United States Grass Fed Beef Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

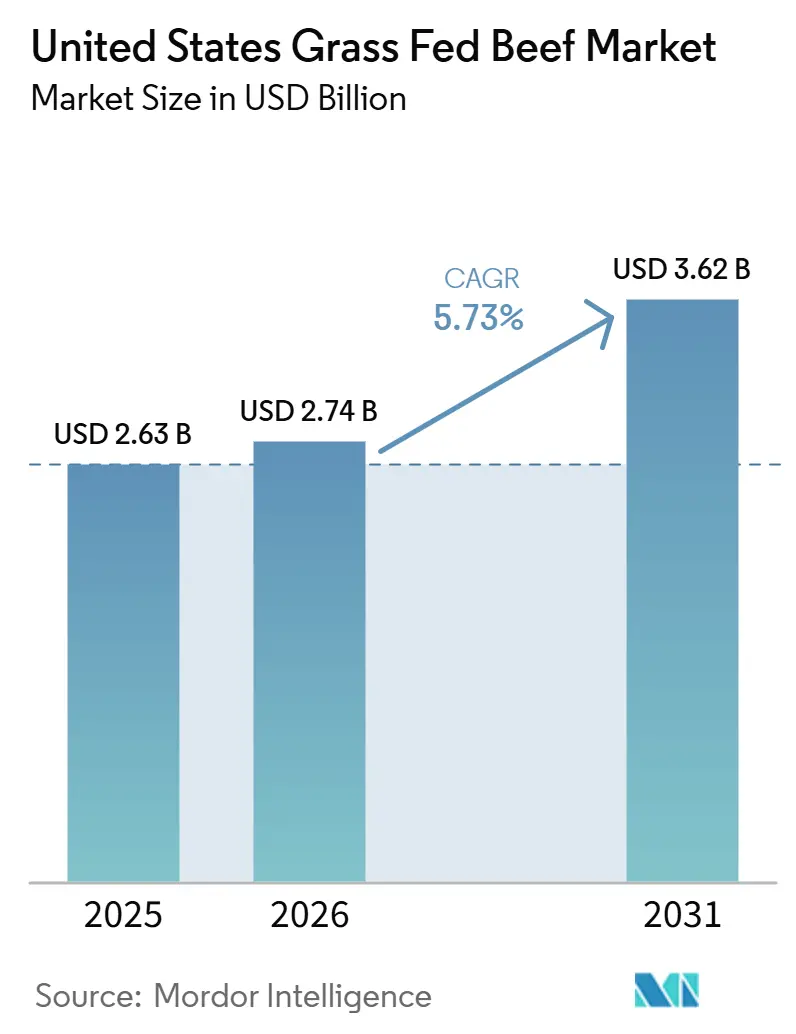

| Base Year Market Size (2025) | USD 2.63 Billion |

| Market Size (2026) | USD 2.74 Billion |

| Market Size (2031) | USD 3.62 Billion |

| Growth Rate (2026 - 2031) | 5.73% CAGR |

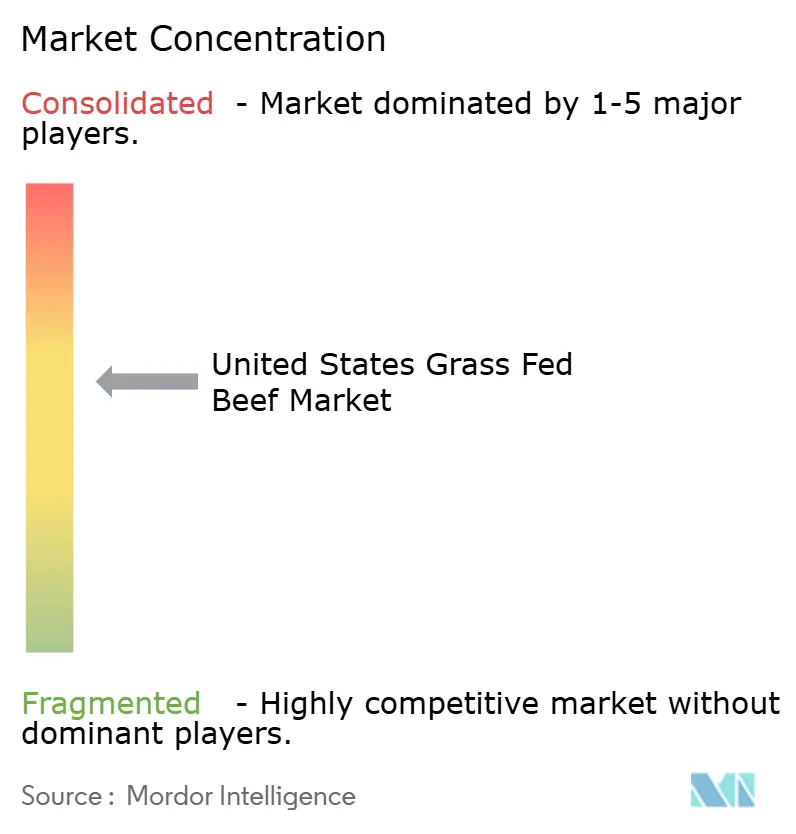

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Grass Fed Beef Market Analysis by Mordor Intelligence

The United States grass-fed beef market size is expected to be valued at USD 2.63 billion in 2025. It is projected to grow from USD 2.74 billion in 2026 to USD 3.62 billion by 2031, registering a CAGR of 5.7% during the forecast period (2026-2031). The United States grass-fed beef market is expanding faster than the broader conventional beef category, as more buyers treat protein quality, label clarity, and animal-raising standards as core purchase criteria rather than optional premium attributes. A June 2026 national survey from Pre Brands showed that 65% of Americans consume beef in a typical week, while 37% actively cite grass-fed as a buying criterion, indicating that the category has moved well beyond a narrow natural foods niche[1]Source: Pre Brands, “June 2026 Consumer Survey,” pre-brands.com. The market is also benefiting from stronger retail execution and improved brand verification, particularly as the USDA formalized documentation expectations for animal-raising claims and made traceability a more meaningful operating requirement for brands seeking scale. Scientific support for nutrient density and soil health positioning is reinforcing premium demand, while regenerative messaging is creating an additional quality layer beyond the base grass-fed claim in parts of the United States grass-fed beef market. However, the lowest United States cattle herd in 75 years, regional finishing concentration, and continued pressure on input costs are keeping supply tight. These factors support pricing but also expose the United States grass-fed beef market to availability, weather-related, and processing constraints.

Key Report Takeaways

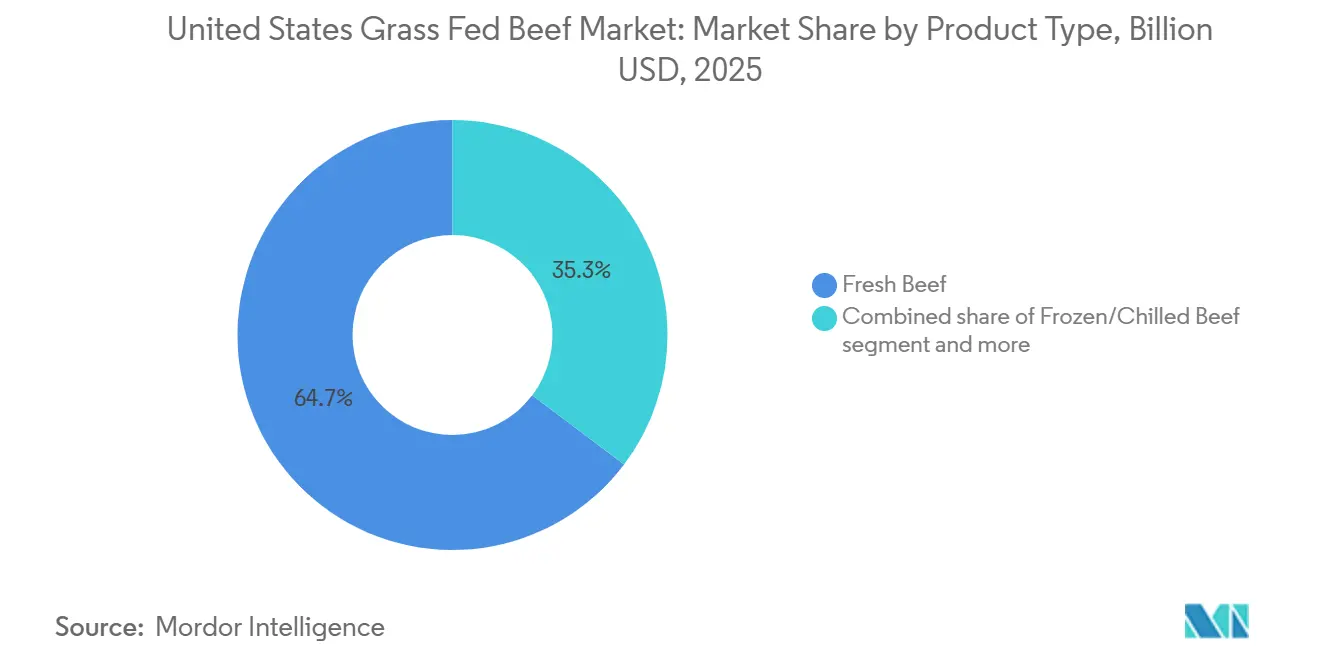

- By product type, Fresh Beef held 64.71% of the United States grass fed beef market share in 2025, while Frozen/Chilled Beef is forecast to record the highest CAGR at 6.96% through 2031.

- By cut type, Steaks accounted for 62.62% of the United States grass fed beef market size in 2025, while Minced Beef is projected to expand at a 7.01% CAGR through 2031.

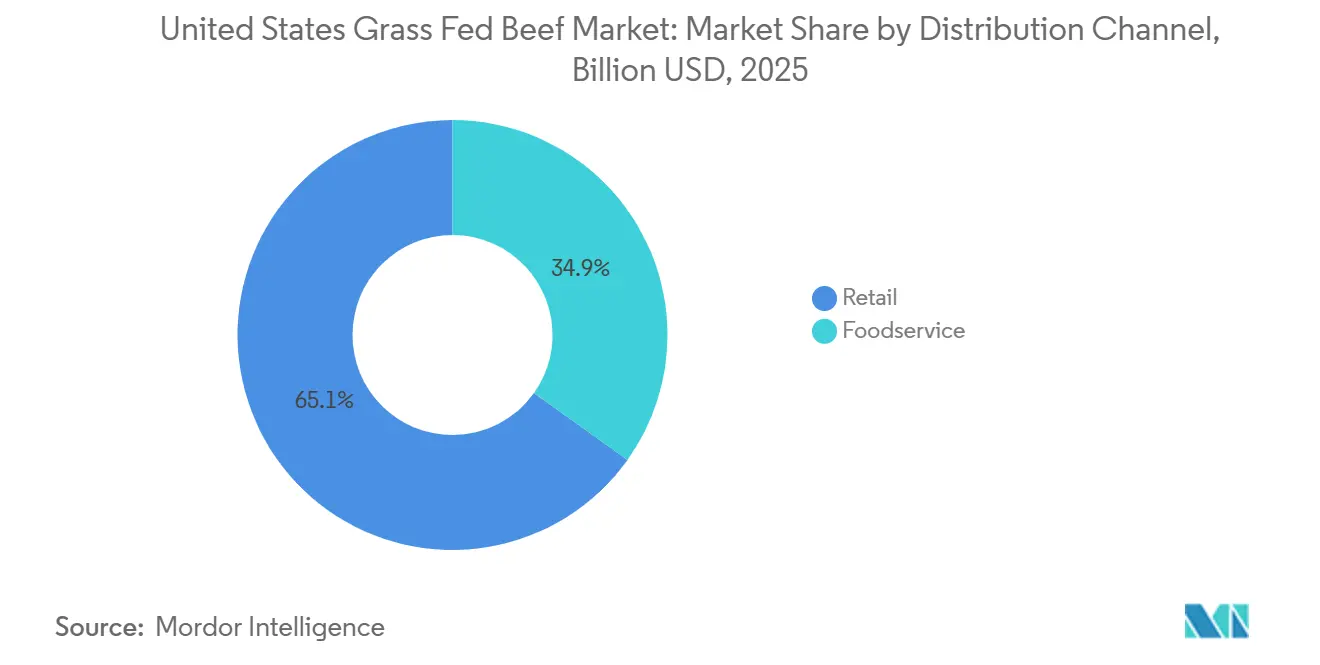

- By distribution channel, Retail captured 65.13% of the United States grass fed beef market size in 2025, while Foodservice is set to grow at the fastest CAGR of 7.51% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Grass Fed Beef Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising premium protein demand among health-focused buyers | +1.3% | National, concentrated in the United States coastal metros and high-income urban clusters | Short term (≤ 2 years) |

| Expansion of traceability and provenance claims | +0.9% | National, with early gains in the Northeast and Pacific Coast markets | Medium term (2-4 years) |

| Retailer and foodservice menu premiumization | +1.0% | National, accelerating in the Southeast, Plains, and Great Lakes | Short term (≤ 2 years) |

| Regenerative grazing and soil health positioning | +0.7% | Midwest, Northern Plains, and Pacific Northwest supply corridors | Medium term (2-4 years) |

| Direct-to-consumer subscription and box models | +0.6% | National, densest in high-income suburban and rural ZIP codes | Medium term (2-4 years) |

| Carcass utilization improvements through niche cut monetization | +0.4% | National, strongest among independent and mid-scale producers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising premium protein demand among health-focused buyers

The protein cycle shaping the United States dietary behavior is shifting toward quality differentiation rather than quantity. The June 2026 Pre Brands national survey is expected to indicate that 31% of Americans identify beef as their most functional protein for health and fitness goals, a positioning historically associated with chicken and fish. Grass-fed beef offers a measurable nutritional advantage: Mayo Clinic documentation confirms that it has lower total fat content, higher omega-3 fatty acid concentrations, and elevated antioxidant levels than conventional beef. A peer-reviewed metabolomics study scheduled for publication in npj Science of Food in 2025 is expected to show that rotational grazing in Southern US pasture-based systems directly improves nutrient density outcomes in finished beef, linking farming practices to a verifiable consumer benefit[2]Source: npj Science of Food, “Rotational Grazing and Nutrient Density,” nature.com. Millennials are expected to surpass Boomers in meat category spending within two years and index significantly higher for claims-based protein purchases, according to the Power of Meat Report 2026. The demand signal is structural, not cyclical. Willingness to pay for premium protein has decoupled from headline beef price inflation, a dynamic that supports grass-fed premiums even as broader food costs moderate.

Expansion of traceability and provenance claims

Traceability is shifting from a regulatory requirement to a brand value driver in the United States grass-fed beef market. In August 2024, USDA FSIS published its updated guideline (FSIS-GD-2024-0006), which formalizes documentation requirements for animal-raising claims, including grass-fed and pasture-raised labels. This update raises the evidentiary burden for brands and creates a meaningful barrier to entry for unverified claimants. A 2025 study published in Agricultural and Food Economics (Springer Nature) identifies blockchain as a promising mechanism for end-to-end provenance documentation, noting that QR-accessible smart labels containing rotational grazing data, antibiotic records, and carbon footprint information can measurably improve consumer trust in premium claims. Verde Farms' May 2026 nutrient density study, benchmarked against competing grass-fed products, represents a new frontier in provenance evidence, where third-party substantiation of nutritional outcomes replaces origin-only storytelling. The USDA AMS Grass Fed Small and Very Small Producer Program provides a certified pathway for smaller operators, but uneven audit coverage creates label dilution risk and systematically benefits brands with robust verification infrastructure[3]Source: U.S. Department of Agriculture Agricultural Marketing Service, “Grass Fed Small and Very Small Producer Program,” ams.usda.gov.

Retailer and foodservice menu premiumization

Retail chains and foodservice operators are structurally repositioning grass-fed beef as a mainstream premium tier rather than a specialty niche. The Power of Meat Report 2026 is expected to document double-digit growth in organic and grass-fed meat across dollars, units, and pounds in 2025. In foodservice, Pura Vida Miami is expected to launch a 100% grass-fed and grass-finished sirloin steak across all national locations in June 2026, targeting the growing protein and wellness dining segment. Additionally, most shoppers identify grass-fed as a key purchase driver for meat. This attribute, along with USDA Prime and hormone-free labeling, has moved beyond a specialty signal to become a mainstream purchase criterion. Verde Farms’ planned expansion to more than 680 Albertsons stores across 21 states by June 2026 illustrates the geographic mainstreaming of grass-fed beef from coastal strongholds into interior markets. The foodservice channel’s projected 7.51% CAGR through 2031 reflects this institutional adoption curve, as corporate dining, college foodservice, and casual dining operators respond to millennial and Gen Z preferences for verified protein sourcing.

Regenerative grazing and soil health positioning

Regenerative grazing is emerging as the next-generation value narrative for pasture-raised beef, expanding the proposition beyond individual health to include land stewardship and climate resilience. In early 2025, Applegate Farms, a subsidiary of Hormel Foods, announced that it had transitioned 100% of the beef used in its hot dogs to certified regenerative grasslands. The transition covered 10.8 million acres, nearly double its original target of 6 million acres, and the company achieved it nine months ahead of schedule. The 2025 npj Science of Food study confirmed that adaptive multi-paddock grazing in Southern US systems simultaneously improved soil organic matter, microbial activity, and beef nutrient density, providing scientific support for regenerative marketing claims. Farm Credit Mid-America's 2026 survey noted that nearly half of US livestock operations planned to increase breeding females in 2026, with forage conditions serving as the primary expansion lever. This trend indicates that pasture-based herd rebuilding is underway and will gradually support grass-fed supply growth. Regenerative certification is becoming a premium layer above the base grass-fed designation, creating a distinction that unlocks an additional pricing tier and ESG procurement preference from large foodservice and retail buyers. The market is effectively bifurcating into standard grass-fed and regenerative grass-fed segments, with the latter commanding premiums that justify higher documentation and audit costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium price gap versus grain-fed beef | -1.4% | National, most acute in price-sensitive interior and rural retail markets | Short term (≤ 2 years) |

| Cold chain and last-mile fulfillment complexity | -0.7% | National, particularly in lower-density suburban and rural areas | Medium term (2-4 years) |

| Certification and label interpretation friction | -0.5% | National; most acute at retail shelf in markets with low grass-fed familiarity | Medium term (2-4 years) |

| Supply concentration in pasture-suitable regions | -0.8% | Midwest and Great Plains finishing corridors; secondary in the Pacific Northwest | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premium price gap versus grain-fed beef

The price differential between grass-fed and conventional grain-fed beef remains the largest barrier to category scale. USDA AMS Quarterly Grass Fed Beef data for Q2 2026 indicates that grass-fed ground beef with 90%+ lean content averaged USD 13.63 per pound in direct-to-consumer sales, substantially higher than conventional equivalents. This gap widens further for premium steak cuts. The ongoing cattle supply contraction further amplifies price sensitivity. According to the USDA Cattle Inventory Report, the US cattle herd reached 86.2 million head on January 1, 2026, the lowest level in 75 years, tightening input costs across all beef supply chains, including grass-fed programs. The Angus Journal, released in April 2026, reported that approximately 57% of the US beef cow herd is concentrated in just 10 states, led by Texas, Oklahoma, and Missouri. As a result, grass-fed producers compete with grain-fed operations for the same regional supply pools without the benefit of comparable processing scale. Grain-fed beef benefits from established distribution infrastructure and volume pricing, allowing it to absorb market price increases more efficiently than grass-fed supply chains, which lack equivalent throughput. The price gap is likely to persist through the current cattle cycle recovery, which USDA ERS outlook data projects to extend into 2028–2029.

Cold chain and last-mile fulfilment complexity

Premium perishable logistics represent a structural cost embedded in every DTC and e-commerce grass-fed beef order. Dry ice sourcing, insulated packaging, carrier delivery windows, and temperature monitoring add meaningful variable costs per shipment. These costs place a disproportionate burden on small-to-mid-scale grass-fed producers that lack centralized fulfillment infrastructure. Crowd Cow, a premium online meat platform, is expected to improve on-time delivery from 70% to more than 99% after transitioning to a specialized last-mile logistics provider in 2025, highlighting the performance volatility of standard carrier networks for frozen perishables. Omaha Steaks invested in rebuilding its fulfillment network around 44 store-as-node micro-fulfillment hubs, supported by a gig delivery partnership, reducing average delivery time from 6.2 days to 1.24 days. This level of infrastructure remains beyond the reach of most pasture-raised beef producers. The complexity discourages smaller ranchers from scaling DTC models and concentrates online sales among better-capitalized operators, limiting the geographic reach of producers in logistics-constrained interior markets. Last-mile investment is expected to remain a sustained operational cost rather than a one-time build, dampening margin expansion for the DTC channel throughout the forecast period.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Fresh Beef Anchors Volume While Frozen Formats Accelerate

Frozen/chilled beef is forecast to register the fastest CAGR among all product types, at 6.96% from 2026 to 2031. This growth reflects a structural shift toward e-commerce fulfillment, DTC subscription boxes, and foodservice bulk procurement, all of which favor the storage stability of frozen and chilled formats over the date constraints of fresh beef. Fresh beef is expected to account for 64.71% of the market in 2025, supported by its established retail positioning, a high share of premium steak cuts sold through supermarket meat cases, and consumer preference for visual quality inspection at the point of purchase. Despite its size advantage, the fresh format faces pressure from format diversification as online and subscription channels reshape purchasing behavior toward frozen shipments. A peer-reviewed study in npj Science of Food (2025) is expected to note that rotational grazing on Southern US pastures improves nutrient density in beef, a finding that, when communicated at the shelf, would disproportionately benefit branded fresh-format operators with traceable supply chains.

Processed beef and canned beef represent smaller but strategically notable segments. Processed formats are gaining traction through grass-fed beef jerky, hot dogs, and bacon, positioned as clean-label convenience proteins that bridge the gap between premium and mass-market offerings. Applegate’s planned June 2026 launch of APPLEGATE NATURALS Natural Uncured Beef Bacon, made from 100% grass-fed, pasture-raised beef and set for immediate distribution to more than 3,000 Walmart stores, indicates that processed grass-fed beef is targeting mass-market scale rather than specialty channel positioning. Canned beef remains niche within the premium grass-fed category but benefits from pantry-stocking and emergency preparedness behavior among rural DTC consumers. Over the longer term, Fresh Beef’s dominant share is expected to gradually decline as cold-chain infrastructure matures, subscription economics improve, and processed grass-fed products reach mass-retail scale.

By Cut Type: Steak Dominance Masks Minced Beef's Strategic Ascent

Steaks are expected to account for 62.62% of the United States grass-fed beef market by cut type in 2025, supported by premium pricing power in foodservice and high-end retail. Ribeye, sirloin, and New York strip cuts command the highest per-pound premiums in grass-fed retail, while their placement on upscale restaurant menus supports both volume and margin growth. “Back to Grass,” a market analysis from the University of Vermont, identified concentrated demand for expensive middle cuts and ground beef as a structural whole-carcass challenge; the cuts consumers prefer most do not balance full-carcass utilization.

Minced beef is the fastest-growing cut type and is projected to register a 7.01% CAGR from 2026 to 2031. Its growth reflects its role as an accessible entry point for first-time grass-fed beef buyers, its strong share in DTC subscription box volumes, and its importance in whole-carcass utilization programs. Creekstone Farms is expected to upgrade its ground beef processing in April 2026 by introducing bowl-chopper technology, which delivers a more gourmet texture and supports a broader retail-ready range, including smash burgers, pucks, and vacuum skin-pack formats. This development is expected to expand the reach of grass-fed ground beef into premium convenience formats. Roasts play a complementary DTC role in seasonal demand cycles and whole-animal purchase models, while other cut types, including organ meats and specialty offal, represent an emerging niche. Nose-to-tail programs that actively market organ meats and specialty cuts report effective revenue increases of 25–40% per animal, according to direct-farm economics analysis. This indicates that improving carcass utilization is both an economic necessity and a meaningful revenue lever for grass-fed producers.

By Distribution Channel: Retail Commands Share as Foodservice Outpaces Growth

Foodservice is expected to be the fastest-growing distribution channel, projected to register a CAGR of 7.51% from 2026 to 2031. Wellness cafés, fine dining chains, and institutional operators are driving growth by integrating grass-fed sourcing into standard procurement. The USDA FSIS regulatory framework for substantiating animal-raising claims (FSIS-GD-2024-0006, August 2024) is increasingly expected to serve as a supplier qualification criterion in institutional foodservice contracts, creating a compliance floor that favors branded operators with documented supply chains over commodity distributors. Retail is expected to hold a 65.13% share in 2025, supported by Supermarkets/Hypermarkets, where major national chains have expanded natural and premium meat shelf space. Mainstream grocery chains are supplementing Specialty Stores, historically the primary grassroots channel for grass-fed brands, as brands scale into Publix, Albertsons, and Harris Teeter and expand the addressable buyer base beyond specialty-channel shoppers.

Online Retail Stores represent the fastest-growing retail sub-channel, as subscription box models from producers such as Parker Pastures, Wholly Cow Market, and Home Place Pastures reduce last-mile pricing disadvantages through predictable per-delivery economics. Verde Farms' planned expansion to more than 680 Albertsons stores across 21 states by June 2026, along with its chainwide presence at Publix (1,400+ locations) and Harris Teeter (269 stores), reflects the market’s shift toward mainstream distribution. Teton Waters Ranch is expected to debut its organic regenerative ground beef line in July 2026, targeting retail and foodservice buyers through a dual-channel launch. This strategy shows how premium grass-fed brands view foodservice as a parallel growth corridor rather than a secondary channel. Other Distribution Channels, including direct farm sales and farmers markets, remain important for producer cash flow and brand building but represent a structurally limited share at scale.

Geography Analysis

The Northeast showed the strongest commercial maturity in the United States grass fed beef market. Grass fed beef retail dollar sales in the region reached USD 108 million during the 13-week period ending September 2024, the highest among all United States regions, according to Meat and Livestock Australia (M&LA). Boston recorded the highest Category Development Index among major United States markets during the same period, at 164.2, indicating unusually strong category intensity compared with the national baseline. A 2026 study in Agricultural Systems found that New York State and New England used only 43% of available pastureland for grazing, highlighting a significant supply opportunity near an already premium demand base. Cornell reporting in April 2026 also stated that Northeast grass-fed beef production is economically viable under scaled or cooperative farm models when shared infrastructure addresses slaughter and processing barriers. For the United States grass fed beef market, the Northeast combines dense urban demand, premium purchasing behavior, and underused pasture capacity, creating a strong mix of current commercial depth and future supply upside.

The South and the Midwest are showing some of the most dynamic expansion patterns in the United States grass fed beef market, particularly in areas developing both consumer demand and supply-side depth. Plains markets recorded 63% year-over-year dollar growth and 65% volume growth during the 13-week period ending September 2024, while Great Lakes markets increased 56% in dollar sales and 66% in volume. Both regions outperformed the national average of 41%, according to Meat and Livestock Australia (M&LA). The Southeast also posted 49% year-over-year dollar growth, supported by broader branded grocery distribution, including Verde Farms’ presence across more than 1,400 Publix stores and all 269 Harris Teeter stores, as noted in the source draft. Chicago recorded 47% dollar growth and 72% volume growth, showing that the Midwest is no longer only a cattle and finishing corridor but is also emerging as a stronger consumption market, according to Meat and Livestock Australia (M&LA). Angus Journal reported in April 2026 that the top 10 beef cow states accounted for 57% of the United States beef cow herd, led by Texas, Oklahoma, Missouri, Nebraska, and South Dakota. This concentration gives the South and Midwest a clear supply adjacency advantage for regional grass-fed programs.

The West presents a more mixed pattern in the United States grass fed beef market, with California showing slower momentum than many newer growth areas. California grassfed retail dollar sales increased 21% during the same 13-week period, below the national average of 41%. San Francisco and Oakland posted negative year-over-year performance of -1%, suggesting a more mature specialty segment. The broader Western region outside California still recorded 31% growth, indicating stronger momentum in markets such as Denver, Phoenix, and Portland, where premium demand is expanding from a lower base. The USDA AMS Grass Fed Small and Very Small Producer Program remains relevant in Western states, as many independent ranches rely on certified pathways to maintain label integrity and meet retail buyer requirements.

Competitive Landscape

The United States grass-fed beef market comprises two broad competitive groups: large conventional protein companies that have expanded into premium claims-based lines and specialist brands built from the outset around dedicated grass-fed supply chains. This structure matters because scale alone does not guarantee an advantage when herd supply remains tight and buyers place significant weight on certification, traceability, and production methods. Verde Farms remains one of the most visible premium players in the United States grass-fed beef market, supported by its broad grocery footprint across Albertsons, Publix, and Harris Teeter and its strong position in organic beef branding. Thousand Hills Lifetime Grazed has pursued a more integrated strategy by acquiring Organic Prairie and Mighty Organic, strengthening its processing, distribution, and retail relationships in regenerative and organic grass-fed beef. This combination of branded shelf presence and supply chain control is shaping a market in which operators with secure cattle access and documented claims can compete more effectively than firms that rely primarily on conventional processing scale.

Strategic moves in the United States grass-fed beef market are clustering around deeper retail channel penetration, processed product expansion, and premium proof points linked to regenerative or nutrient-based differentiation. Applegate is set to expand the category’s reach in June 2026 by launching grass-fed beef bacon in more than 3,000 Walmart stores, demonstrating how value-added products can bring pasture-raised claims into much larger shopping baskets. Verde Farms has taken another route by expanding chain distribution across more states, strengthening everyday store-level visibility and reducing reliance on smaller natural retail formats. JBS is also expected to signal the rising value of documented claims through its 2025 Sustainability Report, scheduled for publication in July 2026, which is expected to detail a Farm Assurance certification program covering grass-fed, free-range, and GMO-free standards. These examples show that competition in the United States grass-fed beef market no longer depends only on product availability, as brands now need proof systems, broader shelf access, and a clear reason for consumers or procurement teams to pay a premium.

Technology and route-to-market design are becoming stronger differentiators in the United States grass-fed beef market, especially as brands seek to reduce dependence on limited retail shelf space. The 2025 Agricultural and Food Economics study is expected to highlight blockchain and QR-enabled smart labels as useful tools for provenance communication, indicating that digital proof can play a direct role in consumer trust and premium conversion. Direct subscription models are also giving some regional players a way to retain more per-pound margin and maintain closer consumer relationships, although cold chain costs remain a limiting factor. The United States grass-fed beef market remains fragmented, but the strongest operators increasingly combine verified sourcing, reliable supply, and scalable channel execution across retail, foodservice, and direct sales.

United States Grass Fed Beef Industry Leaders

JBS S.A.

Tyson Foods, Inc.

Cargill, Incorporated

Perdue Farms Inc.

Verde Farms, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Thousand Hills Lifetime Grazed expanded its regenerative beef model by enhancing grazing management and processing capacity, positioning the company as a vertically integrated operator capable of scaling certified regenerative and organic grass-fed beef across retail and foodservice channels.

- July 2026: Teton Waters Ranch debuted its organic regenerative ground beef product line, entered the premium ground beef segment with USDA-certified organic and regenerative credentials targeting both retail and foodservice buyers.

- June 2026: Verde Farms expanded its partnership with Albertsons by adding the Mountain West and Southern divisions, increasing its total Albertsons footprint to more than 680 stores across 21 states. The new placements included ribeye steaks and multiple ground beef SKUs across previously uncovered regions.

United States Grass Fed Beef Market Report Scope

Grass-fed beef comes from cattle that eat only grass and forage their entire lives, unlike conventional cattle finished on grain. The United States grass fed beef market report is segmented by product type, cut type, and distribution channel. By product type, the market is segmented into fresh beef, processed beef, frozen/chilled beef, and canned beef. By cut type, the market is segmented into steaks, roasts, minced beef, and other cut types. By distribution channel, the market is segmented into foodservice and retail. The retail segment is further sub-segmented into supermarkets/hypermarkets, specialty stores, online retail stores, and other distribution channels. The Market Forecasts are Provided in Terms of Value (USD).

| Fresh Beef |

| Processed Beef |

| Frozen/Chilled Beef |

| Canned Beef |

| Steaks |

| Roasts |

| Minced Beef |

| Other Cut Types |

| Foodservice | |

| Retail | Supermarkets/Hypermarkets |

| Specialty Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

| Product Type | Fresh Beef | |

| Processed Beef | ||

| Frozen/Chilled Beef | ||

| Canned Beef | ||

| Cut Type | Steaks | |

| Roasts | ||

| Minced Beef | ||

| Other Cut Types | ||

| Distribution Channel | Foodservice | |

| Retail | Supermarkets/Hypermarkets | |

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

Key Questions Answered in the Report

What is driving growth in United States grass-fed beef demand through 2031?

Growth is being supported by a stronger interest in protein quality, label transparency, and verified sourcing. The category is projected to rise from USD 2.74 billion in 2026 to USD 3.62 billion by 2031 at a 5.73% CAGR.

Which product format leads sales and which one is growing fastest?

Fresh Beef led with 64.71% share in 2025 because retail shoppers still prefer visible fresh presentation. Frozen/Chilled Beef is growing fastest at a 6.96% CAGR as e-commerce, subscriptions, and bulk foodservice orders expand.

Why do steaks still dominate revenue in this category?

Steaks held 62.62% in 2025 because premium dining and retail buyers are most willing to pay more for visible quality and provenance in high-value cuts. That said, Minced Beef is growing faster at a 7.01% CAGR because it offers a more accessible entry price.

How important is foodservice compared with retail?

Retail remained the largest route with 65.13% share in 2025, but Foodservice is projected to expand faster at a 7.51% CAGR. That reflects broader menu integration by wellness-focused restaurants and institutional buyers.

Page last updated on: