U.S. Dialysis Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

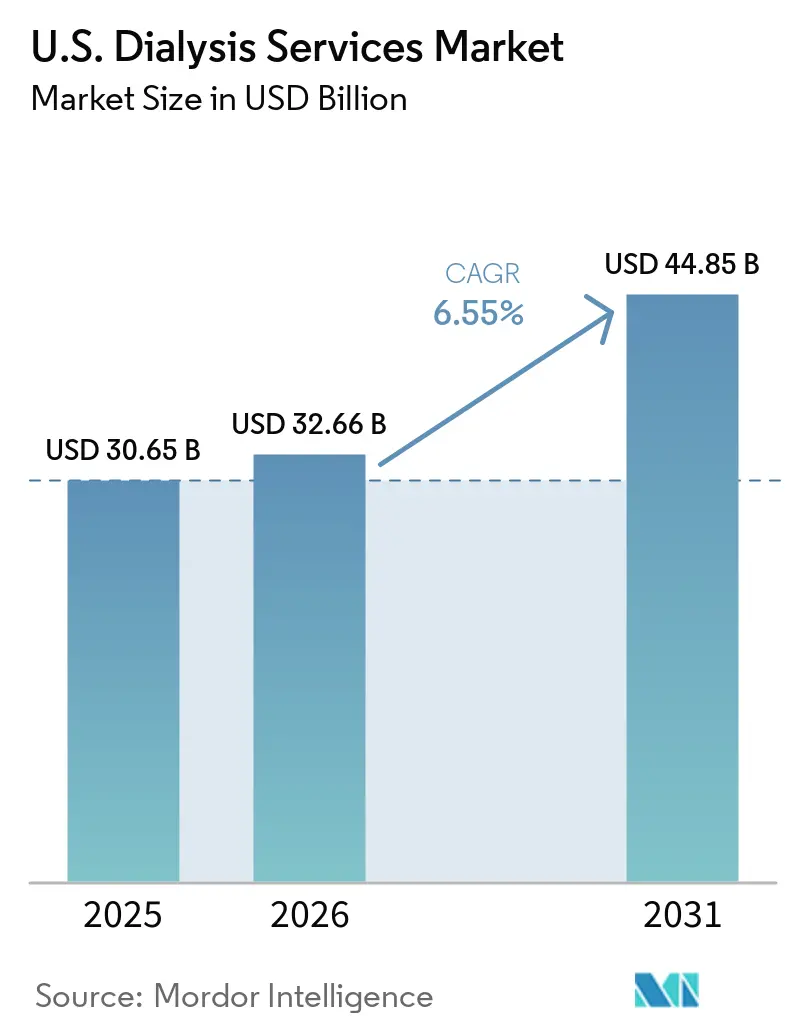

| Base Year Market Size (2025) | USD 30.65 Billion |

| Market Size (2026) | USD 32.66 Billion |

| Market Size (2031) | USD 44.85 Billion |

| Growth Rate (2026 - 2031) | 6.55% CAGR |

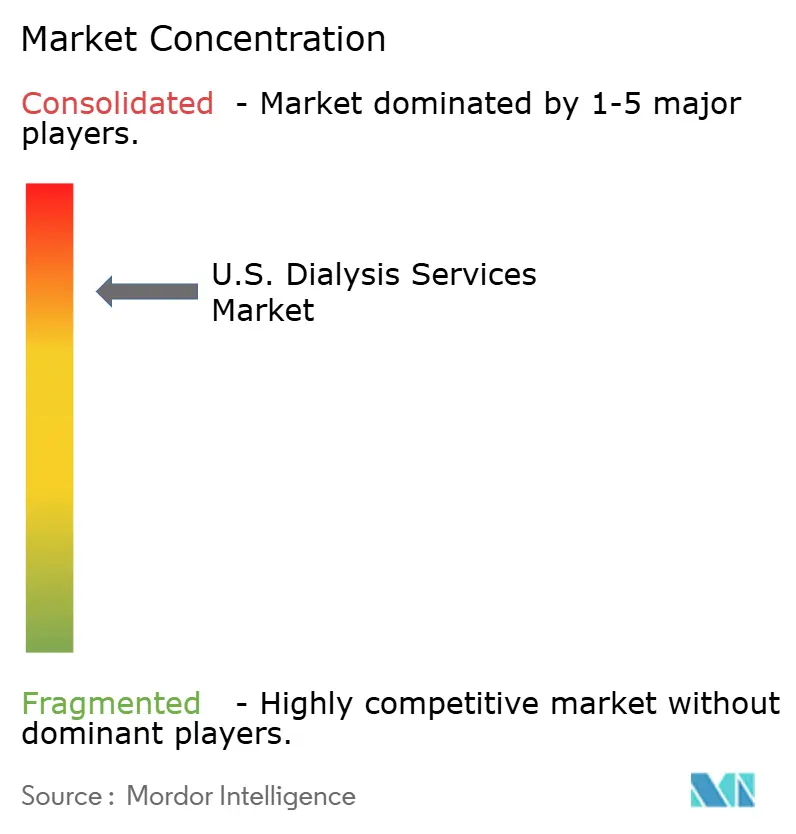

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

U.S. Dialysis Services Market Analysis by Mordor Intelligence

The U.S. Dialysis Services Market size is projected to expand from USD 30.65 billion in 2025 and USD 32.66 billion in 2026 to USD 44.85 billion by 2031, registering a CAGR of 6.55% between 2026 to 2031.

Over 808,000 Americans are living with end-stage kidney disease, with 68% relying on dialysis for life-sustaining treatment. This steady demand highlights the essential nature of dialysis services, even during fluctuations in healthcare spending. The incidence of end-stage kidney disease increased by 31.3% between 2002 and 2024, with prevalence rising by 20,000 cases annually, ensuring a consistent demand for dialysis services in the United States.[1]United States Renal Data System, “Kidney Disease Statistics for the United States,” National Institute of Diabetes and Digestive and Kidney Diseases, niddk.nih.gov

CMS projects payments of USD 6 billion to 7,600 ESRD facilities by 2026, reflecting the robust reimbursement system supporting this care setting. Medicare Advantage enrollment among dialysis patients rose significantly from 24.8% in December 2020 to 47% by December 2022, reshaping contracting, referral flows, and revenue visibility across the United States dialysis services market.[2]Centers for Medicare & Medicaid Services, “Calendar Year 2026 End-Stage Renal Disease Prospective Payment System Final Rule Fact Sheet,” CMS, cms.gov

Key Report Takeaways

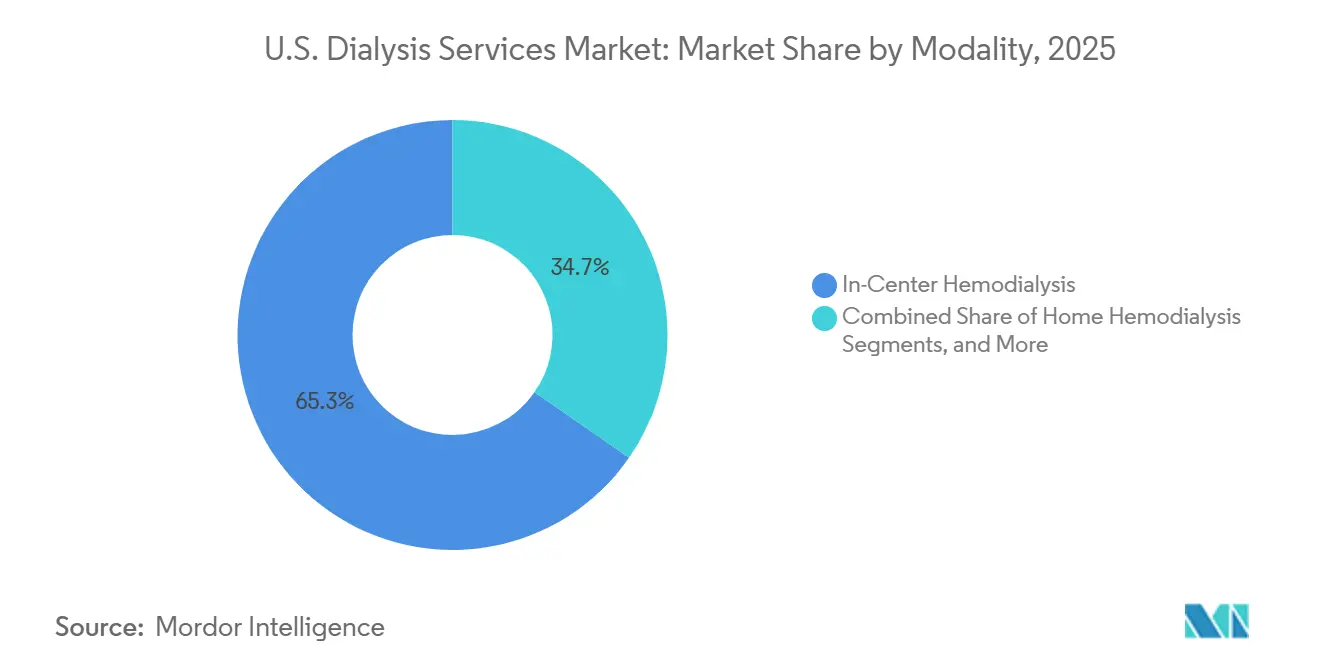

- By modality, in-center hemodialysis held 65.35% share in 2025, while home hemodialysis is forecasted to expand at a 7.12% CAGR through 2031.

- By site of care, freestanding outpatient dialysis centers commanded 69.67% share in 2025, while patient home dialysis is projected to grow at an 8.35% CAGR through 2031.

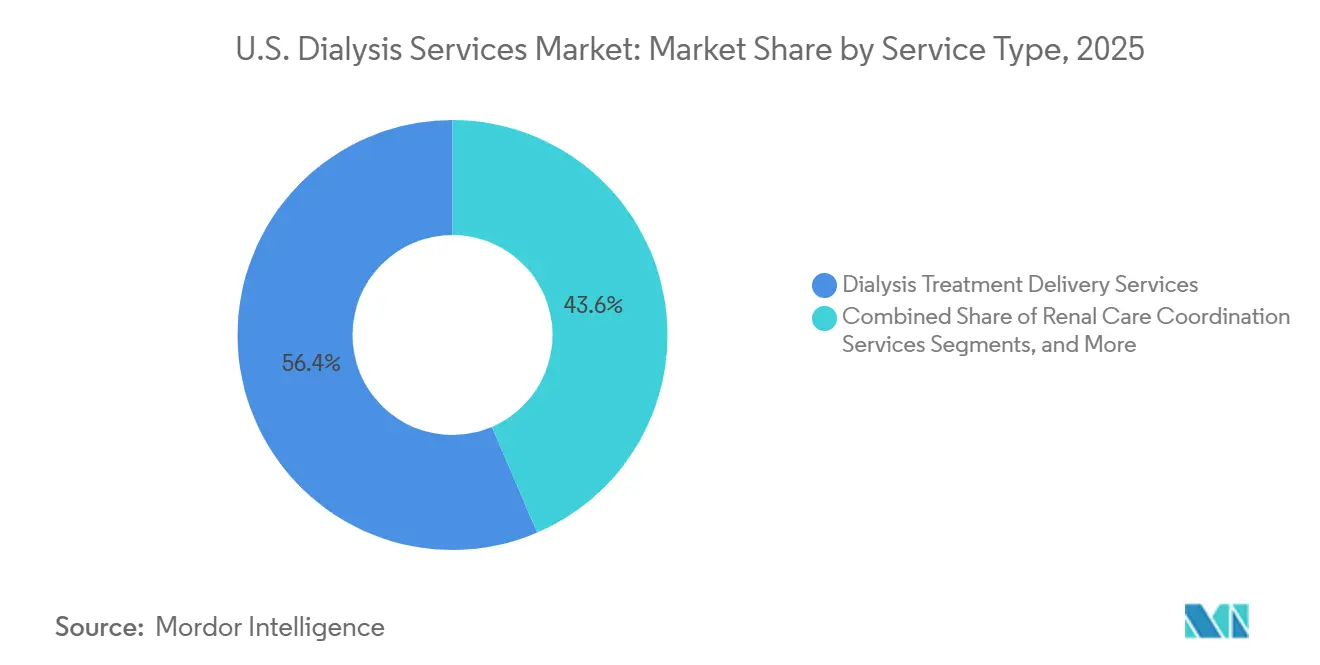

- By service type, dialysis treatment delivery services accounted for 56.45% share in 2025, while home dialysis training and support services are expected to grow at an 8.63% CAGR through 2031.

- By provider type, large dialysis organizations held 55.89% share in 2025, while hospital and health-system affiliated providers are projected to grow at a 6.90% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

U.S. Dialysis Services Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising ESKD treatment population | +2.5% | National, with disproportionate burden in Southern and Southeastern states including Texas, Louisiana, Arkansas, and Georgia | Long term (≥ 4 years) |

| aging and diabetes-linked renal burden | +1.5% | National, with higher density in Sun Belt states with older demographic profiles | Long term (≥ 4 years) |

| home dialysis adoption push | +1.0% | National, with faster uptake in states with stronger CMS ESRD Treatment Choices participation history | Medium term (2-4 years) |

| Medicare base-rate support for ESRD services | +0.8% | National | Short term (≤ 2 years) |

| Staff-assisted home dialysis expansion | +0.4% | National, with strongest relevance in rural Midwest and South markets facing access gaps | Medium term (2-4 years) |

| Medicare advantage ESRD enrollment scale-up | +0.3% | National, with concentrated growth in metro markets with strong Medicare Advantage competition | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising ESKD Treatment Population Drives Structural Demand

The United States dialysis services market is growing steadily due to the increasing need for long-term renal replacement therapy. Between 2002 and 2022, end-stage kidney disease (ESKD) cases rose by 31.3%, with prevalence increasing by 20,000 cases annually. Over 808,000 Americans live with ESKD, and 68% depend on dialysis, creating a stable demand. Medicare coverage ensures financial stability, while CMS projects USD 6 billion in payments to 7,600 ESRD facilities by 2026, driving investments in clinical infrastructure.[3]JAMA Network Open, “Expansion and Marketing of Medicare Advantage to Persons With End-Stage Kidney Disease,” JAMA Network Open, jamanetwork.com Providers focusing on long-term care management across diverse settings are better positioned for growth.

Aging Demographics and Diabetes Prevalence Compound Patient Volumes

Diabetes and hypertension remain key drivers of renal disease in the United States, with aging demographics further compounding the burden. Black Americans face over four times the risk of developing ESKD compared to White Americans, while Hispanic and Native American populations are more than twice as likely to be affected. These disparities shape demand in specific regions, requiring providers to align staffing, referrals, and support services with local needs. Operators addressing high-burden populations through tailored expansions and care coordination are better equipped to manage growing patient volumes and ensure quality outcomes.

Home Dialysis Adoption Push Reconfigures the Care Delivery Footprint

The United States dialysis services market is transitioning toward home-based treatment models, supported by evolving reimbursement policies. CMS has expanded Medicare coverage to include home dialysis for acute kidney injuries and broadened payment adjustments for home and self-dialysis training. Home dialysis requires robust training, patient readiness, and clinical support, making it a gradual but clear shift from center-based care. Providers investing in onboarding systems, training teams, and patient support infrastructure are well-positioned to adapt to changing treatment modalities and enhance patient retention.

Medicare Advantage ESRD Enrollment Transforms Payer Dynamics

Medicare Advantage has significantly impacted the United States dialysis market, with enrollment among dialysis patients rising from 24.8% in December 2020 to 47% by December 2022. This shift emphasizes the importance of network design, utilization reviews, and care authorizations in revenue management. Independent and regional operators must prioritize contract negotiations and referral strategies in competitive markets. The trend also accelerates integrated kidney care models, as payers seek improved hospitalization management and coordinated care pathways. DaVita's risk-based portfolio, managing over USD 5 billion in medical costs, highlights the growing focus on value-based kidney care.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Nurse and technician shortages | -0.8% | National, with acute pressure in rural Midwest and South markets and secondary pressure in urban markets from competing healthcare employers | Short term (≤ 2 years) and Medium term (2-4 years) |

| Medicare-heavy reimbursement pressure | -0.6% | National, with disproportionate impact on freestanding outpatient centers in lower wage-index markets | Medium term (2-4 years) |

| Oral drug bundle cost absorption risk | -0.3% | National, with greater exposure for smaller independent and nonprofit providers | Short term (≤ 2 years) |

| Certificate-of-need and referral lock-in barriers | -0.2% | State-specific, with heavier burden in selected Southern markets and limited impact in CON-exempt states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Nurse and Technician Shortages Constrain Treatment Capacity Expansion

In 2026, workforce shortages continue to constrain the United States dialysis services market, as dialysis delivery relies on skilled nurses, technicians, and support staff. Nearly 25% of full-time nephrology social workers plan to resign within the year, highlighting staffing challenges that extend beyond direct care roles. CMS Conditions for Coverage mandate specific staffing and care protocols for ESRD facilities, making staffing gaps a critical issue affecting scheduling, compliance, and patient access. Rural areas face the greatest impact due to limited recruitment pools and travel distances, while smaller operators struggle with fewer resources to reassign staff. Persistent shortages may hinder capacity growth, particularly in fragile local markets.

Medicare Reimbursement Structure Limits Margin Recovery

The ESRD PPS base rate increases to USD 281.71 per treatment in 2026 from USD 273.82 in 2025, but margin pressures persist due to Medicare's dominant payer mix. With 76% of dialysis patients on Medicare and 43% dually eligible for Medicare and Medicaid, providers face limited pricing flexibility. The termination of the ESRD Treatment Choices Model at the end of 2025 removes a key pathway supporting home dialysis and value-based care. Commercial insurance covers only a small portion of patients, leaving providers exposed to rising costs, staffing challenges, and care-quality demands that outpace reimbursement adjustments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Modality: In-Center Scale Remains Dominant While Home Modalities Gain Momentum

In 2025, In-Center Hemodialysis accounted for 65.35% of the United States dialysis services market, driven by established infrastructure, physician familiarity, and operational routines. Many patients begin and stabilize treatment in clinical settings before transitioning to home options. Fresenius Medical Care reported that nearly 90% of in-center dialysis machines in the United States are their devices, highlighting the role of equipment standardization. Peritoneal dialysis, while smaller in share, remains relevant as it enables treatment outside clinics while maintaining provider-patient relationships.

Home Hemodialysis is projected to grow at a 7.12% CAGR through 2031, making it the fastest-growing modality. CMS's expansion of home and self-dialysis training payments for acute kidney injury patients under the CY2025 ESRD PPS rule reduces cost barriers, encouraging providers to invest in home treatment systems. The market is shifting toward a balanced modality mix, emphasizing patient preparation and home support alongside treatment delivery. Fresenius plans to exit underperforming clinics in 2026 while advancing its 5008X CAREsystem rollout, reflecting network and technology optimization.

By Site of Care: Freestanding Centers Lead While Home-Based Care Gains Ground

Freestanding Outpatient Dialysis Centers held a 69.67% share in 2025, maintaining their lead in the United States dialysis services market due to operational efficiency and scale under the ESRD PPS framework. CMS's 2026 payment increase of 2.2% for freestanding centers, compared to 1.5% for hospital-based facilities, further strengthens their economic position. Hospital-Based Dialysis Centers remain essential for higher-acuity patients and inpatient starts requiring closer monitoring.

Patient Home Dialysis is forecasted to grow at an 8.35% CAGR through 2031, driven by improved reimbursement, training payments, and portability. The CY2025 ESRD PPS rule's expansion of acute kidney injury home dialysis coverage supports this growth. Skilled nursing and post-acute settings also play a role, particularly for older and complex patients transitioning through multiple care settings. Future site-of-care dynamics will depend on seamless coordination of home onboarding, transport, and follow-up care.

By Service Type: Treatment Delivery Holds the Revenue Base While Training Services Grow Fastest

In 2025, Dialysis Treatment Delivery Services represented 56.45% of the United States dialysis services market, reflecting the recurring nature of dialysis and predictable billing under standardized reimbursement. CMS's 2026 base rate of USD 281.71 per treatment reinforces the centrality of treatment delivery in provider economics. Acute and inpatient dialysis services cater to higher-acuity patients with distinct billing pathways.

Home Dialysis Training and Support Services are projected to grow at an 8.63% CAGR through 2031, indicating a shift toward education, monitoring, and support for scalable home care. Renal care coordination services are gaining importance as providers focus on cost management, hospitalization reduction, and patient tracking. DaVita reported managing over USD 5 billion in total medical costs under value-based care arrangements in 2026, highlighting the strategic value of integrated support services.

By Provider Type: Large Organizations Lead While Health-System Providers Expand Faster

Large Dialysis Organizations held a 55.89% share in 2025, leveraging scale advantages such as national purchasing, payer negotiations, and operational efficiency across extensive clinic networks. Decades of market presence have also fostered patient familiarity and referral patterns. However, local trust, nonprofit positioning, and regional integration remain critical for competitive success, as demonstrated by organizations like Northwest Kidney Centers and Satellite Healthcare.

Hospital and Health-System Affiliated Providers are forecasted to grow at a 6.90% CAGR through 2031, supported by direct hospital referrals, smoother transitions for inpatient dialysis starts, and continuity between acute and chronic care. Independent regional providers and nephrologist-led models remain relevant in markets where physician relationships influence patient direction. Future competition will focus on integrating dialysis delivery, home capabilities, and care coordination rather than solely expanding clinic networks.

Geography Analysis

In the United States dialysis services market, the South faces the highest disease burden, with an adjusted end-stage kidney disease incidence of 434 per million population. This is driven by higher rates of diabetes, hypertension, and racial disparities in states like Arkansas, Louisiana, Texas, and Oklahoma. Elevated patient density in these regions increases demand for freestanding centers and home dialysis training. Clinic closures, staffing shortages, or referral delays in rural Southern markets significantly impact access compared to lower-burden regions.

The Northeast experiences the lowest burden, with an end-stage kidney disease incidence of 284.6 per million population, nearly 35% lower than the South. This reflects better early detection of chronic kidney disease, timely nephrology referrals, and fewer comorbidities linked to kidney failure. The Midwest falls in between but faces challenges in rural areas due to limited staffing and weaker site economics, making it more susceptible to service disruptions from labor shortages or network adjustments.

The West and Southwest present a mixed scenario in the United States dialysis services market. Urban areas support multi-provider competition, advanced home dialysis capabilities, and better access to specialists, while rural and frontier regions face longer travel distances and limited service redundancy. Regional performance depends on disease burden, workforce availability, and home treatment feasibility, with opportunities strongest where providers adapt to local clinical needs instead of applying a uniform national approach.

Competitive Landscape

DaVita and Fresenius Medical Care dominate the United States dialysis services market, controlling 80% of facilities and generating 90% of industry revenue. This dominance provides both companies with significant purchasing power, payer leverage, and scale advantages. DaVita is strengthening its position through integrated kidney care, managing over USD 5 billion in medical costs under risk-based arrangements as of March 2026. This value-based care approach enhances its presence across the patient journey, aligning with payer models focused on outcomes and total costs.

In 2026, Fresenius is pursuing a strategy combining clinic optimization with technological advancements. Under its FME25+ transformation program, the company is exiting 64 of up to 100 selected United States dialysis clinics while rolling out the FDA-approved 5008X CAREsystem nationwide. This approach highlights the growing importance of clinical differentiation alongside geographic reach in the United States dialysis market.

Nonprofit, community-based, and hospital-affiliated providers continue to compete effectively in areas where local trust and care continuity are critical. Organizations like Northwest Kidney Centers, Satellite Healthcare, and Dialysis Clinic, Inc. focus on community integration and stable referral relationships rather than national scale. Hospital-affiliated providers are the fastest-growing segment, driven by post-acute integration and inpatient referral continuity. The United States dialysis services market is evolving, with scale dominating at the top and the next tier emphasizing home capabilities, care coordination, and selective network design.

U.S. Dialysis Services Industry Leaders

DaVita Inc.

Fresenius Medical Care AG

U.S. Renal Care

Satellite Healthcare

American Dialysis Centers

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Fresenius Medical Care exited 64 of up to 100 selected U.S. dialysis clinics under its FME25+ transformation program. The initiative aimed for EUR 250 million (USD 290.74 million) in savings and incurred EUR 350 million (USD 407.07 million) in one-time closure costs, targeting EUR 1.2 billion (USD 1.40 billion) in total program savings by 2027. The company also launched the 5008X CAREsystem for hemodiafiltration across U.S. clinics.

- March 2026: DaVita managed over USD 5 billion in medical costs under value-based care arrangements. CMS CKCC program data through 2024 showed consistent quality improvements, reinforcing DaVita's leadership in integrated kidney care in the United States.

- February 2026: DaVita invested USD 200 million in Elara Caring, a national home health provider. The partnership aimed to develop a kidney-specific home care model to reduce hospitalizations and lower care costs for dialysis-dependent patients.

- January 2026: CMS implemented the CY2026 ESRD PPS final rule, increasing the base treatment rate to USD 281.71 from USD 273.82 in 2025. The rule also updated the AKI dialysis payment rate, ended the ESRD Treatment Choices Model, and shortened the ICH CAHPS patient experience survey.

- November 2025: Fresenius Medical Care received FDA approval for the 5008X CAREsystem, a hemodiafiltration-capable dialysis machine. The approval, a key regulatory milestone, enabled early clinic deployments ahead of the 2026 rollout, with nearly 90% of U.S. in-center dialysis machines being Fresenius devices.

U.S. Dialysis Services Market Report Scope

As per the scope of the report, dialysis services are life-sustaining medical treatments that perform the essential functions of the kidneys when they fail. These services filter waste, remove excess fluids, and balance electrolytes in the blood to keep the body functioning.

The U.S. Dialysis Services Market is segmented by modality, site of care, service type, and provider type. By modality, the market includes in-center hemodialysis, home hemodialysis, and peritoneal dialysis. By site of care, the market is segmented into freestanding outpatient dialysis centers, hospital-based dialysis centers, skilled nursing facility dialysis, and patient home dialysis. By service type, the market is categorized into dialysis treatment delivery services, home dialysis training and support services, acute and inpatient dialysis services, post-acute and nursing home dialysis services, renal care coordination services, and others. By provider type, the market is segmented into large dialysis organizations, independent regional providers, nonprofit dialysis providers, hospital and health-system affiliated providers, and nephrologist-owned and joint-venture providers. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| In-Center Hemodialysis |

| Home Hemodialysis |

| Peritoneal Dialysis |

| Freestanding Outpatient Dialysis Centers |

| Hospital-Based Dialysis Centers |

| Skilled Nursing Facility Dialysis |

| Patient Home Dialysis |

| Dialysis Treatment Delivery Services |

| Home Dialysis Training and Support Services |

| Acute and Inpatient Dialysis Services |

| Post-Acute and Nursing Home Dialysis Services |

| Renal Care Coordination Services |

| Others |

| Large Dialysis Organizations |

| Independent Regional Providers |

| Nonprofit Dialysis Providers |

| Hospital and Health-System Affiliated Providers |

| Nephrologist-Owned and Joint-Venture Providers |

| By Modality | In-Center Hemodialysis |

| Home Hemodialysis | |

| Peritoneal Dialysis | |

| By Site of Care | Freestanding Outpatient Dialysis Centers |

| Hospital-Based Dialysis Centers | |

| Skilled Nursing Facility Dialysis | |

| Patient Home Dialysis | |

| By Service Type | Dialysis Treatment Delivery Services |

| Home Dialysis Training and Support Services | |

| Acute and Inpatient Dialysis Services | |

| Post-Acute and Nursing Home Dialysis Services | |

| Renal Care Coordination Services | |

| Others | |

| By Provider Type | Large Dialysis Organizations |

| Independent Regional Providers | |

| Nonprofit Dialysis Providers | |

| Hospital and Health-System Affiliated Providers | |

| Nephrologist-Owned and Joint-Venture Providers |

Key Questions Answered in the Report

What is the size of the U.S. dialysis services market in 2026?

The U.S. dialysis services market is valued at USD 32.66 billion in 2026 and is forecast to reach USD 44.85 billion by 2031 at a 6.55% CAGR.

What is driving growth in dialysis services in the United States?

Growth is supported by a rising end-stage kidney disease population, steady dialysis dependence, home dialysis policy support, and increasing value-based kidney care adoption.

Which dialysis modality leads revenue in the United States?

In-Center Hemodialysis leads the modality segment with a 65.35% share in 2025, showing that center-based treatment still anchors current demand.

Which site of care is growing the fastest for dialysis treatment?

Patient Home Dialysis is the fastest-growing site of care, projected to expand at an 8.35% CAGR through 2031 as reimbursement and training support improve.

Who are the leading companies in U.S. dialysis services?

The market is led by DaVita and Fresenius Medical Care, which together control 80% of facilities and 90% of industry revenue, making the competitive structure highly concentrated.

Why is home dialysis becoming more important in the United States?

Home dialysis is gaining relevance because CMS expanded payment support, providers are investing in training and support services, and payers are pushing for more coordinated and lower-cost care pathways.

Page last updated on: