Inkjet Printers Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

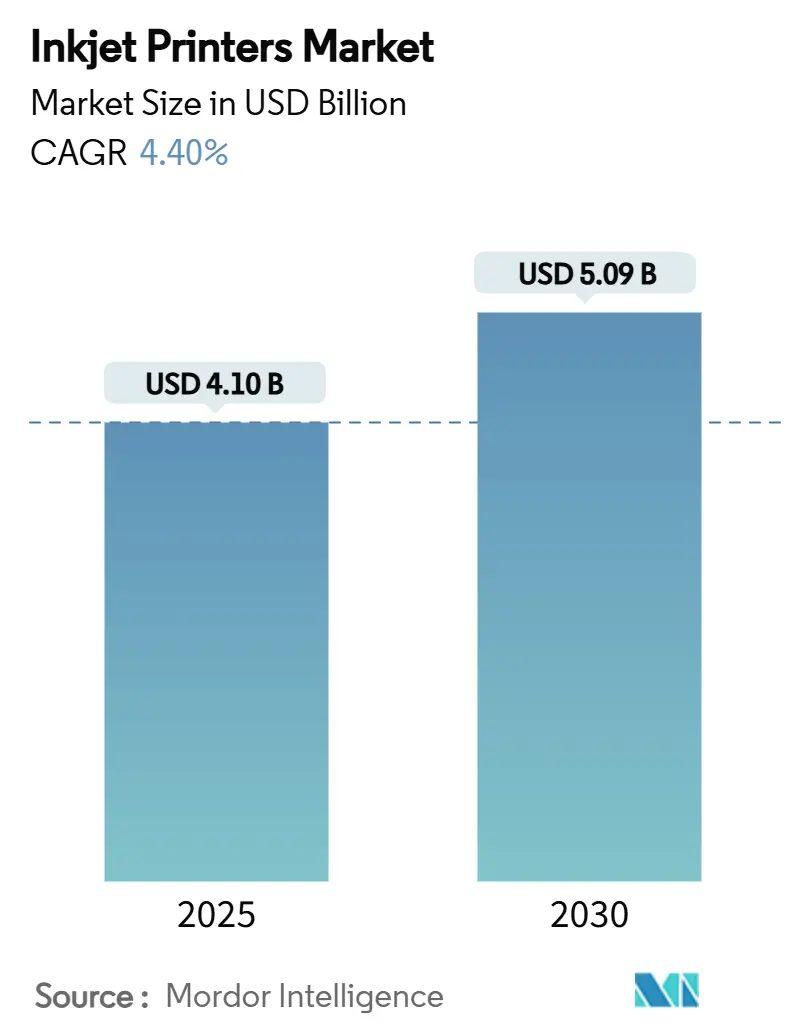

| Market Size (2025) | USD 4.10 Billion |

| Market Size (2030) | USD 5.09 Billion |

| Growth Rate (2025 - 2030) | 4.40% CAGR |

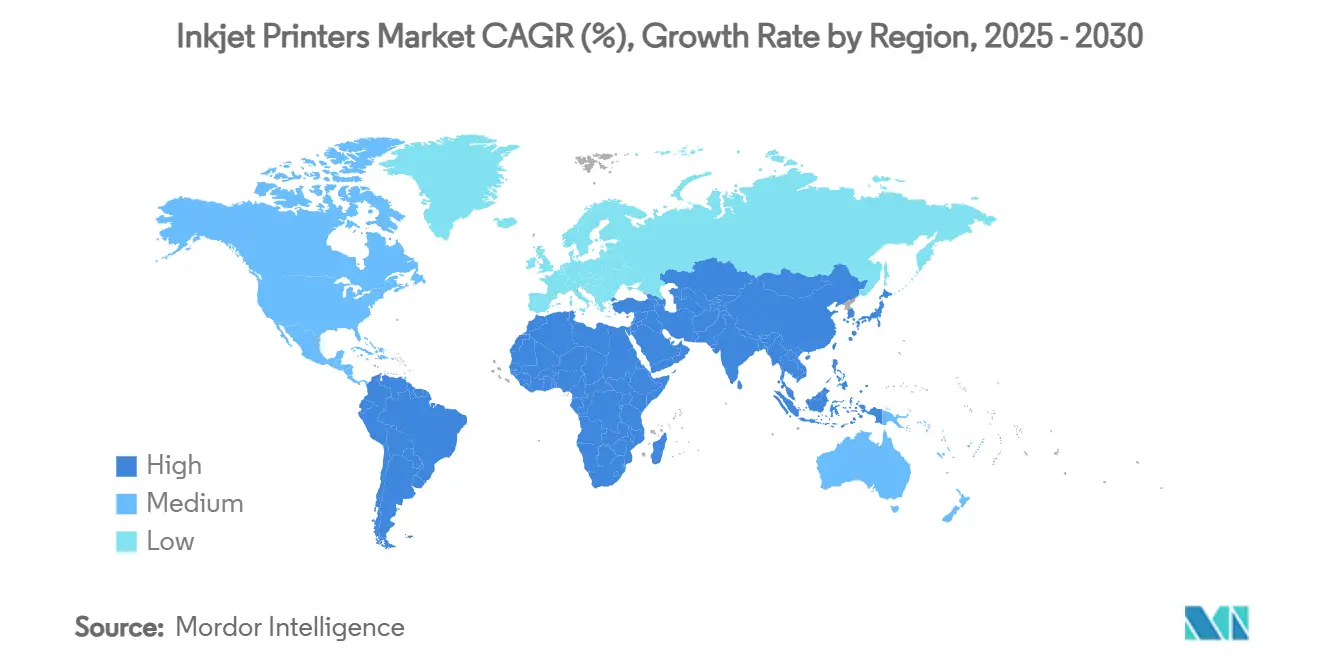

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

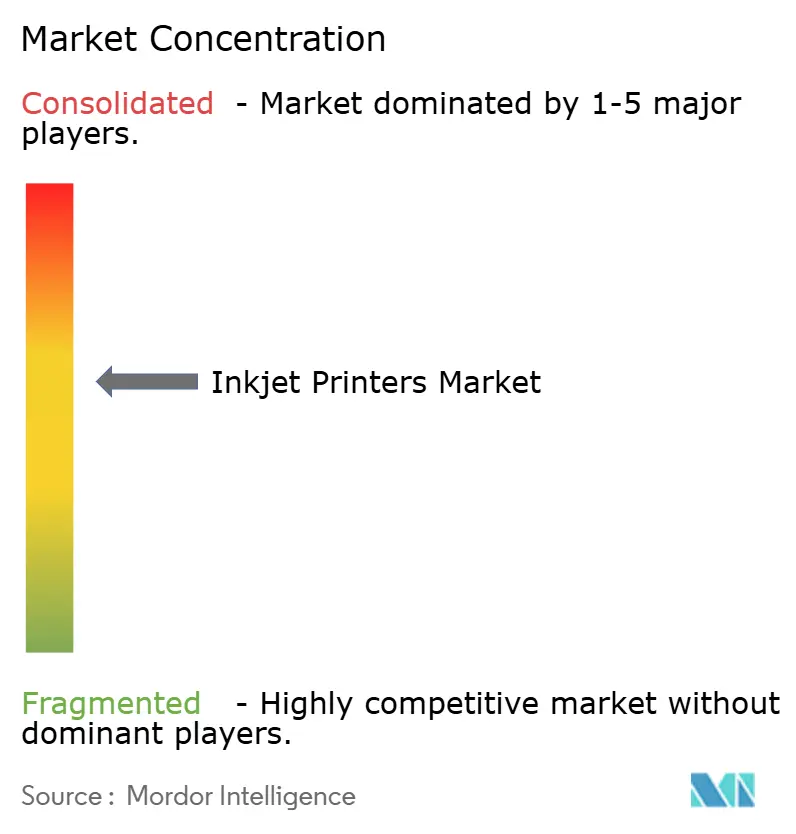

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Inkjet Printers Market Analysis by Mordor Intelligence

The inkjet printers market is valued at USD 4.10 billion in 2025 and is projected to reach USD 5.09 billion by 2030, advancing at a 4.40% CAGR. Hybrid work has prolonged household printing needs while industrial digitalization lifts demand for coding, labeling, and specialty applications. Large-format devices remain essential in architecture and graphics, yet continuous inkjet systems grow quickly as manufacturers seek automated, compliant coding. Asia-Pacific dominates current shipments thanks to its sizable manufacturing base and rapid adoption of Industry 4.0 solutions. Competitive intensity is rising as legacy office-centric vendors confront shrinking print volumes and margin pressure, whereas niche industrial suppliers gain share through application expertise and service models. Subscription-based supplies programs and managed print services continue to stabilize recurring revenue streams for diversified players.

Key Report Takeaways

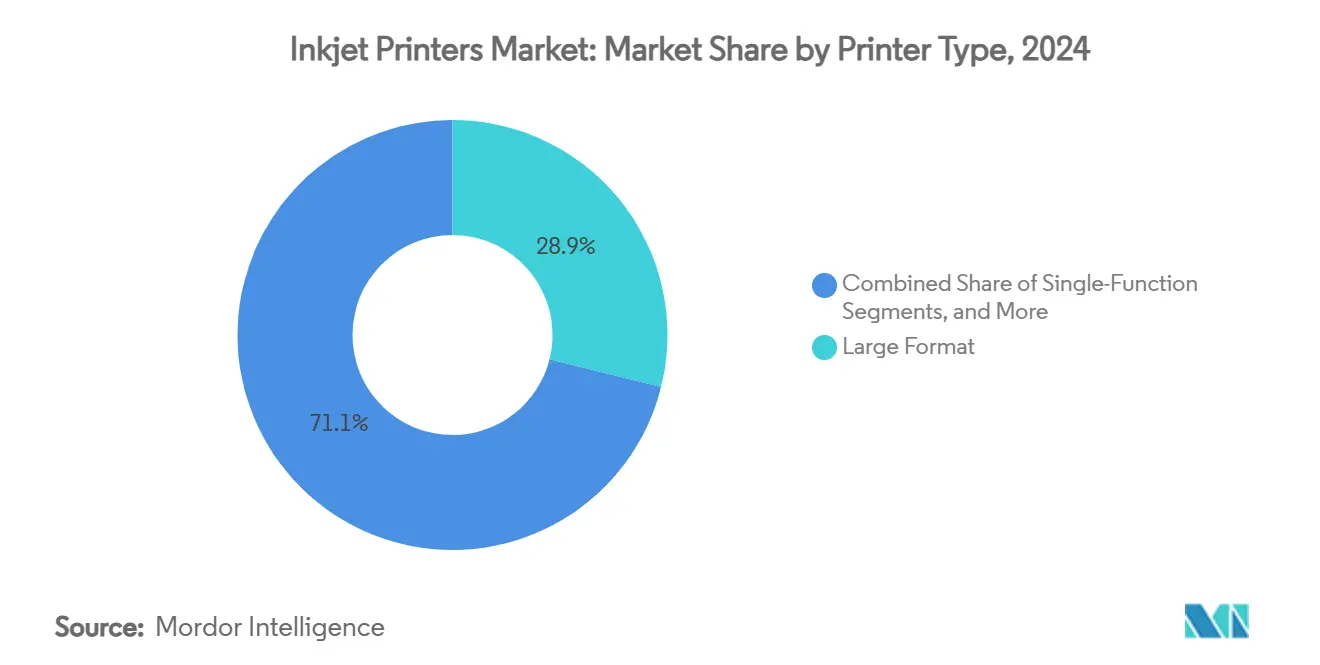

- By printer type, large-format units captured 28.89% share of the inkjet printers market in 2024.

- By technology, inkjet printers market for continuous inkjet technology segment projected to grow at 5.62% CAGR between 2025-2030.

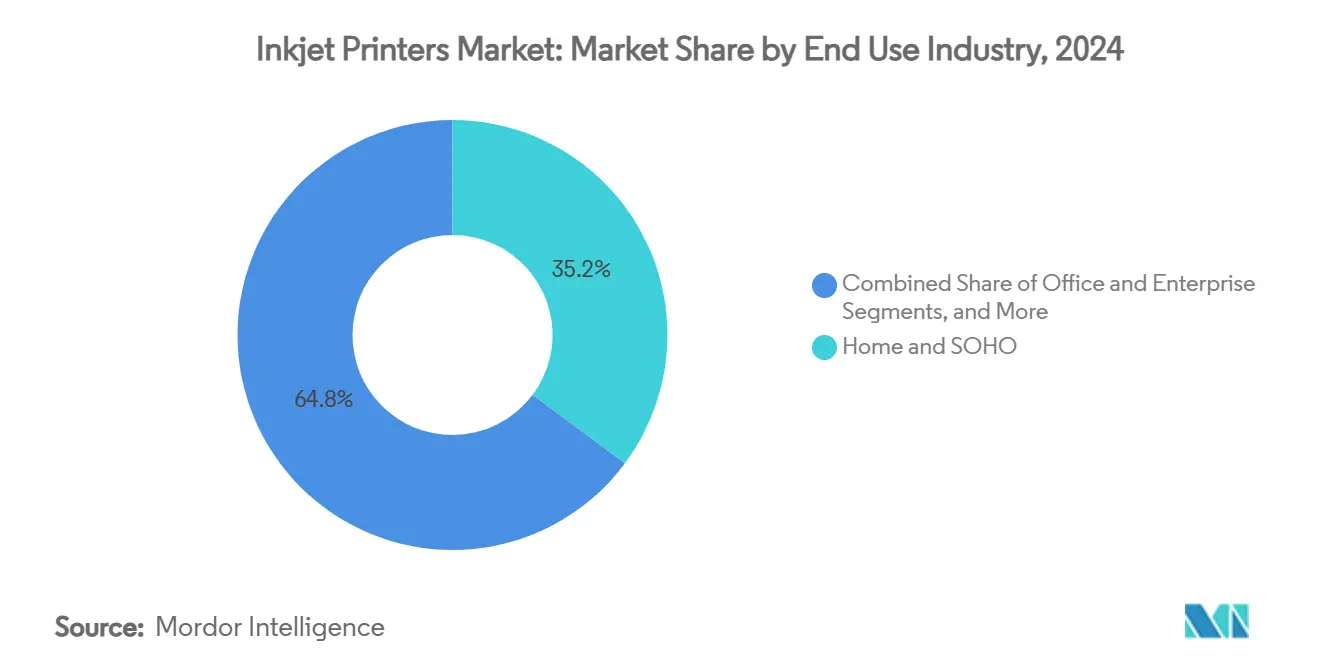

- By end-use industry, home and SOHO applications captured 35.17% share of the inkjet printers market in 2024.

- By substrate, inkjet printers market for textiles segment projected to grow at 5.45% CAGR between 2025-2030.

- By geography, Asia-Pacific captured 31.85% share of the inkjet printers market in 2024.

Global Inkjet Printers Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in hybrid-office demand post-COVID | +0.8% | Global, with higher impact in North America and Europe | Medium term (2-4 years) |

| Rapid penetration of industrial CIJ coding lines | +1.2% | APAC core, spill-over to North America and Europe | Long term (≥ 4 years) |

| Textile digitalisation and fashion on-demand shift | +0.7% | Global, with early gains in Asia-Pacific and Europe | Long term (≥ 4 years) |

| Sustainable water-free ink chemistries gaining preference | +0.5% | Europe and North America leading, APAC following | Medium term (2-4 years) |

| AI-enabled predictive maintenance lowering TCO | +0.4% | North America and Europe early adoption, APAC growth | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Hybrid-Office Demand Post-COVID

Hybrid work arrangements keep household printers running beyond pre-pandemic levels. HP recorded a 5% consumer printing revenue rise in Q1 2025 even as commercial printing softened, highlighting durable residential demand [1]HP Inc., “Q1 2025 Results,” hp.com. Users now expect compact high-capacity tank models that cut cost per page while fitting limited home office space. Vendors respond with cloud-enabled workflows and subscription ink services that ensure ongoing supply visibility and customer lock-in. Canon is rolling out devices explicitly designed for “hybrid working styles” to align with this usage pattern.[2]Canon Inc., “Integrated Report 2024,” global.canon The home-centric trend supports sustained hardware refresh cycles and recurring consumables opportunities for the inkjet printers market.

Rapid Penetration of Industrial CIJ Coding Lines

Manufacturers face mandatory lot coding and traceability requirements, making continuous inkjet systems a non-discretionary investment. US EPA monitoring rules covering ink formulations and capture equipment reinforce compliant technology adoption.[3]U.S. Environmental Protection Agency, “Printing and Publishing Industry Regulations,” epa.gov Ricoh’s inkjet head sales surged in China on the back of new packaging lines, reflecting regional industrial automation momentum. Higher-resolution heads and self-cleaning features curb downtime in fast-moving plants, enhancing total cost of ownership. With Industry 4.0 interfaces, CIJ printers now feed real-time quality data into factory control systems, strengthening their value proposition across Asia-Pacific and beyond.

Textile Digitalization and Fashion On-Demand Shift

Fashion brands are moving from bulk screen printing to digital technologies for shorter runs, customization, and lower environmental impact. Kornit Digital returned to profitability on USD 50.7 million Q3 2024 revenue as demand for its direct-to-garment systems rose. Waterless printing meets tightening environmental rules while slashing lead times, enabling near-shore production. Lectra posted a 154% jump in Asia-Pacific software subscriptions, evidence that design-to-print digital workflows are resonating with regional mills. As e-commerce accelerates personalized apparel, textile inkjet adoption should stay robust.

Sustainable Water-Free Ink Chemistries Gaining Preference

Regulators and corporate ESG goals push the shift toward low-VOCs, water-based, or plant-derived inks. Sakata INX launched its Botanical series using bio-based components to comply with European restrictions on hazardous substances. Brands gain marketing advantages while printers secure permits more easily, especially in Western Europe where emission caps are strict. Premium eco-formulations also open margin prospects as customers accept higher prices for sustainability alignment. The trend positions ink suppliers for value-added differentiation within the inkjet printers market.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile pigment raw-material prices | -0.6% | Global, with higher impact in APAC manufacturing hubs | Short term (≤ 2 years) |

| Rising e-document adoption in mature economies | -0.9% | North America and Europe primarily | Medium term (2-4 years) |

| Stringent VOC/chemical discharge regulations | -0.4% | Europe and North America leading, global expansion | Medium term (2-4 years) |

| Supply-chain concentration in Japan and China print-head makers | -0.5% | Global, with APAC supply chain dependencies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Pigment Raw-Material Prices

Shifts in pigment feedstock costs squeeze consumables margins that underpin profit pools for major OEMs. Canon acknowledged intense price competition and currency swings yet preserved profitability through internal cost control in 2023. Producers rely on concentrated supplier bases, heightening exposure to sudden price spikes. Long-term contracts and partial vertical integration help temper fluctuations, but near-term earnings remain vulnerable, especially for high-volume industrial printers where ink spend is material.

Rising E-Document Adoption in Mature Economies

Digital workflows and electronic signatures keep eroding office print volumes in developed markets. Xerox reported a 9.7% revenue drop to USD 6.22 billion in 2024, mirroring the secular decline of paper-based processes. Government agencies promote paperless communication to save costs and meet sustainability targets. Although legal and security-sensitive documents still demand hard copies, the addressable base for transactional printing contracts. Vendors respond by pivoting toward managed print and content services to offset hardware revenue contraction within the inkjet printers market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Printer Type: Industrial Applications Drive Growth

The segment led by large-format printers captured 28.89% of inkjet printers market share in 2024 as architects, engineers, and sign makers maintained demand for oversized outputs. Continuous inkjet lines, however, are forecast to register a 5.71% CAGR to 2030, buoyed by regulatory coding mandates across food, pharmaceutical, and consumer product factories. Industrial buyers prize uptime, solvent resistance, and speed, making CIJ architectures indispensable. Epson’s USD 5.1 billion expansion of PrecisionCore production signals confidence in long-run industrial demand.[4]Epson Corporation, “Investment in Printhead Production,” corporate.epson Meanwhile, multi-function office devices remain staples where consolidation and fleet optimization prevail, though growth is muted by digital substitution.

Shift toward industrial applications reshapes vendor priorities. Investments now target robust heads capable of harsh environments, AI-based self-maintenance, and eco-friendly inks. As factories automate, printers integrate directly with MES and quality systems, turning coding data into a node of real-time analytics. The inkjet printers market thus moves from low-margin desktop hardware toward industrial platforms that command premium service contracts and recurring consumables revenue.

By Technology: Continuous Inkjet Gains Momentum

Thermal drop-on-demand retained 27.53% share of the inkjet printers market size in 2024 through its ubiquity in consumer and small-office models. Yet continuous inkjet technology is projected to expand at a 5.62% CAGR, favored for non-stop coding where even short pauses are costly. Ricoh’s latest liquid-cooled heads deliver 1,200 dpi at high coverage without sacrificing speed, illustrating CIJ’s advances. Piezo drop-on-demand continues to excel in applications demanding variable droplet control and broad ink compatibility, such as ceramics and electronics.

Progress across all architectures is narrowing the historical trade-offs between speed, resolution, and cost. Hybrid designs emerge in commercial presses, blending CIJ’s productivity with thermal or piezo uniformity for specialized stocks. As users standardize on data-rich Industry 4.0 setups, print technology selection increasingly hinges on integration ease and predictive maintenance capability, factors that will differentiate suppliers within the inkjet printers market.

By End-Use Industry: Packaging Segment Accelerates

Home and SOHO users held a dominant 35.17% share in 2024, thanks to enduring hybrid work. Packaging and labels, however, are slated for the fastest 5.56% CAGR because e-commerce requires clear, traceable codes and brand-consistent graphics. EPA mandates covering ink composition and emissions reinforce compliant equipment adoption for packaged consumer goods. Office and enterprise printing face ongoing digitization headwinds, prompting vendors to pivot toward workflow software and cloud monitoring.

In industrial halls, coding and marking printers are tied directly to production throughput, securing budget priority even in downturns. Textiles and apparel ride the customization wave, leveraging direct-to-fabric printers that minimize inventory and waste. This shift toward application-specific devices underscores the inkjet printers industry's emphasis on vertical expertise and managed solutions rather than general office volume.

By Substrate: Textiles Emerge as Growth Driver

Paper and paperboard still ruled with a 58.18% share in 2024, reflecting ongoing needs for documents, signage, and publishing. Textiles are on track for a 5.45% CAGR as fashion brands adopt near-shore digital production for speed and sustainability. Kornit Digital’s waterless process helps apparel firms meet stricter discharge rules while enabling mass personalization. Plastics and films underpin steady packaging demand, whereas ceramics and glass serve decorative and electronics niches requiring specialized inks.

Substrate diversification demands advancements in adhesion, flexibility, and environmental compliance. Vendors that master ink chemistry for emerging materials can capture margin premium. As regulations tighten around water use and micro-pollutants, water-free textile printing technologies will gain share within the inkjet printers market, reinforcing eco-branding for apparel labels.

Geography Analysis

Asia-Pacific led the inkjet printers market with 31.85% share in 2024 and is expected to clock a 5.38% CAGR through 2030. China boosts regional momentum via factory automation and stringent product coding laws, evidenced by Ricoh’s robust printhead sales surge.[5]Ricoh Company, “Fiscal 2024 Results Presentation,” ricoh.com Japan remains a technology stronghold, with Epson ramping up head production capacity to meet worldwide industrial demand. Textile hubs across Southeast Asia accelerate digital adoption to align with global fashion brands seeking faster cycle times.

North America shows mixed trends. Consumer hardware enjoys hybrid work tailwinds, highlighted by HP’s 5% consumer revenue rise, yet commercial office fleets shrink as enterprises adopt digital documents. Manufacturing reshoring and food safety laws stimulate new CIJ installations, while EPA emission caps push printers toward water-based or low-VOC inks. Vendors emphasize cloud analytics and predictive maintenance to help customers cut operating expenses.

Europe sustains moderate growth. Strict sustainability directives fuel uptake of eco-friendly chemistries and energy-efficient presses. Canon detailed strategic investment in industrial inkjet label printers to serve this demand. The region’s textile sector explores on-demand models to curb overproduction, spurring adoption of direct-to-fabric systems. Eastern Europe and Turkey present incremental manufacturing opportunities, while mature Western markets pivot to managed print services and workflow digitization. Emerging regions in the Middle East, Africa, and South America contribute smaller volumes today but offer runway as infrastructure and regulatory clarity improve.

Mordor Intelligence provides coverage of the inkjet printers market across other key regional markets. Detailed country-level analysis extends to India incorporating local coverage and market participation, as required.

Competitive Landscape

Large incumbents such as HP, Canon, and Epson continue to set volume benchmarks. HP’s USD 4.2 billion printing revenue in Q2 2025 underscored breadth, even though the unit declined 4% year over year. Canon reported JPY 2,346.1 billion (USD 16.5 billion) printing sales in 2023, yet warned of intensifying price pressure that requires cost take-outs. Xerox’s USD 6.22 billion top line in 2024, down 9.7%, illustrated challenges for office-centric portfolios.

Specialists seize growth pockets. Kornit Digital’s rebound in digital textile systems highlights demand for waterless, on-demand fashion solutions. Ricoh and Brother invest aggressively in high-volume industrial heads and labeling to diversify away from commoditized A4 devices. Epson’s multibillion yen commitment to printhead fabrication reinforces control of critical components, which offers strategic leverage in performance and supply security.

Strategic moves center on integrated service models, AI-driven monitoring, and sustainable chemistries. Subscription supplies, device-as-a-service contracts, and predictive analytics platforms sharpen customer retention. Alliances and targeted Mergers and Acquisitions aim to secure vertical expertise in textiles, packaging, and graphics. Consolidation is plausible as firms seek economies of scale and broader application coverage within the inkjet printers market.

Inkjet Printers Industry Leaders

HP Inc.

Canon Inc.

Seiko Epson Corporation

Brother Industries Ltd.

Ricoh Company, Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Ricoh debuted its Pro Z75 and VC80000 presses at Hunkeler Innovationdays, introducing B2 duplex aqueous inkjet at 4,500 sheets per hour and 1,200 dpi continuous production.

- January 2025: Heidelberger Druckmaschinen began customer deployments of the Jetfire 50 hybrid inkjet press integrating offset and digital workflow with water-based inks.

- June 2024: Epson announced a JPY 5.1 billion (USD 0.03 billion) investment to quadruple PrecisionCore MicroTFP head capacity by September 2025, adding 70 jobs.

- May 2024: Brother Group unveiled its CS B2027 strategy targeting JPY 1 trillion (USD 0.006 trillion) revenue by FY2027, earmarking 200 billion yen for industrial printing acquisitions.

Global Inkjet Printers Market Report Scope

| Single-Function |

| Multi-Function (AIO) |

| Large-Format |

| Industrial CIJ |

| Inkjet Press |

| Textile Printers |

| Continuous Inkjet (CIJ) |

| Thermal Drop-on-Demand |

| Piezo Drop-on-Demand |

| Home and SOHO |

| Office and Enterprise |

| Industrial Coding and Marking |

| Packaging and Labels |

| Textile and Apparel |

| Commercial and Photo Printing |

| Paper and Paperboard |

| Plastics and Films |

| Textiles |

| Ceramics and Glass |

| Metals and Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Printer Type | Single-Function | ||

| Multi-Function (AIO) | |||

| Large-Format | |||

| Industrial CIJ | |||

| Inkjet Press | |||

| Textile Printers | |||

| By Technology | Continuous Inkjet (CIJ) | ||

| Thermal Drop-on-Demand | |||

| Piezo Drop-on-Demand | |||

| By End-Use Industry | Home and SOHO | ||

| Office and Enterprise | |||

| Industrial Coding and Marking | |||

| Packaging and Labels | |||

| Textile and Apparel | |||

| Commercial and Photo Printing | |||

| By Substrate | Paper and Paperboard | ||

| Plastics and Films | |||

| Textiles | |||

| Ceramics and Glass | |||

| Metals and Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| Indonesia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How big is the inkjet printers market in 2025?

The inkjet printers market is valued at USD 4.10 billion in 2025, with a projected 4.40% CAGR to 2030.

Which segment is growing the fastest within the inkjet printers market?

Industrial continuous inkjet printers are forecast to grow at a 5.71% CAGR, supported by mandatory product coding requirements.

What factors are driving inkjet printer demand in Asia-Pacific?

Manufacturing automation, product traceability laws, and investments in printhead capacity are propelling Asia-Pacific, which already holds 31.85% market share.

How are sustainability trends influencing inkjet technology?

Tight environmental regulations and corporate ESG goals are accelerating adoption of water-based and bio-derived ink chemistries, particularly in Europe and North America.

Why are office printing volumes declining in mature economies?

Rising e-document workflows, electronic signatures, and paperless government initiatives are curbing traditional office print demand, prompting vendors to pivot toward managed services.

Page last updated on: