DTG Printers Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

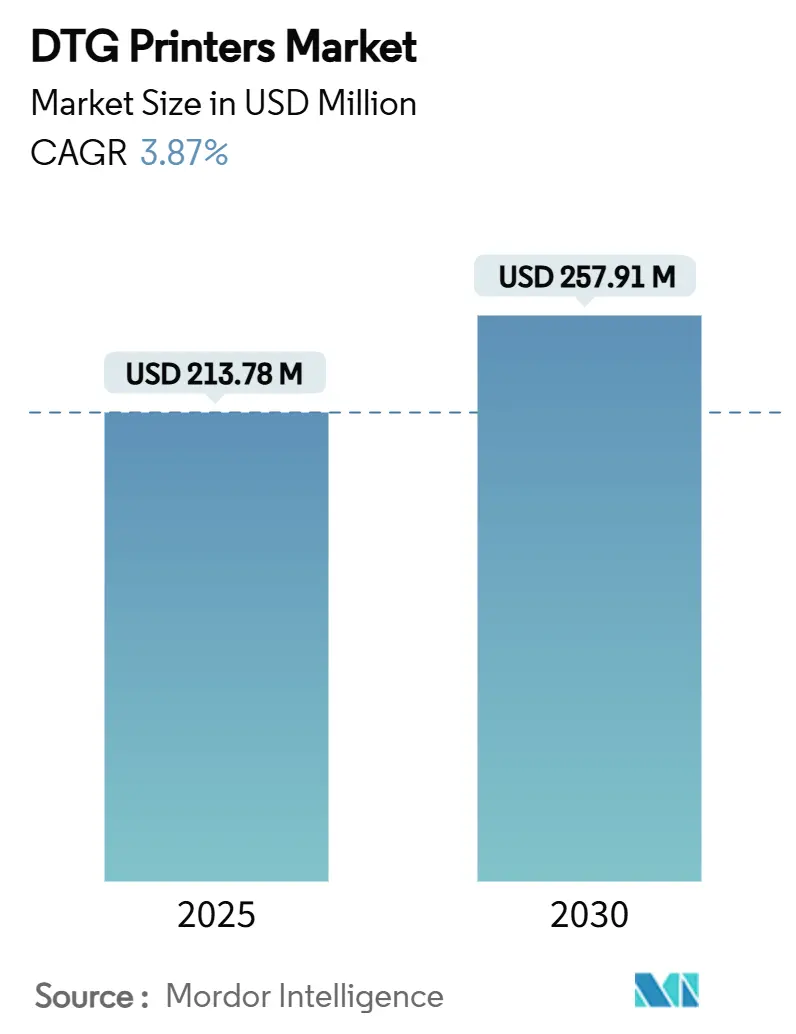

| Market Size (2025) | USD 213.78 Million |

| Market Size (2030) | USD 257.91 Million |

| Growth Rate (2025 - 2030) | 3.87% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

DTG Printers Market Analysis by Mordor Intelligence

The Direct to Garment (DTG) Printers market stands at USD 213.78 million in 2025 and is on course to reach USD 257.91 million by 2030, expanding at a 3.87% CAGR. This steady advance signals a transition from niche adoption toward widespread use as brands demand agile manufacturing that aligns production volumes with real-time online orders. Higher nozzle-density printheads are pushing cost per print down, reinforcing the economic rationale for on-demand models. T-shirt personalization continues to anchor demand, yet downstream opportunities are broadening into sportswear and performance fabrics, where premium inks lift average selling prices. Sustainability mandates, especially in North America and Europe, are accelerating the pivot from solvent to water-based pigment chemistry and thereby securing DTG’s role as an eco-favorable alternative to legacy screen printing. Competitive intensity is rising as large vendors pursue subscription pricing, while regional suppliers seek scale through hybrid DTG-screen systems that mix digital precision with analog cost efficiency, reshaping the DTG Printers market landscape.

Key Report Takeaways

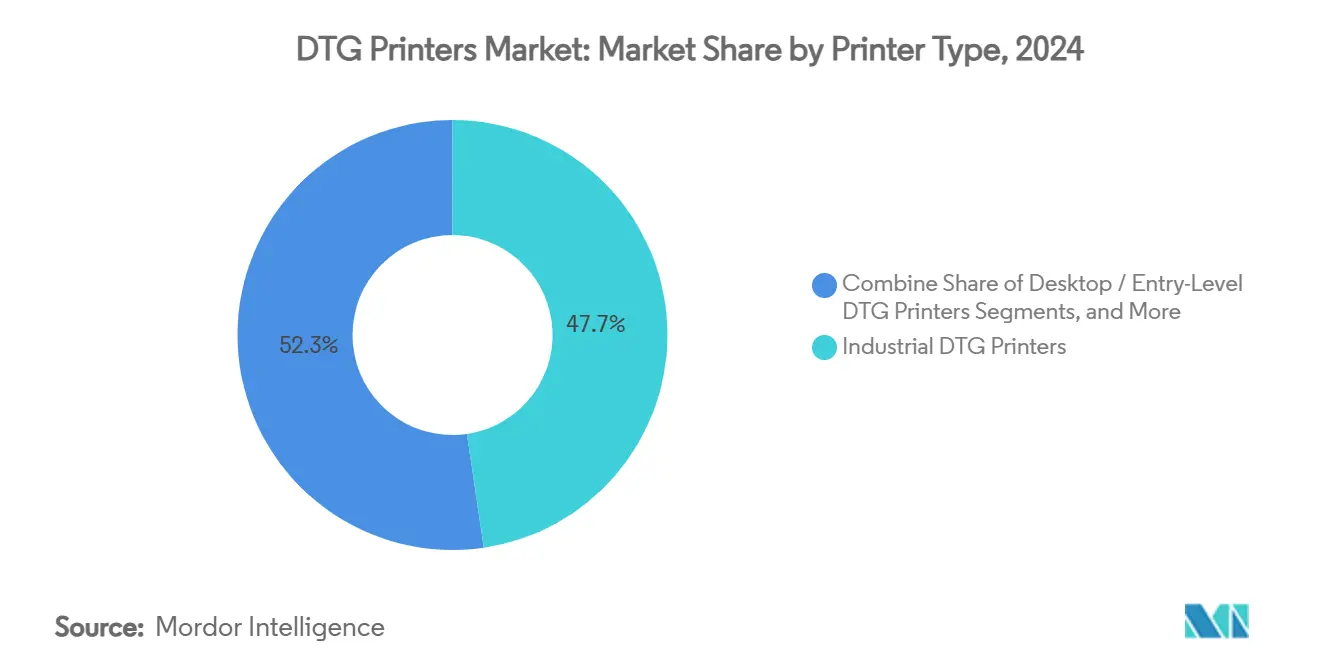

- By printer type, industrial DTG systems held 47.67% of the DTG printers market share in 2024.

- By ink formulation, the specialty fluorescent and metallic inks segment is projected to grow at a 5.04% CAGR between 2025 to 2030.

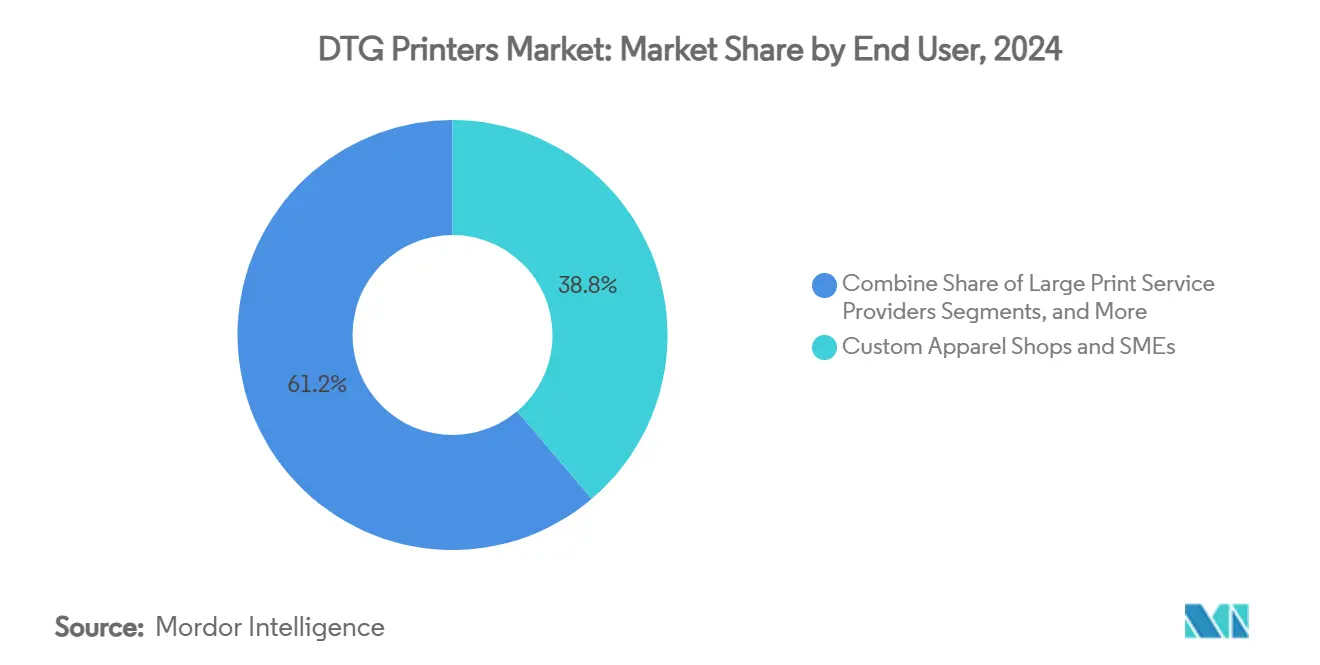

- By end user, custom apparel shops and SMEs accounted for 38.79% of the DTG Printers market size in 2024.

- By application, the sportswear and activewear segment is projected to grow at a 4.82% CAGR between 2025 and 2030.

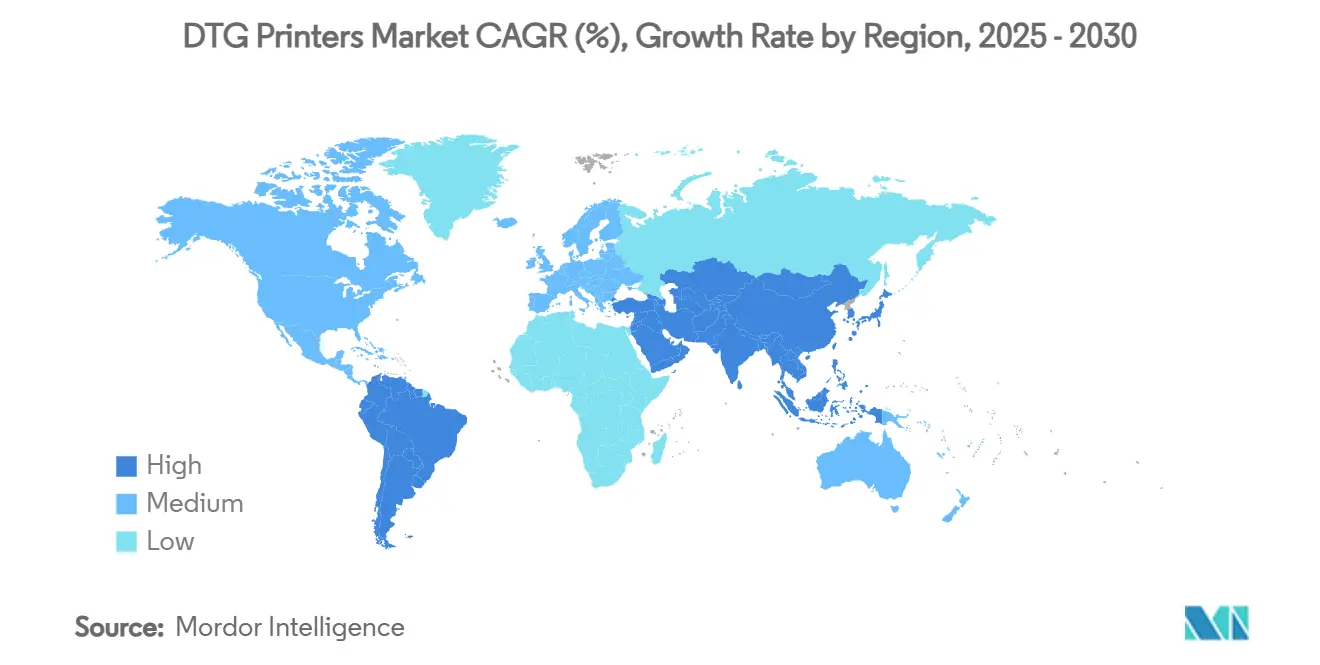

- By geography, Asia-Pacific held 36.23% of the DTG printers market share in 2024.

Global DTG Printers Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift toward mass-customized apparel in fast fashion | +0.8% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Global sustainability mandates & waterless digital printing | +1.2% | EU core, expanding to North America & APAC | Long term (≥ 4 years) |

| Advancements in high-speed single-pass inkjet systems | +0.9% | Global, led by Japan & Germany technology centers | Short term (≤ 2 years) |

| E-commerce & print-on-demand fulfillment models | +1.1% | North America & EU, expanding to APAC urban centers | Medium term (2-4 years) |

| AI-driven automation and micro-factory adoption | +0.6% | Developed markets, gradual APAC adoption | Long term (≥ 4 years) |

| Nearshoring and regionalized production (e.g., EU CBAM) | +0.5% | North America & EU, with Mexico & Eastern Europe gains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rise of Customized Apparel E-commerce

Digital marketplaces now deliver automated personalization from click to ship, and Amazon’s fulfillment algorithms allocate DTG capacity to match each micro-order[1]About Amazon, “Making On-Demand Merchandise Faster,” aboutamazon.com. Retail giants such as Walmart achieve same-week replenishment through Kornit’s Apollo platform, cutting dead inventory and cementing the DTG Printers market as critical infrastructure. Viral social designs propagate across TikTok and Instagram, stimulating fresh print runs without minimum quantities. The cycle closes when real-time demand data feeds production software, eliminating guess-driven overstock. As consumer expectations for uniqueness harden, mass customization migrates from novelty to baseline, deepening structural demand for DTG equipment.

Declining Cost per Print Through Higher Nozzle Density

Piezo printhead engineering raises nozzle counts, boosting single-pass coverage and shrinking ink waste, a priority Epson is addressing via a USD 34 million capacity expansion in Japan[2]Epson, “Epson to Quadruple PrecisionCore Production,” epson.com. Increased line speed permits industrial operators to price closer to screen printing for medium-sized runs, eroding a key cost barrier within theDTG Printers market. Brother’s mid-term sales plan anticipates a 40% industrial revenue mix, indicating confidence that print economics are reaching parity. As learned curves in semiconductor-style fabrication push yield gains, unit prices fall further, promoting faster refresh cycles and widening accessibility for small shops.

Stricter Eco-compliance Favoring Water-based Pigment Inks

Regulators now require up to 60% fewer hazardous air pollutants in textile print facilities, an EPA directive that directly aligns with DTG’s water-based chemistry[3]U.S. Environmental Protection Agency, “National Emission Standards for Textile Printing,” epa.gov. Brands publicize carbon-footprint cuts to win eco-minded shoppers, propelling Kornit’s NeoPigment systems into brand and contract facilities across Europe. DuPont, having lowered greenhouse gases by 58% since 2019, channels R&D into dispersions that achieve bold colors while meeting zero-VOC targets. The combined regulatory and reputational pull shifts capital planning toward DTG in the DTG Printers market, marginalizing solvent-ink screen lines.

On-demand Micro-factory Integration with ERP

Closed-loop ERP workflows convert art files directly into production schedules, orchestrating pre-treatment, print, cure, and packing with minimal human touch. The UK’s Future Fashion Factory shows that digital process alignment can compress lead times from 4-8 months to near-design-week cycles. American labels embed DTG clusters inside distribution centers to bypass seaport delays, while European brands adopt near-shore nodes for sustainability auditing. These networks depend on modular printers networked to cloud dashboards, cementing the DTG Printers market as the core engine of agile supply chains.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital investment for industrial digital systems | -0.7% | Global, particularly impacting SMEs in developing markets | Short term (≤ 2 years) |

| Colour fastness and hand-feel limitations of pigment inks | -0.4% | Quality-sensitive markets in EU & North America | Medium term (2-4 years) |

| VOC/PFAS ink reformulation costs and regulatory hurdles | -0.6% | EU core, expanding to North America & APAC | Long term (≥ 4 years) |

| Semiconductor supply volatility affecting inkjet components | -0.3% | Global, with highest impact in APAC manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Equipment Investment

Industrial DTG lines cost USD 100,000–500,000 plus service contracts, pinching the cash-flow budgets of the very SMEs that generate 38.79% of 2024 demand. Lenders hesitate because secondary markets for used DTG units remain thin, inflating asset-risk premiums. Kornit’s All-Inclusive Click model turns capital expense into per-print operating cost, but adoption is early-stage. Until financing norms stabilize, unit placements will cluster with well-capitalized service providers, moderating the DTG Printers market’s near-term acceleration.

Colour/Opacity Limitations on Dark Garments

Achieving solid white underbases on black fabrics forces multiple passes, halving throughput and hiking ink expense. Even advanced CMYK + White sets that occupy 43.42% share struggle with neon graphics requiring wide gamut saturation. Extra pretreatment steps raise chemical input costs and extend takt time. Research into novel binders continues, yet a commercial breakthrough remains elusive, tempering the DTG Printers market’s expansion into high-end fashion capsules where black dominates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Printer Type: Industrial Dominance with Hybrid Upswing

The DTG Printers market size allocated to industrial units stood at USD 101.9 million in 2024, reflecting a 47.67% grip on global revenue. Operators value these platforms for multi-shift durability, automated maintenance, and calibrated color stability, attributes essential for e-commerce SLA compliance. In practice, each industrial line can output 200–400 pieces per hour, letting print-service providers amortize high list prices over predictable monthly volumes.

Hybrid DTG-screen systems, though smaller today, are scaling at a 4.93% CAGR. They answer the “one roof” requirement: digital for 5-piece niche orders and screen heads for 5,000-piece promotional releases. The resulting equipment flexibility appeals to contract factories in Vietnam, Bangladesh, and Mexico that juggle global brand requirements. Dover’s Caldera software orchestrates color management across both digital and analog heads, showcasing synergy potential[4]Dover Corporation, “Caldera DTF Launch,” dovercorporation.com. As cost curves tighten, hybrids may claim an outsize slice of incremental installations, reshaping supply-chain topology inside the DTG Printers market.

By Ink Type: Specialty Formulations Capture Premium Margin

The DTG Printers market size tied to CMYK + White inks accounted for USD 92.8 million in 2024. Dark-garment demand, powered by streetwear and athleisure trends, forces white layers for opacity. Vendors now bundle degassed white cartridges with integrated recirculation loops to curb sedimentation and nozzle clogging, extending uptime.

Specialty fluorescent and metallic inks, occupying a niche USD 12.1 million slice, are on track for 5.04% annual growth. Aesthetic effects unlock retail mark-ups that offset higher pigment costs. Chemours’ titanium-dioxide enhancements strengthen shimmer permanence, while DuPont develops binder matrices that hold neon chroma under UV exposure. Custom sports jerseys, dancewear, and limited-edition brand drops are early adopters, foreshadowing wider diffusion across the DTG Printers market as color-rich fashion cycles accelerate.

By End User: Micro-factories Lead Structural Reordering

SME print shops, campus stores, and local merch counters generated 38.79% of 2024 consumption, embracing DTG to outflank volume-tied screen printers. Low setup time enables same-day delivery and broad design libraries, a selling point for community organizations and influencer merch operations.

Micro-factories nestled inside brand studios or regional fulfillment centers are expanding at 4.76% CAGR. Zara-style drop models hinge on weekly capsule collections, each requiring batches of 50-500 units. DTG answers that cadence without stranded inventory, aligning with corporate working-capital mandates. Government-backed textile parks in India and funding in Mexico’s near-shore corridors catalyze adoption by subsidizing infrastructure. As distribution gravitates toward regional make-to-order, micro-factories could rewrite volume allocations throughout the DTG Printers market.

By Application: Sportswear Sets the Pace for Technical Expansion

T-shirts, at 51.87% share, remain the entry point for most DTG operators because single-pass cotton prints deliver predictable margins. Merchandise for concerts, esports, and charity events still anchors machine utilization during off-peak seasons.

Sportswear and activewear, however, are growing 4.82% annually, signaling broader textile application reach. Moisture-wicking polyester blends require advanced pre-treatment chemistries, lifting ink set ASPs. Athletic brands co-create personalized kits linked to athlete data feeds, marrying function with individual identity. The DTG Printers market thus benefits from higher-value substrates and expands beyond cotton with each ink-chemistry breakthrough.

Geography Analysis

Asia-Pacific controlled 36.23% revenue in 2024 and is advancing at a 4.98% CAGR, thanks to favorable labor-to-capex ratios and upstream supply integration. China hosts most global contract garment factories, and domestic printer OEMs are entering export lanes with competitively priced mid-range units. Government subsidies for smart-factory retrofits in Vietnam and Thailand are pushing DTG adoption deeper into second-tier cities. India’s new textile parks link zero-liquid-discharge facilities and solar rooftops, positioning DTG as a marquee technology for sustainable export zones.

North America shows mature penetration but still imports 60% of blank garments, leaving reshoring advocates to champion local quick-response hubs. Brands leverage DTG to execute “made-near-consumer” slogans, with California and Texas emerging as cluster states. E-commerce volume peaks trigger temporary capacity shortages, demonstrating that domestic print speed can outweigh lower offshore unit costs under tight delivery promises.

Europe’s eco-compliance agendas dovetail with DTG’s water-based inks. Fashion houses in Italy and France adopt micro-factory nodes to satisfy “green” labeling schemes. Germany’s engineering firms contribute automation retrofits, while regional regulatory strictness accelerates solvent phase-outs. Conversely, South America and the Middle East remain nascent; yet rising disposable incomes in Brazil and the Gulf spur localized customization ventures. Grants that bolster SME equipment funding could accelerate Direct to Garment Printers market dispersion across these territories.

Competitive Landscape

Kornit Digital, Brother, Epson, and Ricoh collectively hold just under 40% of global shipment value, indicating moderate concentration with room for challenger incursions. Kornit’s strength stems from vertically integrated platforms that package hardware, workflow software, and consumables into subscription bundles, ensuring perpetual revenue per printed pixel. Brother uses dealer footprints from office equipment to cross-sell DTG mid-range models, a tactic that shortens sales cycles. Epson advances piezo RandD while lifting in-house printhead capacity by fourfold to safeguard supply.

Regional contenders in Turkey, China, and Spain target price-sensitive SMEs with stripped-down mechanics, trading advanced automation for lower purchase tickets. Hybrid DTG-screen technology forms the current battleground, as seen in Dover’s Caldera integration, which promises “one-driver” workflow consistency. Component shortages, especially for precision piezo heads, test vendor resilience and push alliances with upstream electronics suppliers.

Strategic moves in 2024 highlighted capital return and manufacturing scale-ups. Kornit adopted a USD 100 million buyback, signaling strong cash generation. Ricoh and Toshiba TEC aligned MFP operations to free resources for industrial inkjet RandD. Market participants now chase recurring click fees and software subscriptions rather than one-off hardware revenue, a shift that will likely intensify acquisition activity inside the DTG Printers market.

DTG Printers Industry Leaders

Brother Industries, Ltd.

Kornit Digital Ltd.

Seiko Epson Corporation

Ricoh Company, Ltd.

Aeoon Technologies GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Ricoh formed ETRIA JV with Toshiba TEC to streamline hardware production.

- November 2024: India approved INR 726 crore to develop Lonex Textile Park in Shamli, creating a DTG-ready cluster.

- October 2024: Kornit partnered with Hybrid Digital to deploy Apollo automated lines for big-box retail fulfillment.

- September 2024: Dover’s Caldera rolled out an all-platform Direct-to-Film suite, broadening digital textile accessibility for micro-enterprises.

- September 2024: Kornit Digital initiated a USD 100 million share repurchase program.

Global DTG Printers Market Report Scope

| Industrial DTG Printers |

| Desktop / Entry-Level DTG Printers |

| Hybrid DTG-Screen Printers |

| Mobile/Portable DTG Units |

| Standard CMYK Inks (for light garments) |

| CMYK + White Inks (for dark garments) |

| Specialty Fluorescent and Metallic Inks |

| Custom Apparel Shops and SMEs |

| Large Print Service Providers |

| In-house Corporate Branding Teams |

| Fashion-Brand Micro-Factories |

| T-Shirts |

| Sportswear and Activewear |

| Children's Wear |

| Uniforms and Workwear |

| Hoodies and Sweatshirts |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Printer Type | Industrial DTG Printers | ||

| Desktop / Entry-Level DTG Printers | |||

| Hybrid DTG-Screen Printers | |||

| Mobile/Portable DTG Units | |||

| By Ink Type | Standard CMYK Inks (for light garments) | ||

| CMYK + White Inks (for dark garments) | |||

| Specialty Fluorescent and Metallic Inks | |||

| By End User | Custom Apparel Shops and SMEs | ||

| Large Print Service Providers | |||

| In-house Corporate Branding Teams | |||

| Fashion-Brand Micro-Factories | |||

| By Application | T-Shirts | ||

| Sportswear and Activewear | |||

| Children's Wear | |||

| Uniforms and Workwear | |||

| Hoodies and Sweatshirts | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East and Africa | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the DTG Printers market?

The market is valued at USD 213.78 million in 2025 and is set to climb to USD 257.91 million by 2030.

Which printer type has the largest share?

Industrial DTG systems hold 47.67% of 2024 revenue because their throughput matches high-volume e-commerce needs.

Why are hybrid DTG-screen printers growing fastest?

At a 4.93% CAGR, hybrids let factories switch between small digital runs and large analog orders on one line, boosting cost flexibility.

How is sustainability influencing adoption?

Water-based pigment inks meet tightening EPA and EU rules, making DTG preferable to solvent screen lines for eco-conscious brands.

Which region leads market growth?

Asia-Pacific leads with 36.23% revenue and the highest 4.98% CAGR, backed by integrated supply chains and rising local demand.

What limits wider DTG penetration?

High capital costs USD 100,000–500,000 per industrial line and technical challenges in white-ink opacity on dark garments remain key barriers.

Page last updated on: