Peritoneal Dialysis Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

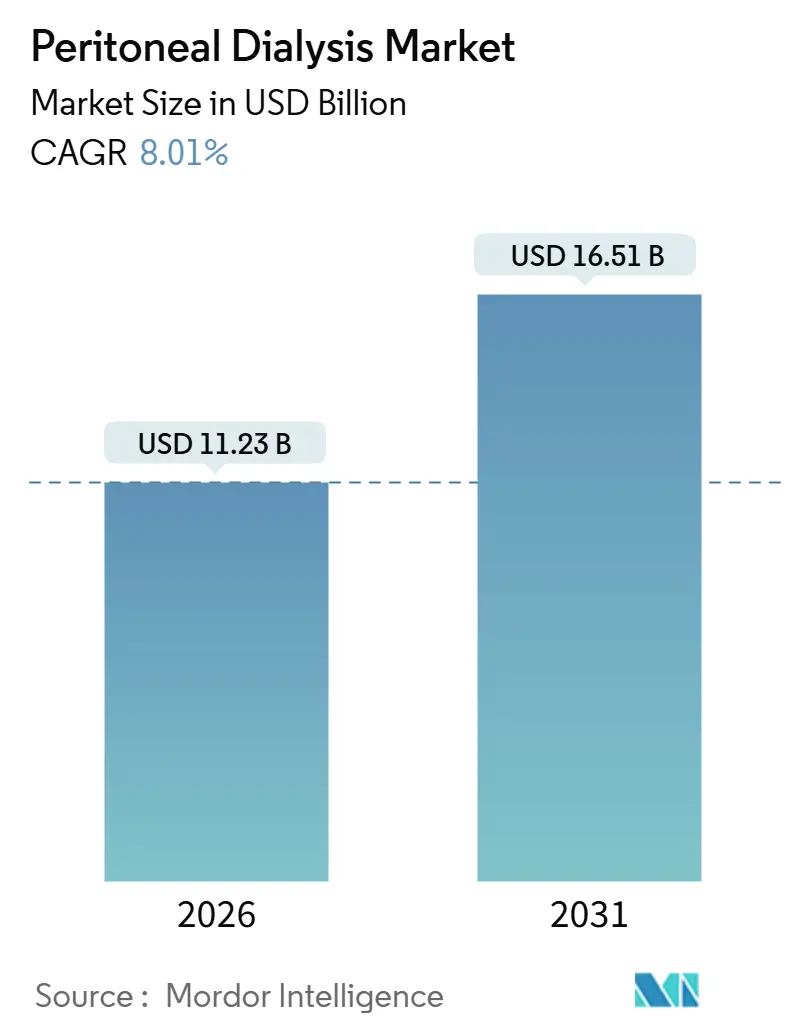

| Market Size (2026) | USD 11.23 Billion |

| Market Size (2031) | USD 16.51 Billion |

| Growth Rate (2026 - 2031) | 8.01% CAGR |

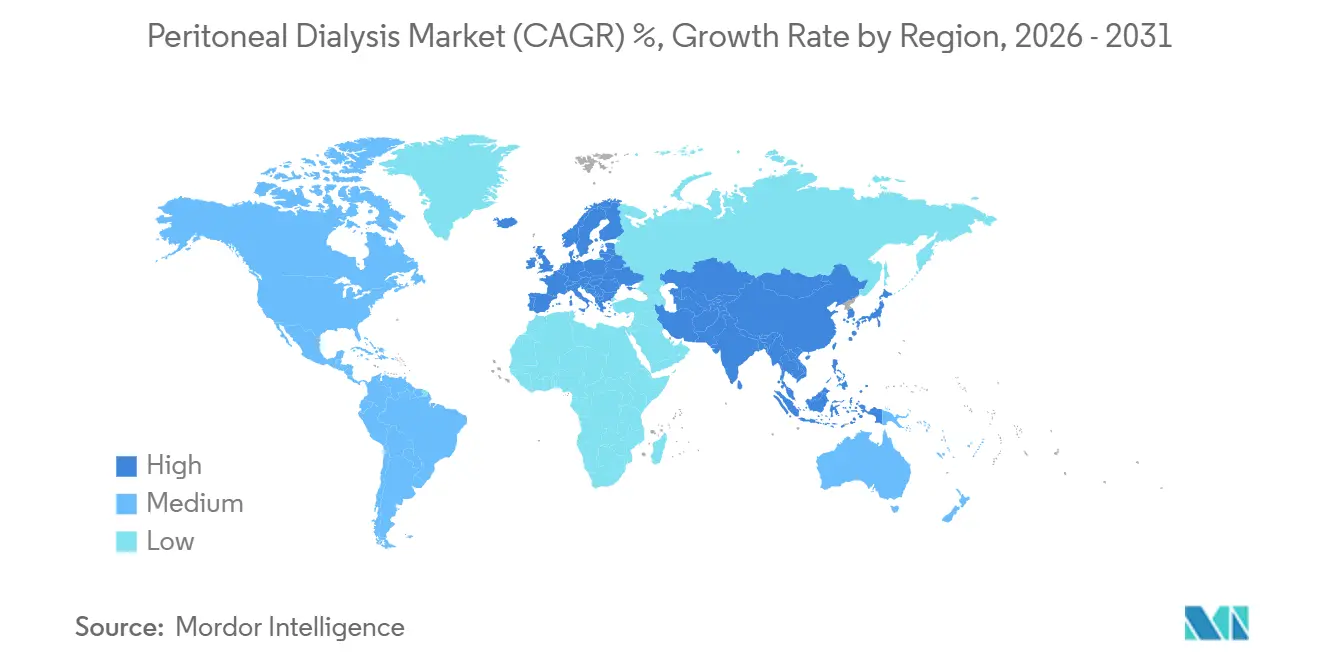

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

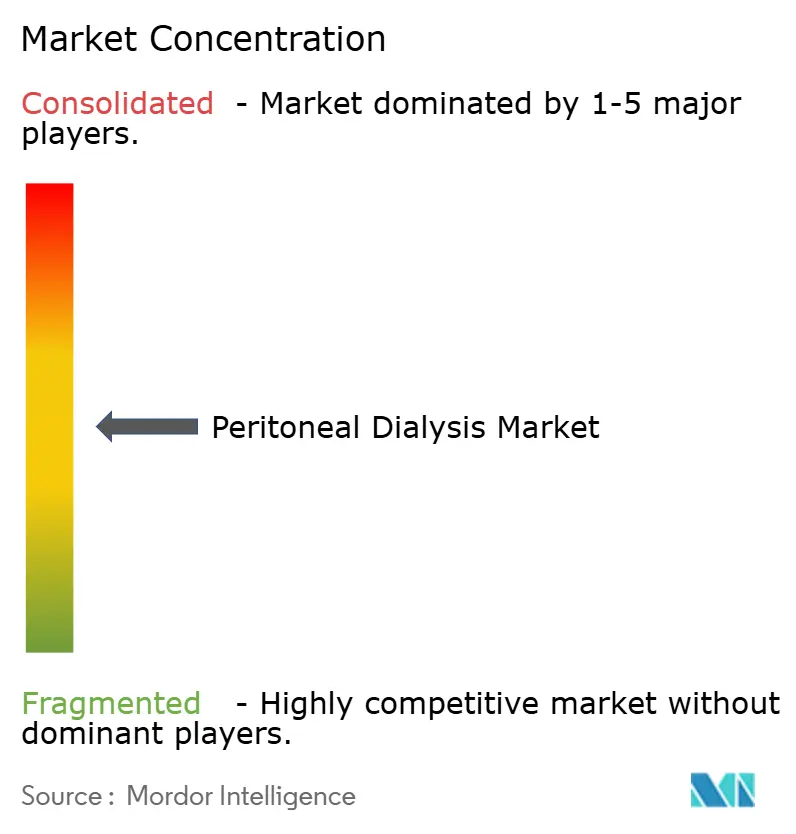

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Peritoneal Dialysis Market Analysis by Mordor Intelligence

The Peritoneal Dialysis Market size is estimated at USD 11.23 billion in 2026, and is expected to reach USD 16.51 billion by 2031, at a CAGR of 8.01% during the forecast period (2026-2031).

This expansion reflects a structural shift away from in-center hemodialysis toward home-based options as payers reward value-based renal care. A mandatory 30% home dialysis penetration target in the United States, coupled with similar “PD-first” policies in parts of Europe and Asia-Pacific, is broadening the peritoneal dialysis market opportunity. Connectivity features embedded in automated cyclers, falling import tariffs on locally manufactured consumables, and the rising burden of diabetes and hypertension are converging to sustain demand. Meanwhile, manufacturers are consolidating supply chains after Hurricane Helene exposed single-site risks, driving dual-sourcing strategies and localized capacity additions. Infection control protocols, reimbursement gaps in select emerging economies, and tariff volatility on plastics and electronics temper the outlook but do not derail the long-term trajectory of the peritoneal dialysis market.

Key Report Takeaways

- By product type, peritoneal dialysis solutions led with 36.81% revenue share in 2025; PD devices are projected to expand at an 8.94% CAGR through 2031.

- By treatment modality, continuous ambulatory peritoneal dialysis captured 64.57% of peritoneal dialysis market share in 2025; automated peritoneal dialysis is advancing at a 9.81% CAGR through 2031.

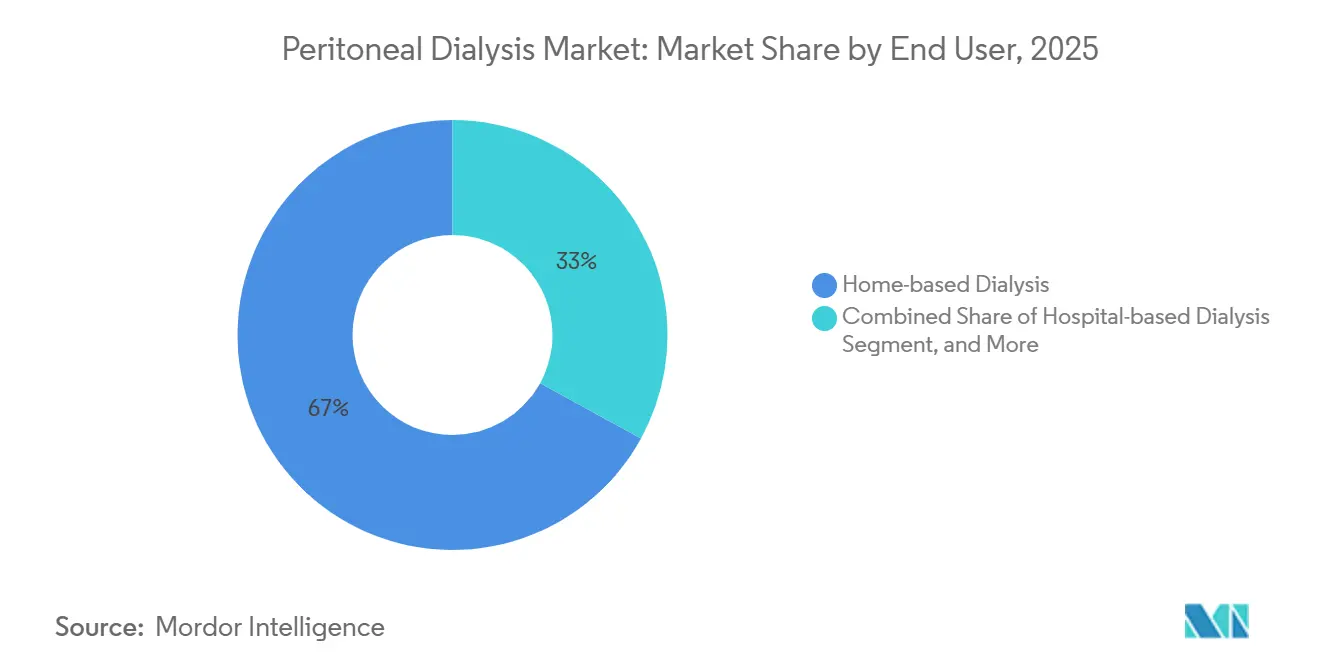

- By end user, home-based dialysis accounted for 67.02% share of the peritoneal dialysis market size in 2025 and is projected to expand at a 12.22% CAGR between 2026 and 2031.

- By geography, North America held 34.83% of peritoneal dialysis market share in 2025 while Asia-Pacific is projected to record a 12.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Peritoneal Dialysis Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Global ESRD & CKD Prevalence | +1.8% | Global, with concentration in North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Growing Preference for Home-Based Renal Replacement Therapy | +2.1% | North America, Europe, Australia | Medium term (2-4 years) |

| Technological Advances in Automated PD Cyclers & Biocompatible Solutions | +1.5% | Global, early adoption in North America & EU | Medium term (2-4 years) |

| Favourable Reimbursement Reforms | +1.3% | United States, Canada, UK, Germany | Short term (≤ 2 years) |

| AI-Enabled Remote Monitoring Platforms for Therapy Optimisation | +0.9% | North America, Western Europe, Japan | Medium term (2-4 years) |

| Supply-Chain Localisation Incentives Lowering Import Dependence | +0.7% | China, India, Brazil, ASEAN | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Global ESRD & CKD Prevalence

The global incidence of end-stage renal disease keeps climbing as diabetes and hypertension become more widespread. The United States Renal Data System logged 130,754 new ESRD cases in 2024, up 2.3% year over year. In China, 132.3 million adults live with chronic kidney disease, yet only 15% receive dialysis, underlining a vast unmet need.[1]National Health Commission of China, “CKD Prevalence Report,” nhc.gov.cn India adds roughly 220,000 ESRD patients annually, but fewer than 10% access maintenance therapy. These epidemiological trends ensure sustained volume growth for the peritoneal dialysis market as health systems seek cost-effective alternatives to in-center hemodialysis, which consumes three times the per-patient annual spend in most OECD settings. Manufacturers respond by scaling up production of glucose-sparing solutions and low-cost cyclers tuned for affordability in emerging markets.

Growing Preference for Home-Based Renal Replacement Therapy

Patient autonomy, pandemic-era infection concerns, and payer incentives are tilting modality selection. Participants in the CMS ESRD Treatment Choice Model increased home therapy starts by 18% between 2021 and 2024. NHS England’s 2024 guidance designates peritoneal dialysis as the default modality unless contraindicated, cutting hospitalization rates by 27% compared with in-center hemodialysis.[2]NHS England, “Clinical Commissioning Policy,” england.nhs.uk A 2024 Journal of the American Society of Nephrology cohort study showed PD patients experienced 41% fewer nosocomial infections during COVID-19 waves. Employers now favor overnight automated therapy that preserves daytime productivity, accelerating adoption among working-age cohorts. These shifts strengthen the medium-term outlook for the peritoneal dialysis market.

Technological Advances in Automated PD Cyclers & Biocompatible Solutions

Connected cyclers transmit treatment data to cloud dashboards, enabling nephrologists to adjust prescriptions without in-person visits. Baxter’s Homechoice Claria logged more than 1.2 million remote sessions in 2024. A randomized Kidney International trial found that remote monitoring reduced technique failure by 34% over 2 years. Biocompatible solutions evolve beyond glucose: icodextrin now represents 22% of European volume and supports long-dwell ultrafiltration. Amino-acid dialysates improved serum albumin by 0.3 g/dL in elderly PD patients according to a 2025 meta-analysis. These innovations extend therapy longevity, reduce dropout risk, and expand the addressable patient pool, reinforcing momentum in the peritoneal dialysis market.

Favorable Reimbursement Reforms

Value-based payment models shorten return-on-investment timelines for home therapy. Medicare raised the composite rate for home dialysis by 3.2% in 2025 and added a USD 150 monthly training payment for six months. Germany now requires nephrologists to document reasons for not offering PD and soft-mandates PD-first counseling. Ontario and British Columbia reimburse remote monitoring at CAD 75 (USD 55) per patient monthly. These reforms align provider incentives with patient-centered outcomes, unlocking faster growth for the peritoneal dialysis market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Peritonitis & Catheter-Related Infection Risk | -1.2% | Global, acute in South Asia, Sub-Saharan Africa, Latin America | Medium term (2-4 years) |

| High Capital & Consumable Cost of APD Systems | -0.9% | Emerging markets (India, Brazil, Southeast Asia, MEA) | Short term (≤ 2 years) |

| Skilled-Staff & Patient-Training Gaps in Emerging Markets | -0.7% | Sub-Saharan Africa, South Asia, Latin America, MEA | Long term (≥ 4 years) |

| Tariff Shocks on Medical-Grade Plastics & Electronics | -0.5% | Global, concentrated impact in import-dependent markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Peritonitis & Catheter-Related Infection Risk

Infection remains the leading cause of technique failure and hospitalization. ISPD guidelines show a global median peritonitis rate of 0.40 episodes per patient-year, with facilities in low-resource regions exceeding 0.80.[3]International Society for Peritoneal Dialysis, “Peritonitis Recommendations,” ispd.org A 2024 Clinical Journal of the American Society of Nephrology study attributed 14% of PD dropouts to catheter infections, often driven by Staphylococcus aureus colonization. Egypt’s PD penetration is below 1% because clinicians cite infection concerns and limited access to prophylactic antibiotics. Manufacturers have rolled out antimicrobial catheter coatings and ultraviolet connectors, yet uptake lags in markets with low per-capita health spending, restraining the peritoneal dialysis market.

High Capital & Consumable Cost of APD Systems

Automated cyclers list from USD 4,000 to USD 8,000, while monthly consumables can reach USD 1,200. Brazil’s Unified Health System reimburses only USD 420, forcing many patients to revert to CAPD. India’s national dialysis program excludes PD, and private insurance caps at INR 25,000 (USD 300), below typical APD spend [MOHFW.GOV.IN]. Kidney International Reports calculated APD is cost-neutral with in-center hemodialysis only above 150 patients per center. These affordability gaps slow APD uptake and curb the growth of the peritoneal dialysis market in emerging economies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Solutions Dominate, Devices Accelerate

Peritoneal dialysis solutions accounted for 36.81% of the peritoneal dialysis market in 2025, driven by recurring consumable purchases that generate predictable revenue streams. Fresenius’ two-chamber bags further reduce contamination risk, bolstering solution loyalty. Conversely, PD devices are projected to grow at an 8.94% CAGR, buoyed by cloud-connected cyclers that enable remote adjustments. Sharesource-enabled units reduced missed exchanges by 31% in 2024. PD sets and catheters, though less valuable, remain critical for therapy initiation, and Medtronic’s dual-cuff silicone designs reported a 12% increase in shipments in 2024.

Rising compliance costs under Europe’s Medical Device Regulation 2017/745 force smaller entrants to exit, tightening competitive intensity yet raising safety. Biocompatible formulations such as icodextrin now represent 22% of European solution sales.JMS introduced bicarbonate blends that mitigate acidosis risk in high transporters. These developments expand clinical choice and sustain product diversification in the peritoneal dialysis market.

By Treatment Modality: CAPD Leads, APD Gains Share

Continuous ambulatory peritoneal dialysis accounted for 64.57% of the peritoneal dialysis market share in 2025 due to lower capital requirements. However, manual exchange burden leads to missed treatments, with 23% of patients skipping at least one weekly exchange. Automated peritoneal dialysis is growing at 9.81% because overnight therapy preserves daytime routines and improves quality-of-life scores by 18% on KDQOL-SF. South Korea reached 47% APD penetration in 2024, supported by reimbursement parity and cycler leasing programs.

Hybrid schedules remain niche, endorsed for fewer than 5% of patients but showing promise in preserving residual renal function. Bundled payment structures in the United States now include remote monitoring, further tilting prescriptions toward APD. This shift aligns with the strategic goals of payers and suppliers to grow the peritoneal dialysis market size for device-enabled modalities.

By End User: Home Dialysis Surges Ahead

Home-based therapy captured 67.02% of the peritoneal dialysis market size in 2025 and is forecast to expand at a 12.22% CAGR, bolstered by mandatory 30% home targets in large U.S. organizations. A Health Affairs analysis placed Medicare’s per-patient annual spend at USD 89,000 for home PD versus USD 96,000 for in-center hemodialysis. Remote monitoring reduced hospitalizations by 27% in a 2024 AJKD real-world review. Hospital settings retain relevance for acute infection management and catheter placement, but are losing share as ambulatory centers take over routine procedures. Dialysis clinics act as training hubs; DaVita reported 18% of 2024 clinic revenue stems from home-support services. Regulatory flexibility that allows nurse-led instruction, as in Japan, alleviates training bottlenecks and extends the reach of peritoneal dialysis to rural populations.

Geography Analysis

North America accounted for 34.83% of the peritoneal dialysis market in 2025, as Medicare Advantage penetration and provincial home-first policies in Canada encouraged home therapy. Model participation raised U.S. home starts by 18% between 2021 and 2024. Mexico increased PD coverage by 9% in 2024, adding 22,000 beneficiaries. The 2024 Baxter plant disruption prompted the FDA to issue emergency import authorizations and sparked debate over mandatory dual sourcing. Ontario achieved 31% incident PD starts in 2025, world-leading by provincial measure.

Europe remains compliance-driven; Germany’s directive increased incident PD by 14% in 2024. NHS England pushed PD initiation to 28% of new dialysis starts in 2024. France’s penetration held at 11% due to cultural hesitance despite improved reimbursement. Southern Europe pilots show financial incentives can shift modality mix within 18 months, foreshadowing further gains in the regional peritoneal dialysis market.

Asia-Pacific will post the fastest growth, with a 12.95% CAGR through 2031. China’s 15% tax rebate and WEGO’s new plant lower import exposure and price points. India’s PLI scheme attracted USD 18 million in catheter capacity expansion at Poly Medicure. Japan added 3.2% more PD patients in 2024, aided by AI-driven alerts and approvals. Australia leverages telehealth for rural coverage. South Korea leads with 43% PD penetration, driven by subsidized leasing.

Middle East, Africa, and South America lag due to reimbursement gaps and training deficits. Brazil’s PD penetration fell to 4.3% in 2023 as monthly reimbursement remains below consumable costs. Saudi Arabia and the UAE each reported sub-10% PD penetration, though Dubai’s 2024 free cycler program hints at future upside. South Africa’s pilot in KwaZulu-Natal achieved 22% PD penetration but awaits national funding. These regions represent latent demand pools that could accelerate if policy barriers are lifted, enlarging the global peritoneal dialysis market.

Competitive Landscape

The peritoneal dialysis market is concentrated, with Vantive and Fresenius Medical Care holding a significant combined share. Vantive, spun off from Baxter in 2024, maintains the Homechoice Claria cycler and Dianeal/Extraneal solution franchises, reporting that connected units account for 34% of its installed base.

Innovation pipelines target portability and sorbent regeneration. AWAK Technologies secured FDA Breakthrough Device designation for a wearable PD device and raised more than USD 20 million to move toward pivotal trials. Medtronic’s dual-cuff Tenckhoff catheters reduced infection and migration risk, lifting 2024 volumes by 12%. Asian firms such as Terumo, Nipro, and Asahi Kasei leverage cost advantages; Terumo’s AI alerts won Japanese approval in March 2025. Chinese newcomer WEGO offers 40% lower-priced solutions from its new plant, targeting Southeast Asia and Latin America. India’s Poly Medicure and Mitra Industries expand export footprints under the PLI incentive.

Regulatory hurdles under Europe’s MDR raise compliance costs. Smaller firms lacking dedicated quality teams face audit logjams, delaying launches and reinforcing incumbents’ scale advantage. Hurricane Helene underscored supply concentration risks, prompting calls for dual sourcing and modular redundancy. Strategic responses include regional manufacturing, cloud-native software upgrades, and leasing models that lower entry costs, all aimed at defending or capturing share in the peritoneal dialysis market.

Peritoneal Dialysis Industry Leaders

Baxter International Inc.

Terumo Corporation

B. Braun Melsungen AG

Fresenius Medical Care AG & Co. KGaA

Medtronic

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Baxter restarted two IV-solution lines at its North Cove plant, restoring 85% of pre-storm capacity after Hurricane Helene.

- December 2025: The FDA granted Breakthrough Device designation to Nephrodite’s Holly implantable continuous dialysis system.

- June 2025: Vantive earmarked USD 1 billion over five years for digitally enabled kidney-care innovations.

- September 2024: Fresenius Medical Care surpassed 14,000 U.S. users on NxStage home hemodialysis systems and introduced the Versi HD with GuideMe software enhancements.

Global Peritoneal Dialysis Market Report Scope

Peritoneal dialysis (PD) is a form of renal replacement therapy that uses the patient's own peritoneal membrane (the lining of the abdominal cavity) as a semi-permeable filter to remove waste products, excess fluid, and electrolytes from the blood. Unlike hemodialysis, which requires an external machine and vascular access, PD is performed inside the body by infusing a sterile dialysis solution (dialysate) into the peritoneal cavity through a surgically placed catheter.

The Peritoneal Dialysis Market Report is Segmented by Product Type (Peritoneal Dialysis Solutions, PD Devices, PD Sets, PD Catheters, Accessories & Services), Treatment Modality (CAPD, APD, Hybrid/Intermittent PD), End User (Home-based, Hospital-based, Dialysis Centres & Clinics), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Market Forecasts are Provided in Terms of Value (USD).

| Peritoneal Dialysis Solutions |

| PD Devices |

| PD Sets |

| PD Catheters |

| Accessories & Services |

| Continuous Ambulatory Peritoneal Dialysis (CAPD) |

| Automated Peritoneal Dialysis (APD) |

| Hybrid / Intermittent PD |

| Home-based Dialysis |

| Hospital-based Dialysis |

| Dialysis Centres & Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Peritoneal Dialysis Solutions | |

| PD Devices | ||

| PD Sets | ||

| PD Catheters | ||

| Accessories & Services | ||

| By Treatment Modality | Continuous Ambulatory Peritoneal Dialysis (CAPD) | |

| Automated Peritoneal Dialysis (APD) | ||

| Hybrid / Intermittent PD | ||

| By End User | Home-based Dialysis | |

| Hospital-based Dialysis | ||

| Dialysis Centres & Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the peritoneal dialysis market in 2031?

The market is forecast to reach USD 16.51 billion by 2031, reflecting an 8.01% CAGR.

Which treatment modality is growing fastest within peritoneal dialysis?

Automated peritoneal dialysis is advancing at a 9.81% CAGR as overnight therapy appeals to working-age patients.

Why are payers promoting home-based dialysis?

Home PD lowers annual Medicare spend to USD 89,000 per patient, compared with USD 96,000 for in-center care, while reducing hospitalization frequency.

How are manufacturers addressing infection risk in peritoneal dialysis?

Firms are launching antimicrobial catheters, ultraviolet connection devices, and AI alerts that predict peritonitis before clinical onset.

Which region is expected to post the highest peritoneal dialysis market growth?

Asia-Pacific will expand at a 12.95% CAGR through 2031, propelled by localization incentives in China and India and mature infrastructure in South Korea.

Page last updated on: