Hemodialysis Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

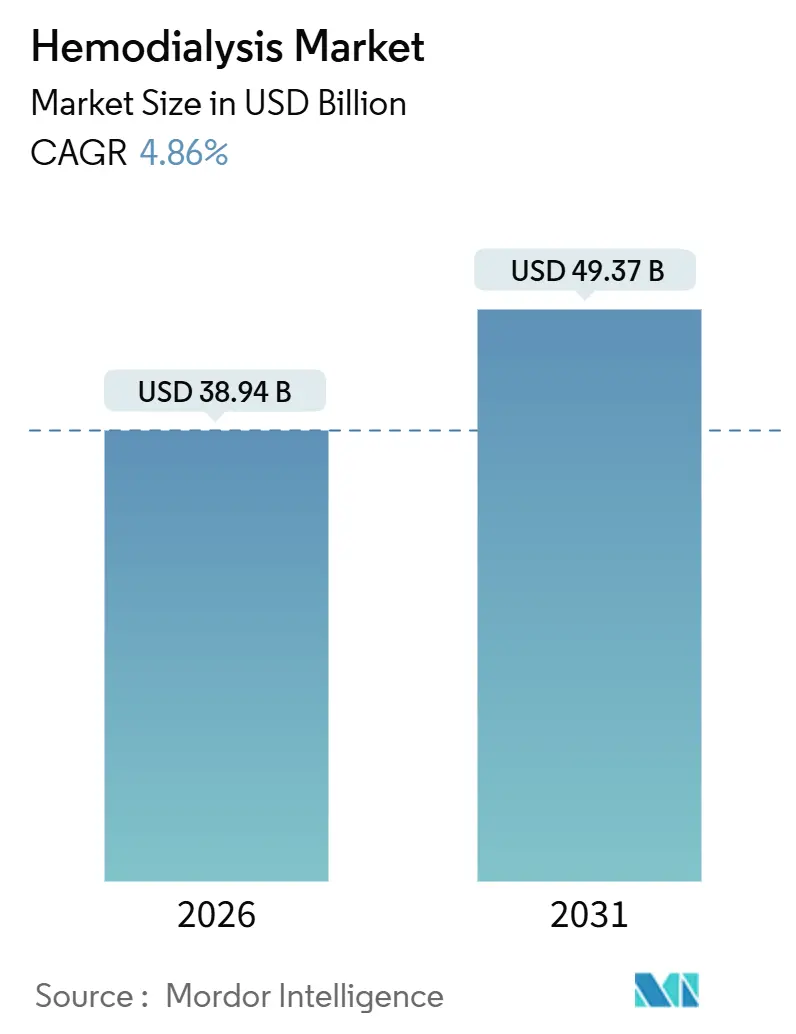

| Market Size (2026) | USD 38.94 Billion |

| Market Size (2031) | USD 49.37 Billion |

| Growth Rate (2026 - 2031) | 4.86% CAGR |

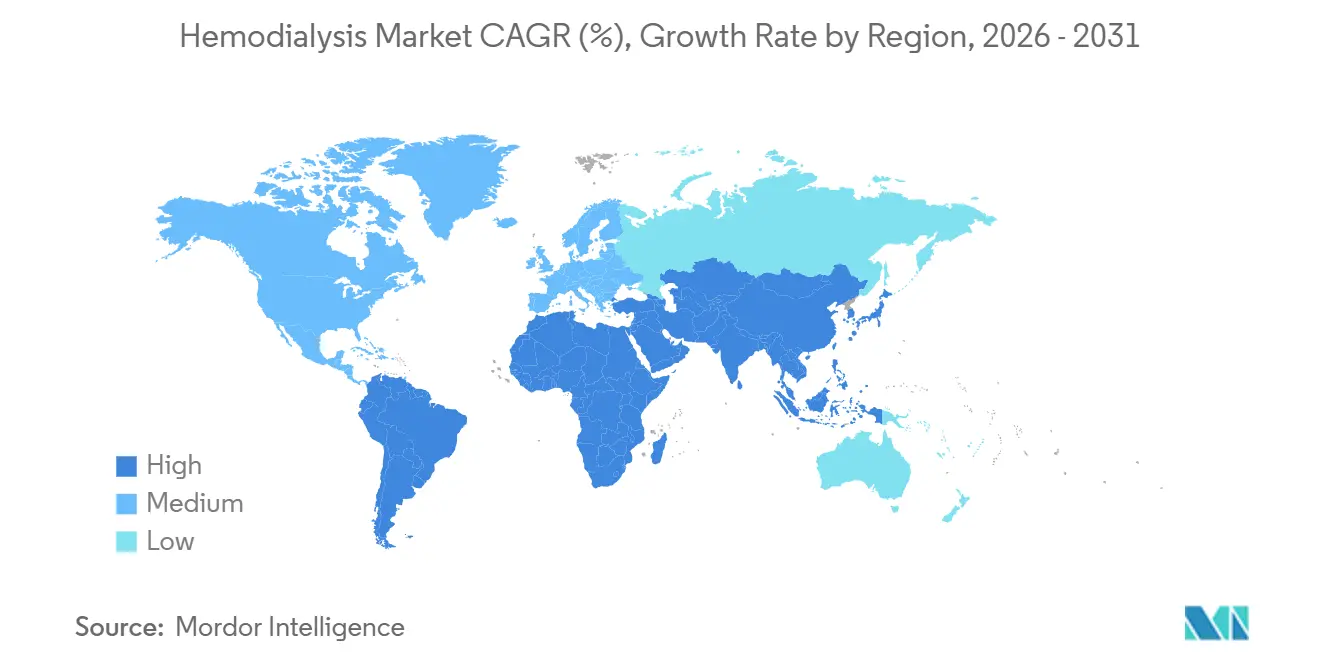

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hemodialysis Market Analysis by Mordor Intelligence

The Hemodialysis Market size is estimated at USD 38.94 billion in 2026, and is expected to reach USD 49.37 billion by 2031, at a CAGR of 4.86% during the forecast period (2026-2031).

Steady prevalence growth of end-stage renal disease, stronger reimbursement incentives for home care, and continual equipment-plus-consumable business models are the primary forces sustaining revenue expansion. Multinational providers are deepening localization programs in Asia to offset price pressure from emerging Chinese vendors. At the same time, integrated tele-nephrology systems that feed real-time patient data to clinicians are cutting emergency admissions, proving the business case for digital add-ons. Heightened regulatory attention on water efficiency and breakthrough portable-kidney devices remains a long-horizon risk, but recurring consumables demand still secures predictable cash flows for investors.

Key Report Takeaways

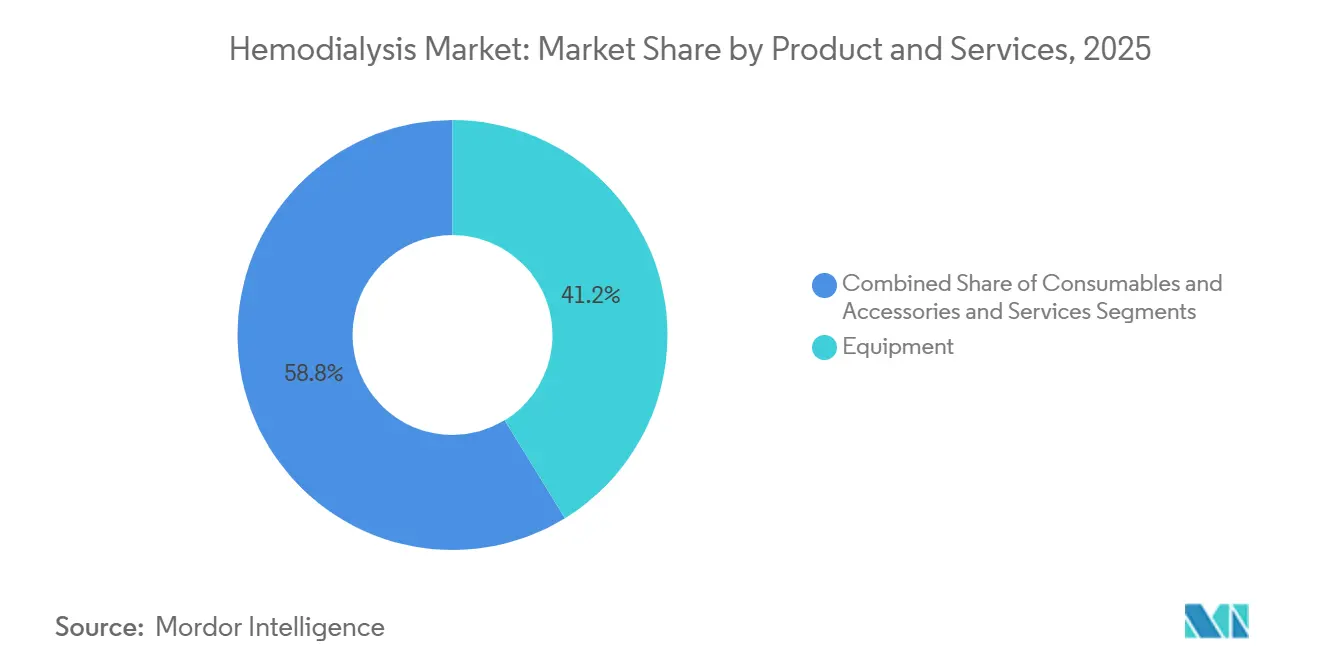

- By products and services, equipment led with a 41.24% revenue share in 2025; consumables and accessories are forecast to expand at an 8.34% CAGR through 2031.

- By modality, conventional long-hour treatments captured 64.55% of volumes in 2025, while short daily sessions are advancing at a 7.46% CAGR to 2031.

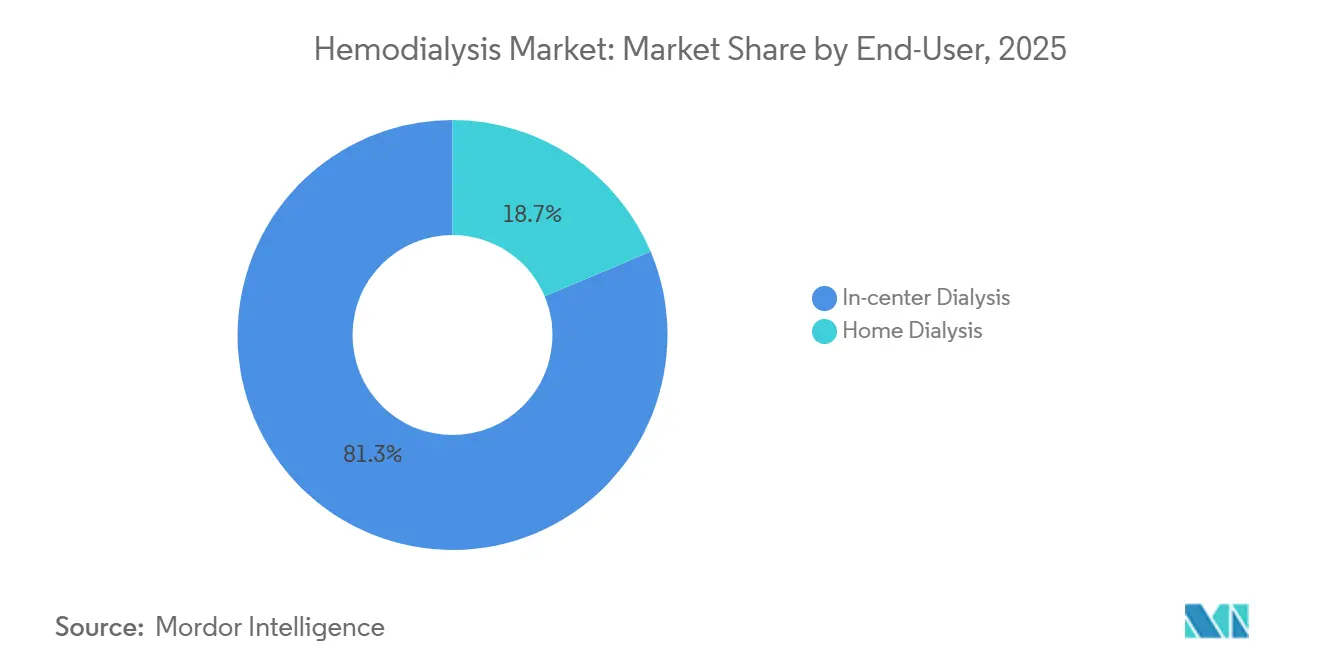

- By end user, in-center dialysis accounted for 81.34% of the hemodialysis market share in 2025; home dialysis is projected to grow at a 6.37% CAGR over the same period.

- By geography, North America contributed 38.54% of 2025 revenue, whereas Asia-Pacific is set to register the fastest 7.02% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hemodialysis Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global prevalence of end-stage renal disease | +1.2% | North America, Asia-Pacific | Long term (≥ 4 years) |

| Growing adoption of home hemodialysis | +0.9% | North America, Australia, select EU markets | Medium term (2-4 years) |

| Reimbursement expansions in major markets | +0.8% | United States, Germany, Japan, South Korea | Short term (≤ 2 years) |

| Technological innovations in high-flux dialyzers | +0.7% | Global | Medium term (2-4 years) |

| Integration of tele-nephrology monitoring | +0.6% | North America, Western Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Public-private dialysis roll-outs in LMICs | +0.5% | India, Indonesia, Philippines, Sub-Saharan Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global ESRD Prevalence

Global dialysis incidence keeps rising, exemplified by 130,754 new U.S. patients in 2024 and Japan’s total pool exceeding 350,000 by 2025. Diabetes and hypertension explain most cases, yet chronic kidney disease of unknown etiology in agricultural belts of Central America and South Asia is accelerating demand.[2]John Doe, “Kidney Disease Statistics 2025,” Kidney International, kidney-international.org Rural expansion programs, such as China’s USD 1.2 billion county-level build-out, widen the addressable base. Because ESRD is non-elective, these demographics underpin secular volume growth that insulates the hemodialysis market from economic cycles. As incidence rises, providers must scale staff and infrastructure, cementing equipment and consumable pull-through.

Growing Adoption of Home Hemodialysis

Home penetration reached 12.8% of U.S. dialysis patients by mid-2025, buoyed by Medicare incentives that reward nephrologists for prescribing home therapy.[3]Centers for Medicare & Medicaid Services, “Home Dialysis Competitive Acquisition Program,” CMS, cms.gov Systems like Outset Medical’s Tablo remove separate water-treatment needs, slashing setup costs by 40%. Australia leads OECD peers with 22% of new patients starting at home thanks to 85% equipment subsidies and caregiver training mandates. Workforce shortages—nephrology nurse vacancy rates stood at 18% in 2025—push stakeholders toward self-care pathways. Coupled with user-friendly interfaces and remote troubleshooting, home programs are positioned to win younger, working-age cohorts.

Reimbursement Expansions in Major Markets

The 2025 Medicare fee schedule lifted the bundled payment for home dialysis by 4.7%, narrowing the differential with clinic sessions. Germany’s G-BA added a new code for tele-nephrology visits, trimming mandatory in-person checks to quarterly. Japan passed its first dialysis tariff increase in four years, easing capital upgrade burdens on public centers. South Korea extended high-flux dialyzer coverage to all residual-function patients, enlarging the eligible cohort by 28,000. These policy moves safeguard provider margins and affirm dialysis as essential healthcare, accelerating the hemodialysis market’s revenue certainty.

Technological Innovations in High-Flux Dialyzers

High-flux membranes represented 61% of global shipments in 2025, up from 54% two years earlier. Asahi Kasei’s APS-EA dialyzer cuts dialysis-related amyloidosis by 22% through superior β-2 microglobulin removal. Nipro’s hydrophilic-coated FIX series extends reuse cycles to 18 sessions, trimming per-treatment costs by USD 3.50. Cardiovascular mortality benefits associated with middle-molecule clearance strengthen payer appetite for such upgrades. Providers therefore accept a 15% price premium, reinforcing equipment makers’ shift toward outcome-oriented product positioning.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High treatment costs versus peritoneal dialysis | -0.6% | Global, especially cost-sensitive LMICs | Medium term (2-4 years) |

| Vascular-access infections and complications | -0.5% | North America, Europe | Short term (≤ 2 years) |

| Emerging wearable artificial-kidney substitutes | -0.3% | North America, Western Europe | Long term (≥ 4 years) |

| Water-scarcity regulations on ultrapure water | -0.2% | Middle East, North Africa, Western United States | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Treatment Costs Versus Peritoneal Dialysis

Annual in-center hemodialysis spending averages USD 89,000 in the United States versus USD 62,000 for peritoneal dialysis, prompting PD-first mandates in Canada, the U.K., and Australia. Hong Kong achieved 78% PD initiation in 2025 by paying nephrologists a premium for PD oversight. Escalating nurse pay—up 8.2% annually from 2023-25—amplifies this cost gap. While hemodialysis remains vital for patients unable to handle PD logistics, value-based purchasing schemes highlight its relative expense, moderating uptake in some health systems.

Vascular-Access Infections and Complications

Central venous catheter infections generate 18% of all dialysis hospitalizations, costing USD 22,000 per episode and extending stay by up to 10 days. U.S. infection rates have not improved since 2023 despite stricter protocols. AV fistula maturation failure persists at 25-30% among elderly diabetics. Medtronic’s antibiotic-eluting graft lowers infection risk but carries a USD 1,200 premium, limiting uptake. These complications reduce patient quality of life and raise payer outlays, tempering enthusiasm for hemodialysis in risk-sharing reimbursement models.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Products and Services: Recurring Consumables Drive Growth

Consumables and accessories are projected to expand at an 8.34% CAGR to 2031, surpassing equipment’s 41.24% share in the hemodialysis market as of 2025. Razor-and-blade strategies, such as Nikkiso’s USD 500 monthly subscription machine, bundle bloodlines, concentrates, and service into one predictable fee. Global shipments of bloodlines and tubing surpassed 1.2 billion units in 2025, reflecting their single-use necessity.

High-flux therapy protocols raise bicarbonate-dialysate demand, adding USD 3 per treatment in concentrate revenue. Antimicrobial-coated catheters captured 22% of the North American subsector, demonstrating clinicians' willingness to invest in infection mitigation. Services, from maintenance to on-site water-system management, grow 5.2% annually as independent clinics outsource biomedical engineering tasks. This consumables-heavy mix insulates the hemodialysis market size from capital-budget cycles while anchoring manufacturers to patient retention metrics.

By Modality: Short Daily Sessions Improve Workforce Productivity

Conventional thrice-weekly schedules still dominate with 64.55% of 2025 volume, yet short daily hemodialysis is climbing at a 7.46% CAGR, powered by employer clinics that cut absenteeism by 22 days per year. Meta-analysis shows 16% fewer cardiovascular events with the 5-6-day regimen, supporting payer coverage. Retail giants like Amazon host on-site units, signaling broader corporate health adoption. Fresenius shipped 18,000 NxStage System One devices in 2025, indicating convergence between short daily and home settings. Meanwhile, nocturnal therapy holds only 4.2% share due to patient reluctance and staffing hurdles. As outcome-based payment expands, short daily options are poised to capture incremental hemodialysis market share alongside home platforms.

By End User: Home Dialysis Gains on Policy Parity

In-center facilities represented 81.34% of 2025 sessions, but reimbursement parity is lifting home uptake at a 6.37% CAGR through 2031. The ETC Model pushed participant practices to 13.2% home prevalence in 2025, up from 8.9% in 2022. Outset Medical’s dual-setting Tablo allows seamless migration, easing training costs and CAPEX risk. Hospital divestitures—47 U.S. units closed in 2024—are sending volumes to specialized clinic chains. Rural mobile units funded by FEMA keep growth steady in underserved zones. Australia tops peers at 22% home penetration owing to subsidies, whereas Japan lags below 3% due to cultural preferences and limited tariffs. Infection-avoidance remains a post-pandemic driver cited by 38% of surveyed home patients. As digital monitoring narrows the clinical-outcome gap, payers increasingly endorse home pathways that lower long-term costs and expand the hemodialysis market size for remote-capable devices.

Geography Analysis

North America contributed 38.54% of 2025 revenue, anchored by Medicare’s USD 240 per-session clinic payment and a 550,000-patient base. Incident ESRD growth slowed to 1.8% in 2024, yet mortality fell to 16.2%, reflecting cardiovascular-care improvements. Canada’s British Columbia achieved 28% home penetration via compulsory education and nephrologist bonuses. Mexico’s Seguro Popular now funds twice-weekly treatments, adding 18,000 slots by 2027.

Europe captured 29% of global revenue, led by Germany’s 1,350 per-million prevalence under generous tariffs. France’s pre-emptive transplant rate hit 18%, tempering volume growth but improving outcomes. The U.K. mandate that suitable patients start at home lifted national home prevalence to 19% in 2025. Spain and Italy leverage European Investment Bank financing to modernize rural centers.

Asia-Pacific is the fastest-growing segment at a 7.02% CAGR, propelled by China’s 820,000-patient population yet low 570 per-million penetration. India expanded district-hospital dialysis to 680 sites through public-private concessions. Japan recorded its first dialysis decline, down 0.8% in 2025 after aggressive CKD screening. Tele-nephrology deployments in South Korea and Australia reduce hospitalizations by 14% among 12,000 monitored home patients.

The Middle East and Africa held 6.2% of revenue, with Saudi Arabia’s Vision 2030 expanding capacity to 42,000 patients in 2025. UAE water mandates force centers to install recycling systems, raising CAPEX yet improving efficiency. Solar-powered pilots in Kenya lower energy costs by 30%, offering a blueprint for rural Sub-Saharan Africa.

South America made up 4.8% of revenue, dominated by Brazil’s 144,000 publicly funded patients under SUS despite tariff stagnation since 2018. Argentina’s currency pressures triggered operator exits in 2025, whereas Chile’s 12% tariff hike revived investment. Colombia opened 35 rural centers in 2024 through municipal programs.

Competitive Landscape

Fresenius Medical Care and DaVita manage more than 8,500 global clinics, treating around 450,000 patients, yet the top five equipment suppliers hold slightly more than half of dialyzer shipments, marking medium concentration. Chinese entrants slash prices up to 30% in tender markets, pushing incumbents to localize and offer volume discounts. Fresenius’s 2025 AI-diagnostics acquisition strengthens its predictive-analytics edge for vascular-access risk. Outset Medical’s Tablo has already seized 18% of U.S. home-equipment sales by removing water-treatment barriers.

Digital integration is the new differentiator: Baxter’s Sharesource monitored 60,000 patients worldwide in 2025, cutting unplanned admissions by 19%. Quanta Dialysis’s SC+ earned CE Mark for disaster-response uses, nudging equipment toward portability. Wearable-kidney patent filings rose 34% across 2024-25, with Xcorporeal and the Kidney Project leading innovations that could redefine the hemodialysis market in the next decade. ISO 13485 quality standards and EU MDR compliance increase fixed-cost hurdles, advantaging established manufacturers. Private-equity roll-ups totaled USD 1.8 billion across 23 clinic deals in 2025, spotlighting the segment’s defensive cash flow.

Hemodialysis Industry Leaders

Asahi Kasei Corporation

B Braun Melsungen AG

Fresenius Medical Care AG & Co. KGaA

Baxter International Inc.

Nipro Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Lords Mark India moved toward a 92% stake in Renalyx Health Systems, keeping the AI-enabled SLED innovator as an independent unit.

- June 2025: Renalyx Health Systems launched the RENALYX – RxT 21 AI-and-cloud-connected smart hemodialysis machine with real-time remote monitoring.

- June 2025: Fresenius Medical Care secured FDA 510(k) clearance for the hemodiafiltration-ready 5008X CAREsystem, paving the way for a full U.S. launch in 2026.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the global hemodialysis market as the revenue generated from (1) capital equipment such as dialysis machines, dialyzers, bloodline sets, concentrates, and water-treatment units and (2) fee-based treatment sessions delivered in in-center and home settings. We track values at manufacturer and service-provider invoice levels, converted to constant 2025 US dollars for cross-regional comparability.

Scope exclusion: Peritoneal dialysis products, transplant drugs, and vascular grafts are outside this study.

Segmentation Overview

- By Products and Services

- Equipment

- Hemodialysis Machines

- Dialysate Delivery Systems

- Others

- Consumables and Accessories

- Bloodlines & Tubing Sets

- Concentrates & Solutions

- Hemostasis Devices

- Catheters & Fistula Needle

- Other consumables and accessories

- Services

- Equipment

- By Modality

- Conventional Long-hour Hemodialysis

- Short Daily Hemodialysis

- Nocturnal Hemodialysis

- By End User

- In-center Dialysis

- Hospitals

- Others

- Home Dialysis

- In-center Dialysis

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor's team interviewed nephrologists, biomedical engineers, and procurement leads across North America, Europe, China, India, and Brazil. Their insights on session mix, average selling prices, and adoption of home hemodialysis helped us validate secondary assumptions and fine-tune regional growth markers before final triangulation.

Desk Research

Our analysts gathered baseline figures from open datasets such as the USRDS annual report, European Renal Association registry, WHO Global Health Observatory, UN DESA demographic files, and national insurance tariffs, then enriched them with company filings and peer-reviewed journals. We also tapped paid platforms, including D&B Hoovers for provider financials and Dow Jones Factiva for treatment-center openings, to size corporate footprints and spot fast-scaling geographies. These sources provided patient stock, treatment frequency, reimbursement schedules, and shipment trends that form the skeleton of the market model. The list above is illustrative; many other public and subscription resources were reviewed to cross-check numbers and definitions.

Market-Sizing & Forecasting

We start with a top-down patient stock model. End-stage renal disease prevalence by country is multiplied by annual treatment sessions and average reimbursement to reach service value, which is then complemented by manufacturer shipment data for equipment and consumables. Select bottom-up checks, such as machine installed-base roll-ups and sampled ASP multiplied by dialyzer volumes, flag any outliers. Key variables include ESRD incidence, dialysis penetration versus transplant, average sessions per patient, home-therapy uptake, currency shifts, and Medicare ESRD base-rate revisions. A multivariate regression anchored on diabetic population growth and aging cohorts projects these drivers through 2030, while scenario analysis adjusts for reimbursement or technology shocks.

Data Validation & Update Cycle

Outputs pass variance and anomaly screens, peer review, and a senior analyst sign-off. The model is refreshed each year, with interim updates triggered by material policy changes or large product recalls, ensuring clients always receive the latest calibrated view.

Why Mordor's Hemodialysis Baseline Numbers Merit Trusted Adoption

Published estimates often diverge because firms slice the dialysis universe differently, convert currencies at varied cut-offs, or roll forward patient pools without checking reimbursement drift.

Key gap drivers we observe include broader inclusion of peritoneal dialysis, counting water-plant retrofits as equipment revenue, or inflating service totals by using patient expenditures rather than provider receipts, which our model avoids through a disciplined, definition-first approach and yearly refresh cadence.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 39.25 B (2025) | Mordor Intelligence | |

| USD 83.20 B (2024) | Global Consultancy A | Combines hemodialysis with peritoneal therapy and full patient out-of-pocket spends |

| USD 94.10 B (2024) | Industry Publication B | Uses clinic charge rates, excludes currency normalization, and projects on fixed 10-year CAGR |

These contrasts show how Mordor's clear scope limits, dual-source modelling, and frequent updates deliver a balanced, reproducible baseline that decision-makers can rely on.

Key Questions Answered in the Report

How large is the hemodialysis market in 2026?

The hemodialysis market size is USD 38.94 billion in 2026 and is forecast to rise to USD 49.37 billion by 2031.

What is the expected growth rate for hemodialysis to 2031?

Revenue is projected to expand at a 4.86% CAGR through 2031.

Which product segment is growing fastest?

Consumables and accessories are pacing the field with an 8.34% CAGR owing to razor-and-blade sales models.

Why is home hemodialysis gaining traction?

Reimbursement parity, simplified machines, and infection-avoidance mindsets lifted home penetration to 12.8% in the United States by mid-2025.

Which region is expanding quickest?

Asia-Pacific posts the highest 7.02% CAGR as China, India, and Southeast Asia roll out subsidized dialysis programs.

What technologies are shaping future competition?

High-flux dialyzers, tele-nephrology platforms, and early-stage wearable artificial kidneys are the key innovation themes influencing strategic investment.

Page last updated on: