Printed Textiles Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

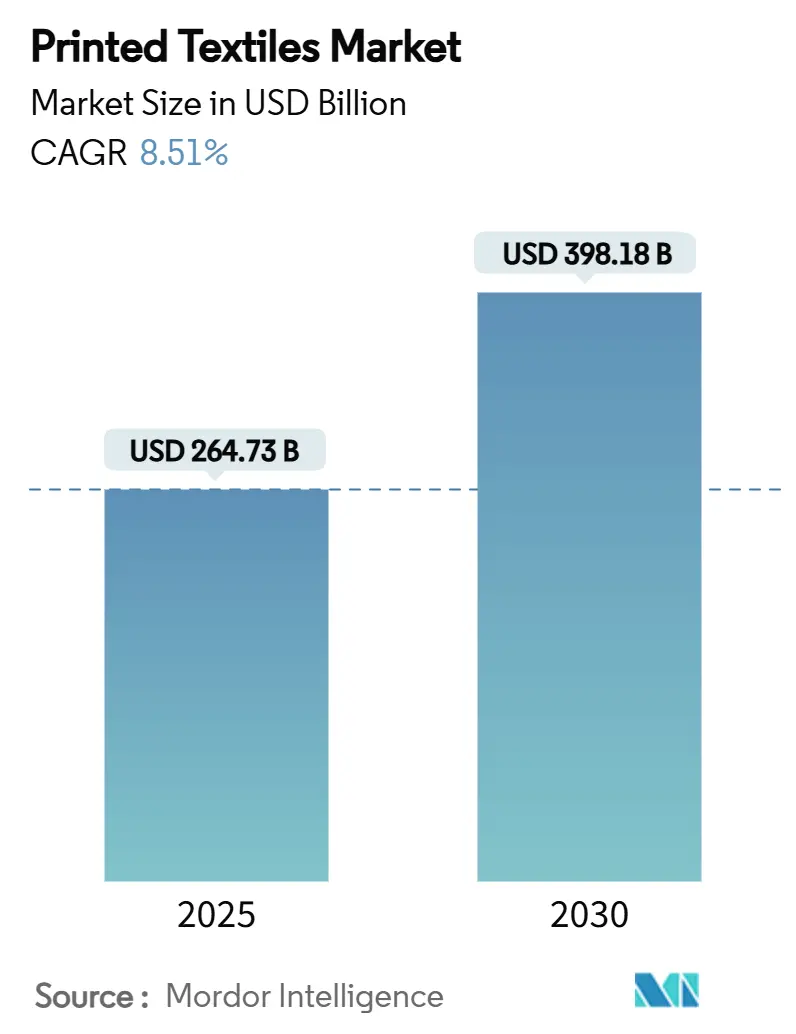

| Market Size (2025) | USD 264.73 Billion |

| Market Size (2030) | USD 398.18 Billion |

| Growth Rate (2025 - 2030) | 8.51% CAGR |

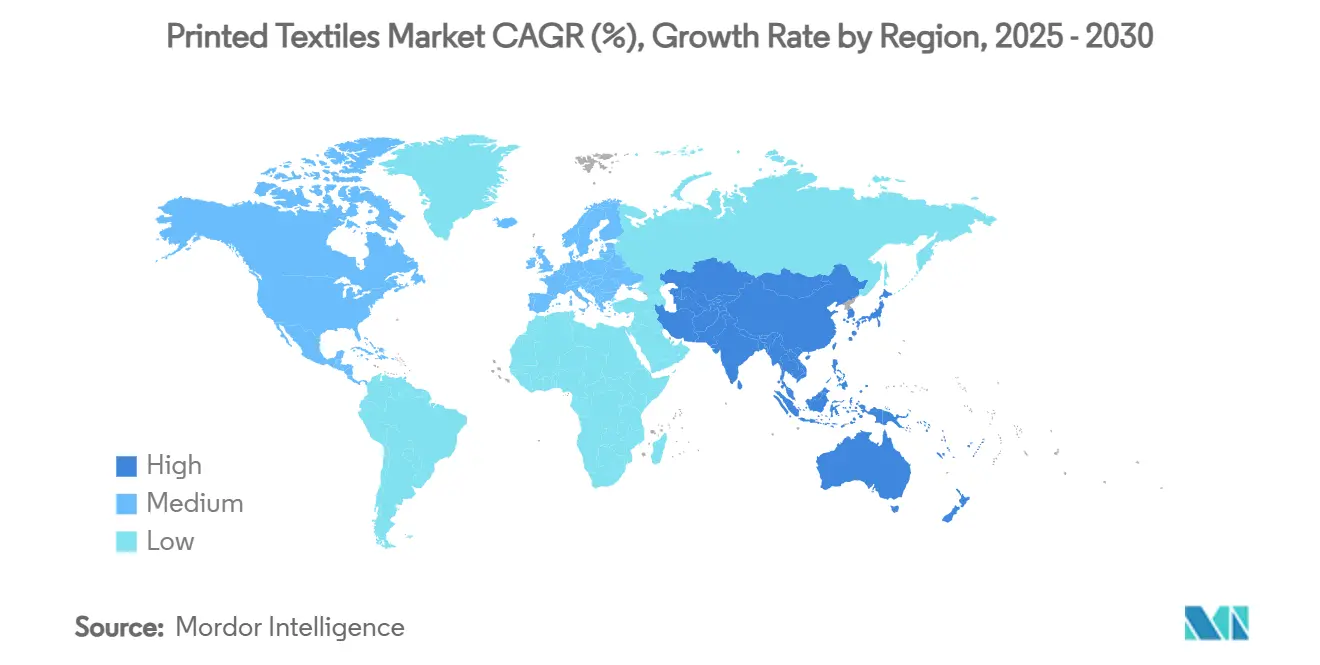

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

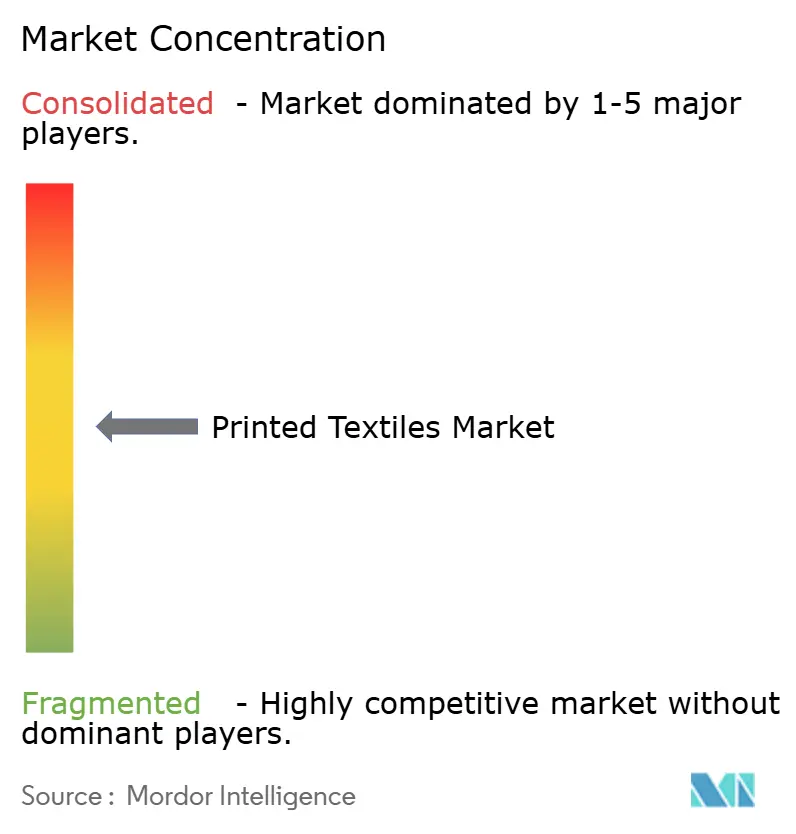

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Printed Textiles Market Analysis by Mordor Intelligence

The printed textiles market size is valued at USD 264.73 billion in 2025 and is forecast to reach USD 398.18 billion by 2030, registering an 8.51% CAGR during the period. Continuous migration from analog to digital platforms, combined with tightening sustainability regulations that favor water-less processes, is the central growth catalyst. New direct-to-fabric and direct-to-garment systems allow on-demand runs with up to 80% lower water use than conventional screen methods. Digital platforms have already saved more than 40 billion liters of water worldwide. Regional competitiveness is evolving: Asia-Pacific continues to anchor global production capacity, yet Middle East and Africa benefits from fresh public incentives that accelerate digitization. Technology advances in single-pass pigment heads, closed-loop workflow software, and modular hybrid lines are lifting productivity curves while shrinking per-print energy intensity.

Key Report Takeaways

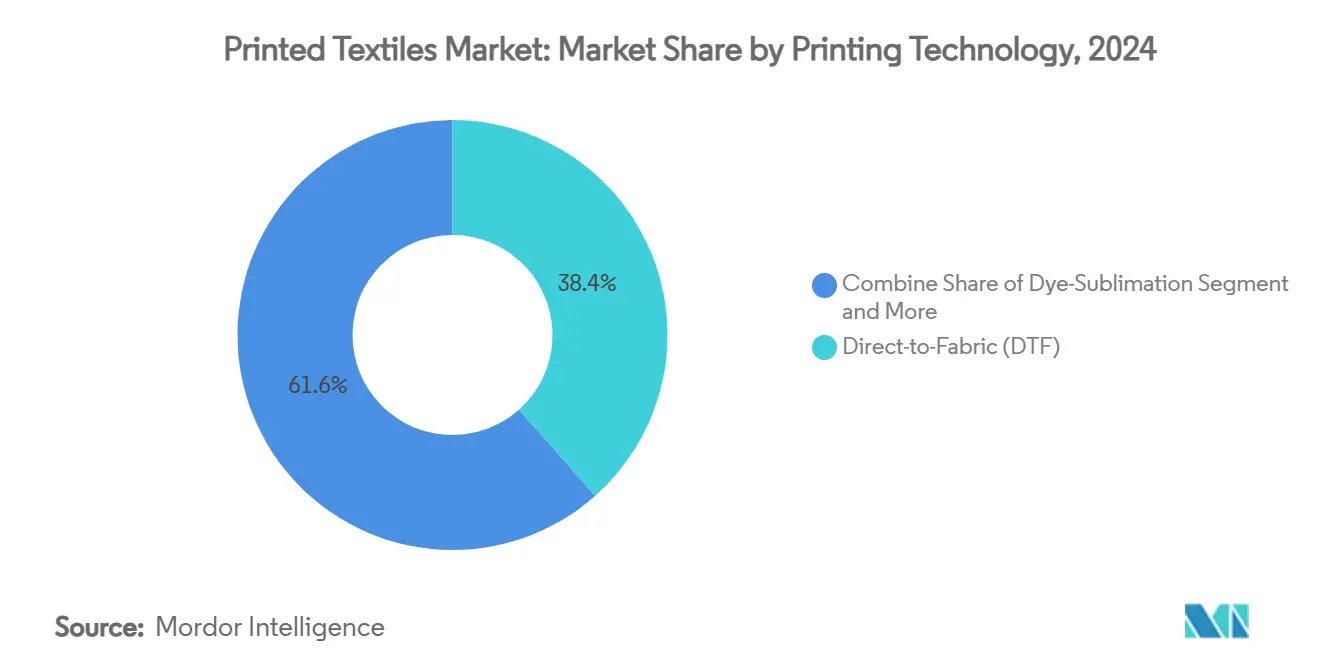

- By printing technology, Direct-to-Fabric captured 38.44% of printed textiles market share in 2024, while pigment single-pass systems are advancing at an 11.83% CAGR to 2030 .

- By ink type, disperse direct inks accounted for 42.85% of the printed textiles market size in 2024; sublimation inks are forecast to post a 10.74% CAGR during the outlook period.

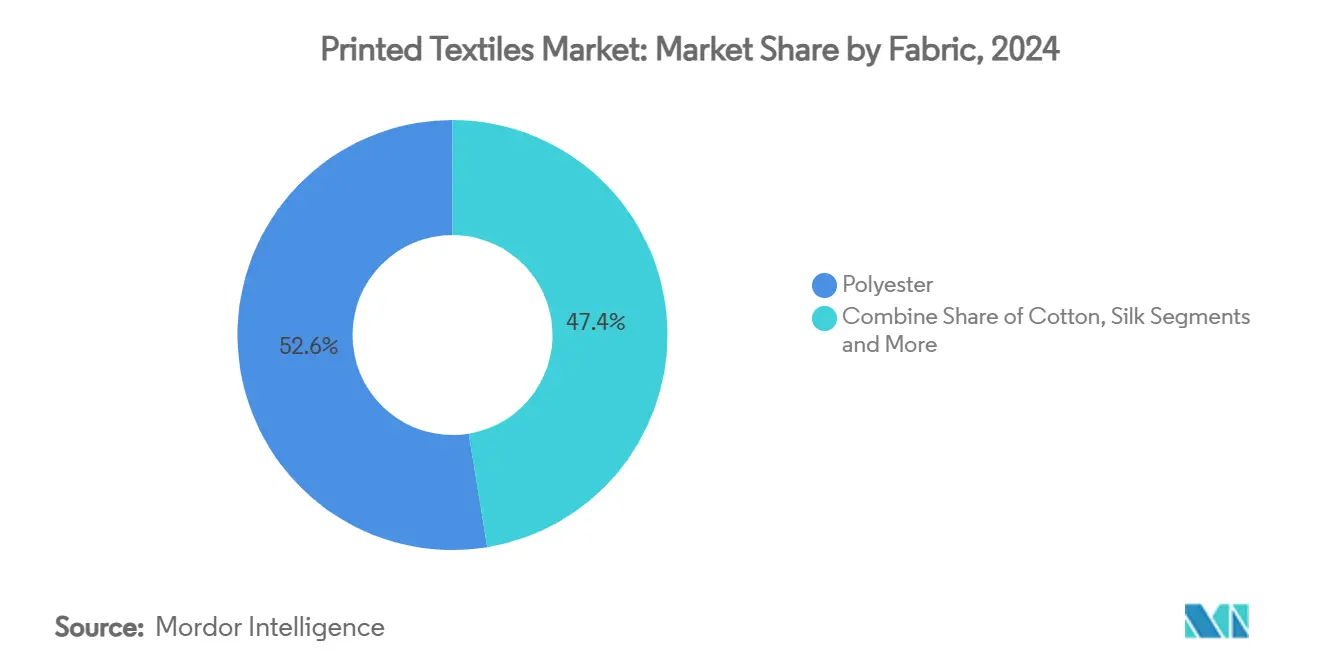

- By substrate, polyester commanded 52.59% of printed textiles market size in 2024 and is set to grow at a 12.11% CAGR through 2030.

- By application, technical textiles represented 39.59% of 2024 demand, whereas fashion and apparel is projected to rise at an 11.45% CAGR to 2030.

- By region, Asia-Pacific led with a 38.67% revenue share in 2024, whereas Middle East and Africa is projected to expand at a 10.98% CAGR through 2030.

Global Printed Textiles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for customised and fast-fashion apparel | +2.1% | Global, with concentration in North America and Europe | Short term (≤ 2 years) |

| Advances in high-speed digital printing platforms | +1.8% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Sustainability regulations pushing water-less printing | +1.5% | Europe and North America, expanding to APAC | Long term (≥ 4 years) |

| Explosive growth of e-commerce on-demand models | +1.3% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Micro-factory near-shoring for hyper-local production | +0.9% | North America and Europe | Medium term (2-4 years) |

| AI-generated designs driving short-run orders | +0.7% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Customised and Fast-Fashion Apparel

Short fashion cycles and direct-to-consumer channels have shrunk order quantities, making sub-100-unit runs commercially viable. Brands re-engineer supply chains around near-real-time replenishment that only digital lines can deliver. Digital printing eliminates minimum order constraints, enabling variable-data graphics on every garment without press make-ready downtime. Major integrators, including Kornit Digital, report rapid take-up of multi-fabric Apollo platforms by hybrid factories targeting just-in-time drops. Personalisation moves beyond fashion into corporate wear and promotional merchandise where on-demand workflows remove inventory risk and enhance campaign agility.

Advances in High-Speed Digital Printing Platforms

Emergent single-pass and multi-row head arrays pass the 1,500 m² per hour threshold while sustaining photographic resolution. Epson’s PrecisionCore Micro-TFP heads illustrate output of 1,590 ft² per hour on 64-inch units. [1]Electronics For Imaging, “Mapping the Future of Textile Printing,” efi.com Source: FESPA, “Sustainability Is the Paradigm of Digital Textile Printing,” fespa.com Integrated AI modules predict nozzle outages and auto-correct colour drift, lifting uptime metrics. Hybrid presses now switch from analog to digital lanes inside the same frame, matching per-order economics without re-rigging. Extended-life heads lengthen overhaul cycles and lower total cost of ownership, unlocking volume segments historically tied to rotary screens.

Sustainability Regulations Pushing Water-less Printing

Regulators treat water stewardship as a statutory obligation. The US NESHAP regime and the EU’s Corporate Sustainability Reporting Directive oblige mills to disclose water and chemical footprints, directing buyers toward water-less systems. [2]United States Environmental Protection Agency, “Printing, Coating, and Dyeing of Fabrics and Other Textiles: NESHAP,” epa.govEquipment makers respond with closed-loop platforms; EFI Reggiani’s ecoTERRA line cuts water use by 80% compared with conventional routes. Buyers increasingly benchmark machines on life-cycle metrics, making low-impact credentials a decisive factor in procurement.

Explosive Growth of E-Commerce On-Demand Models

Online configurators generate millions of unique artwork files, each demanding efficient single-unit processing. Print-on-demand hubs integrate digital presses with automated pick-pack-ship cells to enable same-day dispatch. Pandemic-driven channel shifts locked consumers into custom ordering habits that persist. AI-based recommendation engines design graphics automatically, spawning fresh demand categories from pet portraits to fan-art leggings. [3]The Interline, “Industrialising Innovation: The Business Case for Digital Printing,” theinterline.comQuality convergence between digital and screen output permits premium price tags without offline finishing steps.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of industrial inkjet equipment | -1.4% | Global, particularly impacting emerging markets | Short term (≤ 2 years) |

| Colour-fastness and durability versus analogue prints | -0.8% | Global, with higher impact in technical textiles | Medium term (2-4 years) |

| Scarcity of technicians for complex printheads | -0.6% | Global, acute in APAC and emerging markets | Medium term (2-4 years) |

| Fragmented environmental certification regimes | -0.4% | Europe and North America, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Industrial Inkjet Equipment

Industrial units priced at USD 500,000–2 million dwarf the outlay for a rotary or flat-bed screen set-up. Total cost of ownership expands further after factoring specialist inks, preventive maintenance, and operator certification. Financing remains scarce in developing regions, stalling adoption despite abundant growth headroom. Leasing and modular expansion schemes exist but have limited penetration, leaving capital intensity a short-term brake on conversion from analog lines.

Colour-Fastness and Durability Versus Analogue Prints

Technical textile buyers, from automotive trim to marine upholstery, still prefer screen prints for extreme wash and weather resistance. Research shows higher colour stability on polyester blends after multiple launderings when analog techniques are used. [4]Society for Imaging Science and Technology, “Color Accuracy and Durability for Printed, Branded Textiles,” imaging.org Although new reactive and nano-pigment chemistries narrow the gap, large institutional customers wait for documented field data before switching. The perceived performance deficit slows uptake in critical-spec markets until ink suppliers prove parity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Printing Technology: Direct-to-Fabric Strength Anchors Growth Trajectory

Direct-to-Fabric processes held 38.44% printed textiles market share in 2024, benefiting from compatibility with legacy finishing lines and broad material reach. The printed textiles market size advantage comes from shorter setup times and elimination of film or screen storage, which lowers per-print fixed costs. Single-pass pigment engines, though only a niche today, are scaling at an 11.83% CAGR as mills target water-less operations without sacrificing hand feel.

Demand polarization drives technology mixing. Fashion houses rely on DTG units for micro-drops, while home-textile converters favor high-speed roll-to-roll lines that link directly to stenter frames. Hybrid rigs equipped with automatic palette switches allow operators to run screen for mono-colour yardage and pivot to digital for multicolour or variable-data batches. AI-driven scheduling software allocates designs to the economically optimal lane, boosting throughput and ink yield. Equipment builders therefore bundle RIP, cloud analytics, and service subscriptions into their offerings to lock-in lifetime revenue streams.

By Ink Type: Disperse Direct Retains Leadership Amid Sublimation Uptick

Disperse direct formulations occupied 42.85% of 2024 volume because of their deep penetration into synthetic workwear, banner, and flag lines. Sublimation inks, however, lead growth at 10.74% CAGR as polyester adoption widens in activewear and interior décor. This shift influences the printed textiles market, with colour-gamut improvements and faster transfer at lower calender temperatures accelerating changeover.

Pigment systems now tap binder innovations that secure chemical bonding without post-wash cycles, opening cotton-rich segments previously exclusive to reactive inks. Regulatory pressure on volatile organic compounds pushes converters toward water-based chemistries that meet OEKO-TEX 2025 limits. Ink suppliers consolidate to serve multiprocess customers, evidenced by Archroma’s acquisition of Huntsman Textile Effects, which broadens turnkey portfolios for digital users.

By Fabric/Substrate: Polyester’s Dual Role as Volume Leader and Growth Engine

Polyester controlled 52.59% of 2024 demand and is forecast to post a 12.11% CAGR through 2030, giving it the unusual status of both market leader and fastest mover. Its affinity for sublimation dyes, dimensional stability, and favourable cost curve underpin the printed textiles market expansion. Circular economy pilots now process post-consumer polyester back into printable fibre, aided by ventures such as the Selenis–Syre recycling facility in North Carolina.

Cotton retains relevance in premium apparel, exploiting reactive inks that highlight soft hand feel. Silk and wool hold luxury niches but depend on acid chemistries, limiting volume. Blended fabrics meet performance-price trade-offs, while bio-based PET entrants seek commercial scale. Substrate choice is increasingly a sustainability decision as brands adopt design-for-recycling rules that favour mono-material constructions compatible with established digital ink sets.

By Application: Technical Textiles Provide the Base; Fashion Delivers Momentum

Technical textiles generated 39.59% of revenue in 2024 thanks to automotive, medical, and protective gear segments that command higher unit economics. These fields demand stringent functional coatings and colour durability, anchoring the printed textiles market’s value pool. Automated inspection and traceability modules embedded in digital lines satisfy quality protocols for mission-critical uses.

Fashion and apparel, advancing at an 11.45% CAGR, benefit from fast-fashion calendars and influencer-driven capsule launches that call for nimble print cycles. Direct-to-consumer web stores publish 3D garment previews, routing confirmed orders straight to micro-factories. Home décor, signage, and experiential retail progressively adopt soft-fabric visuals that reduce freight costs versus rigid substrates. Emerging smart-textile applications, including conductive ink patterns for heating elements and IoT sensors, foreshadow a new frontier in functional printed fabrics.

Geography Analysis

Asia-Pacific commanded 38.67% of 2024 shipments on the back of entrenched mills, integrated dye houses, and government incentives that target 70% digital penetration in China’s print halls. India accelerates through seven planned mega textile parks, each reserving floorspace for digital equipment, allowing the printed textiles market to tap export opportunities under duty-free corridors. Vietnam and Bangladesh add capacity through joint-venture clusters that bundle renewable power, water recycling, and training centres.

Middle East and Africa, though a smaller base, records a 10.98% CAGR led by Egypt’s USD 1.1 billion infrastructure upgrade of public spinning and weaving complexes. Gulf Co-operation Council states leverage energy-cost advantages to attract sublimation operations aimed at sports merchandising tied to mega-events. Morocco and Tunisia secure EU near-shoring contracts that require quick lead times and sustainable certification.

North America’s reshoring initiatives elevate regional production of graphic tees, décor fabrics, and event signage. US tariff hikes on imported textiles tighten domestic sourcing rationales. Micro-factories in Los Angeles, Dallas, and Toronto use AI-driven planning to synchronise e-commerce orders with same-day dispatch. Europe retains premium segments, but stringent chemical rules and impending carbon border adjustments push mills toward water-less workflows and renewable electricity sourcing.

Latin America gains momentum from regional trade blocs and brand interest in near-sourcing for US markets. Brazil modernises decades-old rotary plants with hybrid modules, while Mexico’s maquiladora zones add DTG clusters to feed cross-border e-commerce. Overall, geographic expansion aligns with policy incentives, logistics economics, and the availability of skilled digital technicians.

Competitive Landscape

The printed textiles market is moderately fragmented. Technology majors such as Epson, HP Inc., and Kornit Digital continue to extend portfolios through acquisitions and in-house head production. Epson’s USD 34.2 million printhead plant quadruples output capacity before 2025, signalling confidence in sustained digital uptake. Brother Industries’ bid for Roland DG broadens its exposure to large-format textiles. Mimaki, Kyocera, and EFI compete on throughput and software interoperability, bundling cloud diagnostics and consumables subscription models.

Incumbents move toward vertically integrated ecosystems—printer, workflow, ink, and service—locking clients into multi-year contracts. Open-platform newcomers pitch modular heads and agnostic RIPs to undercut closed architectures. AI-enabled predictive maintenance becomes a soft differentiator, with Kornit embedding machine learning that auto-tunes ink laydown for fabric tension variances.

Sustainability shapes competitive priorities. Vendors showcase water-less, energy-efficient lines at MILANO UNICA and ITMA fairs, positioning environmental performance alongside colour fidelity metrics. Strategic alliances emerge between equipment builders and fibre recyclers to co-market circular production stories. Price competition remains acute in entry-level DTG units, yet high-end roll-to-roll and single-pass installations hinge on application expertise and lifetime service reliability.

Printed Textiles Industry Leaders

Kornit Digital Ltd.

Seiko Epson Corporation

HP Inc.

Mimaki Engineering Co., Ltd.,

EFI Reggiani

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Mimaki Engineering launched the Tx330 Series digital textile system with expanded substrate compatibility

- June 2025: Roland DG introduced the TrueVIS XG-640 1,600 mm printer featuring 1,800 dpi output

- April 2025: Epson unveiled the SureColor G6070, its first 35-inch direct-to-film device

- February 2025: Mimaki debuted the Tiger600-1800TS dye-sublimation unit aimed at high-volume soft signage

Global Printed Textiles Market Report Scope

| Direct-to-Fabric (DTF) |

| Direct-to-Garment (DTG) |

| Dye-Sublimation |

| Reactive Inkjet |

| Pigment Single-Pass |

| Reactive |

| Sublimation |

| Pigment |

| Acid |

| Disperse Direct |

| Cotton |

| Polyester |

| Blends |

| Silk |

| Other Fabric / Substrate |

| Fashion and Apparel |

| Home Textiles |

| Technical Textiles |

| Soft Signage and Displays |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Printing Technology | Direct-to-Fabric (DTF) | ||

| Direct-to-Garment (DTG) | |||

| Dye-Sublimation | |||

| Reactive Inkjet | |||

| Pigment Single-Pass | |||

| By Ink Type | Reactive | ||

| Sublimation | |||

| Pigment | |||

| Acid | |||

| Disperse Direct | |||

| By Fabric / Substrate | Cotton | ||

| Polyester | |||

| Blends | |||

| Silk | |||

| Other Fabric / Substrate | |||

| By Application | Fashion and Apparel | ||

| Home Textiles | |||

| Technical Textiles | |||

| Soft Signage and Displays | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current size of the printed textiles market?

The printed textiles market size stands at USD 264.73 billion in 2025 and is projected to grow to USD 398.18 billion by 2030.

Which region generates the highest demand for printed textiles?

Asia-Pacific leads, holding 38.67% of global revenue due to its extensive manufacturing base and sustained government support for digital upgrades.

Which printing technology is expanding the fastest?

Pigment single-pass systems exhibit the fastest momentum, advancing at an 11.83% CAGR as mills seek higher speed, water-less workflows.

Why is polyester so dominant in printed textile substrates?

Polyester aligns perfectly with dye-sublimation chemistry, offers competitive pricing, and now benefits from recycling initiatives that enhance its sustainability profile.

What are the main barriers hindering digital adoption in textile printing?

High capital costs for industrial inkjet equipment and lingering durability concerns in technical applications remain primary restraints, particularly for small and medium-sized enterprises.

How are sustainability regulations influencing market dynamics?

Tighter global rules on water use and chemical emissions accelerate the shift toward water-less digital platforms, making environmental performance a core purchasing criterion.

Page last updated on: