Photo Printers Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 4.69 Billion |

| Market Size (2030) | USD 7.13 Billion |

| Growth Rate (2025 - 2030) | 8.74% CAGR |

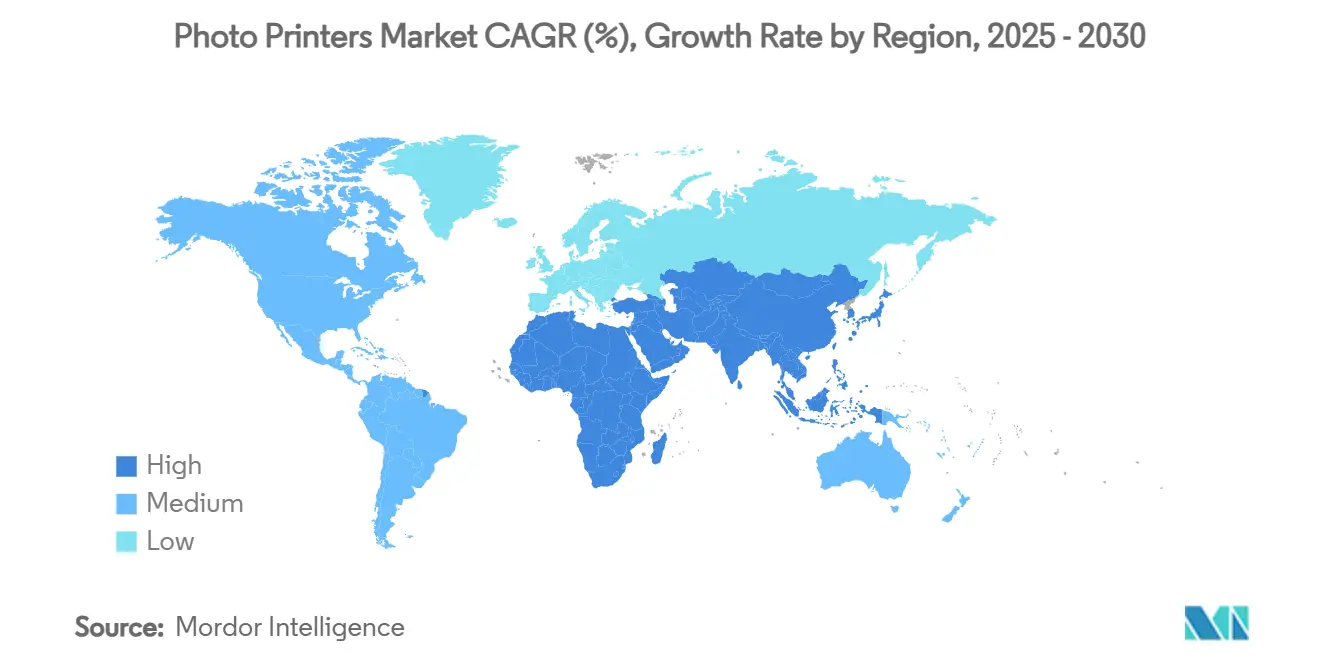

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

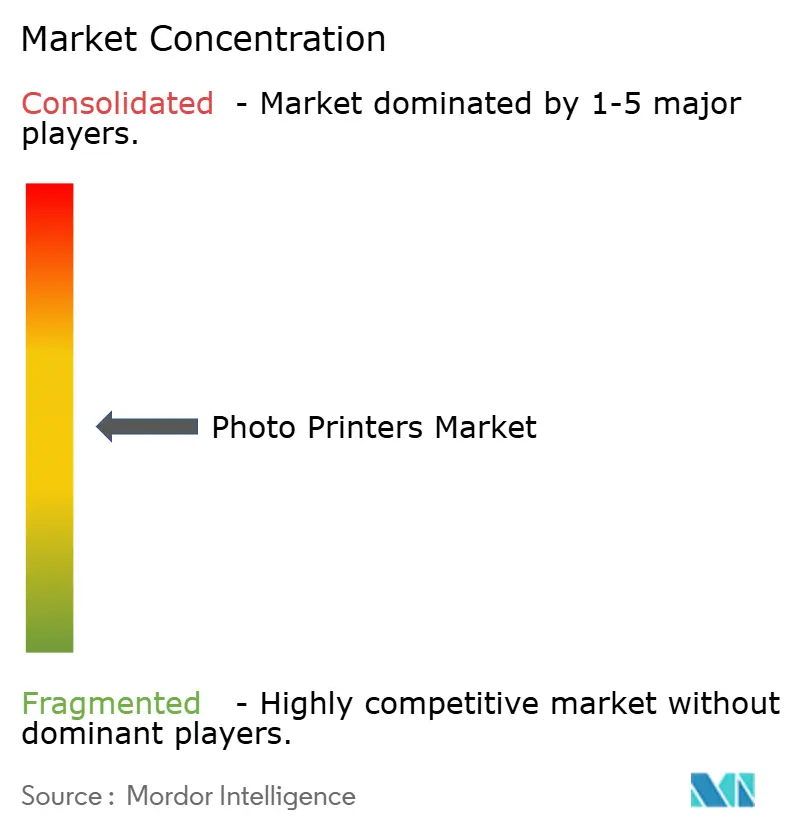

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Photo Printers Market Analysis by Mordor Intelligence

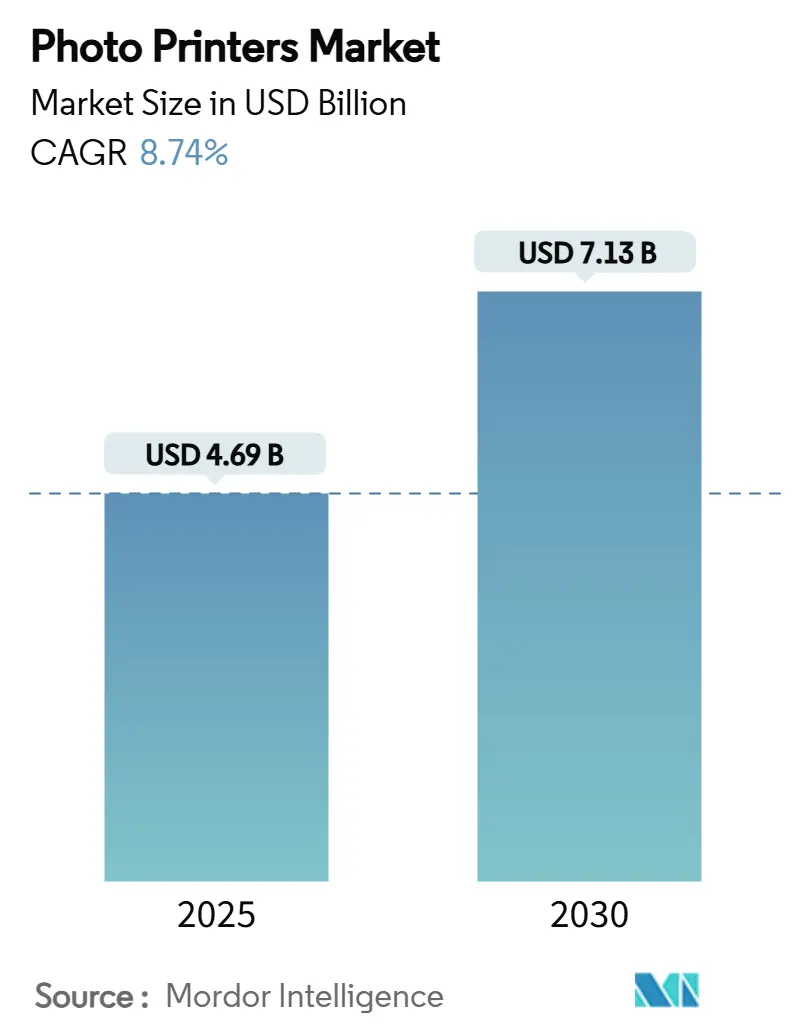

The photo printers market stood at USD 4.69 billion in 2025 and is projected to reach USD 7.13 billion by 2030, advancing at an 8.74% CAGR. Sustained demand for instant prints that complement social sharing, steady progress in inkjet and dye-sublimation quality, and wide smartphone adoption anchor this momentum. Portable models that connect directly to handsets are reshaping purchase priorities, while retail kiosk upgrades keep legacy channels viable. Asia-Pacific’s deep manufacturing base and large mobile user pool reinforce its leadership position, and corporate capital commitments such as Epson’s new printhead plant signal confidence in multiyear growth.[1]Seiko Epson Corporation, “Epson to Construct New Inkjet Printhead Factory,” global.epson At the same time, recurring-revenue consumables models and eco-centric product roadmaps are redefining competitive strategies within the photo printers market.

Key Report Takeaways

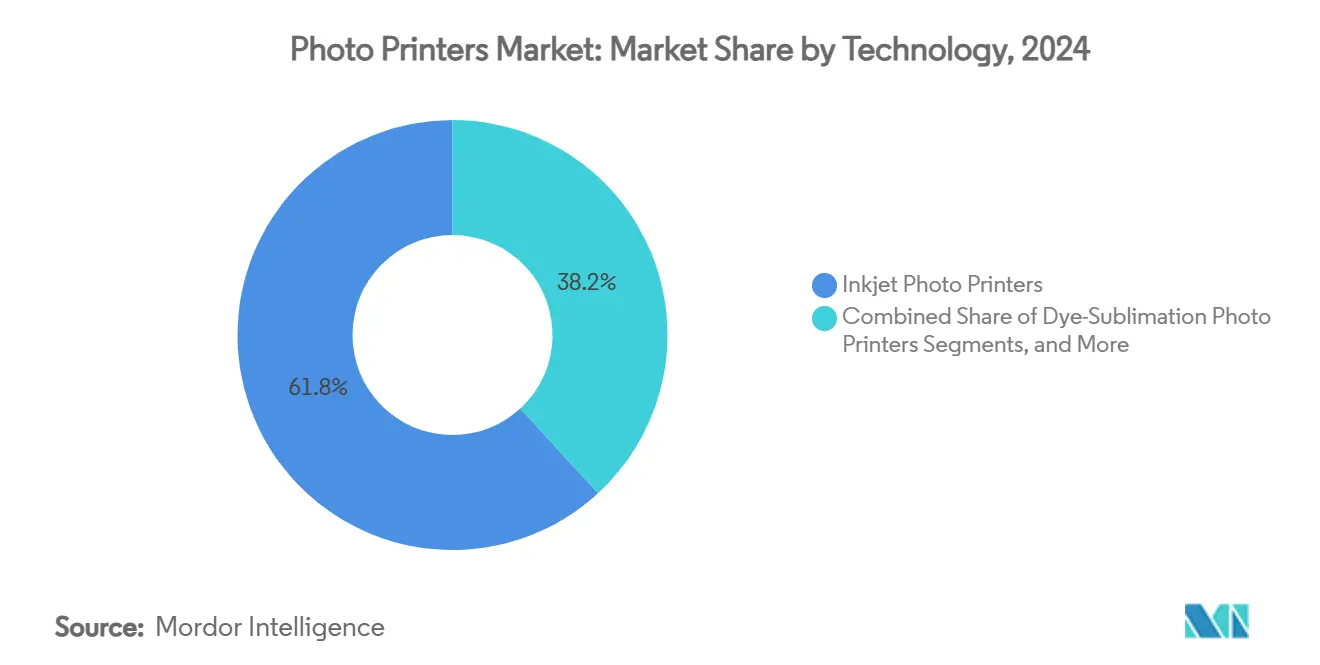

- By technology, inkjet printers captured with a 61.83% share of the photo printers market in 2024.

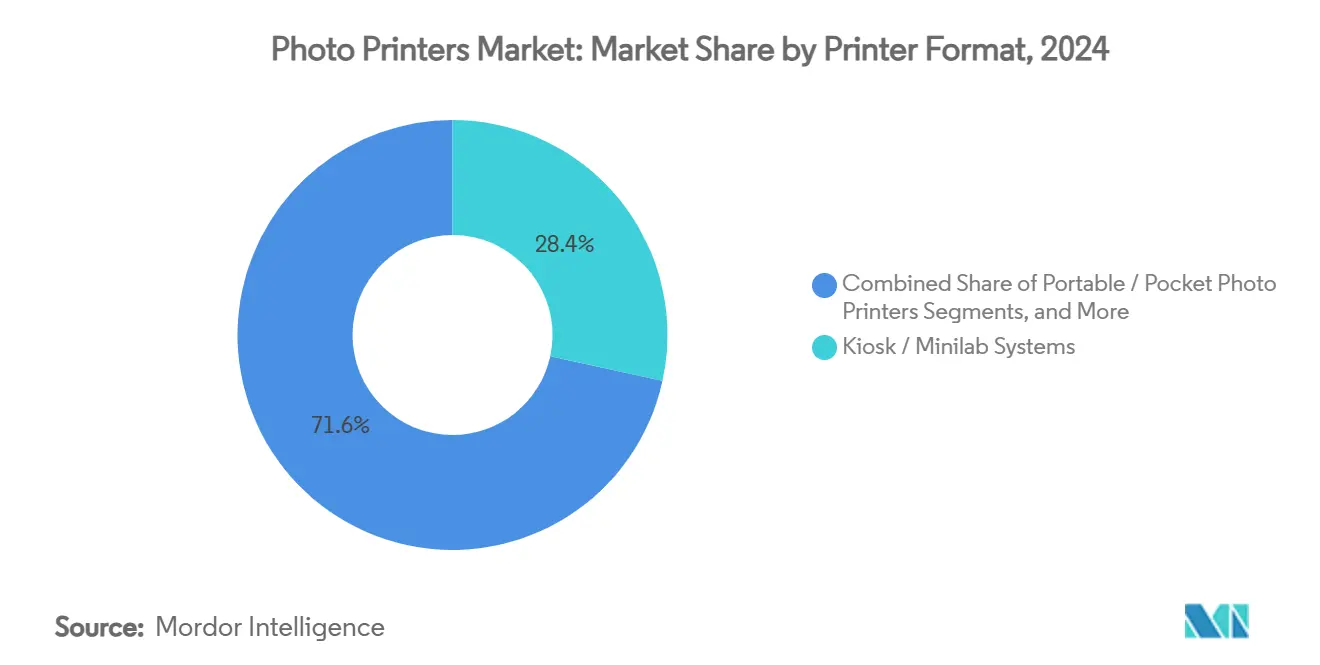

- By printer format, photo printers market for portable/pocket devices segment projected to grow at 10.16% CAGR between 2025-2030.

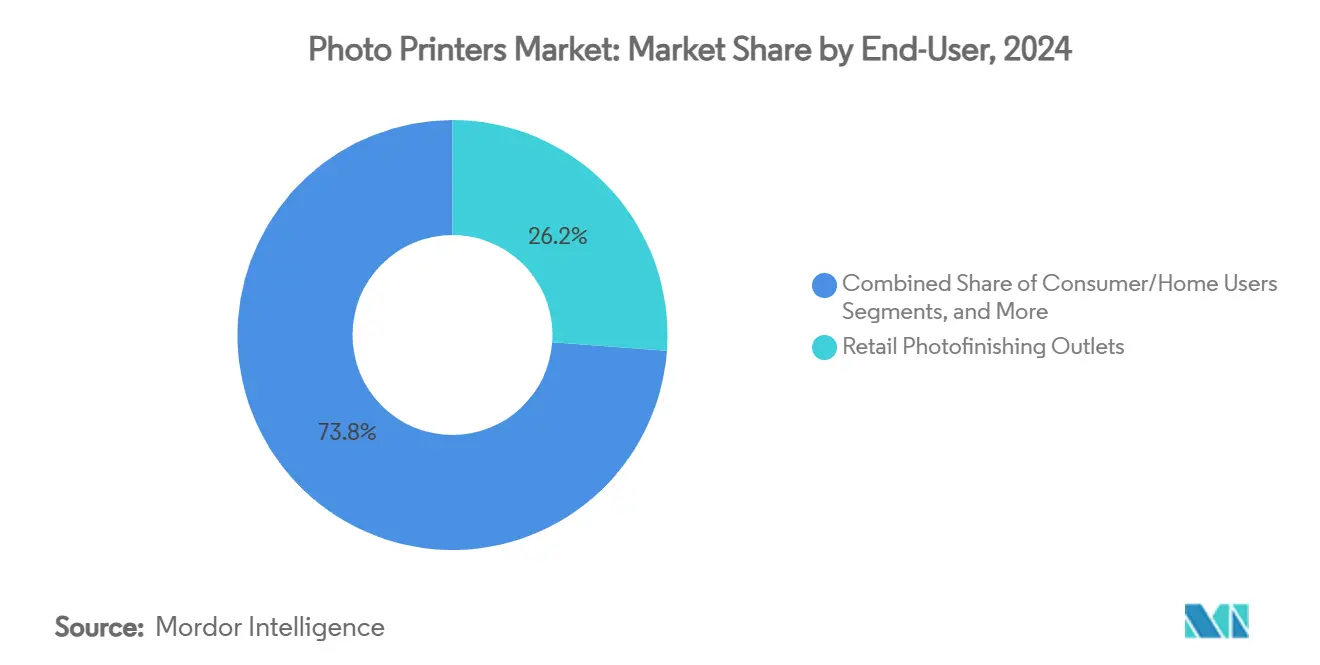

- By end user, retail photofinishing outlets captured with a 26.19% share of the photo printers market in 2024.

- By geography, the photo printers market for the Asia-Pacific region is projected to grow at a 9.72% CAGR between 2025-2030.

Global Photo Printers Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in social-media-driven instant photo printing demand | +1.8% | Global, with concentration in North America and APAC | Short term (≤ 2 years) |

| Technological advances in dye-sublimation and inkjet photorealism | +1.5% | Global, led by Japan and Germany | Medium term (2-4 years) |

| Expansion of event photography and photo-booth installations | +1.2% | North America and Europe, expanding to APAC | Medium term (2-4 years) |

| Rapid adoption of smartphone-connected portable photo printers among Gen-Z and millennials | +2.1% | Global, highest in APAC and North America | Short term (≤ 2 years) |

| Growth in corporate and personalized merchandise applications | +0.9% | North America and Europe, emerging in APAC | Long term (≥ 4 years) |

| Emerging AR-enabled and smart print solutions unlocking new consumer experiences | +0.7% | North America and APAC early adopters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rise in Social-Media-Driven Instant Photo Printing Demand

Photo-centric social platforms are turning digital storytelling into physical keepsakes that strengthen emotional engagement. High-visibility influencers routinely transform curated feeds into tangible memorabilia for limited-edition drops that fuel peer-to-peer commerce. Brick-and-click retailers echo this behavior by offering same-day pickup from mobile uploads, reinforcing the appeal of quick print gratification. As algorithms reward authentic imagery, printed outputs become part of brand toolkits that forge deeper audience ties. Consequently, spontaneous print volumes rise whenever key cultural moments trend, sustaining a broad-based appetite for instant printers within the photo printers market.

Technological Advances in Dye-Sublimation and Inkjet Photorealism

Improved thermal efficiency and wider color gamuts let dye-sublimation engines rival professional lab output, while next-generation inks boost fade resistance in inkjet lines. Canon’s dual-platform strategy covering electrophotography and inkjet equipment underscores the need for cross-segment flexibility. [2]Canon Inc., “Annual Report 2024,” global.canon Image-processing chips borrowed from smartphone pipelines now drive on-device AI that tunes tone, sharpness, and red-eye correction without user input. These innovations mitigate historic frustration with home print quality and stimulate hardware refresh cycles, thereby lifting unit demand across the photo printers market.

Expansion of Event Photography and Photo-Booth Installations

Hybrid events merge physical venues with live streams yet still prize tangible souvenirs. Contemporary photo booths employ augmented-reality lenses, brand overlays, and QR-enabled sharing that dovetail with real-time printing. Professional operators rely on compact, high-throughput devices that function reliably under variable lighting and power constraints. Weddings, corporate activations, and music festivals allocate budget lines specifically for onsite print experiences that enhance attendee satisfaction. This pattern keeps high-margin media and consumables flowing even as base hardware prices compress, reinforcing forward revenue visibility for vendors active in the photo printers market.

Rapid Adoption of Smartphone-Connected Portable Photo Printers Among Gen-Z and Millennials

Wireless protocols such as Wi-Fi Direct and Bluetooth Low Energy simplify pair-and-print workflows integral to a mobile-first lifestyle. Younger cohorts seek tangible collages for scrapbooks, dorm décor, and gift personalization, pivoting from purely digital expression. App ecosystems fold in creative fonts, sticker packs, and social challenges that trigger repeat media purchases. Subscription bundles for ink or ribbon refills transition manufacturers from transactional sales to annuity streams, deepening brand stickiness. As battery densities rise and thermal control improves, palm-sized devices gain endurance that widens use cases during travel or outdoor gatherings, bolstering momentum across the photo printers market.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of digital photo sharing reducing print volumes | -2.3% | Global, most pronounced in developed markets | Short term (≤ 2 years) |

| High cost of consumables and replacement media | -1.8% | Global, particularly impacting price-sensitive segments | Medium term (2-4 years) |

| Environmental concerns around dye-sublimation waste and recycling challenges | -1.1% | Europe and North America, expanding globally | Medium term (2-4 years) |

| Periodic semiconductor supply issues impacting printhead production | -0.6% | Global, with highest impact in APAC manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Proliferation of Digital Photo Sharing Reducing Print Volumes

Cloud galleries and AI-curated albums simplify archiving, thereby lowering the perceived need for routine prints. Feature-rich in-app editing coupled with ephemeral stories satisfies many daily sharing rituals, diverting casual users from physical output. Younger consumers view sustainability as a lifestyle imperative, so they forego printing low-value snapshots that may end up discarded. Even so, higher emotional moments—graduations, milestone trips—still trigger specialty printing, leading to segmentation rather than outright collapse of demand within the photo printers market.

High Cost of Consumables and Replacement Media

Razor-and-blade economics expose users to recurring costs that can exceed initial hardware price over a device’s life cycle. Regulatory guidelines on dye-sublimation waste disposal in the United States and Europe inflate compliance overheads that manufacturers pass through in ribbon and paper pricing epa.gov. Supply fluctuations for specialty substrates lead to price spikes that undercut mass-market appeal. As a result, fiscally cautious buyers may opt for online fulfillment services or crowdsource prints, tempering near-term sales potential for home units across the photo printers market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Inkjet Dominance Meets Dye-Sublimation Upsurge

Inkjet devices captured 61.83% of the photo printers market share in 2024 thanks to multi-surface versatility and entrenched consumer familiarity. Their micro-piezo printheads lay precise droplets on glossy, matte, or canvas media, which supports hobbyists and professionals alike. Vendors exploit modular cartridge systems that lower entry prices while safeguarding margin through refill cycles. Dye-sublimation systems, though smaller in installed base, logged the fastest 9.87% CAGR and are favored for smudge-proof, lab-quality output completed in under a minute. The photo printers market increasingly polarizes around cost-focused inkjet units and premium dye-sub offerings, squeezing mid-tier hybrid concepts.

The photo printers market size attributed to inkjet technology amounted to USD 2.9 billion in 2025, whereas dye-sublimation accounted for USD 1.3 billion and is projected to double by 2030. Epson’s JPY 5.1 billion (USD 0.03 billion) capacity build-out will quadruple inkjet printhead output by late 2025, easing bottlenecks that previously limited commercial placements.[3]Seiko Epson Corporation, “Press Release on Production Expansion,” global.epson Proprietary head chemistry creates lock-in that benefits scale players and discourages new entrants. Meanwhile, thermally efficient dye-sub engines leverage compact heating elements that extend battery life in portable designs, giving that segment a strong youth appeal inside the broader photo printers market.

By Printer Format/Size: Portable Revolution Reshapes Market Structure

Kiosk and minilab systems held 28.42% of the photo printers market size in 2024, underscoring ongoing relevance of retail photo finishing zones inside supermarkets, drugstores, and convenience chains. These stations now embed touch-free interfaces and cloud pull-down options that align with post-pandemic hygiene preferences. Yet portable or pocket printers, with a 10.16% forecast CAGR, represent the most vibrant growth pocket by catering to spur-of-the-moment creativity. Formerly niche zink units have migrated into mainstream channels through lifestyle collaborations that pair pastel devices with matching accessory packs.

Compact desktop A4/A5 printers straddle office and hobby use, offering predictable media costs that please household budgeters, whereas professional desktop A3+ models target galleries that demand archival inks. Large-format 24-inch devices remain indispensable to commercial studios producing wall art, though that slice is narrow. Engineers continue to miniaturize mechanical assemblies, relying on high-torque micro-motors and advanced polymers supplied by precision component firms such as MinebeaMitsumi. As a result, portable units now weigh under 200 g yet deliver 300 dpi output, a milestone that strengthens their pull across the photo printers market.

By End User: Retail Resilience and Event-Driven Upside

Retail photofinishing outlets accounted for 26.19% share of the photo printers market in 2024, benefiting from legacy traffic and trusted brand positioning. Chains bundle online upload portals with same-hour pickup, creating a hybrid model that shields them from pure e-commerce disruption. Consumer/home users form a mature but loyal cohort that values instant gratification and decorative applications like scrapbooking. Professional photographers wrestle with margin compression as smartphone cameras improve, yet they defend niche business by offering large-format metallic prints and curated albums.

Event and entertainment providers, growing at a 10.25% CAGR, fuse experiential marketing with tangible takeaways that extend brand recall beyond an event’s boundary. Corporate activations budget for themed overlays, while amusement parks deploy waterproof media for ride photos. Commercial print service providers meet B2B briefs ranging from point-of-sale displays to personalized merchandise, tapping industrial-scale inkjet lines that prioritize throughput. Each user cluster reinforces the diverse channel matrix that defines the photo printers market and cushions it from single-source volatility.

Geography Analysis

Asia-Pacific dominated the photo printers market with 39.37% share in 2024 and is advancing at a 9.72% CAGR through 2030. Regional leadership springs from vertically integrated supply chains that place component fabs, assembly plants, and logistics hubs within close radius. High smartphone penetration—above 90% in Japan, South Korea, and urban China creates a colossal installed base for portable printer attachments. Cultural practices that value printed keepsakes at ceremonies continue to generate recurring demand. Canon, Brother, and Epson funnel substantial R&D budgets into local ink-science centers, reinforcing innovation velocity and anchoring the region at the forefront of next-generation device launches.

North America’s role in the photo printers market is defined by premium positioning and innovation throughput. Retail labs retrofit kiosks with biometric logins and privacy screens that appeal to security-conscious users, while professional studios adopt pigment-rich inks that satisfy archival standards. Sustainability preferences foster uptake of recyclable cartridges and paper sourced from Forest Stewardship Council-certified suppliers. Corporate demand for event photo activations reinforces utilization rates for mid-volume dye-sub rigs, supporting a balanced revenue mix between consumer and commercial segments.

Europe approaches the photo printers market through the lens of environmental stewardship and regulatory rigor. Extended Producer Responsibility directives obligate manufacturers to collect and recycle spent media, raising compliance hurdles that favor established players with structured take-back schemes. Consumers display willingness to pay premiums for eco-validated products, allowing vendors to preserve margins despite higher operating costs. The region’s intense professional photography culture anchored by fashion capitals like Paris and Milan fuels steady demand for large-format inkjet devices that deliver color-critical proofs. As circular-economy policies tighten, Europe could pioneer reusable cartridge loops that later diffuse globally.

Competitive Landscape

Market leaders HP, Canon, and Epson manage deep patent arsenals, wide channel reach, and large installed bases that confer scale advantages. Each firm coordinates hardware launches with proprietary apps and subscription replenishment plans, transforming product ecosystems into service networks. Canon’s Printing Group booked USD 16.5 billion net sales in 2024 and reoriented into vertical business units to sharpen solution fit.[4] Epson’s micro-piezo technology underpins both consumer photo lines and industrial signage, providing cross-segment leverage that dilutes R&D risk. HP pursues cost discipline through its Future Ready plan aimed at USD 1.9 billion structural savings, which funds pivot into cloud-linked print workflows hp.com.

Smaller manufacturers target specialization to sidestep head-to-head competition. Mitsubishi Electric builds dye-sub kiosks tailored for tourist attractions, while Kodak channels heritage optics know-how into high-gamut dry-lab systems for professional minilabs. Brother’s “CS B2027” strategy earmarks JPY 200 billion (USD 1.32 billion) growth investment for industrial labeling and commercial printing, banking on synergies with mechatronics operations. Supply security has become a differentiator; firms with captive printhead capacity weather semiconductor tightness better than assemblers that outsource core components.

Competitive focus has shifted from page-per-minute specs to total user experience. Seamless smartphone onboarding, cloud backup hooks, and augmented-reality print triggers now influence buying decisions. Vendors therefore expand SDKs that let third-party developers embed print calls into social or productivity apps, widening device utility. Sustainability metrics energy footprint per print, proportion of bio-based plastics join classic quality benchmarks in tender evaluations. Collectively, these pressures keep innovation cycles brisk and reinforce moderate concentration within the photo printers market.

Photo Printers Industry Leaders

HP Inc.

Canon Inc.

Seiko Epson Corporation

Fujifilm Holdings Corporation

Brother Industries, Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Canon issued its Annual Report 2024, outlining a net-zero roadmap and expansion in commercial printing and office MFP segments.

- February 2025: HP reported fiscal 2025 first-quarter printing revenue of USD 4.3 billion, noting 5% growth in consumer printing and a 2% overall decline.

- January 2025: Epson released its Sustainability Report 2024, confirming 100% renewable energy use at major plants and inkjet innovations for lower CO₂ output.

- December 2024: Mitsubishi Electric expanded its Serendie digital platform to strengthen IoT connectivity across printer portfolios.

Global Photo Printers Market Report Scope

| Inkjet Photo Printers |

| Dye-Sublimation Photo Printers |

| ZINK (Zero-Ink) Photo Printers |

| Thermal Transfer Photo Printers |

| Portable / Pocket Photo Printers |

| Compact Desktop Photo Printers (A4/A5) |

| Professional Desktop Photo Printers (A3+) |

| Large-Format Photo Printers (24+) |

| Kiosk / Minilab Systems |

| Consumer / Home Users |

| Professional Photographers and Studios |

| Retail Photofinishing Outlets |

| Event and Entertainment Providers |

| Commercial Print Service Providers |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Technology | Inkjet Photo Printers | ||

| Dye-Sublimation Photo Printers | |||

| ZINK (Zero-Ink) Photo Printers | |||

| Thermal Transfer Photo Printers | |||

| By Printer Format / Size | Portable / Pocket Photo Printers | ||

| Compact Desktop Photo Printers (A4/A5) | |||

| Professional Desktop Photo Printers (A3+) | |||

| Large-Format Photo Printers (24+) | |||

| Kiosk / Minilab Systems | |||

| By End-User | Consumer / Home Users | ||

| Professional Photographers and Studios | |||

| Retail Photofinishing Outlets | |||

| Event and Entertainment Providers | |||

| Commercial Print Service Providers | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Indonesia | |||

| Thailand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the photo printers market?

The photo printers market is valued at USD 4.69 billion for 2025 and is projected to reach USD 7.13 billion by 2030.

Which region leads the photo printers market?

Asia-Pacific led with 39.37% share in 2024 and is expected to post the fastest 9.72% CAGR through 2030.

What technology segment dominates the photo printers market?

Inkjet printers dominate with 61.83% revenue share in 2024, while dye-sublimation models record the quickest 9.87% growth rate.

Why are portable photo printers growing so rapidly?

Smartphone connectivity, Gen-Z demand for tangible keepsakes, and lighter battery-powered designs drive the 10.16% CAGR in portable/pocket devices.

How are environmental regulations affecting the market?

Compliance with waste-disposal rules raises consumables costs, nudging vendors toward recyclable media and refillable cartridges to retain eco-minded buyers.

Which end-user segment is expanding the fastest?

Event and entertainment providers are growing at a 10.25% CAGR because instant prints enhance attendee experience at weddings, concerts, and corporate activations.

Page last updated on: