Hemodialysis Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.44 Billion |

| Market Size (2031) | USD 8.32 Billion |

| Growth Rate (2026 - 2031) | 5.25% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hemodialysis Services Market Analysis by Mordor Intelligence

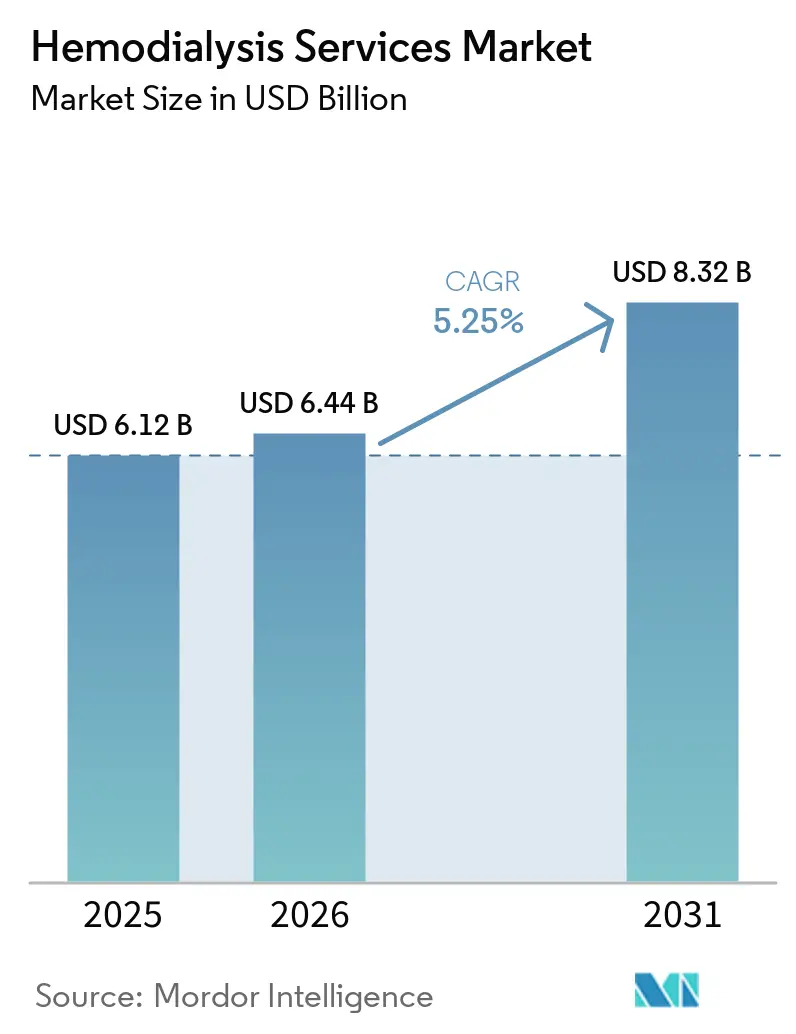

The Hemodialysis Services Market size was valued at USD 6.12 billion in 2025 and is estimated to grow from USD 6.44 billion in 2026 to reach USD 8.32 billion by 2031, at a CAGR of 5.25% during the forecast period (2026-2031).

The market continues to rest on a chronic treatment base because patients with end-stage renal disease usually require 3 dialysis sessions each week for life unless they receive a transplant, and transplant supply remains below patient need. In the United States alone, there are nearly 135,000 new ESRD cases each year and 857,305 people are living with the condition, which keeps treatment volumes firm even when providers face operating pressure. Public reimbursement systems also give the hemodialysis services market a stable payment base, with the CY 2026 ESRD Prospective Payment System supporting nearly 7,600 certified facilities and projected federal payments of USD 6 billion. At the same time, operators are finding fresh room for expansion as home therapy platforms improve monitoring and prescription management, which supports a gradual shift toward lower-cost care models outside the clinic. Competitive strategy in the hemodialysis services market is therefore moving in 2 directions at once, with some providers tightening clinic footprints to protect margins while others invest in digital tools, home programs, and care redesign to capture future demand.

Key Report Takeaways

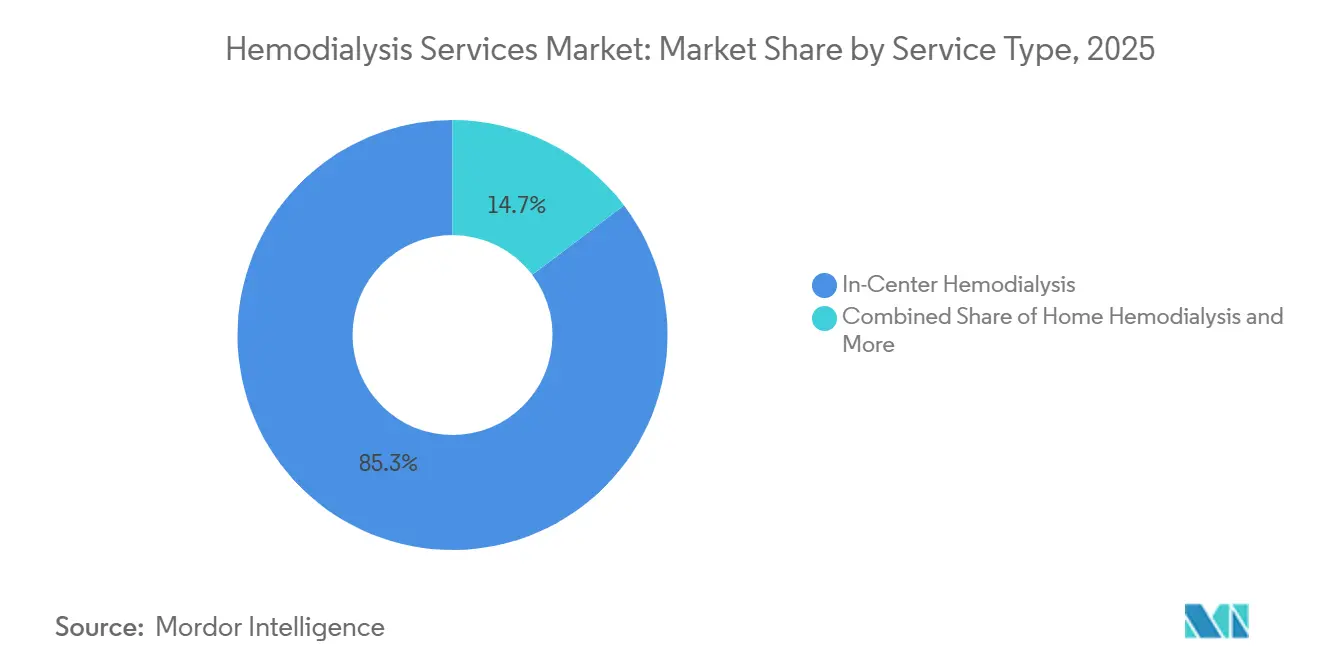

- By service type, in-center hemodialysis led with 85.31% revenue share in 2025, while home hemodialysis is forecast to expand at an 8.38% CAGR through 2031.

- By end user, dialysis centers held 83.24% of revenue in 2025, while home care settings are projected to record a CAGR at 8.52% through 2031.

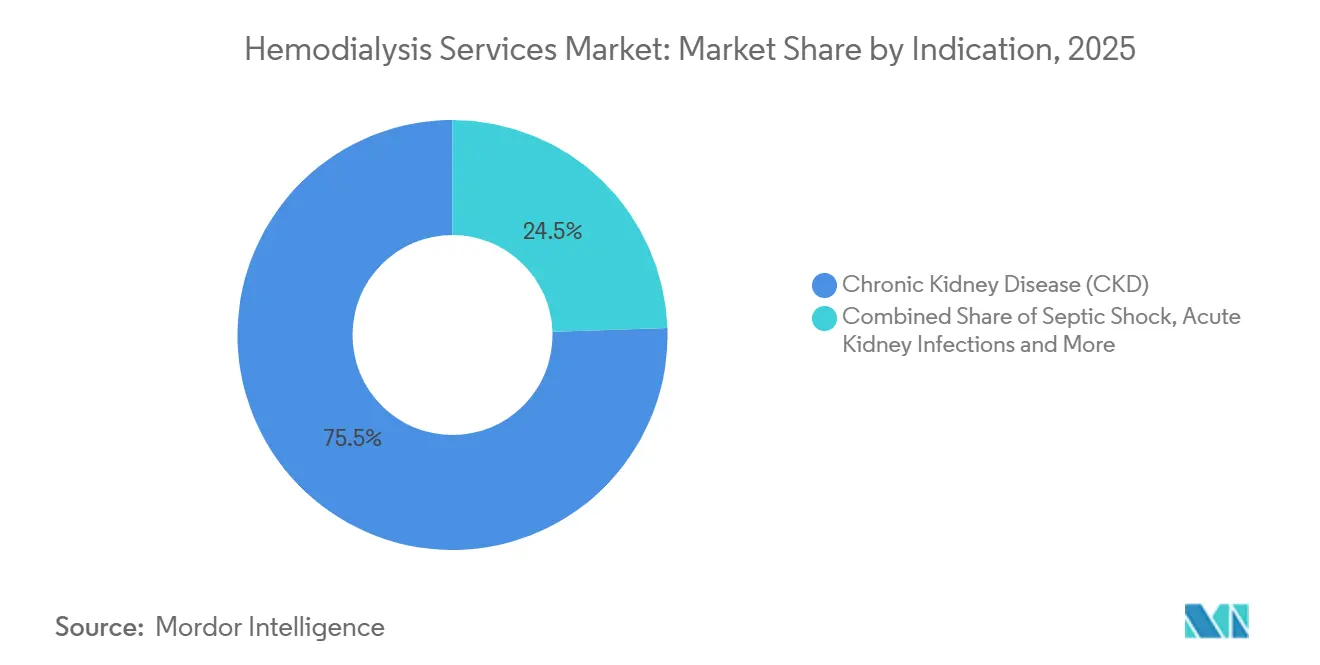

- By indication, chronic kidney disease accounted for 75.52% of revenue in 2025, while septic shock is expected to advance at a 6.25% CAGR through 2031.

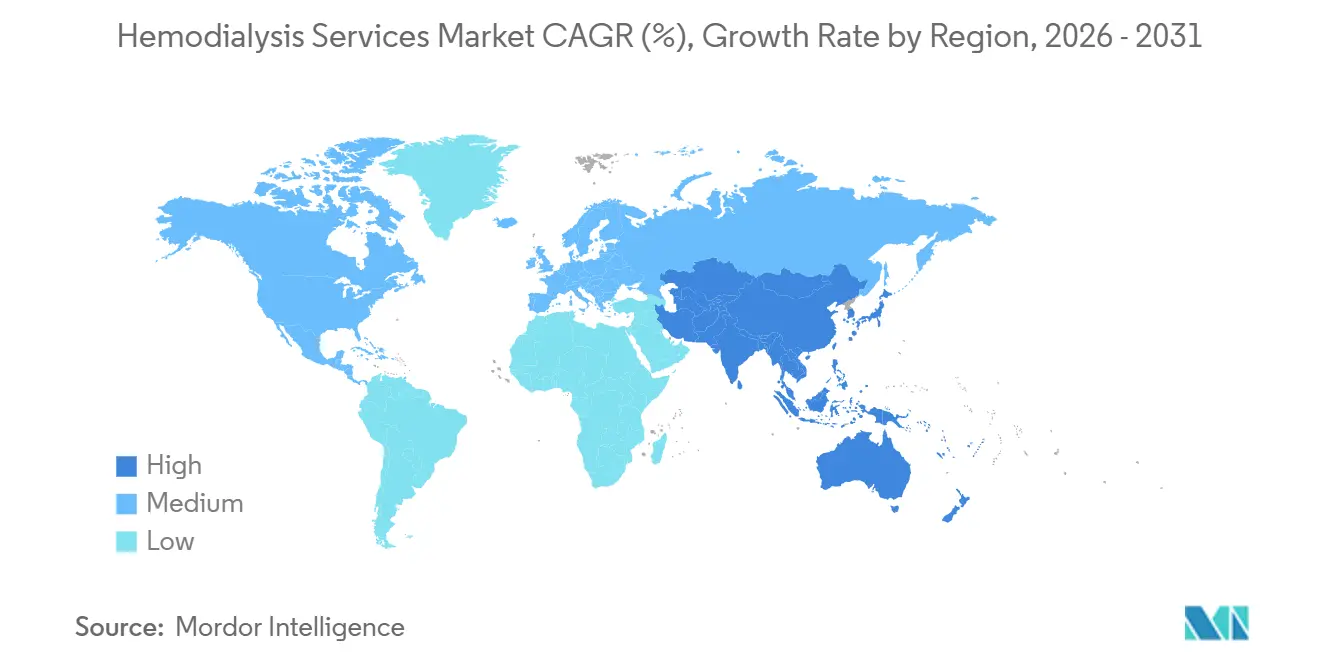

- By geography, North America held 38.22% revenue share in 2025, while Asia-Pacific is projected to grow at a 7.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hemodialysis Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising ESRD Burden and CKD Progression | +1.8% | Global, concentrated in APAC, North America, and MENA | Long term (≥ 4 years) |

| Expanding Medicare and National Dialysis Reimbursement Coverage | +1.3% | North America primary, with spillover to APAC national schemes | Medium term (2-4 years) |

| Shift Toward Home Hemodialysis and Remote Monitoring | +0.8% | North America, Europe, and early gains in APAC | Medium term (2-4 years) |

| Expansion of Center Networks in Urban and Tier-2 Catchments | +0.6% | APAC core, with spillover to MEA and South America | Medium term (2-4 years) |

| Hemodiafiltration Upgrade Cycle in Installed Base Markets | +0.5% | North America and Europe | Short term (≤ 2 years) |

| Telehealth-Led Staffing Efficiency and Lower Chair Time Friction | +0.4% | North America, Europe, and APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising ESRD Burden and CKD Progression

The hemodialysis services market is being pushed by a larger pool of patients with chronic kidney disease who eventually progress to ESRD and require ongoing renal replacement therapy. The Brazilian Dialysis Census 2024 recorded 172,585 patients on dialysis, which represented nearly 55% growth over the prior decade and showed how patient load continues to build across large treatment systems. The same census found that diabetes and hypertension each accounted for 29% of chronic kidney disease etiology, which shows that dialysis demand is still being fed by common long-duration metabolic disorders rather than isolated clinical episodes. This matters because patients who enter treatment later in the disease course often need more complex care, more clinical oversight, and longer treatment continuity, all of which raise the service intensity attached to each patient relationship. The hemodialysis services market also benefits from the fact that ESRD is not a short-cycle condition, so new patient additions tend to accumulate into a durable treatment census instead of rolling off quickly. As a result, rising CKD prevalence does not just widen the patient base, it also supports steadier utilization, more predictable scheduling, and stronger revenue visibility for operators that can handle higher-acuity care[1]Sociedade Brasileira de Nefrologia and Pró Rim, “Censo Brasileiro de Diálise de 2024,” Pró Rim, prorim.org.br.

Expanding Medicare and National Dialysis Reimbursement Coverage

Reimbursement support remains one of the clearest growth supports for the hemodialysis services market because facility economics depend heavily on stable payment rules and frequent treatment billing. The CY 2026 ESRD Prospective Payment System final rule raised the Medicare base rate to USD 281.71 per treatment, which was USD 7.89 higher than in 2025. CMS also projected 2.2% growth in total payments to all ESRD facilities, with freestanding centers receiving a 2.2% increase and hospital-based facilities receiving a 1.5% increase, which reinforces the payment strength behind large outpatient networks. The rule also extended the training add-on payment adjustment for home and self-dialysis through 2026 and aligned the AKI dialysis payment rate at USD 281.71, which broadens the funded pathway for care outside the clinic. Even with that support, the early end of the ESRD Treatment Choices Model showed that payment incentives alone do not automatically shift care models when staffing, patient training, and infrastructure still limit execution. The hemodialysis services market therefore continues to gain from reimbursement breadth, while operators still need to pair that funding with clinical capacity and compliance performance under the ESRD Quality Incentive Program[2]Centers for Medicare & Medicaid Services, “Calendar Year (CY) 2026 End-Stage Renal Disease (ESRD) Prospective Payment System Final Rule,” CMS.gov, cms.gov.

Shift Toward Home Hemodialysis and Remote Monitoring

The hemodialysis services market is also being reshaped by home care technology that reduces the supervision gap between clinics and patients living outside the center. Fresenius Medical Care launched kinexus globally in June 2026, creating one platform for remote therapy monitoring, prescription management, and supply ordering across peritoneal dialysis and home hemodialysis. The platform supports nearly 290,000 patients across 3,539 clinics, which shows that large operators are now treating digital coordination as core operating infrastructure rather than as a side tool. This model matters because session parameters and vital signs can move directly into clinic dashboards, allowing one clinical team to supervise more than one home patient without sacrificing visibility into treatment adherence. Policy direction is moving the same way, with CMS extending payment support for home-based AKI dialysis and the National Kidney Foundation continuing to press for durable telehealth access for kidney patients. Taken together, those changes support a hemodialysis services market where home modalities gain share because they improve both care flexibility and operating efficiency, not just patient convenience.

Hemodiafiltration Upgrade Cycle in Installed Base Markets

Another important support for the hemodialysis services market is the upgrade cycle around high-volume hemodiafiltration in mature installed-base regions. The FDA cleared Fresenius Medical Care’s updated 5008X CAREsystem in May 2025, opening the door for high-volume hemodiafiltration in the United States after years of earlier adoption in Europe and Asia-Pacific. The analysis noted that nearly 160,000 in-center hemodialysis machines across U.S. providers may be eligible for replacement, which points to a meaningful equipment-linked service refresh across clinic networks. By April 2026, the system had reached nearly 100 U.S. clinics and surpassed 100,000 treatments, showing that rollout had already moved beyond pilot scale. High-volume hemodiafiltration can deliver convective volumes of at least 23 liters per session, and the clinical record from other regions has kept provider interest high as U.S. adoption builds. This gives the hemodialysis services market a possible premium layer inside the in-center setting, where centers that upgrade early may be better placed to compete for payer contracts tied to quality and outcomes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Labor Intensity and Nurse Shortage Pressure | -1.2% | North America and Europe severe, global moderate | Long term (≥ 4 years) |

| Vascular Access Failure and Rehospitalization Risk | -0.6% | Global, particularly aging-population markets | Medium term (2-4 years) |

| Water Treatment, Infection Control, and Compliance Overheads | -0.4% | Global, acute in APAC and MEA infrastructure markets | Short term (≤ 2 years) |

| Uneven Reimbursement for Home Modalities and Training Logistics | -0.4% | Europe and South America, less acute in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Labor Intensity and Nurse Shortage Pressure

The most persistent brake on the hemodialysis services market is the labor intensity of treatment delivery, because dialysis care still depends on specialized nurses, nephrologists, technical staff, and strict supervision routines. The U.S. nephrology fellowship fill rate stood at 66% in 2024, which points to a pipeline problem at the same time that patient need continues to rise. The National Center for Health Workforce Analysis projected a 21% shortage of nephrologists by 2037 and a 10% shortage of registered nurses by 2027, with rural areas facing greater exposure to service gaps. Those shortages matter because new chair capacity cannot be fully utilized when a facility cannot staff shifts, train patients, or keep required oversight ratios in place. Telehealth and advanced practice providers can help at the margin, but Medicare’s in-person requirements still limit how far those solutions can scale in routine use. The hemodialysis services market therefore faces a practical ceiling where demand remains strong, but labor shortages slow the pace at which operators can convert that demand into active treatment volume.

Uneven Reimbursement for Home Modalities and Training Logistics

Home care expansion in the hemodialysis services market is also held back by uneven reimbursement rules and the operational burden of training patients before treatment can safely move outside the center. In Brazil, a study commissioned by ABCDT and the Brazilian Society of Nephrology found that public reimbursement for hemodialysis sessions sat 38% below estimated average per-session cost, which limits the room operators have to fund training and home-support infrastructure. In France, the PLFSS 2026 reform will move dialysis funding from session-based payment to individualized weekly lump sums from January 2027, adding nearly 27 patient groups and more administration for mixed-modality providers. Home hemodialysis also requires 4 to 6 weeks of upfront training, which means providers must invest staff time well before a patient reaches steady treatment status. Larger providers can absorb that setup burden more easily, but smaller operators may delay program buildout if reimbursement is not reliable enough to cover early-stage support costs. This keeps the hemodialysis services market on a slower home adoption path in some countries even when patient interest and technology readiness are improving[3]France Rein, “2026, Année Critique Pour La Réforme Du Financement De La Dialyse,” France Rein, francerein.org.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: In-Center Volumes Anchor Revenue While Home Modalities Gain Structural Ground

In-center hemodialysis held 85.31% of hemodialysis services market share by service type in 2025, which shows how strongly the revenue base still depends on clinic-based treatment delivery. This segment remains dominant because dialysis centers provide the machines, trained clinical staff, water treatment systems, and emergency oversight that many patients with multiple comorbidities still need on a regular basis. The hemodialysis services market still leans toward in-center care because these facilities have been built over decades around predictable scheduling, payer familiarity, and strong procedural control. Nocturnal hemodialysis offers higher clearance volumes per session and has appeal for patients who want better daily-life flexibility, but it remains less common because longer chair occupancy changes the economics of each treatment slot. Other service types, including hybrid and home-linked modalities, continue to add smaller revenue streams in markets where public policy supports treatment outside the traditional center.

Home hemodialysis is the fastest-growing service type with an 8.38% CAGR from 2026 to 2031, which shows where future care redesign is concentrated inside the hemodialysis services market. Outset Medical received FDA 510(k) clearance in January 2026 for the next-generation Tablo hemodialysis system, which was also the first dialysis system cleared under the FDA’s 2025 medical device cybersecurity requirements. The system is now deployed across more than 1,000 U.S. healthcare facilities, which suggests that providers are increasingly willing to back technology that supports simpler movement across care settings. That tighter regulatory bar may give an edge to vendors that can meet newer compliance standards, which could narrow supplier choice over time while strengthening the operating case for scalable home programs in the hemodialysis services market.

By End User: Dialysis Center Networks Dominate But Home Care’s Value Logic Shifts Operator Priorities

Dialysis centers commanded 83.24% share of the hemodialysis services market size by end user in 2025, which reflects the scale advantage of fixed-site treatment networks. These networks support high-volume, standardized treatment with recurring patient visits, which has made them the core operating model for for-profit service chains. Hospitals remain the second major end-user base because acute dialysis needs in intensive care settings still require close integration with broader hospital care pathways. This is especially relevant as septic shock and sepsis-associated acute kidney injury increase the need for intermittent hemodialysis and continuous renal replacement therapy in high-acuity settings. Other end users, including nursing homes and specialty rehabilitation facilities, still represent a smaller part of the hemodialysis services market but are gaining relevance as dialysis care follows an older and more medically complex patient base.

Home care settings are the fastest-growing end-user category, and this part of the hemodialysis services market size is projected to expand at an 8.52% CAGR through 2031. CMS widened this path when it extended AKI home dialysis payment in the 2025 ESRD PPS rule, which brought some acute patients into the home-care revenue base as well. The hemodialysis services market is responding because the home setting can lower avoidable hospital use, improve scheduling flexibility, and fit payer efforts to contain cost without reducing treatment continuity. This means the center-to-home shift is no longer a narrow option for selected patients only, but a broader operating priority for providers that want to build a more flexible end-user mix in the hemodialysis services market

By Indication: CKD Sustains the Revenue Base While Septic Shock Drives Acute Demand Growth

Chronic kidney disease accounted for 75.52% of the hemodialysis services market size by indication in 2025, which confirms that long-duration renal failure remains the core source of revenue and utilization. This segment is durable because CKD stage 5 requires renal replacement therapy on an ongoing basis, which creates patient relationships that often continue for years with repeated weekly sessions. The hemodialysis services market therefore benefits from a demand stream that is both recurring and clinically necessary, which supports stable treatment volume even in periods of operating strain. Acute kidney infections form a smaller indication pool, but they still generate meaningful short-cycle demand because treatment episodes can be resource heavy even when they do not convert into long-term care. That split between long-duration CKD and shorter acute events gives the hemodialysis services market a base of steady revenue with a smaller but important layer of episodic hospital-linked demand.

Septic shock is the fastest-growing indication with a 6.25% CAGR through 2031, which reflects the rising dialysis burden tied to severe sepsis and ICU care. A multi-center ICU study covering 187,888 adult patients found sepsis-associated acute kidney injury in 46.6% of sepsis cases, and nearly 1 in 8 of those patients required kidney replacement therapy within the first week. Mortality also rose sharply when septic shock accompanied AKI, which increases the need for hospital-adjacent dialysis capacity that can respond quickly to critical-care demand. Providers that can connect acute dialysis in hospitals with downstream outpatient follow-up are therefore better placed to capture both the immediate treatment episode and any later conversion into chronic care inside the hemodialysis services market.

Geography Analysis

North America held 38.22% of hemodialysis services market share in 2025, which made it the largest regional revenue base in the period. The United States supports this position through a Medicare ESRD entitlement that covers dialysis patients regardless of age, which gives the region a strong public reimbursement foundation. In CY 2026, the ESRD PPS base rate stands at USD 281.71 and is projected to generate nearly USD 6 billion in Medicare payments to nearly 7,600 ESRD facilities, which was a 2.2% increase from CY 2025. The analysis also showed that chain ownership remained very high among Medicare-certified dialysis facilities, which explains why scale, payer contracting, and operating efficiency remain central competitive tools in the hemodialysis services market. South America presents a different picture, where patient need continues to expand but lower public reimbursement creates a tighter investment environment for network growth.

Europe was the second-largest regional presence, with Germany and France identified as its anchor markets in the hemodialysis services market. Germany reflects a mature, high-penetration system backed by statutory health insurance, while France supports a large dialysis population through a nationally organized care structure. France’s PLFSS 2026 legislation will shift dialysis financing from per-session payment to individualized weekly lump sums from January 2027, which is intended to encourage more home and autonomous dialysis use. That policy change matters across the wider hemodialysis services market in Europe because national health systems often influence provider investment decisions more directly than pure private pricing dynamics.

Asia-Pacific is the fastest-growing regional segment with a 7.65% CAGR through 2031, which gives the hemodialysis services market its strongest geographic expansion runway. The network expansion in underserved urban and semi-urban catchments, especially in large population countries, where access is still catching up with disease burden. This regional pattern is important because new clinic buildout in high-need areas can add volume quickly once reimbursement and supply conditions support regular service delivery. The Middle East and Africa still represent a smaller share of the hemodialysis services market, but public-private investment models and selective international expansion are gradually widening the regional care footprint.

Competitive Landscape

The hemodialysis services market is highly consolidated in developed regions and much more dispersed across emerging countries, so competitive conditions vary sharply by geography. Large operators benefit from network density, reimbursement expertise, supply coordination, and the ability to spread compliance costs across wider clinic footprints. In the United States, the DaVita and Fresenius Medical Care together controlled close to 75 to 80% of outpatient capacity, which helps explain why scale continues to shape pricing leverage, clinic operations, and patient transfer dynamics. The hemodialysis services market is not standing still, however, because even the largest operators are adjusting their footprints, digital systems, and care models rather than relying on clinic count alone. That combination of concentration and redesign means the leading part of the hemodialysis services market is now competing on care architecture and operating discipline as much as on physical network presence.

Fresenius Medical Care offers one clear example of that shift through its FME25+ transformation, its rollout of the 5008X CAREsystem, and its broader effort to align technology, clinic operations, and value-based care tools. The company also increased ownership in Interwell Health in September 2025, which signaled a stronger commitment to models that connect dialysis operations with value-based kidney care management. At the same time, Fresenius has been exiting selected U.S. clinics, which shows that capital is being redirected toward stronger assets rather than spread evenly across the footprint. Those moves suggest that leadership in the hemodialysis services market is increasingly tied to whether operators can improve margin quality while still upgrading clinical capability.

Technology suppliers are also shaping competition in the hemodialysis services market by giving providers new ways to shift treatment across sites of care. Outset Medical’s next-generation Tablo clearance in January 2026 and its deployment in more than 1,000 U.S. healthcare facilities show how device innovation can influence both hospital insourcing and home program design. Fresenius Medical Care’s June 2026 launch of kinexus adds another example, because digital coordination tools can strengthen patient oversight while making home dialysis easier to manage at scale. In that sense, the hemodialysis services market is becoming more competitive not only through ownership concentration, but also through the ability to connect centers, homes, digital systems, and payer-backed care pathways in one operating model.

Hemodialysis Services Industry Leaders

Fresenius Medical Care AG & Co. KGaA

B. Braun SE

DaVita Inc.

Diaverum AB

Baxter International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: NephroPlus, part of Nephrocare Health Services, expanded its presence by acquiring dialysis assets from Northern Mindanao Dialysis Clinic Inc. and Aliaga Hemodialysis Centre Inc. in the Philippines. With this acquisition, NephroPlus operates over 520 clinics across India, the Philippines, Saudi Arabia, Uzbekistan, and Nepal.

- May 2026: NefroCenter Group took a significant step in its growth strategy by acquiring Sant'Anna Nursing Home in Imperia, Liguria, along with three coastal dialysis centers. This expansion extended its network from regions like Lazio, Lombardy, and Emilia-Romagna to northern coastal Italy, furthering its regional consolidation efforts.

Global Hemodialysis Services Market Report Scope

As per the scope of the report, hemodialysis services refer to medical treatments that involve the use of a machine (dialyzer) to filter waste products, excess fluids, and toxins from the blood of patients whose kidneys are unable to perform these functions effectively.

The segmentation of the hemodialysis services market is categorized by service type, end user, indication, and geography. By service type, the market includes in-center hemodialysis, home hemodialysis, nocturnal hemodialysis, and other services. By end user, it is segmented into dialysis centers, hospitals, home care, and other users. By indication, the market covers chronic kidney disease (CKD), acute kidney infections, septic shock, and other conditions. Geographically, the market is divided into North America, Europe, Asia-Pacific, Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| In-Center Hemodialysis |

| Home Hemodialysis |

| Nocturnal Hemodialysis |

| Other Service Types |

| Dialysis Centers |

| Hospitals |

| Home Care Settings |

| Other End Users |

| Chronic Kidney Disease (CKD) |

| Acute Kidney Infections |

| Septic Shock |

| Other Indications |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | In-Center Hemodialysis | |

| Home Hemodialysis | ||

| Nocturnal Hemodialysis | ||

| Other Service Types | ||

| By End User | Dialysis Centers | |

| Hospitals | ||

| Home Care Settings | ||

| Other End Users | ||

| By Indication | Chronic Kidney Disease (CKD) | |

| Acute Kidney Infections | ||

| Septic Shock | ||

| Other Indications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the hemodialysis services market?

The hemodialysis services market size stands at USD 6.44 billion in 2026 and is forecast to reach USD 8.32 billion by 2031 at a 5.25% CAGR.

Which service type leads hemodialysis services revenue?

In-center hemodialysis led service-type revenue with an 85.31% share in 2025, showing that clinic-based treatment still anchors current revenue generation.

Which end-user setting is growing fastest in dialysis care delivery?

Home care settings are projected to grow at an 8.52% CAGR through 2031, supported by reimbursement support and stronger remote monitoring tools.

What is driving long-term demand for hemodialysis services?

The largest long-term demand driver is the growing ESRD and CKD patient pool, supported by recurring treatment need and limited transplant availability.

Which region leads revenue and which one grows fastest?

North America held the largest share at 38.22% in 2025, while Asia-Pacific is forecast to expand at a 7.65% CAGR through 2031.

What is the main operational risk for dialysis providers?

Labor intensity remains the main operating risk because nephrologist and nurse shortages can limit how much capacity operators can actually bring online.

Page last updated on: