U.S. Dialysis Centers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 32.21 Billion |

| Market Size (2026) | USD 33.81 Billion |

| Market Size (2031) | USD 43.09 Billion |

| Growth Rate (2026 - 2031) | 4.97% CAGR |

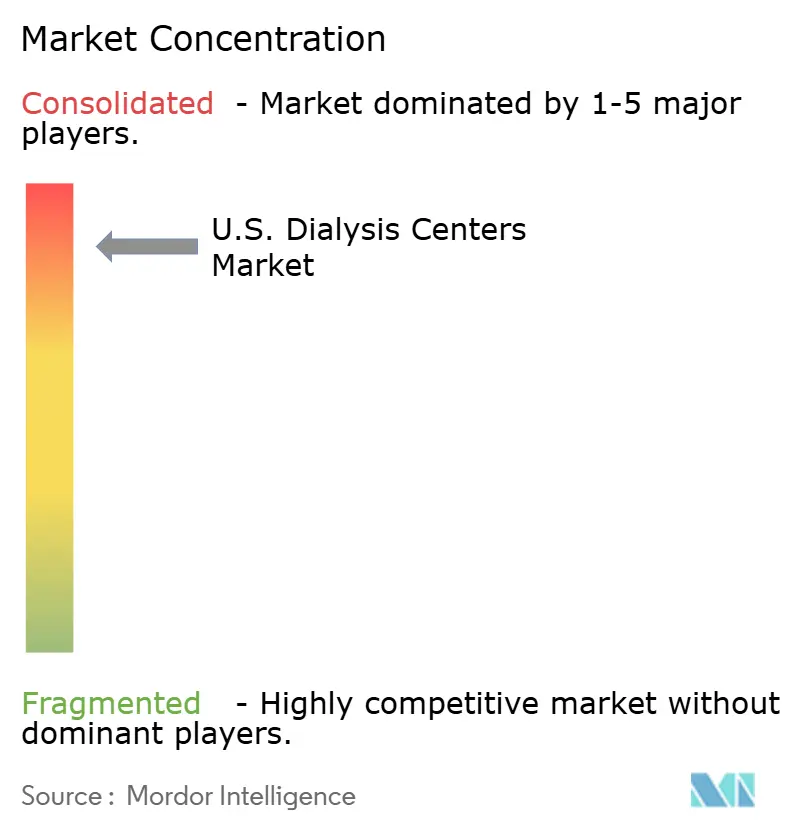

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

U.S. Dialysis Centers Market Analysis by Mordor Intelligence

The U.S. Dialysis Centers Market size is projected to expand from USD 32.21 billion in 2025 and USD 33.81 billion in 2026 to USD 43.09 billion by 2031, registering a CAGR of 4.97% between 2026 to 2031.

In the United States, over 857,000 individuals live with end-stage kidney disease, with approximately 135,000 new cases annually. Due to limited transplant availability, 68% of these patients rely on chronic dialysis for treatment.[1]United States Renal Data System, “2024 Interactive Annual Data Report,” National Institute of Diabetes and Digestive and Kidney Diseases, niddk.nih.gov The dialysis centers market in the United States benefits from a stable payer structure, as Medicare covers the majority of dialysis patients, ensuring consistent treatment demand across the country. For CY 2026, regulators have proposed an ESRD Prospective Payment System base rate of USD 281.06 per treatment, reflecting a USD 7.24 increase from 2025.[2]Centers for Medicare & Medicaid Services, “Calendar Year (CY) 2026 End-Stage Renal Disease (ESRD) Prospective Payment System Proposed Rule, CMS-1830-P,” CMS Newsroom, cms.gov This adjustment addresses rising operating costs, although providers continue to face margin pressures. The market is witnessing a shift in care delivery, with growing adoption of home-based programs, peritoneal dialysis, and integrated kidney care contracts. These trends are influencing investment strategies for major operators and creating opportunities for community-based models.

Key Report Takeaways

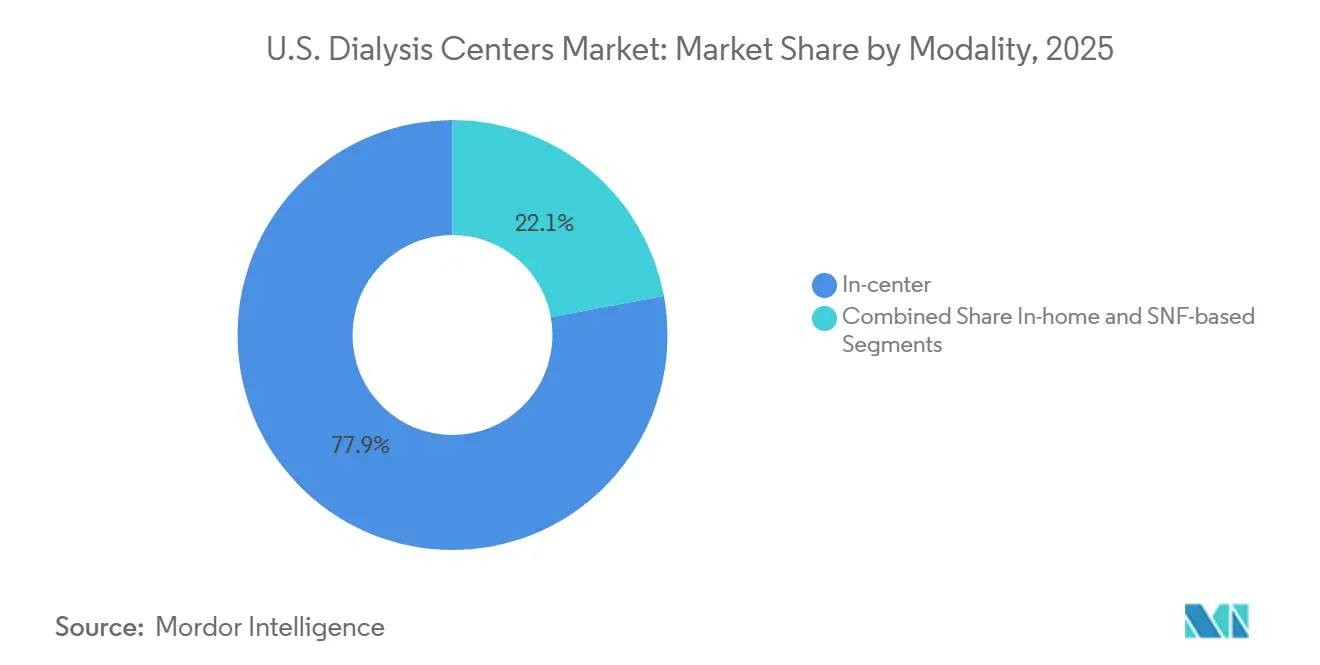

- By modality, in-center dialysis held 77.89% of the U.S. dialysis centers market share in 2025, while in-home dialysis is projected to expand at a 7.00% CAGR through 2031.

- By dialysis type, hemodialysis accounted for 89.40% of revenue in 2025, while peritoneal dialysis is projected to grow at a 6.10% CAGR through 2031.

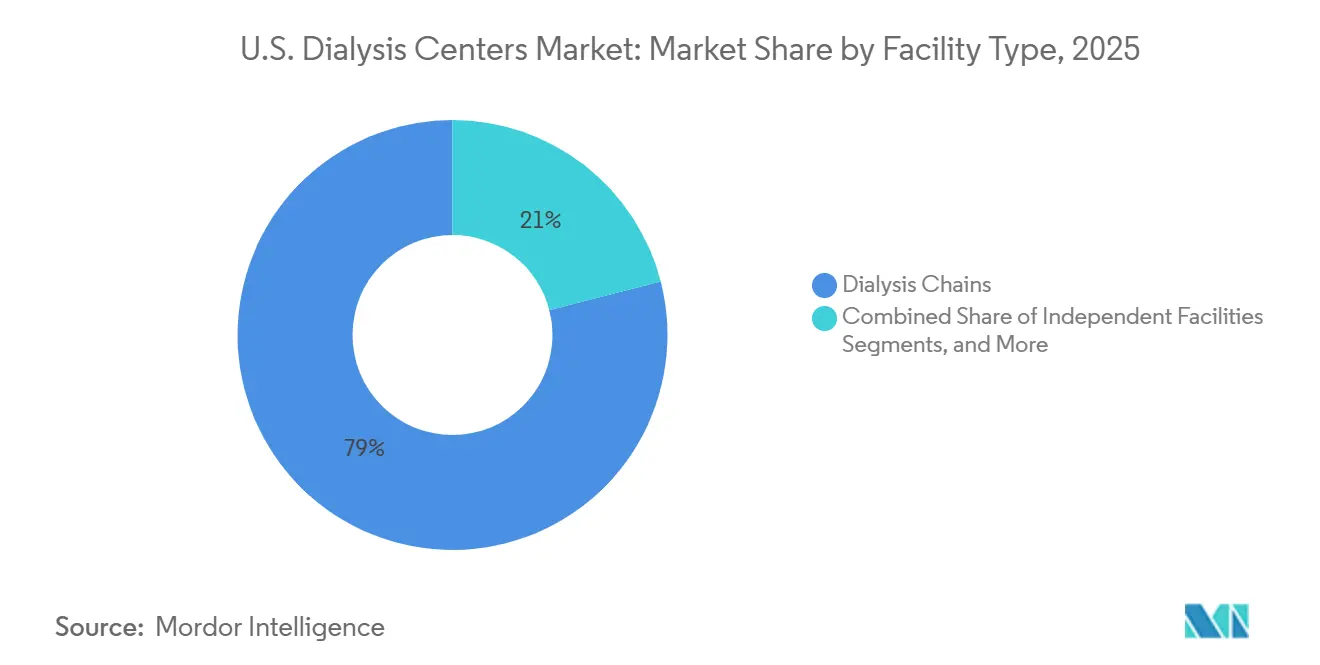

- By facility type, dialysis chains accounted for 78.99% of the U.S. dialysis centers market size in 2025, while independent facilities are expected to grow at a 5.90% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

U.S. Dialysis Centers Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising ESKD prevalence from diabetes, hypertension, and other causes | +0.9% | National, with concentrated impact in the Southeast, South, and Midwest | Long term (≥ 4 years) |

| Durable Medicare-funded treatment demand base | +0.8% | National across rural and urban ESRD facilities | Medium term (2-4 years) |

| Home dialysis expansion by leading center operators | +0.6% | National, with stronger penetration in the West and Northeast and emerging uptake in the Southeast | Medium term (2-4 years) |

| Medicare Advantage and integrated kidney-care adoption | +0.5% | National, with early gains in urban CKCC-enrolled markets | Short term (≤ 2 years) |

| High-volume hemodiafiltration rollout in U.S. clinics | +0.4% | Initially concentrated in Fresenius Kidney Care pilot regions and then scaling nationally | Medium term (2-4 years) |

| AKI home-dialysis billing expansion | +0.3% | National, with faster uptake in states with stronger home health infrastructure | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising ESKD Prevalence from Diabetes, Hypertension, and Related Causes

The United States dialysis centers market continues to grow, driven by an increasing patient base. The ESKD population has risen steadily in the early 2020s, with diabetes, hypertension, and chronic kidney disease remaining significant contributors. Approximately 37 million adults in the United States, or 1 in 7, live with chronic kidney disease, with many undiagnosed until advanced stages. Incident ESKD cases increased by 31.3% between 2002 and 2022, highlighting a widening demand base. An aging treated population and limited transplant eligibility further sustain the market's growth.

Durable Medicare-funded Treatment Demand Base

The United States dialysis centers market benefits from Medicare's ESKD coverage, ensuring a stable payment foundation. CMS projects nearly USD 6.9 billion in payments to 7,600 ESRD facilities in CY 2026, up from USD 6.6 billion to 7,700 facilities in 2025. The proposed CY 2026 base rate of USD 281.06 per treatment, reflecting a 1.9% market basket update, provides payment stability. This model supports care continuity, keeps facilities operational, and maintains demand even during economic challenges.

Home Dialysis Expansion by Leading Center Operators

Home care is a growing segment in the United States dialysis centers market, driven by policy changes, operator investments, and care coordination. Currently, 14.1% of the dialysis population receives treatment at home, a significant increase from a decade ago. CMS has supported this shift by extending Medicare payments for AKI home dialysis, introducing training add-ons, and maintaining pathways for innovative supplies. Leading operators like DaVita are expanding integrated care efforts, though home care's operational complexity requires value-based contracts or strong clinical management models for profitability.

Medicare Advantage and Integrated Kidney-Care Adoption

Medicare Advantage (MA) has become a significant force in the United States dialysis centers market, with over 54% of Medicare-eligible dialysis patients with ESKD enrolled in MA by 2025. MA plans prioritize cost efficiency, favoring operators with strong care coordination, data systems, and risk management.[3]Centers for Medicare & Medicaid Services, “Calendar Year 2025 End-Stage Renal Disease (ESRD) Prospective Payment System (PPS) Final Rule, CMS-1805-F,” CMS Newsroom, cms.gov DaVita managed over USD 5.6 billion in annualized medical spending under risk-based kidney care arrangements in late 2025, showcasing the competitive advantage of scale. Smaller operators face challenges as the market increasingly emphasizes actuarial risk, utilization management, and multidisciplinary care infrastructure.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Staffing scarcity and wage inflation | -0.8% | National, with sharper pressure in rural areas and underserved markets | Long term (≥ 4 years) |

| Government-heavy payer mix and reimbursement pressure | -0.7% | National, with stronger effect in markets that lack commercial payer depth | Medium term (2-4 years) |

| ETC model termination weakens home-dialysis catalyst | -0.4% | National, with stronger relevance in hospital referral regions affected by ETC design | Short term (≤ 2 years) |

| Oral-only phosphate-binder bundling pressure | -0.3% | National across ESRD PPS-reimbursed facilities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Staffing Scarcity and Wage Inflation

Staffing shortages are a critical challenge in the United States dialysis centers market, particularly in areas struggling to recruit nurses, technicians, and social workers. CMS regulations require a registered nurse to be present during dialysis, turning staffing gaps into compliance risks. Providers face rising wage demands, shift differentials, agency reliance, and burnout, while payment updates fail to match labor cost pressures. To address this, providers like U.S. Renal Care are building internal talent pipelines, such as their 2025 program to train nephrology nurses. Rural and smaller markets are most affected, limiting the ability to expand or stabilize treatment capacity.

Government-heavy Payer Mix and Reimbursement Pressure

The United States dialysis centers market depends heavily on government reimbursements, restricting pricing flexibility when costs outpace payment updates. CMS has proposed a 1.9% aggregate payment increase for CY 2026, with hospital-based ESRD facilities receiving a smaller 1.5% increase compared to 1.9% for freestanding centers. Larger chains manage better due to scale, purchasing power, and administrative capacity, while smaller operators and hospital-based sites struggle to spread overhead and negotiate terms. This dynamic drives market consolidation as reimbursement pressures persist despite steady patient demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Modality: In-Home Dialysis Reshapes the Care Delivery Model

In 2025, in-center dialysis dominated the United States dialysis centers market, capturing 77.89% of the revenue. This reflects the model's reliance on fixed clinics, scheduled chair capacities, and established workflows. In-home dialysis, projected to grow at a 7.00% CAGR through 2031, is the fastest-growing modality, supported by Medicare policy changes that ease financial burdens for providers expanding home programs. While clinic demand remains strong, home care is reshaping the care model with a focus on patient education, remote oversight, and supply logistics.

The in-center model retains advantages for patients needing close supervision or transportation support. Meanwhile, SNF-based dialysis serves as a transitional setting for frail patients, reducing hospital readmissions by 15%, as highlighted by DaVita. This diversification enhances the delivery capacity of the United States dialysis centers market.

By Dialysis Type: Peritoneal Dialysis Builds a Larger Role Beside Hemodialysis

In 2025, hemodialysis led the United States dialysis centers market, accounting for 89.40% of revenue. Its dominance is driven by established infrastructure, provider familiarity, and reimbursement pathways. Fresenius Medical Care strengthened this segment with the commercialization of the 5008X CAREsystem, enhancing clinical capabilities without altering the core delivery model.

Peritoneal dialysis, though smaller, is projected to grow at a 6.10% CAGR through 2031. Its appeal lies in supporting overnight routines, work-life balance, and reduced clinic visits. Advancements like automated cyclers and remote monitoring have improved scalability, while expanded reimbursement policies further support home-based kidney care. The modality mix is gradually balancing, though hemodialysis remains the primary revenue driver.

By Facility Type: Independent Operators Find Room Within a Consolidated Structure

In 2025, dialysis chains dominated the United States dialysis centers market, accounting for 78.99% of revenue. DaVita and Fresenius controlled nearly 80% of facilities and generated about 90% of industry revenue. Their scale provides advantages in procurement, staffing, and technology investments, while CMS payment policies favor freestanding centers over hospital-based facilities, reinforcing chain dominance.

Independent facilities, projected to grow at a 5.90% CAGR through 2031, focus on local relationships, physician ownership, and niche services. These providers excel in targeted settings like home programs or post-acute partnerships but face tight margins due to reimbursement and compliance pressures. Growth is likely to remain selective, preserving the chain-led structure of the United States dialysis centers market.

Geography Analysis

The Southeast remains the largest demand cluster in the United States dialysis centers market due to the overlapping prevalence of kidney failure, diabetes, hypertension, and access gaps. States like Georgia and Alabama face a burden exceeding the national average, reflecting the region's persistent challenges in kidney care delivery. African Americans are nearly four times more likely than Whites to develop kidney failure, a risk profile significant in Southern states with large Black populations. Florida's aging population and Texas's high diabetes rates further drive demand, making network economics heavily dependent on regional disease burdens.

The Northeast exhibits a distinct profile in the United States dialysis centers market, combining dense urban demand with strong ties to academic medical centers and a preference for home-based kidney care. States such as New York, Massachusetts, and New Jersey lead in home dialysis adoption and integration with advanced clinical infrastructure. This region prioritizes program depth, technology, and coordinated care over facility expansion, with competition shaped by care sophistication and payer diversity.

The Midwest and West contribute uniquely to the United States dialysis centers market, driven by different factors. The Midwest faces elevated kidney disease rates due to diabetes prevalence, aging populations, and inconsistent preventive care access. In contrast, the West Coast, led by California, is associated with higher peritoneal dialysis adoption and stronger home program penetration. These regional variations highlight that the market grows through localized demand patterns, rewarding diverse operational models across the country.

Competitive Landscape

The United States dialysis centers market is highly concentrated, with DaVita and Fresenius Medical Care operating nearly 80% of facilities and generating approximately 90% of industry revenue. This duopoly impacts supplier negotiations, payer leverage, staffing systems, clinical rollouts, and scaling new operating models. By late 2025, DaVita reported USD 5.6 billion in annualized medical spending under risk-based arrangements, covering around 66,000 patients. Fresenius plans to differentiate clinically in 2026 through the commercialization of high-volume hemodiafiltration using the 5008X CAREsystem.

Mid-tier players, including U.S. Renal Care, Dialysis Clinic, Inc., Satellite Healthcare, Innovative Renal Care, and Northwest Kidney Centers, focus on quality, local partnerships, and home program depth. Innovative Renal Care is expanding through partnerships, such as its 2025 launch with Akebia Therapeutics for Vafseo across 230+ centers in 28 states. Vantive's collaboration with U.S. Renal Care aims to enhance home dialysis access and improve patient experiences, reflecting a trend of leveraging external technology partnerships.

Opportunities exist in areas where the duopoly has limited reach, such as rural coverage, SNF-linked dialysis, and specific value-based care arrangements. Smaller and mid-sized operators can succeed by building local physician relationships, integrating post-acute care, or strengthening home support in targeted regions. However, reimbursement pressures, compliance demands, and staffing shortages continue to challenge independent expansion. The market is expected to remain concentrated, with innovation and localized differentiation driving niche opportunities rather than a broad competitive shift.

U.S. Dialysis Centers Industry Leaders

DaVita Inc.

Fresenius Medical Care AG

U.S. Renal Care, Inc.

Dialysis Clinic, Inc.

Satellite Healthcare, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Fresenius Medical Care commenced the U.S. commercialization of its 5008X CAREsystem. The company launched its high-volume hemodiafiltration therapy nationwide, aiming for a 15-30% adoption rate across approximately 2,600-2,800 Fresenius Kidney Care clinics by the end of 2026.

- August 2025: Akebia Therapeutics partnered with Innovative Renal Care to introduce Vafseo across all IRC clinics. IRC adopted a standardized treatment protocol for Vafseo, an FDA-approved oral therapy for treating anemia in dialysis patients with CKD, across its 230+ dialysis centers in 28 states.

U.S. Dialysis Centers Market Report Scope

As per the scope of the report, dialysis centers are specialized healthcare facilities that perform life-sustaining treatments, primarily hemodialysis, for patients with chronic kidney disease (CKD) or end-stage renal disease (ESRD). They filter waste, excess fluids, and toxins from the blood when a patient's kidneys can no longer function.

The U.S. dialysis centers market is segmented by modality, dialysis type, and facility type. By modality, the market includes in-center, in-home, and SNF-based. By dialysis type, the market is segmented into hemodialysis and peritoneal dialysis. By facility type, the market is categorized into dialysis chains, independent facilities, and hospital-based. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| In-center |

| In-Home |

| SNF-based |

| Hemodialysis |

| Peritoneal Dialysis |

| Dialysis Chains |

| Independent Facilities |

| Hospital-based |

| By Modality | In-center |

| In-Home | |

| SNF-based | |

| Dialysis Type | Hemodialysis |

| Peritoneal Dialysis | |

| By Facility Type | Dialysis Chains |

| Independent Facilities | |

| Hospital-based |

Key Questions Answered in the Report

What is the 2026 value of the U.S. dialysis centers market?

The U.S. dialysis centers market stands at USD 33.81 billion in 2026 and is forecast to reach USD 43.09 billion by 2031 at a 4.97% CAGR.

Which modality leads revenue in U.S. dialysis centers?

In-center dialysis remains the leading modality, holding 77.89% of revenue in 2025, although in-home dialysis is growing faster at a 7.00% CAGR through 2031.

Which dialysis type is expanding faster through 2031?

Peritoneal dialysis is growing faster, with a projected 6.10% CAGR, while hemodialysis still dominates current revenue with an 89.40% share in 2025.

Why is Medicare so important for dialysis center demand in the United States?

Medicare coverage for ESKD creates a stable reimbursement base and supports recurring treatment demand across most of the patient population, which reduces volume volatility for providers.

Why does the Southeast matter so much for dialysis center operators?

The region carries a heavier kidney failure burden, and risk factors such as diabetes, hypertension, and unequal preventive care access keep demand concentrated there.

How concentrated is competition among U.S. dialysis center operators?

Competition is highly concentrated because DaVita and Fresenius together control close to 80% of facilities and generate approximately 90% of industry revenue, while smaller players compete in selected niches.

Page last updated on: