U.S. Packaged Food Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.62 Trillion |

| Market Size (2026) | USD 1.75 Trillion |

| Market Size (2031) | USD 2.60 Trillion |

| Growth Rate (2026 - 2031) | 8.28% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

U.S. Packaged Food Market Analysis by Mordor Intelligence

By 2031, the U.S. packaged food market, valued at USD 1.62 trillion in 2025 and USD 1.75 trillion in 2026, is set to reach USD 2.60 trillion, marking a CAGR of 8.3% from 2026 to 2031. After a volume squeeze due to inflation in 2024, the market is regaining momentum. While higher food prices bolstered dollar sales, they simultaneously pressured unit demand. Time constraints remain pivotal in the packaged food sector. Even as more households dine at home, there's a pronounced preference for products that minimize preparation time. Digital platforms increasingly influence purchasing decisions. With the surge in online grocery shopping, the significance of search visibility and digital content in the packaged food arena has amplified. Health considerations are evolving. Beyond traditional low-fat or low-sugar claims, there's a notable shift towards reformulation, enrichment with protein and fiber, and a focus on cleaner ingredients. Concurrently, enhanced private-label strategies and heightened scrutiny of ingredients at the state level are compressing margins for branded products. This scenario underscores the growing importance of portfolio discipline, swift reformulation, and packaging tailored to specific channels in the competitive landscape of the packaged food market.

Key Report Takeaways

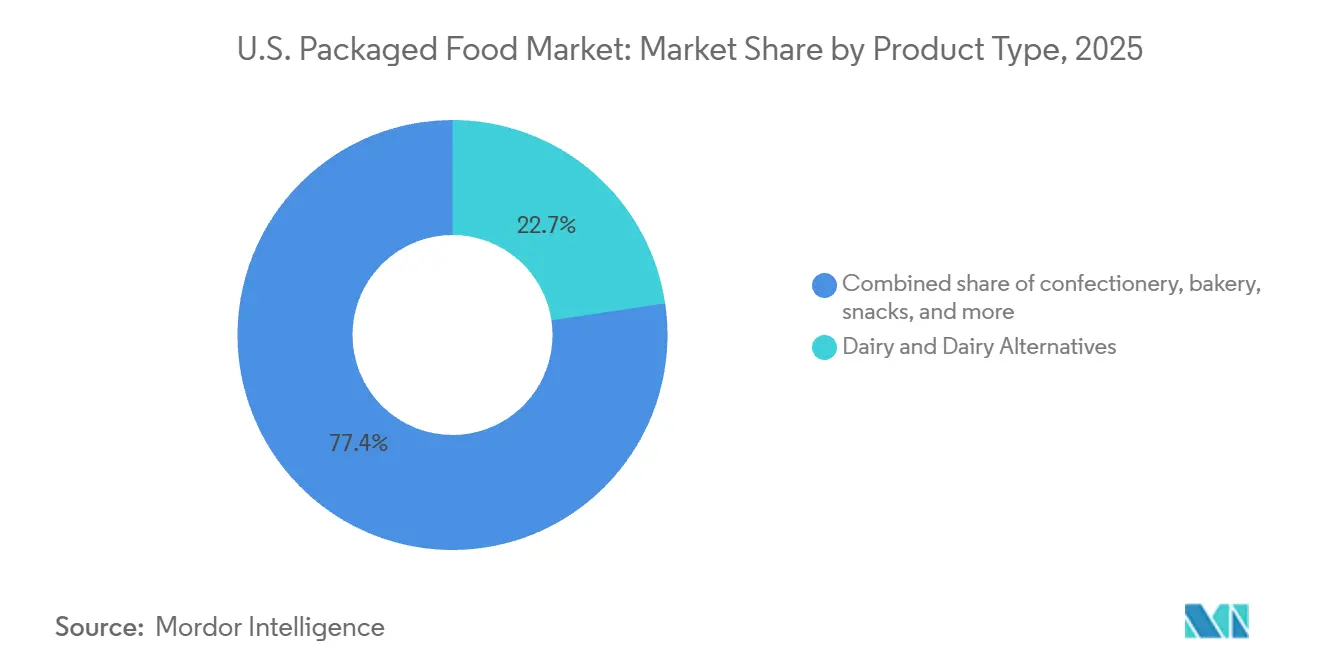

- By product type, Dairy and Dairy Alternatives led with 22.7% share in 2025, while Ready Meals is projected to grow at 8.5% through 2031.

- By category, Conventional products held 76.9% share in 2025, while Natural, Organic, and Free-From are forecast to expand at 9.0% through 2031.

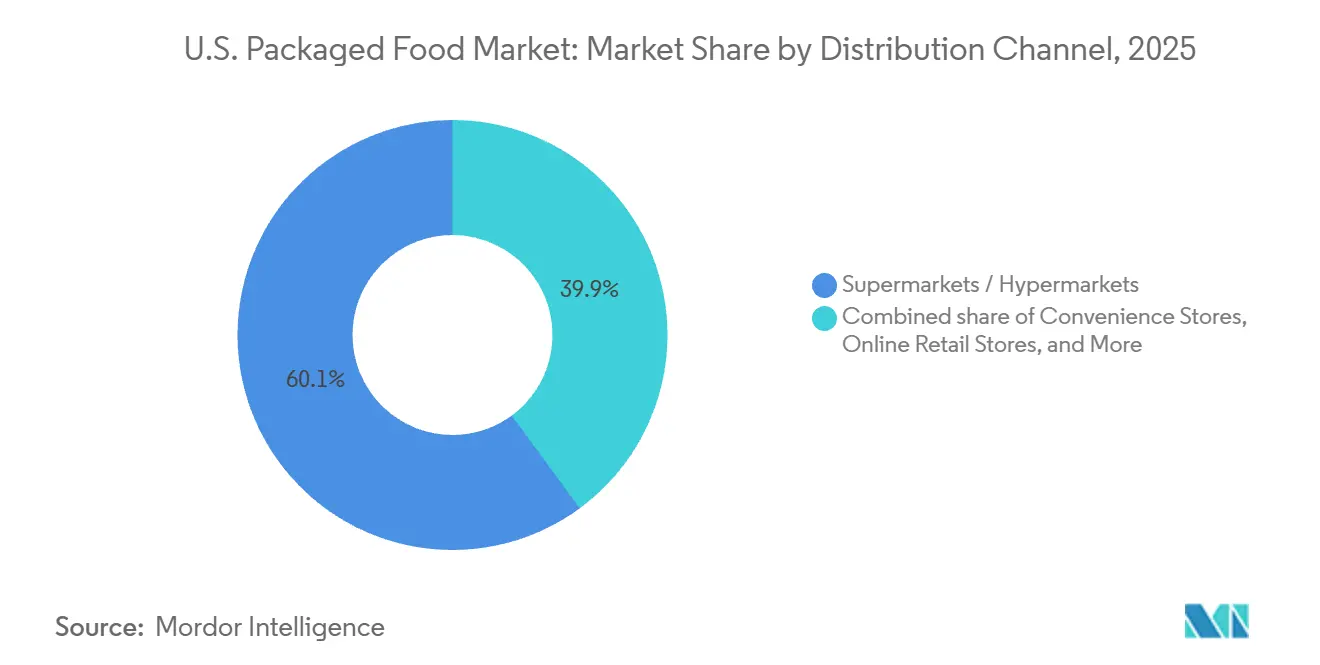

- By distribution channel, Supermarkets and Hypermarkets accounted for 60.1% share in 2025, while Online Retail Stores are projected to grow at 8.9% through 2031.

- By geography, the South held 38.0% share in 2025, while the Northeast is expected to grow at 8.4% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

U.S. Packaged Food Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Busy lifestyles and time scarcity | +2.1% | Global, with concentrated gains in Northeast and West urban metros | Short term (≤ 2 years) |

| Sustainability and eco-friendly packaging | +0.8% | National, with early gains in West Coast and Northeast metros | Medium term (2–4 years) |

| Digital marketing and social media influence | +1.2% | National; strongest among Gen Z and Millennial demographics | Short term (≤ 2 years) |

| Plant-based and flexitarian diets | +0.9% | National, with premium channel over-indexing in West and Northeast | Medium term (2–4 years) |

| Health and wellness consciousness | +1.3% | National, with above-average penetration in Midwest and Northeast | Short term (≤ 2 years) |

| Private-label and retailer-brand expansion | +1.5% | National, with strongest gains in South and Midwest value channels | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Busy Lifestyles and Time Scarcity Are Redefining Convenience

In the U.S., time scarcity has shifted from being a fleeting concern to a fundamental driver of food purchasing habits. According to Purdue University's March 2026 Consumer Food Insights Report, 58% of Americans prioritize convenience and time savings when opting for processed packaged foods. This trend notably boosts the popularity of ready meals, single-serve snacks, and portable dairy products[1]Source: Purdue University, “Many Consumers View Processed Foods as Unhealthy but Convenient”, purdue.edu. As employees return to the office, weekday mornings have become crunch time for meal prep. This has led to a surge in demand for high-protein breakfast cereals and grab-and-go bakery items, positioning them as rapidly growing segments in the packaged food landscape. Furthermore, the distinction between ambient and chilled packaged foods is becoming less clear. Retailers and manufacturers are now jointly investing in refrigerated bays for ready meals, a territory once deemed unconventional for packaged foods. General Mills highlighted this industry shift at the CAGNY conference in early 2026, forecasting a 25% boost in net sales for FY2026, driven by new product launches emphasizing bold flavors and health-conscious convenience. Additionally, the FDA's revised definition of the "healthy" nutrient content claim, set for voluntary adoption from April 2025, is reshaping the shelf positioning of convenience products.

Health and Wellness Consciousness Redirects Portfolio Investment

Health and wellness trends are transforming the U.S. packaged food market, going beyond basic labeling to drive significant changes in product formulations across snacks, dairy, bakery, and breakfast cereals. SPINS' 2026 Trends & Predictions Report identifies "fibermaxxing" as a growing consumer behavior, with legume-based and high-fiber products showing clear volume growth across multiple sales channels. Additionally, the rising use of GLP-1 weight-loss medications, currently used by 12% of U.S. consumers with another 21% expressing interest, is creating new demand for packaged foods that are nutrient-rich, high in protein, and portion-controlled. This shift indicates that product formats, rather than traditional categories, will increasingly drive market growth. PepsiCo is responding to these trends with its 2026 initiatives, such as simplifying ingredients in Lay's and Tostitos, launching Doritos Protein, and adding protein and fiber to its Quaker product lines. These actions reflect a broader industry strategy where major consumer packaged goods (CPG) companies are integrating health-focused features into mainstream brands instead of limiting them to premium-tier products. Supporting this trend, FMI's 2026 Report on Food Industry Contributions to Health & Well-Being reveals that 72% of retailers are reformulating private-label products to include more protein and fiber, demonstrating that this is a widespread priority across both branded and private-label goods.

Digital Marketing and Social Media Are Compressing the Innovation Cycle

Social media has significantly shortened the time it takes for trends to transition from emergence to retail shelves in the U.S. packaged food market. For example, Google search data from the 12 months ending in September 2024 shows a 130% increase in searches for "boudin balls" and a 94% rise for "knafeh." This highlights how social platforms can drive consumer interest and purchasing intent even before retailers adapt their assortments. As a result, manufacturers now view localized, limited-edition SKUs as effective marketing tools rather than high-risk investments. According to Deloitte's 2026 forecast, AI-driven referrals already account for 15%–20% of total traffic at some grocery chains, prompting manufacturers to adopt "generative engine optimisation" strategies to ensure their products remain visible to consumers. Kraft Heinz exemplifies this shift with its "Lighthouse" AI control tower, developed in collaboration with Microsoft, which now manages 85% of supply chain decisions in North America. This demonstrates how technology is enhancing both marketing strategies and operational efficiency. Additionally, the 2025 Food & Health Survey by IFIC found that only 11% of consumers currently use apps like Yuka to scan ingredient lists. This indicates that most consumers still rely on traditional packaging and digital content, offering brands a valuable opportunity to connect with their audience before algorithm-driven consumption becomes more dominant.

Private-Label Expansion Is Structurally Reshaping Branded Market Share

In the U.S. grocery landscape, private-label growth has transitioned from a mere recessionary trade-down to a lasting structural shift. By 2025, store brand sales soared to a record USD 282.8 billion, marking a 3.3% increase. This growth rate is nearly threefold that of national brands, which saw a modest 1.2% uptick. Additionally, store brand unit sales reached an unprecedented 68.7 billion units. Notably, 82% of households with incomes exceeding USD 100,000 are ramping up their private-label purchases, outpacing their lower-income counterparts. This trend underscores a shift driven more by quality perception than mere price sensitivity. Ahold Delhaize USA is pushing its "Growing Together" strategy, aiming for 45% of total store sales to come from its own brands. Meanwhile, Kroger has made a significant move, rolling out over 1,100 new private-label products in FY2025, with a pronounced emphasis on health-centric and ready-to-eat items. For branded manufacturers, this shift presents a paradox: the key to a sustainable competitive edge has shifted from scale to agility, particularly in flavor innovation and channel-specific packaging. This is crucial as private labels now swiftly mirror emerging trends, often within just 6–12 months.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shelf-life limitations and fresh-food competition | -0.7% | National; most acute in urban Northeast and West Coast markets | Short term (≤ 2 years) |

| Regulatory scrutiny and labeling changes | -0.5% | National; state-level fragmentation most severe in California, Texas, Louisiana | Medium term (2–4 years) |

| Growing skepticism about ultra-processed and highly engineered products | -0.8% | National; highest intensity among Millennial parents and West Coast consumers | Medium term (2–4 years) |

| Supply-chain and sourcing complexity for clean-halo ingredients | -0.4% | National, with premium channel exposure in Northeast and West | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ultra-Processed Skepticism Is Fragmenting Consumer Demand

In the U.S. packaged food market, consumers are increasingly cautious about processed ingredients. According to IFIC's 2025 Food & Health Survey, 80% of Americans now consider a food's processing status before buying, up from 76% in 2023[2]Source: International Food Information Council, “Consumer Research on Processed Foods”, ific.org . Additionally, awareness of the "ultra-processed" label surged by 12 percentage points in just a year, reaching 40% of adults. Notably, IFIC data highlights that negative online sentiment towards ultra-processed foods (UPFs) has quadrupled since 2022. This surge is largely attributed to Millennial parents, a demographic known for its above-average grocery spending, who are vocally criticizing seed oils, artificial ingredients, and added sugars. The MAHA initiative, highlighted in a May 2025 White House assessment, noted that about 70% of over 300,000 branded grocery items are classified as "ultra-processed." This revelation has spurred a flurry of state-level regulations: Louisiana's SB 14 prohibits 15 specific ingredients in school meals, Texas's SB 25 requires front-label warnings, and California's AB 1264 is set to define UPFs for school food restrictions by 2032. A March 2026 report from Healthy Eating Research noted that 17 food manufacturers, primarily in snack foods and desserts, have pledged to eliminate synthetic dyes. However, these changes might not significantly enhance diet quality, as the focus remains on low-risk additives, sidelining concerns like added sugars and sodium. Navigating this landscape is complex: the FDA's GRAS reform process, coupled with an impending federal definition of UPFs, introduces multi-year uncertainties for portfolio planning.

Shelf-Life Constraints Strengthen Fresh-Food Competition

Fresh and refrigerated foods are increasingly taking over shelf space, particularly at the expense of ambient packaged formats. This shift is especially evident in snacking, dairy-related products, and grab-and-go meals. Trends in consumer health, the broader availability of GLP-1 medications, a heightened focus on nutrient density, and a meticulous approach to ingredient scrutiny are all steering purchasing decisions towards short-dated chilled products. However, packaged food manufacturers grapple with a unique challenge: while consumers link freshness to health, extending the shelf life of chilled products often necessitates preservative systems. These systems, in turn, can clash with the growing demand for clean-label products. A March 2026 survey from Purdue University highlighted a regional disparity in food insecurity: the West stands about 7.5 percentage points better off than the South. This finding underscores a significant dynamic: the South, with its vast base of packaged food consumers, is driven by convenience and price. Yet, this very demographic faces constraints in accessing fresh food, which tempers the risk of substitution in that area. In contrast, affluent metropolitan markets on the Northeast and West Coast are witnessing a direct competition. Here, fresh meal kits and direct-to-consumer chilled products are vying for the Ready Meals segment, a territory traditionally dominated by packaged foods.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Ready Meals and Dairy Drive Divergent Growth Paths

In 2025, Dairy and Dairy Alternatives held a 22.65% share of the US packaged food market, driven by its role as both a staple and a hub for functional innovations. Retailers have heavily invested in high-protein dairy formats, with Kroger's Simple Truth Protein line expanding to over 110 products since its September 2025 launch. Ready meals are expected to lead product type growth with an 8.51% CAGR from 2026 to 2031, fueled by time constraints, at-home eating trends, and demand for portion-controlled, nutrient-rich meals influenced by GLP-1. Snacks are benefiting from private-label premiumisation and social media-driven flavour trends, with bold global flavours and protein-rich formats driving innovation. In 2025, PepsiCo's Sun Chips and Siete brands surpassed USD 1 billion in retail sales, growing over 16%.

Bakery, especially specialty loaves, functional buns, and sourdoughs, is evolving, with natural brands holding 6% of the category and driving 14% growth in specialty lines. Breakfast Cereals are leveraging protein and fibre enrichment trends, aligning with the FDA's updated "healthy" nutrient content claim, effective voluntarily since April 2025. Baby Food faces reformulation challenges following Nestlé's January 2026 infant formula recall and increased scrutiny on ingredient transparency. Global flavour trends are revitalizing Condiments and Sauces, with SPINS data showing international sauces as popular among younger consumers. Kraft Heinz's February 2025 launch of its "Flavor Tour" globally-inspired sauce line targets the dipping sauce category, which posted a 35% three-year CAGR. Meat, poultry, seafood, and substitutes remain dominated by large processors, but plant-based meat alternatives are declining from their 2021-2022 peak due to concerns over taste and ingredient complexity.

By Category: Natural/Organic/Free-From Outpaces Conventional Despite Scale Gap

In 2025, conventional packaged food commanded a significant 76.95% market share, buoyed by the inertia of established brands, accessible price points, and an extensive range of SKUs. Yet, the Natural/Organic/Free-From segment is projected to outpace the overall market with a robust 9.02% CAGR from 2026 to 2031, signaling a demographic and values-driven shift in demand. In 2024, while natural products enjoyed a 3.7% year-over-year dollar growth in multi-outlet channels, conventional products faced a 1.9% decline. This stark contrast highlights the resilience of the clean-label trend, even amidst inflationary pressures.

Interestingly, the surge in the Natural/Organic/Free-From segment is being propelled more by private labels than by established premium brands. Lines like Nature's Promise from Ahold Delhaize USA and Kroger's Simple Truth, both boasting organic and clean-label certifications, are outpacing their branded rivals, making organic and free-from products more accessible. Data from SPINS in 2026 reveal that nearly 40% of younger millennials and Gen Z consumers adhere to specialty diets, steering clear of artificial sweeteners, sugar alcohols, and high-fructose corn syrup. This demographic is pivotal to the category's expansion. Regulatory shifts are also playing a crucial role: the American Bakers Association's commitment in November 2025 to phase out certified FD&C colors from baked goods by December 2028 is set to hasten the shift from conventional to natural products in bakeries, as these reformulated items gain easier certification under natural and free-from labels.

By Distribution Channel: Online Retail Disrupts the Supermarket Gravity Model

In 2025, Supermarkets and Hypermarkets commanded a dominant 60.08% share of sales, bolstered by their diverse product range, investments in private labels, and efficient click-and-collect services. Meanwhile, Online Retail Stores are set to outpace the competition, projected to grow at a robust 8.95% CAGR from 2026 to 2031. A pivotal shift is the rise of AI in grocery shopping: AI chatbots now account for 15%–20% of referrals for certain retailers. This has led to automated ordering for items like low-consideration packaged foods, pantry staples, snacks, and condiments. Brands boasting strong digital product data and favorable review scores stand to gain significantly from this trend.

As consumers increasingly seek value, foot traffic is shifting away from Convenience Stores towards mass retailers, club outlets, and online platforms. In 2025, Kroger's digital sales surpassed USD 16 billion, buoyed by seven straight quarters of double-digit growth in e-commerce. Their success is attributed to a hybrid fulfillment strategy, leveraging both physical stores and third-party delivery services like Instacart, DoorDash, and Uber Eats. This transition diminishes the relevance of traditional trade marketing tactics, such as end-caps and in-aisle promotions. Instead, the spotlight now shines on digital shelf placement and algorithm-driven product visibility, marking a new battleground for packaged food brands.

Geography Analysis

In 2025, the South boasts a commanding 38.03% share of the US packaged food market, driven by its vast population, a penchant for private labels, and a robust culture of dining at home. Notably, food insecurity in the South exceeds that of the West by about 7.5 percentage points. This disparity underscores a consistent demand for value-oriented conventional and private-label packaged goods in the region. Meanwhile, the Northeast is set to outpace all regions with an 8.35% CAGR growth rate through 2031. This surge is fueled by a dense concentration of affluent millennial households, who tend to spend more on functional, organic, and premium packaged goods, alongside a strong urban e-commerce presence. By May 2026, Amazon had ascended to the position of "Number Two Grocer" in Northeast metropolitan areas, underscoring the region's advanced online grocery shopping trend and its challenge to traditional grocery chains.

The Midwest showcases a dual narrative: while self-reported diet quality scores lag about 2 points behind the West, taste preferences soar highest in both the Midwest and West (each at 87 out of 100), overshadowing the South (80) and Northeast (77). This indicates that Midwestern consumers prioritize taste, leading to sustained demand for indulgent snacks and comfort foods. Although the West holds a smaller slice of the packaged food market, it outshines others in Sustainable Food Purchasing, boasting a score that's roughly 6 points above the Northeast on sustainability metrics. This positions the West as a fertile ground for innovations in eco-friendly and plant-based packaging. In the South, state-level compliance is paramount. Legislation like Texas SB 25 and Louisiana SB 14 mandates front-label and ingredient disclosures, compelling manufacturers to juggle dual reformulation strategies for both school and retail markets.

Competitive Landscape

In the US packaged food market, multinational giants like Nestlé, PepsiCo, The Kraft Heinz Company, General Mills, and Conagra Brands dominate, spanning categories from snacks and meals to dairy, cereals, beverages, and frozen foods. Competition hinges on robust brand portfolios, vast distribution networks, innovative products, and economies of scale. These leading firms are channeling investments into premiumization, healthier formulations, and convenience-driven products, aligning with shifting consumer preferences.

To cater to health-conscious consumers, market players are prioritizing clean-label ingredients, high-protein offerings, functional nutrition, and plant-based products. Key strategies include product innovation, mergers and acquisitions, and diversifying portfolios. Furthermore, companies are amplifying investments in digital commerce, direct-to-consumer avenues, and data-centric marketing to bolster consumer ties and enhance market reach. Meanwhile, private-label brands from major retailers are ramping up competition by offering cost-effective alternatives without compromising on quality or variety.

The competitive arena is further enriched by the rise of emerging brands and niche manufacturers, honing in on specific segments like organic, natural, ethnic, gluten-free, and premium foods. While industry behemoths leverage scale and brand clout, smaller entities carve their niche through innovation, transparency, sustainability, and unique product positioning. As the market leans more towards convenience, wellness, and value, both established and budding brands are reshaping their product lines and supply chain tactics to stay relevant in the US packaged food landscape.

U.S. Packaged Food Industry Leaders

Nestlé SA

PepsiCo, Inc.

The Coca-Cola Company

General Mills Inc.

Mondelez International

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: The Campbell's Company acquired a 49% interest in La Regina, the Italian maker of Rao's Homemade pasta sauces, for USD 286 million in a deal structured with an initial payment of USD 146 million and a deferred USD 140 million payment due one year later; Rao's Homemade has exceeded USD 1 billion in trailing 12-month net sales, making it Campbell's fourth billion-dollar brand.

- May 2026: Cal-Maine Foods, the largest US egg company, acquired the Van's Foods brand assets from Sara Lee Frozen Bakery for an undisclosed amount, targeting a 10% increase in prepared food annual sales; Van's Foods is the market leader in gluten-free frozen waffles in the better-for-you breakfast segment

- May 2026: Bel Group acquired Ingenuity Foods' Brainiac® and Little Brainiac® brands to expand its better-for-you snacking portfolio in North America, reinforcing its GoGo squeeZ® platform and citing ongoing US production expansion following a recent plant expansion in South Dakota.

U.S. Packaged Food Market Report Scope

| Dairy and Dairy Alternatives |

| Confectionery |

| Bakery |

| Snacks |

| Meat, Poultry and Seafood and Substitutes |

| Breakfast Cereals |

| Baby Food |

| Food Spread |

| Ready Meals |

| Condiments and Sauces |

| Other Product Types |

| Conventional |

| Natural/Organic/Free-From |

| Supermarkets / Hypermarkets |

| Convenience Stores |

| Online Retail Stores |

| Other Distribution Channels |

| South |

| Midwest |

| West |

| Northeast |

| By Product Type | Dairy and Dairy Alternatives |

| Confectionery | |

| Bakery | |

| Snacks | |

| Meat, Poultry and Seafood and Substitutes | |

| Breakfast Cereals | |

| Baby Food | |

| Food Spread | |

| Ready Meals | |

| Condiments and Sauces | |

| Other Product Types | |

| By Category | Conventional |

| Natural/Organic/Free-From | |

| By Distribution Channel | Supermarkets / Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Other Distribution Channels | |

| By Region | South |

| Midwest | |

| West | |

| Northeast |

Key Questions Answered in the Report

How large is the United States packaged food space in 2026?

It stands at USD 1.75 trillion in 2026 and is projected to reach USD 2.60 trillion by 2031 at an 8.3% CAGR.

Which product area leads sales in the United States packaged food market?

Dairy and Dairy Alternatives leads with a 22.7% share in 2025, supported by staple demand and growth in high-protein and lactose-free formats.

Which product area is growing fastest through 2031?

Ready Meals is forecast to expand at 8.5% through 2031 because consumers continue to prefer convenient and portion-managed meal options.

Which sales channel is changing competitive behavior the most?

Online Retail Stores is growing fastest at 8.95% CAGR, and ecommerce already contributes nearly three-quarters of total U.S. grocery dollar growth.

Page last updated on: