North America Commercial Printing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

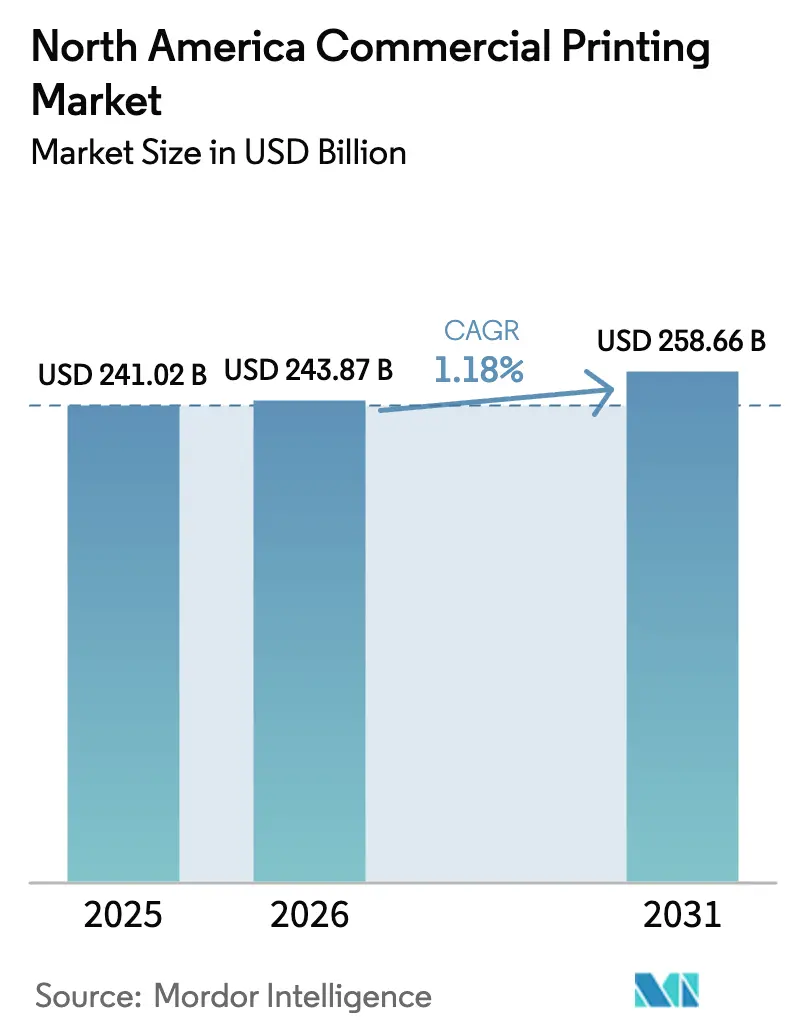

| Base Year Market Size (2025) | USD 241.02 Billion |

| Market Size (2026) | USD 243.87 Billion |

| Market Size (2031) | USD 258.66 Billion |

| Growth Rate (2026 - 2031) | 1.18% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Commercial Printing Market Analysis by Mordor Intelligence

The North America commercial printing market size is expected to grow from USD 241.02 billion in 2025 to USD 243.87 billion in 2026 and is forecast to reach USD 258.66 billion by 2031 at 1.18% CAGR over 2026-2031. This moderate growth reflects a mature landscape where technology upgrades, sustainability mandates, and service-mix realignment outweigh volume expansion as the principal value drivers. Packaging continues to drive revenue, while security printing accelerates through authentication mandates, and nearshoring shifts work toward flexible workflows that can execute short runs without compromising quality. Printers that deploy end-to-end automation, variable data capabilities, and omnichannel fulfillment capture share from firms locked into legacy offset footprints. Meanwhile, brand owners’ sustainability targets, labor shortages, and fluctuations in raw material costs collectively redefine competitive strategy in the North America commercial printing market.

Key Report Takeaways

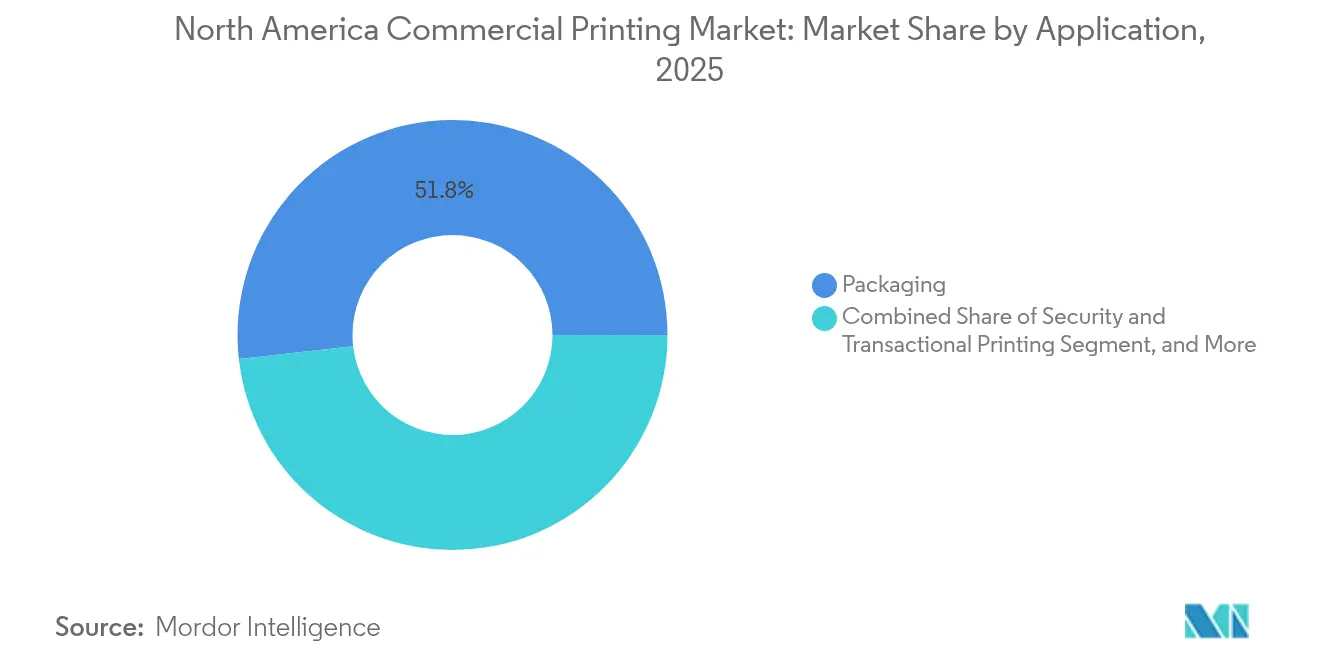

- By application, packaging led with 51.78% revenue share of the North America commercial printing market in 2025, while security and transactional printing is projected to grow at a 2.14% CAGR to 2031.

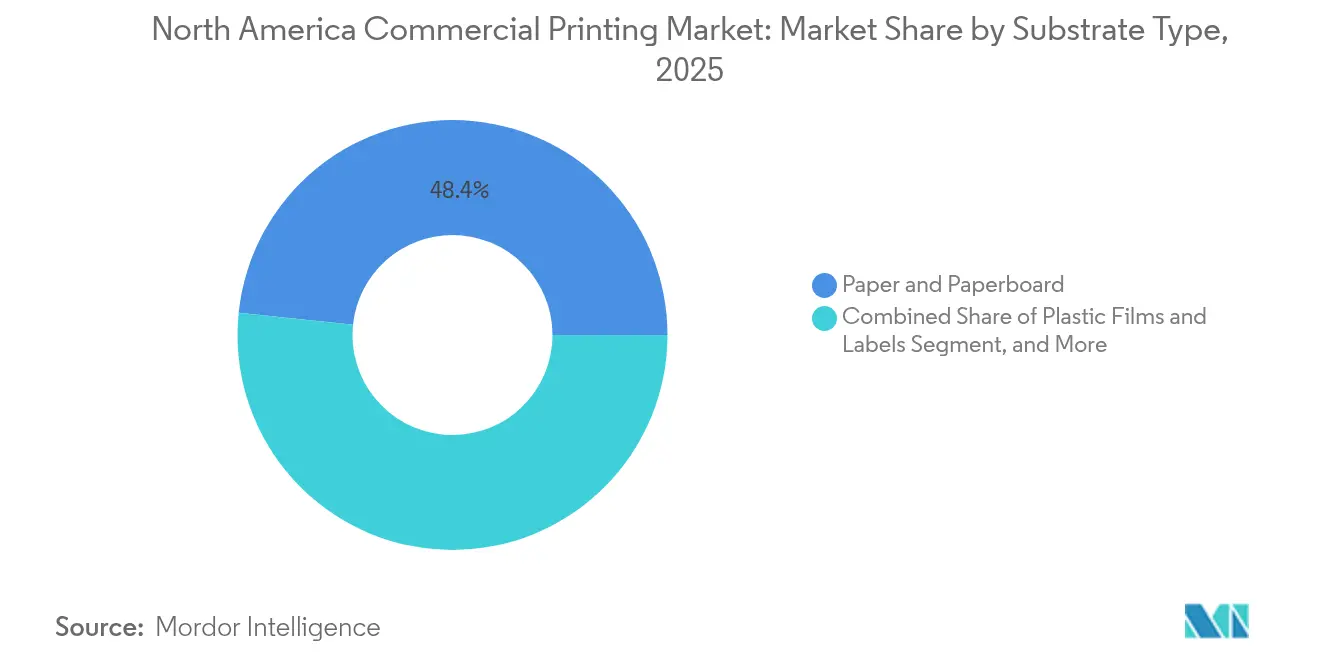

- By substrate, paper and paperboard accounted for 48.35% of the North America commercial printing market size in 2025, whereas plastic films and labels are set to expand at a 2.07% CAGR through 2031.

- By printing technology, offset lithography maintained 41.95% of the North America commercial printing market share in 2025, while digital inkjet is forecast to grow at 2.58% CAGR between 2026-2031.

- By end-user industry, food and beverage represented 28.35% share of the North America commercial printing market size in 2025, and healthcare is advancing at a 2.74% CAGR through 2031.

- By geography, the United States controlled 78.05% of the North America commercial printing market in 2025 and Mexico is expected to expand at 2.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Commercial Printing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for flexible and e-commerce packaging | +0.4% | North America with Mexico focus | Medium term (2-4 years) |

| Growing adoption of digital printing technologies | +0.3% | United States and Canada | Long term (≥ 4 years) |

| Expansion of variable data printing for mass personalisation | +0.2% | United States, Canada | Medium term (2-4 years) |

| Increasing short-run, on-demand print orders from SMEs | +0.2% | North America | Short term (≤ 2 years) |

| Sustainability regulations accelerating low-VOC ink uptake | +0.1% | California, New York, Rhode Island | Long term (≥ 4 years) |

| Growth of industrial inkjet for direct-to-shape printing | +0.1% | United States-Mexico corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Flexible and E-Commerce Packaging

E-commerce fulfillment has stimulated a sustained shift toward lightweight, durable, and brandable packs that travel safely through parcel networks. Amazon’s USD 2.0 billion annual print spend tilts heavily toward corrugated formats and digitally printed inserts that enable individualized unboxing moments while cutting excess materials. Implementation of higher de minimis thresholds under the USMCA reduces customs frictions, unlocking incremental cross-border shipments valued at USD 423 million and channeling more work to North American packaging converters. [1]U.S. International Trade Commission, “U.S.-Mexico-Canada Trade Agreement: Likely Impact on the U.S. Economy and on Specific Industry Sectors,” usitc.gov Converters leveraging variable-data workflows accommodate SKU proliferation and shorter lead times, positioning the North America commercial printing market to monetize packaging’s strategic role in brand storytelling and supply-chain efficiency.

Growing Adoption of Digital Printing Technologies

Installed fleets of HP Indigo, PageWide, and comparable high-speed inkjet presses achieve offset-like quality at sub-1,000-unit run lengths, reshaping cost curves for direct mail and short-run packaging. Workflow platforms such as HP Site Flow integrate order intake, imposition, and logistics, allowing unattended overnight production that mitigates labor shortages. As variable data becomes table stakes for omnichannel marketing, digital’s share of the North America commercial printing market expands steadily despite the sector’s overall modest CAGR.

Expansion of Variable Data Printing for Mass Personalisation

Brand owners seeking one-to-one engagement embed QR codes, versioned imagery, and geo-targeted offers within direct mail and packaging materials. Renewed interest in direct mail stems from rising digital ad costs and the loss of signal in third-party cookie tracking; response uplift offsets premium print prices when campaigns utilize precise data segmentation. Installations such as N2 Company’s PageWide presses demonstrate that high-volume personalization is technically and economically feasible, catalyzing adoption among publishers, healthcare firms, and CPG brands that view printed touchpoints as measurable components of integrated campaigns.

Increasing Short-Run, On-Demand Print Orders from SMEs

SMEs utilize print-on-demand to test product variants and seasonal packaging without tying up working capital in inventory. Typical lot sizes of 50-100 units flow through web-to-print portals that bypass traditional quoting cycles, triggering automated workflows all the way through kitting and shipment. Saal Digital, for example, processes 5,000 daily online orders via HP Indigo presses that swing between photo books and marketing collateral with minimal downtime. The consequent democratization of high-quality print fuels the long-tail revenue pool within the North America commercial printing market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in paper and petrochemical raw material prices | -0.3% | North America with Canada exposure | Short term (≤ 2 years) |

| Market disruption owing to shift toward digital media | -0.2% | United States urban centers | Long term (≥ 4 years) |

| Capital-intensive nature of high-speed press investments | -0.15% | United States and Canada | Medium term (2-4 years) |

| Shortage of skilled press operators and pre-press technicians | -0.1% | North America manufacturing corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Paper and Petrochemical Raw Material Prices

Paper pricing fluctuates with shifts in mill capacity and energy costs, while ink costs track crude oil benchmarks, compressing printer margins during periods of commodity price increases. Taylor Corporation notes that the tightness of coated and uncoated inventory in 2024 forced printers to increase working capital and diversify suppliers to ensure allotments. [2]Taylor Corporation, “Commercial Print Market Trends,” taylor.comPostal rate hikes expected in 2025 add further pressure on direct mail economics, compelling printers to enhance operational efficiency to absorb cost pass-through resistance from budget-conscious clients.

Market Disruption Owing to Shift Toward Digital Media

Newspaper, magazine, and catalog volumes continue their multi-year decline as advertisers shift their spending to measurable online formats. Printing Impressions estimates that as many as 4,000 small shops face a consolidation risk amid shrinking job-shop work and underutilized equipment. Survivors evolve into marketing service providers or pivot into packaging, labels, and security applications where print offers irreplaceable physical utility. The North America commercial printing market thus redistributes capacity toward segments resilient to digital substitution.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Substrate Type: Plastic Films Gain Traction

Plastic films and labels recorded the fastest expansion at 2.07% CAGR through 2031, reflecting brand preference for flexible formats that deliver barrier protection and shelf impact. Shrink-sleeve demand in Mexico underscores the substrate’s utility for 360-degree messaging on beverages and household chemicals. Although paper and paperboard still held 48.35% of North America commercial printing market size in 2025, digital press compatibility and superior ink adhesion increasingly tilt high-value jobs toward plastic films that accept variable data and shorter runs without sacrificing quality.

Paper’s entrenched base in publishing and direct mail ensures volume stability, yet sustainability goals steer projects toward lightweight grades and certified fiber. Specialty synthetics support outdoor signage and harsh-environment labels, creating niche opportunities for converters equipped with UV-curable inkjet lines. Collectively, substrate diversification enables printers to hedge against commodity swings and capture margin in high-performance applications that transcend traditional paper-centric workflows across the North America commercial printing market.

By Printing Technology: Digital Inkjet Momentum Builds

Offset lithography retained 41.95% North America commercial printing market share in 2025 because its economics remain compelling for uniform, high-volume runs. Nonetheless, digital inkjet’s 2.58% forecast CAGR signals a structural pivot as variable data, shorter runs, and labor scarcity tilt ROI calculations in its favor. High-speed web inkjet presses now rival offset color gamut while eliminating plate costs and slashing makeready waste.

Flexography keeps a firm grip on long-run food packaging with FDA-compliant ink sets, whereas gravure persists in ultra-long jobs where cylinder longevity offsets tooling expense. Hybrid platforms blend inkjet imprinting with flexo or offset bases, allowing inline personalization and cost optimization on a single pass. Printers employing such mixed-platform strategies gain agility to serve advertising, packaging, and label contracts under one roof, reinforcing competitiveness in the North America commercial printing market.

By Application: Security Printing Accelerates

Packaging dominated the market with a 51.78% revenue share in 2025, as e-commerce, CPG, and private-label products increased the number of packaging SKUs. Simultaneously, security and transactional printing outpaced all other segments, growing at 2.14% CAGR, driven by anti-counterfeiting features, track-and-trace mandates, and financial services compliance workflows. Pharmaceutical serialization, now hard-coded in FDA regulations, drives demand for micro-text, variable codes, and tamper-evident seals that require specialized equipment and secure data management.

Advertising print, once beleaguered, regains relevance within omnichannel campaigns that leverage print’s sensory value alongside digital retargeting. Direct mail’s measurable lift in response rates supports its continued role, even as overall ad budgets shift toward digital. Publishers mitigate declining offset runs by offering print-on-demand books that align production with sell-through data, ensuring sustainability and margin retention within the North America commercial printing market.

By End-User Industry: Healthcare Rises

Food and beverage buyers accounted for 28.35% of 2025 revenue, thanks to relentless package redesigns, nutritional labeling changes, and sustainability pledges. However, the pharmaceutical and broader healthcare cluster is the fastest-growing consumer group, with a 2.74% CAGR through 2031, driven by the expansion of biologics, cold-chain labeling, and patient-specific literature packs. Serialization, barcoding, and tamper evidence are now baseline specifications, elevating the technical barrier to entry and supporting premium pricing for compliant suppliers.

Retail and e-commerce categories funnel demand toward corrugated inserts and return-ready packaging that meet brand experience mandates while minimizing waste. Education and media purchasers sustain textbook print through hybrid learning models, albeit with tempered volume, whereas the automotive and aerospace sectors generate durable labeling and technical documentation jobs that are impervious to digital substitution, thereby enriching the application mix across the North America commercial printing market.

Geography Analysis

The United States captured 78.05% share of the North America commercial printing market in 2025, reflecting its entrenched infrastructure, dense buyer concentration, and early adoption of digital workflows. California anchors low-VOC regulatory leadership, forcing printers to retrofit their presses with emission controls, a cost hurdle that favors scale players capable of incurring capital expenditures. Financial hubs such as New York and Chicago concentrate high-margin color work for finance, entertainment, and luxury retail clients, ensuring domestic demand remains robust despite the sector’s low overall CAGR.

Canada offers a complementary niche, excelling in security documents, cross-border logistics support, and bilingual packaging. USMCA provisions that disallow forced data localization streamline cloud-based workflow integration, allowing Canadian sites to execute just-in-time jobs for U.S. distribution without costly duplication of IT infrastructure. Stable operating conditions and proximity to the U.S. Eastern Seaboard make Canadian plants ideal overflow and specialty hubs within the North America commercial printing market.

Mexico stands out with a 2.55% forecast CAGR through 2031 as nearshoring relocates automotive, electronics, and apparel production from Asia to Mexican industrial corridors. Label converters are investing in automation, sustainability certifications, and RFID integration to meet U.S. brand compliance expectations. As Mexican facilities mature, they increasingly compete on quality rather than just cost, reshaping sourcing strategies for multinational print buyers seeking resilience and speed-to-market in the North America commercial printing market.

Competitive Landscape

The competitive field remains moderately fragmented, but rising capital intensity and labor shortfalls accelerate consolidation. The top 25 corporate print buyers now account for 49% of demand among the largest 100 print purchasers, concentrating negotiation leverage and prompting suppliers to expand their service portfolios.[3]Printing Impressions, “Top 100 Print Buyers for 2025,” printingimpressions.com RR Donnelley’s USD 50 million modernization in Georgia underscores the race to blend offset capacity with digital assets capable of variable data, while PRINTING United Alliance surveys show that mid-tier firms are prioritizing automated finishing to reduce labor exposure.

White-space opportunities cluster around pharmaceutical serialization, sustainable packaging, and direct-to-shape inkjet for consumer products. Hybrid manufacturing models that integrate cloud-based ordering, AI-driven scheduling, and robotics-assisted finishing help mitigate skilled labor gaps. Firms that master this Industry 5.0 paradigm secure higher wallet share within the North America commercial printing market, whereas smaller shops lacking upgrade capital become acquisition targets or exit altogether.

North America Commercial Printing Industry Leaders

C-P Flexible Packaging Inc.

American Packaging Corporation

Resource Label Group LLC

Amcor plc

Graphic Packaging International LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: PRINTING United Alliance published its 2025 Top 100 Print Buyers forecast identifying corporate purchasers with annual spend above USD 20 billion.

- October 2024: HP released a trend report projecting digital press sales to overtake analog units by 2026.

- August 2024: Printing Impressions ranked PepsiCo, Disney, and Amazon as the top three corporate print buyers with USD 2.2 billion, USD 2.1 billion, and USD 2.0 billion spends respectively.

- June 2024: The FDA strengthened control procedures for pharmaceutical product labeling under 21 CFR 211.125, increasing demand for compliant print workflows.

North America Commercial Printing Market Report Scope

Commercial printing provides various services necessary to prepare printed material, often involving a printing press. The commercial printing market is not limited to advertising and branding. It also includes publication printing, graphics printing, labels, and packaging. In addition to this, publication printing involves producing books, magazines, newspapers, and other printed materials. Furthermore, graphic printing focuses on items like catalogs, advertising materials, security prints, etc. The market study comprises various printing types, such as offset lithography, inkjet, flexographic, and other types, which are used under applications in packaging, publishing, and advertising across regions.

The North American commercial printing market is segmented by technology (offset lithography, inkjet, flexographic, screen, gravure, others (electrophotography and letterpress)), by application (direct mail, books and stationery, business forms and cards, tickets (lottery, others), advertising (printed signage, POP/POS display, etc.), transactional print, security, labels, packaging (paper and other packaging), other applications), by country (United States, Canada). The report offers market forecasts and size in value (USD) for all the above segments.

| Paper and Paperboard |

| Plastic Films and Labels |

| Metal/Foil |

| Other Substrate Types |

| Offset Lithography |

| Flexography |

| Screen |

| Inkjet |

| Gravure |

| Other Printing Technologies |

| Packaging |

| Publishing |

| Advertising and Promotional |

| Security and Transactional |

| Other Applications |

| Food and Beverage |

| Pharmaceuticals and Healthcare |

| Retail and E-Commerce |

| Education and Media |

| Banking, Financial Services and Insurance (BFSI) |

| Other End-User Industries |

| United States |

| Canada |

| Mexico |

| By Substrate Type | Paper and Paperboard |

| Plastic Films and Labels | |

| Metal/Foil | |

| Other Substrate Types | |

| By Printing Technology | Offset Lithography |

| Flexography | |

| Screen | |

| Inkjet | |

| Gravure | |

| Other Printing Technologies | |

| By Application | Packaging |

| Publishing | |

| Advertising and Promotional | |

| Security and Transactional | |

| Other Applications | |

| By End-User Industry | Food and Beverage |

| Pharmaceuticals and Healthcare | |

| Retail and E-Commerce | |

| Education and Media | |

| Banking, Financial Services and Insurance (BFSI) | |

| Other End-User Industries | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the current value of the North America commercial printing market?

The market totaled USD 243.87 billion in 2026 and is projected to reach USD 258.66 billion by 2031.

Which application area generates the most revenue?

Packaging leads with 51.78% of total 2025 revenue, driven by e-commerce and flexible pack formats.

Which country is growing fastest for commercial printing in North America?

Mexico is rising at a 2.55% CAGR through 2031 due to nearshoring and cross-border e-commerce demand.

How are digital presses affecting the sector?

Digital inkjet technology is forecast to climb at 2.58% CAGR as variable data, short runs, and automation outpace offset for many jobs.

What is the biggest cost headwind for printers?

Volatile paper and petrochemical prices reduce margins, forcing tighter inventory management and supplier diversification.

Page last updated on: