Thermal Printing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 45.49 Billion |

| Market Size (2031) | USD 56.20 Billion |

| Growth Rate (2026 - 2031) | 4.32% CAGR |

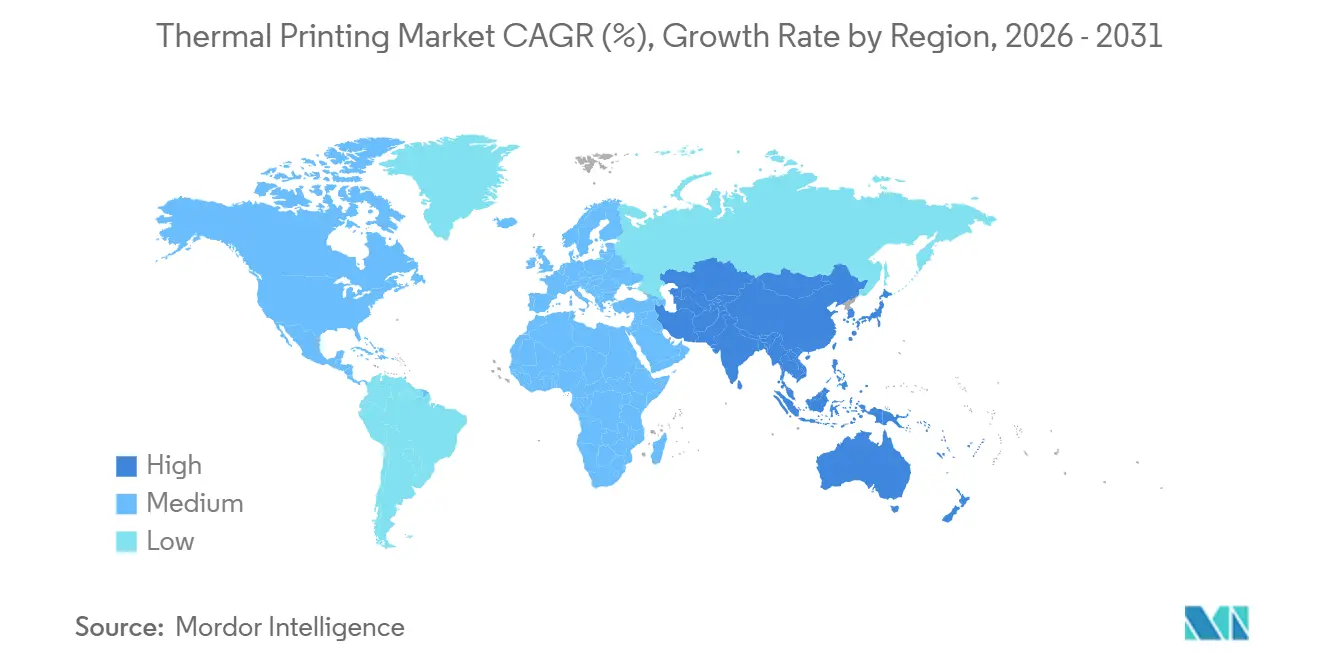

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

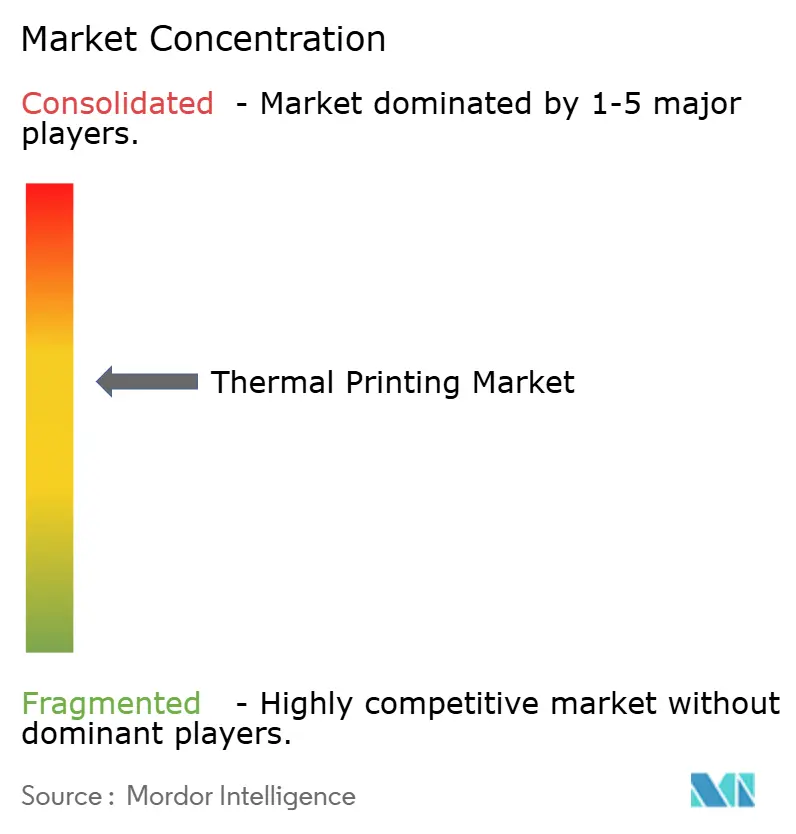

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thermal Printing Market Analysis by Mordor Intelligence

The thermal printing market is valued at USD 45.49 billion in 2026 and is projected to reach USD 56.20 billion by 2031, advancing at a 4.32% CAGR, underscoring steady growth in market size and demand for mobile and linerless solutions. Growth reflects rising parcel volumes, regulatory shifts toward electronic receipts, and sustained advantages in total cost of ownership over inkjet and laser alternatives. Wireless mobile printers continue to penetrate field-service and last-mile workflows, while phenol-free and linerless media are lowering switching costs and inviting new entrants. Investments in predictive maintenance algorithms that curtail unplanned downtime, together with expanding cold-chain logistics for biologics, are opening premium revenue streams. Geographic momentum is rebasing toward Asia Pacific, where fulfillment infrastructure and mobile point-of-sale deployments are scaling more rapidly than replacement cycles in North America and Europe.

Key Report Takeaways

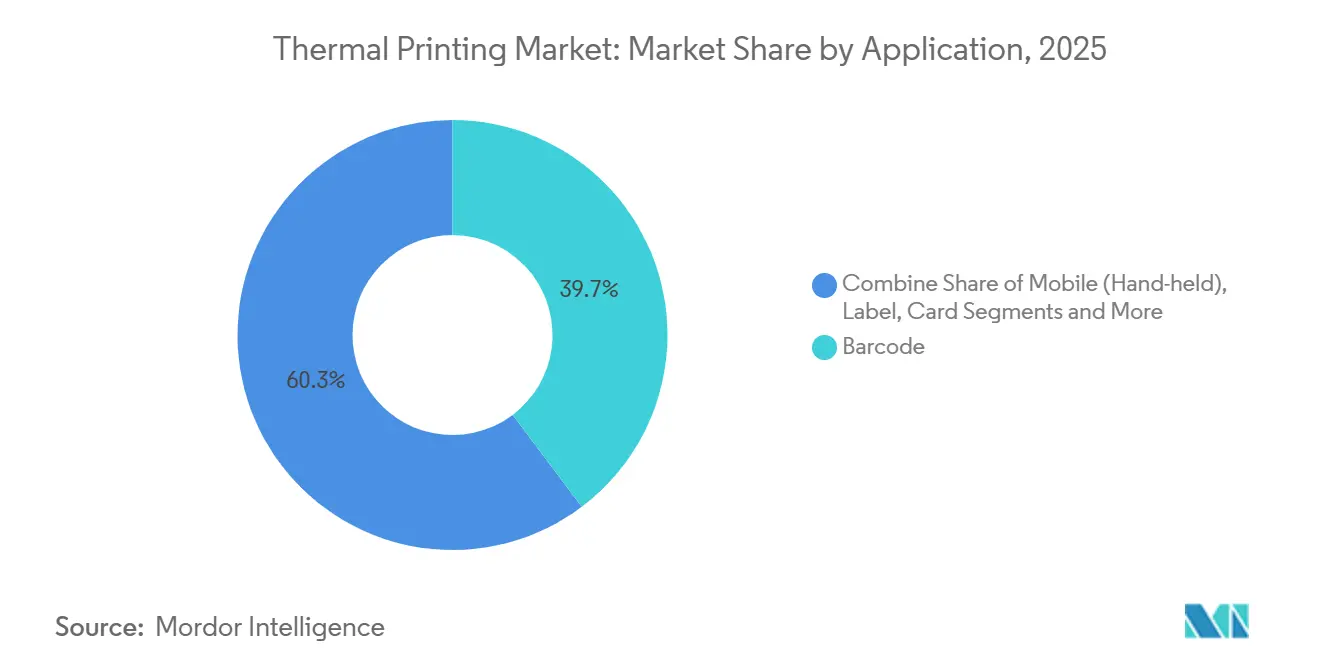

- By application, barcode printing led with a 39.73% revenue share in 2025 in the thermal printing market, while mobile handheld printers are set to record the fastest growth at a 5.06% CAGR through 2031.

- By printing technology, direct thermal held 51.74% of thermal printing market share in 2025, whereas thermal transfer is forecast to expand at a 5.65% CAGR over the same horizon.

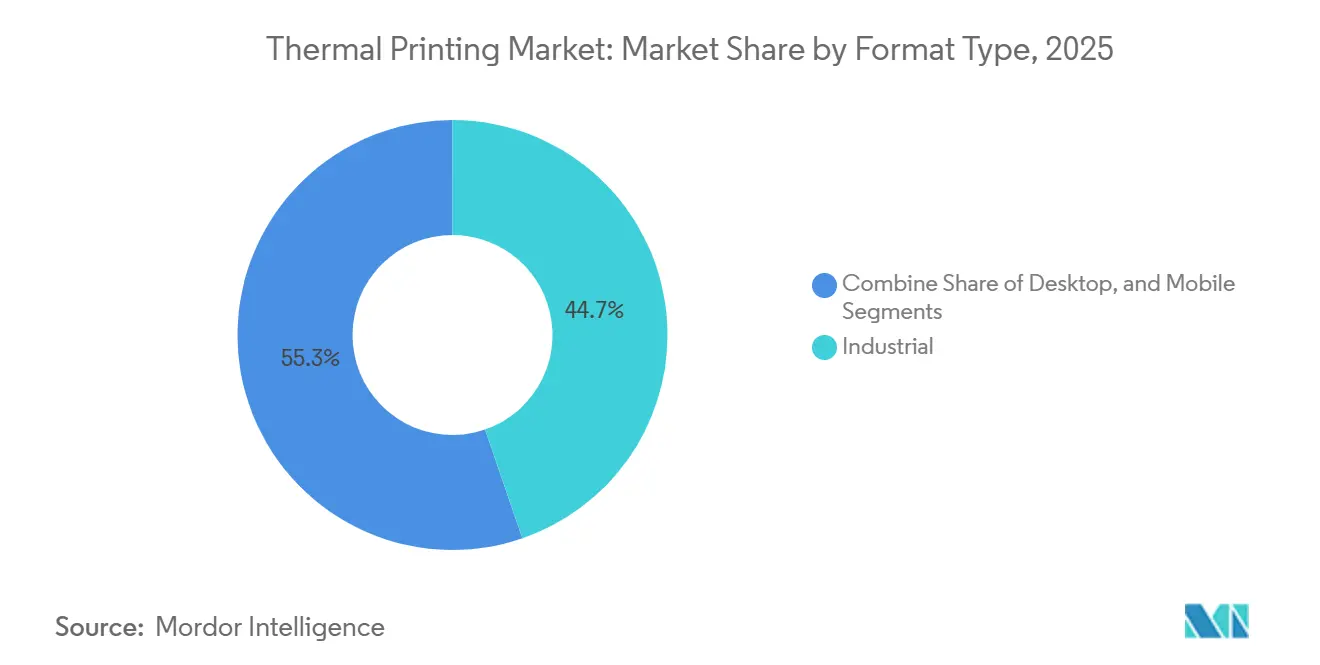

- By format, industrial printers accounted for 44.73% of thermal printing market size in 2025, yet mobile printers are poised to grow at a 5.45% CAGR to 2031.

- By end-use, retail and e-commerce dominated with 52.83% in 2025 in the thermal printing market, while healthcare is projected to rise at a 5.87% CAGR through 2031.

- By region, North America contributed 38.73% to revenue in 2025 in the thermal printing market, whereas Asia Pacific is on track for a 5.62% CAGR, reflecting robust investments in logistics networks.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Thermal Printing Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce logistics boom fuels barcode and shipping-label volumes | +1.2% | Global, with concentration in North America, Europe, and Asia Pacific e-commerce hubs | Medium term (2-4 years) |

| Rapid adoption of wireless/mobile printers in field and last-mile ops | +0.9% | Global, particularly Asia Pacific and North America last-mile delivery networks | Short term (≤ 2 years) |

| Lower TCO versus inkjet/laser for high-volume label and receipt jobs | +0.7% | Global, strongest in Retail and E-commerce, Transportation and Logistics sectors | Long term (≥ 4 years) |

| Surge in cold-chain IoT sensors requiring on-demand frost-resistant labels | +0.6% | North America and Europe pharmaceutical cold-chain corridors, expanding to Asia Pacific | Medium term (2-4 years) |

| Rise of phenol-free, liner-less media to meet ESG scorecards | +0.5% | Europe and North America, driven by corporate sustainability mandates | Medium term (2-4 years) |

| Embedded AI diagnostics reducing print-head downtime in 24/7 fulfilment hubs | +0.4% | North America and Europe large-scale fulfillment centers, early adoption in Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-Commerce Logistics Boom Fuels Barcode and Shipping-Label Volumes

Parcel growth tied to cross-border digital commerce is directly lifting thermal label consumption. Express carriers enforce GS1-compliant formats that must be printed on demand, prompting small merchants to adopt desktop direct thermal units that bring per-label costs below USD 0.01.[1]UPS, “GS1 Barcode Compliance Requirements for Automated Sortation,” ups.com Omnichannel fulfillment strategies decentralize printing across micro-warehouses, multiplying consumables revenue for original-equipment manufacturers by having every node regularly replenish media and printheads. Manufacturers respond with Ethernet- and Wi-Fi-enabled printers that can be centrally queued, ensuring real-time label flow at each dock door. The compounding effect of rising parcel counts and distributed printing nodes positions shipping labels as a durable volume anchor for the thermal printing market.

Rapid Adoption of Wireless/Mobile Printers in Field and Last-Mile Operations

Bluetooth Low Energy and Wi-Fi Direct protocols have removed the need for fixed access points, making mobile printers indispensable for delivery agents, nurses, and service technicians. Brother’s RJ2150 RuggedJet 2 prints 1,100 two-inch labels per charge and meets IP54 and MIL-STD-810G durability standards.[2]Brother Industries Ltd., “RJ2150 RuggedJet 2 Mobile Printer Specifications,” brother-usa.com BIXOLON extends portability to healthcare with wipe-disinfectant certification, allowing bedside wristband printing that cuts transcription errors.[3]BIXOLON Co., “XD5-40IId Healthcare Mobile Printer,” bixolon.com Cloud label design apps let users modify templates on smartphones, reducing IT bottlenecks and shortening deployment cycles. As fleets grow, OEMs secure new annuity streams in batteries, chargers, and durable media optimized for mobile environments, deepening overall thermal printing market penetration.

Lower Total Cost of Ownership Versus Inkjet/Laser for High-Volume Jobs

Direct-thermal printers eliminate toner, fusers, and developers, bringing total print costs down to roughly USD 0.005 per 4 x 6-inch label compared with USD 0.03 for similar inkjet output. Industrial thermal-transfer models add a ribbon yet remain cheaper over five years due to lower energy draw and fewer consumables than laser peers. Honeywell’s PM45 allows on-site printhead swaps in under 10 minutes, preventing downtime losses that can exceed USD 5,000 per hour in automated fulfillment centers. The simplicity of the technology demands little operator training, a critical edge as warehouse labor costs climb. These economics reinforce the appeal of the thermal printing market to organizations processing tens of thousands of labels each shift.

Surge in Cold-Chain IoT Sensors Requiring On-Demand Frost-Resistant Labels

Biologic drugs and vaccines travel within tight temperature bands, and each parcel now embeds IoT sensors that transmit telemetry. TOPPAN’s temperature-logger label combines an integrated battery and sensor, requiring unique serialization at the final distribution node. Sensos offers a cellular smart label relaying GPS and temperature data every 15 minutes, necessitating just-in-time encoding of shipment parameters. Compliance regimes such as the European Good Distribution Practice rule mandate traceability for every item, driving adoption of industrial thermal-transfer units that incorporate RFID modules. Cold-chain requirements, though a smaller slice of current demand, command premium pricing and lift the average selling price within the overall thermal printing market.

Restraints Impact Analysis of Thermal Printing Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High maintenance and print-head replacement costs | -0.8% | Global, particularly acute in Industrial format segment with 24/7 operations | Short term (≤ 2 years) |

| RFID tags and e-receipts displacing some thermal applications | -0.6% | Europe and North America retail, expanding to Asia Pacific urban centers | Medium term (2-4 years) |

| Phenol/BPA regulations inflating specialty-paper input costs | -0.4% | Europe and North America, driven by REACH and FDA compliance requirements | Long term (≥ 4 years) |

| Pulp-price volatility disrupting global label-stock supply | -0.3% | Global, with acute impact in regions dependent on imported paper stocks | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Maintenance and Print-Head Replacement Costs

Industrial printheads cost USD 400-1,200 and last 30-60 kilometers of media. Fulfillment centers running 50,000 labels daily face replacements every six to twelve months, sometimes exceeding the printer’s purchase price. Proprietary interfaces prevent interchangeability, keeping prices high and locking buyers into single-vendor ecosystems. Canon’s predictive lifespan model shows accelerated degradation under high-duty-cycle conditions, making accurate failure timing difficult to predict. While preventive swaps curb downtime, they inflate operating budgets, creating resistance among smaller enterprises and tempering the expansion of the thermal printing market.

RFID Tags and E-Receipts Displacing Some Thermal Applications

Retailers deploying item-level RFID realize inventory accuracy gains without scanning barcodes, reducing the need for printed labels on individual items. Zara and H&M mandate RFID tagging, diminishing barcode volumes in apparel outlets. Simultaneously, European regulations require merchants to issue digital receipts, and surveys show overwhelming consumer support, curbing the use of point-of-sale paper rolls. Printed labels remain necessary for logistics and regulated products, yet displacement trends shave volume growth and require vendors to innovate in durable and intelligent media to safeguard the thermal printing market’s relevance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Thermal Printing Market Segment Analysis

By Application:

Barcode Usage Anchors Logistics WorkflowsBarcode printing commanded 39.73% of 2025 revenue, demonstrating how standardized identifiers underpin fulfillment and inventory operations across commerce and manufacturing. Mobile handheld units add flexibility, expanding at a 5.06% CAGR as drivers and technicians print labels at the point of task, reducing errors and speeding workflows. Point-of-sale and receipt applications remain sizable, but digital receipt mandates in France and Germany are moderating growth. Card printing, dominated by dye-diffusion thermal transfer, supports secure identity issuance for governments and enterprises, while kiosk and ticket printing address transportation and entertainment needs. RFID label printing merges thermal imaging with inlay encoding to satisfy omnichannel tracking requirements, and the diversity of use cases helps stabilize overall demand in the thermal printing market.

Direct thermal simplicity is particularly suited to shipping labels, where images need only remain legible throughout the parcel lifecycle. Thermal transfer dominates asset tagging and outdoor labels that must withstand chemical or ultraviolet exposure. Hybrid applications such as RFID require both printed and encoded data, reinforcing the technology’s centrality in supply-chain visibility. As cold-chain routing, smart-label adoption, and sustainability certifications converge, application-specific media formulations are proliferating, limiting commoditization and sustaining margin dispersion in the thermal printing market.

By Printing Technology:

Simplicity Versus Durability Shapes AdoptionDirect thermal held 51.74% share in 2025, favored for receipt and short-lifecycle labels that benefit from ribbon-free economics. Thermal transfer is growing faster, at a 5.65% CAGR, as manufacturers require labels that remain intact for years in harsh environments, driving incremental growth in the thermal printing market in industrial sectors. Dye-diffusion thermal transfer, though niche, secures high-resolution photo ID and payment card applications, with Evolis’ 600 dpi retransfer technology enhancing edge-to-edge image quality.

Technology choice often hinges on lifecycle costs. Direct thermal strips out ribbon spend and lowers maintenance, but suffers image fade under heat or light after several months, limiting use outdoors or in long-term archives. Thermal transfer uses consumable ribbons yet yields prints that remain readable for up to a decade, providing compliance assurance in chemical, electronics, and automotive settings. Toshiba TEC’s dual-mode devices allow users to switch between methods, optimizing expense and durability in mixed-duty environments. Environmental mandates encouraging linerless and phenol-free media further influence technology selection, encouraging continual innovation across the thermal printing market.

By Format Type:

Industrial Throughput Meets Mobile FlexibilityIndustrial models generated 44.73% revenue in 2025, prized for fast print speeds, metal chassis durability, and high-capacity media that support three-shift operations. Mobile units, however, are scaling fastest, growing 5.45% per year as e-commerce drivers and warehouse pickers demand lightweight, battery-powered tools. Desktop printers bridge retail counters and small fulfillment cells with plug-and-play USB setups under USD 500, ensuring they remain the volume leader in unit terms. SATO’s 600-meter ribbon capacity enables unattended overnight industrial runs.

Presence of mixed fleets is typical, with organizations selecting form factors based on task criticality rather than standardizing on a single category. Brother’s RuggedJet lines demonstrate how shock resistance and sealed housings enable them to withstand construction sites or cold storage, while Star Micronics’ linerless desktop units reduce waste in quick-service restaurants. Such specialization secures niches for new entrants and sustains competitive diversity inside the thermal printing market.

By End-Use Industry:

Healthcare and Logistics Drive Specialized DemandRetail and e-commerce remained the anchor with 52.83% of 2025 revenue, thanks to receipts, shelf labels, and shipping documentation. Healthcare is forecast to grow at 5.87% through 2031 as hospitals implement barcoded patient wristbands and laboratories expand specimen tracking. Transportation operators rely on thermal waybills and pallet tags, while manufacturing lines integrate printers within conveyor systems to label work-in-process. Governments issue secure credentials on dye-sublimation card printers such as HID FARGO’s HDP6600 for motor-vehicle departments.

Diversified demand insulates suppliers from downturns in any single vertical. When hospitality receipts soften, logistics labels often rise. Nevertheless, each sector’s unique compliance and media needs impede cross-segment standardization, preserving specialized product lines and sustaining growth lanes for the thermal printing industry even as individual verticals fluctuate.

Geography Analysis

North America Thermal Printing Market

North America accounted for 38.73% of 2025 revenue, supported by mature logistics infrastructure, mandatory GS1 standards, and government contracts such as the United States Postal Service’s rollout of mobile printers for rural carriers. Canadian retailers are adopting linerless solutions to comply with plastics regulations, and Mexican near-shoring is spurring the installation of industrial printers in new warehouses. RFID uptake and digital receipts temper point-of-sale roll consumption, keeping North American growth muted but steady, thereby safeguarding regional revenue for the thermal printing market.

APAC Thermal Printing Market

Asia-Pacific is the fastest-growing territory, projected to grow at a 5.62% CAGR through 2031, driven by surging parcel volumes in China, India’s tax-driven digitization of receipts, and the rise of cross-border e-commerce in Southeast Asia. China processed 132 billion parcels in 2024, cementing thermal labels as a logistics staple. India’s pharmaceutical and automotive sectors are targets for SATO’s multilingual WT4-AXB industrial printer, underlining demand for regionally tailored firmware. Regional growth rests on ongoing investments in warehousing automation and mobile point-of-sale adoption across emerging metropolitan areas, boosting overall thermal printing market size.

EMEA and South America Thermal Printing Market

Europe occupies a balanced middle position, with sustainability mandates driving phenol-free and linerless adoption while digital-receipt requirements stifle some retail volumes. France’s electronic receipt law and Germany’s extended producer responsibility for label liners illustrate divergent regulatory pressures. Brexit-related customs paperwork keeps United Kingdom label usage elevated, and Southern Europe’s expanding biologics cold chain sustains demand for frost-resistant media. Meanwhile, the Middle East and Africa are channeling smart-city logistics investments into thermal infrastructure, and South America’s demand is concentrated in Brazil’s retail sectors, highlighting that future volumes depend heavily on macroeconomic stability and infrastructure expansion.

Regulatory Landscape

Thermal printing demand in packaging and labeling is shaped by packaging-waste and traceability rules that define what must be printed, how durable it must be, and how it must be read in automated supply chains. In the EU, the Packaging and Packaging Waste Regulation, Regulation (EU) 2025/40, tightens requirements around harmonized packaging labeling, recyclability, and waste reduction, pushing brands and converters toward media choices such as linerless formats and compliant coatings. In 2026, the European Commission also issued related interpretive or guidance communication to support implementation.

Food and pharma labeling rules reinforce machine-readable coding and material-safety compliance. In the US, the FDA FSMA 204 Food Traceability Rule sets a compliance deadline (July 2028) for traceability data capture, increasing the importance of clear, durable, scannable barcodes and 2D codes at the case and unit level in relevant categories. In Asia, India continues to update and consolidate packaging compliance via FSSAI packaging compendiums that address migration and safety for food-contact packaging, while China has updated GB 7718-2025 for prepackaged food labeling, with implementation scheduled from 2027. This raises the bar for accurate, legible variable-information printing across high-volume consumer packaging streams.

Value Chain Analysis

The thermal printing value chain spans specialized components, consumables, and OEM integration. Upstream inputs include semiconductors and electronics for controller boards, ceramic substrates and thin-film resistor arrays for thermal printheads, and specialty chemicals and coatings plus paper and film for direct-thermal media and thermal-transfer ribbons. Thermal printheads are a critical choke point because manufacturing is concentrated among specialized suppliers (for example, ROHM Semiconductor and Gulton) with tight tolerances and proprietary coatings, making qualification cycles and supply continuity central to OEM delivery performance.

Midstream players include consumable manufacturers (for example, DNP for thermal-transfer ribbons and UPM Raflatac for label materials) alongside label converters that supply application-specific formats (shipping labels, cold-chain labels, linerless receipts). Printer OEMs assemble hardware, firmware, and printhead modules, and they depend on global distributors, VARs, and systems integrators to deploy fleets into retail, logistics, healthcare, and manufacturing workflows. Enterprise software connectors and device-management layers increasingly sit alongside the physical channel. Downstream, end users drive recurring spend through replenishment of media, ribbons, batteries (for mobile units), and service contracts, while supply risks concentrate around printhead availability, semiconductor lead times for electronics, and pulp or paper price volatility for coated stocks. As a result, many mission-critical sites such as 24/7 fulfillment hubs emphasize dual-sourcing and higher safety inventories.

Competitive Landscape

Four multinationals, Zebra Technologies, SATO Holdings, Toshiba TEC, and Honeywell, collectively capture most of the global revenue, relying on proprietary consumables and long-term service contracts to entrench customers. Zebra’s USD 1.3 billion acquisition of Elo in January 2025 expanded its reach into interactive retail displays that integrate thermal printers as peripherals, signaling a broader ecosystem strategy. Star Micronics and Brother challenge incumbents through phenol-free and linerless innovations that lower consumable costs and ease environmental compliance, eroding legacy lock-in.

Asian challengers, notably TSC, Bixolon, and Xprinter, exploit local manufacturing cost advantages to win tenders in price-driven markets, especially among small logistics firms spinning up fulfilment nodes nationwide. To defend margins, incumbents emphasize total cost of ownership, highlighting head durability, energy savings, and superior remote service infrastructure. Sustainability has emerged as an important differentiator, such as SATO’s refreshed CL4NX Plus packaging slices CO₂ emissions by 39% across the box lifecycle, an advantage during bids with ESG scoring components.

Software ecosystems increasingly dictate hardware choice. Cloud APIs that expose printer status, job queues, and security logs let DevOps teams fold labelling into CI/CD-style architectures. Vendors bundle low-code connectors to SAP, Oracle, and Microsoft Dynamics, easing deployment friction. As asset visibility platforms pivot to edge AI, partnerships between printer OEMs and machine-vision firms bring label validation cameras under a single pane of glass. Meanwhile, IP litigation around printhead coatings and energy-efficient dot heaters intensifies as companies race to extend duty cycles. Overall, the competitive theatre balances innovation, cost pressure, and sustainability, ensuring the thermal printing market continues evolving rather than ossifying.

Thermal Printing Industry Leaders

Zebra Technologies Corporation

Sato Holdings Corporation

Honeywell International Inc.

Brother International Corporation

BIXOLON Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Thermal Printing Market Companies Covered in this Report

- Zebra Technologies Corporation

- SATO Holdings Corporation

- Toshiba TEC Corporation

- Honeywell International Inc.

- Brother Industries Ltd.

- Star Micronics Co., Ltd.

- Seiko Instruments Inc.

- Citizen Systems Japan Co., Ltd.

- Fujitsu Frontech Ltd.

- Seiko Epson Corporation

- BIXOLON Co., Ltd.

- TSC Auto ID Technology Co., Ltd.

- Printronix Auto ID Inc.

- Avery Dennison Corporation

- Evolis SA

- Axiohm SAS

- CognitiveTPG LLC

- Dymo – Newell Brands Inc.

- Posiflex Technology Inc.

- Xiamen Rongta Technology Co., Ltd.

- Brady Corporation

- cab Produkttechnik GmbH and Co KG

- GoDEX International Co., Ltd.

- Dascom Holdings Ltd.

Market Opportunities and Future Outlook

Opportunity is opening around consumables and media innovation where regulation, sustainability scorecards, and operational constraints intersect. Linerless and phenol-free media adoption creates whitespace for OEMs and material suppliers that can deliver reliable print performance with lower waste and compliant chemistries, particularly in Europe and North America where packaging-waste rules and chemical restrictions are most influential. Cold-chain and regulated traceability workflows also expand premium lanes for thermal transfer printing with durable labels and consistent barcode and 2D readability, aligning with mandates such as the US FDA FSMA 204 Food Traceability Rule (compliance deadline July 2028), which increases emphasis on scannable codes through complex distribution.

Supply-side investments in 2026 show where capacity and product development are concentrating. In May 2026, ARMOR-IIMAK announced an investment of nearly USD 6 million to expand its Boone County, Kentucky operation to raise thermal transfer ribbon capacity, signaling renewed focus on regional production and shorter lead times for industrial identification consumables. On the specialty paper side, China added thermal base paper capability in May 2026 with a new high-speed MG specialty paper machine at APPs Jindong Dagang mill in Zhenjiang (reported at 120,000 tons per year), while Lecta expanded its Termax thermal paper range in May 2026. Together, these moves support a market shift toward differentiated, application-specific media (durability, coat weights, and sustainability attributes) rather than commodity receipt paper alone, and they heighten competitive pressure between vertically integrated consumables players and OEM ecosystems built around proprietary supplies and device-management software.

Recent Industry Developments in Thermal Printing Market

- June 2026: Zebra Technologies introduced new software platforms for frontline operations, including Zebra Nucleus for ecosystem oversight and Workcloud IO and Workcloud BI to support AI-assisted workflow automation. The move reinforces the shift of thermal printing deployments toward managed device fleets where software, data, and security controls influence hardware selection across retail and logistics environments.

- April 2026: Honeywell agreed to sell its Productivity Solutions and Services business to Brady Corporation for USD 1.4 billion, a portfolio that includes identification and printing solutions used in warehouse and industrial labeling workflows. The transaction concentrates more auto-ID and printing capabilities under a specialist identification supplier, reshaping competitive dynamics and channel coverage for thermal printing solutions.

- May 2025: Star Micronics launched the TSP143IV SK linerless receipt printer, positioning linerless media as a practical route to reduce consumable waste in point-of-sale and hospitality printing. This product direction supports broader adoption of linerless formats where sustainability requirements and cost-to-serve pressures are driving changes in receipt and label workflows.

Thermal Printing Market Report Scope and Research Methodology

Market Definition and Coverage

For this methodology, the thermal printing market is defined as the revenue generated from thermal printing hardware and closely linked consumables that enable barcode, POS, ticketing, and labeling outputs across commercial and industrial workflows.

Scope exclusions: We exclude finished labels produced by converters and any refurbished or second-hand printer resale value.

Segments Covered in This Report

- By Application

- Barcode

- POS / Receipt

- Label

- Card

- RFID

- Kiosk and Ticket

- Mobile (Hand-held)

- By Printing Technology

- Direct Thermal (DT)

- Thermal Transfer (TT)

- Dye Diffusion Thermal Transfer (D2T2)

- By Format Type

- Industrial

- Desktop

- Mobile

- By End-Use Industry

- Retail and E-commerce

- Transportation and Logistics

- Manufacturing and Warehouse

- Healthcare and Pharma

- Government and Public Safety

- Hospitality and Entertainment

- Banking and Financial Services

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map the demand pool, set realistic adoption boundaries, and keep the sizing logic tied to observable signals. We referred to public sources such as US Census Bureau manufacturing and trade releases, USITC DataWeb for import and export trends on printers and related parts, OECD and World Bank macro indicators, and WTO trade statistics to cross-check regional shipment direction.

To keep the model practical, we also used company annual reports, investor presentations, product specification sheets, and reputable press coverage to understand typical pricing ladders, replacement cycles, and where direct thermal versus thermal transfer is chosen. Patent databases were reviewed in a light way to confirm the pace of feature improvements like connectivity, durability, and printhead life, which can shift average selling prices over time. For gaps in private company visibility, we relied on paid subscriptions that provide company financials and intelligence, plus a shipment-level import and export database to validate trade-linked volumes. These desk sources are not exhaustive, and many other public references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with printer OEM channel teams, component and media participants, distributors, system integrators, and large end users across retail, logistics, healthcare, and manufacturing. Because this is a global market, inputs were balanced across APAC, EMEA, and the Americas so adoption assumptions, pricing steps, and replacement timing could be confirmed in more than one region.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 17% | APAC: 40% |

| Mid tier: 41% | Functional/Unit leaders: 41% | EMEA: 33% |

| Smaller Players: 22% | Managers: 42% | Americas: 27% |

Market-Sizing & Forecasting

Market sizing starts with a top-down build where production and trade data, along with installed-base refresh patterns, are used to reconstruct the annual demand for thermal printers and related consumables in revenue terms. Once the demand pool is formed, it is split by likely usage intensity and technology mix so the price and volume math stays realistic by region.

Key inputs in the model include: thermal printer shipments indicated by trade codes and manufacturing output signals, average selling prices by printer format (desktop, mobile, industrial) and by use case, the share of direct thermal versus thermal transfer in high-throughput labeling, replacement cycles linked to duty cycle and printhead wear, and the expansion rate of logistics and e-commerce parcel handling that drives label and receipt volumes. Where direct public data is thin, we run sampled bottom-up checks using channel feedback on unit volumes and typical price bands, which helps adjust totals without assuming full visibility.

For forecasting, we rely on scenario analysis supported by multivariate regression checks, where growth is tied to drivers such as industrial production, retail and logistics activity, and trade momentum for printing hardware. Assumptions on ASP movement are updated using inputs on component cost direction and feature-driven mix shifts, then validated again through follow-up calls when an outlier appears.

Data Validation & Update Cycle

Validation is done through several passes so the final numbers align with real-world signals. We compare model outputs against independent indicators such as trade trends, macro activity proxies for key end users, and observed price bands from the market. Any variance that looks too large to be explained by mix or region is investigated.

Before sign-off, the work goes through an internal analyst review where assumptions, currency conversions, and year labels are checked for consistency. If a major mismatch appears, respondents are re-contacted to confirm whether it is driven by a one-time event, a pricing reset, or a change in supply availability. Reports are refreshed annually, and interim updates are made when material events occur, followed by a final pre-delivery refresh so clients receive the latest view.

Mordor Intelligence's Thermal Printing Market Size Versus Other Published Estimates

Published market sizes for thermal printing can differ even when they look like they measure the same scope, because the update cycle and the currency timing behind price and volume assumptions are not always aligned. Differences also come from what gets counted as thermal printing revenue, particularly when supplies and adjacent outputs are treated inconsistently.

In our checks, the spread usually comes from how fast average selling prices are refreshed after component cost changes, how printer versus supplies revenue is separated, and whether the model is revalidated against trade and shipment signals after the latest year closes. The table below illustrates this range, and the gap is mainly explained by refresh cadence and when FX rates are applied to regional revenues, which is handled differently in the validation steps used by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 45.49 B (2026) | |

| Global Consultancy A | USD 53.75 B (2026) | Uses a higher 2026 level by applying a broader offering split and faster ASP uplift assumptions, and the public summary does not clearly show trade or shipment cross-checks after currency conversion. |

| Industry Publisher B | USD 48.10 B (2025) | Runs on a different base year and a longer horizon, and the published view does not clarify how printer formats and supplies are priced over time or how regional FX timing is standardized across the model. |

Overall, the comparison points to timing and scope choices as the main reasons numbers move apart, rather than a single math issue. When pricing steps, FX timing, and unit-demand signals are refreshed in a consistent way, the resulting market size is easier to trace back to clear drivers and repeatable checks.

Key Questions Answered in the Report

What is the projected value of the thermal printing market by 2031?

The market is expected to reach USD 56.20 billion by 2031, expanding at a 4.32% CAGR.

Which segment is growing fastest within thermal printing applications?

Mobile handheld printing is rising at a 5.06% CAGR through 2031 on the back of field-service and last-mile delivery demand.

Why do many logistics firms choose thermal over inkjet or laser printing?

Thermal printers deliver lower total cost of ownership, with per-label costs near USD 0.005 and fewer mechanical failures, making them ideal for high-volume shipping environments.

How are sustainability trends affecting thermal printing adoption?

Phenol-free and linerless media, together with regulations on single-use plastics and chemical restrictions, are spurring upgrades to environmentally friendly printers and consumables.

Which region is forecast to contribute most to incremental market growth?

Asia Pacific leads growth, with a 5.62% CAGR driven by expanding e-commerce logistics and mobile point-of-sale deployments.

Page last updated on: