Print Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 20.67 Billion |

| Market Size (2031) | USD 24.22 Billion |

| Growth Rate (2026 - 2031) | 3.22% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

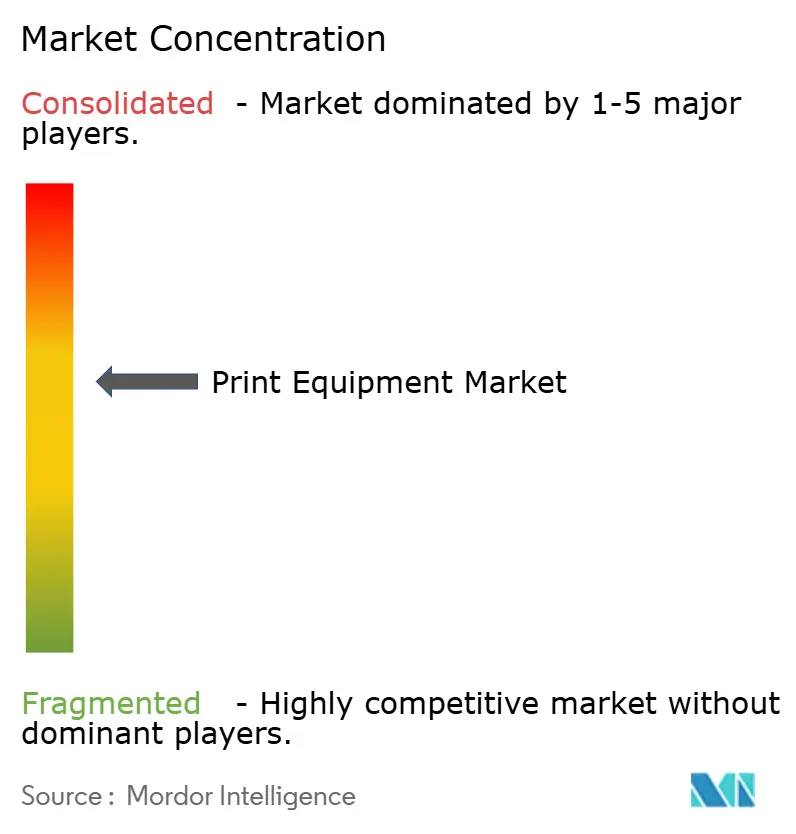

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Print Equipment Market Analysis by Mordor Intelligence

The Print Equipment Market size is projected to expand from USD 19.98 billion in 2025 and USD 20.67 billion in 2026 to USD 24.22 billion by 2031, registering a CAGR of 3.22% between 2026 to 2031. Demand is shifting from offset-dominated lines toward digital and hybrid presses as converters chase fast changeovers, minimal makeready, and variable-data features. Food and pharmaceutical labeling rules in the European Union and the United States are pulling capital toward presses that support serialization and allergen declarations. E-commerce fulfillment centers are buying narrow-web digital equipment to print shipping boxes on the day of dispatch, while brand owners widen SKU counts to serve micro-segments. Competitive pressure from software-centric entrants is forcing incumbent press makers to add cloud-connected workflow platforms and subscription plans, a pivot that raises refinancing needs but promises sticky service revenue.

Key Report Takeaways

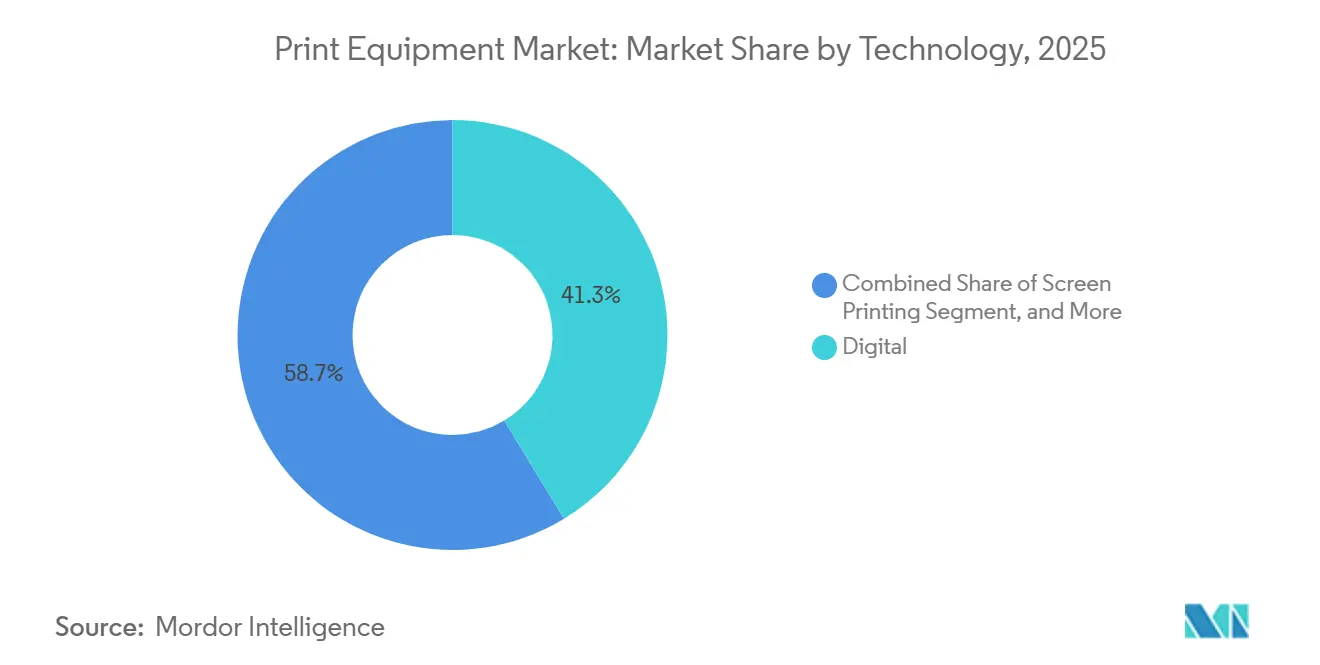

- By technology, digital technology led the print equipment market with 41.32% market share in 2025 and is forecast to expand at a 4.02% CAGR through 2031.

- By equipment type, press equipment held a 37.32% share of the print equipment market size in 2025, while post-press and finishing systems posted the fastest trajectory at a 3.84% CAGR over 2026-2031.

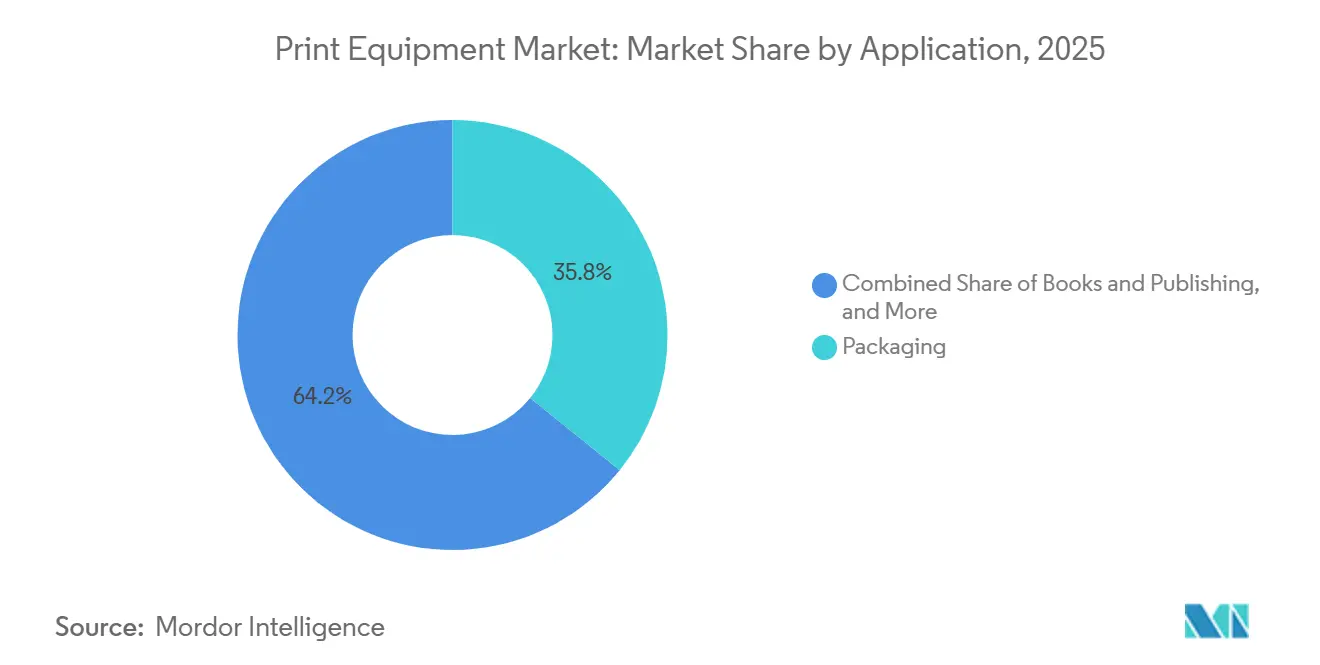

- By application, packaging accounted for 39.81% of the print equipment market in 2025 and is advancing at a 3.96% CAGR through 2031.

- By end user, packaging converters accounted for 44.32% of demand in 2025 and are growing at a 3.78% CAGR through 2031.

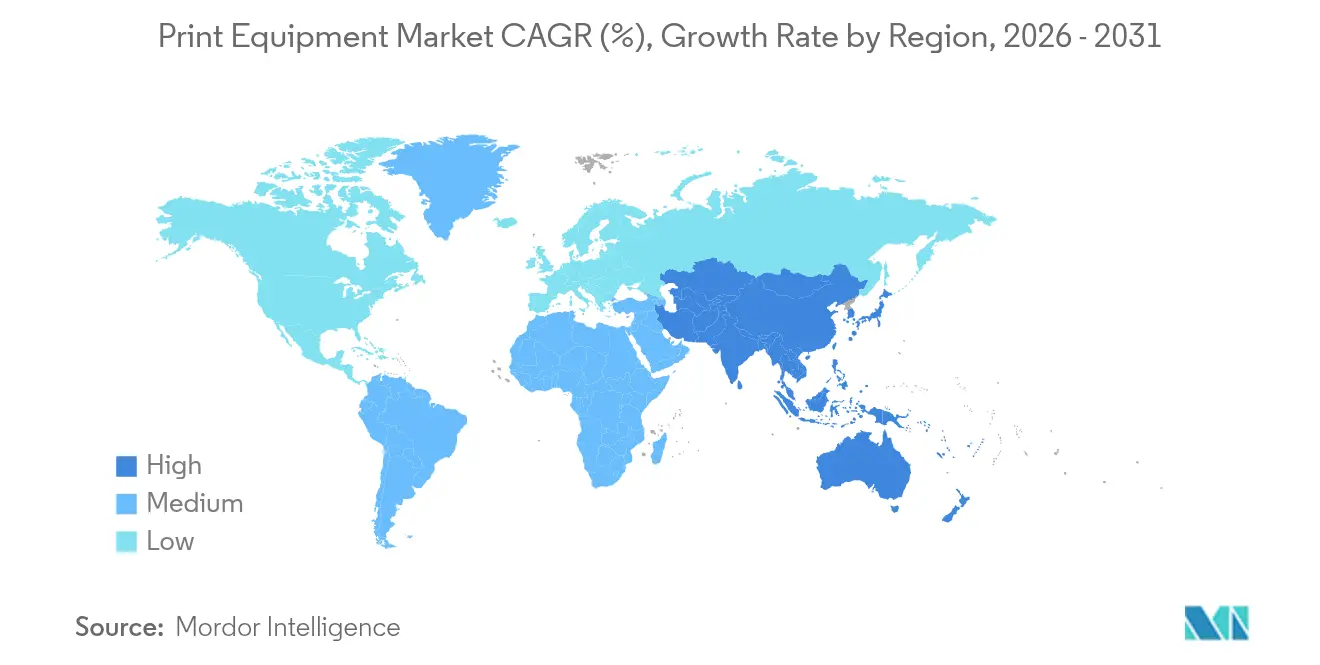

- By geography, Asia-Pacific accounted for 41.43% of global volume in 2025 and is projected to grow at a 4.12% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Print Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Tailwinds for Food and Pharma Digital Labels | +0.9% | Global, Led by EU and North America | Medium Term (2–4 Years) |

| On-Demand Book and Packaging Runs Driving CAPEX | +0.7% | North America and Europe, Expanding to Asia-Pacific | Short Term (≤2 Years) |

| Brand-Owner Push for SKU Proliferation | +0.6% | Global | Medium Term (2–4 Years) |

| Hybrid Press Adoption Reduces Total Cost of Ownership | +0.5% | Europe and North America | Long Term (≥4 Years) |

| AI-Based Predictive Maintenance Minimizes Press Downtime | +0.4% | High-Automation Markets | Medium Term (2–4 Years) |

| Rise of Decentralized Micro-Factories Near End Users | +0.3% | Asia-Pacific and Middle East | Long Term (≥4 Years) |

| Source: Mordor Intelligence | |||

Regulatory Tailwinds For Food And Pharma Digital Labels

EU and U.S. labeling mandates now require digital watermarks, variable allergen labeling, and batch-level traceability, pushing converters toward inkjet retrofits and greenfield digital press purchases. India added QR serialization for export drugs in April 2025, reinforcing this global convergence.[1]Food Safety and Standards Authority of India, “QR Code Serialization Requirements,” fssai.gov.in Brand owners are prequalifying suppliers based on ISO 12647 compliance, so press vendors bundle spectrophotometers and closed-loop calibration with every sale to pass customer audits. Digital presses also help converters avoid penalties that EU regulators can levy at up to 4% of global turnover for mislabeled food products, a risk that makes analog changeover errors untenable. To hedge against future rule changes, pharmaceutical packagers now specify presses that accept both water-based and UV-curable inks, ensuring headroom for low-migration formulations once PFAS restrictions tighten. The net effect is that digital serialization has become a board-level CAPEX trigger rather than a mere regulatory checkbox.

On-Demand Book And Packaging Runs Driving CAPEX

Short-run economics flipped after 2024, when 62% of commercial printers accepted jobs below 500 units, up from 41% in 2020, thanks to toner and inkjet lines that erase plate cost and makeready waste. E-commerce hubs now print corrugated boxes on-site, reducing inventory costs and enabling same-day seasonal promotions. Cimpress committed more than USD 100 million for HP Indigo units to localize production and cut order-to-ship cycles from 72 to 24 hours. Publishers such as Springer Nature moved 78% of backlist titles to print-on-demand, eliminating the need to pulp unsold stock. Offset press makers are racing to bolt inkjet bars onto web lines so they can chase jobs that fall in the 1,000-10,000 range, where analog speed still matters. As these hybrid prototypes prove reliable, lenders are starting to offer structure-specific leasing packages that bundle service and consumables, lowering the hurdle rate for mid-size shops.

Brand-Owner Push For SKU Proliferation

Unilever launched 1,200 new SKUs in 2024, a 35% jump that forces packaging suppliers to shrink changeover windows from hours to minutes.[2]Unilever, “Annual Report and Accounts 2024,” unilever.com Procter and Gamble highlights limited-edition packaging as a core growth lever, intensifying the need for plate-free variable graphics. Sustainability targets complicate ink selection because recyclable mono-material films limit solvent tolerance, pushing converters toward modular presses that switch chemistries mid-shift. Digital presses let marketers A/B-test label artwork at the shelf within one replenishment cycle, a feedback loop impossible with analog tooling. Large converters therefore invest in multi-technology lines that mix water-based, UV, and solvent stations under common workflow software. Smaller plants without this capital either merge into larger networks or exit, accelerating market consolidation.

Hybrid Press Adoption Cuts Total Cost Of Ownership

Heidelberg’s Cartonmaster CX-145 unites flexographic and inkjet stations, so folding-carton converters slash plate inventory while maintaining analog speed for long runs. Bobst, Koenig, and Bauer aim to commercialize a gravure-digital hybrid that meets opacity demands for metalized films where inkjet still lags. Benchmarking shows hybrids break even above 10,000 impressions with frequent SKU change because they eliminate plate cost on variable panels while retaining high line speed. Dual-skill labor is scarce, so vendors embed AI job routing and automated registration to mask process complexity from operators. Early adopters report 18% lower total waste and a 12-month payback when hybrid lines replace two separate presses. Finance arms of manufacturers now offer performance-based leases tied to uptime, further sweetening adoption economics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Graphic-Paper Prices Squeeze Margins | −0.6% | Europe And North America | Short Term (≤2 Years) |

| Skilled Press-Operator Shortage | −0.5% | Europe And North America | Medium Term (2–4 Years) |

| Escalating Cyber-Security Risks In Cloud-Connected Presses | −0.3% | Global | Medium Term (2–4 Years) |

| PFAS Regulations Limiting Certain Ink Chemistries | −0.2% | Europe, Select United States States | Long Term (≥4 Years) |

| Source: Mordor Intelligence | |||

Volatile Graphic-Paper Prices Squeeze Margins

Nordic and Brazilian pulp spikes in early 2025 lifted coated-sheet prices 18%, squeezing printer EBITDA and delaying press upgrades. EU circular-economy rules encourage recycled fiber, but variable sheet quality forces operators to recalibrate presses more often, increasing downtime and ink lay-down. Converters with thin 8-12% margins struggle to pass these hikes through multi-year customer contracts, so CAPEX for new lines slips down the priority list. Some offset printers hedge pulp risk with futures contracts, yet hedging fees rose 22% in 2025, eroding the benefit. Digital vendors pitch reduced waste, but high-coverage inkjet jobs consume expensive ink and drums, muting savings. As a result, investment bifurcates: large groups lock multi-year paper deals and adopt high-speed inkjet, while small shops defer upgrades and ride spot-market volatility.

Skilled Press-Operator Shortage

The U.S. Bureau of Labor Statistics projects a 7% decline in press-operator employment between 2024 and 2034 as retirements outpace new entrants.[3]United States Bureau of Labor Statistics, “Printing Workers Outlook,” bls.gov Germany’s trade body reports that 40% of printers cite staffing as their top capacity constraint, prompting increased workflow automation spending.[4]Bundesverband Druck und Medien, “Skilled Labor Survey 2025,” bvdm-online.de Vendors answer with remote diagnostics and AI color matching, but these cloud links expose plants to cybersecurity and network-outage risks. Apprenticeship programs cannot fill the gap fast enough, so some converters recruit gamers and retrain them on digital presses that resemble large touch-screen consoles. Asia-Pacific printers now echo the concern as younger workers favor e-commerce and coding roles, driving wage inflation for experienced operators. Without labor relief, converters cap utilization at 85-90% to avoid burnout, limiting revenue growth even when demand surges.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Digital Gains Momentum

Digital captured 41.32% of the print equipment market in 2025 and rose at 4.02% annually. Inkjet and toner lines appeal to converters who need variable graphics without plate costs, a value that offsets slower raw speed. The print equipment market size for digital presses is forecast to expand significantly as publishers pivot to print-on-demand. Offset retains long runs, yet its slice narrows each year. Flexographic units stay vital for high-opacity flexible films, while gravure holds ultra-long decorative work. Screen equipment remains a niche for textiles and electronics. Converters increasingly choose hybrid rigs that bolt inkjet bars onto flexo webs, balancing run length and personalization.

Canon and Heidelberg joined forces in 2024 on a B2 electrophotographic engine, aiming to anchor hybrid mid-volume models. Ricoh’s production inkjet roadmap targets label converters craving plate elimination. Advances in aqueous inkjet have improved adhesion on uncoated stock, yet rub resistance still trails solvent systems.

By Equipment Type: Post-Press Automation Accelerates

Press hardware held 37.32% of 2025 tonnage, but post-press equipment is the fastest-growing segment, with a 3.84% CAGR, as plants automate die-cutting, folding, and inspection. The print equipment market share for finishing lines is growing as labor shortages make robotic blank separation and vision QC more attractive. Heidelberg’s Cartonmaster integrates these steps, showing how turnkey cells compress floor space and cycle time. Pre-press systems commoditize under cloud workflows, yet remain essential for color control. Ancillary gear, such as slitters and laminators, sustains demand in flexible packaging, where converters juggle multiple substrates each shift.

Bobst logged a 28% order rise for Mastercut die-cutters in 2024, reflecting the urgency to cut downtime. Sheet-fed presses still dominate commercial work thanks to their format agility, whereas roll-fed lines shrink as magazine volume declines. Format-wise, B1 and B2 classes secure mid-runs, while B3 serves quick printers. Proprietary ancillary bundles raise switching costs and draw antitrust scrutiny in the EU and the United States.

By Application: Packaging Dominates

Packaging owned 39.81% of 2025 volume and is set to climb 3.96% through 2031 as e-commerce commands short-run corrugated and flexible jobs. The print equipment market size for packaging presses benefits from fulfillment centers printing boxes on demand to trim inventory. HP secured USD 50 million in Indigo orders from ePac, underscoring digital economics below 10,000 impressions. Books and publishing shrink in unit terms, but print-on-demand props volume stability. Advertising and signage migrate toward roll-fed inkjet for banners and retail displays. Security and transactional printing remain niche but sticky due to regulatory barriers.

UNCTAD pegged global online retail at 22% of sales in 2025, reinforcing corrugated growth. Flexible-pack converters add inkjet bars to legacy flexo lines, marrying speed with personalization. Books rely on just-in-time runs that cut warehousing and pulping costs, while signage splits between flatbed screen for mass runs and inkjet for targeted graphics.

By End User: Converters Lead Spend

Packaging converters held 44.32% of outlays in 2025 and grow at 3.78% as they chase recyclable mono-material orders and SKU bursts. The print equipment market share among converters climbs because hybrid presses reduce waste and downtime. Commercial printers diversify into checks and secure docs yet wrestle with uncertain catalog demand. In-plant shops are downsizing fleets and outsourcing peak loads, accelerating consolidation. Quick-print outlets face online brokers with algorithmic pricing, forcing exits or mergers.

DS Smith invested GBP 120 million (USD 152 million) to add digital corrugated capacity across Europe. Commercial printers deploy wide-format inkjet for signage, stretching sales skills into substrates and finishing. In-plant retreats, born during remote work shifts, free capacity that larger converters absorb. Vertical integration blurs lines as packaging groups buy commercial shops to internalize label work.

Geography Analysis

Asia-Pacific accounted for 41.43% of global volume in 2025 and is projected to grow at 4.12% through 2031. China’s CNY 8 billion (USD 1.1 billion) subsidy funds digital press rollouts in smaller cities, shrinking logistics miles. India’s drug exporters are retrofitting lines for EU serialization, boosting inkjet demand. Japan’s majors embrace hybrid presses for short-run packaging, while Australia faces import-duty drag on new equipment. South Korea grows in screen systems for semiconductor packaging.

Europe and North America together account for about 45% of the 2025 tons, but growth is slow. EU traceability rules push converters toward digital serialization, straining small operators. Germany saw 4% fewer overall installs in 2024, yet digital orders rose 12% as firms pursued waste-cutting initiatives. The United States splits: large packaging houses pour money into high-speed inkjet, while many commercial shops sweat legacy offset assets. Canada consolidates as mid-sized printers fold or merge.

South America, the Middle East, and Africa hold the rest. Brazil invests in flexo for food packaging but fights import-cost volatility. Saudi Arabia backs local printing under Vision 2030 with soft loans for presses. The United Arab Emirates markets free-zone print hubs to serve Gulf and Africa. South Africa grapples with energy costs but sees selective inkjet buys for pharma cartons, while Kenya scales packaging lines for regional consumer demand.

Competitive Landscape

Top manufacturers Heidelberg, Koenig and Bauer, HP, Canon, and Bobst together held roughly a 40%-45% share in 2025, indicating moderate concentration. Each pivots from hardware sales to subscription service, embedding remote diagnostics that promise higher margins but raise cyber exposure. Heidelberg refinanced EUR 436 million (USD 462 million) in January 2026 to back this shift and cut interest expense. Epson bought EFI’s Fiery front-end for USD 591 million, deepening vertical integration and locking in consumables. Canon and Heidelberg co-develop B2 engines for hybrid presses, yet execution risks remain if converters delay capital amid macro headwinds.

Workflow software now differentiates vendors more than press mechanics. Machine-learning modules predict roller wear and adjust ink dosing, reducing dependence on veteran operators. ISO 12647 compliance sits high on RFP checklists, compelling bundling of color spectrophotometers and closed-loop systems. Smaller players Mark Andy, Nilpeter, and Gallus focus on narrow-web label presses, competing on application know-how and fast service rather than scale. Online job-routing platforms emerge as indirect rivals by commoditizing excess capacity and tightening converter margins.

The mid-term battlefield centers on hybrid configurations that weld analog speed to digital personalization. No single vendor yet dominates these systems, leaving room for alliances and joint ventures. Capital intensity and supply-chain resilience will dictate winners as component lead times and financing costs fluctuate.

Print Equipment Industry Leaders

Heidelberger Druckmaschinen AG

Bobst Group SA

HP Inc.

Canon Inc.

Koenig and Bauer AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Heidelberg refinanced EUR 436 million (USD 462 million) debt, extending maturities to 2029 and trimming annual interest by EUR 15 million.

- November 2025: Heidelberg reported a 7% order-intake rise, with 42% of new presses bundled with Prinect subscriptions.

- June 2025: Heidelberg launched Cartonmaster CX-145, a hybrid folding-carton line with robotic blank separation.

- May 2025: HP booked a USD 50 million Indigo order from ePac Flexible Packaging covering multiple 25K units.

Global Print Equipment Market Report Scope

The Print Equipment Market Report is Segmented by Technology (Web-offset Lithographic, Flexographic, Gravure, Screen Printing, Digital), Equipment Type (Pre-press Systems, Press, Post-press and Finishing, Ancillary and Inline Converting), Application (Books and Publishing, Advertising and Signage, Security and Transactional, Packaging, Other Applications), End-User Industry (Packaging Converters, Commercial Printers, In-plant/Corporate, Quick Print and Copy Shops), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Web-offset Lithographic |

| Flexographic |

| Gravure |

| Screen Printing |

| Digital |

| Pre-press Systems |

| Press(Sheet-fed, Roll-fed) |

| Post-press and Finishing |

| Ancillary and Inline Converting |

| Books and Publishing |

| Advertising and Signage |

| Security and Transactional |

| Packaging |

| Other Applications |

| Packaging Converters |

| Commercial Printers |

| In-plant/Corporate |

| Quick Print and Copy Shops |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Kenya | |

| Rest of Africa |

| By Technology | Web-offset Lithographic | |

| Flexographic | ||

| Gravure | ||

| Screen Printing | ||

| Digital | ||

| By Equipment Type | Pre-press Systems | |

| Press(Sheet-fed, Roll-fed) | ||

| Post-press and Finishing | ||

| Ancillary and Inline Converting | ||

| By Application | Books and Publishing | |

| Advertising and Signage | ||

| Security and Transactional | ||

| Packaging | ||

| Other Applications | ||

| By End-User Industry | Packaging Converters | |

| Commercial Printers | ||

| In-plant/Corporate | ||

| Quick Print and Copy Shops | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will global demand for print equipment be by 2031

Volume is forecast to reach 24.22 million tons by 2031, reflecting a 3.22% CAGR from 2026.

Which technology is growing fastest

Digital presses, already 41.32% of 2025 volume, are advancing at 4.02% per year as converters pursue variable data and short runs.

Why are packaging converters investing most heavily

E-commerce and SKU proliferation require rapid changeovers and serialized codes, making digital and hybrid presses attractive for packaging lines.

What region leads new equipment installations

Asia-Pacific captures 41.43% of 2025 volume and expands at 4.12% through 2031, supported by Chinese and Indian incentive programs.

How are manufacturers changing their business models

Incumbents are shifting from one-time hardware sales to subscription service, bundling workflow software and predictive maintenance to lock in recurring revenue.

Page last updated on: