Textile Printers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

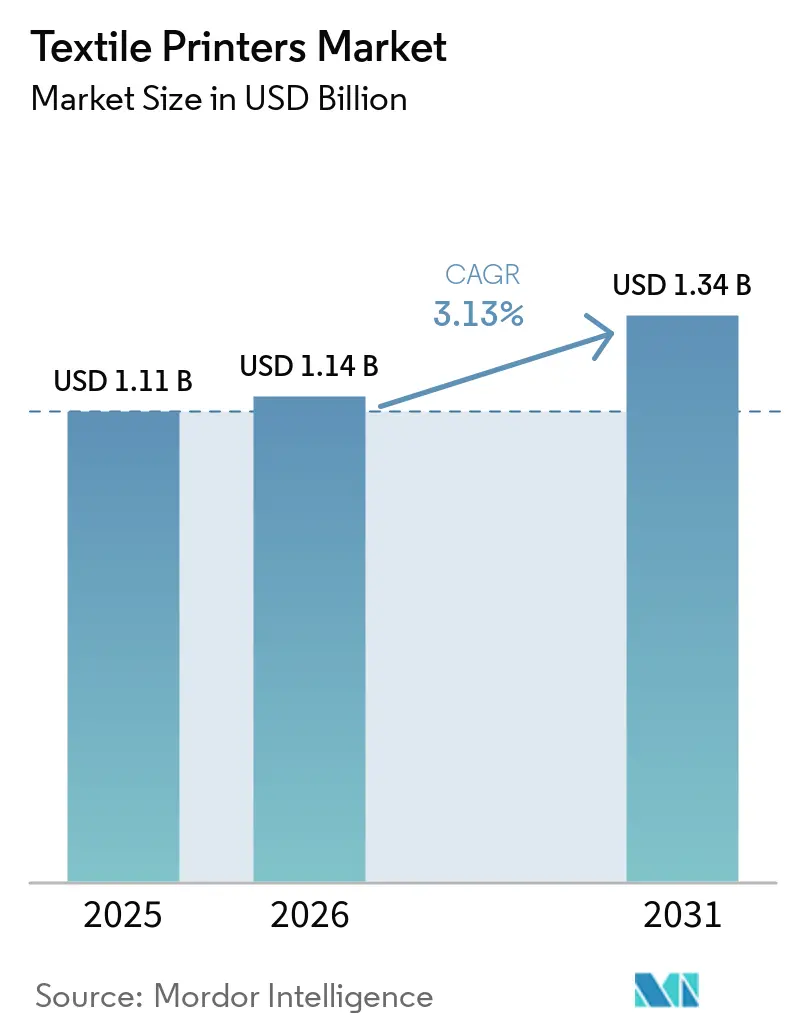

| Market Size (2026) | USD 1.14 Billion |

| Market Size (2031) | USD 1.34 Billion |

| Growth Rate (2026 - 2031) | 3.13% CAGR |

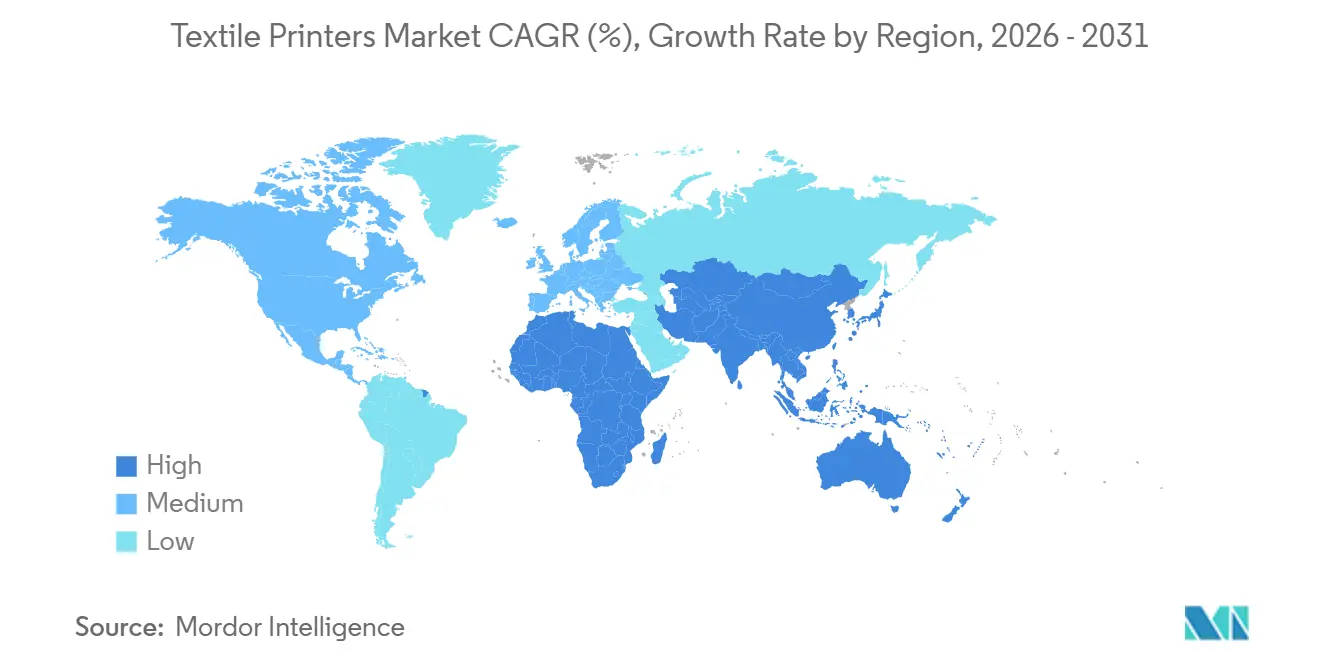

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

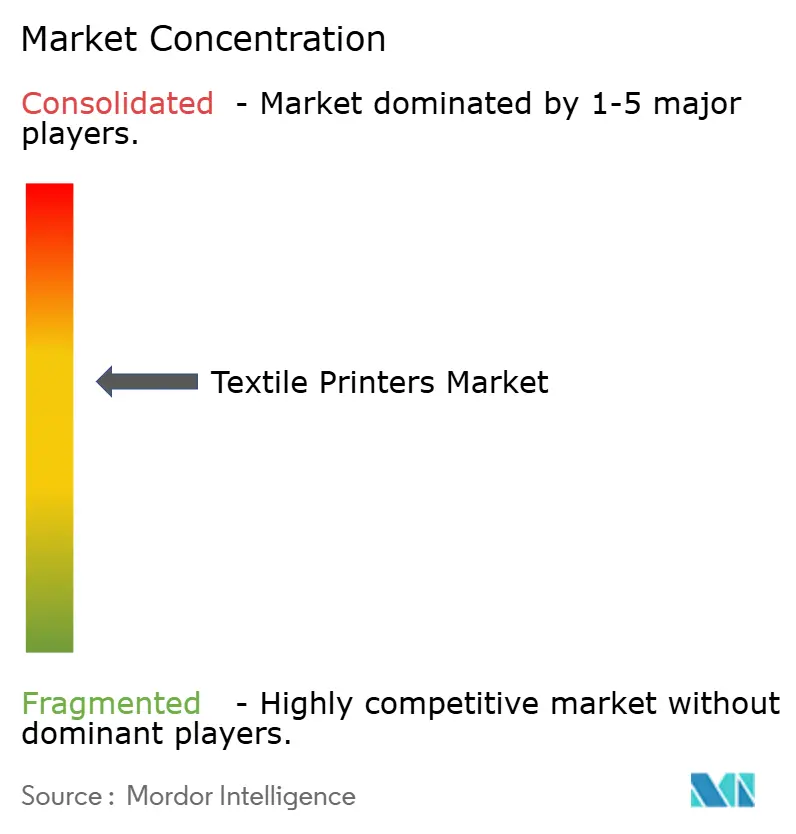

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Textile Printers Market Analysis by Mordor Intelligence

The textile printers market size was valued at USD 1.11 billion in 2025 and was estimated to grow from USD 1.14 billion in 2026 to reach USD 1.34 billion by 2031, at a CAGR of 3.13% during the forecast period (2026-2031). Rapid migration from analog screens to digital inkjet architectures, the commercial rollout of waterless pigment chemistries that comply with Zero Discharge of Hazardous Chemicals (ZDHC) protocols, and AI-orchestrated production workflows that shorten order cycles from weeks to days are reshaping competitive dynamics. In 2025, digital inkjet platforms accounted for a major share of revenue, with single-pass systems now matching the throughput of mid-range rotary screens, while pigment inks reopened growth pathways by closing historic fastness gaps with reactive dyes. Brands are also repurposing textile printers for soft signage and event backdrops, enabling quick promotional refreshes without PVC banners. Geography remains a two-speed story; Asia-Pacific accounts for the largest installed base, but Africa records the fastest growth as multilateral programs direct capital to greenfield mills.

Key Report Takeaways

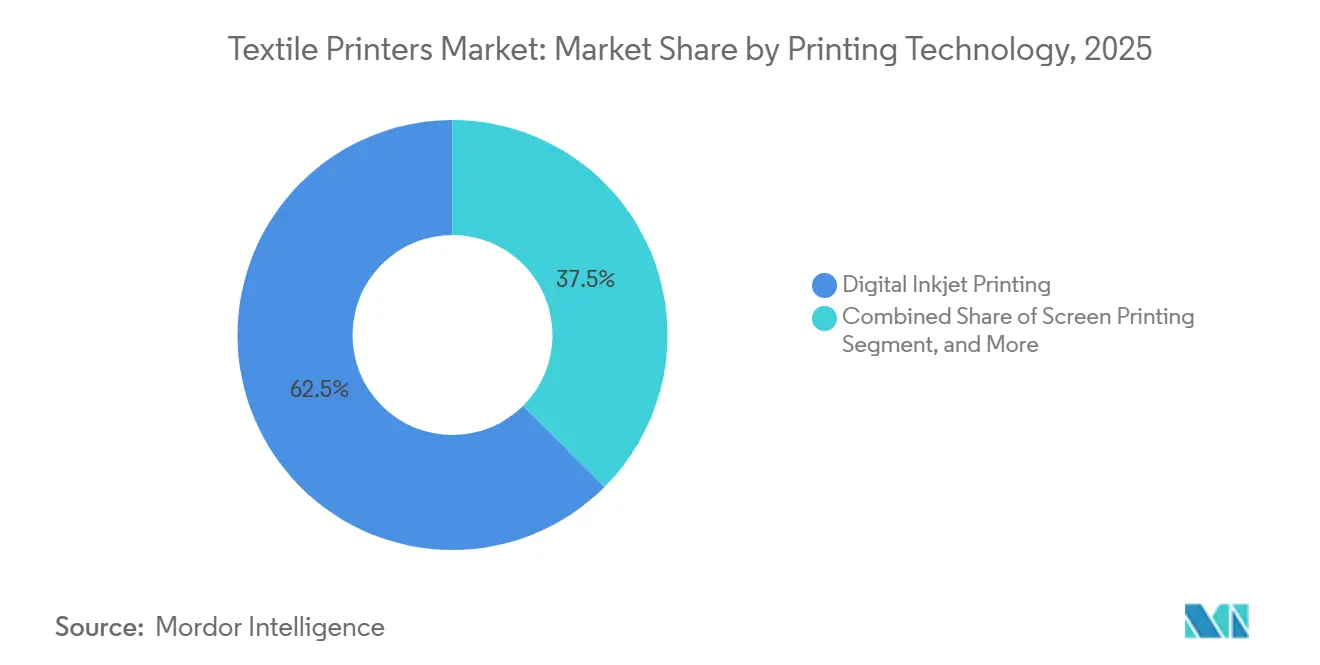

- In terms of printing technology, digital inkjet platforms led the textile printers market with a 62.51% share in 2025 and are projected to grow at a 3.45% CAGR through 2031.

- By ink type, disperse and sublimation inks accounted for 41.08% of the market in 2025, while pigment formulations are the fastest-growing category, expanding at a 4.22% CAGR between 2026 and 2031, as polymer encapsulation addresses wash-fastness and abrasion constraints.

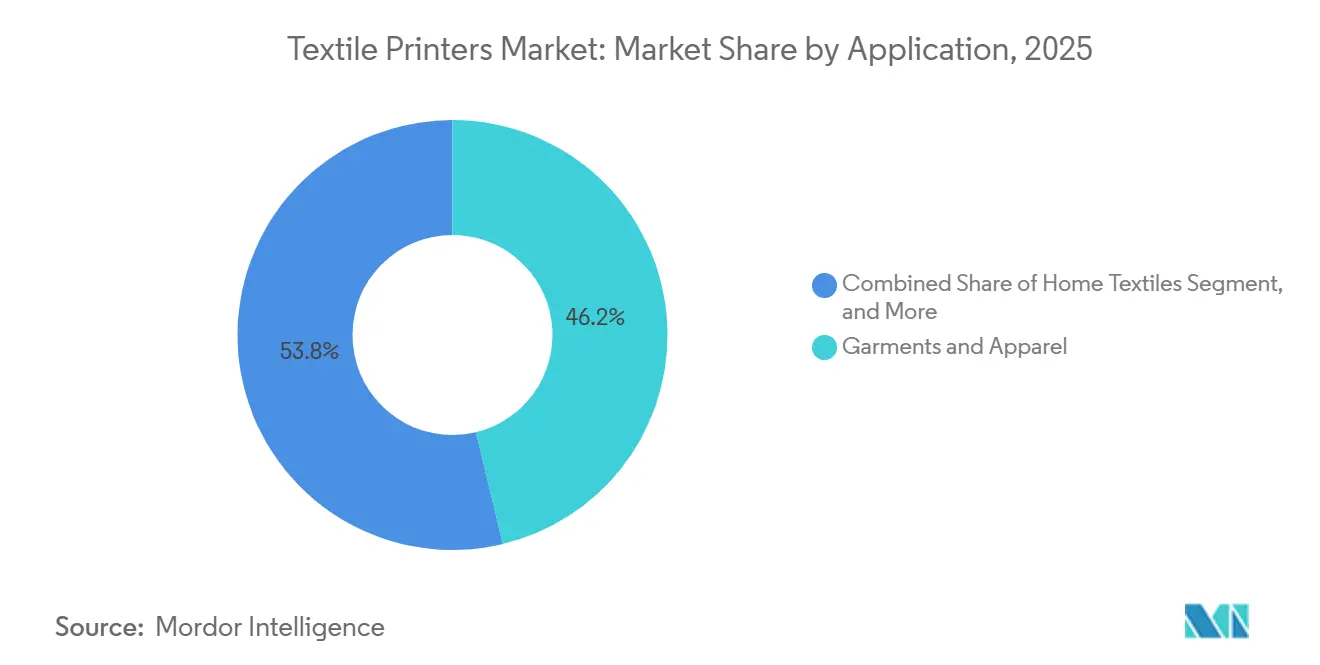

- By application, garments and apparel led the market with a 46.24% share in 2025, while signage and display graphics outpaced traditional garment printing with a 4.05% CAGR forecast to 2031, reflecting retailers’ shift toward short-run promotional fabrics.

- By fabric, cotton accounted for 48.15% of the textile printers market in 2025, while polyester recorded a 3.67% CAGR through 2031, driven by low-temperature sublimation dyes that protect elastane blends.

- By geography, Asia-Pacific captured 39.34% share of the textile printers market in 2025, yet Africa is expected to record the highest regional CAGR at 3.91% through 2031 under the WTO Cotton Initiative.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Textile Printers Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Fast Fashion and Customized Apparel | +0.9% | Global, weighted to North America, Europe, and Asia-Pacific cities | Short term (≤ 2 years) |

| Shift From Analog to Digital Printing in Textiles | +0.8% | Asia-Pacific and Europe lead, spillover to South America and the Middle East | Medium term (2-4 years) |

| Advancements in High-Speed Inkjet Heads and Sublimation Inks | +0.6% | Asia-Pacific core, North America, Europe | Medium term (2-4 years) |

| Expanding E-Commerce and Web-to-Print Platforms | +0.5% | North America and Europe are strong, Asia-Pacific is rising | Short term (≤ 2 years) |

| Adoption of Waterless Pigment Ink Printers to Meet ZDHC | +0.4% | Europe and North America lead, Asia-Pacific accelerating | Long term (≥ 4 years) |

| Integration of AI-Based Print Workflow Automation | +0.3% | North America, Europe, select Asia-Pacific mills | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Fast Fashion and Customized Apparel

Weekly micro-drops now replace seasonal collections, pushing converters toward low-minimum orders that analog screens cannot satisfy. Digital devices eliminate screen engraving and allow pattern changes in minutes, enabling European brands to nearshore production for rapid replenishment. Operators that adopted single-pass pigment printers in 2025 reported double-digit reductions in inventory write-offs after shifting to print-on-demand models. Logistics savings also mount as fabric is printed closer to the point of sale, a factor that aligns with upcoming Europe traceability mandates.

Shift From Analog to Digital Printing in Textiles

Digital penetration is accelerating once job lengths fall below 1 000 meters, the economic break-even against rotary screens. Platforms such as the Epson SureColor F10070H integrate inline pretreatment and fixation, combining multiple wet processes into a single dry pass.[1]Seiko Epson Corporation, “SureColor F10070H Integrates Pretreatment and Fixation,” global.epson.com Polyester sportswear has moved fastest because dye sublimation avoids post-print washing, but cotton and viscose are catching up now that inline curing achieves comparable fastness. These dynamics explain why direct-to-fabric inkjet systems outsold rotary screens for the first time in China during 2025.

Advancements in High-Speed Inkjet Heads and Sublimation Inks

Next-generation piezoelectric heads deliver 1 200 dpi at industrial duty cycles, while recirculating designs mitigate nozzle failures and cut maintenance stops. Low-energy disperse dyes now sublimate at 180 °C, reducing energy use by 15% and enabling safe transfer onto polyester-spandex activewear. Fluorescent color sets have entered mainstream production, eliminating the final screen-printing holdout for neon accents. Taken together, these advances remove the throughput and color-gamut barriers that once limited digital adoption.

Expanding E-Commerce and Web-to-Print Platforms

More than 150 specialized portals globally now route artwork directly to networked direct-to-garment printers, shrinking delivery windows to five days or less. Average order values are falling as competition intensifies, yet platform providers offset margin pressure by offering modular hardware that pivots between direct-to-film and direct-to-garment modes. North America and Europe generate two-thirds of revenue today, but Asian marketplaces are integrating on-demand textile modules that could redraw the revenue map by 2028.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Capital Investment for Industrial-Scale Machines | -0.7% | Global, acute in South America, Africa, and smaller Asia-Pacific | Short term (≤ 2 years) |

| Volatility in Textile Ink Raw Material Prices | -0.5% | Global, pronounced in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Limited Color Gamut and Fastness for Certain Digital Inks | -0.3% | Global, affects fashion and home-textile segments | Medium term (2-4 years) |

| Regulatory Scrutiny on Wastewater Nanoparticles | -0.2% | Europe leads, North America, and Asia-Pacific monitoring | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial Capital Investment for Industrial-Scale Machines

Single-pass printers priced between USD 500 000 and USD 2 million are out of reach for many small and medium enterprises. Even where leasing is available, required credit guarantees keep adoption uneven, prolonging reliance on rotary screens in South America and Africa. Equipment-as-a-service models gained traction in 2025, yet payback still depends on volumes above 500 000 m² per year, a threshold few emerging-market converters can reach.

Volatility in Textile Ink Raw Material Prices

Titanium dioxide and disperse-dye intermediates experienced double-digit price swings in 2024-2025, forcing converters to renegotiate contracts mid-cycle.[2]ICIS Chemical Business, “Titanium Dioxide Price Trends 2024,” icis.com Smaller ink formulators lack scale to hedge raw material exposure, freezing research and development budgets and slowing innovation. Polyester-resin costs tethered to crude-oil benchmarks further complicate pricing, especially in regions that import feedstocks, reducing margins and dampening capital expenditure on new printers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Printing Technology: Single-Pass Throughput Redefines Cost Curves

Digital inkjet solutions accounted for 62.51% of 2025 revenue, making the segment a key driver of the textile printers market's growth. Between 2026 and 2031, the segment is projected to grow at a 3.45% CAGR, as single-pass machines match analog speed while offering unlimited pattern flexibility. The textile printers market now rewards software-driven uptime more than purely mechanical attributes, prompting suppliers to couple predictive-maintenance analytics with hardware leases.

Screen printing still dominates high-volume commodity runs because rotary units exceed 100 m min-¹, but their relevance erodes each time brands push for localized production or smaller order lots. Flatbed screens persist for textured effects unattainable with inkjet drops, though even this moat is narrowing as multi-layer digital varnish evolves. Hybrid platforms that hold a base screen station followed by inkjet heads are gaining share among converters unwilling to scrap legacy assets overnight.

By Ink Type: Pigment Advances Close Performance Gaps

Pigment chemistries, expanding at a 4.22% CAGR, are enabling the textile printers market to achieve grade 4-5 wash-fastness without relying on water-intensive steaming processes. This advancement is crucial to helping the market comply with Zero Discharge of Hazardous Chemicals (ZDHC) limits and with upcoming EU disclosure regulations. NeoPigment inks, combined with inline pretreatment modules, have now achieved cotton yields previously achieved only with reactive dyes. As a result, several textile mills across Asia have begun decommissioning their steamers, a trend that gained momentum in 2025, reflecting a significant shift in production practices driven by sustainability and regulatory compliance.[3]Kornit Digital Ltd., “NeoPigment Achieves Grade 4-5 Fastness,” kornit.com

Disperse and sublimation inks, which accounted for 41.08% of 2025 revenue, continue to dominate the polyester sportswear segment due to their compatibility with synthetic fabrics and vibrant color output. However, the growth rate in this segment is slowing as brands diversify their fabric choices to include multiple blends, reducing dependency on polyester alone. Meanwhile, UV-curable ink sets are gaining traction in the signage industry, particularly in applications where outdoor durability and resistance to environmental factors are critical. Additionally, bio-based binders, though currently a small share of the market, are gradually gaining adoption as brands incorporate life-cycle assessments into their purchasing decisions, aligning with sustainability goals and regulatory requirements.

By Application: Signage Growth Surpasses Garment Volume

Garments and apparel still accounted for 46.24% of 2025 throughput, yet soft signage recorded the highest segment CAGR at 4.05%, signaling a shift in the textile printers market toward more diversified revenue streams. Event agencies and retail chains increasingly replaced traditional PVC banners with polyester backdrops, which are easier to install, foldable for reuse, and more environmentally friendly. This trend has driven double-digit hardware upgrades in wide-format printing shops as businesses adapt to meet the growing demand for sustainable, efficient solutions.

Home textiles have seen significant benefits from made-to-order models, which help reduce over-stocking and waste. For instance, European retailers have introduced bespoke curtain-printing services with delivery windows as short as 2 weeks, catering to consumer preferences for customization and quick turnaround times. Meanwhile, technical textiles represent a promising white-space opportunity, though their growth is currently constrained by stringent certification cycles in industries such as automotive and medical. However, advancements in pigment-ink durability are beginning to shorten these qualification timelines, paving the way for broader adoption in these specialized applications.

By Fabric: Polyester Rises on Low-Temperature Sublimation

Cotton accounted for 48.15% of 2025 demand, driven by its widespread use in casual wear for its comfort and breathability. Polyester, on the other hand, exhibited a promising growth trajectory with a 3.67% CAGR, driven by advancements in low-energy disperse dyes that enhanced its compatibility with stretch blends. The market share of textile printers associated with polyester saw significant improvement following the introduction of 2025 models capable of sublimating at 180 °C, effectively preventing elastane degradation and expanding application possibilities.

Silk and niche regenerated fibers continued to cater to small but stable market segments, primarily targeting luxury accessories. However, the increasing use of fiber blends has introduced complexity into pre-treatment processes, prompting operators to invest in AI-driven profile libraries to streamline operations. To accommodate diverse customer demands, operators now maintain an inventory of six to eight ink sets, which, while increasing working-capital requirements, ensures the ability to accept a wide range of job orders and enhances operational flexibility.

Geography Analysis

Asia-Pacific accounted for 39.34% of the 2025 value and is projected to grow significantly through 2031, as China’s digital penetration surpasses 35% by 2030 and India’s incentive scheme refunds up to 25% of capital outlays. Investment clusters in Surat and Guangdong lead installations of single-pass dye-sublimation lines, with software upgrades driving incremental demand in Japan and South Korea. Southeast Asian exporters, notably Vietnam and Bangladesh, are installing hybrid platforms to remain competitive amid near-shoring in Europe.

Africa is experiencing the fastest regional growth, at 3.91%, driven by the WTO Cotton Initiative, which is channeling USD 5 billion into the development of integrated textile parks in Ethiopia, Egypt, Morocco, and Kenya. In Ethiopia, mills within the Hawassa Industrial Park installed pigment-inkjet corridors in 2025 to meet the growing demand of European retailers for traceability in their supply chains. Meanwhile, Morocco is capitalizing on its geographical proximity to Spain and France, enabling it to deliver printed fabric to these markets within 72 hours, thereby strengthening its position as a key supplier in the region.[4]World Trade Organization, “Cotton Initiative Investment Plan,” wto.org

North America and Europe expand more slowly, at 2.8% and 2.9% respectively, yet remain technology incubators. AI-based color-matching and digital product passports accelerate digital retrofits in these mature markets. South America and the Middle East lag due to import tariffs and limited technical support, although premium hospitality refurbishments in the United Arab Emirates now specify waterless pigment lines to meet internal sustainability charters.

Competitive Landscape

Competition in the market remains moderately concentrated, with the top five suppliers accounting for a significant portion of the 2025 revenue. Western incumbents are focusing on differentiation through robust software ecosystems and subscription-based offerings, which provide recurring revenue streams and enhance customer retention. On the other hand, Chinese manufacturers are aggressively undercutting hardware prices by as much as 40%, forcing established brands to shift their strategies toward service-oriented revenue models. For instance, Kornit Digital’s Atlas Intelligence Cloud processed an impressive 243 million garment impressions in Q4 2025, highlighting how workflow analytics have become as critical as mechanical speed in influencing purchase decisions.

Printhead licensors, including Kyocera, Epson, and Fujifilm, are leveraging their intellectual property by selling nozzle arrays to third-party machine builders. This approach has compressed hardware margins and intensified competition at the integration layer, where value addition is becoming increasingly important. Meanwhile, start-ups are gaining traction by promoting open-ink architectures that significantly lower consumable costs. This strategy has resonated particularly well with converters in emerging markets such as Africa and South America, where businesses are keen to avoid vendor lock-in and reduce operational expenses.

Patent filings during 2025-2026 are primarily focused on advancements in recirculation systems, inline pretreatment technologies, and AI-driven color adjustment mechanisms. These trends indicate a clear shift from traditional mechanical innovation toward data-centric and software-driven differentiation. Vertical integration is also playing a pivotal role in shaping channel strategies. For example, Durst’s acquisition of Technomac has enabled the company to offer bundled print-and-finish lines, which reduce floor space requirements by up to 40%. Similarly, Fujifilm’s dual role as both a printhead supplier and an equipment vendor has created channel friction, prompting some integrators to invest in developing proprietary printheads to maintain competitive independence.

Textile Printers Industry Leaders

Seiko Epson Corporation

Kornit Digital Ltd.

Electronics For Imaging (EFI Reggiani)

HP Inc.

Mimaki Engineering Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Mimaki Engineering Co., Ltd. has unveiled its flagship TS330 series, bolstering its range of sublimation transfer inkjet printers. The TS330 boasts a high-density, high-resolution printhead, enhanced by the company's proprietary imaging technology.

- January 2026: In response to surging global demand for versatile, efficient textile transfer printing, Epson unveiled the SureColor G9000, its latest high-production Direct-To-Film (DTFilm) printer.

- October 2025: EFI Reggiani introduced the EXTRA 3400, a 3.4 m, 100 m/min single-pass printer aimed at home textiles and soft signage.

- September 2025: MS Printing Solutions and JK Group, both under Dover Group, unveiled five multi-pass (MP) printers, aiming to elevate benchmarks in digital textile printing. The newly launched MP Series, built on an advanced platform, boasts notable enhancements in its body design, construction architecture, user interface, electronics, and print heads, and prioritizes safety and user-friendliness.

Global Textile Printers Market Report Scope

The Textile Printers Market encompasses the global industry involved in the manufacturing, distribution, and use of textile printing equipment, technologies, inks, and related solutions for applying designs, patterns, colors, and graphics to textile substrates. This market includes a wide range of printing technologies such as digital inkjet printing, screen printing, and other conventional and advanced textile printing methods used across diverse fabric types, including cotton, polyester, silk, blends, and specialty textiles.

The Textile Printers Market Report is Segmented by Printing Technology (Digital Inkjet Printing, Screen Printing, and Other Printing Technologies), Ink Type (Reactive Dye Inks, Acid Dye Inks, Pigment Inks, Disperse and Sublimation Inks, UV-Curable and Hybrid Inks, and Other Ink Types), Application (Garments and Apparel, Home Textiles, Signage and Display Graphics, Technical Textiles, and Other Applications), Fabric (Cotton, Polyester, Silk, Blends, and Other Fabrics), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Digital Inkjet Printing | Direct-to-Fabric (DTF) |

| Direct-to-Garment (DTG) | |

| Dye-Sublimation | |

| Single-Pass and Others | |

| Screen Printing | Rotary Screen |

| Flatbed Screen | |

| Other Printing Technologies |

| Reactive Dye Inks |

| Acid Dye Inks |

| Pigment Inks |

| Disperse and Sublimation Inks |

| UV-Curable and Hybrid Inks |

| Other Ink Types |

| Garments and Apparel |

| Home Textiles |

| Signage and Display Graphics |

| Technical Textiles |

| Other Applications |

| Cotton |

| Polyester |

| Silk |

| Blends |

| Other Fabrics |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Israel | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Printing Technology | Digital Inkjet Printing | Direct-to-Fabric (DTF) |

| Direct-to-Garment (DTG) | ||

| Dye-Sublimation | ||

| Single-Pass and Others | ||

| Screen Printing | Rotary Screen | |

| Flatbed Screen | ||

| Other Printing Technologies | ||

| By Ink Type | Reactive Dye Inks | |

| Acid Dye Inks | ||

| Pigment Inks | ||

| Disperse and Sublimation Inks | ||

| UV-Curable and Hybrid Inks | ||

| Other Ink Types | ||

| By Application | Garments and Apparel | |

| Home Textiles | ||

| Signage and Display Graphics | ||

| Technical Textiles | ||

| Other Applications | ||

| By Fabric | Cotton | |

| Polyester | ||

| Silk | ||

| Blends | ||

| Other Fabrics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the textile printers market, and how fast is it growing?

The textile printers market size reached USD 1.11 billion in 2025 and is projected to climb to USD 1.34 billion by 2031, reflecting a 3.13% CAGR over 2026-2031.

Which printing technology holds the largest share of global revenue?

Digital inkjet equipment led with 62.51% of 2025 revenue, owing to single-pass architectures that now match analog speed.

Why are pigment inks gaining traction in textile printing?

Polymer-encapsulated pigment inks now achieve grade 4-5 wash-fastness without water-intensive steaming, supporting ZDHC compliance and driving the fastest segment CAGR of 4.22%.

Which geographic region is expanding the fastest?

Africa records the highest regional CAGR at 3.91% through 2031, supported by the WTO Cotton Initiative and new industrial parks in Ethiopia, Egypt, and Morocco.

How are equipment suppliers differentiating in a crowded market?

Leading vendors focus on cloud-based workflow analytics, predictive maintenance, and consumable subscription models, while budget manufacturers compete primarily on upfront hardware cost.

What barriers still limit digital adoption among smaller converters?

High capital outlays of USD 500000-2 million for industrial single-pass printers and volatile raw-material prices extend payback periods beyond five years for low-volume operators.

Page last updated on: