Processed Beef Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

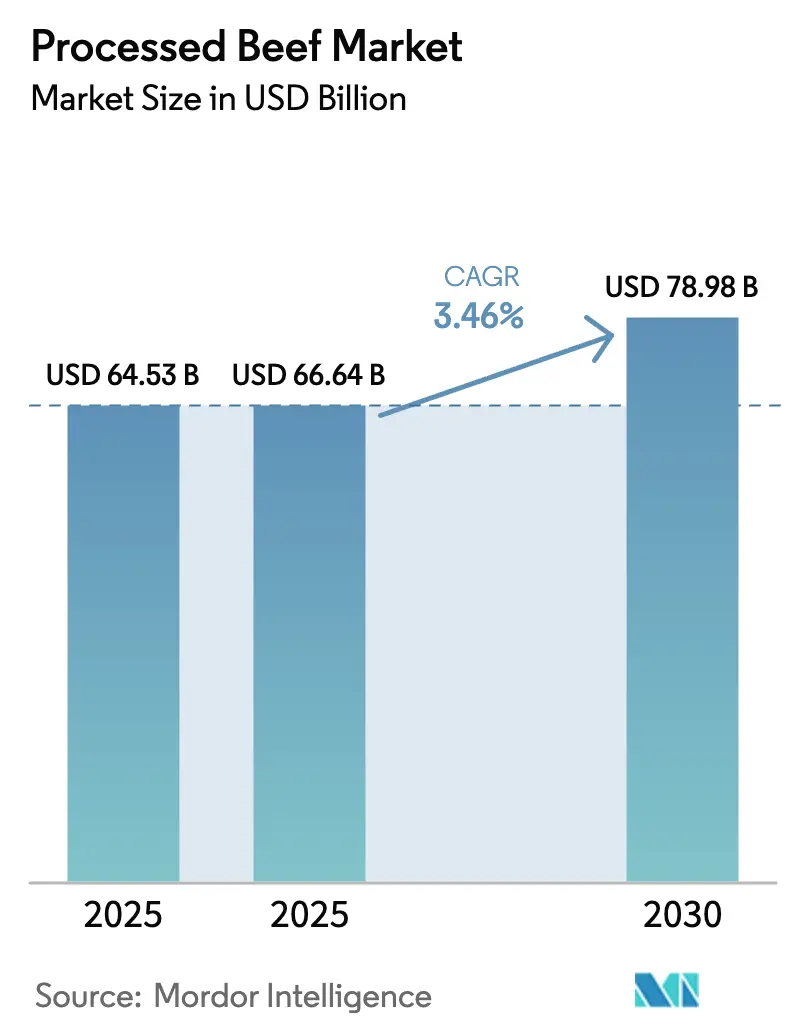

| Market Size (2025) | USD 66.64 Billion |

| Market Size (2030) | USD 78.98 Billion |

| Growth Rate (2026 - 2031) | 3.46% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Processed Beef Market Analysis by Mordor Intelligence

The processed beef market size was valued at USD 64.53 billion in 2025 and estimated to grow from USD 66.64 billion in 2026 to reach USD 78.98 billion by 2031, at a CAGR of 3.46% during the forecast period (2026-2031). Demand holds steady because consumers prize protein convenience, while processors innovate around blockchain traceability, clean-label recipes and high-pressure processing that lengthen chilled shelf life without preservatives. North America retains a 39.44% revenue lead thanks to entrenched c-store networks and the highest per-capita beef intake worldwide. Asia-Pacific shows the fastest regional momentum at 3.92% CAGR as rising middle-class incomes and halal export corridors open fresh outlets for shelf-stable beef snacks. Competitive intensity is moderate, yet the top five suppliers still channel capital toward automation and capacity realignment to offset tight cattle inventories and input-cost swings.

Key Report Takeaways

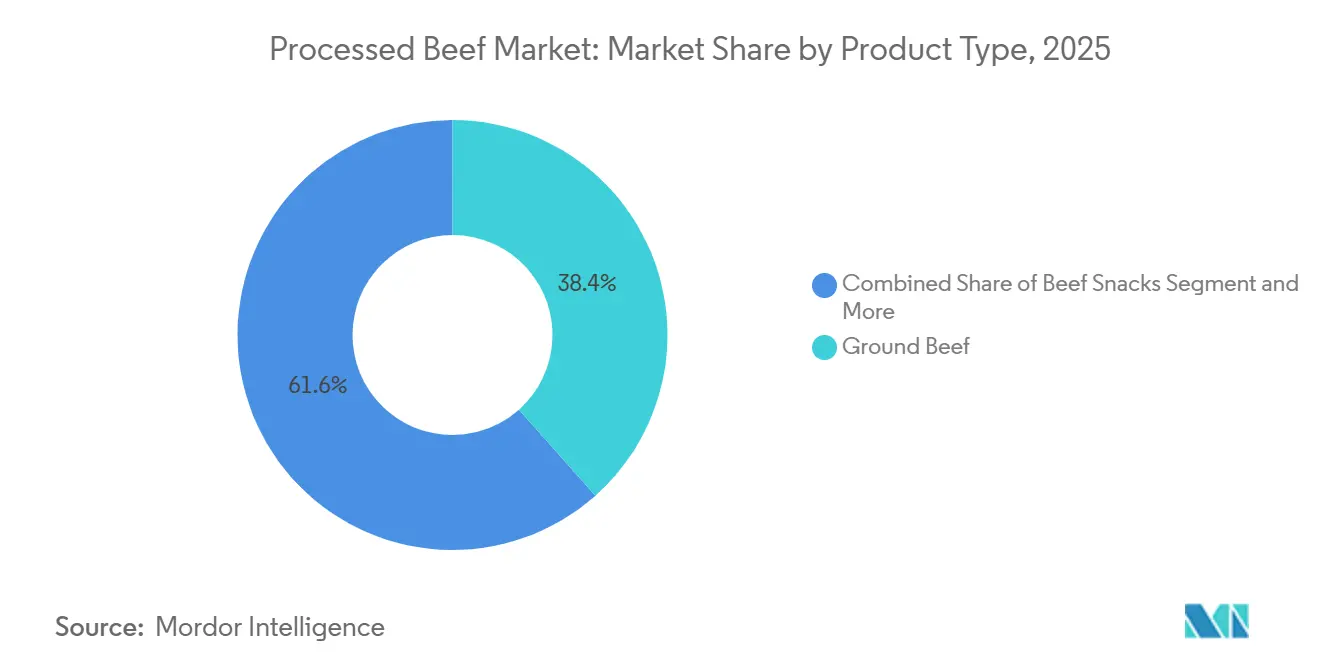

- By product type, ground beef led with 38.43% of the processed beef market share in 2025, while beef snacks are forecast to advance at a 4.62% CAGR through 2031.

- By processing method, fresh-chilled held 43.78% of the processed beef market size in 2025, yet ready-to-eat and ready-to-heat products are poised for 4.25% CAGR growth to 2031.

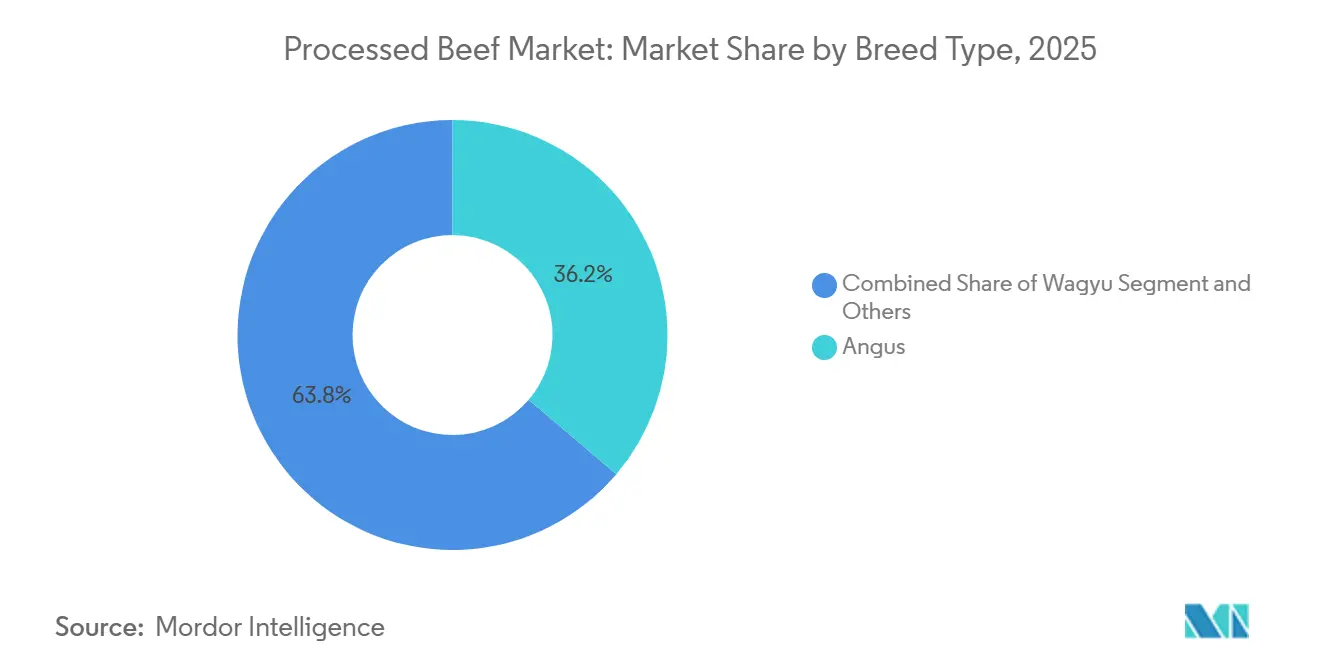

- By breed, Angus commanded 36.21% share of the processed beef market size in 2025, whereas Wagyu is projected to post the fastest 5.37% CAGR over 2026-2031.

- By distribution channel, off-trade captured 63.35% revenue in 2025; on-trade is expected to rebound with a 6.45% CAGR as business travel and tourism normalize.

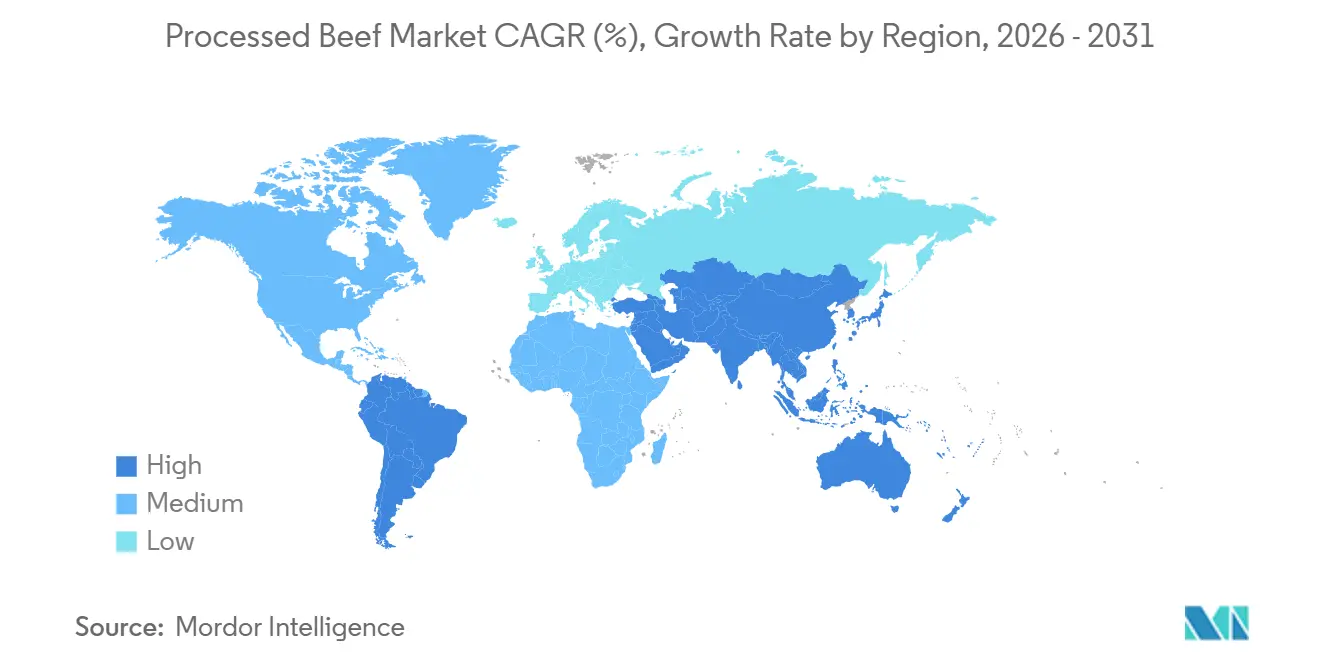

- By region, North America accounted for 39.44% of global revenues in 2025; Asia-Pacific is the fastest-growing region with a 3.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Processed Beef Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for shelf-stable beef snacks | +0.8% | North America, Asia-Pacific urban hubs, Middle East | Short term (≤ 2 years) |

| Blockchain traceability in premium lines | +0.6% | North America, EU, Middle East, Australia | Medium term (2-4 years) |

| High-pressure processing (HPP) adoption | +0.7% | EU, North America, Asia-Pacific export hubs | Medium term (2-4 years) |

| Halal-focused SKUs for export markets | +0.9% | UAE, Saudi Arabia, Indonesia, Malaysia, North Africa | Short term (≤ 2 years) |

| Premiumization via grass-fed, antibiotic-free | +0.5% | North America, Western Europe, Australia | Medium term (2-4 years) |

| Automation in slicing and packaging | +0.4% | Australia, North America, EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Shelf-Stable Beef Snacks in Convenience Channels

Jack Link's nationwide rollout of three-ingredient beef slices in March 2026, grass-fed beef, vinegar, and salt delivering 31 grams of protein per 2-ounce bag, captures the convergence of clean-label reformulation and convenience-channel expansion. The company's February 2026 launch of Carnivore Bites, a 65-piece bulk format priced at USD 19.99, targets value-conscious consumers trading down from protein bars and shakes, repositioning jerky from impulse snack to pantry staple. Brand collaborations amplify trial: Jack Link's Doritos Nacho Cheese beef jerky, launched February 2026 in partnership with PepsiCo, leverages Frito-Lay's distribution muscle to place protein snacks in 180,000+ convenience stores, while limited-time Squid Game-inspired Korean Ssamjang jerky (September 2024) drove 22% lift in millennial engagement via QR-code gamification. Natural preservation technologies, air-drying, vinegar-based marinades, and HPP, eliminate sodium nitrite while maintaining 12-18 month ambient shelf life, satisfying FDA's 2025 guidance capping nitrite at 120 ppm in ready-to-eat beef. Convenience-channel penetration is critical: U.S. c-store protein-snack sales grew 14% in 2025, outpacing total store growth of 3.2%, as grab-and-go formats align with commuter and on-the-go eating occasions, according to the NACS.

Integration of Blockchain Traceability in Premium Lines

BeefLedger's 2024 pilot with Meat and Livestock Australia demonstrated that blockchain-verified provenance commands 8-12% price premiums in export markets, with Middle Eastern buyers prioritizing halal certification, feedlot history, and antibiotic-free claims[1]Source: BeefLedger, “Blockchain Provenance Pilot with Meat & Livestock Australia,” BeefLedger, beefledger.io . MBRF Global Foods, formed via Marfrig's June 2025 merger with BRF, is deploying blockchain across Brazilian Angus exports to UAE and Saudi Arabia, recording ranch-to-port data on Hyperledger Fabric to satisfy importer due-diligence requirements under UAE Federal Decree-Law No. 2 of 2024 on food traceability. U.S. processors face parallel pressure: FSMA 204 traceability mandates effective November 2026 require lot-level tracking for chilled beef, and blockchain offers immutable audit trails that reduce compliance overhead by 30–40% versus manual record-keeping according to FDA. Consumer willingness-to-pay studies show that QR-code access to farm-level data increases purchase intent by 18% points among U.S. households earning >USD 75,000 annually, validating blockchain as a margin-accretive tool rather than a cost center. Australian processors, Kilcoy Global Foods and Australian Meat Group, are integrating blockchain with AI-driven scribing systems to link carcass-level yield data to downstream primal cuts, enabling real-time quality assurance and customer-specific specification adherence.

Adoption of High-Pressure Processing Extending Shelf Life Without Preservatives

HPP applies 400-600 MPa hydrostatic pressure to packaged beef for 3-6 minutes, achieving >5 log reduction in Listeria monocytogenes and E. coli O157:H7 without thermal degradation of myoglobin or texture, according to the Journal of Food Science[2]Source: Institute of Food Technologists, “High-Pressure Processing Effects on Beef Safety and Quality,” Journal of Food Science, ift.onlinelibrary.wiley.com. Peer-reviewed trials demonstrate that HPP-treated ground beef maintains microbial safety and color stability for 45-60 days under refrigeration versus 14-21 days for untreated product, enabling processors to serve distant markets without freezing or chemical preservatives. European Union Regulation 2019/1021 restricts sodium nitrite in cured beef to 150 mg/kg, and HPP offers a nitrite-free pathway to meet safety standards while preserving cured-beef flavor profiles, Spanish and Italian processors have adopted HPP for prosciutto-style beef and bresaola, achieving 30% shelf-life extension and 12% reduction in spoilage-related waste. North American premium retailers, Whole Foods, Sprouts, mandate HPP for fresh ground-beef SKUs to minimize recall risk, and processors report that HPP's USD 0.15-0.25 per pound cost is offset by reduced shrink and extended distribution radius. HPP equipment costs, USD 1.5-3.0 million per 350-liter vessel, favor large processors and co-packers, creating consolidation pressure as mid-tier players outsource HPP to toll manufacturers.

Expansion of Halal and Region-Specific SKUs for Export Markets

U.S. beef exports to Middle East markets reached USD 456 million in 2025, up 19% year-over-year, with halal-certified processed beef, ground beef, jerky, and ready-to-eat kofta, accounting for 34% of volume, according to the U.S. Meat Export Federation. Brazilian processors dominate halal trade: ABIEC (Associação Brasileira das Indústrias Exportadoras de Carnes) reports that Brazil exported 1.89 million tonnes of beef in 2025, with UAE, Saudi Arabia, and Egypt absorbing 28% of volume, and halal-certified processed beef (burgers, sausages, canned corned beef) grew 16% in 2025 as Middle Eastern retailers expand frozen-food aisles. UAE's 2024 tripling of Brazilian beef imports, from 47,000 tonnes in 2023 to 141,000 tonnes in 2024, reflects Dubai's emergence as a re-export hub for halal processed beef to East Africa and South Asia. China's 2026 beef import quotas allocate 15% of volume to halal-certified suppliers, creating openings for Indonesian and Malaysian processors to serve Muslim-majority provinces, though quota administration and safeguard tariffs constrain growth according to the China Customs. Certification fragmentation remains a barrier: UAE accepts 12 halal certifiers, Saudi Arabia recognizes 8, and Indonesia mandates LPPOM MUI certification, forcing exporters to maintain parallel audit trails and increasing per-unit compliance costs by USD 0.05-0.08.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in trim and lean beef prices | -0.7% | North America, Australia, Brazil | Short term (≤ 2 years) |

| Scrutiny on nitrites and nitrates | -0.4% | EU, North America, Australia | Medium term (2-4 years) |

| Cold-chain logistics cost pressure | -0.3% | North America, EU, Asia-Pacific import corridors | Medium term (2-4 years) |

| Retail move toward fresh over processed | -0.5% | North America urban, Western Europe, Australia metro | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Scrutiny on Nitrites and Nitrates in Cured Products

FDA's 2025 guidance capped sodium nitrite in ready-to-eat beef products at 120 ppm, down from the prior 200 ppm limit, forcing reformulation of jerky, deli meats, and cured sausages[3]Source: U.S. Food and Drug Administration, “FSMA 204 Traceability Rule and Sodium Nitrite Guidance,” FDA, fda.gov. European Union Regulation 2019/1021 restricts sodium nitrite to 150 mg/kg in cured beef, and France's 2024 national action plan targets a 25% reduction in nitrite use by 2027, pressuring processors to adopt celery powder (naturally occurring nitrate) or HPP as alternatives. Consumer advocacy groups, Center for Science in the Public Interest, Environmental Working Group, cite epidemiological studies linking nitrite consumption to colorectal cancer risk, and class-action lawsuits filed in California in 2024 allege that processors failed to disclose nitrosamine formation during cooking, according to Center for Science in the Public Interest. Reformulation costs are non-trivial: replacing sodium nitrite with celery powder increases ingredient costs by USD 0.12-0.18 per pound, and sensory trials show that celery-powder-cured beef scores 8-12% lower on flavor intensity and color stability versus sodium-nitrite controls, according to the Journal of Food Science. Jack Link's three-ingredient beef lineup, launched March 2026 with grass-fed beef, vinegar, and salt, demonstrates that clean-label positioning can command 15–20% price premiums, offsetting reformulation costs, but legacy brands face stranded-asset risk if they cannot pivot SKU portfolios quickly. Regulatory fragmentation complicates export strategies: Japan permits 200 ppm sodium nitrite, China allows 150 ppm, and UAE defers to Codex Alimentarius (156 ppm), forcing processors to maintain region-specific formulations and increasing SKU complexity by 30–40%.

Cold-Chain Dependency Elevates Logistics Cost for Chilled Beef

FSMA 204 traceability mandates effective November 2026 require temperature-monitored shipment records for chilled beef, adding USD 0.08-0.12 per pound in compliance overhead as processors deploy IoT sensors, cloud-based logging, and third-party audits. Refrigerated trucking rates in North America averaged USD 2.85 per mile in Q1 2026, up 11% year-over-year, driven by diesel-price volatility and driver shortages, American Trucking Associations reports a 78,000-driver deficit, with refrigerated segments experiencing 15% higher turnover than dry-van. Cold-chain infrastructure gaps constrain growth in emerging markets: India's cold-storage capacity totals 37 million tonnes, but only 4% is dedicated to meat, and power outages disrupt temperature control in 18-22% of shipments, forcing processors to over-rely on frozen formats that sacrifice margin, according to the National Centre for Cold Chain Development (NCCD). China's cold-chain logistics costs, USD 0.22-0.28 per pound for chilled beef versus USD 0.12-0.15 for frozen, incentivize importers to favor frozen over chilled, limiting premium-product penetration, according to China Cold Chain Logistics. Processors are investing in insulated packaging and phase-change materials to extend ambient hold-time: Cryopak's PCM-28 maintains 2–4°C for 72 hours without refrigeration, enabling direct-to-consumer shipments, but packaging costs rise by USD 0.35–0.50 per unit. Regulatory harmonization remains elusive: EU mandates continuous temperature monitoring for chilled beef, while U.S. FSIS accepts time-temperature indicators, and Australia requires real-time GPS tracking, forcing exporters to over-engineer cold-chain systems to satisfy the strictest jurisdiction, according to Food Safety and Inspection Service (FSIS).

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Ground Beef Anchors Volume, Snacks Capture Premiumization

Ground beef commands 38.43% market share in 2025, anchored by foodservice demand, quick-service restaurants and institutional buyers consume 62% of U.S. ground-beef production, and retail private-label penetration, which reached 47% share in 2025 as grocers deploy cost-plus pricing to compete with branded SKUs. Beef snacks are the fastest-growing segment at 4.62% CAGR during 2026-2031, driven by clean-label reformulation and brand collaborations: Jack Link's three-ingredient lineup (March 2026) and Doritos Nacho Cheese jerky (February 2026) exemplify how flavor innovation and simplified ingredient decks unlock convenience-channel growth. Cooked and smoked beef deli meats, pastrami, corned beef, faces headwinds from nitrite scrutiny, with EU Regulation 2019/1021 capping sodium nitrite at 150 mg/kg and forcing processors to adopt celery powder or HPP, increasing costs by USD 0.12–0.18 per pound. Frozen beef specialties, meatballs, patties, and value-added entrées, serve institutional and export markets, with Brazil exporting 1.89 million tonnes of beef in 2025, 34% of which was frozen processed beef destined for Middle East and North African halal markets, according to ABIEC. Cured and shelf-stable beef, jerky, biltong, canned corned beef, benefits from ambient distribution economics, eliminating cold-chain costs of USD 0.22-0.28 per pound and enabling penetration of rural and emerging markets where refrigeration infrastructure is sparse, according to the China Cold Chain Logistics.

Historical CAGR for ground beef between 2019 and 2025 averaged 2.1%, reflecting mature-market saturation and private-label commoditization, while beef snacks grew at 6.8% during the same period, underscoring the category's shift toward premium, protein-forward positioning, according to Power of Meat 2026 The Food Industry Association. Ready-to-eat beef products, meal kits, microwaveable entrées, are gaining traction as retailers deploy chef-inspired, single-serve formats: H-E-B's Meal Simple Parmesan Stuffed Beef Flank Steak and Fresco Foods' Homestyle Braised Beef (fresh, never frozen, no preservatives) compete directly with quick-service restaurants by offering restaurant-quality meals with <20-minute prep times. Canned and aseptic beef, corned beef, beef stew, remain staples in military and emergency-preparedness channels, with U.S. Defense Logistics Agency purchasing 47 million pounds of canned beef in FY2025, but consumer demand is flat as younger cohorts favor fresh and frozen formats.

By Processing Method: Fresh-Chilled Dominates, Ready-to-Eat Gains Share

Fresh-chilled processing holds 43.78% market share in 2025, serving retail meat cases and foodservice operators who prioritize color stability and perceived freshness, yet cold-chain dependency adds USD 0.08-0.12 per pound in FSMA 204 compliance costs and USD 0.22-0.28 per pound in refrigerated logistics. Ready-to-eat and ready-to-heat formats are the fastest-growing segment at 4.25% CAGR during 2026-2031, as retailers deploy microwaveable, single-serve meal kits that compete with quick-service restaurants: Kraft Heinz's Velveeta Beef Stroganoff One Pan Dinner Kit and J.T.M.'s Beef Philly Cheese Steak Kit (36 oz, makes 4 sandwiches) exemplify convenience-driven innovation. Frozen processing accounts for 28% share in 2025, dominated by export-oriented players, Brazil's 1.89 million tonnes of beef exports in 2025 included 642,000 tonnes of frozen processed beef (burgers, sausages, meatballs) destined for Middle East halal markets. Canned and aseptic processing serves niche applications, military procurement, emergency rations, shelf-stable retail, but faces volume declines as consumers trade up to frozen and fresh formats; U.S. canned-beef consumption fell 3.2% in 2025, according to the USDA.

HPP is reshaping fresh-chilled economics: processors report that 600 MPa pressure for 3 minutes extends shelf life by 30–50% without nitrites, enabling distribution to markets 1,000+ miles from production facilities and reducing spoilage-related waste by 12%, according to the Journal of Food Science. Ready-to-eat formats benefit from automation: AI-driven portioning systems at JBS's Cactus, Texas plant (USD 150 million expansion, completion early 2027) deliver ±2-gram accuracy for single-serve meal-kit components, reducing labor costs by 30% and improving yield consistency. Frozen processing faces margin pressure from energy costs, blast-freezing consumes 0.18–0.22 kWh per pound, and U.S. industrial electricity rates rose 9% in 2025, but frozen formats remain essential for export markets where cold-chain infrastructure is unreliable. Canned beef's decline reflects generational shifts: Power of Meat 2026 reports that households under age 45 purchased 42% less canned beef in 2025 versus 2020, favoring frozen and fresh formats that align with meal-prep and batch-cooking trends.

By Breed Type: Angus Anchors Premium Retail, Wagyu Captures Foodservice Upside

Angus beef commands 36.21% market share in 2025, anchored by USDA Certified Angus Beef® brand recognition and retailer private-label programs, Costco's Kirkland Signature Angus ground beef and Walmart's Angus Choice line leverage breed-specific labeling to justify 12–18% price premiums over commodity beef, as per the USDA. Wagyu is the fastest-growing segment at 5.37% CAGR during 2026-2031, driven by Japan's export liberalization and Australian Wagyu producers targeting U.S. and Chinese foodservice channels with marbling scores (BMS 6–9) that command 3–5× price premiums over commodity beef. Brazilian certified Angus exports soared 34% in 2025, reaching 127,000 tonnes, as Middle Eastern and U.S. buyers prioritize breed-verified provenance and blockchain traceability according to the ABIEC. Hereford and Charolais breeds serve niche grass-fed and organic segments, with Hereford accounting for 8% of U.S. grass-fed beef production in 2025, but limited brand recognition constrains retail penetration, according to the USDA. Other breeds, including crossbreds and dairy-beef hybrids, supply commodity ground-beef and processed-beef markets, where breed-specific claims offer minimal price uplift.

Wagyu's 5.37% forecast CAGR reflects supply-side expansion: Australian Wagyu herd inventories grew 11% in 2025, and U.S. full-blood Wagyu registrations increased 18%, enabling processors to scale production beyond ultra-premium steakhouse channels into retail ground-beef and burger formats according to the Australian Wagyu Association. Snake River Farms' American Wagyu ground beef, retailing at USD 12.99 per pound versus USD 5.49 for conventional ground beef, demonstrates that marbling-driven flavor intensity can command 137% premiums even in commodity-adjacent categories. Grass-fed and antibiotic-free claims are increasingly breed-agnostic: Jack Link's March 2026 launch of three-ingredient grass-fed beef slices (31 grams protein, USD 6.99 per 2-ounce bag) positions grass-fed as a processing attribute rather than a breed marker, enabling processors to source from diverse breed pools while maintaining clean-label positioning.

By Distribution Channel: Off-Trade Dominates, On-Trade Recovers Post-Pandemic

Off-trade channels, supermarkets, hypermarkets, specialty stores, and online retailers, command 63.35% market share in 2025, driven by private-label penetration (47% of ground-beef volume) and retailer investments in prepared-meal programs: H-E-B's Meal Simple, Whole Foods' 365 Everyday Value, and Kroger's Home Chef meal kits position retailers as direct competitors to foodservice. On-trade channels, restaurants, hotels, catering, are the fastest-growing segment at 6.45% CAGR during 2026-2031, reflecting post-pandemic recovery in tourism and business travel: Japan's 2025 tourist arrivals reached 36.9 million, up 16% year-over-year, driving high-end dining demand and supporting 680,000 tonnes of beef imports in 2026. Supermarkets and hypermarkets account for 41% of off-trade volume in 2025, leveraging scale to negotiate direct-from-processor contracts and deploy cost-plus pricing that undercuts branded SKUs by 15-20%. Online retailers, Amazon Fresh, Instacart, Thrive Market, grew 19% in 2025, capturing 8% of off-trade volume, as direct-to-consumer beef subscriptions (ButcherBox, Crowd Cow) deploy blockchain traceability and grass-fed claims to justify 25-35% premiums over supermarket equivalents.

Specialty stores, butcher shops, natural-foods retailers, serve premium and niche segments, with grass-fed, organic, and halal-certified beef accounting for 62% of specialty-store volume in 2025, but high operating costs (rent, labor) limit geographic expansion. On-trade recovery is uneven: quick-service restaurants (QSRs) consumed 62% of U.S. ground-beef production in 2025, up 4% year-over-year, as McDonald's, Wendy's, and Burger King expanded value menus to compete with inflation-sensitive consumers, while fine-dining beef consumption grew 11% as affluent households increased discretionary spending. Foodservice operators are adopting portion-control automation: JBS's Cactus, Texas expansion includes AI-driven portioning systems that deliver ±2-gram accuracy for QSR patties, reducing labor costs by 30% and improving yield consistency. Online penetration faces cold-chain constraints: direct-to-consumer shipments require insulated packaging and phase-change materials (USD 0.35–0.50 per unit), and last-mile refrigerated delivery adds USD 8–12 per order, limiting profitability to high-ticket subscriptions.

Geography Analysis

North America holds 39.44% market share in 2025, anchored by the United States' 27.5 billion pounds of beef production and entrenched convenience-retail infrastructure, that enable shelf-stable beef snacks and ready-to-eat meal kits to reach the population. JBS's USD 150 million Cactus, Texas expansion (groundbreaking February 2026, completion early 2027) signals confidence in long-term domestic demand despite Tyson's retrenchment, Tyson closed its Lexington, Nebraska plant and reduced Amarillo operations to a single shift, citing tight cattle supplies and margin pressures. Canada's processed-beef market is consolidating: Maple Leaf Foods spun off pork operations into Canada Packers in October 2025 and is expanding its U.S. protein footprint in 2026, targeting mid-single-digit revenue growth via brand-led differentiation and operational efficiency. Mexico's beef processing is export-oriented, with 34% of production destined for U.S. foodservice and retail, and USMCA rules-of-origin requirements incentivize Mexican processors to source U.S. feeder cattle to qualify for duty-free access as per the USDA. FSMA 204 traceability mandates effective November 2026 add USD 0.08-0.12 per pound in compliance costs, pressuring small and mid-tier North American processors to consolidate or exit.

Asia-Pacific is the fastest-growing region at 3.92% CAGR during 2026-2031, driven by rising middle-class incomes, urbanization-led demand for convenience formats, and halal-certified export corridors. China's 2026 beef import quotas allocate 850,000 tonnes to Australia, Brazil, and Argentina, yet safeguard tariffs (12% on volumes exceeding quota) and supplier-specific allocations constrain growth, Brazil's allocation fell 8% in 2026 due to prior-year quota overruns. India's processed-beef market is constrained by cultural and regulatory barriers, most states ban cattle slaughter, but buffalo-meat processing thrives, with India exporting frozen buffalo meat primarily to Middle East and Southeast Asian halal markets. Australia's exports beef majorly for China, Japan, and the U.S. absorbing major share of volume, and Australian processors are deploying AI-driven scribing systems, Kilcoy Global Foods' IR-SCRIBE achieves >90% cutting accuracy within millimeters, delivering AUD 4.92-5.19 gross benefit per head and 1.15-1.21 year ROI. Indonesia and Thailand are emerging processed-beef importers, with halal-certified frozen burgers and sausages growing as quick-service restaurant chains expand in Jakarta and Bangkok.

Europe is a major consumer for processed-beef with Germany, UK, France, Italy, and Spain representing highest regional volumes, however per-capita consumption is decliningdue to sustainability concerns and plant-based alternatives eroded demand, as stated by the EU Commission. EU Regulation 2019/1021 restricts sodium nitrite in cured beef to 150 mg/kg, and France's 2024 national action plan targets a 25% reduction in nitrite use by 2027, forcing processors to adopt celery powder or HPP, reformulation costs of USD 0.12-0.18 per pound compress margins for legacy deli-meat and sausage lines. South America is dominated by Brazil and Argentina, which together exported 2.4 million tonnes of beef in 2025, including processed into frozen burgers, sausages, and canned corned beef for Middle East, North Africa, and Asian halal markets according to ABIEC. Marfrig's September 2025 merger with BRF created MBRF Global Foods, a BRL 152 billion revenue entity operating in 117 countries with projected annual synergies of BRL 805 million, and the combined entity is deploying blockchain across Brazilian Angus exports to Middle East markets. Chile, Peru, and Colombia are emerging processors, with Chile exporting processed beef primarily frozen burgers and sausages to Asian markets, and Peru's halal-certified beef exports to Middle Eastern buyers. Middle East and Africa imports processed-beef with UAE, Saudi Arabia, South Africa, Nigeria, and Egypt as top markets, and halal certification is mandatory for majority of regional volume.

Competitive Landscape

The processed beef market exhibits fragmented market with the top five players JBS S.A., Tyson Foods, Marfrig Global Foods, Cargill, and Kraft Heinz collectively holding smaller global share, yet regional fragmentation persists as mid-tier processors serve localized halal, organic, and grass-fed niches. Strategic divergence defines 2025–2026: JBS committed USD 785 million across proteins, including USD 150 million to expand its Cactus, Texas fabrication floor and ground-beef capacity by early 2027, while Tyson shuttered its Lexington, Nebraska plant and reduced Amarillo operations, signaling contrasting views on U.S. cattle-supply recovery. Marfrig's September 2025 merger with BRF created MBRF Global Foods, a BRL 152 billion revenue entity projecting BRL 805 million in annual synergies via unified logistics, single operating systems, and tax optimization, positioning the combined entity to dominate South American exports and Middle Eastern halal corridors.

White-space opportunities cluster around clean-label reformulation and automation: Jack Link's three-ingredient beef lineup (March 2026) and Doritos Nacho Cheese jerky (February 2026) demonstrate that brand collaborations and simplified ingredient decks unlock convenience-channel growth, while Kilcoy Global Foods' AI-driven scribing system (>90% cutting accuracy, 1.15–1.21 year ROI) proves that robotics can deliver measurable yield improvements in labor-constrained markets. Emerging disruptors include direct-to-consumer subscription services, ButcherBox, Crowd Cow, that deploy blockchain traceability and grass-fed claims to justify 25–35% premiums over supermarket equivalents, bypassing traditional retail and capturing affluent, digitally native cohorts. Technology adoption is reshaping competitive dynamics: JBS's Cactus expansion integrates AI-driven portioning systems that deliver ±2-gram accuracy for single-serve meal-kit components, reducing labor costs by 30% and improving yield consistency, while Australian processors, Kilcoy Global Foods, Australian Meat Group, are deploying IR-SCRIBE robotic scribing across two plants, validating that 3D vision + machine learning can replace skilled manual labor in safety-critical cutting operations.

HPP adoption remains concentrated among large processors and co-packers due to USD 1.5–3.0 million per 350-liter vessel capital costs, creating consolidation pressure as mid-tier players outsource HPP to toll manufacturers or exit premium segments. Blockchain traceability is transitioning from pilot to production: MBRF Global Foods is deploying Hyperledger Fabric across Brazilian Angus exports to UAE and Saudi Arabia, recording ranch-to-port data to satisfy importer due-diligence requirements, and BeefLedger's 2024 pilot with Meat & Livestock Australia demonstrated 8–12% price premiums for blockchain-verified provenance. Regulatory compliance, FSMA 204 traceability mandates, EU nitrite restrictions, halal certification fragmentation, favors integrated players with treasury depth and regulatory-affairs teams, widening the cost gap between large processors (USD 0.08-0.12 per pound compliance overhead) and small operators (USD 0.18-0.25 per pound).

Processed Beef Industry Leaders

JBS S.A.

Tyson Foods Inc.

Marfrig Global Foods

Cargill, Incorporated

The Kraft Heinz Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: JBS USA broke ground on a USD 150 million expansion at its Cactus, Texas beef processing facility, constructing a new state-of-the-art fabrication floor and expanded ground-beef room to increase operational efficiency and production capacity; the project is expected to be completed by early 2027.

- February 2026: Jack Link's partnered with PepsiCo to launch Doritos Nacho Cheese-flavored beef jerky and meat sticks, available online and at retailers nationwide, leveraging Frito-Lay's distribution network to place protein-forward snacks in 180,000+ convenience stores and capitalizing on consumer demand for bold flavors and convenient, high-protein formats.

- September 2025: Marfrig's merger with BRF received unconditional approval from Brazil's antitrust authority (CADE), creating MBRF Global Foods with annual revenues of BRL 152 billion, operations in 117 countries, and projected annual synergies of BRL 805 million via unified commercial and logistics systems, streamlined corporate framework, and tax optimization.

- June 2025: Tyson Foods launched Wright Brand Premium Sausage Links featuring beef-based varieties with 12-13 grams protein per serving, targeting growing consumer demand for premium, protein-rich beef products with nationwide rollout .

Global Processed Beef Market Report Scope

Processed beef refers to beef that has been modified through methods such as grinding, curing, smoking, cooking, or preservation to enhance flavor, shelf life, and convenience. The processed beef market is segmented by product type, processing method, breed type, distribution channel, and geography. By product type, the market includes ground beef, cooked/smoked beef, cured and shelf-stable products, frozen beef specialties, and beef snacks. Based on processing method, the market is categorized into fresh-chilled, frozen, canned/aseptic, and ready-to-eat/ready-to-heat products. By breed type, the market covers Angus, Wagyu, Hereford, Charolais, and other breeds. Based on distribution channel, the market is segmented into on-trade and off-trade. By geography, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (USD million) and volume(Tons).

| Ground Beef |

| Cooked/Smoked Beef |

| Cured and Shelf-stable |

| Frozen Beef Specialties |

| Beef Snacks |

| Fresh-chilled |

| Frozen |

| Canned/Aseptic |

| Ready-to-Eat/Ready-to-Heat |

| Angus |

| Wagyu |

| Hereford |

| Chalorais |

| Others |

| On-trade | |

| Off-trade | Supermarkets/Hypermarkets |

| Specialty Stores | |

| Online Retailers | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| Thailand | |

| Singapore | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Ground Beef | |

| Cooked/Smoked Beef | ||

| Cured and Shelf-stable | ||

| Frozen Beef Specialties | ||

| Beef Snacks | ||

| By Processing Method | Fresh-chilled | |

| Frozen | ||

| Canned/Aseptic | ||

| Ready-to-Eat/Ready-to-Heat | ||

| By Breed Type | Angus | |

| Wagyu | ||

| Hereford | ||

| Chalorais | ||

| Others | ||

| By Distribution Channel | On-trade | |

| Off-trade | Supermarkets/Hypermarkets | |

| Specialty Stores | ||

| Online Retailers | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the processed beef market in 2026?

It is valued at USD 66.64 billion and is on track to reach USD 78.98 billion by 2031 at a 3.46% CAGR.

Which product category is growing fastest?

Beef snacks, including jerky and biltong, are projected to expand at a 4.62% CAGR through 2031 thanks to clean-label recipes and convenience-store demand.

What role does HPP play in processed beef safety?

High-pressure processing achieves >5 log pathogen reduction while extending chilled shelf life by up to 50%, allowing nitrite reduction and wider distribution.

Why are halal-certified SKUs important?

Halal products already make up one-third of U.S. beef exports to the Middle East and benefit from export corridors into Southeast Asia and North Africa.

How are blockchain platforms used in beef supply chains?

Processors record ranch-to-port data on systems like Hyperledger Fabric, enabling QR-code verification that lifts willingness to pay by up to 12%.

Page last updated on: