driving further uptake. Converters that master variable data workflows gain stickier relationships with retailers who track origin and freshness in near real time.

Advent of Single-Pass, High-Speed Inkjet Presses

Single-pass architecture places every color bar inline, achieving throughputs once reserved for offset while still printing unique data on every sheet.[3]Agfa-Gevaert, “SpeedSet Orca Single-Pass Press,” agfa.com Systems like Agfa-Gevaert’s SpeedSet Orca reach 11,000 sheets per hour, while Fujifilm-Barberán’s HS Series runs 350 meters per minute on decorative laminates. Makeready waste falls up to 70%, an advantage in an era of elevated substrate costs. These platforms attract converters in pharmaceuticals and direct mail that need offset quality plus serialization. Water-based chemistries compliant with Nordic Swan ecolabels further accelerate adoption among retailers committed to greener supply chains.

Shift Toward Decentralized Micro-Factories Enabling Just-In-Time Customization

Supply disruptions and freight volatility have prompted brands to relocate production nearer to demand centers. Compact inkjet units slot easily into micro-factories, unlike large offset lines. Roland DG’s PeriQ360 and Perivallo360m decorate cylindrical objects inside beverage co-packing plants, removing the need to ship pre-printed sleeves. HP Inc.’s PrintOS cloud now delivers remote substrate profiles so color matches across multiple small sites. The model resonates in textiles, where Brother Industries’ GTX Pro BULK outputs 1 200 shirts per day, allowing fashion startups to promise 48-hour delivery.

Rapid Adoption of Enzyme-Based Colorants for Biodegradable Textiles

Sustainability mandates push apparel and décor suppliers toward bio-based inks that break down in industrial composting. University of Vienna researchers demonstrated enzyme-catalyzed indigo with conventional fastness, proving commercial viability. Mimaki Engineering secured GREENGUARD Gold for latex inks used indoors without ventilation. Toyo Ink’s de-inking technology enables closed-loop textile recycling, meeting extended producer responsibility laws in Europe. Retailers adopting take-back programs now specify certified inks in purchase contracts, pulling demand across the value chain.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Shift of Ad-Spend into Digital Channels | -1.3% | Global, strongest in North America and Europe | Short term (≤ 2 years) |

| Persistent Capex Premium Over Legacy Flexo and Screen Lines | -1.1% | Global, acute in South America and Middle East markets | Medium term (2-4 years) |

| Tightening Effluent Discharge Limits on Nano-Pigments Across Southeast Asia | -0.5% | Southeast Asia, spillover to South Asia | Medium term (2-4 years) |

| Supply-Chain Fragility for Piezoelectric Ceramics Limiting Print-Head Availability | -0.7% | Global, acute in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerating Shift of Ad-Spend into Digital Channels

Advertisers redirect budgets toward programmatic display, social media, and connected TV. The United Kingdom logged a 1.5% slide in print ad spend during Q3 2025 while digital rose 8.2%. Newspaper closures and pagination cuts undermine run lengths for high-speed inkjet web presses, especially in North America and Europe. The revenue drag is immediate because publishers often cancel entire print editions rather than scale them back gradually. As broadband penetration tops 85% in developed markets, similar defection is emerging in parts of Asia-Pacific.

Persistent Capex Premium Over Legacy Flexo and Screen Lines

Entry-level single-pass inkjet units list 40%-60% above comparable flexographic presses. For converters serving stable, long-run work, payback often exceeds three years, a hurdle compounded by volatile exchange rates in South America and the Middle East. Although Screen Holdings now offers modular label systems that add stations over time, baseline investment still surpasses USD 1 million. Higher ink costs versus solvent formulations widen the total-cost-of-ownership delta. Until financing terms improve, smaller converters may postpone upgrades and continue depreciating legacy equipment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Printing Technology: Continuous Systems Capture High-Speed Coding

Continuous inkjet is expected to expand at an 8.45% CAGR through 2031. Continuous inkjet gained momentum because pharmaceutical, beverage, and food producers demand line speeds above 600 meters per minute. The inkjet printing market size for high-speed coding applications is expected to expand fastest under this technology cohort. Videojet and Domino have integrated thermal inkjet heads directly on conveyor lines, enabling real-time serialization for track-and-trace compliance. Meanwhile, drop-on-demand maintains leadership in wide-format graphics thanks to its superior image fidelity and substrate versatility.

The inkjet printing market share for drop-on-demand stood at 45.63% in 2025, reflecting broad usage in graphics, textiles, and packaging. Manufacturers such as Canon and Xerox now merge inline spectrophotometry with drop-on-demand to guarantee ISO-compliant color, blurring historical quality gaps with offset. In Asia-Pacific, where multi-shift factories value uptime, continuous systems gain traction despite higher initial pricing, signaling gradual mix change over the forecast horizon.

By Ink Type: Latex Inks Advance Outdoor Signage

Aqueous inks dominated with 34.77% of market share in 2025, especially for indoor graphics and publishing where low odor is mandatory. Yet latex formulations are projected to record 8.23% CAGR, as municipalities tighten volatile organic compound rules. The inkjet printing market size for latex inks is set to climb alongside growth in vehicle wraps and outdoor retail signage that must withstand abrasion without solvent emissions.

Latex adoption accelerates further because new printheads cure at lower temperatures, allowing printing on heat-sensitive textiles. Solvent technologies persist in fleet graphics where durability trumps environmental compliance, though regulatory pressure in California and the European Union is steadily eroding that niche. Hybrid UV-water-based chemistries such as Fujifilm’s Aquafuze show how vendors balance sustainability with adhesion on rigid substrates.

By Component: Software And Services Underpin Recurring Revenue

Printers still account for the largest market share of 50.68% in 2025, yet vendors increasingly monetize software subscriptions and predictive-maintenance packages. Software and services are projected to climb at an 8.77% CAGR. These services reduce unplanned downtime by nearly one-fifth and automatically replenish consumables, locking customers into branded ecosystems. The inkjet printing market size, attached to services, therefore grows faster than hardware and consumables.

Printhead suppliers remain concentrated, with a few Japanese and European firms dominating the supply of micro-machined nozzles essential for industrial presses. As cloud dashboards normalize device monitoring, converters are beginning to treat output equipment as part of an integrated data environment rather than isolated machinery. This shift is moving procurement decisions from a focus on capital expense to emphasizing lifecycle value.

By Application: Fast Fashion Speeds Textile Printing Uptake

Packaging leads with 27.88% of share in 2025 because fast-moving consumer goods need variable SKU data, but textiles deliver the sharpest future ascent, expected to surge at a 9.12% CAGR. On-demand garment production allows fashion labels to refresh designs every six weeks while avoiding unsold stock. The inkjet printing market size for custom apparel is therefore paced to widen rapidly, supported by devices capable of 1 200 shirts per day with minimal operator intervention.

Label printing stays resilient, particularly for craft beverages seeking short runs and frequent design changes. Electronics and PCB printing occupies a small, high-growth corner where solder-mask and conductive inkjet lines shorten prototype cycles. Commercial print and publishing continue to contract as content migrates online, reinforcing the strategic pivot toward industrial and packaging verticals.

By Substrate Material: Textile Fabrics Emerge As Fastest-Growing Base

Paper and paperboard remain the dominant substrates with 40.71% of share in 2025 thanks to books, cartons, and commercial print, yet polyester and cotton fabrics now post the fastest gains with 9.24% CAGR during the forecast period. Direct-to-garment workflows combine inline pre-treatment with roll-to-roll dryers, letting converters switch between apparel and home-décor orders within one shift. The inkjet printing market size for textile substrates is supported by fashion retailers demanding local, just-in-time manufacturing.

Plastic films, foils, and metal cans benefit from variable-data coding that eliminates separate label layers. Glass and ceramic tiles are another pocket of expansion as architects specify custom façades and interior panels. Specialty materials such as leather, cork, and bio-based boards command premium pricing for personalized gifts and luxury packaging, illustrating the breadth of substrate diversification.

Geography Analysis

Asia-Pacific led the inkjet printing market in 2025, capturing 39.87% of the market share on the back of China’s electronics and textile production, India’s rising packaging demand, and Japan’s printhead innovations. Government incentives for smart manufacturing in China, along with capacity expansions by Toyo Ink India, sustain a robust equipment pipeline. Local vendors in China now supply competitively priced UV and textile printers that pressure imported brands, while Japanese firms refine piezoelectric materials that power the next generation of high-frequency heads.

South America is projected to be the fastest-growing region, with a 9.09% CAGR through 2031, as converters digitalize to hedge against logistics uncertainty. Valgroup’s installation of the first HP Indigo 200K press in the region showcases a decisive move toward label runs measured in days rather than weeks. Ink production capacity additions in Brazil and a widening distributor network across Argentina and Chile enable quicker consumable supply, lowering downtime for regional users and solidifying local ecosystems.

North America and Europe together contribute nearly 45% of revenue but face maturing commercial print segments. Nevertheless, both regions lead in pharmaceutical, décor, and industrial applications where strict serialization, indoor air-quality, and color-management standards prevail. The Middle East and Africa, while smaller, exhibit accelerating adoption as free-trade zones in the Gulf incentivize localized packaging production. Turkey’s textile export base is similarly modernizing with digital printers that serve European fashion retailers demanding sustainable supply chains.

Competitive Landscape

Competitive intensity is fragmented, with the top vendors such as HP Inc., Canon Inc., Seiko Epson Corp., Fujifilm Holdings Corp., Xerox Holdings Corp., and others. These firms defend installed bases through proprietary ink chemistries, chipped cartridges, and bundled service agreements that guarantee uptime. The remaining share is fragmented across specialists targeting niches such as conductive inks, direct-to-object decoration, and large-format signage.

Technology differentiation revolves around jetting frequency, drop size control, and software-defined workflows. Fujifilm Dimatix filed 2025 patents for grayscale heads that vary voltage waveforms, enabling photographic gradients without sacrificing speed. HP Inc. lowered operating temperatures on new thermal modules, extending compatibility to heat-sensitive substrates. Compliance with ISO 12647 color and GREENGUARD indoor requirements now features prominently in bid evaluations, pushing vendors to maintain rapid firmware and ink-set updates.

Open-architecture challengers position against lock-in by accepting third-party inks and integrating with off-the-shelf RIP software. Start-ups such as Nano Dimension and Optomec capitalize on functional electronics printing where incumbent knowledge is limited. Meanwhile, established vendors invest heavily in cloud diagnostics and machine learning to predict component wear, attempting to tie customers into multi-year subscription bundles that combine hardware, consumables, and analytics.

Inkjet Printing Industry Leaders

HP Inc.

Canon Inc.

Seiko Epson Corp.

Brother Industries Ltd.

Ricoh Company Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Canon Inc. introduced varioPRESS iV7 and varioPRINT iX1700 digital presses featuring inline spectrophotometers that maintain ISO 12647 color conformance.

- January 2026: HP Inc. expanded PrintOS to include remote substrate profiling, cutting multi-site campaign turnaround by 30%.

- November 2025: Valgroup installed the first HP Indigo 200K in South America, enabling promotional label runs without central import.

- October 2025: Mimaki Engineering launched TX330-1800 and Tiger600-1800TS textile printers aimed at personalized home décor.

Global Inkjet Printing Market Report Scope

Inkjet printing is the most widely used form of digital printing for small, inexpensive consumer models and expensive professional machines. The market is defined by the revenue accrued from selling inkjet printing solutions worldwide.

The Inkjet Printing Market Report is Segmented by Printing Technology (Drop-On-Demand Inkjet, Continuous Inkjet, and Other Printing Technologies), Ink Type (Aqueous, Solvent-Based, UV-Curable, Latex, Dye-Sublimation, and Other Ink Types), Component (Printers, Ink Cartridges and Bulk Inks, Print-Heads, and Software and Services), Application (Books and Publishing, Commercial Print, Advertising, Transactional, Labels, Packaging, Textile Printing, Electronics and PCB Printing, and Other Applications), Substrate Material (Paper and Paperboard, Plastic Films and Foils, Textile, Metal, Glass and Ceramics, and Other Substrate Materials), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Drop-On-Demand Inkjet |

| Continuous Inkjet |

| Other Printing Technologies |

| Aqueous |

| Solvent-Based |

| UV-Curable |

| Latex |

| Dye-Sublimation |

| Other Ink Types |

| Printers |

| Ink Cartridges and Bulk Inks |

| Print-Heads |

| Software and Services |

| Books and Publishing |

| Commercial Print |

| Advertising |

| Transactional |

| Labels |

| Packaging |

| Textile Printing |

| Electronics and PCB Printing |

| Other Applications |

| Paper and Paperboard |

| Plastic Films and Foils |

| Textile |

| Metal |

| Glass and Ceramics |

| Other Substrate Materials |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Printing Technology | Drop-On-Demand Inkjet | ||

| Continuous Inkjet | |||

| Other Printing Technologies | |||

| By Ink Type | Aqueous | ||

| Solvent-Based | |||

| UV-Curable | |||

| Latex | |||

| Dye-Sublimation | |||

| Other Ink Types | |||

| By Component | Printers | ||

| Ink Cartridges and Bulk Inks | |||

| Print-Heads | |||

| Software and Services | |||

| By Application | Books and Publishing | ||

| Commercial Print | |||

| Advertising | |||

| Transactional | |||

| Labels | |||

| Packaging | |||

| Textile Printing | |||

| Electronics and PCB Printing | |||

| Other Applications | |||

| By Substrate Material | Paper and Paperboard | ||

| Plastic Films and Foils | |||

| Textile | |||

| Metal | |||

| Glass and Ceramics | |||

| Other Substrate Materials | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Spain | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large will global spending on inkjet printing reach by 2031?

It is projected to attain USD 178.67 billion by 2031, reflecting a 7.24% CAGR over 2026-2031.

Which region offers the quickest growth opportunity?

South America shows the fastest regional pace with a forecast 9.09% CAGR, driven by localized label and packaging demand.

What segment leads future expansion in applications?

Textile printing is set to grow at 9.12% CAGR as fashion brands migrate to on-demand production models.

Why are single-pass presses gaining traction?

They deliver offset-level throughput while retaining variable-data capability, reducing makeready waste by up to 70%.

What is driving the shift toward latex inks?

Tightening VOC regulations and the need for scratch-resistant outdoor graphics push converters toward water-based latex chemistries.

How are vendors securing recurring revenue?

Cloud platforms such as HP PrintOS and Roland DG Connect package predictive maintenance and consumable replenishment into subscription models.

Page last updated on: