U.S. Cord Blood Banking Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

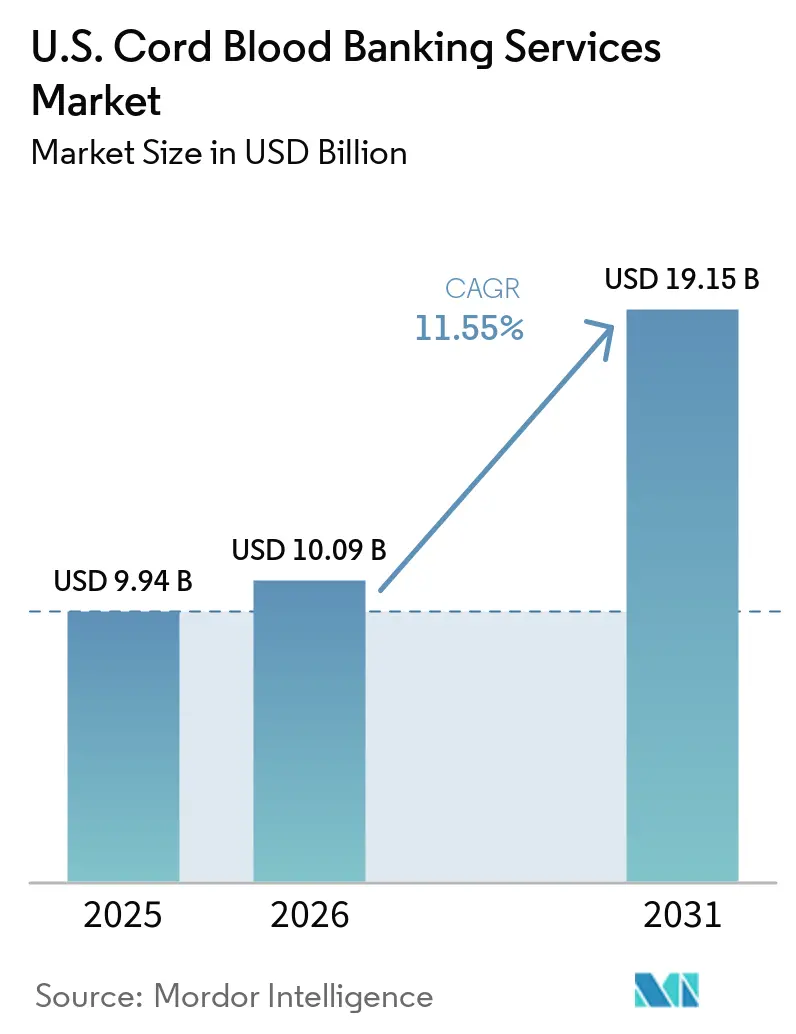

| Base Year Market Size (2025) | USD 9.94 Billion |

| Market Size (2026) | USD 10.09 Billion |

| Market Size (2031) | USD 19.15 Billion |

| Growth Rate (2026 - 2031) | 11.55% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

U.S. Cord Blood Banking Services Market Analysis by Mordor Intelligence

The U.S. Cord Blood Banking Services Market size is projected to be USD 9.94 billion in 2025, USD 10.09 billion in 2026, and reach USD 19.15 billion by 2031, growing at a CAGR of 11.55% from 2026 to 2031.

The United States cord blood banking services market has transitioned from a narrow newborn storage service to a critical component of the stem cell transplant system and the broader cell therapy supply chain. Federal support for public inventories, increased physician recognition of cord blood's HLA matching value for ethnically underrepresented patients, and the growing number of investigational therapies using cord blood are driving demand across collection, processing, storage, and release services. In fiscal year 2025, the C.W. Bill Young Cell Transplantation Program facilitated over 8,400 unrelated blood stem cell transplants, with more than 7,200 serving United States patients, highlighting cord blood's continued relevance in active transplant pathways.[1]HRSA, “Donation and Transplantation Statistics – FY2025,” U.S. Health Resources & Services Administration, bloodstemcell.hrsa.gov Private banking leads in revenue due to its extensive customer base, while public banking benefits from policy support, transplant center demand, and the need for diverse inventories.

Key Report Takeaways

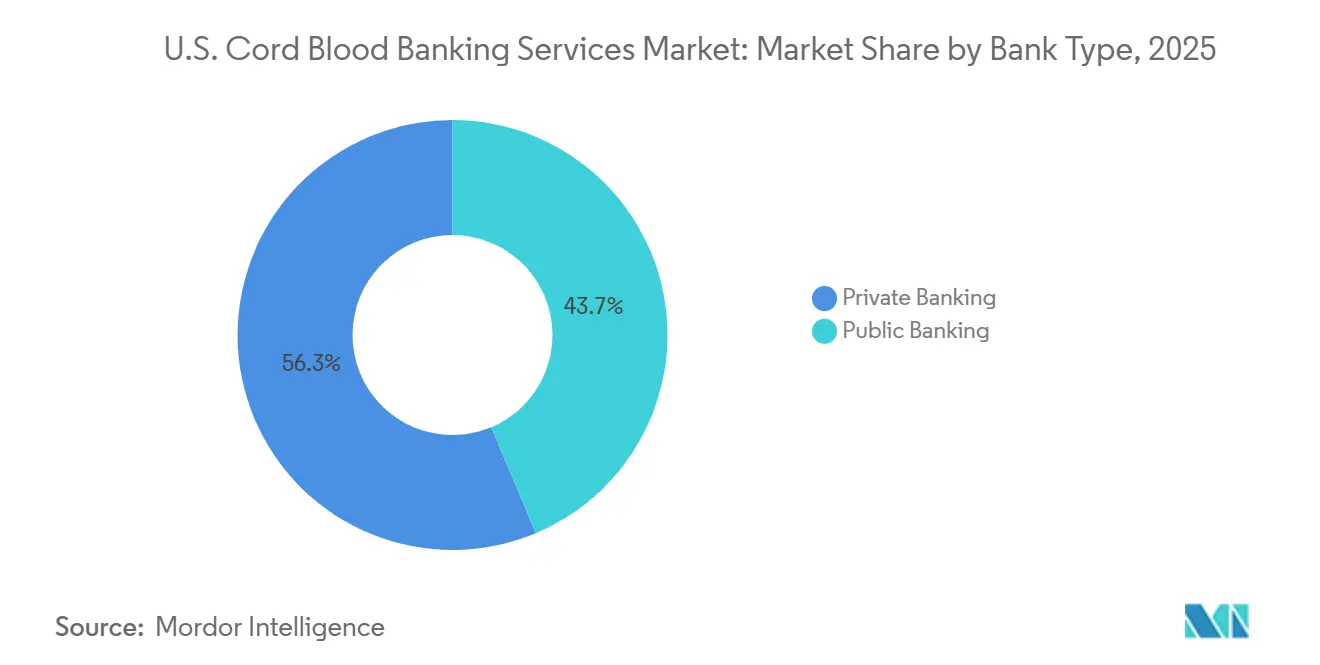

- By bank type, private banking held 56.35% of the U.S. cord blood banking services market share in 2025, while public banking is projected to expand at an 11.95% CAGR through 2031.

- By service type, cryogenic storage and monitoring accounted for 66.76% share of the U.S. cord blood banking services market size in 2025, while processing and testing is projected to grow at a 12.25% CAGR through 2031.

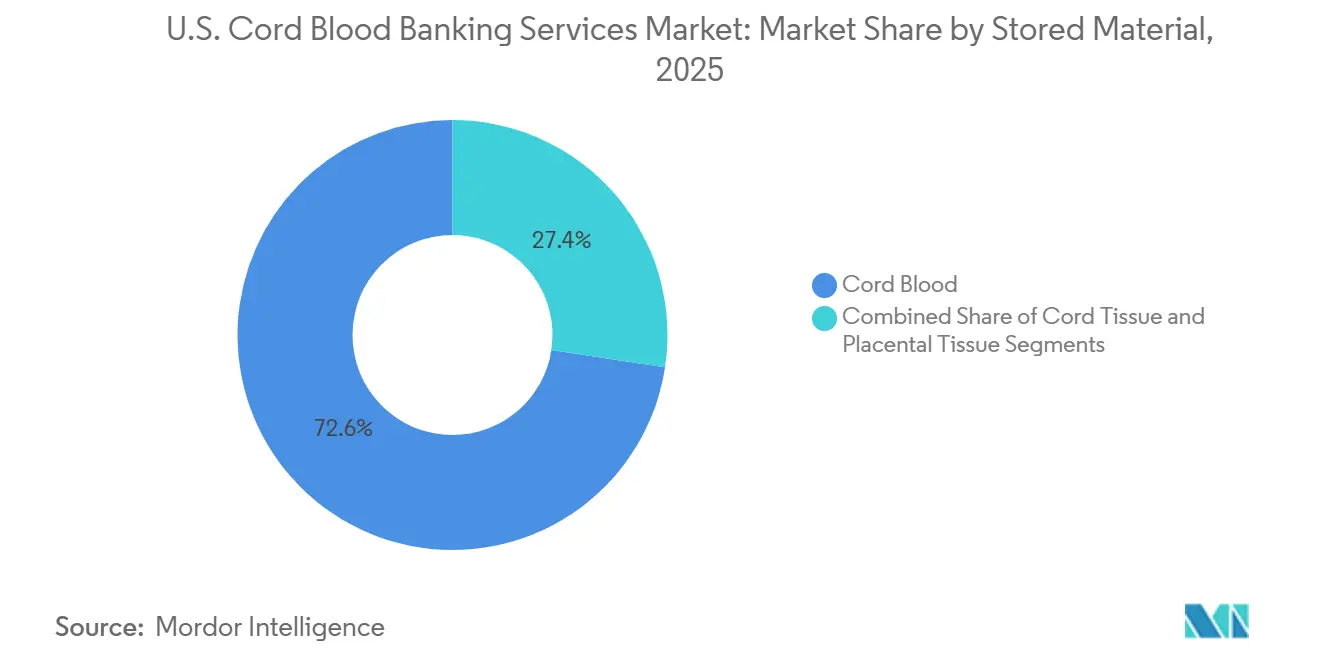

- By stored material, cord blood held 72.64% revenue share in 2025, while cord tissue is expected to record the fastest growth at a 12.75% CAGR through 2031.

- By application, cancer-related indications accounted for 36.75% of revenue in 2025, while metabolic disorders are expected to expand at a 13.10% CAGR through 2031.

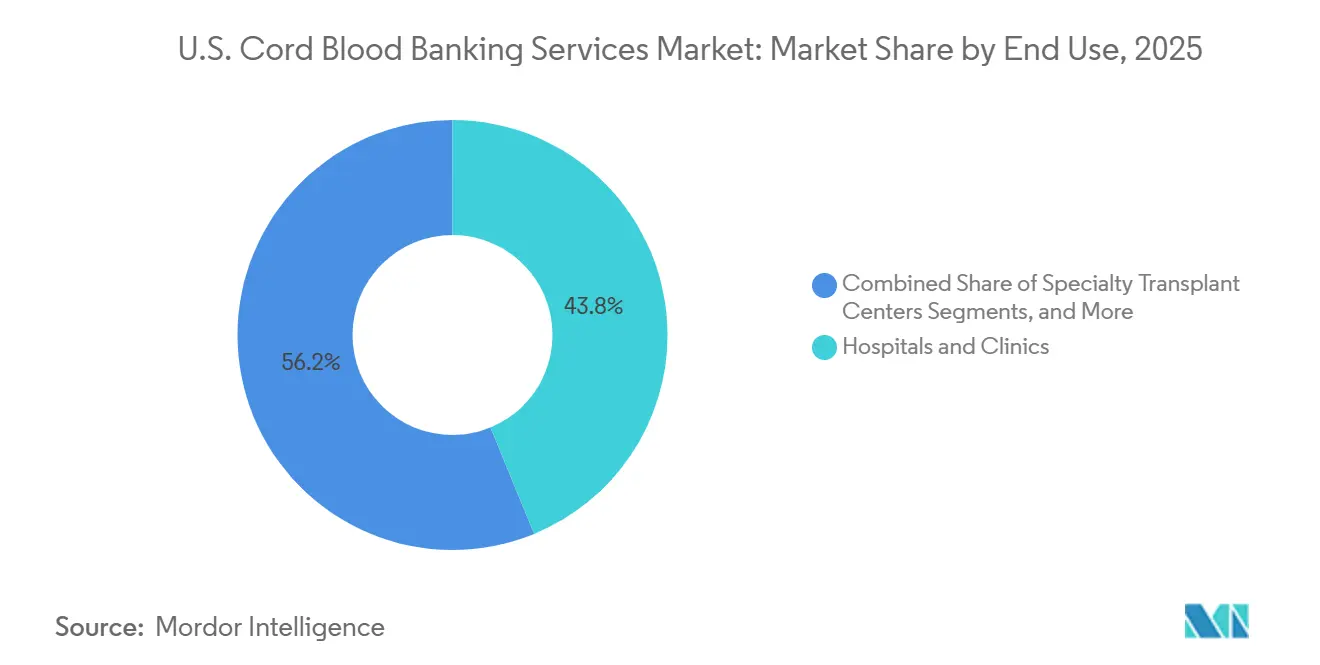

- By end use, hospitals and clinics held 43.76% share in 2025, while research institutes are projected to grow at a 12.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

U.S. Cord Blood Banking Services Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| rising awareness of newborn stem-cell preservation | +2.5% | National, with concentrated gains in Southeast including Florida and Georgia, Southwest including Texas, and Northeast including New York and New Jersey | Medium term (2-4 years) |

| broader transplant use across hematologic and immune disorders | +3.2% | National, strongest in states with major academic transplant centers including Texas, New York, California, and North Carolina | Short term (≤ 2 years) |

| improvements in cryopreservation and cell-recovery workflows | +1.8% | National, with spillover to research clusters in California, Florida, and Massachusetts | Medium term (2-4 years) |

| federal support for public inventory and donor diversity | +1.4% | National, with early gains in high diversity markets including Texas, California, and Florida | Short term (≤ 2 years) |

| demand for cord-blood-derived starting material in cell therapy manufacturing | +2.6% | National, with early gains in biotech clusters in California, Massachusetts, and Texas | Short term (≤ 2 years) |

| minority-match gap increasing value of diverse banked inventories | +1.8% | National, concentrated in high minority birth states including Texas, California, Florida, Georgia, and New York | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Awareness Of Newborn Stem-Cell Preservation

Awareness of newborn stem cell preservation varies significantly across racial, linguistic, and income demographics, indicating that demand is closely tied to education and trust-building efforts. A 2025 study highlighted that only 31.4% of Spanish-speaking pregnant Hispanic women were aware of cord blood banking, with 70% lacking understanding of its purpose. The study also noted that 91.3% of respondents cited lack of knowledge as a barrier, 63% expressed distrust, and 20% had fears about donation.[2]PubMed, “Study On Awareness Of Cord Blood Banking Among Spanish-Only Speaking Pregnant Hispanic Women,” PubMed, pubmed.ncbi.nlm.nih.gov This highlights the importance of targeted outreach in driving enrollment growth. Hispanic families, a significant and growing birth cohort in the United States, remain underrepresented, leading to reduced supply despite high demand.

Broader Transplant Use Across Hematologic And Immune Disorders

Cord blood is increasingly being utilized for a broader range of hematologic and immune disorders, moving beyond its traditional focus on leukemia. The C.W. Bill Young Cell Transplantation Program facilitated over 8,400 unrelated hematopoietic cell transplants in fiscal year 2025, demonstrating the scale of unrelated donor transplantation in the United States. In April 2026, the FDA approved Cellenkos for a Phase 2 trial of CK0801, a cord blood-derived therapy targeting transfusion-dependent aplastic anemia patients. Phase 1 results from 2024 showed promising outcomes, with a significant percentage of patients achieving health milestones.[3FDA, “Cord Blood Banking Information for Consumers,” U.S. Food and Drug Administration, fda.gov ] Additionally, Fred Hutch reported a 96% one-year survival rate in April 2026 for patients using a pooled cord blood transplant, with no severe graft versus host disease cases observed. These developments reinforce the growing role of cord blood in transplants and emerging therapies.

Demand For Cord-Blood-Derived Starting Material In Cell Therapy Manufacturing

Banked cord blood units are increasingly recognized as valuable starting materials for cell therapy development and manufacturing. In January 2025, Ucello received FDA IND approval for UC101, the world’s first umbilical cord blood-derived CAR T product, developed with support from VectorBuilder. Several programs utilizing cord blood-derived natural killer cells are also advancing in hospitals and research institutions, driving demand for high-quality source material. This shift prioritizes attributes like cell count, HLA typing, viability, and collection quality over simple access to stored units. Banks with robust processing systems, clear release standards, and detailed documentation are better positioned to meet these evolving needs. In February 2025, New York Blood Center Enterprises signed a letter of intent with Human Life CORD Japan to expand manufacturing collaborations for umbilical cord tissue-derived mesenchymal stromal cells through Comprehensive Cell Solutions.

Federal Support For Public Inventory And Donor Diversity

Federal support remains critical to stabilizing the public segment of the United States cord blood banking market. In 2025, HRSA allocated USD 15.8 million to contracted cord blood banks, slightly down from USD 16.5 million in 2024. This funding, tied to FDA biologics license capabilities, emphasizes the collection of genetically diverse units. As of September 2025, over 53% of the 247,900 cord blood units on the national registry were genetically varied, with 45% classified as White non-Hispanic. This federal backing not only preserves inventory but also enhances public banks' competitiveness by reducing transaction barriers and ensuring availability for hard-to-match patients. RAND has recommended increasing funding in high-diversity areas and exploring specialization in ethnic collection, emphasizing the clinical and operational importance of donor diversity.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High private banking out-of-pocket cost | -1.2% | National, most acute in lower income Southern and Midwestern states | Medium term (2-4 years) |

| Stringent FDA and state compliance burden | -0.8% | National, concentrated in states with additional state licensing including New York, New Jersey, California, and Maryland | Long term (≥ 4 years) |

| Weak public-bank unit economics | -0.5% | National, concentrated in NCBI contracted public banks | Medium term (2-4 years) |

| Alternative donor pathways reducing cord-blood transplant share | -0.7% | National, most notable in major academic transplant centers with haplo programs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Private Banking Out-Of-Pocket Cost

In the United States, high private banking costs significantly limit family enrollment in cord blood banking services. Consumers face charges between USD 1,500 and USD 3,000 for collection and processing, with annual storage fees ranging from USD 150 to USD 300. Over 20 years, total costs can exceed USD 4,000 for cord blood storage alone and USD 8,000 for combined cord blood and tissue storage. These expenses disproportionately affect lower-income households and families who could benefit from diverse inventories. Simplifying payment structures, clarifying benefits, and emphasizing HSA or FSA eligibility can help private banks reduce enrollment drop-offs.

Alternative Donor Pathways Reducing Cord-Blood Transplant Share

Alternative donor pathways are reducing cord blood's share in transplants within the United States. In 2024, cord blood accounted for nearly 5% of unrelated allogeneic hematopoietic cell transplants, while haploidentical protocols gained dominance at many high-volume centers. Despite this, cord blood remains relevant in specific cases, particularly where donor matching is challenging. A 2025 trial showed that combining haploidentical peripheral blood stem cells with unrelated cord blood improved 1-year disease-free survival compared to using bone marrow, highlighting its continued importance for pediatric patients and minority groups.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Bank Type: Private Scale And Public Growth Operate Side By Side

In 2025, private banking held 56.35% of the United States cord blood banking services market share, driven by an accumulated enrolled base rather than clinical superiority over public banking. Private banks benefit from subscription-based storage, strong consumer branding, and monetization of collection, processing, and long-term storage through family relationships.

Public banking is projected to grow at an 11.95% CAGR through 2031, making it the faster-growing segment in the United States cord blood banking market. Growth is driven by HRSA contract renewals, transplant center reliance on public inventory, and demand for genetically diverse units. Regulatory requirements, including FDA and state-level licensing, favor hybrid operators managing both family storage and public programs, enabling them to optimize margins while serving diverse channels.

By Service Type: Storage Leads Today While Processing Gains Value

Cryogenic storage and monitoring accounted for 66.76% of the United States cord blood banking services market in 2025, reflecting the long-term fee model sustaining private banking. Storage generates recurring revenue, funds laboratory operations, and supports cross-selling of related services. Efficient collection and logistics remain critical, though the focus is shifting toward services enhancing quality and usability.

Processing and testing is expected to grow at a 12.25% CAGR through 2031, driven by demand for validated cell recovery, viability, and release readiness. Platforms like Cryo-Cell International’s PrepaCyte-CB emphasize improved cell recovery, while retrieval and release services are set to rise with increased transplant use and investigational programs. This shift enhances revenue per stored unit and prioritizes laboratory capabilities over storage capacity.

By Stored Material: Cord Blood Remains Core While Cord Tissue Gains Ground

Cord blood held 72.64% of stored material revenue in 2025, maintaining its leadership in the United States cord blood banking market. Its dominance is due to its established role in hematopoietic reconstitution, clinical familiarity, and strong alignment with donor matching registries, ensuring relevance across transplant, release, and research applications.

Cord tissue is forecast to grow at a 12.75% CAGR through 2031, driven by interest in mesenchymal stromal cell applications for inflammatory, autoimmune, and orthopedic uses. Placental tissue, while the smallest segment, is gaining attention as a source of hematopoietic progenitors and mesenchymal stromal cells, supporting broader material portfolios for storage providers.

By Application: Oncology Leads Revenue While Metabolic Disorders Grow Fastest

In 2025, oncology-related indications accounted for 36.75% of application revenue, making it the largest clinical use category in the United States cord blood banking market. Acute leukemia, lymphoma, and multiple myeloma drive transplant demand, while cord blood’s matching flexibility supports minority patients needing unrelated grafts. The application mix remains rooted in traditional transplant medicine.

Metabolic disorders are projected to grow at a 13.10% CAGR through 2031, driven by emerging evidence of cord blood infusion benefits in cerebral palsy, autism spectrum disorder, and metabolic errors. Other applications, including autoimmune conditions and regenerative uses, are expected to grow as clinical trials progress, diversifying future demand.

By End Use: Hospitals Lead While Research Institutes Accelerate

Hospitals and clinics held 43.76% of the market share in 2025, dominating the United States cord blood banking market. Specialized hematology and oncology centers play a key role in releasing cord blood units for transplants, while home storage users provide a stable base for private banking despite slower growth due to awareness and affordability challenges.

Research institutes are expected to grow at a 12.88% CAGR through 2031, driven by the increasing use of cord blood in investigational therapies and manufacturing programs. Banks are adapting to support research-grade procurement and traceability, positioning research and specialty applications for a larger share of future demand while hospitals remain the primary release channel.

Geography Analysis

California, Texas, and New York dominate the United States cord blood banking services market due to high birth volumes, major transplant centers, and robust collection networks. California's state-funded Umbilical Cord Blood Collection Program has created a public inventory with greater racial and ethnic diversity than the national average, improving match potential for underserved groups. High birth rates in cities like Los Angeles, San Francisco, and San Diego enhance California's supply advantage. Public awareness efforts by UC Davis Health further strengthen the state's position by improving donation rates and inventory quality.

Southern and Southwestern states, particularly Texas, Florida, and Georgia, represent key growth areas for the United States cord blood banking services market. Texas benefits from BioBridge Global’s Texas Cord Blood Bank, which has collected ethnically diverse units since 2005 for the national Be The Match network. Outreach quality remains critical, as language barriers impact awareness among Hispanic and minority families. Cord blood increases the probability of finding a stem cell donor for racial and ethnic minorities from 16% to over 80%, addressing a significant need in these regions.

The Northeastern corridor, including New York, New Jersey, Massachusetts, Pennsylvania, and Maryland, features a dense network of private processing laboratories and public bank operations. Vitalant Cord Blood Services, formed through the merger of ITxM Cord Blood Services and New Jersey Cord Blood Bank, actively participates in the National Cord Blood Inventory and the NMDP registry. In the Midwest, states like Indiana, Michigan, and Ohio host infrastructure-focused operators and contract processing facilities supporting multi-regional networks. Areas in the Upper Midwest and Rocky Mountain regions with lower hospital donation density are increasingly served by mail-in kit models. Regional performance in the United States cord blood banking services market depends on birth diversity, transplant infrastructure, hospital partnerships, and laboratory presence.

Competitive Landscape

The United States cord blood banking services market exhibits a split structure, with the private segment moderately concentrated and the public segment fragmented across academic centers, regional blood organizations, and five HRSA-contracted institutions. Leading private operators, including CBR Systems, ViaCord, and Cryo-Cell International, benefit from brand recognition, extensive enrollment pipelines, and large stored inventories. CBR Systems holds the largest private inventory in the country with over 1.1 million cord blood units, while Cryo-Cell International stores more than 250,000 specimens, focusing on processing quality and release readiness. Smaller private players like Americord Registry, Anja Health, FamilyCord, and AlphaCord compete through pricing, guarantees, and consumer-friendly enrollment offers, emphasizing laboratory quality and trust as families evaluate long-term commitments.

Cryo-Cell International leverages technology and accreditation as competitive tools in the United States cord blood banking services market. The company holds exclusive rights to the PrepaCyte-CB processing platform and has renewed FACT accreditation from April 2026 to April 2029 under NetCord-FACT standards, reinforcing its focus on quality and compliance. Americord differentiates itself with guarantees and payment flexibility, offering a USD 110,000 quality guarantee and interest-free 24-month payment plans. On the public side, the shift toward cell therapy manufacturing support as a secondary revenue stream is significant. Public and nonprofit operators, such as New York Blood Center’s Comprehensive Cell Solutions and MD Anderson’s investigational program infrastructure, are expanding beyond transplant inventory to focus on release quality, contract readiness, and therapeutic development support.

U.S. Cord Blood Banking Services Industry Leaders

CBR Systems, Inc.

ViaCord

Cryo-Cell International, Inc.

Americord Registry

AlphaCord, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Cryo-Cell International secured renewed FACT accreditation, valid until April 2029, for its cord blood collection, banking, and release services for both related and unrelated donations. The accreditation was awarded following full compliance with NetCord-FACT Standards.

- April 2026: Fred Hutch announced Phase 2 trial results indicating that 96% of patients (27 out of 28) with leukemias and myelodysplastic syndrome achieved at least one-year survival using a pooled cord blood transplant product, with no severe acute or chronic graft versus host disease reported.

- April 2026: Cellenkos received FDA clearance to commence a Phase 2 clinical trial for CK0801, an allogeneic cord blood-derived regulatory T cell therapy designed for transfusion-dependent aplastic anemia patients who have not responded to prior treatments.

- March 2026: Caribou Biosciences obtained FDA Regenerative Medicine Advanced Therapy designation for CB-011, a CRISPR-edited allogeneic anti-BCMA CAR-T cell therapy targeting relapsed or refractory multiple myeloma.

- February 2026: HRSA reported allocating USD 15.8 million in 2025 to NCBI-contracted cord blood banks, resulting in the addition of over 3,900 new NCBI units during FY2025. By September 2025, the CWBYCTP registry included over 247,900 cord blood units, with 53% classified as genetically diverse.

U.S. Cord Blood Banking Services Market Report Scope

As per the scope of the report, cord blood banking is the process of collecting the blood left in a baby’s umbilical cord and placenta after birth and storing it in a specialized facility. This blood is rich in stem cells used to treat over 80 serious diseases, including certain cancers, blood disorders, and immune deficiencies.

The U.S. cord blood banking services market is segmented by bank type, service type, stored material, application, and end use. By bank type, the market includes private banking and public banking. By service type, the market is segmented into collection & logistics, processing & testing, cryogenic storage & monitoring, and retrieval & release services. By stored material, the market is categorized into cord blood, cord tissue, and placental tissue. By application, the market is segmented into cancers, blood disorders, metabolic disorders, and others. By end use, the market is segmented into hospitals & clinics, specialty transplant centers, research institutes, and home storage users. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Private Banking |

| Public Banking |

| Collection & Logistics |

| Processing & Testing |

| Cryogenic Storage & Monitoring |

| Retrieval & Release Services |

| Cord Blood |

| Cord Tissue |

| Placental Tissue |

| Cancers |

| Blood Disorders |

| Metabolic Disorders |

| Others |

| Hospitals & Clinics |

| Specialty Transplant Centers |

| Research Institutes |

| Home Storage Users |

| By Bank Type | Private Banking |

| Public Banking | |

| By Service Type | Collection & Logistics |

| Processing & Testing | |

| Cryogenic Storage & Monitoring | |

| Retrieval & Release Services | |

| By Stored Material | Cord Blood |

| Cord Tissue | |

| Placental Tissue | |

| By Application | Cancers |

| Blood Disorders | |

| Metabolic Disorders | |

| Others | |

| By End Use | Hospitals & Clinics |

| Specialty Transplant Centers | |

| Research Institutes | |

| Home Storage Users |

Key Questions Answered in the Report

What is the projected value of the U.S. cord blood banking services space by 2031?

It is forecast to reach USD 19.15 billion by 2031, rising from USD 11.09 billion in 2026 at an 11.55% CAGR.

Which bank type currently leads revenue in the United States?

Private banking leads with a 56.35% share in 2025, supported by its long established enrolled family base.

Which service area is expanding the fastest through 2031?

Processing and testing is the fastest growing service category, advancing at a 12.25% CAGR as quality requirements increase.

Why is donor diversity so important in cord blood storage and release?

Diverse inventories improve matching for minority patients, and HRSA reported that 53% of the more than 247,900 units on the registry were genetically varied as of September 2025.

Which application area is expected to grow the fastest?

Metabolic disorders are projected to grow at a 13.10% CAGR through 2031, supported by early clinical work in cerebral palsy, autism spectrum disorder, and inborn errors of metabolism.

Which end users are shaping future demand most strongly?

Hospitals and clinics remain the largest end users with 43.76% share in 2025, while research institutes are growing fastest at a 12.88% CAGR due to cell therapy development needs.

Page last updated on: