Hemodialysis Catheters Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.98 Billion |

| Market Size (2031) | USD 1.26 Billion |

| Growth Rate (2026 - 2031) | 5.16% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hemodialysis Catheters Market Analysis by Mordor Intelligence

The Hemodialysis Catheters Market size is expected to grow from USD 0.94 billion in 2025 to USD 0.98 billion in 2026 and is forecast to reach USD 1.26 billion by 2031 at 5.16% CAGR over 2026-2031.

The hemodialysis catheters market is experiencing growth due to the expanding global dialysis population, driving consistent demand for both short-term and long-term vascular access devices. Diabetes and hypertension remain the leading causes of kidney failure requiring replacement therapy, ensuring a broad and sustained treatment pool for catheter suppliers. Public funding gaps in several countries push many patients into urgent dialysis initiation, maintaining the relevance of catheters even in non-high-income systems. Competition in the hemodialysis catheters market focuses on flow performance, infection prevention, and bundled insertion tools, making product differentiation critical beyond pricing. Despite clinical efforts to reduce catheter dependence and address catheter-related infections, catheter use is expected to remain essential through 2031, as many patients transition slowly to permanent access pathways.

Key Report Takeaways

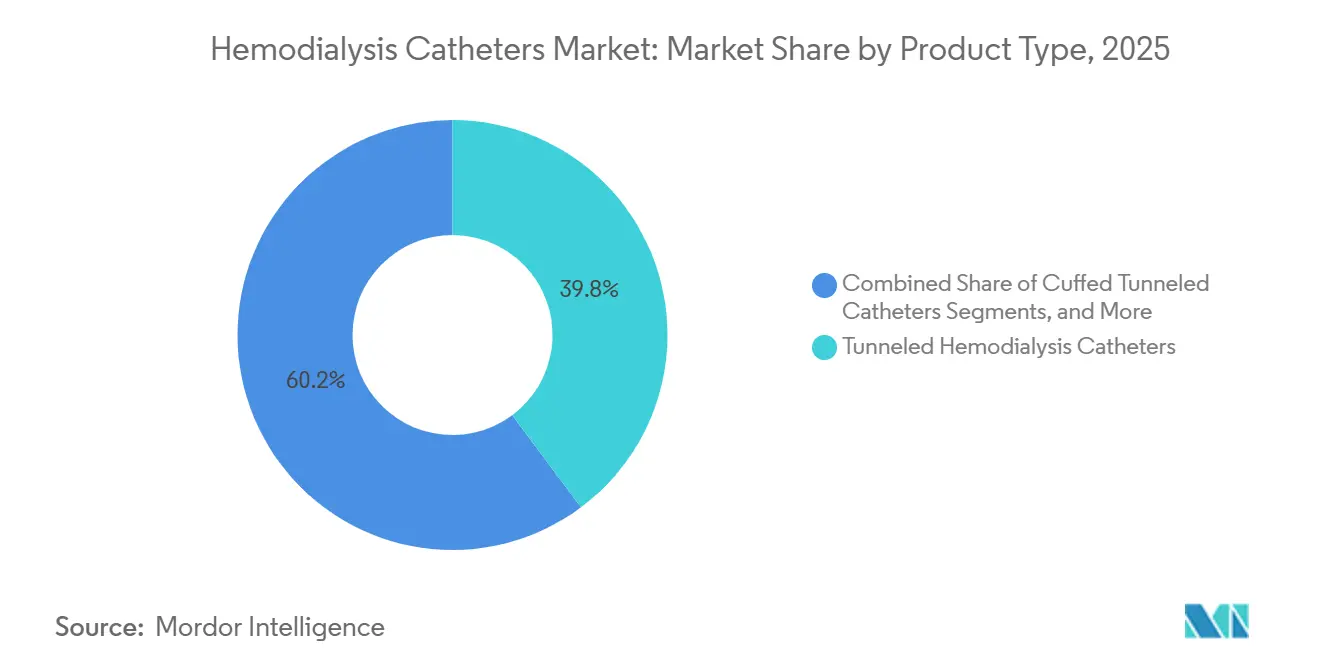

- By product type, tunneled catheters held 39.81% of the hemodialysis catheters market share in 2025, while cuffed tunneled catheters recorded the highest projected CAGR at 6.90% through 2031.

- By material, polyurethane accounted for 46.35% of the hemodialysis catheters market size in 2025, while silicone is forecast to expand at a 7.25% CAGR through 2031.

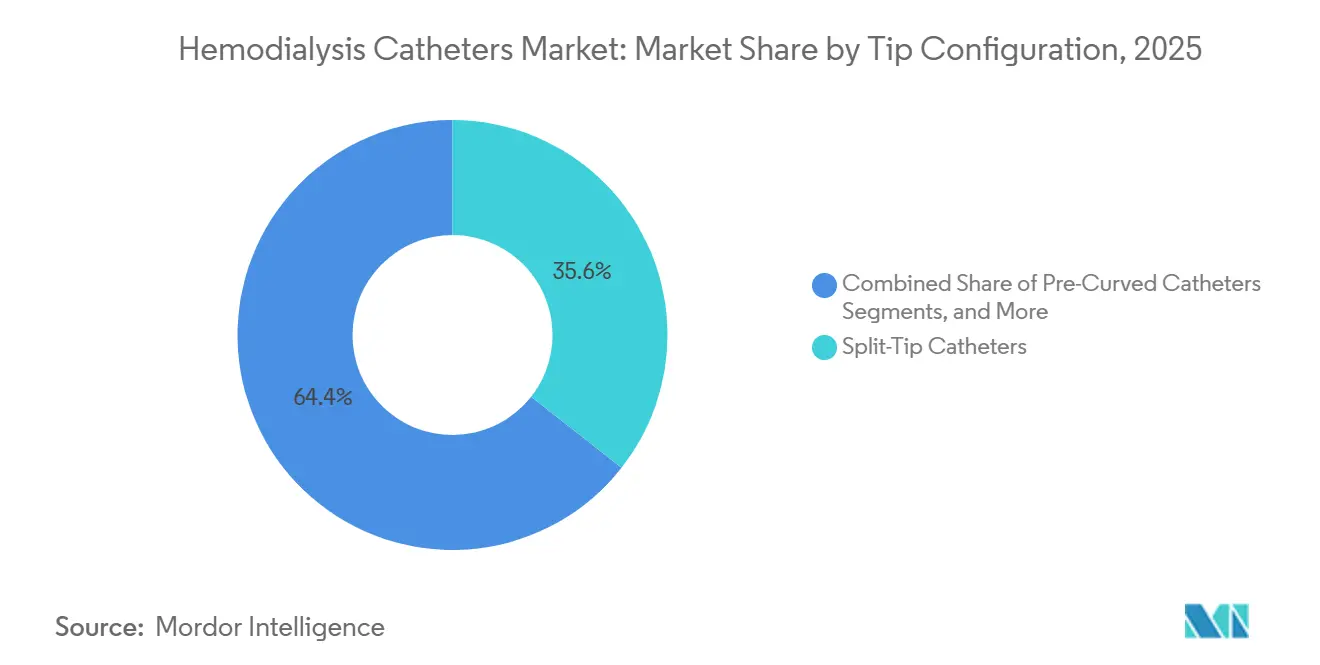

- By tip configuration, split-tip catheters led with a 35.56% share in 2025, while pre-curved catheters are projected to grow the fastest at a 7.95% CAGR through 2031.

- By application, chronic hemodialysis captured 39.76% share in 2025, while home hemodialysis is advancing at an 8.20% CAGR through 2031.

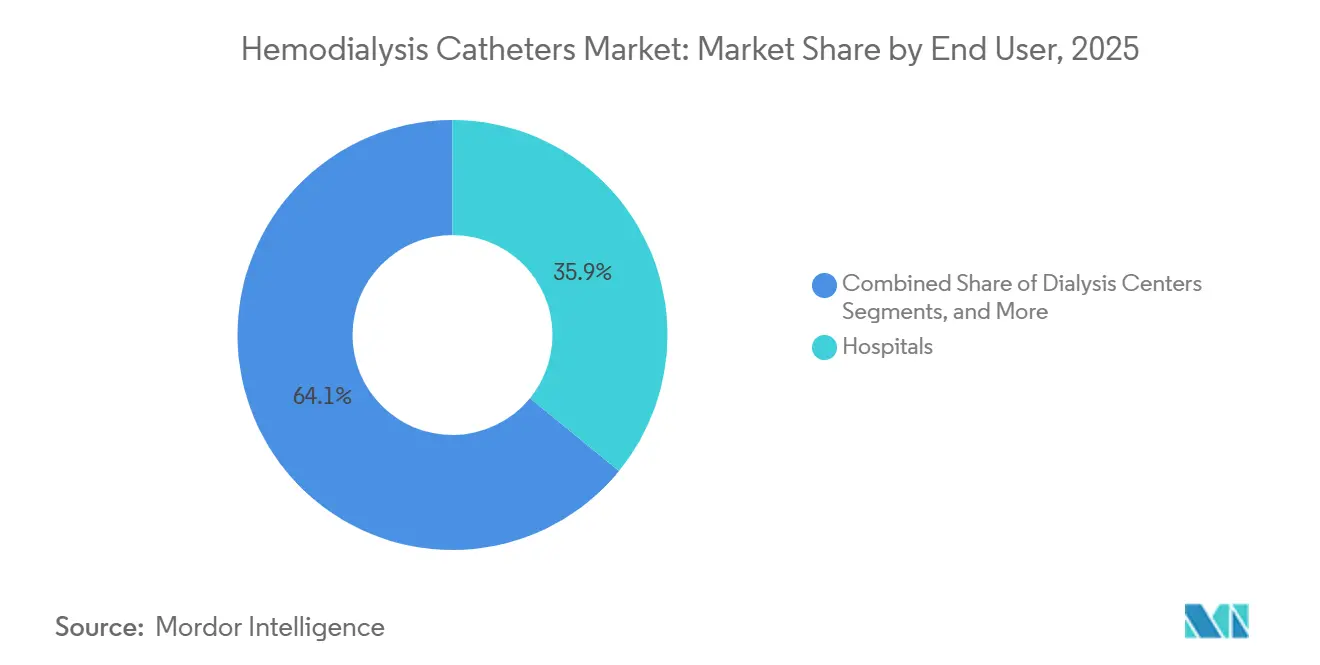

- By end user, hospitals held 35.86% share in 2025, while dialysis centers are expected to record fastest growth at a 7.55% CAGR through 2031.

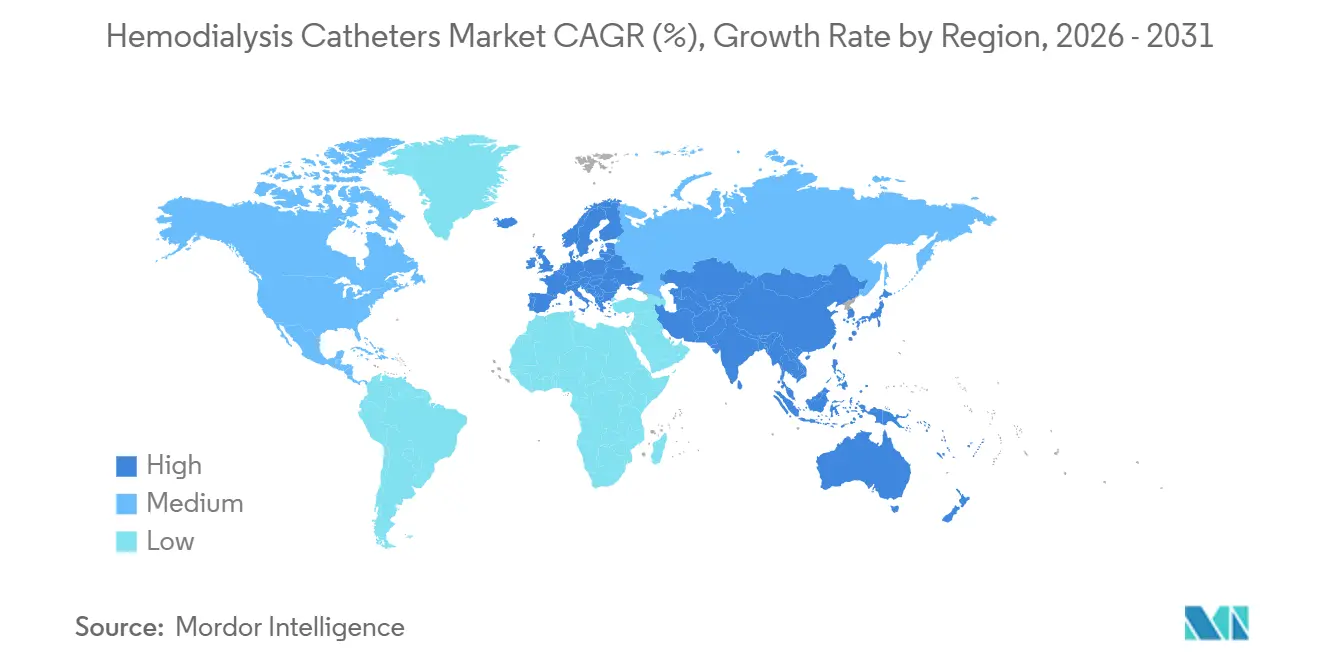

- By geography, North America led with 42.55% share in 2025, while Asia-Pacific is forecast to grow the fastest at a 6.26% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hemodialysis Catheters Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising chronic kidney disease and end-stage renal disease prevalence | +0.8% | Global, strongest in North America, Asia-Pacific, and Middle East and Africa | Long term (≥ 4 years) |

| Growing reliance on catheter-based initiation of hemodialysis | +0.6% | Global, with stronger impact in emerging markets | Short term (≤ 2 years) |

| Rising demand for antimicrobial and biocompatible catheters | +0.5% | North America and Europe, with increasing adoption in Asia-Pacific | Medium term (2-4 years) |

| Increased home hemodialysis adoption and portable alternatives | +0.4% | North America, Australia, Germany, and gradually Japan | Medium term (2-4 years) |

| Expansion of dialysis capacity in emerging markets | +0.3% | India, China, Southeast Asia, and Middle East and Africa | Long term (≥ 4 years) |

| Greater use of catheter kits and procedure-efficiency tools | +0.2% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising CKD and End-Stage Renal Disease Burden Structurally Anchors Demand

The hemodialysis catheters market is experiencing increased demand due to the rising global prevalence of chronic kidney disease (CKD). In 2025, 788 million adults worldwide were reported to have CKD, highlighting its growing importance in health system planning.[1]GBD 2023 Collaborators, “Global, Regional, and National Prevalence of Kidney Failure With Replacement Therapy and Associated Aetiologies, 1990–2023,” The Lancet Global Health, thelancet.com Regions with high disease prevalence but limited treatment access face challenges, leading to late patient arrivals and reliance on emergency catheter placements instead of planned fistula surgeries. In the U.S., the latest USRDS update showed a continued rise in both incident and prevalent end-stage renal disease (ESRD) cases, primarily driven by diabetes and hypertension. Older patients now represent a larger share of the treatment pool, with frailty and comorbidities making traditional access methods less reliable. This has led to increased use of tunneled catheters for extended periods, supporting market growth.

Catheter-Based Hemodialysis Initiation Remains the Clinical Default in Acute Settings

Despite guidelines favoring preplanned permanent access, many patients begin hemodialysis in urgent settings, sustaining demand for hemodialysis catheters. Acute kidney injury and unplanned ESRD presentations make non-tunneled central venous catheters the most practical option in hospitals and emergency units. The CMS 2025 ESRD payment update expanded Medicare coverage for home dialysis related to acute kidney injury, broadening treatment settings for catheter placement.[2]Centers for Medicare & Medicaid Services, “MM13686, ESRD and Acute Kidney Injury Dialysis, CY 2025 Updates,” CMS, cms.gov In India, dialysis capacity expanded significantly in 2025 and 2026, with 79 new dialysis centers in Telangana government hospitals and over 6,425 patients served through 4.12 lakh sessions under the PMNDP by December 2025.[3]Needle-Free Connectors in Tunneled Central Venous Catheters for Hemodialysis, A Prospective Single-Centre Safety and Feasibility Study,” PMC, pmc.ncbi.nlm.nih.gov In emerging markets, limited surgical capacity for fistula creation often results in prolonged use of emergency catheters, driving market growth alongside dialysis network expansion.

Antimicrobial and Biocompatible Catheter Engineering Becomes a Differentiator

The hemodialysis catheters market is evolving with advancements in infection control and material performance. Studies in 2025 and 2026 demonstrated the effectiveness of polyurethane-based coatings in delivering antibacterial and biocompatible properties, enhancing catheter performance. Buyers increasingly demand clinically validated designs, moving beyond marketing claims. The CMS 2025 update introduced a dedicated HCPCS code for taurolidine citrate heparin catheter locking solutions, strengthening reimbursement support for advanced catheter care. These developments are driving the market toward innovative platforms that combine material durability with infection-control features.

Home Hemodialysis Growth Reshapes Catheter Design Requirements

The rapid growth of home hemodialysis is reshaping catheter design requirements, emphasizing patient comfort, ease of use, and infection risk reduction. Home hemodialysis is the fastest-growing application, with an 8.20% CAGR through 2031. Fresenius Medical Care reported that 16% of its U.S. dialysis treatments were home-based in 2025, with over 15,300 patients using the NxStage portable system, a 6% increase from 2024. A 2025 safety study supported the use of needle-free connectors on tunneled catheters in home settings.[4]Synthetic Engineering of Central Venous Catheter Based on Antibacterial Endothelial Simulation,” Frontiers in Materials, frontiersin.org While home penetration remains limited in some developed markets due to reimbursement structures or patient preferences, the market is shifting toward lighter, safer, and more user-friendly catheter designs to meet the demands of home-based treatments.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Catheter-related bloodstream infections, thrombosis, and associated clinical complications | -0.7% | Global, with strongest pressure in North America and Europe where infection metrics are closely tracked | Medium term (2-4 years) |

| Shift toward arteriovenous fistula and graft vascular access pathways | -0.4% | North America, Europe, and Japan | Medium term (2-4 years) |

| Shortage of skilled vascular access operators | -0.2% | Asia-Pacific, Middle East and Africa, and rural North America | Long term (≥ 4 years) |

| Hospital budget pressure and reimbursement sensitivity | -0.2% | Europe and emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

CRBSI and Thrombosis Impose Clinical, Regulatory, and Commercial Costs

Catheter-related bloodstream infections (CRBSI) and thrombosis significantly challenge the hemodialysis catheters market by impacting patient safety, increasing hospital costs, and influencing procurement decisions. A 2025 study highlighted that sodium bicarbonate locks achieved infection-free catheter survival rates comparable to gentamicin citrate locks and better than heparin locks. Thrombosis exacerbates these issues by promoting biofilm development, reducing flow, and increasing device abandonment risks. Hospitals now demand measurable performance metrics for premium products, driven by CDC dialysis safety guidance emphasizing strict catheter care, observation, and aseptic practices. This scrutiny raises the competitive bar for manufacturers defending price and market share.

Arteriovenous Fistula Prioritization Redirects, but Does Not Eliminate, Catheter Use

The hemodialysis catheters market faces ongoing pressure from the preference for arteriovenous fistulas (AVFs) and grafts over catheters for permanent access. The 2025 KDOQI vascular access guideline shifted to a personalized approach for end-stage kidney disease patients while still advocating reduced catheter exposure. A 2025 review noted high AVF maturation failure rates among female, elderly, and severe vascular disease patients, highlighting the uneven transition away from catheters. The UK Kidney Association's 2025 update reflects a more selective approach to catheter use. In regions like China, India, and parts of the Middle East and Africa, delayed referrals and limited fistula surgery capacity sustain catheter dependency, while North America, Western Europe, and Japan experience stronger pressure to reduce catheter use.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Tunneled Catheter Dominance Coexists With Cuffed Design Acceleration

In 2025, tunneled catheters held a 39.81% share of the hemodialysis catheters market, maintaining their position as the leading product type. Their dominance is driven by their widespread use among chronic patients who face challenges with fistula creation, are awaiting access maturation, or are unsuitable for surgical access. Clinicians prefer tunneled systems for their stable flow and extended dwell period, which non-tunneled devices cannot provide. Within this category, cuffed designs are projected to grow at a 6.90% CAGR through 2031, reflecting a shift in demand.

Cuffed designs are gaining traction due to their ability to reduce dislodgement risks and create a barrier against bacterial migration through tissue ingrowth around the cuff. Products like Mozarc Medical’s Palindrome Precision line and Teleflex's Arrow ErgoPack systems with antimicrobial technology highlight the segment's evolution toward feature-rich offerings. Non-tunneled catheters remain essential in emergency and ICU settings, where placement speed is critical. The aging dialysis population further drives the relevance of tunneled cuffed devices, as many elderly patients remain catheter-dependent longer than anticipated, balancing urgent-use volume with chronic-care value.

By Material: Polyurethane Leads While Silicone Gains on Biocompatibility Claims

In 2025, polyurethane accounted for 46.35% of the hemodialysis catheters market, making it the leading material. Its mechanical strength, radiopacity, and compatibility with sterilization and coating processes make it suitable for both acute and chronic catheter formats. Polyurethane's leadership is also linked to its adoption in standard product families from major suppliers. Silicone, however, is projected to grow at a 7.25% CAGR through 2031, making it the faster-growing material category.

Material competition is evolving, with future advancements likely to focus on modified polymer chemistry rather than replacing polyurethane or silicone. Polyurethane is expected to maintain its leadership in the short term, while silicone gains traction in applications prioritizing long-dwell comfort and biocompatibility. Both materials are expected to remain relevant for distinct clinical needs.

By Tip Configuration: Split-Tip Proven Performance Faces Pre-Curved Design Challenge

Split-tip catheters held a 35.56% share in 2025, leading the tip configuration segment in the hemodialysis catheters market. Their success is attributed to their ability to maintain flow and minimize recirculation compared to older step-tip designs. Established product lines from Merit Medical and BD have reinforced their familiarity among physicians and buyers. However, pre-curved catheters are forecasted to grow at a 7.95% CAGR through 2031, indicating a shift in design preference.

Pre-curved catheters are gaining popularity due to their natural fit with internal jugular anatomy, reducing positional flow issues post-placement. This feature is particularly beneficial for elderly patients and those with challenging anatomies. BD’s Equistream line, offering both curved and straight options, reflects a strategy of expanding configuration choices within existing platforms, minimizing customer switching costs while advancing product portfolios.

By Application: Chronic Dialysis Scale Steady as Home Segment Accelerates

Chronic hemodialysis accounted for 39.76% of the market in 2025, making it the largest application segment. This reflects the significant ESRD population requiring consistent treatments, driving steady demand for catheter replacements and maintenance. The growing incident patient pool, particularly among diabetes and hypertension cases, underscores chronic dialysis's role as the market's foundational demand center.

Acute hemodialysis remains critical as the initial treatment for late-presenting ESRD patients and AKI cases requiring rapid intervention. Home hemodialysis is the fastest-growing segment, projected to expand at an 8.20% CAGR through 2031, supported by broader reimbursement policies and increased provider adoption. Future designs for home-use catheters are expected to enhance safer and more controlled self-management.

By End User: Hospitals Retain Volume Leadership While Dialysis Centers Grow Faster

In 2025, hospitals secured a 35.86% share, making them the primary end-user in the hemodialysis catheters market. Their dominance is linked to their roles in initial placements, acute stabilization, ICU treatments, and managing unplanned dialysis patients. Emergency and critical care units heavily rely on non-tunneled catheters, emphasizing the importance of timely treatment initiation. Hospitals also play a pivotal role in addressing complex access-related complications, revisions, and infections, solidifying their leading share even as outpatient dialysis services expand.

Dialysis centers, however, are on a growth trajectory, projected to expand at a 7.55% CAGR through 2031, making them the fastest-growing end-user segment. Their rise is fueled by both private chain expansions and government-supported capacity additions, particularly in regions where district-level services are scaling up. NephroPlus exemplifies this trend, showcasing expansion across India, the Philippines, Uzbekistan, and Saudi Arabia, underscoring how organized networks can amplify recurring access demand. Additionally, in the U.S., ambulatory surgical centers are gaining prominence for insertion procedures, especially as certain hospital systems reduce their in-center dialysis offerings.

Geography Analysis

In 2025, North America held a 42.55% share of the hemodialysis catheters market, maintaining its position as the largest regional player. The United States led this dominance due to its extensive dialysis patient base, advanced insertion capabilities, and widespread use of tunneled catheters in chronic care. The CMS CY 2025 ESRD payment update, which introduced AKI home dialysis payment parity and a new HCPCS code for taurolidine heparin locking solutions, strengthened the catheter care environment. MedPAC projected a 1.7% increase in the 2026 Medicare base payment rate for dialysis services, signaling a positive economic outlook for facilities. In Canada, transplant limitations sustained demand by keeping a significant chronic hemodialysis population in long-term treatment.

Europe remained a key player in the hemodialysis catheters market in 2025, driven by an aging population and a significant CKD burden. As of January 2025, 21.6% of the EU population was aged 65 or older, supporting consistent demand for renal replacement therapies. A CKD analysis reported a median prevalence of 12.8% in Eastern and Central Europe, highlighting the region's renal disease challenges. Germany, the UK, and France led the market, though the adoption of premium-coated catheters varied due to differing reimbursement and procurement policies.

Asia-Pacific is projected to grow at a 6.26% CAGR through 2031, making it the fastest-growing regional segment in the hemodialysis catheters market. China and India are driving this growth by expanding dialysis capacity to address unmet renal care needs. In 2025, China's dialysis population reached 1.34 million, with domestic producers increasing their role in local supply, supporting volume growth and reducing import dependency. India's Pradhan Mantri National Dialysis Programme, with over 1,200 district hospital centers by 2025, enhanced treatment access and increased demand for reliable catheter procurement. Japan remains clinically advanced with stringent standards, while South America and the Middle East and Africa are expanding through public renal care programs and selective private network growth.

Competitive Landscape

Global medtech giants dominate the hemodialysis catheters market, controlling a significant portion of its value. Meanwhile, regional suppliers are more active in competing within price-sensitive segments. Key players include Becton Dickinson, Teleflex, Mozarc Medical, Fresenius Medical Care, Merit Medical, B. Braun, and Cook Medical. Competition among these companies extends beyond mere catheter availability. It is increasingly influenced by features like infection control, support for insertion workflows, and evidence of long-term stable performance. Consequently, the market prioritizes depth of features and clinical credibility over mere portfolio breadth. Additionally, procurement pressures from hospital systems and organized dialysis networks challenge smaller suppliers, making it essential for them to offer distinct product differences to scale.

In April 2026, BD introduced the CentroVena One insertion system, an all-in-one central line device, pushing competition into procedural efficiency and safety. In June 2025, Fresenius Medical Care expanded U.S. commercialization of its 5008X CAREsystem after FDA clearance, a move that redefined expectations for vascular access products. Teleflex's kit expansion and Mozarc's innovations in chronic dialysis catheters highlight the market's shift toward workflow support and chronic-use optimization as key competitive advantages. The market favors companies that combine device performance with straightforward, defensible clinical applications.

Asian manufacturers are increasingly navigating regulatory pathways to penetrate higher-value markets. For instance, Haolang Medical USA Corporation secured FDA 510(k) clearance for its hemodialysis catheter in May 2025, marking a significant entry of Chinese designs into the U.S. market. However, the landscape is not without challenges. A February 2026 Class I recall, linked to a sheath introducer component, impacted both Merit Medical and Arrow-associated kits, highlighting the swift repercussions of safety events in the industry. This blend of innovation, regulatory navigation, and stringent quality checks keeps the competitive arena lively, even in the absence of a clear market leader. While the hemodialysis catheters market leans toward established players, it remains sufficiently open for compliant newcomers to carve out niches.

Hemodialysis Catheters Industry Leaders

B. Braun SE

Medtronic plc

Teleflex Incorporated

Becton, Dickinson and Company

Fresenius Medical Care AG and Co. KGaA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Mozarc Medical announced plans for a 4,500 square-meter renal access catheter manufacturing facility in Costa Rica, targeting full-scale operations by September 2026.

- December 2025: CorMedix Therapeutics reported interim results from a real-world study on DefenCath use in adult hemodialysis patients with central venous catheters.

- June 2025: Fresenius Medical Care began broader U.S. commercialization of the 5008X CAREsystem after receiving FDA clearance in May 2025, with a full launch planned for 2026.

- May 2025: Haolang Medical USA Corporation received FDA clearance for its hemodialysis and apheresis catheter, marking the entry of a China-origin design into the U.S. market.

Global Hemodialysis Catheters Market Report Scope

As per the scope of the report, a hemodialysis catheter is a flexible tube placed into a large vein (usually in the neck or chest) to quickly remove blood, filter it through a machine, and return it to the body. It acts as temporary vascular access for people with kidney failure.

The hemodialysis catheters market is segmented by product type, material, tip configuration, application, end-user, and geography. By product type, the market includes tunneled hemodialysis catheters (cuffed tunneled catheters and non-cuffed tunneled catheters) and non-tunneled hemodialysis catheters (single lumen non-tunneled catheters, double lumen non-tunneled catheters, and triple lumen non-tunneled catheters). By material, the market is segmented into polyurethane, silicone, and composite & other polymer materials. By tip configuration, the market is categorized into step-tip catheters, split-tip catheters, symmetric catheters, and pre-curved catheters. By application, the market is segmented into chronic hemodialysis, acute hemodialysis, and home hemodialysis. By end-user, the market is segmented into hospitals, dialysis centers, ambulatory surgical centers, and home care settings. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Tunneled Hemodialysis Catheters |

| Cuffed Tunneled Catheters |

| Non-Cuffed Tunneled Catheters |

| Non-Tunneled Hemodialysis Catheters |

| Single Lumen Non-Tunneled Catheters |

| Double Lumen Non-Tunneled Catheters |

| Triple Lumen Non-Tunneled Catheters |

| Polyurethane |

| Silicone |

| Composite and Other Polymer Materials |

| Step-Tip Catheters |

| Split-Tip Catheters |

| Symmetric Catheters |

| Pre-Curved Catheters |

| Chronic Hemodialysis |

| Acute Hemodialysis |

| Home Hemodialysis |

| Hospitals |

| Dialysis Centers |

| Ambulatory Surgical Centers |

| Home Care Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Tunneled Hemodialysis Catheters | |

| Cuffed Tunneled Catheters | ||

| Non-Cuffed Tunneled Catheters | ||

| Non-Tunneled Hemodialysis Catheters | ||

| Single Lumen Non-Tunneled Catheters | ||

| Double Lumen Non-Tunneled Catheters | ||

| Triple Lumen Non-Tunneled Catheters | ||

| By Material | Polyurethane | |

| Silicone | ||

| Composite and Other Polymer Materials | ||

| By Tip Configuration | Step-Tip Catheters | |

| Split-Tip Catheters | ||

| Symmetric Catheters | ||

| Pre-Curved Catheters | ||

| By Application | Chronic Hemodialysis | |

| Acute Hemodialysis | ||

| Home Hemodialysis | ||

| By End User | Hospitals | |

| Dialysis Centers | ||

| Ambulatory Surgical Centers | ||

| Home Care Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2031 value of the hemodialysis catheters space?

The report places the 2026 value at USD 0.985 billion and forecasts it to reach USD 1.26 billion by 2031 at a 5.16% CAGR.

Which product category leads catheter demand in dialysis access?

Tunneled catheters led product demand with a 39.81% share in 2025, reflecting their central role in chronic dialysis access.

Which application is growing the fastest through 2031?

Home hemodialysis is the fastest-growing application, with an 8.20% CAGR through 2031, supported by broader reimbursement and expanding use of home systems.

Why does North America remain the largest regional revenue contributor?

North America held 42.55% share in 2025 because of its large dialysis base, strong reimbursement structure, and high use of tunneled catheters in chronic care.

What is the biggest clinical risk affecting catheter adoption?

Catheter-related bloodstream infections and thrombosis remain the key risks because they raise hospital costs, trigger procurement reviews, and intensify regulatory and clinical scrutiny.

Which end-user group is expanding the fastest?

Dialysis centers are growing the fastest, with a 7.55% CAGR through 2031, as private operators and public programs continue to expand treatment capacity.

Page last updated on: