U.S. Ambulatory Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 321.95 Billion |

| Market Size (2026) | USD 339.5 Billion |

| Market Size (2031) | USD 442.37 Billion |

| Growth Rate (2026 - 2031) | 5.45% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

U.S. Ambulatory Services Market Analysis by Mordor Intelligence

The U.S. Ambulatory Services Market size is expected to grow from USD 321.95 billion in 2025 to USD 339.5 billion in 2026 and is forecast to reach USD 442.37 billion by 2031 at 5.45% CAGR over 2026-2031.

In 2026, CMS initiated the phase-out of the Medicare Inpatient-Only list, removing 285 codes primarily for musculoskeletal procedures and adding 573 codes to the ASC Covered Procedures List, strengthening the procedure pipeline for the United States ambulatory services market. National Health Expenditure projections published in 2025 indicated a 5.5% annual growth in physician and clinical services spending through 2033, aligning with the anticipated growth of the United States ambulatory services market.[1]Ambulatory Surgery Center Association, “CMS Releases 2026 Final Payment Rule,” Ambulatory Surgery Center Association, ascassociation.org Extended Medicare telehealth flexibilities through December 2027, increasing outpatient cancer demand, and the growing use of AI-enabled diagnostics and robotic tools are expanding the scope of outpatient care in the United States ambulatory services market. However, challenges such as revenue-cycle cyber risks and persistent staffing shortages continue to create operational inconsistencies, even as the market demonstrates durable growth potential.

Key Report Takeaways

- By care setting, primary care clinics held 38.75% of revenue in 2025, while telehealth and virtual clinics are projected to grow at a 7.23% CAGR through 2031.

- By service type, treatment accounted for 42.75% of revenue in 2025, while diagnosis is forecast to expand at a 6.90% CAGR from 2026 to 2031.

- By specialty, gastroenterology led with a 25.70% revenue share in 2025, while oncology is projected to advance at an 8.42% CAGR through 2031.

- By ownership model, hospital or health-system-owned facilities held a 31.21% revenue share in 2025, while physician-owned facilities are projected to grow at an 8.33% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

U.S. Ambulatory Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact On CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inpatient-to-outpatient site-of-care migration | +1.8% | National, accelerated in Sun Belt states and major metropolitan corridors | Short term (≤ 2 years) |

| Aging population and chronic disease burden | +1.4% | National, with stronger demand in retirement destinations and high Medicare Advantage states | Long term (≥ 4 years) |

| Minimally invasive and digital technologies broaden outpatient access | +1.1% | National, with early adoption concentrated in large academic and urban outpatient networks | Medium term (2-4 years) |

| Value-based care and payer steerage to lower-cost settings | +0.8% | National, with higher penetration in states with mature value-based contracting | Medium term (2-4 years) |

| 2026 ASC covered-procedure expansion and inpatient-only phase-out | +0.6% | National, with stronger near-term effect in orthopedic, cardiovascular, and GI corridors | Short term (≤ 2 years) |

| Permanent virtual supervision expands staffing flexibility | +0.4% | National, with higher usefulness in rural markets and dispersed provider networks | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Inpatient-To-Outpatient Site-Of-Care Migration

The migration from inpatient to outpatient settings continues to drive volume growth in the United States ambulatory services market. In 2026, CMS removed 285 musculoskeletal procedures from the Inpatient-Only list and added 573 new codes to the ASC Covered Procedures List, including cardiac electrophysiology ablations and posterior lumbar interbody fusion.[2]Ambulatory Surgery Center Association, “CMS Releases 2026 Final Payment Rule,” Ambulatory Surgery Center Association, ascassociation.org This change enables procedures previously confined to hospitals to transition to outpatient settings, expanding the procedure mix and increasing opportunities for ambulatory operators. Additionally, commercial Medicare Advantage plans often align with traditional Medicare site-of-service patterns, amplifying the impact of CMS policy changes across payer channels and solidifying this trend as a key growth driver for the market.

Aging Population And Chronic Disease Burden

Demographic trends are creating sustained demand for the United States ambulatory services market. Medicare spending is projected to grow at 7.8% annually through 2033, reflecting the impact of an aging population. By 2050, 142.7 million adults aged 50 and older are expected to have at least one chronic condition, driving demand for outpatient services in cardiovascular management, nephrology, oncology infusion, and behavioral health.[3]John P. Ansah and Chi-Tsun Chiu, “Projecting the Chronic Disease Burden Among the Adult Population in the United States Using a Multi-State Population Model,” Frontiers in Public Health, pmc.ncbi.nlm.nih.gov Outpatient cancer care is particularly significant, with projected volumes reaching 222 million encounters over the next decade. These trends anchor the market's growth to long-term population health needs rather than short-term economic fluctuations.

Minimally Invasive And Digital Technologies Broaden Outpatient Access

Technological advancements are expanding the scope of procedures in the United States ambulatory services market. Robotic platforms, such as Medtronic’s Hugo system and Johnson & Johnson’s OTTAVA, are increasingly suited to outpatient settings due to their compact and mobile designs. RadNet reported a 19.7% year-over-year growth in advanced imaging volumes in Q1 2026 and anticipates over 70% of studies will utilize clinical AI by the end of 2026. AI-driven tools for scheduling, decision support, and revenue cycles enhance operational efficiency, making technology both a clinical enabler and a cost advantage for ambulatory operators.

Value-Based Care, Covered-Procedure Expansion, And Virtual Supervision Flexibility

Value-based care models and payer strategies are driving growth in the United States ambulatory services market. By 2024, Medicare Advantage enrollment reached 54% of eligible beneficiaries, with plans steering patients toward ASCs and freestanding clinics through prior authorization and cost-sharing mechanisms. CMS’s TEAM bundled payment model rewards cost-effective, high-quality care, strengthening the position of independent ASCs and physician-led platforms. The 2026 expansion of covered procedures further supports this shift, particularly in orthopedics, cardiovascular, and GI services. Extended telehealth flexibilities through December 2027 and virtual supervision capabilities enhance staffing reach, particularly in rural and distributed networks, supporting flexible and efficient care delivery models.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Regulatory complexity and reimbursement variability | -0.7% | National, most acute in CON-law states and states with complex Medicaid frameworks | Medium term (2-4 years) |

| Workforce shortages and clinician burnout | -0.5% | National, with stronger pressure in rural and underserved markets | Long term (≥ 4 years) |

| Clearinghouse and cybersecurity fragility in revenue-cycle infrastructure | -0.4% | National, especially among smaller practices with limited IT redundancy | Short term (≤ 2 years) |

| Site-neutral payment expansion pressures hospital outpatient margins | -0.3% | National, with highest exposure in grandfathered off-campus HOPDs and hospital-affiliated departments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Complexity, Reimbursement Variability, And Site-Neutral Payment Pressure

The regulatory framework of the United States ambulatory services market remains intricate and costly. Operators must address federal payment policies, state Certificate of Need rules, private payer credentialing, and HIPAA compliance simultaneously. The CY 2026 OPPS/ASC Final Rule, extending site-neutral payment to drug administration services in certain off-campus hospital outpatient departments, is expected to reduce Medicare OPPS spending by USD 290 million in 2026. CMS has also retained the 340B remedy offset for 2026 and indicated a larger conversion factor reduction in 2027, adding financial strain on outpatient hospital operations. These regulatory shifts create revenue planning uncertainties for smaller operators, leading to cautious capital allocation and an uneven operating environment across the United States ambulatory services market.

Workforce Shortages, Burnout, And Revenue-Cycle Cybersecurity Fragility

Workforce shortages remain a critical constraint in the United States ambulatory services market. A study highlighted by the AMA found that 47.9% of physicians frequently work with understaffed teams, contributing to increased burnout and a 15.4% intent-to-leave rate within two years. AMGA reported a 4.8% decline in primary care staffing ratios over three years and annual turnover rates of 17% to 18% for key roles like RNs and medical assistants. Additionally, the February 2024 ransomware attack on Change Healthcare, affecting approximately 192.7 million individuals, exposed the sector's reliance on limited revenue-cycle intermediaries. Smaller practices and local networks face heightened risks due to limited IT resources. While these challenges do not halt growth, they constrain the ability of providers to efficiently meet demand in the United States ambulatory services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Care Setting: Telehealth Disrupts A Primary-Care-Led Market

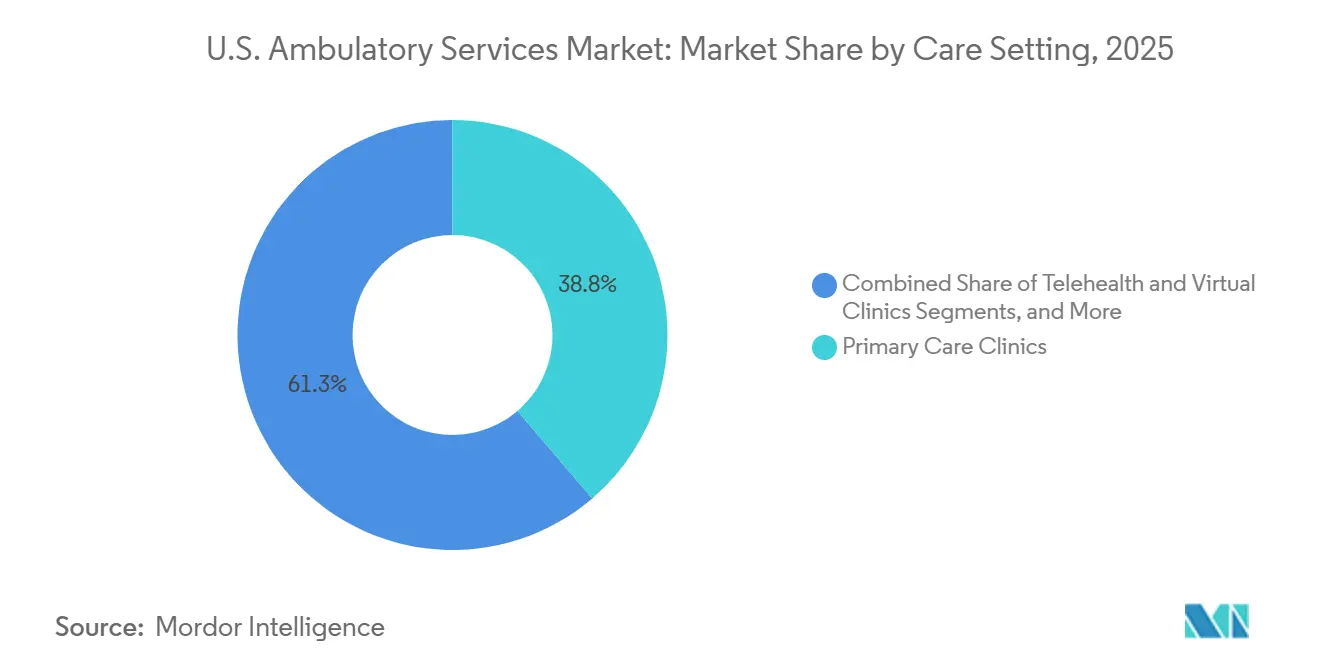

In 2025, Primary Care Clinics held a 38.75% revenue share, maintaining their leadership in the United States ambulatory services market. This dominance highlights their role as the primary access point for routine evaluations, chronic disease management, referrals, and follow-up care. However, the shift toward higher acuity or procedural density settings is pressuring traditional clinics to enhance workflows and improve patient retention.

Telehealth and Virtual Clinics are projected to grow at a 7.23% CAGR through 2031, making them the fastest-growing segment in the United States ambulatory services market. Growth is driven by Medicare's telehealth flexibilities extended until December 2027 and the increasing integration of telehealth into behavioral health and follow-up consultations. By December 2025, mental health telehealth accounted for 28.2% of specialty encounters, reflecting the rapid adoption of off-site care models.

By Service Type: Treatment Dominates But Diagnosis Expands Quickly

Treatment services accounted for 42.75% of revenue in 2025, making it the largest segment in the United States ambulatory services market. This reflects the higher reimbursement rates for procedures compared to routine consultations. Ambulatory surgery centers (ASCs) reported EBITDA margins of 24.1% in 2024, with only slight easing expected by 2029. As more procedures shift from hospitals to outpatient settings, treatment-heavy facilities are expected to maintain their lead.

Diagnosis is projected to grow at a 6.90% CAGR from 2026 to 2031, making it the fastest-growing segment in the United States ambulatory services market. Digital Health's annual recurring revenue nearly doubled to USD 96.9 million between March 2025 and March 2026, showcasing the growing role of diagnostic platforms in generating software-based revenue streams.

By Specialty: Gastroenterology Leads While Oncology Sets The Growth Pace

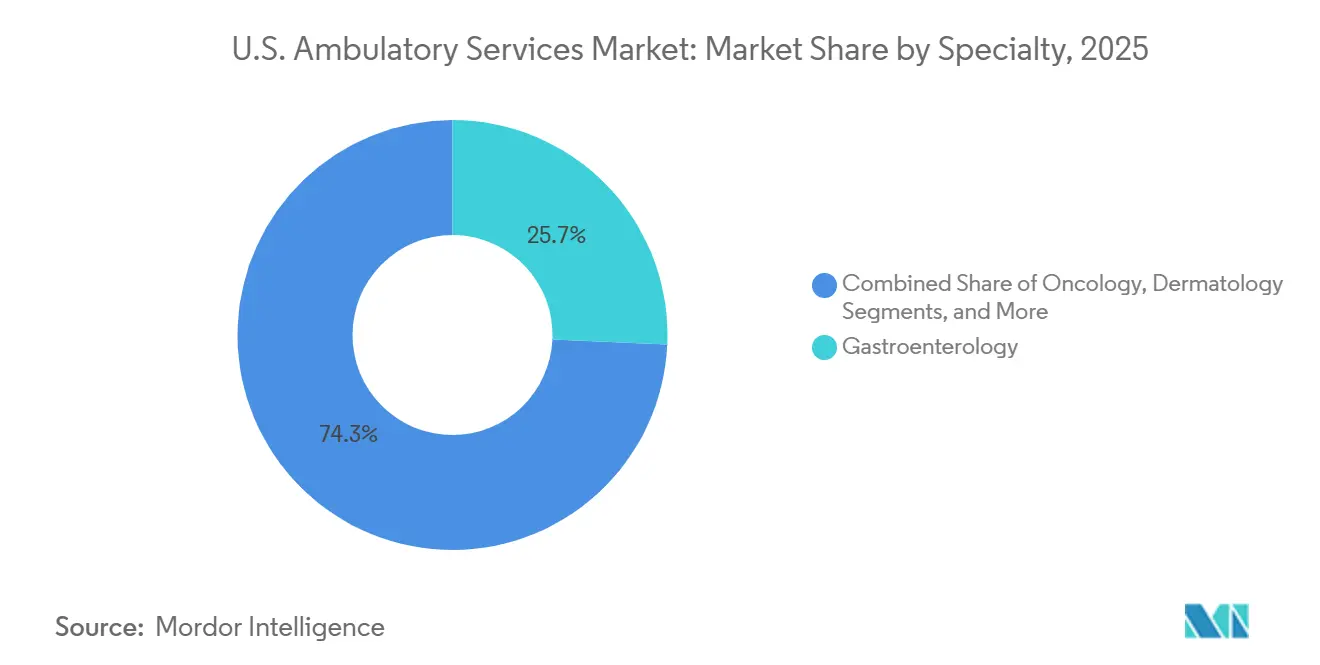

In 2025, Gastroenterology held a 25.70% revenue share, leading the specialty mix in the United States ambulatory services market. Established procedures like colonoscopy and advanced GI treatments benefit from clinical familiarity and strong reimbursement rates. The specialty also attracts acquisition interest, as seen in SCA Health’s acquisition of U.S. Digestive Health Management in early 2025, indicating its appeal as a stable cash-flow segment.

Oncology is projected to grow at an 8.42% CAGR through 2031, making it the fastest-growing specialty in the United States ambulatory services market. Growth is supported by ambulatory infusion, radiation therapy, immunotherapy management, and a cancer burden of nearly 2.04 million new diagnoses in 2025. Capital investments, such as Cencora's acquisition of OneOncology and McKesson's Core Ventures transaction in 2025, further highlight the segment's strategic importance.

By Ownership Model: Health-System Scale Faces A More Agile Physician-Led Challenge

In 2025, Hospital or Health-System-Owned facilities accounted for 31.21% of revenue, making them the largest ownership category in the United States ambulatory services market. Their scale supports payer negotiations, physician alignment, referral capture, and capital investments. However, site-neutral reimbursements are eroding the pricing advantages historically enjoyed by hospital-affiliated outpatient departments. The CY 2026 OPPS/ASC rule aligns certain drug administration services with Physician Fee Schedule rates, adding margin pressure to hospital ownership models.

Physician-Owned facilities are projected to grow at an 8.33% CAGR through 2031, making them the fastest-growing ownership model in the United States ambulatory services market. CMS policies addressing cost inflation tied to hospital employment incentives provide physician-led ASCs with a competitive edge in specific procedure categories. Corporate and private-equity-backed operators are also expanding, while joint ventures align physician incentives with system-level capital and operational support.

Geography Analysis

Sun Belt states, including Florida, Texas, Arizona, and the broader Southeast, are driving growth in the United States ambulatory services market. This expansion is supported by an aging population and increasing outpatient utilization. Florida, a key retirement destination, experiences strong demand for nephrology, orthopedics, cardiovascular management, and oncology infusion services. Texas is emerging as a major development hub, with Surgery Partners reporting double-digit growth in musculoskeletal and total joint procedures in Sun Belt markets during Q1 2026. The company also opened nine new facilities in the past year, highlighting the region's strategic importance. However, Certificate of Need requirements in many states continue to restrict new entrants and protect established providers in regulated markets.

The Northeast and Pacific Coast exhibit a different trend in the United States ambulatory services market, where managed care penetration and value-based contracting are more advanced. States like California and Massachusetts favor operators skilled in managing outcomes, data reporting, and payer integration over procedure volume. RadNet's presence in California, New York, Maryland, and Florida demonstrates the critical role of geography in influencing patient demand, reimbursement mix, and technology deployment.

Competitive Landscape

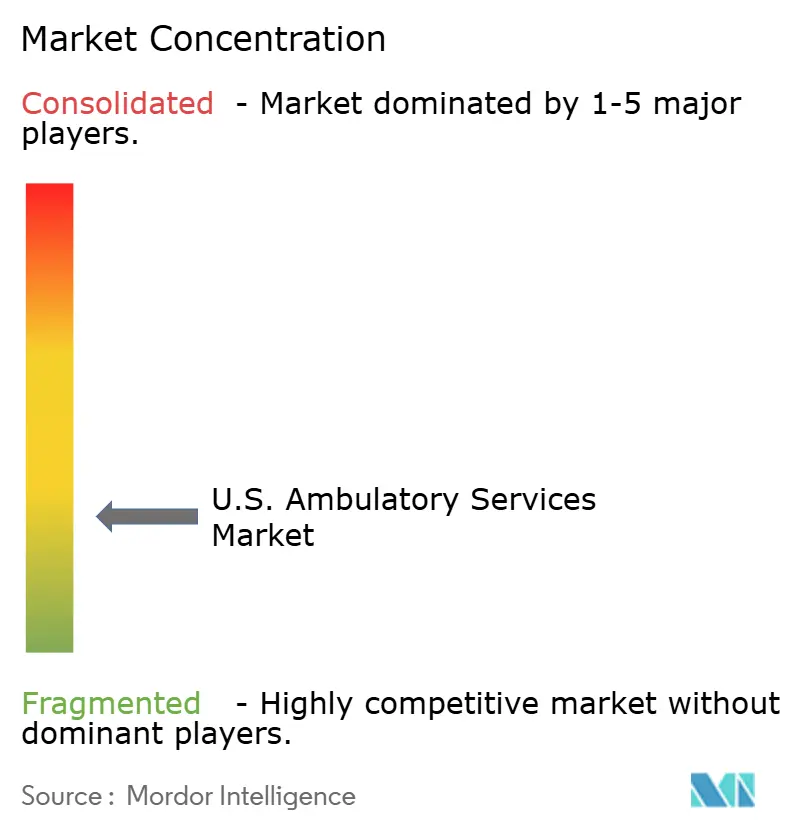

While the United States ambulatory services market remains fragmented at the facility level, consolidation is progressing rapidly at the platform level. A significant portion of freestanding ASCs continues to operate independently. However, four to five scaled platforms now command a substantial share of the national procedure volume. Key players like USPI, SCA Health, Surgery Partners, and the proposed merger of Ascension with AMSURG are pivotal in shaping both national scale and regional density. Ascension Health's proposed USD 3.9 billion acquisition of AMSURG is set to expand Ascension’s ASC footprint from 58 to over 300 centers across 34 states, significantly enhancing its national presence. This highlights a shift in consolidation focus from individual facility roll-ups to the assembly of scaled networks.

USPI exemplifies the platform strategy dominating the United States ambulatory services market. In 2025, USPI generated over USD 5.1 billion in ambulatory revenue and expanded its reach by adding 35 facilities, supported by nearly USD 350 million in capital investments. Surgery Partners is also scaling, with full-year 2025 revenue of USD 3.3 billion and projected 2026 revenue between USD 3.35 billion and USD 3.45 billion. These operators compete through local physician partnerships, diverse case mixes, new developments, and the capacity to handle more complex procedures. Health systems are increasingly entering the competition via joint ventures rather than direct ownership, further intensifying the competitive landscape in a widely dispersed market.

U.S. Ambulatory Services Industry Leaders

SCA Health

Surgery Partners

HCA Healthcare Surgery Ventures

AMSURG

American Family Care

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Sutter Health and Allina Health signed a letter of intent for a proposed USD 26 billion system merger, creating a portfolio of nearly 45 ASCs and planning a USD 2 billion investment in new ambulatory care sites in Minnesota and western Wisconsin.

- December 2025: Cencora completed the acquisition of the remaining controlling interest in OneOncology from TPG for approximately USD 5 billion, valuing the enterprise at USD 7.4 billion and consolidating one of the largest community-based ambulatory oncology networks in the country.

- November 2025: CMS released the CY 2026 OPPS/ASC Final Rule, adding 573 new codes to the ASC Covered Procedures List, including cardiac ablations and lumbar spine procedures, initiating a 3-year IPO list phase-out, and increasing ASC payment rates by 2.6%.

U.S. Ambulatory Services Market Report Scope

As per the scope of the report, Ambulatory services (commonly referred to as ambulatory care or outpatient care) are medical services provided on an outpatient basis without requiring an overnight hospital stay.

The U.S. Ambulatory Services Market is segmented by care setting, service type, specialty, and ownership model. By care setting, the market includes primary care clinics, surgical specialty clinics, urgent care centers, freestanding emergency departments, diagnostic imaging centers, specialty clinics, home healthcare agencies, and telehealth and virtual clinics. By service type, the market is segmented into diagnosis, observation and consultation, treatment, wellness and preventive care, and rehabilitation. By specialty, the market is categorized into primary care, orthopedics, ophthalmology, gastroenterology, cardiovascular, pain management, nephrology and dialysis, dermatology, oncology, behavioral health, women’s health, and dental and oral surgery. By ownership model, the market is segmented into physician-owned, hospital or health-system-owned, corporate or private-equity-owned, and joint ventures. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Primary Care Clinics |

| Surgical Specialty Clinics |

| Urgent Care Centers |

| Freestanding Emergency Departments |

| Diagnostic Imaging Centers |

| Specialty Clinics |

| Home Healthcare Agencies |

| Telehealth and Virtual Clinics |

| Diagnosis |

| Observation and Consultation |

| Treatment |

| Wellness and Preventive Care |

| Rehabilitation |

| Primary Care |

| Orthopedics |

| Ophthalmology |

| Gastroenterology |

| Cardiovascular |

| Pain Management |

| Nephrology and Dialysis |

| Dermatology |

| Oncology |

| Behavioral Health |

| Women's Health |

| Dental and Oral Surgery |

| Physician-Owned |

| Hospital or Health-System-Owned |

| Corporate or Private-Equity-Owned |

| Joint Ventures |

| By Care Setting | Primary Care Clinics |

| Surgical Specialty Clinics | |

| Urgent Care Centers | |

| Freestanding Emergency Departments | |

| Diagnostic Imaging Centers | |

| Specialty Clinics | |

| Home Healthcare Agencies | |

| Telehealth and Virtual Clinics | |

| By Service Type | Diagnosis |

| Observation and Consultation | |

| Treatment | |

| Wellness and Preventive Care | |

| Rehabilitation | |

| By Specialty | Primary Care |

| Orthopedics | |

| Ophthalmology | |

| Gastroenterology | |

| Cardiovascular | |

| Pain Management | |

| Nephrology and Dialysis | |

| Dermatology | |

| Oncology | |

| Behavioral Health | |

| Women's Health | |

| Dental and Oral Surgery | |

| By Ownership Model | Physician-Owned |

| Hospital or Health-System-Owned | |

| Corporate or Private-Equity-Owned | |

| Joint Ventures |

Key Questions Answered in the Report

What is the size of the US ambulatory services sector in 2026 and 2031?

The US ambulatory services market size stands at USD 399.50 billion in 2026 and is projected to reach USD 442.37 billion by 2031, growing at a 5.45% CAGR during 2026-2031.

Which care setting is growing the fastest in outpatient services?

Telehealth and Virtual Clinics are the fastest-growing care setting, with a projected 7.23% CAGR through 2031, supported by extended Medicare telehealth flexibilities through December 2027.

Which service type contributes the most revenue in ambulatory care?

Treatment is the largest service type, accounting for 42.75% of revenue in 2025, reflecting the stronger reimbursement profile of procedural outpatient care.

Which specialty has the strongest growth outlook through 2031?

Oncology is projected to grow the fastest at an 8.42% CAGR through 2031, supported by ambulatory infusion expansion and nearly 2.04 million new U.S. cancer diagnoses in 2025.

What is driving the shift from inpatient to outpatient services in the United States?

The biggest drivers are CMS procedure migration policies, payer steerage to lower-cost sites, aging-related chronic disease demand, and wider use of minimally invasive and digital technologies.

What are the main risks facing outpatient care providers through 2031?

The main risks are workforce shortages, clinician burnout, regulatory complexity, reimbursement variability, and revenue-cycle disruption linked to cybersecurity events such as the Change Healthcare incident.

Page last updated on: