United States Hemodialysis And Peritoneal Dialysis Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

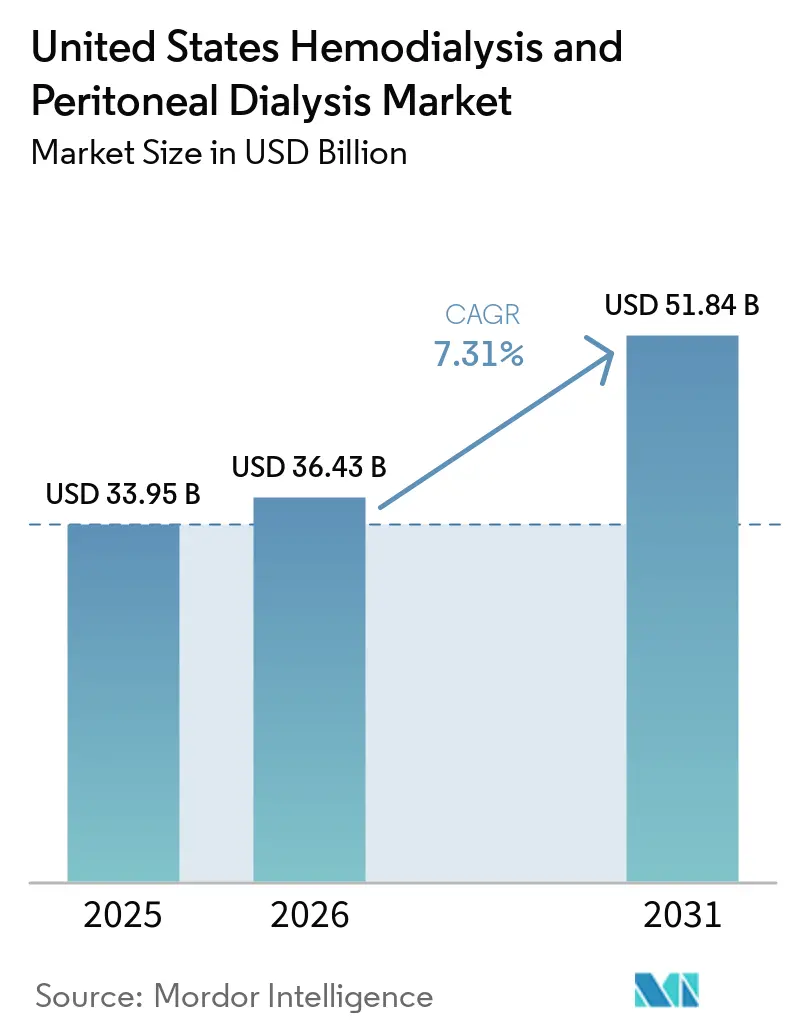

| Base Year Market Size (2025) | USD 33.95 Billion |

| Market Size (2026) | USD 36.43 Billion |

| Market Size (2031) | USD 51.84 Billion |

| Growth Rate (2026 - 2031) | 7.31% CAGR |

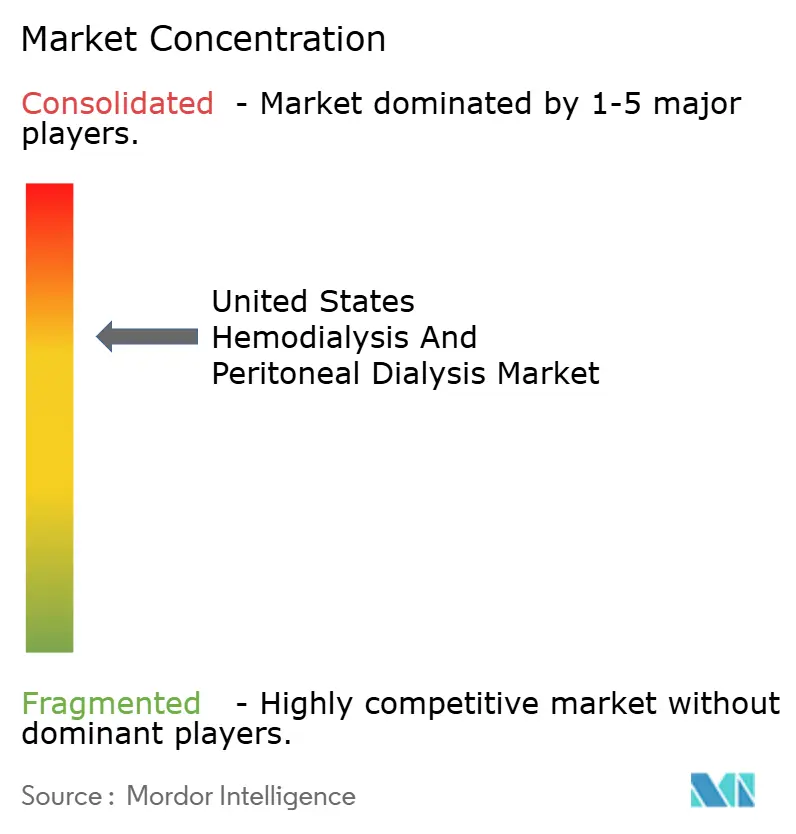

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Hemodialysis And Peritoneal Dialysis Market Analysis by Mordor Intelligence

The United States Hemodialysis And Peritoneal Dialysis Market size was valued at USD 33.95 billion in 2025 and is estimated to grow from USD 36.43 billion in 2026 to reach USD 51.84 billion by 2031, at a CAGR of 7.31% during the forecast period (2026-2031).

The United States (US) hemodialysis and peritoneal dialysis market rests on a treatment-dependent patient pool, with 857,305 Americans living with end-stage kidney disease and 560,230 on dialysis as of June 30, 2025, while new incident cases add close to 135,000 patients each year. Demand in the US hemodialysis and peritoneal dialysis market remains steady because dialysis is essential therapy rather than an elective service, which keeps utilization resilient across broader economic cycles. The US hemodialysis and peritoneal dialysis market also benefits from USD 130 billion in annual Medicare spending on kidney disease, equal to 24% of total Medicare outlays even though ESKD affects 1% of beneficiaries. Hemodialysis still anchors the current revenue base, while policy support for home treatment, connected device upgrades, and value-based kidney care are widening the commercial opportunity set for home-capable platforms and recurring consumables. The end of the ETC model on December 31, 2025 also showed that care-site behavior does not move easily through payment pressure alone, so the next phase of the US hemodialysis and peritoneal dialysis market is more likely to be shaped by workflow-ready technology, interoperability, and operator execution than by blunt reimbursement incentives.

Key Report Takeaways

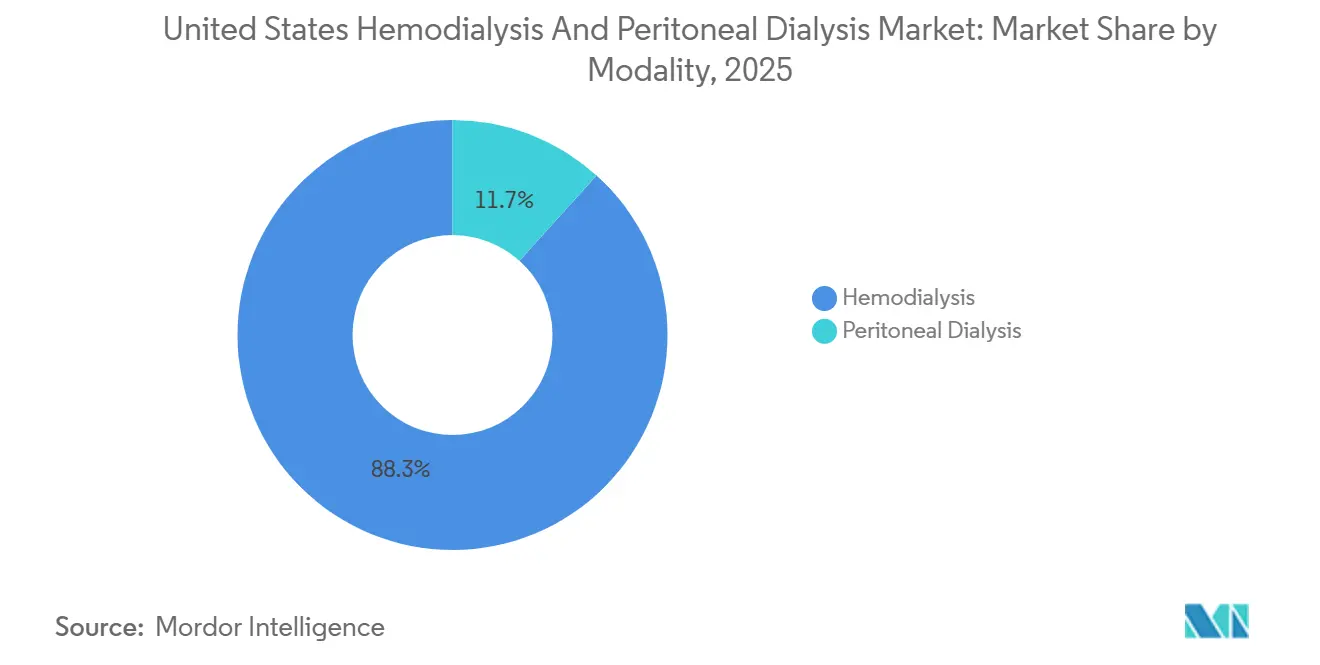

- By modality, hemodialysis led with 88.31% revenue share in 2025, while peritoneal dialysis is forecast to expand at an 8.38% CAGR through 2031.

- By product and service, services held 68.24% revenue share in 2025, while consumables are projected to grow at an 8.52% CAGR through 2031.

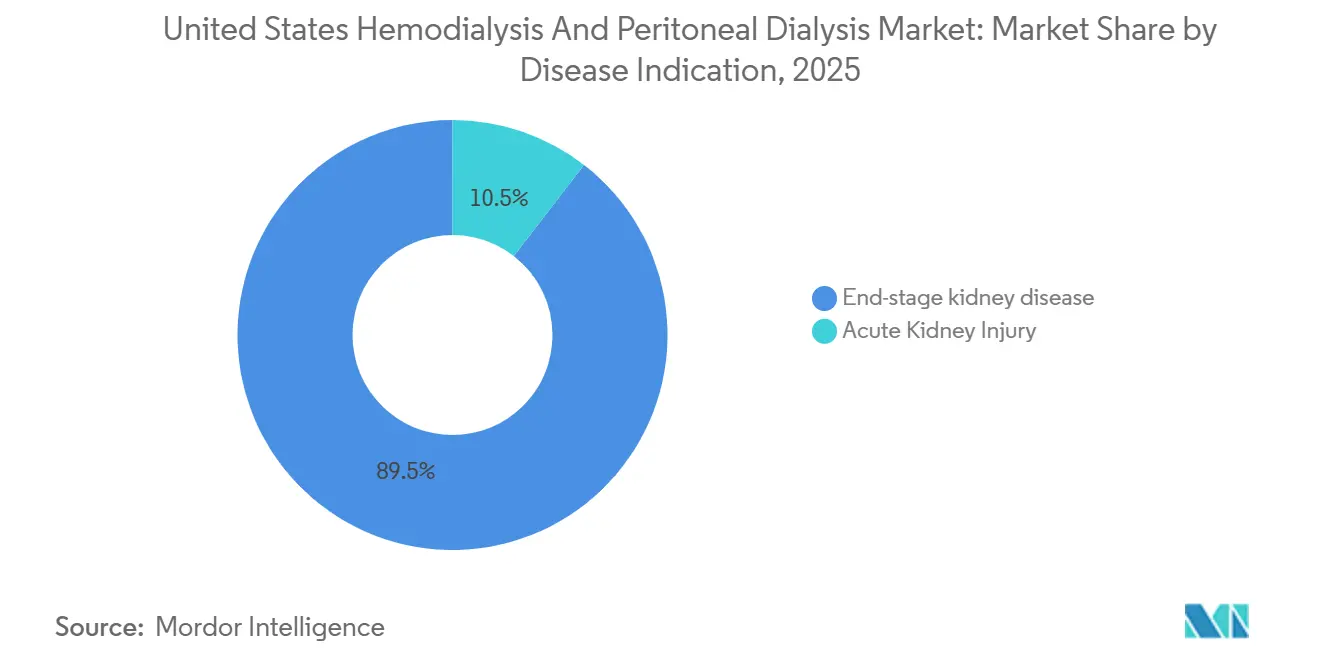

- By disease indication, ESKD and CKD accounted for 89.52% of revenue in 2025 and also recorded the highest projected CAGR at 8.25% through 2031.

- By end-use setting, hospital-based dialysis centers captured 78.54% revenue share in 2025, while home care settings are advancing at an 8.83% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Hemodialysis And Peritoneal Dialysis Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising ESKD Burden From Diabetes And Hypertension | +2.1% | National, with highest incidence in the South and Southeast including Alabama, Mississippi, and Louisiana | Long term (≥ 4 years) |

| Home Dialysis Adoption And Reimbursement Support | +1.4% | National, with urban regions ahead and rural adoption accelerating | Medium term (2-4 years) |

| Kidney Transplant Shortage Sustaining Dialysis Demand | +0.9% | National, with transplant access disparities largest in the Southeast and rural Midwest | Long term (≥ 4 years) |

| Connected Dialysis And Therapy Upgrade Cycle | +0.8% | Concentrated in large integrated delivery networks in the Northeast, Mid-Atlantic, and West Coast | Medium term (2-4 years) |

| AKI Home Dialysis Reimbursement Expansion | +0.5% | National, with early gains in the Southeast and urban academic medical centers | Short term (≤ 2 years) |

| Medicare Advantage And Value-Based Kidney Care Steering | +0.6% | National, with stronger activity in Florida, Texas, and California | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising ESKD Burden from Diabetes and Hypertension

Diabetic nephropathy and hypertensive renal disease continue to feed the core treatment pipeline for the US hemodialysis and peritoneal dialysis market. The United States recorded 135,000 new ESKD cases in 2025, and CKD affected 15% of U.S. adults, which leaves a large upstream pool at risk of progression into long-duration dialysis care[1]National Institute of Diabetes and Digestive and Kidney Diseases, “Kidney Disease Statistics for the United States,” NIDDK, niddk.nih.gov. Incident ESKD among Black Americans runs at 3.8 times the rate seen among White Americans, and the heaviest burden remains concentrated in states with weaker chronic disease management capacity. That racial and regional concentration means the US hemodialysis and peritoneal dialysis market continues to expand even when providers add transplant referrals or improve screening. The emerging benefit from GLP-1 therapies is real, but Fresenius still framed that effect as a long-range factor rather than a near-term volume reset for 2026 through 2031.

Home Dialysis Adoption and Reimbursement Support

CMS widened support for home treatment when it extended Medicare payment for dialysis in the home setting to beneficiaries with acute kidney injury beginning January 1, 2025. The rule also allowed ESRD facilities to bill the home and self-dialysis training add-on payment for AKI beneficiaries, and the training add-on was set at USD 95.6 per session in the final rule. Vantive linked its Sharesource remote monitoring platform with lower all-cause mortality and fewer hospitalizations, which broadens the case for home modalities beyond patient convenience alone. CMS also expanded TPNIES eligibility to certain home dialysis machines and set payment at 65% of the MAC-determined pre-adjusted price, reduced by a USD 9.32 offset, for 2 calendar years. Together, those changes lower adoption friction and support a larger installed base for the US hemodialysis and peritoneal dialysis market in home settings.

Kidney Transplant Shortage Sustaining Dialysis Demand

The transplant bottleneck continues to support the volume floor of the US hemodialysis and peritoneal dialysis market. The United States completed 27,573 kidney transplants in 2025, which was 102 fewer than in 2024 and marked a rare annual decline outside pandemic disruption[2]United Network for Organ Sharing, “U.S. Surpasses 49,000 Organ Transplants While Deceased Organ Donations Dip,” UNOS, unos.org. HHS OIG reported that more than 90,000 people remained on the kidney waitlist and only 15% received a donated kidney, which leaves dialysis as the default therapy for most patients who progress to advanced disease. NIDDK reported all-cause mortality of 74.3 per 1,000 patient-years for kidney transplant recipients versus 187.7 for dialysis patients, which shows how strongly transplant scarcity extends dialysis exposure. Because supply-side transplant capacity remains tight, the demand base for the US hemodialysis and peritoneal dialysis market is likely to remain structurally supported throughout the forecast period.

Connected Dialysis and Therapy Upgrade Cycle

The US hemodialysis and peritoneal dialysis market is entering a replacement cycle driven by clinical performance, cybersecurity, and workflow requirements rather than simple equipment age. Fresenius received FDA clearance for the HDF-capable 5008X CAREsystem in May 2025, began introducing the therapy in select U.S. clinics in the second half of 2025, and is converting 20% of its U.S. installed base in 2026 across 28 states while training more than 7,200 nurses and technicians and transitioning 36,000 patients. Fresenius tied that rollout to CONVINCE trial evidence that high-volume hemodiafiltration delivered a 23% lower all-cause mortality rate than conventional hemodialysis. Outset’s next-generation Tablo cleared the FDA in January 2026 as the first hemodialysis platform built to the FDA’s June 2025 cybersecurity standards, and shipments begin in the second quarter of 2026. Nikkiso also entered the cycle with the DBB-06 PRO launch in December 2025, adding full-assist functionality that automates priming and blood-return procedures for facilities facing staffing pressure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reimbursement-Cost Mismatch For Providers | -1.2% | National, most acute for independent freestanding centers in high-wage metropolitan areas | Medium term (2-4 years) |

| Nephrology Nursing And Technician Shortage | -0.9% | National, most severe in rural Southeast and Midwest where pipeline programs are thinnest | Long term (≥ 4 years) |

| PD Fluid Supply Fragility | -0.4% | National, with concentrated vulnerability in markets dependent on a single domestic supplier | Short term (≤ 2 years) |

| Oral Phosphate-Binder Bundle Workflow Burden | -0.3% | National, with disproportionate impact on smaller freestanding centers that have fewer pharmacist resources | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Reimbursement-Cost Mismatch for Providers

The 2026 ESRD PPS base rate was finalized at USD 281.7 per treatment, which was a 2.2% increase from 2025. DaVita reported patient care costs per treatment of USD 273.3 in 2025 and USD 280.1 in the first quarter of 2026, which shows how quickly provider costs moved toward the reimbursement ceiling. This pressure is harder for independent freestanding centers because they do not have the same purchasing leverage, balance sheet strength, or vertical supply integration as the largest operators. Fresenius also highlighted projected Medicaid funding cuts through 2034 as a secondary risk for centers that serve dually eligible patients in greater proportions. If that mismatch persists, the US hemodialysis and peritoneal dialysis market could see slower investment in new equipment, tighter center economics, and a faster gap between national chains and smaller providers.

Nephrology Nursing and Technician Shortage

Workforce limits remain a real brake on the US hemodialysis and peritoneal dialysis market because machines and policy changes still need trained staff to turn into treatment capacity. DaVita reported a broad investment in workforce development, including close to USD 1 million in scholarships for 370 nurses by July 2025 and support for more than 2,400 teammates through its Bridge to Your Dreams program. Fresenius is training more than 7,200 nurses and technicians for its 2026 HDF rollout, which shows how strongly human capital availability affects even well-funded technology programs. Nikkiso’s DBB-06 PRO was launched with full-assist functionality that automates routine treatment steps, and that kind of automation directly addresses staff burden where hiring remains difficult. The staffing gap is therefore not only a labor issue but also a factor that shapes which providers in the US hemodialysis and peritoneal dialysis market can scale new modalities fast enough to capture growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Modality: In-Center Hemodialysis Still Commands Volume, But Home PD Rewrites Margins

Hemodialysis held 88.31% of the US hemodialysis and peritoneal dialysis market share in 2025, which reflects the installed clinical base, long-standing physician familiarity, and payer workflows built around in-center treatment. The modality also remains central to equipment replacement because Fresenius began commercial rollout of the 5008X CAREsystem in the United States after FDA clearance in May 2025. Fresenius is converting 20% of its U.S. installed base in 2026 and aims to replace the full installed base with the 5008X by the end of 2030, which keeps hemodialysis clinically current rather than operationally static. That matters because high-volume hemodiafiltration gives the hemodialysis segment a clinical upgrade path at the same time that providers face pressure to improve outcomes and staffing efficiency.

Peritoneal dialysis remains the smaller modality, but its 8.38% CAGR makes it the faster-moving part of the US hemodialysis and peritoneal dialysis industry through 2031. The shift is supported by home treatment policy, remote monitoring, and the practical need to move appropriate patients away from fixed in-center schedules. CMS strengthened that direction by extending home dialysis payment to AKI beneficiaries and by continuing support mechanisms for home equipment through TPNIES. Vantive also said Sharesource has supported more than 100 million home dialysis treatments globally, which shows how remote patient management is moving from a helpful feature to a routine care tool. The CMS update to Kt/V adequacy measures for payment year 2027 adds separate reporting expectations for HD and PD, which means modality growth in the US hemodialysis and peritoneal dialysis market now sits alongside tighter performance visibility.

By Product & Service: Services Anchor Revenue, Consumables Fuel Growth

Services accounted for 68.24% of revenue in 2025, so the largest share of the US hemodialysis and peritoneal dialysis market still comes from treatment delivery rather than device sales. That structure favors large operators because scale supports billing, labor deployment, and payer contracting across thousands of treatment sites. DaVita reported average revenue per treatment of USD 417.6 in the first quarter of 2026, which shows that service revenue remains the core earnings driver even in a cost-sensitive environment. The service-heavy mix also explains why provider strategy in the US hemodialysis and peritoneal dialysis market increasingly focuses on center productivity, patient retention, and risk-based care management rather than simple unit expansion.

Consumables are the faster-growth layer, with the US hemodialysis and peritoneal dialysis market size for consumables projected to expand at 8.52% CAGR through 2031. That growth comes from recurring treatment use, especially as home schedules can require more frequent sessions than the standard in-center pattern. Outset reported that consumables and services made up 70% of revenue in the first quarter of 2026, which shows how installed-base monetization is becoming a major commercial lever. Rockwell reinforced that theme when it launched a single-use bicarbonate cartridge in February 2025 to target a USD 100 million disposables sub-market. Devices still matter because connected HDF and home-capable platforms create multi-year replacement demand, but the margin logic in the US hemodialysis and peritoneal dialysis industry is moving more clearly toward recurring supplies and associated services.

By Disease Indication: ESKD and CKD Drive Both Volume and Growth

ESKD and CKD accounted for 89.52% of revenue in 2025, and this segment is also forecast to grow at 8.25% CAGR through 2031. That combination is unusual in a mature healthcare category because the largest segment is also the fastest-growing one. The US hemodialysis and peritoneal dialysis market size for ESKD and CKD remains supported by a growing treatment population, with 857,305 Americans living with ESKD and incident cases adding close to 135,000 patients each year. Because transplant supply has not kept pace, the chronic disease segment continues to generate the longest and most predictable treatment exposure in the US hemodialysis and peritoneal dialysis market.

The AKI segment still matters, but its commercial scale depends more on pathway redesign than on disease burden alone. CMS widened the addressable base by allowing home dialysis billing for AKI patients, which gives providers and device makers a new reimbursement-supported route outside the inpatient setting. Even so, the pace of growth depends on whether facilities build protocols that support discharge, training, and follow-up without compromising care continuity. This means AKI is a meaningful adjacency for the US hemodialysis and peritoneal dialysis market, but it does not displace the central role of CKD progression in driving long-run demand. The result is a disease mix where chronic kidney failure remains the dominant base and acute kidney injury adds targeted new opportunities rather than a broad reset of market structure.

By End-use Setting: Hospital Bases Dominate Today, While Home Settings Gain Momentum

Hospital-based dialysis centers held 78.54% of revenue in 2025, which shows how much of the US hemodialysis and peritoneal dialysis market remains tied to established inpatient and hospital-linked care pathways. That position is reinforced by the complexity of advanced renal care, referral patterns, and the concentration of specialist teams in hospital systems. Freestanding centers still handle a large share of chronic outpatient hemodialysis volume, with DaVita alone operating 2,666 U.S. outpatient dialysis centers as of March 31, 2026. The scale of those networks keeps hospital-linked and freestanding delivery central to the US hemodialysis and peritoneal dialysis market even as care models begin shifting toward the home. Smaller freestanding operators, however, are more exposed to reimbursement-cost pressure because they do not have the same ability to spread labor and procurement costs across large national footprints.

Home care settings are the fastest-growing end-use segment at 8.83% CAGR, and that is where the directional change in the US hemodialysis and peritoneal dialysis market is most visible. Fresenius said 16% of its U.S. treatments were delivered at home in 2025, and more than 15,300 U.S.-based patients used its NxStage portable home hemodialysis system, up 6% from 2024. CMS support for AKI home dialysis, the TPNIES pathway for home machines, and stronger remote monitoring tools all make that setting easier to scale than it was a few years ago. Skilled nursing and long-term care settings still present an underdeveloped opportunity, especially for portable and workflow-light systems that can operate with less fixed infrastructure. That shift does not remove the importance of hospitals, but it does make end-use diversification a defining feature of the US hemodialysis and peritoneal dialysis market through 2031.

Geography Analysis

The US hemodialysis and peritoneal dialysis market does not split into country-level regions, but regional demand differences still shape where treatment volume, labor stress, and growth opportunities concentrate. The South and Southeast carry the heaviest ESKD burden, with states such as Alabama, Mississippi, Louisiana, Georgia, and Texas facing above-average exposure to diabetes and hypertension. CMS data also showed AKI rates of 108.8 per 1,000 person-years among Black Medicare beneficiaries in high-burden areas, which points to a concentrated regional need for both chronic and acute dialysis services. Large providers maintain broad coverage in these regions, and DaVita’s national network of 2,666 U.S. outpatient centers gives it direct exposure to the biggest regional treatment pools[3]DaVita Inc., “1st Quarter 2026 Results,” DaVita, davita.com.

The Northeast and Mid-Atlantic remain important because they host dense academic medical centers, hospital-based dialysis programs, and integrated kidney care operations. That concentration supports earlier adoption of advanced modalities, more organized transition planning, and stronger ability to test new reimbursement-linked workflows. The same regions are well positioned for connected therapy upgrades because large systems can absorb training, data integration, and procurement change more quickly than fragmented local providers. Non-contiguous areas such as Alaska, Hawaii, and U.S. Pacific territories received a Non-Contiguous Areas Payment Adjustment of up to 25% on the non-labor portion of ESRD PPS payments in the 2026 final rule, which reflects persistent operating cost disparities in those geographies.

The West has become an active battleground for home dialysis and independent supply growth inside the US hemodialysis and peritoneal dialysis market. Rockwell added 30 new customers in the Western United States in the fourth quarter of 2025, and the region moved to more than 10% of its customer clinic footprint. That shift shows how supplier relationships can move quickly when competitors exit or when health systems seek more resilient procurement options. Western urban markets also fit the operating logic of home dialysis because provider density, logistics support, and technology readiness are generally stronger than in thinner rural networks. The same regional mix makes the West a practical test bed for connected devices, portable treatment models, and consumables-led revenue strategies. Taken together, regional differences do not create separate national submarkets, but they do shape how fast providers can expand the US hemodialysis and peritoneal dialysis market across modality, setting, and supplier categories.

Competitive Landscape

The US hemodialysis and peritoneal dialysis market is concentrated at the service-delivery level. This concentration gives the largest operators unusual control over treatment capacity, payer relationships, clinical protocol rollout, and equipment purchasing. Even so, the strategic paths of the leading companies are separating rather than converging. Fresenius is leaning into clinical differentiation through HDF and installed-base renewal, while DaVita is pushing harder into integrated kidney care and risk-based coordination.

Fresenius has made one of the clearest strategic moves in the US hemodialysis and peritoneal dialysis market by launching the 5008X CAREsystem across 28 states in 2026, training more than 7,200 nurses and technicians, and transitioning 36,000 patients while rationalizing lower-performing clinics. DaVita’s main move has been the expansion of integrated kidney care, with 62,600 patients in risk-based arrangements and USD 5.4 billion in annualized medical spend under management as of March 2026. DaVita also said its Integrated Kidney Care segment became profitable for the first time in 2025, which gives it a clearer economic base for value-based care expansion. The difference is important because one company is using clinical platform renewal to defend center economics, while the other is using care coordination and risk management to widen its role around the dialysis episode.

The challenger set is also becoming more technology focused. Outset received FDA clearance in January 2026 for its next-generation Tablo platform, which the company said was the first hemodialysis system designed to meet the FDA’s June 2025 cybersecurity standards and was scheduled to begin shipping in the second quarter of 2026. Nikkiso launched the DBB-06 PRO in December 2025 with full-assist workflow automation, which targets facilities that need lower staff burden without sacrificing treatment capability. Rockwell has responded through supply continuity and consumables expansion, including multi-year agreements with Innovative Renal Care and an extension with one of the largest dialysis providers in the country. Fresenius disclosed 7,890 active patents in its renal care portfolio, which shows that intellectual property remains a serious competitive tool alongside service scale. As a result, competition in the US hemodialysis and peritoneal dialysis market is no longer defined only by center count, because cybersecurity readiness, workflow automation, remote connectivity, and recurring supply economics are becoming equally important.

United States Hemodialysis And Peritoneal Dialysis Industry Leaders

Fresenius Medical Care AG

DaVita Inc.

U.S. Renal Care, Inc.

Innovative Renal Care

Dialysis Clinic, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Rockwell Medical signed a 3-year product purchase agreement with Heritage Dialysis, Michigan-based home dialysis provider, to supply PureCart bicarbonate cartridges, RenalPure, and SteriLyte, further expanding the company's home dialysis consumables footprint.

- March 2026: Mozarc Medical partnered with the Fetal Health Foundation to advance its Carpediem pediatric dialysis machine for neonatal AKI, expanding the company's U.S. clinical reach beyond adult chronic kidney care.

- January 2026: Outset Medical received FDA 510(k) clearance for its next-generation Tablo hemodialysis platform, the first HD system cleared under the FDA's June 2025 cybersecurity guidance, with shipments commencing in Q2 2026, enabling healthcare providers to insource dialysis with enterprise-grade security and EMR interoperability.

- December 2025: Nikkiso launched its DBB-06 PRO, the first FDA-cleared U.S. hemodialysis machine with full-assist functionality, D-FAS, that automates priming and blood-return procedures, reducing healthcare worker burden and procedural errors in dialysis facilities facing staffing shortages.

United States Hemodialysis And Peritoneal Dialysis Market Report Scope

As per the scope of the report, hemodialysis is a medical procedure that removes waste products, excess fluid, and toxins from the blood when the kidneys are no longer able to perform these functions effectively. Peritoneal Dialysis is a type of dialysis that uses the lining of the abdomen (peritoneum) as a natural filter. A special solution called dialysate is introduced into the abdominal cavity through a catheter.

The segmentation for the United States hemodialysis and peritoneal dialysis market is categorized by modality, product and service, disease indication, and end-use setting. By modality, the market is divided into hemodialysis and peritoneal dialysis. By product and service, it includes devices, consumables, and services. By disease indication, the segmentation covers end-stage kidney disease/chronic kidney disease (CKD) and acute kidney injury. By end-use setting, the market is segmented into freestanding dialysis centers, hospital-based dialysis centers, home care settings, and skilled nursing and long-term care settings. For each segment, the market size and forecast are provided in terms of value (USD).

| Hemodialysis |

| Peritoneal Dialysis |

| Devices |

| Consumables |

| Services |

| End-stage Kidney Disease/CKD |

| Acute Kidney Injury |

| Freestanding Dialysis Centers |

| Hospital-based Dialysis Centers |

| Home Care Settings |

| Skilled Nursing and Long-term Care Settings |

| By Modality | Hemodialysis |

| Peritoneal Dialysis | |

| By Product & Service | Devices |

| Consumables | |

| Services | |

| By Disease Indication | End-stage Kidney Disease/CKD |

| Acute Kidney Injury | |

| By End-use Setting | Freestanding Dialysis Centers |

| Hospital-based Dialysis Centers | |

| Home Care Settings | |

| Skilled Nursing and Long-term Care Settings |

Key Questions Answered in the Report

What is the current size of the U.S. dialysis sector for hemodialysis and peritoneal dialysis?

It stood at USD 36.43 billion in 2026 and is projected to reach USD 51.84 billion by 2031 at a 7.31% CAGR.

Which treatment type grows faster in the United States, hemodialysis or peritoneal dialysis?

Peritoneal dialysis grows faster, with an 8.38% CAGR through 2031, even though hemodialysis still held 88.31% of revenue in 2025.

Why does demand remain stable even during economic pressure?

Dialysis is non-discretionary care for patients with advanced kidney failure, so treatment demand is tied to medical need rather than consumer spending cycles.

What is pushing home treatment uptake in renal care?

CMS support for home dialysis in AKI, TPNIES support for home machines, and remote monitoring platforms are making home care more practical and more scalable.

Which patient group drives most revenue growth?

ESKD and CKD patients are the main driver, accounting for 89.52% of revenue in 2025 and the fastest disease-segment CAGR of 8.25% through 2031.

Page last updated on: